HBM For Automotive AI Processor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

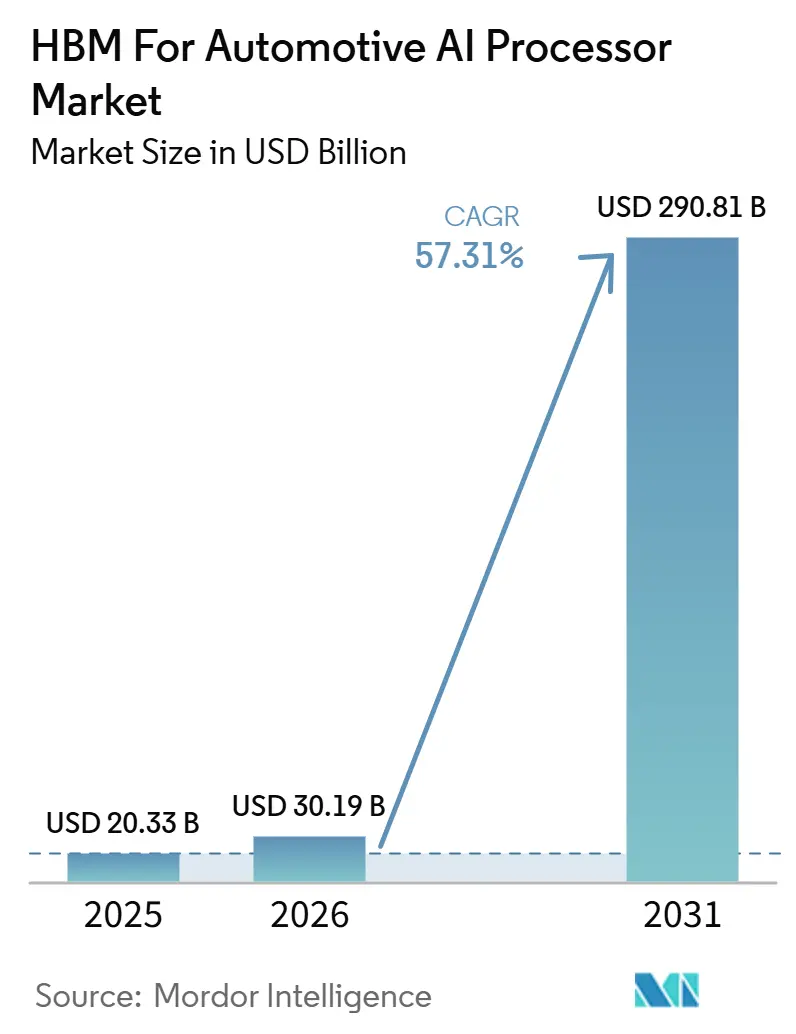

| Market Size (2026) | USD 30.19 Billion |

| Market Size (2031) | USD 290.81 Billion |

| Growth Rate (2026 - 2031) | 57.31% CAGR |

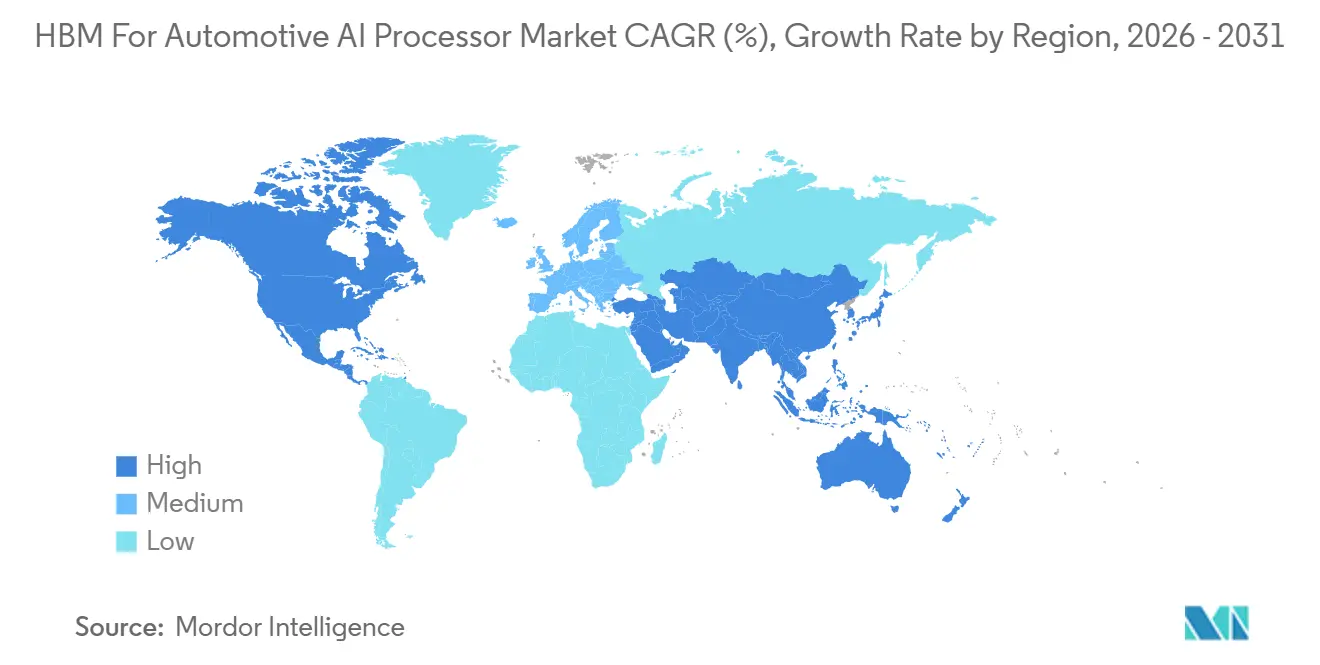

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

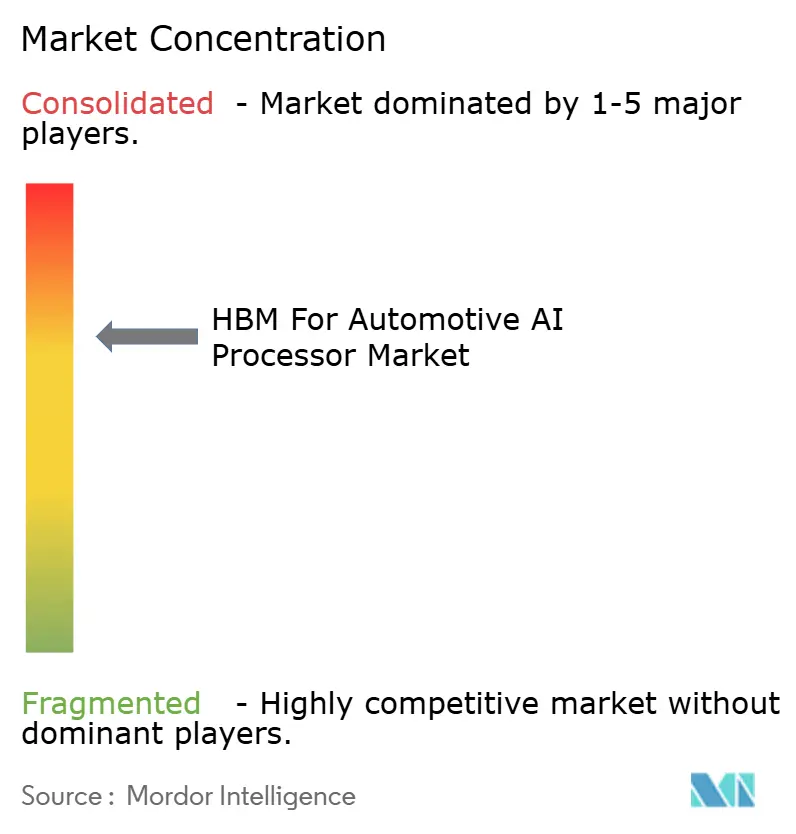

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM For Automotive AI Processor Market Analysis by Mordor Intelligence

The HBM for automotive AI processor market size is expected to increase from USD 20.33 million in 2025 to USD 30.19 million in 2026 and reach USD 290.81 million by 2031, growing at a CAGR of 57.31% over 2026-2031. The HBM for automotive AI processor market is moving from early platform planning into active qualification, sourcing, and design-in activity as centralized vehicle compute becomes more common across premium programs. Demand is rising because software-defined vehicle roadmaps are keeping more code, models, and data inside the vehicle, while higher autonomy programs are pushing memory bandwidth needs beyond what legacy architectures can support on their own. The competitive position of suppliers is also becoming more durable because once an OEM selects a platform with integrated HBM, the memory choice often stays fixed through a multi-year vehicle cycle. Supply discipline remains a major commercial factor because HBM capacity is heavily concentrated and the automotive version must clear long qualification cycles before it can ship at scale. This leaves room for early qualified suppliers and platform partners to secure long visibility in the HBM for automotive AI processor market while later entrants face a narrower design window.

Key Report Takeaways

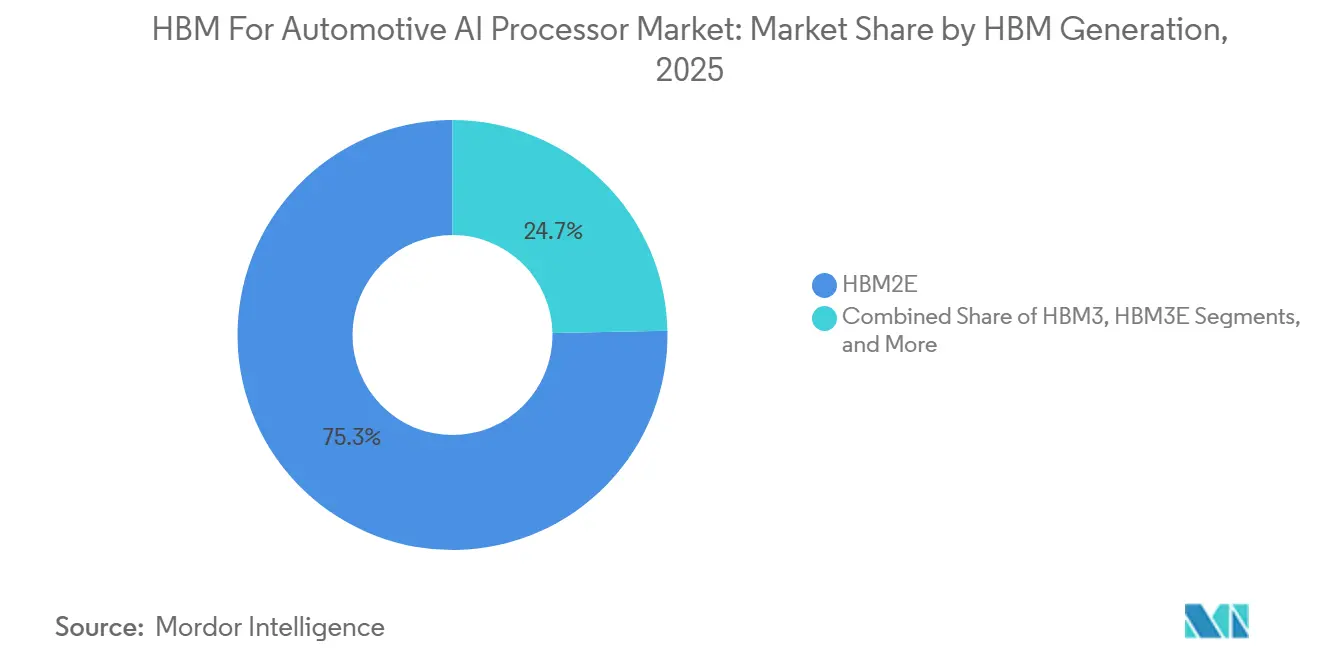

- By HBM generation, HBM2E held 75.31% share of the HBM for automotive AI processor market in 2025, while HBM4 is projected to expand at a 57.91% CAGR through 2031.

- By processor type, GPU-based AI processors held 51.12% share in 2025, while heterogeneous AI SoCs are projected to expand at a 58.29% CAGR through 2031.

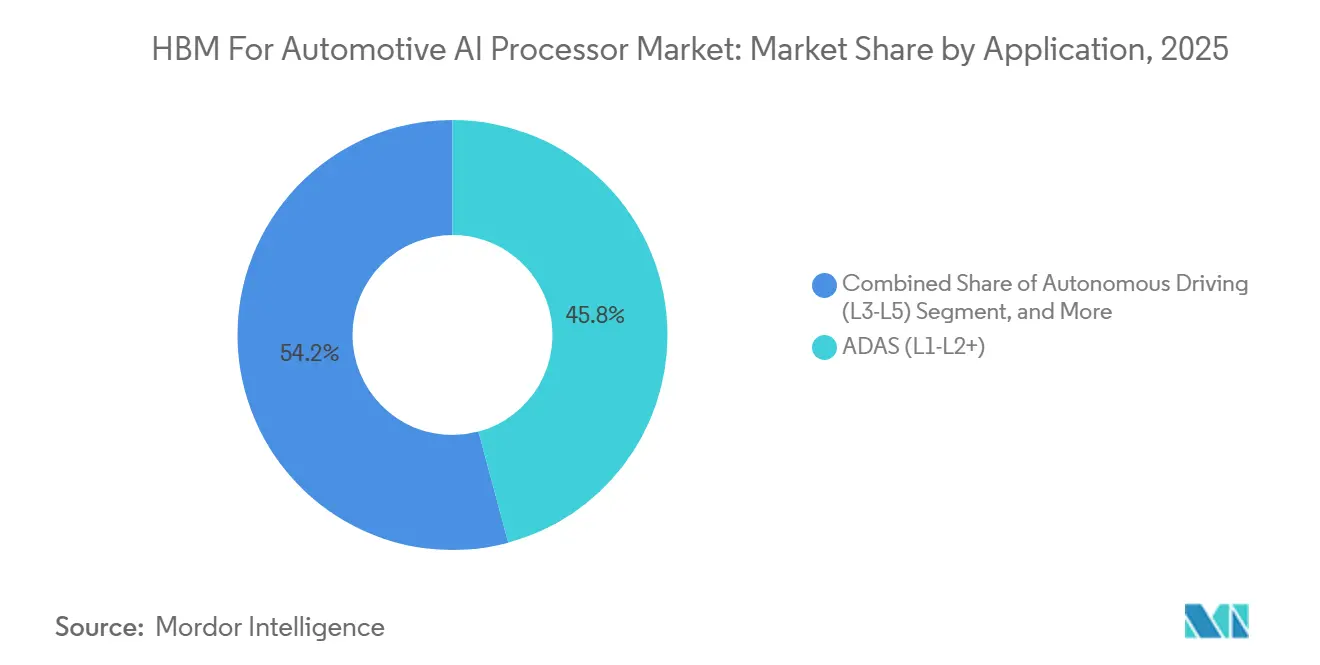

- By application, ADAS L1-L2+ held 45.82% share in 2025, while autonomous driving L3-L5 is projected to expand at a 58.23% CAGR through 2031.

- By vehicle type, passenger cars held 83.94% share of the HBM for automotive AI processor market in 2025, while heavy commercial vehicles are projected to expand at a 57.84% CAGR through 2031.

- By geography, North America held 41.78% share in 2025, while Asia-Pacific is projected to expand at a 58.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM For Automotive AI Processor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Centralized Vehicle Compute Increases Bandwidth Intensity | +14.5% | Global, concentrated in North America and China | Medium term (2-4 years) |

| ADAS Safety Requirements Push Higher Memory Throughput | +11.2% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Software-Defined Vehicle Architectures Raise In-Vehicle Data Loads | +8.8% | Global, with strong relevance in Europe and China | Medium term (2-4 years) |

| Automotive AI Processors Need Low Latency Memory for Real-Time Inference | +7.3% | Global, with strong relevance in Asia-Pacific and North America | Short term (≤ 2 years) |

| In-Cabin Generative AI Expands Compute and Memory Demand | +5.9% | North America and China for premium cockpit platforms | Short term (≤ 2 years) |

| HBM Qualification Tied to Premium Platform Design Wins | +4.2% | Global, strongest in North America, Europe, and Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Centralized Vehicle Compute Increases Bandwidth Intensity

The HBM for automotive AI processor market is being pushed by the move from distributed ECU layouts to centralized vehicle compute platforms that pull more functions into a shared processing domain.[1]NVIDIA, “NVIDIA Unveils DRIVE Thor, Centralized Car Computer Unifying Cluster, Infotainment, Automated Driving, and Parking in a Single, Cost-Saving System,” NVIDIA Newsroom NVIDIA said DRIVE AGX Thor consolidates cluster, infotainment, automated driving, and parking into one SoC and scales up to 2,000 FP4 teraflops, which shows how quickly vehicle compute density is rising at the platform level. Micron stated that Level 3 systems require 100 GB/s to 256 GB/s of DRAM bandwidth, while advanced Level 4 platforms can move beyond 1 TB/s under heavier sensor fusion conditions. That gap matters because current LPDDR5X implementations already stretch toward high throughput levels, so the next step in performance depends less on adding controllers and more on changing the memory architecture itself. ISO 26262 and long validation cycles also narrow the range of acceptable memory choices because the subsystem has to support both safety and sustained performance inside the same vehicle program. Once an OEM commits to centralized compute, the HBM for automotive AI processors market gains a stronger demand base because the memory roadmap becomes part of the platform decision rather than a late-stage component swap.

ADAS Safety Requirements Push Higher Memory Throughput

The HBM for automotive AI processor market is also benefiting from the rising technical floor for ADAS hardware as safety systems move into more sensor-rich and software-heavy operating conditions.[2]Micron Technology, “Micron Makes Automotive Memory SAFER,” Micron Technology Micron's automotive memory framework highlighted 256-bit to 512-bit memory bus widths and 8.5 Gbps I/O signaling rates for advanced LPDDR5X use cases, which shows how far current systems already push conventional memory designs. As vehicles process more camera, radar, and lidar data at the same time, the problem shifts from isolated feature execution toward sustained multi-sensor fusion under strict power and thermal limits. Mobileye said in January 2026 that future EyeQ6H commitments exceeded 19 million systems, which points to broad OEM alignment behind more integrated perception and surround ADAS architectures. That scale matters because high-volume ADAS deployments shape the hardware baseline that future autonomy programs build on top of in the HBM for automotive AI processors market. As the safety stack becomes more compute-intensive, memory throughput moves closer to a core design criterion instead of a secondary tuning variable.

Software-Defined Vehicle Architectures Raise In-Vehicle Data Loads

The HBM for automotive AI processor market is being supported by software-defined vehicle programs that keep expanding the software and model load that must remain active inside the vehicle after launch. Micron said software code volume in high-end vehicles is expected to rise from nearly 100 million lines to close to 1 billion lines as software-defined architectures mature. That change raises the need for memory subsystems that can handle dense code bases, larger AI models, and repeated over-the-air updates without forcing a redesign of the platform. Visteon introduced an AI-ADAS compute module in January 2026 that supports hybrid edge-cloud AI for cockpit and ADAS functions on NVIDIA software, which reflects how compute domains are now being designed to work together instead of as separate blocks. LG Electronics also introduced an AI Cabin Platform for CES 2026 that runs multimodal language, vision, and image-generation models on automotive hardware from NVIDIA and Qualcomm, adding a second software-heavy workload inside the same vehicle environment. As more features stay live in the vehicle throughout the ownership cycle, bandwidth and density begin to rise together, which supports continued expansion in the HBM for automotive AI processors market.

Automotive AI Processors Need Low Latency Memory for Real-Time Inference

Real-time inference keeps the HBM for automotive AI processor market focused on memory systems that can respond quickly under live driving conditions rather than only looking strong in peak benchmark results. Micron's published automotive memory framework shows that advanced ADAS and autonomy stacks already require wide buses and sustained throughput while staying within automotive power and reliability limits. Qualcomm and BMW brought Snapdragon Ride Pilot into production in the BMW iX3 in September 2025, which shows that automated driving platforms are already crossing from development into deployed vehicle programs. Mobileye's January 2026 update on EyeQ6H commitments shows that OEMs are selecting integrated perception platforms at large scale, which increases the pressure on memory subsystems to deliver predictable response times. In practical terms, processor branding loses some value when the memory path cannot keep pace with sensor fusion and model execution inside the vehicle. That is why low-latency memory remains a core requirement for competitive platform design across the HBM for automotive AI processors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive Qualification Cycles Slow Commercialization | -5.8% | Global, universal AEC-Q100 requirement | Short term (≤ 2 years) |

| Thermal And Power Constraints Limit HBM Adoption in Mass Market Vehicles | -4.2% | Global, with acute pressure in Asia-Pacific mass-market segments | Medium term (2-4 years) |

| HBM Cost Premium Restricts Penetration Beyond Premium Segments | -3.5% | Asia-Pacific and other price-sensitive markets | Medium term (2-4 years) |

| Supply Concentration Creates Allocation Risk for Automakers and Tier 1 Suppliers | -2.9% | Global, strongest for non-preferential automotive buyers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automotive Qualification Cycles Slow Commercialization

Qualification remains one of the strongest limits on the HBM for automotive AI processor market because automotive memory cannot move on the same timetable as data-center memory.[3]Weebit Nano, “The Road to AEC-Q100 Qualification,” Weebit Nano Weebit Nano described the AEC-Q100 path as requiring stress testing across 3 production lots with 77 samples per lot and zero failures over 1,000 to 2,000 hours of accelerated testing. The same framework also includes temperature cycling from -55°C to 150°C and full failure analysis, which makes the qualification burden especially heavy for a stacked memory architecture such as HBM. That burden extends beyond the memory die because the base die, through-silicon vias, packaging stack, and processor integration all have to prove long-cycle reliability in vehicle conditions. Functional safety adds a second layer because ISO 26262 documentation and safety validation must align with the memory design before the platform can scale across OEM programs. This slows commercialization in the HBM for automotive AI processor market even when demand signals are strong and capacity exists elsewhere in the broader AI memory ecosystem.

Thermal And Power Constraints Limit HBM Adoption in Mass Market Vehicles

Thermal and power limits still restrict the HBM for automotive AI processor market because vehicle electronics do not operate in the controlled cooling environment used in servers. Automotive platforms must withstand wide temperature ranges and long durability cycles, so any memory stack that raises local heat density creates a packaging and reliability challenge at the module level. SK Hynix said HBM4 development moved to a 12-layer product and the new generation is built for higher bandwidth, which implies a denser electrical and thermal design burden as memory performance moves forward. The IEEE ITHERM 2025 work on compact thermal modeling for HBM also showed that accurate system-in-package thermal characterization is essential for avoiding localized hotspots under real workloads. These constraints are easier to absorb in premium vehicles and specialized fleets that already justify stronger cooling systems and higher compute spending. In lower-priced vehicles, the same constraints delay adoption because the memory advantage must be weighed against packaging, cooling, and cost tradeoffs inside the HBM for automotive AI processors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Generation: HBM2E Holds the Revenue Base as HBM4 Resets the Roadmap

HBM2E held 75.31% of the HBM for automotive AI processor market share in 2025, which reflected the generation already tied to production automotive AI platforms and long vehicle design cycles. That position did not signal a pause in technology progress, because much of the revenue base came from earlier processor selections that stayed locked into production after initial vehicle launch. In the HBM for automotive AI processor market, those earlier commitments matter because automotive programs usually stay in production for several years after the memory choice is finalized. That creates a durable tail for HBM2E even while newer generations move into evaluation and qualification for future vehicle launches. HBM3 and HBM3E therefore sit in an intermediate position, where they are technically closer to the next wave of automotive AI platforms but still depend on automotive-grade validation before broader adoption can follow.

HBM4 is projected to expand at a 57.91% CAGR from 2026 to 2031, which makes it the strongest forward generation in the HBM for automotive AI processor market. SK Hynix said in March 2025 that it completed the world's first HBM4 development and prepared for mass production, which confirms that supplier roadmaps are already aligned around the next bandwidth step. The company later shipped 12-layer HBM4E samples in June 2026 with 16 Gbps per pin data transfer speed and more than 20% better power efficiency than HBM4, showing how quickly the performance ladder is moving. Even so, the automotive path will remain slower than the data-center path because AEC-Q100 and safety requirements stretch the timing between initial product release and vehicle-grade availability. This means the HBM for automotive AI processor industry is likely to see a long overlap period where HBM2E supports the installed base while HBM4 builds the next round of design wins.

By Processor Type: GPU Platforms Lead Today, But SoC Convergence is Quietly Reshaping Demand

GPU-based AI processors accounted for 51.12% of the HBM for automotive AI processor market size in 2025, which matched the strong deployment base of GPU-centered compute platforms in premium automotive programs. That lead is closely tied to the commercial reach of NVIDIA's DRIVE ecosystem, which has secured design commitments from a broad list of global OEMs for advanced automated driving programs. In the HBM for automotive AI processor market, GPU platforms still offer the clearest production reference point because they entered vehicle programs earlier and built a wider installed base across premium applications. At the same time, the center of demand is starting to shift because OEMs want fewer chips handling more domains, especially as cockpit, ADAS, and centralized compute begin to converge. That shift reduces the appeal of discrete compute blocks and supports architectures that combine multiple accelerators inside a unified automotive design.

Heterogeneous AI SoCs are projected to expand at a 58.29% CAGR from 2026 to 2031, which makes them the fastest-growing processor group in the HBM for automotive AI processor market. Their rise reflects a broader move toward domain convergence, where the value of the processor depends on how well it combines AI acceleration, graphics, connectivity, and memory access within one platform. Qualcomm's production deployment with BMW and its expanded 2026 collaboration with Stellantis show how scalable automotive SoCs are being positioned for multi-domain deployment across next-generation vehicle architectures. ASIC-based and NPU-based processors still hold value for focused workloads where efficiency, cost control, or validated function matter more than broad flexibility. FPGA-based processors remain useful in prototyping and validation, but the HBM for automotive AI processor industry is increasingly favoring production-ready platforms that offer higher integration and cleaner system scaling.

By Application: Autonomous Driving Takes the Lead for Growth While ADAS Anchors Today's Revenue

Autonomous driving L3-L5 is projected to expand at a 58.23% CAGR from 2026 to 2031, which makes it the most aggressive application path in the HBM for automotive AI processor market. Micron said that DRAM bandwidth needs rise sharply as autonomy levels move upward, with the most demanding Level 4 workloads crossing well beyond the range that lower-bandwidth memory can support on its own. NVIDIA said DRIVE Hyperion has been adopted for Level 4 programs by BYD, Geely, Isuzu, and Nissan, alongside earlier commitments from Mercedes-Benz, Toyota, GM, Hyundai, and Kia. NVIDIA and Uber also announced in March 2026 that they plan to deploy DRIVE AV-powered autonomous vehicles across 28 cities by 2028, which gives the application a clearer commercial rollout path. Together, these moves suggest that the HBM for automotive AI processor market will see autonomous driving set the pace for the next memory performance requirement rather than simply following broader ADAS upgrades.

ADAS L1-L2+ accounted for 45.82% of the HBM for automotive AI processor market size in 2025, which kept it as the largest current application base. That share reflected the large installed base of production vehicles using lane keeping, adaptive cruise, emergency braking, and other sensor-driven functions that are already commercial today. Most of these systems still rely on LPDDR5 or LPDDR5X, but the HBM for automotive AI processor market is affected as ADAS moves from isolated functions toward fuller surround perception and fused decision layers. AI cockpit and occupant-facing systems remain smaller than ADAS and autonomy, yet LG's CES 2026 platform shows that multimodal models are starting to create a separate memory-intensive workload inside the cabin. Telematics, connectivity, V2X, and automotive edge AI computing should remain smaller near-term segments, but they still broaden the number of vehicle functions competing for memory resources over time.

By Vehicle Type: Passenger Cars Drive Volume While Commercial Vehicles Point to the Longer-Range Opportunity

Heavy commercial vehicles are projected to expand at a 57.84% CAGR from 2026 to 2031, which makes them the fastest-growing vehicle class in the HBM for automotive AI processors market. The segment benefits from a clearer economic case because fleet operators can tie higher autonomy spending to route efficiency, labor reduction, and utilization gains more directly than many passenger car buyers can. NVIDIA said at GTC 2026 that Isuzu and TIER IV are jointly developing a Level 4 autonomous bus powered by DRIVE AGX Thor, which gives the commercial vehicle path a visible program example. Commercial platforms can also absorb higher compute and cooling cost more easily when the hardware supports measurable fleet returns and longer operating schedules. For that reason, heavy commercial demand could become an important second growth engine in the HBM for automotive AI processor market even if passenger vehicles remain larger in absolute value for most of the forecast period.

Passenger cars accounted for 83.94% of the HBM for automotive AI processor market size in 2025, which confirms that premium passenger platforms remain the first large-scale entry point for advanced automotive AI memory. NVIDIA's ecosystem footprint across Mercedes-Benz, Toyota, GM, Hyundai, Kia, Nissan, BYD, and Geely shows that passenger vehicle programs still define most current design activity in the HBM for automotive AI processor market. Premium passenger vehicles tend to adopt new compute and memory architectures earlier because they can carry higher electronics content and support richer software feature sets across infotainment and driver assistance. Light commercial vehicles sit between the two extremes and are likely to follow passenger platform timing as shared compute designs move into broader fleets. Over time, the passenger car concentration should ease, but it remains the main revenue anchor for the HBM for automotive AI processor market today.

Geography Analysis

North America held 41.78% of HBM for automotive AI processor market share in 2025, which made it the leading regional base for current demand. The region benefits from NVIDIA's broad DRIVE ecosystem footprint, with design commitments spanning Mercedes-Benz, Toyota, GM, Hyundai, Kia, Nissan, BYD, Geely, Isuzu, and others across high-end automated driving programs. Micron and General Motors signed a Strategic Customer Agreement on July 1, 2026 to secure long-term memory and storage supply for GM vehicle production, which strengthens the local sourcing case for future automotive platforms. Qualcomm's Ride Pilot debut with BMW in September 2025 and its validation across more than 60 countries also show how North American platform suppliers are influencing automated driving programs well beyond their home region.

Europe remained a major demand center in 2025 because premium OEM concentration and advanced vehicle electronics programs kept the region tightly linked to the HBM for automotive AI processor market. NVIDIA said Mercedes-Benz's upcoming S-Class is being built on NVIDIA DRIVE AV with an L4-ready architecture, which makes Europe an important premium design-win region for high-bandwidth memory adoption. Stellantis and Qualcomm expanded their multi-year collaboration in May 2026 to deploy Snapdragon Digital Chassis platforms across next-generation vehicle architectures, which added scale to the region's cockpit, connectivity, and ADAS transition. The regional pattern is therefore less about early memory volume on its own and more about how premium programs in Europe keep setting the technical baseline for future vehicle compute stacks.

Asia-Pacific is projected to expand at a 58.22% CAGR from 2026 to 2031, which makes it the fastest-growing region in the HBM for automotive AI processor market. Growth in the region is tied to the concentration of memory manufacturing, the rising role of Asian OEMs in advanced vehicle compute, and the widening number of automated driving programs that now sit inside the DRIVE ecosystem. SK Hynix shipped 12-layer HBM4E samples in June 2026 and highlighted better power efficiency and larger stack capacity, which underscores the region's importance on the supply side of next-generation automotive memory. Hyundai Motor and Kia also expanded their strategic partnership with NVIDIA in March 2026 for next-generation autonomous driving technology based on DRIVE Hyperion, which reinforces Asia-Pacific's role in future vehicle platform rollouts. South America and Middle East and Africa remained earlier-stage regions for the HBM for automotive AI processors market because high-autonomy deployment and local high-performance platform manufacturing are still less developed there.

Competitive Landscape

The HBM for automotive AI processor market remains highly concentrated on the memory supply side because only a small number of vendors control meaningful HBM production and qualification capacity. In this tier, competitive advantage depends not only on output but also on who can align new HBM generations with automotive qualification timelines and platform roadmaps. SK Hynix strengthened that position by completing HBM4 development in 2025 and shipping 12-layer HBM4E samples in 2026, which showed both technology leadership and a fast commercialization cadence. Micron built a different advantage by tying domestic supply and customer agreements more closely to automotive programs, as seen in its July 2026 Strategic Customer Agreement with General Motors.

On the platform side, NVIDIA remains the broadest ecosystem anchor in the HBM for automotive AI processor market because DRIVE Hyperion has been adopted across a wide group of global OEM programs. Qualcomm is the clearest large-scale challenger, with the BMW iX3 production launch and the expanded Stellantis partnership showing that its automotive compute roadmap is now embedded in real vehicle programs. Mobileye holds a separate position in ADAS-heavy deployments, and its disclosed EyeQ6H commitments show that it still has strong pull with OEMs pursuing scalable surround sensing programs. This means the HBM for automotive AI processors market is concentrated in memory supply while remaining more varied at the processor and platform layer.

Strategic moves in 2025 and 2026 show that the market is being shaped through long-cycle partnerships rather than one-off component transactions. Micron's agreement with GM was designed to secure reliable supply and future platform support, which highlights how memory vendors are trying to lock in demand ahead of wider software-defined vehicle adoption. SK Hynix used early HBM4 and HBM4E milestones to strengthen its position with major customers, which may matter as automotive qualification shifts attention to the next generation. NVIDIA extended the platform opportunity by expanding its autonomous vehicle partnership with Uber and by broadening Hyperion adoption across global OEMs, which supports longer demand visibility for advanced automotive memory. Stellantis and Qualcomm also deepened their collaboration around ADAS, cockpit, and connectivity, which shows that platform standardization is becoming a direct route to larger memory content over time.

HBM For Automotive AI Processor Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Micron Technology and General Motors signed a Strategic Customer Agreement to secure long-term, reliable supply of memory and storage platforms critical to GM's vehicle production and future platform innovation. The agreement is one of 16 SCAs Micron highlighted during its fiscal Q3 2026 earnings call, signaling a systematic effort to lock in automotive supply chain relationships ahead of SDV-driven memory demand escalation.

- June 2026: SK Hynix shipped 12-layer HBM4E samples to major customers, offering a maximum data transfer speed of 16 Gbps per pin and over 20% power efficiency improvement compared to HBM4. The product employs the company's Advanced MR-MUF packaging technology, achieving 48 GB capacity in a 12-layer stack, with implications for AI data-center customers and a downstream automotive qualification roadmap.

- May 2026: Stellantis and Qualcomm Technologies announced an expanded multi-year collaboration to deploy Snapdragon Digital Chassis SoCs, covering ADAS, cockpit, and connectivity, across next-generation Stellantis vehicle architectures, integrating with Stellantis's STLA Brain platform. The scalable standardization approach is designed to improve cost efficiency and accelerate time to market across Stellantis brands.

- March 2026: NVIDIA and Uber announced an expansion of their autonomous vehicle partnership, targeting a fleet of NVIDIA DRIVE AV software-driven autonomous vehicles across 28 cities on 4 continents by 2028. Deployment is planned to begin in Los Angeles and San Francisco in H1 2027, with systematic city-by-city rollout through the Alpamayo autonomous vehicle model suite.

Global HBM For Automotive AI Processor Market Report Scope

The HBM for Automotive AI Processor Market refers to the industry segment focused on the integration of High Bandwidth Memory (HBM) technology into automotive-grade artificial intelligence (AI) processors, enabling advanced driver-assistance systems (ADAS), autonomous driving, and real-time in-vehicle data processing.

The HBM for Automotive AI Processor Market Report is Segmented by HBM Generation (HBM2E, HBM3, HBM3E, and HBM4), Processor Type (GPU Based AI Processors, ASIC Based AI Processors, NPU Based AI Processors, FPGA Based AI Processors, and Heterogeneous AI SoCs), Application (ADAS (L1-L2+), Autonomous Driving (L3-L5), AI Cockpit and Occupant Monitoring, Telematics, Connectivity, and V2X, and Automotive Edge AI Computing), Vehicle Type (Passenger Cars, Light Commercial, and Heavy Commercial), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| GPU Based AI Processors |

| ASIC Based AI Processors |

| NPU Based AI Processors |

| FPGA Based AI Processors |

| Heterogeneous AI SoCs |

| ADAS (L1-L2+) |

| Autonomous Driving (L3-L5) |

| AI Cockpit and Occupant Monitoring |

| Telematics, Connectivity, and V2X |

| Automotive Edge AI Computing |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By HBM Generation | HBM2E | |

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| By Processor Type | GPU Based AI Processors | |

| ASIC Based AI Processors | ||

| NPU Based AI Processors | ||

| FPGA Based AI Processors | ||

| Heterogeneous AI SoCs | ||

| By Application | ADAS (L1-L2+) | |

| Autonomous Driving (L3-L5) | ||

| AI Cockpit and Occupant Monitoring | ||

| Telematics, Connectivity, and V2X | ||

| Automotive Edge AI Computing | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of HBM for automotive AI processor market?

The market is estimated at USD 30.19 million in 2026 and is forecast to reach USD 290.81 million by 2031 at a 57.31% CAGR.

Which HBM generation leads current revenue?

HBM2E led with 75.31% share in 2025 because existing automotive AI platforms remain tied to long design and production cycles.

Which processor architecture is growing the fastest?

Heterogeneous AI SoCs are projected to expand at a 58.29% CAGR through 2031 as cockpit, ADAS, and centralized compute functions continue to converge.

Why is autonomous driving the strongest application driver?

Autonomous driving L3-L5 is projected to grow at a 58.23% CAGR because higher autonomy requires much more bandwidth for sensor fusion and real-time AI processing.

Which vehicle category creates the largest current demand?

Passenger cars accounted for 83.94% of 2025 revenue because premium passenger platforms remain the first large-scale users of advanced automotive AI compute.

Which region is growing the fastest?

Asia-Pacific is projected to expand at a 58.22% CAGR through 2031, supported by strong memory supply capacity and expanding advanced vehicle compute programs.

Page last updated on: