HBM For AI Inference Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

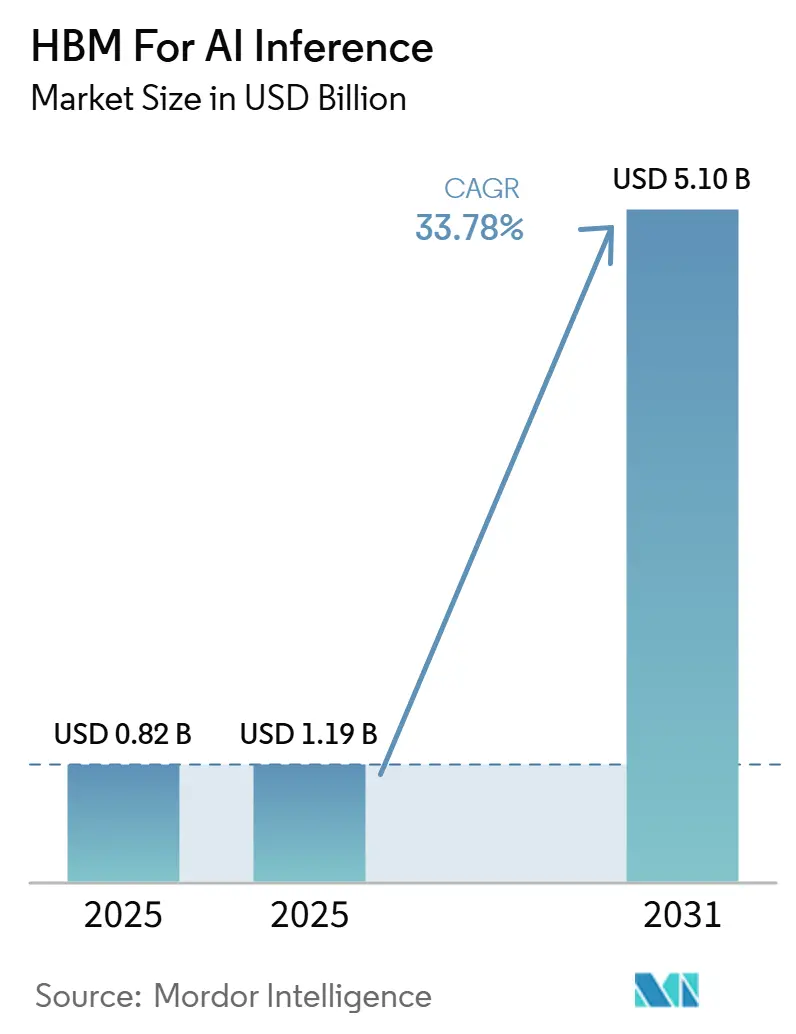

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 5.10 Billion |

| Growth Rate (2025 - 2031) | 33.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

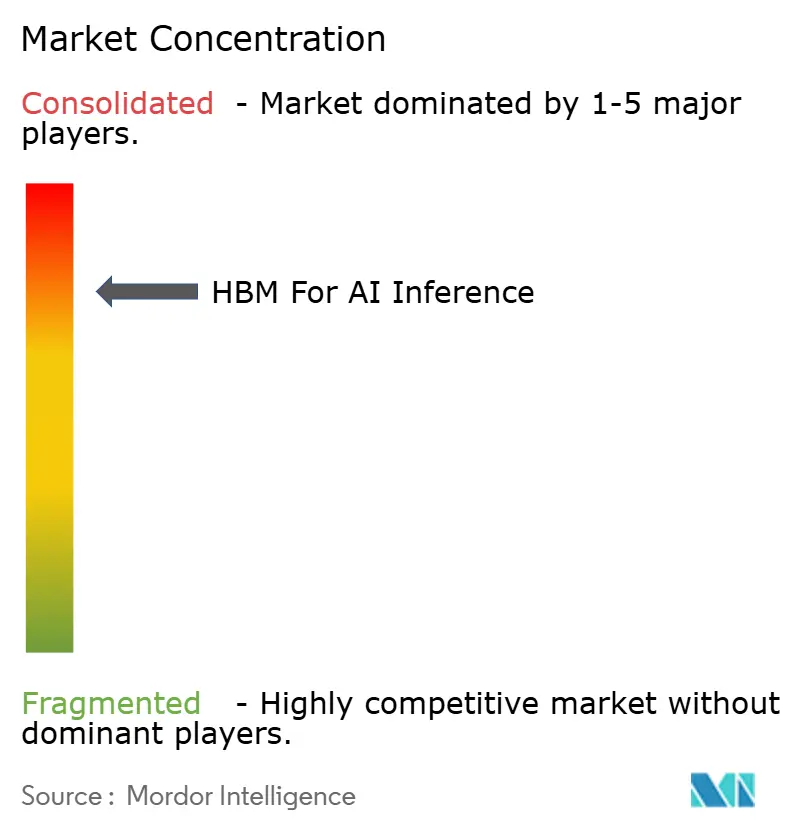

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM For AI Inference Market Analysis by Mordor Intelligence

The HBM for AI inference market was valued at USD 0.82 billion in 2025 and is forecast to reach USD 5.1 billion by 2031, growing at a CAGR of 33.78% during 2026-2031. The expansion reflects a clear shift in AI spending from training-heavy cycles toward inference-heavy deployment, where memory bandwidth has become a core performance limit rather than a supporting specification. As models move toward longer contexts, higher concurrency, and more agentic use cases, accelerator design is placing more value on moving data efficiently than on adding compute alone. The demand base is also widening because hyperscalers are no longer the only route to HBM consumption, as custom silicon programs now procure advanced memory directly for internal inference stacks. Supply remains tight because HBM stack yields, advanced packaging availability, and qualification timelines are all constraining how quickly new capacity turns into deployable product. Over the forecast period, the HBM for AI inference market is poised to grow as content per accelerator rises and broader adoption spreads across cloud, enterprise, and regional AI infrastructure programs.

Key Report Takeaways

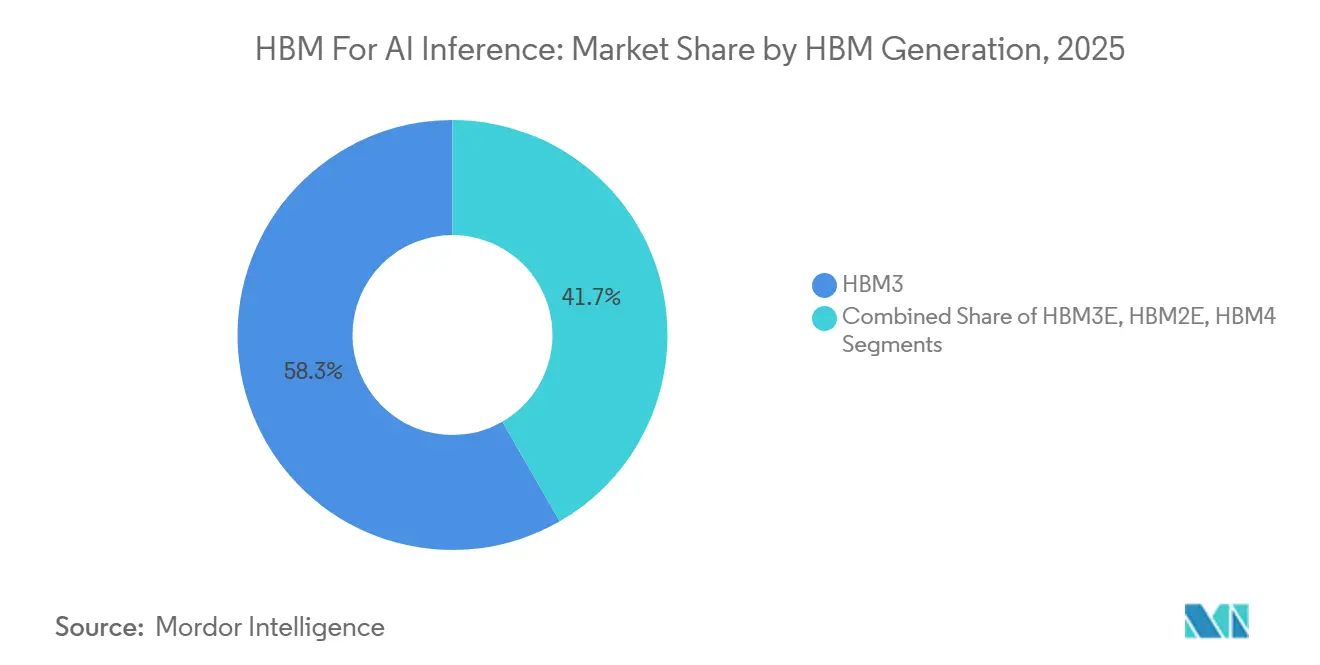

- By HBM generation, HBM3 held 58.31% share in 2025, while HBM4 is projected to expand at a 34.58% CAGR through 2031 in HBM for AI Inference Market.

- By compute platform, GPUs accounted for 82.74% of the market in 2025, while NPU is expected to record the fastest growth at a 34.73% CAGR through 2031 in HBM for AI Inference Market.

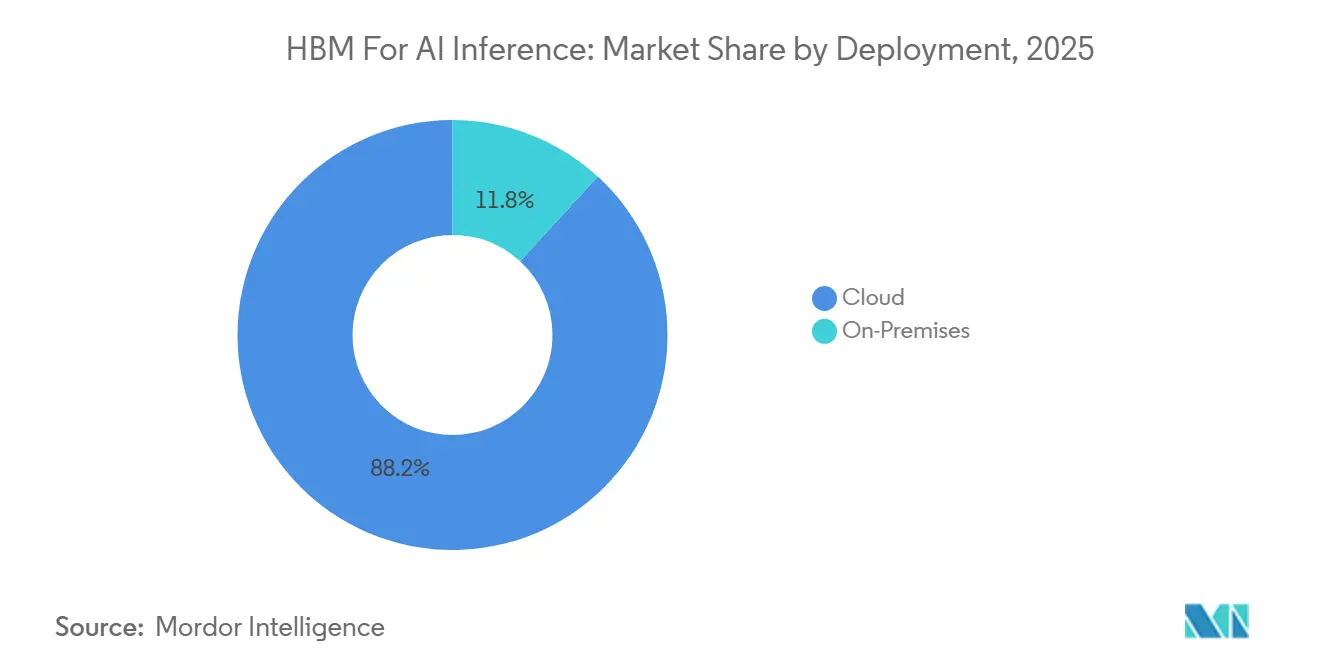

- By deployment, cloud held 88.19% of the AI inference market share in 2025 and is projected to expand at a 34.16% CAGR through 2031 in HBM for AI Inference Market.

- By end user, cloud service providers accounted for 78.26% of the market in 2025, while enterprises are projected to expand at a 34.76% CAGR through 2031 in HBM for AI Inference Market.

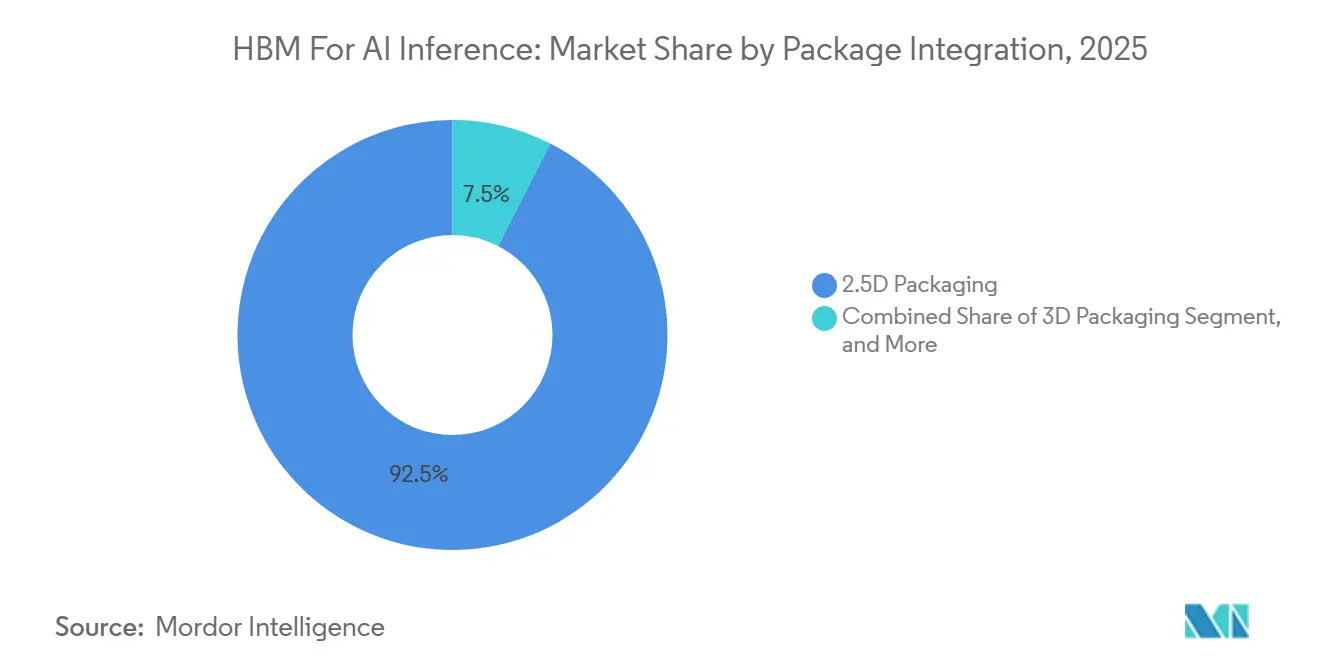

- By package integration, 2.5D packaging captured 92.49% share in 2025, while chiplet-based integration is expected to grow at a 34.29% CAGR through 2031 in HBM for AI Inference Market.

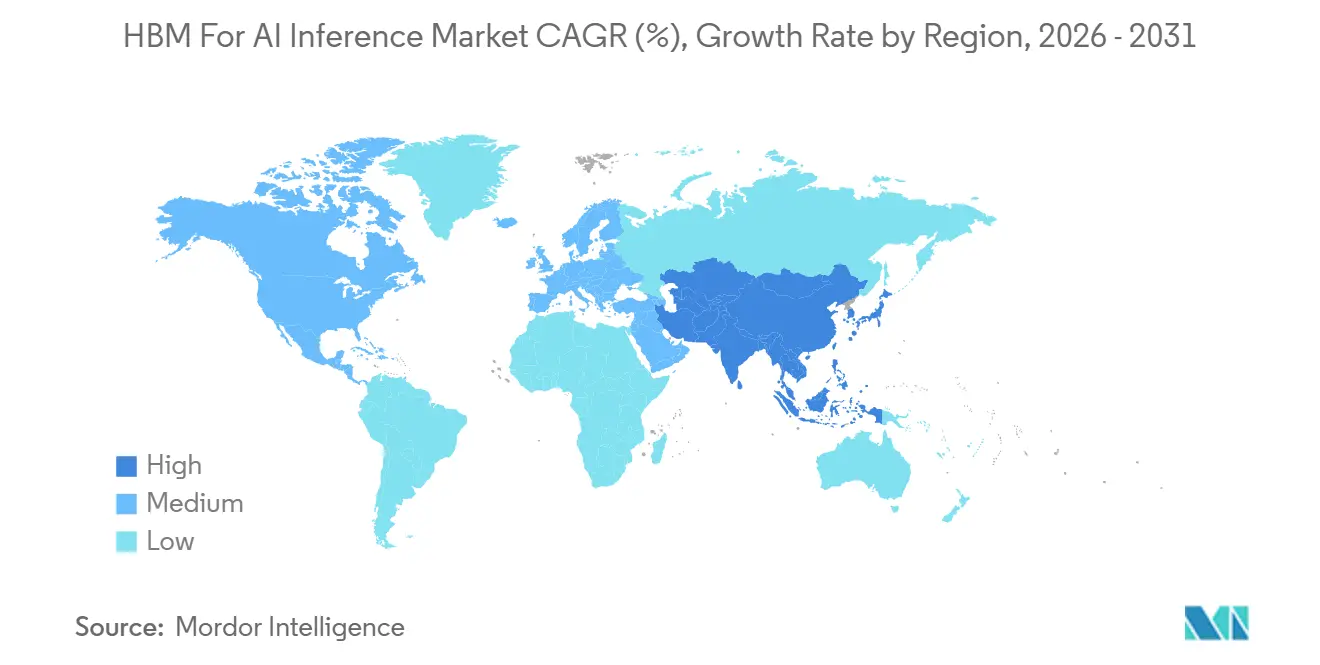

- By geography, North America accounted for 49.93% of the AI inference market in 2025, while Asia-Pacific is projected to grow at a 34.64% CAGR through 2031 in HBM for AI Inference Market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM For AI Inference Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative AI Workload Density Raising HBM Per-Accelerator Content | +7.5% | Global, concentrated in North America and APAC | Short term (≤ 2 years) |

| Memory-Bound Inference From Long-Context Models | +6.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Cloud and Hyperscaler AI Cluster Expansion | +6.2% | North America dominant, APAC gaining | Medium term (2-4 years) |

| Edge Inference Demand for Lower Latency and Higher Energy Efficiency | +3.9% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Advanced Packaging Progress Enabling Higher Stack Counts | +3.2% | APAC core, Taiwan and South Korea, spill-over to North America | Long term (≥ 4 years) |

| Inference-First Custom Silicon Adoption by Hyperscalers | +2.8% | North America and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generative AI Workload Density Raising HBM Per-Accelerator Content

Each new accelerator cycle delivers greater memory capacity and bandwidth, turning product upgrades into direct expansion for the HBM AI inference market. NVIDIA stated that the Blackwell B200 features 192 GB of HBM3e and delivers 8.0 TB/s of memory bandwidth per GPU, which materially increases memory capacity per device versus the prior generation. NVIDIA also outlined the Vera Rubin platform, which is built around a much larger HBM bandwidth envelope, showing that the next performance step is being built around memory movement as much as compute density. Micron said HBM4 is designed to improve both throughput and power efficiency for agentic AI inference, which strengthens the case for higher HBM content even when accelerator unit growth is uneven. Samsung began commercial HBM4 shipments in 2026 and positioned the product around higher performance and better thermal behavior, reinforcing that memory stack value is rising with every platform change. This pattern matters because the HBM for AI inference market can keep expanding even when accelerator shipments do not rise at the same pace, as more revenue is being captured in every qualified package.

Memory-Bound Inference From Long-Context Models

The HBM for AI inference market is also being lifted by the simple fact that long-context inference reads memory far more aggressively than earlier model deployments. Micron described agentic AI inference as highly sensitive to memory traffic and showed that concurrency and KV-cache pressure can sharply extend response time when memory access becomes the bottleneck.[1]Micron Technology, “HBM4 Product Page,” Micron Technology, micron.com As context windows grow, the memory requirement scales with active sequence handling and not only with model size, which keeps pushing buyers toward higher-bandwidth memory tiers. Micron’s HBM4 specification targets greater than 2.8 TB/s per stack and more than 20% better power efficiency than HBM3e, which directly supports lower cost per token at scale. In practical deployment terms, memory bandwidth now influences inference quality of service, cluster utilization, and energy use simultaneously. That is why the HBM for AI inference market is increasingly tied to model architecture and serving behavior, rather than just headline accelerator launches.

Cloud and Hyperscaler AI Cluster Expansion

Cloud infrastructure remains the primary deployment route for the HBM in the AI inference market because the largest inference fleets are still being built within hyperscaler environments. Microsoft introduced Maia 200 in January 2026, featuring 216 GB of HBM3e and 7 TB/s of memory bandwidth for inference use within its own data center footprint. AWS positioned Trainium3 with 144 GB of HBM3e and 4.9 TB/s of bandwidth, showing that internal accelerator programs are now scaling memory capability as a first-order design feature. Google documented the TPU Ironwood with 192 GB of HBM and 7.37 TB/s of bandwidth, confirming that HBM demand is broadening beyond a single accelerator vendor and into several large internal silicon stacks. These deployments matter because they create durable, multi-year procurement channels for advanced memory across multiple cloud operators simultaneously. As a result, the HBM for AI inference market is becoming less dependent on a single GPU roadmap and more exposed to the wider buildout of cloud inference capacity.

Edge Inference Demand for Lower Latency and Higher Energy Efficiency

Edge demand is still smaller than cloud demand, but it is becoming a meaningful expansion layer for the HBM for the AI inference market as more inference shifts closer to devices and local systems. The fastest growth in the compute mix is driven by NPU-based inference, reflecting demand for lower latency, tighter power budgets, and more local processing in AI PCs, embedded systems, and device-side use cases. That shift matters because local inference is more sensitive to energy efficiency than training-oriented server design. Micron stated that HBM4 is designed to deliver more than 20% better power efficiency than HBM3e, strengthening the case for advanced memory in performance-constrained deployments. Meta also showed that its inference-focused custom silicon roadmap is increasing memory bandwidth to support generative AI experiences at scale, aligning with the broader direction toward memory-centric optimization. Over time, this broadens the HBM for AI inference market from a pure data center story into one that also reflects where inference is executed and how tightly power and latency are managed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Package-Level Thermal and Yield Constraints | -3.9% | Global, acutely felt in South Korea and Taiwan | Short term (≤ 2 years) |

| Limited Qualified Supply Base for Advanced HBM | -3.3% | Global, with supply bottleneck in South Korea and Japan | Medium term (2-4 years) |

| Heavy Dependence on Advanced Packaging Capacity | -2.6% | APAC core, Taiwan, spill-over to North America | Medium term (2-4 years) |

| Export Controls and Supply Chain Localization Friction | -2.1% | China, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Package-Level Thermal and Yield Constraints

Thermal management and stack yield remain immediate limits on how quickly the HBM for AI inference market can convert demand into shipped revenue. Siemens noted that HBM4 increases both interface density and package complexity, making thermal behavior a first-order design issue before production begins. Higher layer counts increase heat concentration within the stack, which raises the burden on bonding quality, package design, and system cooling. Samsung’s 2026 HBM4 launch emphasized thermal resistance improvements, which shows that suppliers are treating heat and stability as core commercial requirements rather than secondary optimizations.[2]Samsung, “Samsung Ships Industry-First Commercial HBM4 with Ultimate Performance for AI Computing,” Samsung Global Newsroom, samsung.com When those factors slow qualification or reduce usable output, effective supply grows more slowly than announced capacity. This restraint does not weaken demand for the HBM for AI inference market, but it does cap how fast qualified supply can reach large inference programs.

Limited Qualified Supply Base for Advanced HBM

The HBM for AI inference market is constrained by the fact that advanced supply remains concentrated in a very small group of qualified memory vendors. NVIDIA and SK hynix announced a multiyear technology partnership in June 2026 to co-develop memory across a broad future product roadmap, which underlines how strategic supplier access has become. Samsung also said it had begun mass production and commercial shipment of HBM4 in 2026, reinforcing that only a few suppliers are in a position to serve the highest-end demand tiers. Micron’s HBM4 roadmap and product positioning show the same pattern, where qualification, power efficiency, and bandwidth targets define supplier relevance more than raw wafer expansion alone. Because so few vendors can qualify at the top performance tiers, procurement risk stays high for cloud operators, accelerator OEMs, and custom silicon programs. That narrow supply base keeps pricing power elevated and makes allocation strategy a central commercial issue across the HBM for AI inference market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Generation: HBM4 Transition Reshapes the Memory Hierarchy

HBM3 held 58.31% share in 2025, while HBM4 is projected to expand at a 34.58% CAGR through 2031. That split shows a market still anchored in current deployment volume, but already moving toward a new standard for inference performance. HBM3 remained dominant because Hopper, H200, and early Blackwell systems accounted for the largest share of deployed accelerator demand in 2025. HBM3e served as the bridge generation, helping suppliers and customers raise bandwidth without waiting for full HBM4 qualification at scale. HBM2E remained in a smaller legacy role, primarily tied to older accelerator installations that still support active inference workloads.

The next phase is being shaped by commercial readiness rather than by specification alone. Samsung said its HBM4 product delivers 11.7 Gbps per pin and 3.3 TB/s per stack with improved power efficiency and thermal resistance. Micron positioned HBM4 at more than 2.8 TB/s per stack and with more than 20% better power efficiency than HBM3e, keeping the generation shift centered on inference economics.[3]Micron Technology, “HBM4 Product Page,” Micron Technology, micron.com As suppliers move into HBM4E sampling and qualification, the HBM for AI inference market is likely to see faster turnover between memory generations than earlier accelerator cycles. That faster cadence will reward suppliers that can scale output and validate performance quickly, because customers are increasingly aligning memory selection with token throughput, power draw, and package density rather than with backward compatibility alone.

By Compute Platform: GPU Dominance Masks an NPU Acceleration Curve

GPU accounted for 82.74% of demand in 2025, while NPU is projected to expand at a 34.73% CAGR through 2031. The starting point still reflects the reality that frontier inference workloads are concentrated in GPU-rich cloud clusters. GPU dominance also reflects the installed software ecosystem, which continues to favor mature accelerator stacks for large model serving. CPU and FPGA platforms remain relevant for narrower latency-sensitive or low-batch tasks, but they do not define the volume center of current demand. The main change is that specialized inference hardware is now growing faster than general-purpose accelerator deployment.

That change is visible in both design choices and procurement models across the HBM for the AI inference market. AWS built Trainium3 around HBM3e and positioned it for generative AI inference rather than for broad training parity, which shows how memory behavior is guiding custom silicon design. Google documented TPU Ironwood with 192 GB of HBM, underscoring that purpose-built inference platforms still converge on advanced memory integration. NVIDIA’s roadmap is also moving toward more inference-oriented capabilities, which narrows the practical gap between GPU-centric and NPU-like design priorities. In that context, the HBM for AI inference industry is shifting from a single dominant compute pattern toward a broader accelerator mix, even though GPUs are likely to remain the largest platform through the forecast period.

By Deployment: Cloud Concentration Evolves as On-Premises Broadens

Cloud held 88.19% share in 2025 and remains the largest deployment mode across the HBM for the AI inference market. That position reflects the scale economics of centralized inference serving, where hyperscalers can spread hardware cost across large customer bases and fast-rising model traffic. It also reflects the concentration of advanced accelerator procurement inside a limited number of very large operators. On-premises deployment remains smaller, but it is still important in regulated, security-sensitive, and latency-bound environments. As enterprises move beyond pilots, on-premises demand is rising in absolute terms even though cloud still dominates the total mix.

Cloud based deployment is projected to expand at a 34.16% CAGR through 2031. The internal structure of cloud demand is changing in ways that matter for supplier strategy. Microsoft deployed Maia 200 for its own inference workloads, showing that part of cloud demand is now sourced through operator-designed silicon rather than merchant GPUs alone. That shift does not weaken cloud concentration, but it does redistribute bargaining power within the HBM for AI inference market toward hyperscalers that control both deployment and chip architecture. At the same time, data sovereignty rules and sector-specific compliance requirements continue to provide a floor for non-cloud installations in public-sector, financial, and healthcare environments. This means the long-term deployment picture is not a simple winner-take-all outcome, but a cloud-led structure with durable expansion space for controlled local inference infrastructure.

By End User: Enterprise Broadening Accelerates Beyond CSP Concentration

Cloud service providers accounted for 78.26% of the market in 2025, while enterprises are projected to expand at a 34.76% CAGR through 2031. That balance shows that hyperscalers remain the core buying group today, but it also points to a broader demand base over time. Cloud operators remain the primary owners of large-scale inference hardware because they run the largest general-purpose serving environments. Government demand is also expanding as sovereign AI programs move from planning to physical infrastructure commitments. Device OEMs remain early in the cycle, yet they could become more important as local inference becomes more capable.

The enterprise ramp matters because production deployment uses far more infrastructure than pilot testing. Once organizations move from trial workloads into embedded document processing, internal copilots, and sector-specific model serving, they need more concurrency, more memory, and more reliable latency behavior. Meta’s MTIA 450 roadmap doubled HBM bandwidth from the prior generation to support generative AI inference, underscoring how memory expansion is becoming central across different deployment models. That same logic also supports the enterprise side of the HBM for AI inference market, where inference cost and responsiveness become operational issues rather than experimental concerns. Over the forecast period, enterprise demand will not overtake cloud service providers in share, but it will help make end-user demand less concentrated than it was in the earlier training-led cycle.

By Package Integration: 2.5D Dominance Stable, Chiplets Drive the Next Inflection

2.5D packaging held 92.49% share in 2025, while chiplet-based integration is projected to grow at a 34.29% CAGR through 2031. The current dominance of 2.5D reflects the established use of interposer-based integration for pairing logic dies with HBM stacks in advanced AI accelerators. This model fits the present needs of high-bandwidth inference systems because it balances performance, packaging maturity, and manufacturability better than most alternatives. 3D packaging remains smaller because it increases integration complexity and still serves a narrower market segment. Even so, the next wave of scaling is already exposing the limits of current package geometry.

The growth outlook for chiplet-based integration stems from physical limits and the need to support more complex memory arrangements within HBM for the AI inference market. Samsung’s public HBM4 direction and NVIDIA’s broader roadmap both point toward denser package-level coupling between compute and memory. Siemens also highlighted that next-generation HBM design requires deeper thermal and package co-optimization, which favors more modular and scalable integration approaches over time. As stack counts increase, chiplet-based approaches are likely to gain importance because they offer a more flexible path for routing, thermal management, and die partitioning. The practical result is that packaging will remain a major differentiator in how quickly suppliers and customers can scale advanced memory into commercial inference systems.

Geography Analysis

North America held 49.93% of the global total in 2025 and remained the largest regional demand center in the HBM for AI inference market. The region benefits from the concentration of hyperscalers, internal silicon programs, and commercial model-serving infrastructure. Microsoft launched Maia 200 for inference in its U.S. data center footprint, which shows how regional demand is being reinforced by operator-owned accelerator stacks. North America also remains the main center for the commercial deployment of frontier AI services, which sustains high pull-through for advanced memory. Even with that demand strength, the region still depends heavily on Asian supply chains for qualified HBM output and advanced packaging.

Asia-Pacific is projected to grow at a 34.64% CAGR through 2031 and is the main production base for the HBM for AI inference market. South Korea remains central because Samsung and SK Hynix are core suppliers across the top performance tiers. Samsung’s HBM4 commercialization in 2026 confirms the region’s role in advancing next-generation memory from the roadmap to volume shipments. Japan is also strengthening its position through Micron’s Hiroshima expansion plans, which support a broader manufacturing footprint for advanced HBM.[4]Micron Technology, “HBM4 Product Page,” Micron Technology, micron.com Taiwan remains indispensable through advanced packaging and system integration, even when memory wafers are produced elsewhere. As AI infrastructure investment rises across Japan, India, South Korea, and Taiwan, the Asia-Pacific region is strengthening both the supply and demand sides of the HBM for AI inference market.

Europe, South America, and the Middle East and Africa together represent a smaller share, but their role is gradually improving. In Europe, data sovereignty priorities and public-sector AI programs are supporting local interest in controlled-inference capacity. South America is still limited in scale, yet cloud adoption and selective data center investment are creating a steadier base for future HBM demand. The Middle East and Africa are earlier in the buildout cycle, but national AI programs and early data center projects are beginning to translate into demand for HBM-equipped systems. Across these regions, the near-term role is not to rival North America or Asia-Pacific in scale, but to expand the geographic reach of the HBM for AI inference market and reduce its dependence on a small set of mature deployment centers.

Competitive Landscape

The HBM for AI inference market remains highly concentrated at the supply tier, with SK hynix, Samsung Electronics, and Micron Technology controlling the qualified memory base for advanced AI accelerators. That structure gives memory vendors unusual leverage because buyers cannot easily switch suppliers without risking qualification delays and deployment slippage. The market is also unusual because competition is occurring across product readiness, thermal performance, supply access, and packaging compatibility simultaneously. This means leadership is not decided by capacity claims alone, but by the ability to deliver validated stacks into major accelerator programs. In practical terms, the competitive field is narrow, capital-intensive, and closely tied to long-term customer partnerships.

SK hynix has strengthened its position by deepening roadmap alignment with NVIDIA, which formalized a multiyear technology partnership in June 2026. Samsung is competing through volume recovery and faster commercialization, as shown by its industry-first commercial HBM4 shipment and continued push on next-generation stack performance. Micron is using power-efficiency positioning and a clear product roadmap to reinforce its role in the top tier of supply. On the demand side, Microsoft, AWS, and Google are shifting competitive power by designing their own inference silicon and specifying large HBM footprints directly. These moves are making the HBM for AI inference market more multipolar at the chip design layer, even as supply remains tight at the memory layer.

There is still room for differentiation beyond the top three memory vendors, but most of it lies in architecture and integration rather than in direct HBM manufacturing. SambaNova presented the SN50 RDU with a three-tier memory structure that combines HBM, large-capacity memory, and fast SRAM, demonstrating that inference platform vendors are optimizing across the memory hierarchy rather than simply asking for larger stacks. Academic research is also exploring memory classes that could complement HBM in inference clusters, including managed-retention concepts that trade write performance for read-oriented efficiency. Even so, alternatives are not yet displacing HBM at the top end of inference deployment, because bandwidth, maturity, and ecosystem alignment still favor the current stack-based model. The overall competitive picture, therefore, stays concentrated, but it is evolving toward closer coordination between memory producers, cloud operators, and custom silicon designers.

HBM For AI Inference Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK hynix announced a multiyear technology partnership on June 7, 2026, covering co-development of next-generation memory for NVIDIA's full product roadmap, including Vera Rubin AI supercomputers, Vera CPUs, RTX Spark personal AI computers, and Jetson Thor robotics platforms, extending a component supply relationship into a cross-product joint architecture program spanning AI infrastructure, personal AI, and physical AI.

- May 2026: Meta disclosed MTIA 450, an inference-optimized custom AI chip scheduled for mass deployment in early 2027, which doubled HBM bandwidth compared to MTIA 400 to address generative AI inference performance requirements, reflecting broad custom silicon convergence on memory bandwidth as the primary inference optimization target.

- February 2026: Samsung Electronics began mass production and commercial shipment of HBM4, delivering 11.7 Gbps per pin and 3.3 TB/s per-stack bandwidth, approximately 2.7x that of HBM3e, with 40% better power efficiency and 10% enhanced thermal resistance, marking the industry's first commercial HBM4 product.

- January 2026: Microsoft unveiled Maia 200, an AI inference accelerator built on TSMC's 3nm process with 216 GB of HBM3e at 7 TB/s and over 10 petaFLOPS of FP4 performance, initially deployed at the US Central datacenter in Des Moines, Iowa, to serve GPT-5.2, Microsoft Foundry, and Microsoft 365 Copilot inference workloads.

Global HBM For AI Inference Market Report Scope

The HBM for AI Inference Market Report is segmented by HBM Generation (HBM2E, HBM3, HBM3E, and HBM4), Compute Platform (GPU, CPU, NPU, and FPGA), Deployment (Cloud and on-Premises), End User (Cloud Service Providers, Enterprises, Government and Public Sector, Other End Users), Package Integration (2.5D Packaging, 3D Packaging, and Fan-Out Packaging), and Geography, North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| GPU |

| CPU |

| NPU |

| FPGA |

| Other Compute Platforms |

| Cloud |

| On-Premises |

| Cloud Service Providers |

| Enterprises |

| Government and Public Sector |

| Other End Users |

| 2.5D Packaging |

| 3D Packaging |

| Fan-Out Packaging |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By HBM Generation | HBM2E | |

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| By Compute Platform | GPU | |

| CPU | ||

| NPU | ||

| FPGA | ||

| Other Compute Platforms | ||

| By Deployment | Cloud | |

| On-Premises | ||

| By End User | Cloud Service Providers | |

| Enterprises | ||

| Government and Public Sector | ||

| Other End Users | ||

| By Package Integration | 2.5D Packaging | |

| 3D Packaging | ||

| Fan-Out Packaging | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and future value of the HBM for AI inference market?

The HBM for AI inference market was valued at USD 0.82 billion in 2025 and is forecast to reach USD 5.1 billion by 2031 at a 33.78% CAGR.

Which HBM generation leads today and which one is growing fastest?

HBM3 led with 58.31% share in 2025, while HBM4 is expected to post the fastest growth at a 34.58% CAGR through 2031.

Why is memory bandwidth becoming so important for AI inference?

Longer-context and higher-concurrency inference workloads depend heavily on moving model weights and cache data quickly, which makes HBM bandwidth a direct performance driver.

Which compute platform dominates demand for HBM in inference workloads?

GPUs held 82.74% share in 2025 because large-scale inference still runs mainly in GPU-dense cloud environments, though NPUs are growing faster at 34.73% CAGR.

Which region is leading demand and which region is growing fastest?

North America led with 49.93% share in 2025, while Asia-Pacific is projected to record the fastest expansion at a 34.64% CAGR through 2031.

What is the main risk to supply growth over the next few years?

The main risk is not demand weakness, but the combination of stack yield limits, thermal complexity, and a very small qualified supplier base for advanced HBM products.

Page last updated on: