HBM For Defense and Space Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 70.27 Million |

| Market Size (2031) | USD 320.59 Million |

| Growth Rate (2026 - 2031) | 35.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

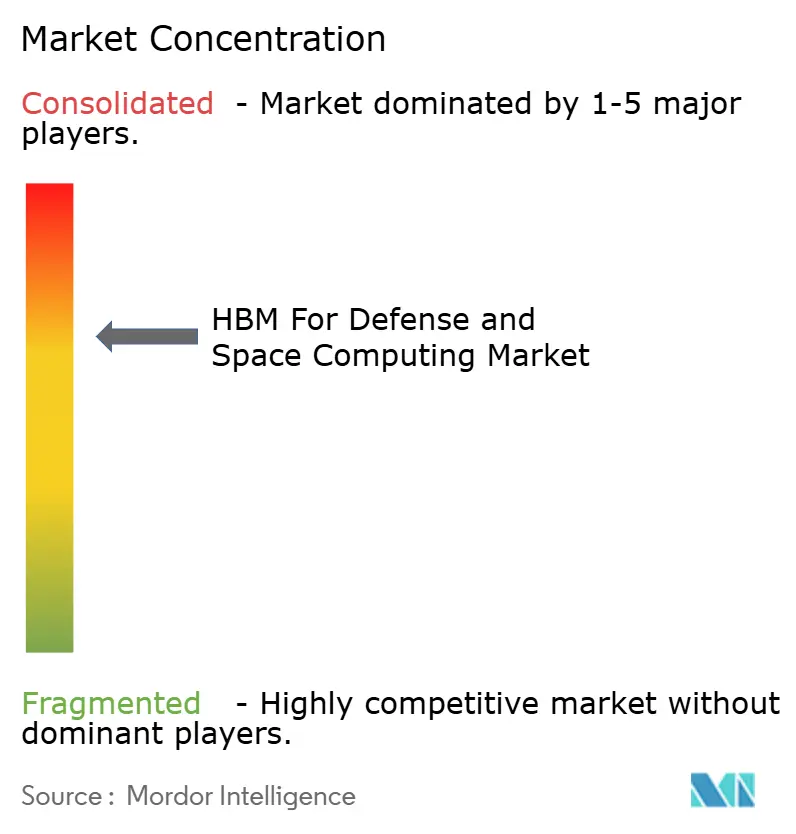

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM For Defense and Space Computing Market Analysis by Mordor Intelligence

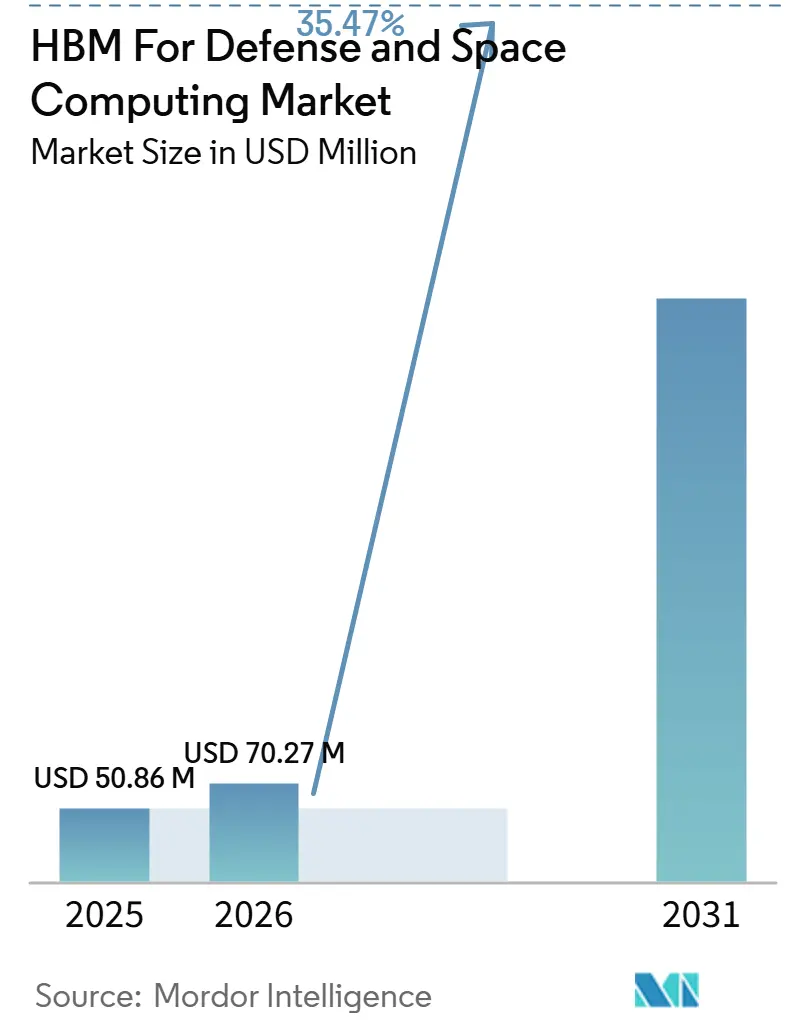

The HBM for defense and space computing market was valued at USD 50.86 million in 2025 and is projected to reach USD 320.59 million by 2031, advancing at a CAGR of 35.47% during 2026-2031. The pace of expansion reflects how quickly defense and space programs are moving toward memory-intensive AI, sensor fusion, and onboard processing requirements that older memory architectures cannot support at the same power and size limits. Public funding is also tightening the link between semiconductor policy and defense electronics adoption, especially where trusted manufacturing and advanced packaging now shape procurement timing. The HBM for defense and space computing market is also benefiting from the fact that each commercial HBM generation creates a later qualification window for military and space platforms, which keeps the design pipeline active across multiple program cycles. Competitive pressure remains uneven because memory supply is concentrated among a small number of DRAM vendors, while integration work is spread across a wide set of defense primes and embedded computing specialists. That mix keeps the HBM for defense and space computing market highly opportunity-rich for suppliers that can align packaging access, qualification readiness, and open-architecture compliance.

Key Report Takeaways

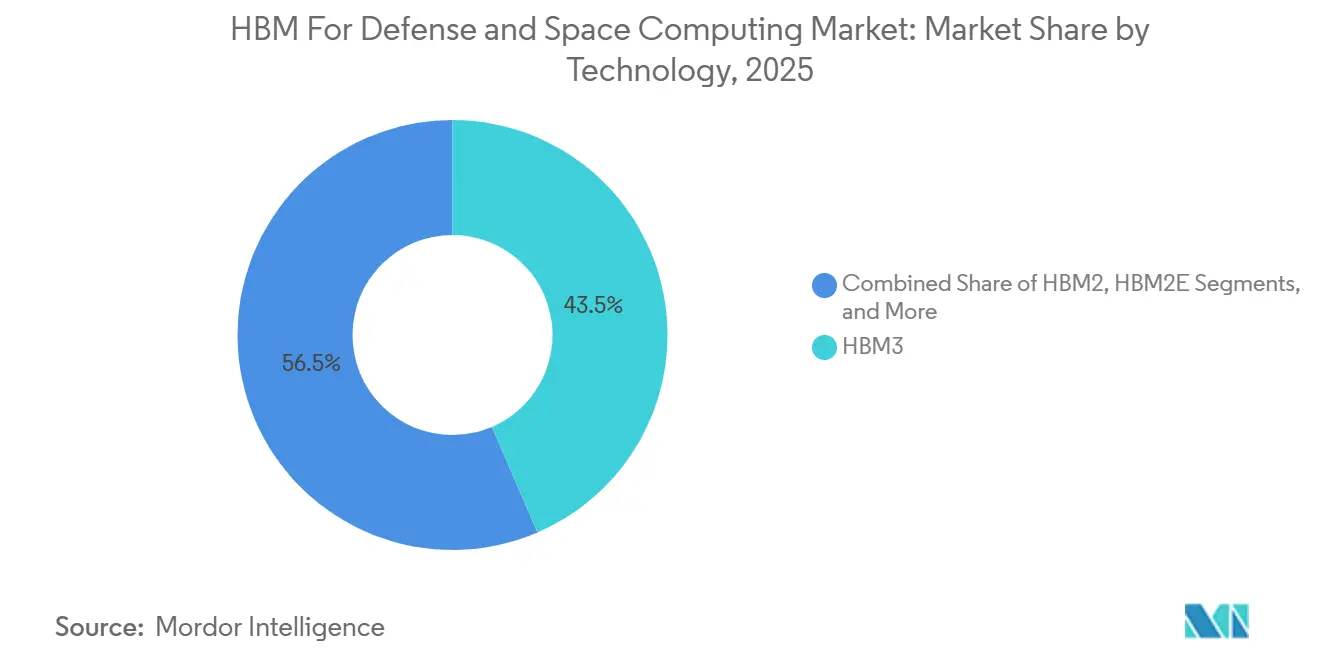

- By technology, HBM3 led with 43.54% revenue share of the HBM for defense and space computing market in 2025, while HBM4 is projected to expand at a 36.67% CAGR through 2031.

- By memory capacity per stack, the 8 GB to 16 GB band held 47.81% share in 2025, while the 16 GB to 32 GB band is projected to grow at a 36.44% CAGR through 2031.

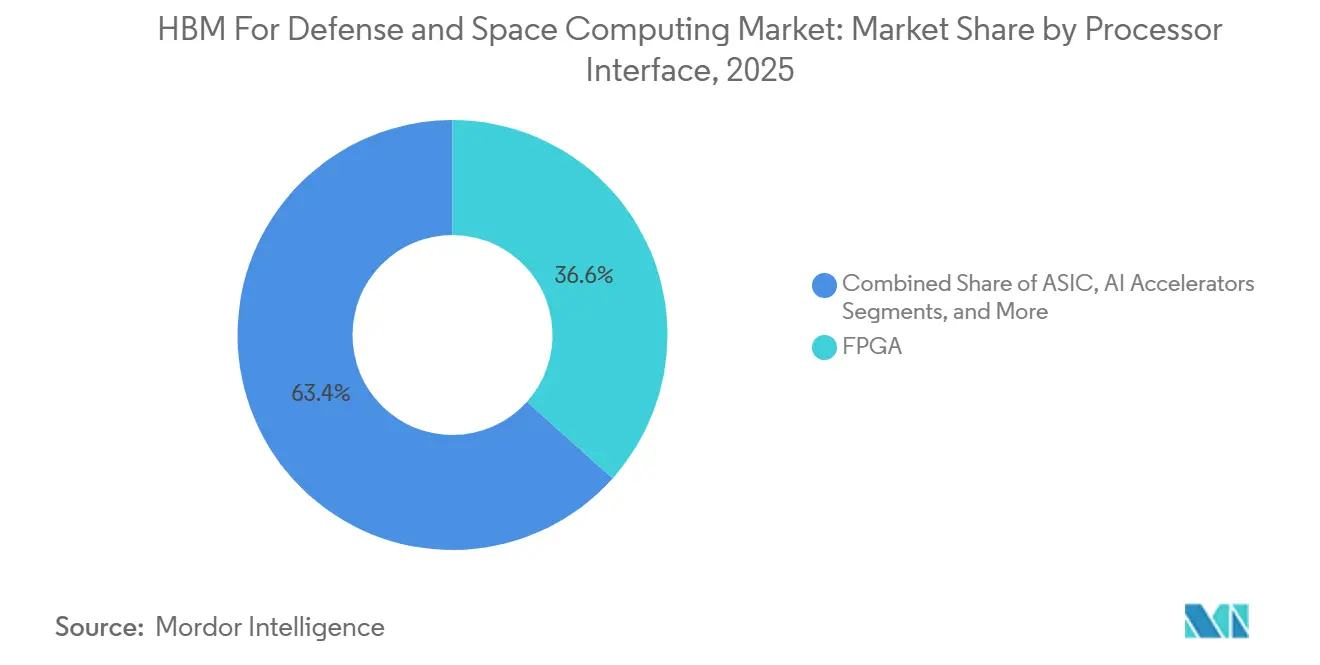

- By processor interface, FPGA accounted for 36.62% share in 2025, while AI accelerators are projected to advance at a 36.32% CAGR through 2031.

- By application, radar, EO and SIGINT processing captured 31.48% share of the HBM for defense and space computing market in 2025, while AI and autonomous systems are projected to expand at a 36.58% CAGR through 2031.

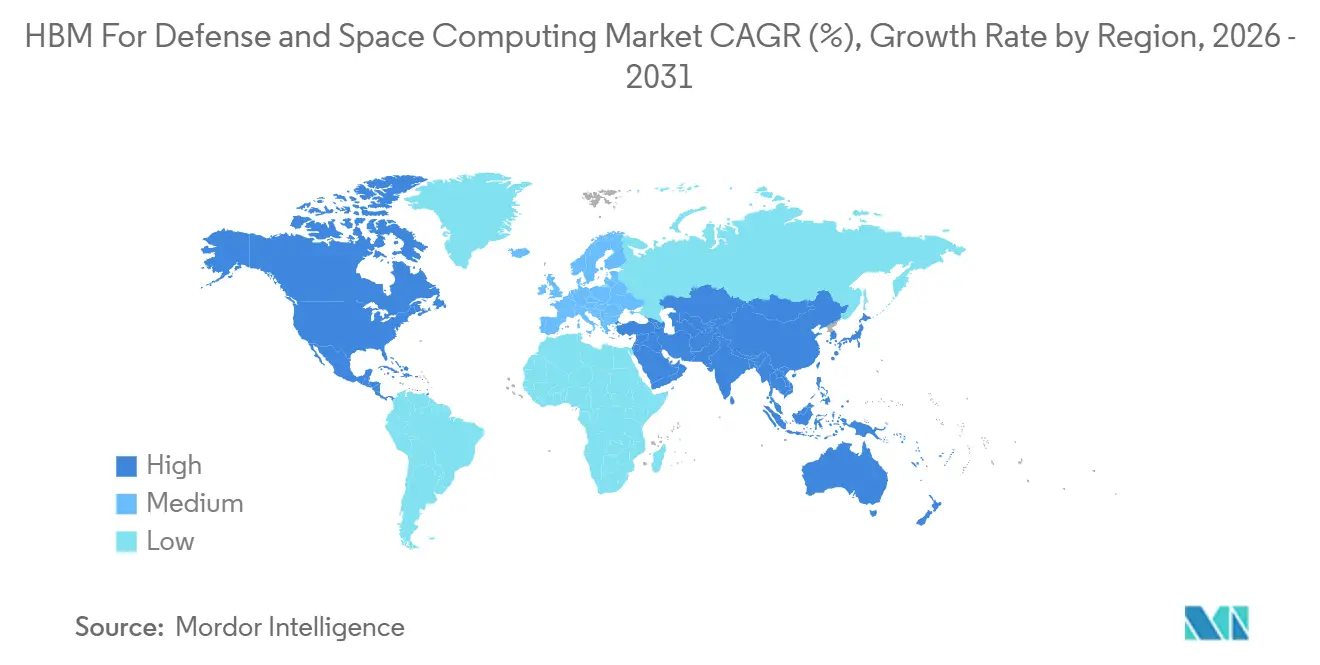

- By geography, North America held 49.06% share in 2025, while Asia-Pacific is projected to grow at a 36.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM For Defense and Space Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HBM Demand in Space-Grade AI and Sensor Fusion Workloads | +9.0% | Global | Long term (≥ 4 years) |

| Defense Prime Shift Toward Onboard Real-Time Analytics | +8.0% | North America and Europe | Medium term (2-4 years) |

| Transition From Discrete Memory to 3D-Stacked Memory in SWaP-Constrained Mission Computers | +6.5% | North America and Asia-Pacific | Medium term (2-4 years) |

| Government Funding for Domestic Advanced Semiconductor Supply Chains | +4.5% | North America | Medium term (2-4 years) |

| Growth in Reconfigurable Mission Processing Architectures Using GPUs, FPGAs, and AI Accelerators | +4.0% | Global | Long term (≥ 4 years) |

| Extended Lifecycle Modernization of Legacy Military and Space Platforms | +3.0% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising HBM Demand in Space-Grade AI And Sensor Fusion Workloads

Space systems are moving beyond relay and observation roles and are increasingly expected to process fused sensor data directly onboard, which raises the bandwidth bar for the HBM for defense and space computing market. A 2026 study in Scientific Reports described an onboard computing architecture that could run autonomous mission planning, multisatellite sensor fusion, and health management without constant ground support, which points to sustained demand for local high-bandwidth memory in future spacecraft designs.[1]J. Rao, W. Zhao, M. Ma, et al., “A High-Performance Onboard Computing Architecture For Autonomous Satellite Mission Planning,” Scientific Reports, nature.com This change also improves operational security because more local inference means less routine transmission of raw data during vulnerable communication windows. Syntiant and Novi Space showed this shift in March 2026 when they demonstrated low-power AI inference in orbit for real-time object detection, which gave the HBM for defense and space computing market a visible proof point for practical deployment. Frontgrade Gaisler also reinforced the same direction through its April 2025 Swedish National Space Agency contract to commercialize neuromorphic AI for space, showing that onboard AI has moved into funded program activity rather than remaining a laboratory concept.

Defense Prime Shift Toward Onboard Real-Time Analytics

Defense integrators are redesigning mission computers around real-time local analytics, and that is pushing the HBM for defense and space computing market into mainstream platform design. Parry Labs launched Forge Boss in September 2025 as the first 3U VPX card to combine FPGA signal processing with AI acceleration for tactical-edge mission computing, which shows how high-bandwidth memory is now tied to deployable open-architecture modules rather than stand-alone prototypes. Pacific Defense extended that direction in March 2026 with its DSP3100VP module built on AMD Versal AI Edge Series Gen 2, aimed at electronic warfare, signal intelligence, and autonomous tracking workloads where data must be processed immediately at the edge. HBM also reduces the amount of high-speed signaling between separate memory and processor devices, which lowers electromagnetic compatibility stress in airborne and ruggedized systems and makes qualification easier for defense primes. As more SOSA- and CMOSS-aligned products come to market, the HBM for defense and space computing market is gaining from a purchasing model that rewards performance and compliance at the same time.

Transition From Discrete Memory To 3D-Stacked Memory in SWaP-Constrained Mission Computers

The shift from discrete DRAM toward stacked memory has become a practical design response to tight size, weight, and power limits, and that is widening adoption in the HBM for defense and space computing market. AMD cited 8x memory bandwidth and 63% lower power for its Versal HBM ACAP against DDR-based approaches, which explains why rugged mission computers are moving toward integrated memory architectures in airborne and unmanned systems. Board simplification is also important because fewer routing paths, fewer controllers, and fewer connectors reduce mass and potential failure points in platforms that must operate for long periods without service. This hardware consolidation also lowers the number of separate memory parts that program offices must qualify, which can shorten refresh cycles and make upgrades easier to manage across long-life platforms. As this pattern spreads, the HBM for defense and space computing market is moving from a performance-led adoption case toward a lifecycle cost and reliability case.

Government Funding for Domestic Advanced Semiconductor Supply Chains

Government funding is giving the HBM for defense and space computing market a stronger domestic manufacturing and qualification base, especially in the United States. The CHIPS for America Defense Fund allocated USD 400 million per year from FY2023 through FY2027, and the FY2025 plan directed USD 265.108 million to advanced technology development that includes 3D and additive manufacturing techniques relevant to advanced packaging.[2]U.S. Department of Defense Office of the Under Secretary of Defense, “FY2025 CHIPS Act Spend Plan,” U.S. Department of Defense, comptroller.defense.gov BAE Systems said in August 2025 that CHIPS Act funding would modernize its Microelectronics Center in Nashua, New Hampshire, which is one of the few U.S. defense-focused GaAs and GaN wafer foundries and supports higher chip output for multiple military branches. The funding pattern is effectively creating a commercial track that races ahead on volume and a defense track that follows with trusted-source qualification, which shapes when each HBM generation can realistically enter military programs. That separation keeps the HBM for defense and space computing market dependent on early insertion planning because buyers that wait too long risk entering a qualification cycle just as the commercial industry has moved on to the next generation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation Qualification, Screening, and Reliability Costs | -3.5% | Global | Long term (≥ 4 years) |

| Limited Supply of HBM-Qualified Advanced Packaging Capacity | -2.5% | Global | Short term (≤ 2 years) |

| Export Controls and Trusted-Foundry Constraints | -2.0% | North America and Asia-Pacific | Medium term (2-4 years) |

| Thermal, Power, and Integration Complexity in Ruggedized Platforms | -1.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Radiation Qualification, Screening, and Reliability Costs

Radiation qualification remains one of the hardest barriers for the HBM for defense and space computing market because each new generation must pass a long and costly validation path before it can be trusted in critical missions. Teledyne e2v began production of its 16 GB DDR4-X1 flight models in March 2026 after an extended qualification process, and even this involved a memory architecture that sits well behind current commercial HBM generations. HBM adds further complexity because stacked dies and through-silicon vias introduce radiation behaviors that older qualification methods were not built to evaluate. BAE Systems highlighted the same burden in June 2026 when it demonstrated its Endura processor on a radiation-hardened platform while still operating within trusted-source rules for high-assurance use. As long as test, screening, and reliability costs remain heavy, the HBM for defense and space computing market will keep qualifying new generations slower than the commercial memory cycle.

Limited Supply of HBM-Qualified Advanced Packaging Capacity

Limited advanced packaging capacity is a near-term supply constraint for the HBM for defense and space computing market because commercial AI programs absorb most of the highest-value packaging slots. The market depends heavily on processes such as CoWoS and CoWoS-L, and those lines are being filled first by large data center accelerator programs with much higher order volumes than defense buyers can place.[3]Micron Technology, “HBM4,” Micron, micron.com Smaller defense procurement lots also make it harder for integrators to reserve packaging access early, which can delay schedules even when the program budget is intact. Many defense programs are therefore leaning toward FPGA-integrated HBM options because the silicon vendor absorbs more of the packaging burden and reduces exposure to stand-alone allocation problems. Micron's July 2026 groundbreaking for an HBM plant expansion in Hiroshima signals future relief, but the HBM for defense and space computing market will still face a lag before new capacity meaningfully improves availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Legacy HBM3 Dominates as HBM4 Opens a New Qualification Race

HBM3 held 43.54% of the HBM for defense and space computing market share in 2025, while HBM4 is projected to expand at a 36.67% CAGR through 2031 from a much smaller base. JEDEC released the HBM4 standard in April 2025 with a 2048-bit interface, up to 2 TB/s total bandwidth, 32 channels per stack, and backward compatibility with HBM3 controllers, which makes the transition path more practical for defense designs already in qualification. Commercial availability is moving faster than defense adoption because the HBM for defense and space computing market still needs a 24- to 36-month qualification window before HBM4 can support broader mission use. Samsung began shipping 12-layer HBM4E samples in May 2026, and the product reached 3.6 TB/s bandwidth with 48 GB capacity and 16% better energy efficiency than the prior generation.

That gap between commercial release and defense readiness is important because it creates a recurring design-in cycle rather than a single upgrade event in the HBM for defense and space computing market. Older HBM1 and HBM2 deployments will continue to serve a limited retrofit base, but they are losing relevance as legacy programs near end of service life. The next phase may also become more specialized because design work around HBM4 points toward customized base-die logic that could support defense-specific correction, control, or acceleration functions within the stack itself. If that direction holds, the HBM for defense and space computing industry may begin to diverge from the commercial roadmap rather than simply follow it with a delay. Commercial volume trends will still matter because they determine how much leverage defense buyers have when negotiating access to later generations.

By Memory Capacity Per Stack: Mid-Tier Capacity Band Anchors Current Designs

The 8 GB to 16 GB band accounted for 47.81% of the HBM for defense and space computing market size in 2025, while the 16 GB to 32 GB band is projected to expand at a 36.44% CAGR through 2031. The leading band reflects the current design point for mission computers, SIGINT processors, and space-grade AI boards that must fit into constrained thermal and mass envelopes. It also marks the range where HBM begins to deliver a clear performance and power advantage over conventional memory while still fitting into existing rugged cooling designs. Up to 4 GB and 4 GB to 8 GB categories remain tied to older deployments and face a narrowing opportunity set as those platforms move toward replacement. Above 32 GB options are entering evaluation for the most demanding computing loads, but they face a steeper path on radiation and integration.

Bandwidth density is what makes the higher-capacity transition more meaningful for the HBM for defense and space computing market than raw capacity alone. Micron stated that its HBM4 36 GB 12-high stack reached more than 2.8 TB/s and over 20% better power efficiency than HBM3E, which supports a design shift toward fewer stacks carrying more throughput. Radar and SIGINT systems are often limited by how fast data can move rather than by nominal compute resources, so a single higher-bandwidth stack can change architecture choices across the board. That is why the move into the 16 GB to 32 GB band signals a reset in memory design rather than a simple specification increase in the HBM for defense and space computing market. Fewer stacks can also reduce board area and the number of interfaces that must be qualified, which makes the higher-capacity band more attractive from both performance and program cost perspectives.

By Processor Interface: FPGA Reconfigurability Holds the Lead as AI Accelerators Scale

FPGA captured 36.62% share in 2025, while AI accelerators are projected to grow at a 36.32% CAGR through 2031 within the HBM for defense and space computing market. FPGA leadership remains tied to the defense procurement model because reconfigurable hardware lets operators refresh algorithms without redesigning the entire platform. That flexibility matters in platforms that stay in service for years and must absorb new workloads after deployment. At the same time, AI accelerators are gaining ground because autonomy, classification, tracking, and local decision systems increasingly need deterministic inference at high bandwidth. GPU systems remain relevant in selected airborne and space computing roles, especially where commercial compute modules can be adapted for harsh-environment use.

The boundary between FPGA and AI accelerator categories is also becoming less clear in the HBM for defense and space computing market. AMD Versal HBM devices combine AI engines, DSP resources, and integrated HBM in one adaptive platform, which means a single product line can address both categories depending on program use. Parry Labs used this direction in Forge Boss by pairing FPGA signal processing and AI acceleration in one SOSA-aligned VPX card for tactical-edge workloads. Pacific Defense followed with a module designed for electronic warfare, signal intelligence, and autonomous tracking, which shows how integrated HBM platforms are becoming core building blocks instead of niche options. This pattern helps the HBM for defense and space computing market because vendors that package memory inside the processor platform can reduce packaging risk for defense integrators and speed design wins.

By Application: SIGINT Leads While Autonomous Systems Gain Momentum

Radar, EO and SIGINT processing held 31.48% share in 2025, while AI and autonomous systems are projected to grow at a 36.58% CAGR through 2031 in the HBM for defense and space computing market. Sensor-heavy workloads remain the largest demand pool because wide-aperture radar, hyperspectral imaging, and real-time signal exploitation need sustained throughput that conventional memory cannot reliably provide in the same form factor. Mission computing and high-performance computing also form a major secondary base because they support command, control, fire control, and other onboard compute tasks across naval and airborne systems. Spacecraft onboard processing is gaining speed as constellations shift from data collection toward onboard filtering, compression, and inference. Electronic warfare also deepens memory demand because countermeasure and spectral analysis workloads keep widening in real-time complexity.

The growth pattern in AI and autonomous systems is distinct because it depends on consistent memory access and fast response, not just peak bandwidth. Syntiant and Novi Space demonstrated low-power AI object detection in orbit in March 2026, which showed that onboard autonomy is already moving into practical mission scenarios. Planet Labs also ran an end-to-end AI inference pipeline in orbit in April 2026, completing geo-rectified object detection onboard and reducing data return delay. On the ground, loitering munitions and autonomous vehicles increasingly need local fusion of camera, lidar, and radio-frequency feeds at millisecond timing, which expands the application base of the HBM for defense and space computing market beyond its earlier signal-processing center of gravity. This is why AI inference is becoming just as important as raw sensor throughput in shaping future demand.

Geography Analysis

North America held 49.06% of the HBM for defense and space computing market share in 2025, which kept it in the leading regional position. The United States anchors that lead through its scale in defense electronics procurement and through direct support for trusted manufacturing and advanced semiconductor work. The CHIPS for America Defense Fund is allocating USD 400 million per year through FY2027, and that continues to support the domestic base needed for advanced packaging, trusted sourcing, and qualification activities. The ATSP5 contract framework also strengthens the region because it covers a wide microelectronics lifecycle and includes 3D advanced packaging work that matters directly to the HBM for defense and space computing market. Canada supports the regional base through allied procurement in surveillance, maritime patrol, and space intelligence, while Mexico remains a smaller participant tied mainly to support and indirect supply chain roles.

Europe held the second-largest position in 2025, supported by NATO modernization programs and next-generation air and unmanned platform activity in the HBM for defense and space computing market. France, Italy, the United Kingdom, and Germany remain the main regional contributors through radar, mission systems, satellite programs, and electronic warfare work. Frontgrade Gaisler received European Commission funding in May 2026 under the COSMIC7 program to develop a 7 nm RISC-V processor for space applications, which supports a stronger regional computing base next to future high-bandwidth memory configurations. EU industrial policy is also nudging procurement toward allied and regional suppliers for sensitive applications, which should gradually improve Europe's position in the HBM for defense and space computing market.

Asia-Pacific is projected to advance at a 36.47% CAGR through 2031, making it the fastest-growing region in the HBM for defense and space computing market. South Korea remains central because global HBM supply depends heavily on Korean vendors, and Samsung moved further ahead in May 2026 by shipping 12-layer HBM4E samples to major customers. Japan is strengthening its role through defense spending growth and through Micron's July 2026 groundbreaking for a major HBM expansion in Hiroshima, which signals long-cycle investment in regional memory capacity. Taiwan remains critical because advanced packaging availability in the wider region depends heavily on TSMC, which makes packaging access a shared constraint across commercial and defense programs. India is still at an early stage, but domestic semiconductor policy and defense modernization are starting to create a pathway for future participation in the HBM for defense and space computing market. South America and the Middle East and Africa remain nascent demand zones where procurement of imported defense electronics matters more than local HBM development.

Competitive Landscape

The HBM for defense and space computing market has a split structure because memory supply is highly concentrated while system integration remains widely fragmented. At the component level, SK hynix, Samsung, and Micron dominate global HBM output, which gives the supply base an oligopolistic profile even before defense qualification is considered. At the integration level, defense primes, embedded computing specialists, and radiation-hardening firms compete across program-specific designs, open-architecture modules, and mission computers. This creates a competition model in which packaging access, qualification readiness, and compliance with defense standards matter as much as raw device performance. The HBM for defense and space computing market therefore rewards suppliers that can bridge commercial memory progress with trusted deployment requirements more effectively than firms that only offer one side of that equation.

The commercial memory vendors are competing on production scale and generation timing, and those moves shape the future cost and availability curve for the HBM for defense and space computing market. Samsung began shipping industry-first 12-layer HBM4E samples in May 2026, which signaled its push to secure early leadership in next-generation bandwidth and efficiency. Micron entered high-volume production of its HBM4 36 GB 12-high stack in Q1 2026, establishing a commercial baseline that future defense qualification programs are likely to track closely. SK hynix also delivered HBM4E 12-high stack samples ahead of schedule in June 2026, which shows how narrow the timing race has become among top memory suppliers.

A second layer of competition is emerging among defense-focused specialists that are turning HBM platforms into deployable rugged systems inside the HBM for defense and space computing market. BAE Systems demonstrated its Endura processor in June 2026 on a radiation-hardened platform, which illustrates a strategy of adapting commercial process capability to high-assurance space missions. Parry Labs advanced a separate path with Forge Boss for tactical-edge mission computing, while Pacific Defense introduced an AI-enabled VPX digital signal processor for warfare and tracking roles, both of which show how smaller specialists can move quickly in open-architecture deployments. Aitech and Teledyne e2v also showed how integration partnerships can support radiation-tolerant onboard AI computing through the SP1 SpaceVPX platform announced in February 2026. The absence of a defense-specific HBM qualification standard still leaves room for differentiation, so the firms that validate later-generation HBM earliest are likely to secure an advantage in the HBM for defense and space computing market.

HBM For Defense and Space Computing Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Micron broke ground on a USD 9.3 billion HBM plant expansion in Hiroshima, Japan, one of the largest single-country semiconductor facility investments by a U.S. memory manufacturer. The capacity expansion is targeted at HBM4 and future-generation production, reinforcing Micron's multi-cycle supply commitment to both commercial AI and defense computing markets.

- June 2026: BAE Systems successfully demonstrated its Endura SoC operating resiliently in natural space and the most severe strategic radiation environments, using GlobalFoundries' commercially licensed RH45nm silicon-on-insulator platform. The milestone positions Endura as a high-performance processor candidate for Class A space missions, with the company now accepting orders for Software Development Units through its U.S. Department of Defense Category 1A Trusted Source facility in Manassas, Virginia.

- May 2026: Samsung Electronics began shipping the industry's first 12-layer HBM4E samples to major global customers, delivering up to 3.6 TB/s bandwidth per stack, 48 GB capacity, 16% improved energy efficiency, and more than 14% better thermal resistance, all using Samsung's 1c-nm DRAM process and a 4 nm logic base die.

- May 2026: Aitech Systems announced integration of the NVIDIA IGX Thor platform into its S-A2300 COTS AI Supercomputer and future space-grade designs, significantly expanding onboard AI processing capabilities for satellites and edge AI missions in harsh environments. This represents Aitech's third generation of space-rated supercomputers.

Global HBM For Defense and Space Computing Market Report Scope

The Global HBM for Defense and Space Computing Market refers to the industry segment focused on the integration of High Bandwidth Memory (HBM) technology into defense and aerospace-grade computing systems, enabling ultra-fast data processing, low latency, and energy-efficient performance for mission-critical applications.

The HBM for Defense and Space Computing Market Report is Segmented by Technology (HBM2, HBM2E, HBM3, HBM3E, and HBM4), Memory Capacity Per Stack (Up To 4 GB, 4 GB To 8 GB, 8 GB To 16 GB, 16 GB To 32 GB, and Above 32 GB), Processor Interface (CPU, GPU, FPGA, ASIC, AI Accelerators, and Networking and Communication Processors), Application (Mission Computing, High-Performance Computing, AI and Autonomous Systems, Radar, EO and SIGINT Processing, Spacecraft On-Board Processing, and Electronic Warfare and Signal Processing), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2 |

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| Up To 4 GB |

| 4 GB To 8 GB |

| 8 GB To 16 GB |

| 16 GB To 32 GB |

| Above 32 GB |

| CPU |

| GPU |

| FPGA |

| ASIC |

| AI Accelerators |

| Networking and Communication Processors |

| Mission Computing |

| High-Performance Computing |

| AI and Autonomous Systems |

| Radar, EO and SIGINT Processing |

| Spacecraft On-Board Processing |

| Electronic Warfare and Signal Processing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Technology | HBM2 | |

| HBM2E | ||

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| By Memory Capacity Per Stack | Up To 4 GB | |

| 4 GB To 8 GB | ||

| 8 GB To 16 GB | ||

| 16 GB To 32 GB | ||

| Above 32 GB | ||

| By Processor Interface | CPU | |

| GPU | ||

| FPGA | ||

| ASIC | ||

| AI Accelerators | ||

| Networking and Communication Processors | ||

| By Application | Mission Computing | |

| High-Performance Computing | ||

| AI and Autonomous Systems | ||

| Radar, EO and SIGINT Processing | ||

| Spacecraft On-Board Processing | ||

| Electronic Warfare and Signal Processing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the HBM for defense and space computing market size through 2031?

The HBM for defense and space computing market was valued at USD 50.86 million in 2025 and is projected to reach USD 320.59 million by 2031 at a 35.47% CAGR during 2026-2031.

Which technology segment leads HBM adoption in defense and space computing?

HBM3 led in 2025 with 43.54% share, reflecting the lag between commercial memory launches and defense qualification cycles.

Which application is growing fastest in defense and space HBM deployment?

AI and autonomous systems are projected to grow the fastest at a 36.58% CAGR through 2031 as more platforms shift toward local inference and sensor-to-action processing.

Why is North America the largest regional opportunity?

North America held 49.06% share in 2025 because of U.S. defense electronics demand, trusted-foundry requirements, and sustained semiconductor funding support.

What is limiting wider HBM deployment in military and space systems?

The main constraints are radiation qualification cost, long reliability screening cycles, and limited access to advanced packaging capacity.

Which processor interface remains most important today?

FPGA held 36.62% share in 2025 because reconfigurable hardware fits long defense procurement cycles and allows later algorithm updates without full hardware redesign.

Page last updated on: