HBM CoWoS Packaging Capacity and Supply-Demand Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

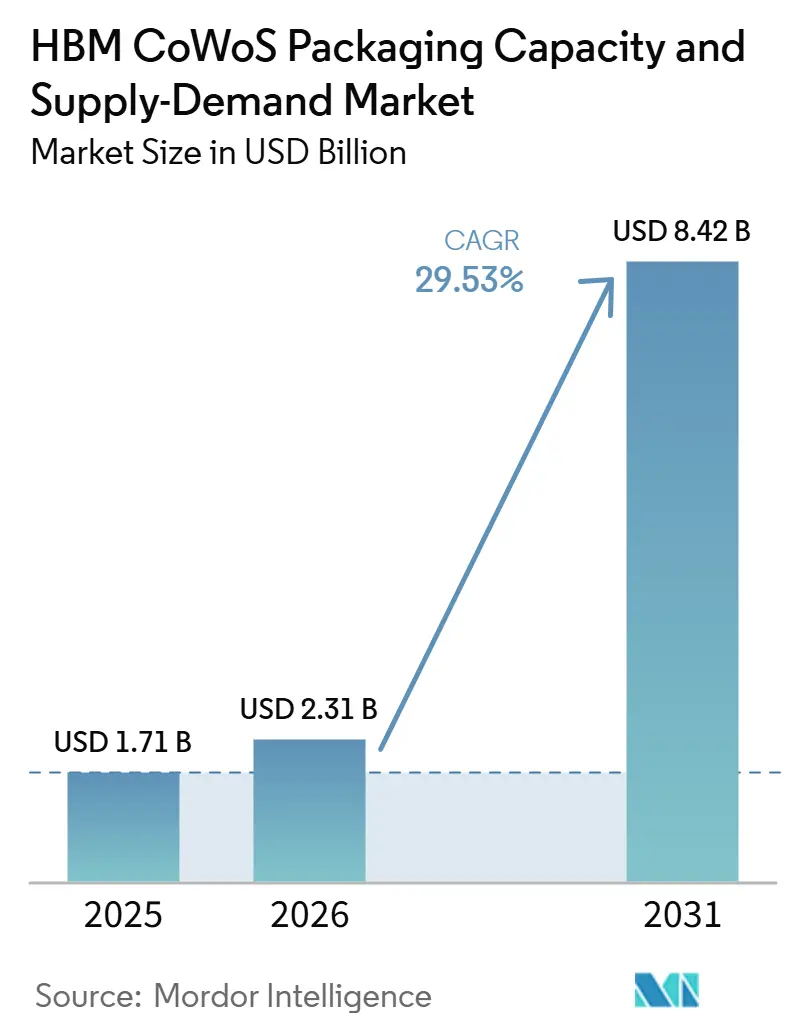

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 8.42 Billion |

| Growth Rate (2026 - 2031) | 29.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

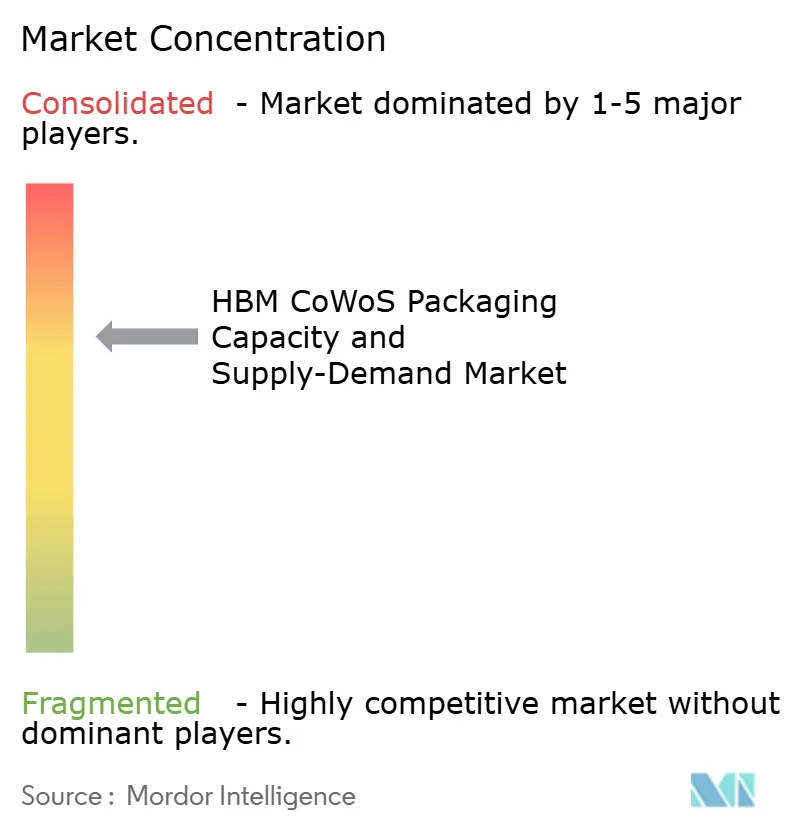

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM CoWoS Packaging Capacity and Supply-Demand Market Analysis by Mordor Intelligence

The HBM CoWoS packaging capacity and supply-demand market size is expected to increase from USD 1.71 billion in 2025 to USD 2.31 billion in 2026 and reach USD 8.42 billion by 2031, growing at a CAGR of 29.53% over 2026-2031. The HBM CoWoS packaging market is being shaped by a persistent mismatch between demand for AI packaging and the pace at which qualified CoWoS capacity can be added across the supply chain. That imbalance is keeping allocation tight, extending booking cycles, and giving the small group of qualified packaging providers stronger control over pricing, customer selection, and production scheduling. The HBM CoWoS packaging capacity and supply-demand market is also changing because larger AI processors are using more package area and higher memory density, which raises packaging demand faster than chip shipment growth alone would suggest. North America is becoming a stronger expansion zone because government-backed investment is supporting local packaging, testing, and HBM-related capacity, even though Asia-Pacific remains the center of current output. The HBM CoWoS packaging capacity and supply-demand market still faces execution risk from long equipment lead times, strict customer qualification cycles, and trade controls that can delay how quickly new capacity turns into usable supply.

Key Report Takeaways

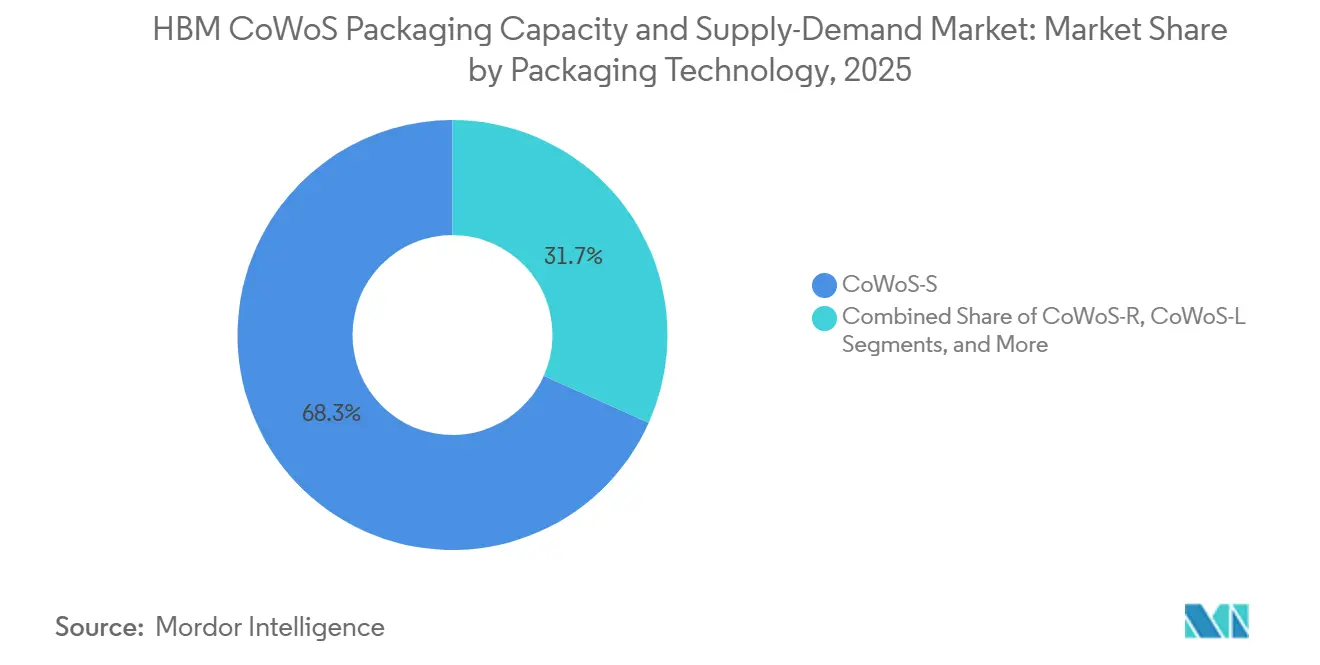

- By packaging technology, CoWoS-S held 68.31% share in 2025, while CoWoS-L is projected to expand at a 30.33% CAGR through 2031 in the HBM CoWoS packaging capacity and supply-demand market.

- By HBM generation, HBM3E accounted for 55.73% share in 2025, while HBM4 is projected to advance at a 30.42% CAGR through 2031.

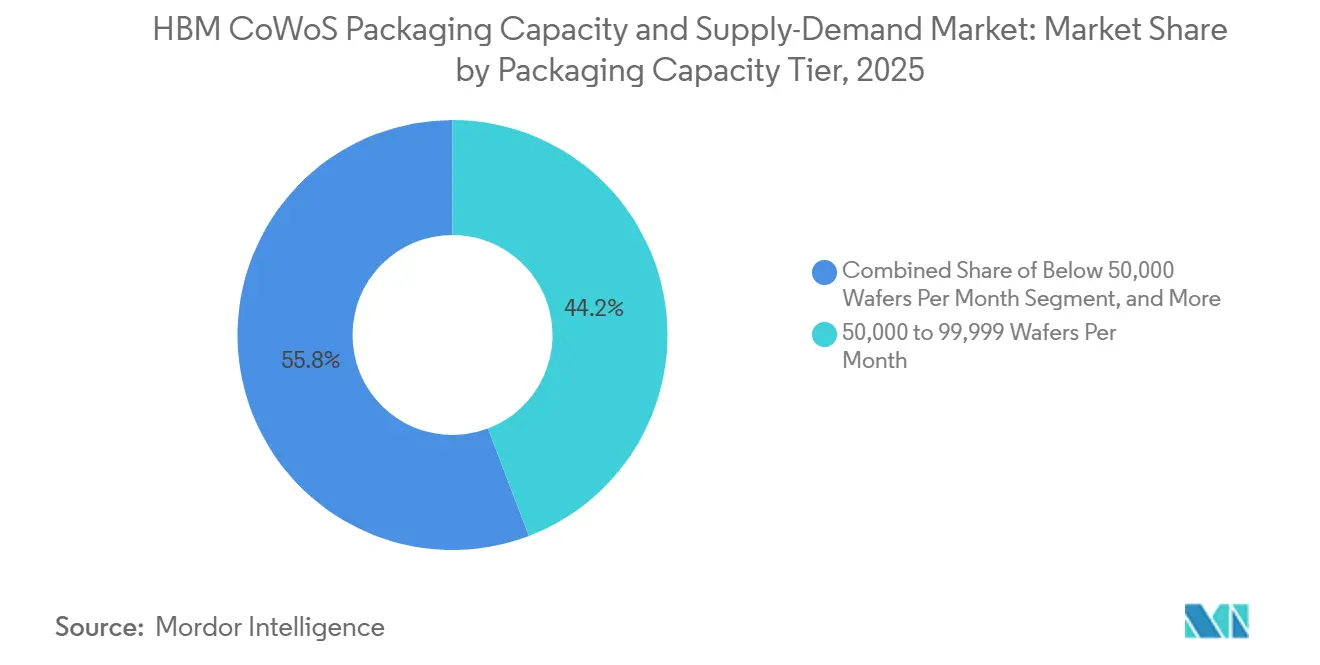

- By packaging capacity tier, the 50,000 to 99,999 wafers per month segment accounted for 44.22% share in 2025, while the 150,000 wafers per month and above tier is projected to expand at a 30.26% CAGR through 2031in the HBM CoWoS packaging capacity and supply-demand market.

- By end user, GPU and AI chip vendors held 59.03% share in 2025, while hyperscalers and cloud providers are projected to expand at a 30.71% CAGR through 2031.

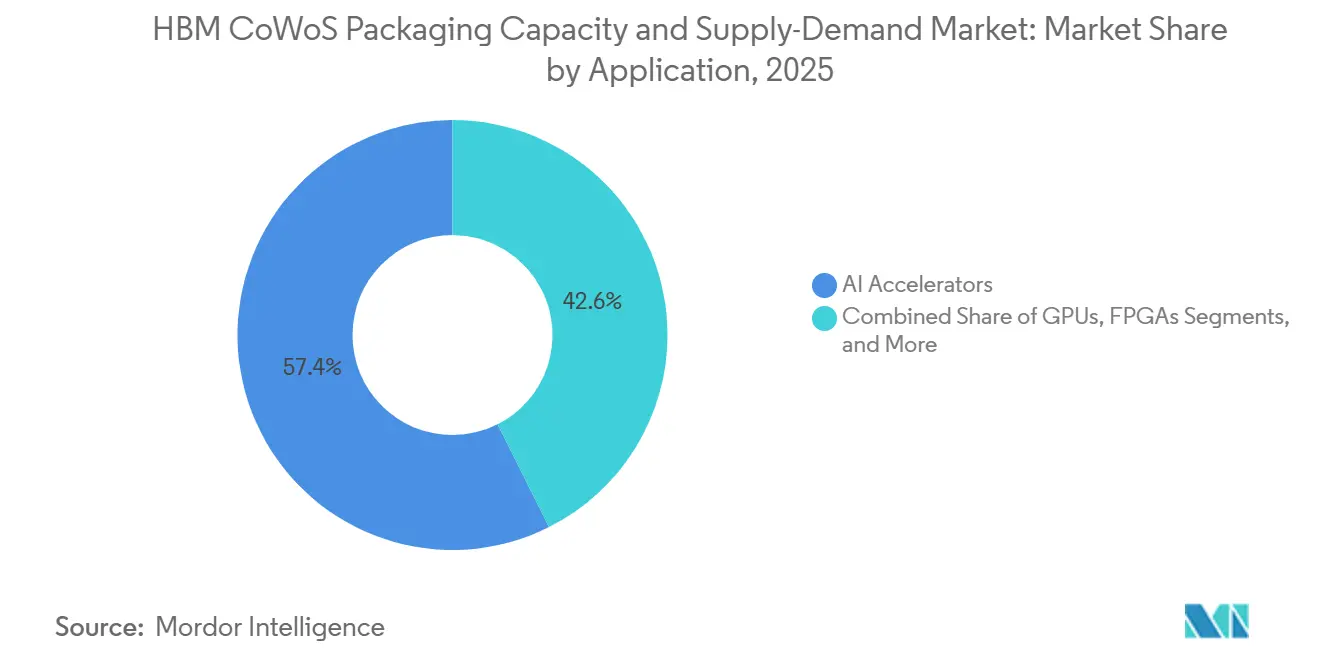

- By application, AI accelerators accounted for 57.41% share in 2025, while networking and data center processors are projected to advance at a 30.68% CAGR through 2031in the HBM CoWoS packaging capacity and supply-demand market.

- By geography, Asia-Pacific held 79.84% of the HBM CoWoS packaging capacity and supply-demand market share in 2025, while North America is projected to expand at a 30.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM CoWoS Packaging Capacity and Supply-Demand Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Accelerator Demand Outpacing Advanced Packaging Capacity | +8.5% | Global, Asia-Pacific core including Taiwan, South Korea, and Japan, and North America | Short term (≤ 2 years) |

| HBM4 Adoption Increasing Interposer Complexity and Wafer Demand | +6.2% | Global, with Taiwan in packaging and South Korea in memory | Medium term (2-4 years) |

| Hyperscaler Co-Design and Long-Term Capacity Reservation Behavior | +4.8% | North America and Asia-Pacific core, with spillover to Europe | Short term (≤ 2 years) |

| Government Incentives for Memory and Advanced Packaging Expansion | +3.5% | North America, with early gains in South Korea and Japan | Medium term (2-4 years) |

| Multi-Sourcing of Packaging and Memory Across Regions | +2.8% | Global, with Asia-Pacific core and spillover to North America and Middle East and Africa | Medium term (2-4 years) |

| CoWoS-L Migration Raising Packaged Bit Output per Wafer | +2.1% | Global, centered on Taiwan advanced packaging lines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Accelerator Demand Outpacing Advanced Packaging Capacity

The HBM CoWoS packaging capacity and supply-demand market is still being defined by the gap between AI system demand and the amount of qualified CoWoS output available to serve it. IEEE reported that TSMC expanded CoWoS capacity by 106% in 2025, yet the supply chain remained tight because those additions were absorbed quickly by customer demand.[1]IEEE Heterogeneous Integration Roadmap, “Supply Chain Chapter 18,” IEEE Electronics Packaging Society, ieee.org TSMC also stated at its 2026 annual shareholder meeting that CoWoS capacity was fully booked through the end of 2026, which shows that spot availability remained limited even after large expansion efforts. This matters because the bottleneck is not limited to wafer count alone, since each new accelerator generation tends to use larger packages and more HBM content within each device. That pattern means packaging demand rises through both shipment growth and package complexity, so the HBM CoWoS packaging capacity and supply-demand market keeps tightening even while nominal capacity grows. The result is a market where customers with early commitments secure supply, while later entrants face longer lead times, delayed launches, and less flexibility in product timing.

HBM4 Adoption Increasing Interposer Complexity and Wafer Demand

The move toward newer HBM generations is raising the technical burden placed on interposers, memory interfaces, and thermal control across the HBM CoWoS packaging capacity and supply-demand market. SK hynix introduced its iHBM thermal solution in May 2026, embedding cooling elements directly within the package structure to reduce thermal resistance by 30%, which highlights how memory scaling is now pushing packaging design into a more demanding role.[2]SK hynix, “SK Hynix Unveils iHBM Thermal Solution to Boost AI Performance,” SK hynix Newsroom, skhynix.com The same direction is visible in customer qualification work around HBM4E, where suppliers are focusing on heat removal, stack reliability, and advanced package integration rather than simple memory density gains. As the memory subsystem becomes larger and hotter, the interposer and surrounding package have to handle more routing density and stricter electrical conditions across the same footprint. That raises wafer demand in practical terms because more complex packages take longer to qualify, place more pressure on known good yield, and slow how quickly new output becomes usable in production. The HBM CoWoS packaging capacity and supply-demand market therefore benefits from the value uplift tied to HBM4 migration, even though that same transition adds engineering friction and keeps supply tight for longer.

Hyperscaler Co-Design and Long-Term Capacity Reservation Behavior

Large cloud companies are changing how the HBM CoWoS packaging capacity and supply-demand market operates because they now engage packaging supply earlier and more directly than in prior compute cycles. TSMC confirmed in 2026 that its advanced packaging capacity was fully booked through year-end, which reflects the strength of long-duration reservations rather than short-term spot demand.[3]Taiwan Semiconductor Manufacturing Company, “2026 Annual General Meeting and Shareholder Communications,” TSMC, tsmc.com This behavior gives the largest buyers a stronger influence over allocation because they can secure packaging windows long before smaller chip developers finalize production plans. It also changes product planning, since packaging architecture now has to be locked earlier in the design cycle when customers want guaranteed access to qualified lines. That shift favors hyperscalers that can coordinate silicon design, HBM sourcing, and foundry relationships across several years instead of a single launch cycle. The HBM CoWoS packaging capacity and supply-demand market is therefore becoming more structured around committed demand, which improves visibility for top suppliers but makes access less flexible for smaller fabless companies.

Government Incentives for Memory and Advanced Packaging Expansion

Public incentives are becoming an important support for the HBM CoWoS packaging capacity and supply-demand market because new advanced packaging capacity requires high capital intensity and long payback periods. In January 2025, the US Department of Commerce finalized USD 1.4 billion in NAPMP awards, including USD 1.1 billion for Natcast piloting facilities and USD 300 million for substrate and materials research efforts. In December 2024, SK hynix received up to USD 458 million in direct funding and up to USD 500 million in loans to support its USD 3.87 billion Indiana investment tied to HBM memory packaging and advanced packaging research. In the same month, Amkor Technology received up to USD 407 million to build an advanced packaging and test facility in Arizona, strengthening domestic packaging capability for AI chip supply chains. These moves do not remove the current bottleneck immediately, but they improve the medium-term pipeline of qualified sites, local materials work, and customer confidence in non-Taiwan packaging options. The HBM CoWoS packaging market gains from this because government support is helping create the regional infrastructure that private capital alone was slower to fund before the current AI cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TSMC CoWoS Capacity Remains the Binding Constraint | -3.5% | Global, centered on Taiwan and Asia-Pacific core | Short term (≤ 2 years) |

| TSV Yield Losses Rise at Higher Stack Heights | -2.1% | Global, with South Korea in memory and Taiwan in packaging | Medium term (2-4 years) |

| Thermal Density Limits at Higher Bandwidth and Stack Count | -1.5% | Global | Long term (≥ 4 years) |

| Export Controls and Qualification Delays Slow China-Led Demand Conversion | -1.2% | China, with spillover to North America and Asia-Pacific qualification hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

TSMC CoWoS Capacity Remains the Binding Constraint

The largest near-term limit on the HBM CoWoS packaging capacity and supply-demand market is that the highest-value packaging flows still depend heavily on one supplier and a narrow set of qualified lines. IEEE noted that TSMC was outsourcing an estimated 240,000 to 270,000 wafers annually to OSAT partners in 2026, with most of that overflow directed to Amkor and Siliconware Precision Industries for less complex CoWoS flows. That arrangement helps relieve pressure, but it does not fully solve the shortage for the most advanced package types that need the deepest process experience and the highest qualification confidence. The HBM CoWoS packaging capacity and supply-demand market remains constrained because every new line also needs tools, process tuning, customer certification, and stable yield before it contributes meaningfully to supply. Equipment lead times and qualification cycles stretch this process over many quarters, so announced capacity does not convert into practical output as quickly as demand is rising. This keeps the market concentrated, preserves strong supplier leverage, and delays the point at which supply conditions move from allocation-driven to more balanced.

TSV Yield Losses Rise at Higher Stack Heights

Yield pressure at higher stack heights is another real restraint on the HBM CoWoS packaging capacity and supply-demand market because memory scaling is placing more stress on package reliability and thermal stability. SK hynix highlighted the need for direct package-level cooling through its iHBM approach in 2026, showing that thermal and physical limits are becoming central design issues rather than secondary packaging considerations. As HBM stacks become taller and hotter, even small defects or warpage issues can undermine final package quality and reduce usable output. This matters for the entire assembly chain because lower memory stack yield can delay package integration, increase qualification time, and reduce confidence in large-scale customer ramps. The HBM CoWoS packaging capacity and supply-demand market therefore faces a technical brake that sits inside the memory-package interface rather than only at the foundry or OSAT capacity level. Until suppliers show repeatable high-yield performance on more demanding stack configurations, part of the forecast expansion will continue to be moderated by reliability and ramp discipline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Technology: CoWoS-S Dominance Gives Way to CoWoS-L At Scale

CoWoS-S accounted for 68.31% of the packaging technology segment in 2025, which shows how strongly the HBM CoWoS packaging capacity and supply-demand market still relied on a proven silicon interposer format during the base year. Its leadership came from long qualification history, wide deployment in AI training systems, and a familiar production flow for customers that needed high bandwidth without redesigning the entire package concept. CoWoS-S also benefited from the fact that many active programs were already locked to established interposer geometries, which supported continuity in procurement and output. In practical terms, it remained the workhorse format while the HBM CoWoS packaging capacity and supply-demand industry prepared for a more demanding package mix over the forecast period. That position was important because customers preferred lower execution risk while the broader AI hardware cycle was already facing allocation pressure and long booking windows.

The growth direction is now shifting toward CoWoS-L, which is forecast to expand at a 30.33% CAGR through 2031 and become the main scale platform for larger accelerators in the HBM CoWoS packaging capacity and supply-demand market. Its appeal is tied to physical scalability, since larger package footprints and heavier HBM content place pressure on monolithic interposer approaches. This transition matters because package size is now becoming a direct competitive factor rather than only a manufacturing detail. As compute dies and memory stacks expand together, suppliers need packaging formats that can support more demanding layouts without making yield losses unacceptable at scale. CoWoS-R remains relevant for cost-sensitive designs where full silicon density is not essential, which gives the market an intermediate option between premium and lower-complexity flows. Other emerging formats remain earlier in their commercialization path, but they are already influencing design planning because customers want alternatives that could reduce future dependence on a single advanced package architecture. The HBM CoWoS packaging capacity and supply-demand market therefore is not moving away from CoWoS-S overnight, but the value mix is gradually shifting toward solutions that can support larger, hotter, and more memory-dense AI systems. That shift also raises package area demand per device, which means packaging revenue can keep climbing even when device unit growth slows. The segment shows how technology choice in the HBM CoWoS packaging capacity and supply-demand market is increasingly being set by package scale limits rather than by simple cost differences alone.

By HBM Generation: HBM4 Redefines Packaging Economics

HBM3E held 55.73% of the HBM generation segment by value in 2025, which gave it the leading revenue position in the HBM CoWoS packaging capacity and supply-demand market during the base year. That outcome reflected its broad use in active AI accelerator programs and the long qualification cycles that keep customers on a chosen memory-package configuration after deployment begins. Once an interposer, thermal path, and HBM stack arrangement are validated together, customers are usually cautious about making immediate changes. This preserved HBM3E demand into 2026 even as suppliers moved their development attention toward later generations. HBM2, HBM2E, and HBM3 therefore remained in the mix mostly through residual deployments rather than through new strategic momentum.

HBM4 is the fastest-growing sub-segment and is projected to advance at a 30.42% CAGR through 2031, which makes it a major value driver for the HBM CoWoS packaging market. The reason is not only a memory speed increase, but also the broader redesign effort it triggers across the package, thermal system, and qualification roadmap. Newer HBM generations are pushing suppliers to treat cooling, reliability, and package integration as a larger part of product differentiation, which was clear in SK hynix's 2026 iHBM thermal launch. This is why the transition to HBM4 carries larger economic implications than a normal memory upgrade, since it changes how the package is engineered and how quickly volume can be certified. The HBM CoWoS packaging capacity and supply-demand market size for next-generation memory-linked designs rises because each program requires more engineering depth, closer memory-foundry coordination, and stronger process control across assembly stages. At the same time, the installed base of HBM3E programs creates a bridge period where old and new generations overlap, which prevents a sudden demand handoff. That overlap supports revenue resilience during the transition window, even though it also adds complexity to planning and capacity reservation. The HBM CoWoS packaging capacity and supply-demand industry therefore gains from both continuity and upgrade pressure, since mature programs keep shipping while more advanced ones raise average package value. This segment shows that memory generation shifts are becoming a central pricing and allocation force across the HBM CoWoS packaging capacity and supply-demand market rather than a background technology change.

By Packaging Capacity Tier: Mid-Tier Clusters Anchor Current Output, High-Tier Drives Growth

The 50,000 to 99,999 wafers per month tier held 44.22% share in 2025, which made it the operational center of the HBM CoWoS packaging capacity and supply-demand market during the base year. This tier captured the output range where established facilities were already qualified and able to support meaningful customer programs before the latest expansion cycle fully materialized. It also reflected the practical reality that advanced packaging scale depends on process depth and customer trust, not only on factory size. Smaller capacity tiers remained relevant for overflow work and earlier-stage regional participation, but they were not yet the main engine of supply for the largest AI packages. That gave the middle tier an important stabilizing role because it connected proven output with the first wave of demand acceleration.

The fastest growth is expected in the 150,000 wafers per month and above tier, which is projected to expand at a 30.26% CAGR through 2031 as the HBM CoWoS packaging capacity and supply-demand market pushes toward larger industrial scale. IEEE pointed to TSMC expansion and OSAT participation from companies such as Amkor and Siliconware as part of the broader effort to move the supply base into higher output brackets IEEE.ORG. This higher tier matters because it represents the level of sustained volume needed to reduce allocation pressure in a meaningful way rather than just soften it temporarily. The 100,000 to 149,999 wafers per month range sits between those two positions and acts as a practical ramp corridor for sites that are still moving toward larger customer commitments. Regulatory and customer qualification requirements also shape how much of this nameplate capacity can actually serve premium programs, so not every installed line contributes equally to usable supply. The HBM CoWoS packaging capacity and supply-demand market size linked to the uppermost tier should therefore grow faster than share alone suggests, because qualified high-volume output is where customer urgency is strongest. This segment also shows why capacity is a strategic variable, since the real bottleneck is qualified throughput under customer-approved conditions rather than nominal factory capability. As long as qualification remains selective, the HBM CoWoS packaging capacity and supply-demand market will continue rewarding suppliers that can combine scale with process credibility. That is why large future capacity announcements matter most when they come with evidence of customer readiness and not only capital spending.

By End User: GPU Vendors Lead, Hyperscalers Accelerate Fastest

GPU and AI chip vendors represented 59.03% of total demand in 2025, which placed them at the center of the HBM CoWoS packaging market in the base year. Their leadership reflected direct control over package specifications, close foundry relationships, and the ability to secure allocation for large AI platforms before downstream buyers entered the queue. These companies were the first point of demand because they defined die layouts, HBM configurations, and package choices that shaped the entire supply chain. That gave them a natural advantage in a supply-constrained environment where technical qualification and reservation timing mattered as much as end demand. Their role also explains why packaging remained closely tied to merchant accelerator roadmaps during the early part of the forecast period.

Hyperscalers and cloud providers are projected to expand at a 30.71% CAGR through 2031, making them the fastest-growing end-user group in the HBM CoWoS packaging capacity and supply-demand market. Their rise comes from the shift toward custom silicon programs, where large cloud operators are moving from indirect exposure through GPU procurement to direct involvement in package planning and allocation. This is part of a wider change in which the end customer is no longer only a buyer of finished accelerators, but also a sponsor of the packaging path that makes those devices available at scale. The June 2026 long-term partnership between TSMC and Amkor in Arizona supports this direction by building a domestic framework for advanced packaging and test services for key customers. Semiconductor companies beyond merchant GPU vendors, along with networking, automotive, and aerospace participants, still represent smaller shares, but they are part of the same competition for scarce qualified output. The HBM CoWoS packaging capacity and supply-demand market share held by GPU and AI chip vendors in 2025 may look dominant, yet the faster growth of hyperscalers suggests that control over future demand will become more distributed across the design chain. This shift matters because hyperscalers can align silicon, memory, and infrastructure planning over several years, which improves their ability to secure supply. It also means supplier relationships may increasingly be built around platform partnerships rather than one-time product cycles. The HBM CoWoS packaging capacity and supply-demand market is therefore evolving from a vendor-led demand model toward a more shared structure where cloud operators influence both package decisions and long-range capacity planning.

By Application: AI Accelerators Define the Market, Networking Emerges as Next Growth Vector

AI accelerators accounted for 57.41% of application value in 2025, which made them the leading use case across the HBM CoWoS packaging capacity and supply-demand market. That result was expected because the technical strengths of CoWoS are closely aligned with large training-class devices that need high bandwidth memory and dense die-to-die integration. These products justify premium packaging because their system value is high and their memory requirements are difficult to meet with simpler assembly methods. GPUs formed the next-largest application layer, with overlap in practice because many leading AI training platforms use GPU-based architectures packaged through CoWoS. This concentration shows that the HBM CoWoS packaging capacity and supply-demand market grew first around the applications that were most willing to pay for scarce advanced package capacity.

Networking and data center processors are projected to expand at a 30.68% CAGR through 2031, which makes them the fastest-growing application in the HBM CoWoS packaging capacity and supply-demand market. SEMI noted the growing role of high-end packaging in advanced data processing and bandwidth-intensive system architectures, supporting the case for wider use beyond training accelerators alone. This growth is important because AI infrastructure is spreading pressure across the full data center fabric, not only the compute node. As inference loads, switching activity, and memory traffic rise together, networking silicon and data center processors need higher memory bandwidth and more advanced package solutions than in previous deployment cycles. That expands the addressable workload base for CoWoS and reduces the degree to which future growth depends on a single device category. High-performance computing, FPGA, and application processor programs remain smaller contributors, but they broaden the demand profile and create additional use cases for high-bandwidth package integration. The HBM CoWoS packaging capacity and supply-demand market size attached to non-training applications should therefore rise as more infrastructure functions begin to justify HBM-enabled packaging. This changes the application mix gradually rather than suddenly, since AI accelerators are likely to remain the core revenue engine through the forecast period. Even so, the segment points to a broader commercialization path where packaging growth follows the spread of memory-intensive computing across more system functions. That makes application diversification a meaningful support for the long-term resilience of the HBM CoWoS packaging capacity and supply-demand market.

Geography Analysis

Asia-Pacific held 79.84% of the HBM CoWoS packaging capacity and supply-demand market in 2025, which clearly established it as the center of present-day supply, manufacturing depth, and ecosystem coordination. This position rested on Taiwan's packaging lines, South Korea's HBM production base, and Japan's role in supplying critical substrate, chemical, and equipment inputs. The HBM CoWoS packaging capacity and supply-demand market size in Asia-Pacific remained far ahead of other regions because the full chain from memory through packaging was already concentrated there before the current AI upcycle accelerated. That concentration created a structural manufacturing advantage that competing regions are only beginning to address through policy and new investment programs.

Taiwan remained the anchor within Asia-Pacific because the highest-value CoWoS flows stayed closest to TSMC's most mature packaging infrastructure and customer relationships. South Korea also strengthened its relevance as memory packaging became more important to final system performance and not only to DRAM output. In July 2026, Samsung Electronics and SK hynix announced plans for HBM packaging fabrication facilities in South Korea's Chungcheong region as part of an industrywide KRW 392 trillion investment plan, equal to USD 252.5 billion, which reinforced the region's push into packaging scale. This matters for the HBM CoWoS packaging capacity and supply-demand market because the balance of advantage is shifting from front-end process leadership alone toward tighter coordination between memory and back-end integration. China remained a large potential demand center, but export controls and packager approval requirements continued to limit how much of that demand could translate into accessible leading-edge packaging programs. The result was that Asia-Pacific kept its dominance, but that dominance was increasingly split between Taiwan's foundry-led packaging depth and South Korea's expanding memory-linked packaging ambitions.

North America is the fastest-growing region and is projected to expand at a 30.44% CAGR through 2031 in the HBM CoWoS packaging market. The region's growth is being supported by direct public funding, strategic domestic projects, and customer preference for packaging locations closer to allied supply chains and hyperscale demand centers. The January 2025 NAPMP awards and the December 2024 CHIPS incentives for SK hynix and Amkor created a clearer domestic path for advanced packaging scale-up. The June 2026 TSMC-Amkor partnership in Arizona added a long-term operating framework that linked foundry demand with local packaging and test execution. Europe still held a modest direct packaging position in this report period, while South America and the Middle East and Africa remained small because they lacked comparable semiconductor manufacturing infrastructure.

Competitive Landscape

The HBM CoWoS packaging capacity and supply-demand market remained highly concentrated at the leading edge because only a small group of suppliers could handle the most demanding package flows with the required customer confidence. TSMC stayed in the strongest position because it controlled the most mature CoWoS ecosystem, the deepest customer qualification base, and the most strategic relationships with AI accelerator developers. This concentration was reinforced by the fact that overflow to OSAT partners helped overall supply, but did not fully replace the leader's role in the most advanced package configurations. The HBM CoWoS packaging capacity and supply-demand market therefore looked oligopolistic at the top and more fragmented at lower-complexity overflow levels.

Memory suppliers were competing just as actively, since package performance increasingly depends on how well HBM, thermal design, and system integration work together. SK hynix used product and process moves to strengthen its position, including the May 2026 iHBM announcement that reduced thermal resistance by 30% through embedded cooling elements inside the package. Samsung Electronics and SK hynix also raised the strategic value of South Korea's packaging footprint with their July 2026 plan for new HBM packaging fabrication facilities in the Chungcheong region. These steps show that competition is no longer limited to supplying memory bits, since packaging reliability, thermal control, and location strategy are now central competitive tools. The HBM CoWoS packaging capacity and supply-demand market is also giving OSAT companies more strategic relevance because they can absorb overflow work, support regional diversification, and help customers build secondary sourcing paths. Amkor's Arizona expansion and its 10-year partnership with TSMC is one of the clearest examples, since it formalized a U.S. packaging route for advanced customers even if full production is expected later.

The competitive pattern suggests that leaders are trying to secure advantage through capacity, geography, and process specialization at the same time. TSMC is defending leadership through booking control and ecosystem depth, while SK hynix is using thermal innovation and packaging-linked investment to raise its strategic value across future HBM ramps. Amkor is positioning itself as a critical overflow and domestic execution partner through Arizona capacity supported by both customer agreements and CHIPS-related funding. The HBM CoWoS packaging capacity and supply-demand market should therefore remain concentrated, with competition focused less on broad commoditized volume and more on who can deliver qualified high-complexity output under tight customer schedules.

HBM CoWoS Packaging Capacity and Supply-Demand Industry Leaders

Taiwan Semiconductor Manufacturing Company Limited

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

ASE Technology Holding Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Samsung Electronics and SK hynix announced plans to build HBM packaging fabrication facilities in South Korea's Chungcheong region as part of an industrywide KRW 392 trillion (USD 252.5 billion) investment commitment, including SK hynix's KRW 20 trillion (USD 12.9 billion) for its P&T7 advanced packaging and test facility. The investment signals a structural shift of advanced packaging capacity expansion to South Korea alongside Taiwan.

- June 2026: TSMC and Amkor Technology announced a 10-year agreement to enhance advanced semiconductor packaging capabilities in Arizona, establishing a procurement framework for CoWoS and InFO packaging and test services. The partnership, backed by Amkor's USD 7 billion Arizona campus, formalizes a domestic U.S. packaging node for TSMC's key customers, with production expected from 2028.

- May 2026: SK hynix announced the iHBM solution, which integrates cooling elements (ICEs) directly within the HBM package at the die-to-die physical layer interface, reducing thermal resistance by 30% compared with conventional HBM architectures. The company plans to adopt this approach in HBM5 and subsequent generations, creating a new packaging-level thermal management category.

- February 2026: SK hynix committed USD 15 billion to HBM3, HBM3E, and early HBM4 capacity expansion, with total committed spend across advanced packaging and fabrication plants in the US and South Korea reported to exceed USD 30 billion, including approximately USD 27 billion in fiscal 2026.

Global HBM CoWoS Packaging Capacity and Supply-Demand Market Report Scope

The Global HBM CoWoS Packaging Capacity and Supply-Demand Market refers to the industry segment focused on the production capacity, availability, and demand dynamics of High Bandwidth Memory (HBM) integrated with Chip-on-Wafer-on-Substrate (CoWoS) advanced packaging technology.

The HBM CoWoS Packaging Capacity and Supply-Demand Market Report is Segmented by Packaging Technology (CoWoS-S, CoWoS-R, CoWoS-L, and Other Packaging Technology), HBM Generation (HBM2 and HBM2E, HBM3, HBM3E, HBM4, and HBM4E and Beyond), Packaging Capacity Tier (Below 50,000 Wafers Per Month, 50,000 to 99,999 Wafers Per Month, 100,000 to 149,999 Wafers Per Month, and 150,000 Wafers Per Month and Above), End User (GPU and AI Chip Vendors, Hyperscalers / Cloud Providers, Semiconductor Companies (Fabless & IDMs), Networking and Telecom Equipment Vendors, Automotive Semiconductor Suppliers, and Aerospace and Defense Electronics), Application (AI Accelerators, High-Performance Computing, GPUs, FPGAs, Networking and Data Center Processors, and Application Processors), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| CoWoS-S |

| CoWoS-R |

| CoWoS-L |

| Other Packaging Technology |

| HBM2 and HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| HBM4E and Beyond |

| Below 50,000 Wafers Per Month |

| 50,000 to 99,999 Wafers Per Month |

| 100,000 to 149,999 Wafers Per Month |

| 150,000 Wafers Per Month and Above |

| GPU and AI Chip Vendors |

| Hyperscalers / Cloud Providers |

| Semiconductor Companies (Fabless & IDMs) |

| Networking and Telecom Equipment Vendors |

| Automotive Semiconductor Suppliers |

| Aerospace and Defense Electronics |

| AI Accelerators |

| High-Performance Computing |

| GPUs |

| FPGAs |

| Networking and Data Center Processors |

| Application Processors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Packaging Technology | CoWoS-S | |

| CoWoS-R | ||

| CoWoS-L | ||

| Other Packaging Technology | ||

| By HBM Generation | HBM2 and HBM2E | |

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| HBM4E and Beyond | ||

| By Packaging Capacity Tier | Below 50,000 Wafers Per Month | |

| 50,000 to 99,999 Wafers Per Month | ||

| 100,000 to 149,999 Wafers Per Month | ||

| 150,000 Wafers Per Month and Above | ||

| By End User | GPU and AI Chip Vendors | |

| Hyperscalers / Cloud Providers | ||

| Semiconductor Companies (Fabless & IDMs) | ||

| Networking and Telecom Equipment Vendors | ||

| Automotive Semiconductor Suppliers | ||

| Aerospace and Defense Electronics | ||

| By Application | AI Accelerators | |

| High-Performance Computing | ||

| GPUs | ||

| FPGAs | ||

| Networking and Data Center Processors | ||

| Application Processors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the HBM CoWoS packaging capacity and supply-demand market?

The HBM CoWoS packaging capacity and supply-demand market was valued at USD 1.71 billion in 2025, reached USD 2.31 billion in 2026, and is forecast to reach USD 8.42 billion by 2031 at a 29.53% CAGR.

What is driving demand for HBM CoWoS packaging capacity and supply-demand market?

The main driver is AI accelerator demand that continues to exceed qualified advanced packaging supply, which keeps allocation tight and extends booking cycles.

Which packaging technology currently leads this space?

CoWoS-S led in 2025 with 68.31% share, supported by its established use in AI training and HPC deployments.

Which HBM generation is expected to grow the fastest?

HBM4 is the fastest-growing generation, with a projected CAGR of 30.42% through 2031 as next-generation memory programs require more advanced package integration.

Which region dominates production today?

Asia-Pacific led with 79.84% share in 2025 because Taiwan, South Korea, and Japan together provide the deepest manufacturing and materials base.

Which end users are expanding the fastest?

Hyperscalers and cloud providers are the fastest-growing end-user group, with a projected CAGR of 30.71% through 2031 as custom AI silicon programs scale further.

Page last updated on: