HBM 8-Hi Vs 12-Hi Stack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 10.70 Billion |

| Growth Rate (2026 - 2031) | 24.20% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM 8-Hi Vs 12-Hi Stack Market Analysis by Mordor Intelligence

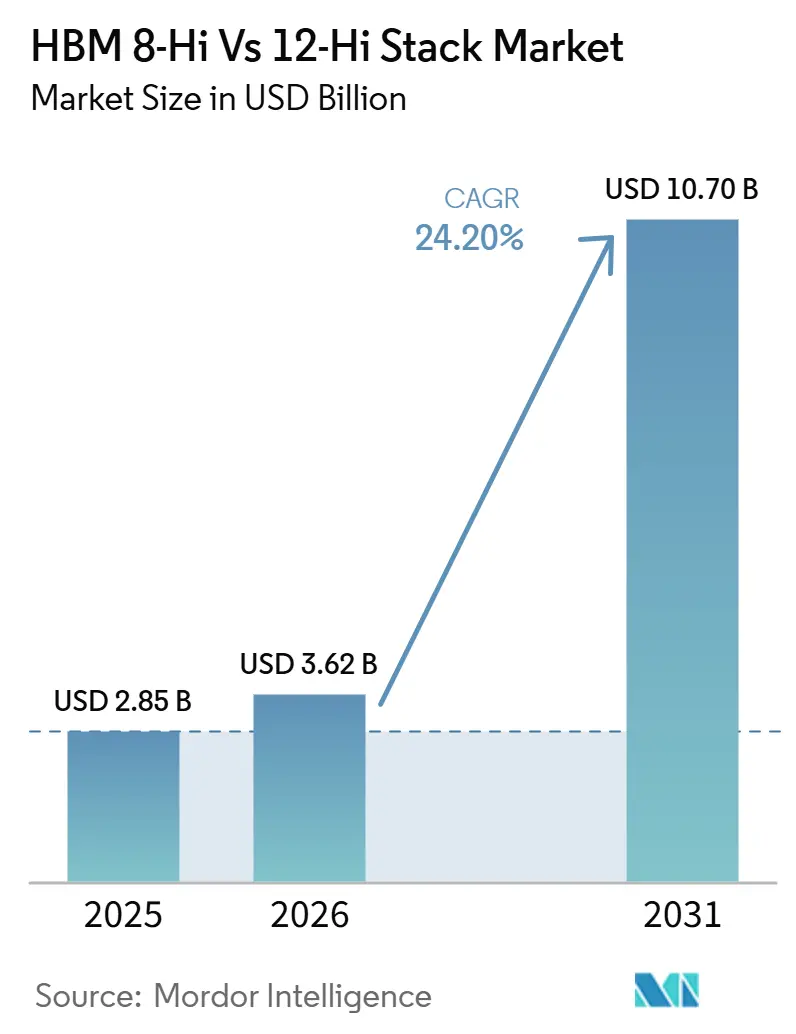

The HBM 8-Hi vs 12-Hi stack market size is expected to increase from USD 2.85 billion in 2025 to USD 3.62 billion in 2026 and reach USD 10.70 billion by 2031, growing at a CAGR of 24.20% over 2026-2031. The HBM 8-Hi vs 12-Hi stack market is expanding because AI accelerator roadmaps now treat stack height as a product-level design choice rather than a back-end packaging detail. NVIDIA’s 8-Hi HBM4 path focuses on higher bandwidth per pin, while AMD’s 12-Hi HBM4 path focuses on higher capacity per package, and that split has made memory architecture a direct point of commercial differentiation. Demand is also rising because inference server upgrades are increasing HBM content per system, which supports revenue growth even when unit growth slows. Supply remains concentrated among a small group of manufacturers, but buyer leverage has become stronger in the highest-performance tiers as multi-year co-development agreements shape qualification and allocation. Near-term growth is still constrained by advanced packaging limits and higher-layer TSV yield challenges, which means the HBM 8-Hi vs 12-Hi stack market is likely to remain supply tight as demand from GPU and custom ASIC programs continues to build.

Key Report Takeaways

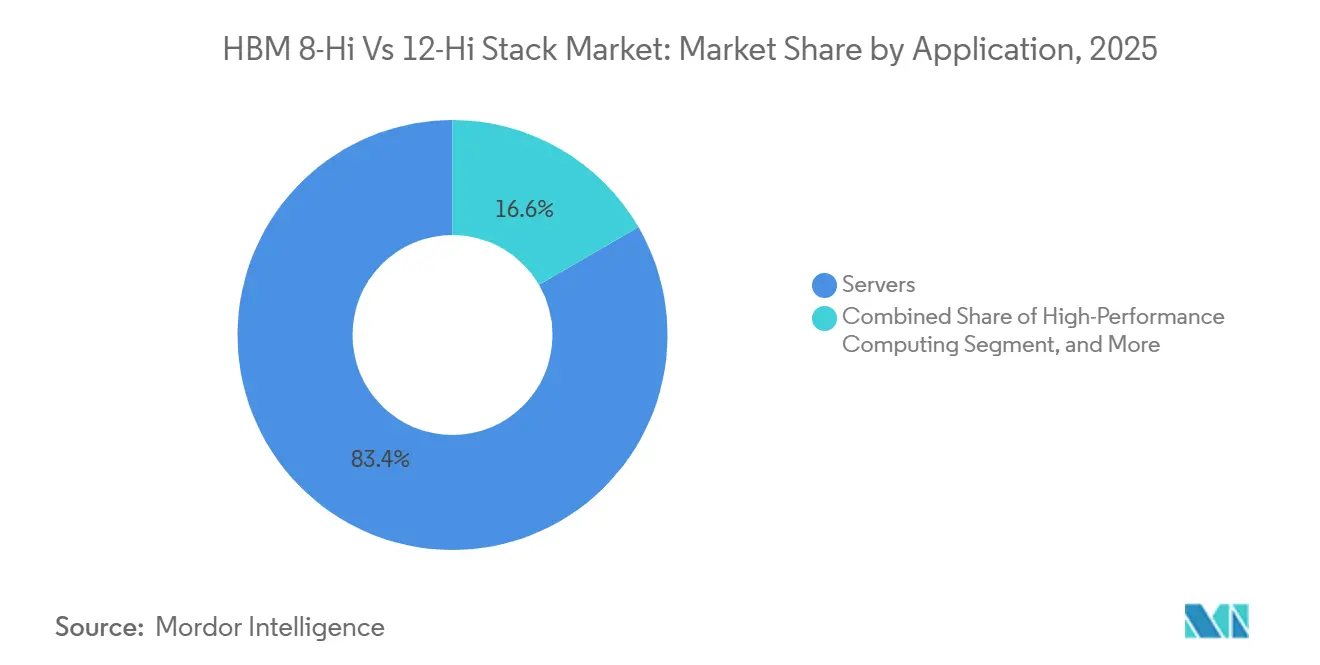

- By application, servers held 83.38% of the HBM 8-Hi vs 12-Hi stack market in 2025, also it is expected to grow at 25.19% through 2031.

- By technology, HBM3E was the leading generation in 2025, while HBM4 is projected to expand at a 25.08% CAGR through 2031.

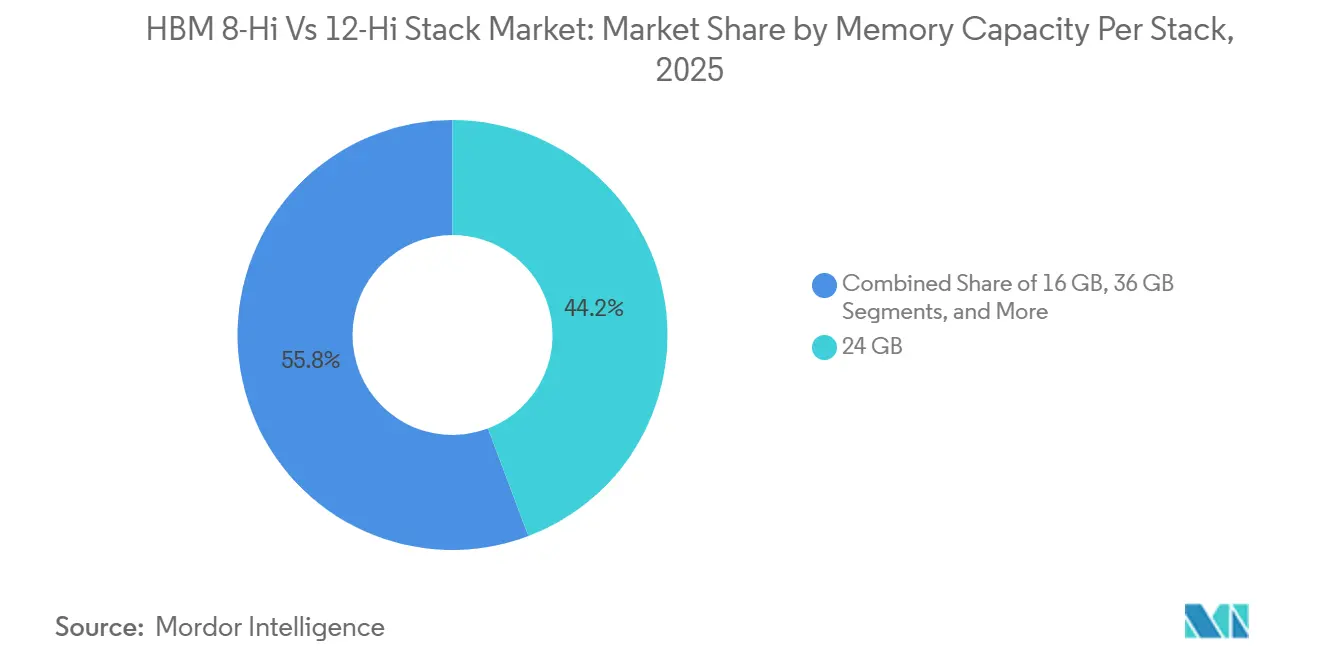

- By memory capacity per stack, 24 GB accounted for 44.24% of the market in 2025, while the above 36 GB tier is projected to expand at a 25.11% CAGR through 2031.

- By processor interface, GPU integration held 79.93% of the market in 2025, while AI accelerator and ASIC interfaces were identified as the fastest-growing interface category during the forecast period.

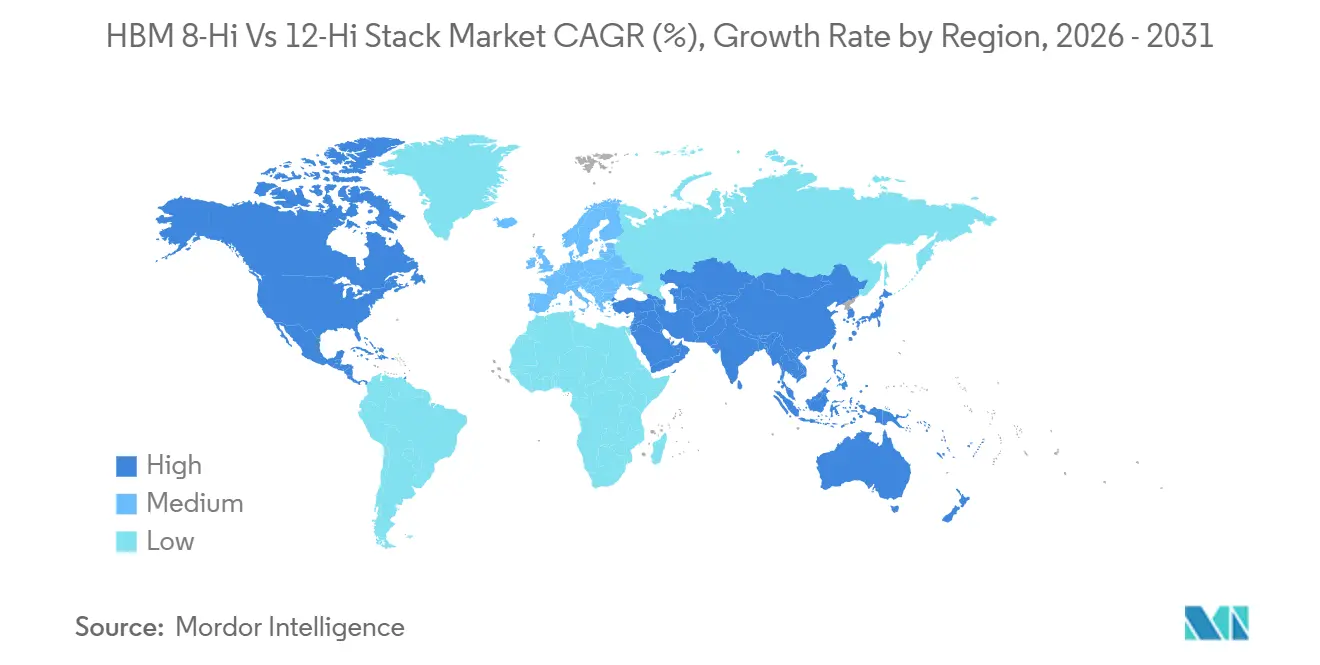

- By geography, Asia-Pacific held 74.62% of the market in 2025, while North America was identified as the fastest-growing regional segment through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM 8-Hi Vs 12-Hi Stack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AI Accelerator Bandwidth Scaling | +5.5% | Global, with concentrated demand in North America and Asia-Pacific | Short term (≤ 2 years) |

| HBM4 Qualification Pull From Leading GPU Platforms | +4.5% | Global, qualification decisions in North America and manufacturing in Asia-Pacific | Short term (≤ 2 years) |

| Long-Term Supply Agreements Favoring 12-Hi Qualification | +3.5% | Global, anchored in Asia-Pacific manufacturing and North American demand centers | Medium term (2-4 years) |

| Hybrid Bonding and Thermal Design Improvements Enabling Higher Stacks | +2.5% | Asia-Pacific core, with spillover to North America via TSMC and OSAT facilities | Medium term (2-4 years) |

| Packaging Capacity Expansion at TSMC and OSAT Partners | +2.0% | Asia-Pacific core, especially Taiwan and South Korea, with ramp in North America | Medium term (2-4 years) |

| Inference Server Density Upgrades Increasing HBM Content Per System | +1.5% | Global, with early gains in North America and Asia-Pacific data center clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid AI Accelerator Bandwidth Scaling

Every major accelerator generation has raised the minimum memory bandwidth needed for competitive AI training and inference, and that shift has pushed the HBM 8-Hi vs 12-Hi stack market into a faster upgrade cycle. NVIDIA’s Rubin platform raised aggregate HBM4 bandwidth well above the level used in earlier systems, which increased the pressure on memory suppliers to deliver higher-performing stacks without extending qualification windows.[1]Samsung Global Newsroom, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com Micron stated in late 2025 that its HBM4 products were operating above 11 Gbps and ramping at a pace that was materially faster than HBM3E, which showed that higher pin-speed targets had already become a commercial requirement rather than a lab milestone. That shift matters because the HBM 8-Hi vs 12-Hi stack market now responds to accelerator roadmaps first, and supplier planning follows those roadmap decisions. It also raises the barrier for new entrants because faster stacks require stronger process control, faster qualification, and tighter integration with the GPU and ASIC development cycle. The immediate result is stronger demand for both high-speed 8-Hi stacks and higher-capacity 12-Hi stacks as platform vendors optimize for different system outcomes.

HBM4 Qualification Pull from Leading GPU Platforms

Qualification on flagship GPU programs has become one of the clearest commercial triggers in the HBM 8-Hi vs 12-Hi stack market. JEDEC released the formal HBM4 standard in April 2025, and that step gave suppliers and chip designers a common framework around a 2,048-bit interface and 32 independent channels.[2]JEDEC Solid State Technology Association, “JEDEC Publishes HBM4 Standard,” JEDEC, jedec.org SK hynix shipped the first 12-layer HBM4 samples to customers in March 2025 using its Advanced MR-MUF process, which positioned it early in the next platform cycle. Samsung then moved into commercial HBM4 mass production in February 2026 with 24 GB to 36 GB products built on a 4 nm logic base die, showing that more than one supplier could support the first wave of HBM4 deployment. Synopsys also validated the first HBM4 IP test chip on a 3 nm process, which showed that the design ecosystem was already aligning around the new standard. Together, these steps reduced single-source risk for buyers and made supplier competition more intense across the HBM 8-Hi vs 12-Hi stack market.

Long-Term Supply Agreements Favoring 12-Hi Qualification

Multi-year supply arrangements are shaping qualification and allocation in the HBM 8-Hi vs 12-Hi stack market with more force than open-market spot buying. SK hynix signed a multi-year co-development and supply agreement with NVIDIA in June 2026 that covered HBM4 and next-generation AI memory for rack-scale AI systems.[3]SK hynix Newsroom, “New Facility Investment for Yongin Semiconductor Cluster,” SK hynix Newsroom, news.skhynix.com That agreement matters because future 12-Hi and higher-layer programs are now being aligned with contracted platform roadmaps, which reduces uncertainty for both volume planning and capital spending. SK hynix also approved additional investment for its Yongin semiconductor cluster in February 2026, taking total committed capital for the first fab to KRW 31 trillion (USD 21.5 billion) and advancing capacity plans in response to AI demand. Micron stated that its full 2026 HBM4 allocation had already sold out, which showed that pre-committed demand had become the primary mechanism for pricing and volume visibility in upper-tier stacks. As a result, the HBM 8-Hi vs 12-Hi stack market is being shaped as much by long-horizon contractual alignment as by immediate benchmark performance.

Hybrid Bonding and Thermal Design Improvements Enabling Higher Stacks

Thermal performance remains central to the HBM 8-Hi vs 12-Hi stack market because taller stacks face higher resistance and tighter system-level cooling limits. Research published in Electronics in 2025 found that heat buildup becomes materially more severe beyond 12 layers in hybrid-bonded three-dimensional memory structures. That finding helps explain why early HBM4 products stayed with microbump-based approaches while suppliers prepared more advanced bonding paths for later products. Samsung stated that its HBM4 delivered a 10% improvement in thermal resistance and a 30% gain in heat dissipation versus HBM3E, which made thermal performance a clearer selling point in high-power accelerator systems. Samsung also shipped 48 GB HBM4E samples in May 2026, and SK hynix followed with 12-layer HBM4E samples in June 2026, which showed that the next stage of stack scaling was already under active customer review. These improvements support the HBM 8-Hi vs 12-Hi stack market because memory thermal behavior now affects full accelerator reliability, not just component specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TSV Yield Losses Above 12-Layer Stacks | -4.0% | Asia-Pacific core, especially South Korea and Taiwan, affecting all major HBM manufacturers | Short term (≤ 2 years) |

| Limited CoWoS and SoIC Advanced-Packaging Capacity | -3.5% | Asia-Pacific core, with Taiwan dominant and spillover to Malaysia and South Korea | Short term (≤ 2 years) |

| Thermal Throttling in High-Bandwidth Devices | -2.5% | Global, with system-level risk concentrated in North American data centers | Medium term (2-4 years) |

| Qualification Concentration Risk Tied to a Small Number of Buyers | -2.0% | Global, concentrated in North America among GPU vendors and hyperscalers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

TSV Yield Losses Above 12-Layer Stacks

TSV yield remains one of the hardest production limits in the HBM 8-Hi vs 12-Hi stack market because each added layer increases alignment and reliability pressure. Work presented at IEEE IRPS 2025 found that TSV keep-out zone proximity in HBM3E can degrade back-end reliability as layouts tighten, and that effect becomes more difficult to manage in 12-Hi and higher configurations. The same production issue has practical commercial effects because stable yield in taller stacks requires several quarters of process learning before volume output becomes dependable. That learning cycle slows the pace at which the HBM 8-Hi vs 12-Hi stack market can translate demand into shipment growth. It also helps explain why qualification delays remained visible even for well-funded suppliers that had already established strong positions in earlier HBM generations. Until yield improves at the same pace as stack ambition, upper-layer products will continue to face tighter supply than demand.

Limited CoWoS and SoIC Advanced-Packaging Capacity

Advanced packaging remains a binding bottleneck for the HBM 8-Hi vs 12-Hi stack market because memory stacks only generate revenue after integration with high-end compute dies. TSMC expanded CoWoS capacity from 35,000 wafers per month in 2024 to 70,000 to 80,000 wafers per month by the end of 2025, and it targeted 115,000 to 140,000 wafers per month by the end of 2026. Even with that expansion, TSMC reported in 2026 that the supply-demand gap was only narrowing rather than disappearing, which meant demand was rising almost as quickly as new lines were being commissioned. The HBM 8-Hi vs 12-Hi stack market therefore remains constrained not only by memory fabrication but also by the pace of CoWoS assembly and related advanced packaging capacity. This issue is wider than the GPU cycle because cloud providers and custom ASIC developers are also booking large packaging allocations. Since next-generation panel-based packaging has been delayed well beyond the forecast horizon, this bottleneck is likely to remain a near-term limit on realized output.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Servers Anchor Structural Demand Amid Inference Densification

Servers accounted for 83.38% of the HBM 8-Hi vs 12-Hi stack market share in 2025, which shows how strongly current demand is tied to AI accelerator infrastructure. The HBM 8-Hi vs 12-Hi stack market stayed centered on servers because high-layer HBM is still used mainly where extreme memory bandwidth and capacity justify a premium system bill. The server refresh cycle is also increasing HBM content per rack, not only the number of systems shipped, and that changes the revenue mix in favor of denser deployments. NVIDIA’s Vera Rubin NVL72 carries 20.7 terabytes of HBM4 per rack versus 8 terabytes in the earlier Grace Blackwell system, which lifts memory content by 2.6x at the rack level. Samsung expected its HBM sales to more than triple in 2026 from 2025, which was consistent with the rise in HBM content per server platform.

The rest of the application mix remained much smaller, although networking and HPC stood closest to the server segment in commercial relevance. Networking demand rose for the same basic reason, which is that AI clusters need switching silicon that can move data at speeds closer to the accelerators they connect. Broadcom-related custom ASIC programs supported that direction by increasing the role of HBM in merchant networking and AI infrastructure silicon, even though the server category remained dominant in the HBM 8-Hi vs 12-Hi stack market. HPC remained important but moved more slowly because government and research deployments follow longer funding and installation cycles. Consumer electronics and automotive and transportation stayed early in adoption because the cost premium of HBM remained difficult to justify in products with tighter cost and power limits.

By Technology: HBM4 Poised to Reshape the Generation Mix

HBM4 is projected to expand at a 25.08% CAGR in the HBM 8-Hi vs 12-Hi stack market size through 2031, making it the fastest-growing technology generation in the forecast period. JEDEC’s April 2025 HBM4 release doubled the interface width to 2,048 bits and standardized 32 independent channels, which materially increased the bandwidth ceiling for next-generation products. Samsung stated that its commercial HBM4 reached up to 3.3 TB/s per stack, which underscored why new GPU and ASIC programs were aligning around this generation. The HBM 8-Hi vs 12-Hi stack market still relied heavily on HBM3E in 2025 because Blackwell and MI350 production cycles kept that generation relevant even as HBM4 moved into qualification and early ramp. This overlap means the technology shift is not a one-step replacement and will play out over several platform cycles.

Older generations such as HBM2, HBM2E, and HBM3 continued to serve legacy HPC and graphics deployments that had not yet completed refresh cycles. Those tiers are likely to lose share over time, but they still provide a base level of revenue in the early years of the forecast. The more important transition is between HBM4 and HBM4E, where suppliers are already trying to extend bandwidth and capacity without waiting for a full generational reset. Samsung shipped 48 GB 12-layer HBM4E samples in May 2026, and SK hynix shipped 12-layer HBM4E samples in June 2026, which showed that the technology pipeline within the HBM 8-Hi vs 12-Hi stack industry was already moving past first-wave HBM4. Synopsys also validated HBM4 IP on a 3 nm process, which supports the broader design ecosystem needed for faster adoption in custom silicon.

By Memory Capacity Per Stack: 24 GB Leads While Ultra-Dense Tiers Gain Speed

The 24 GB tier held 44.24% of the HBM 8-Hi vs 12-Hi stack market size in 2025, reflecting the strong presence of 12-Hi HBM3E and early 12-Hi HBM4 products. This segment benefited from broad platform relevance because 12-layer designs naturally mapped to the capacities needed in current AI systems. The HBM 8-Hi vs 12-Hi stack market kept 24 GB in the lead because it sits at the center of current commercial deployment, where suppliers and buyers can balance density, yield, and qualification speed. The above 36 GB tier is projected to grow at a 25.11% CAGR through 2031 as HBM4 and HBM4E move into 36 GB and 48 GB configurations. That demand pattern comes from inference operators that want larger models to remain inside GPU HBM, where avoiding external memory access helps protect latency and throughput.

The 16 GB and up to 8 GB tiers are losing share because new platforms are moving away from lower-density options. The 36 GB tier remains commercially important because it offers a midpoint between today’s dominant 24 GB products and the ultra-dense configurations that are still climbing the qualification curve. SK hynix shipped 36 GB 12-layer HBM4 samples in March 2025, which confirmed that this tier had already moved from concept to customer sampling. A notable split inside the HBM 8-Hi vs 12-Hi stack market is that NVIDIA’s 8-Hi path is linked to lower per-stack capacity with higher pin-speed emphasis, while AMD’s 12-Hi path is linked to much higher system capacity. That platform split allows the 24 GB tier and the above 36 GB tier to grow at the same time for different commercial reasons.

By Processor Interface: GPU Leadership Masks Rapid ASIC Diversification

GPU interfaces captured 79.93% of the HBM 8-Hi vs 12-Hi stack market share in 2025, which reflects NVIDIA and AMD’s control over current AI accelerator deployment. The HBM 8-Hi vs 12-Hi stack market is still highly dependent on GPUs because they remain the main compute engine for large-scale AI training and inference. Within that GPU base, the architectural split is clear because NVIDIA is using 8-Hi stacks to emphasize bandwidth per pin, while AMD is using 12-Hi stacks to emphasize memory capacity per system. That makes the processor interface discussion inseparable from the core design split that defines the HBM 8-Hi vs 12-Hi stack market. CPU interfaces remained smaller but relevant in selected HPC systems where on-package memory can improve latency-sensitive workloads.

The AI accelerator and ASIC segment was the fastest-growing interface category because hyperscalers are funding custom silicon programs that can bypass merchant GPUs in selected workloads. Google’s Ironwood TPU generation used HBM with 192 GiB of capacity and 7.37 TB/s of bandwidth, which showed that the custom ASIC route is becoming a material demand channel for advanced memory. That shift matters because custom ASIC programs usually run on multi-year roadmaps, which gives suppliers more visibility on required memory specifications and volume timing. Synopsys and Rambus have also become more important to the HBM 8-Hi vs 12-Hi stack industry because controller IP and validation work are now embedded deeper into custom silicon programs. FPGA and other interfaces remained niche but retained value in networking, defense, and signal-processing workloads where HBM’s lower power per bit can still justify a premium.

Geography Analysis

Asia-Pacific held 74.62% of the HBM 8-Hi vs 12-Hi stack market share in 2025, which reflects the concentration of memory fabrication and advanced packaging across South Korea and Taiwan. The HBM 8-Hi vs 12-Hi stack market remains centered in Asia-Pacific because SK hynix and Samsung run primary HBM DRAM production in South Korea, while Taiwan holds a large share of CoWoS packaging capacity through TSMC and related suppliers. South Korea sits at the center of current supply growth because SK hynix accelerated investment in the Yongin semiconductor cluster and continued to expand capacity in response to AI-related demand. Taiwan is equally critical because the pace of CoWoS ramp directly affects how much HBM can reach the end market as packaged accelerator modules. India remained at an early stage in semiconductor manufacturing, and its current programs did not yet intersect with HBM-class production.

North America was the fastest-growing geography in the forecast period because hyperscaler capital spending continued to pull more advanced memory into domestic AI infrastructure. The U.S. CHIPS and Science Act also encouraged localization of advanced memory and packaging capacity, which supported the region’s role in the HBM 8-Hi vs 12-Hi stack market. Micron outlined a multi-decade USD 50 billion domestic investment commitment with more than USD 6 billion in expected federal support for leading-edge fabs in Idaho and New York. SK hynix also announced a USD 3.87 billion advanced packaging facility in Indiana, which showed that packaging localization had started to move from policy goal to committed investment. These moves matter because buyers increasingly prefer supply options that reduce geopolitical concentration risk.

Europe’s HBM demand remained linked mainly to HPC programs and automotive AI development, but the region still lacked primary HBM manufacturing capacity. That left Europe dependent on Asia-Pacific suppliers and pushed local projects toward the back of allocation queues when supply tightened. South America and the Middle East and Africa remained smaller demand centers, with growth tied mainly to sovereign AI infrastructure and data center programs. Their direction depended more on infrastructure spending and external supplier access than on local semiconductor production. As a result, the HBM 8-Hi vs 12-Hi stack market still showed a clear imbalance between where memory is made and where future AI compute demand is accelerating.

Competitive Landscape

The HBM 8-Hi vs 12-Hi stack market remained extremely concentrated on the supply side because SK hynix, Samsung Electronics, and Micron Technology controlled primary HBM DRAM manufacturing. SK hynix maintained the strongest HBM position through 2025 and into 2026, and its June 2026 agreement with NVIDIA strengthened that lead by tying future memory development to one of the largest AI platform roadmaps in the sector. Samsung responded by pushing a vertically integrated HBM4 strategy built around its own 4 nm logic base die and in-house DRAM manufacturing, which allowed it to compete on both performance and system design control. Samsung also stated that HBM4 cumulative sales surpassed USD 1 billion within 130 days of commercial mass production and that all 2026 HBM production had already been pre-committed by customers. Micron followed a different path by acquiring PSMC’s P5 fab in Tongluo for USD 2 billion, which accelerated capacity expansion without the longer lead time of a greenfield project.

Below the three primary suppliers, the HBM 8-Hi vs 12-Hi stack market became more fragmented around packaging, testing, and design enablement. TSMC held a gatekeeper role because CoWoS capacity remained sold out well ahead of delivery, which gave the company strong influence over which accelerator programs moved fastest into volume. OSAT providers such as ASE Technology Holding, Amkor Technology, and Powertech Technology were expanding toward more advanced packaging roles, but qualification at 12-Hi and above still required time and proven yield performance. That made advanced packaging less of a simple outsourcing step and more of a competitive filter for the whole HBM 8-Hi vs 12-Hi stack market.

Another area of competition opened in custom HBM configurations tied to hyperscaler ASIC programs. Buyers such as Google, Amazon, and Microsoft have been requesting memory designs that differ in base-die logic, thermal envelope, and I/O needs, which created room for premium pricing and closer co-design. Synopsys strengthened that channel by validating the first HBM4 IP test chip on a 3 nm node, which made advanced controller and integration work more credible for custom silicon teams. The practical result is that the HBM 8-Hi vs 12-Hi stack market is concentrated at the top, but the surrounding ecosystem is becoming more specialized and strategically important.

HBM 8-Hi Vs 12-Hi Stack Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

Taiwan Semiconductor Manufacturing Company Limited

Amkor Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK hynix signed a multi-year co-development and supply agreement on June 8, 2026, covering HBM4 and next-generation AI memory for NVIDIA's "AI factory" infrastructure, including the Vera Rubin platform. The deal, disclosed during CEO Jensen Huang's visit to South Korea, gives SK hynix structural allocation priority and co-design influence over future HBM stack specifications.

- June 2026: Jensen Huang confirmed on June 5, 2026, that all three HBM4 suppliers, SK hynix, Samsung Electronics, and Micron Technology, had passed qualification and entered production for NVIDIA's Vera Rubin platform, with Q3 2026 customer shipments scheduled. This marks the first NVIDIA GPU generation entering volume production with simultaneous multi-vendor HBM supply, shifting pricing leverage toward the buyer.

- June 2026: Samsung Electronics reported that HBM4 cumulative sales surpassed USD 1 billion within 130 days of commercial mass production commencement, with year-end projections above USD 10 billion. Samsung also disclosed that all its 2026 HBM production capacity had been pre-committed by customers, with year-on-year HBM shipment growth expected to exceed 200%.

- May 2026: Samsung Electronics shipped the industry's first 12-layer 48 GB HBM4E samples to major global customers, featuring 14 to 16 Gbps pin speed, over 3.6 TB/s memory bandwidth per stack, exceeding 20% improvement over HBM4, and targeting integration with NVIDIA's next-generation Vera Rubin Ultra accelerator planned for 2027.

Global HBM 8-Hi Vs 12-Hi Stack Market Report Scope

The Global HBM 8-Hi vs 12-Hi Stack Market refers to the specialized industry segment that compares and analyzes demand, adoption, and technological advancements between High Bandwidth Memory (HBM) modules configured in 8-high (8-Hi) and 12-high (12-Hi) stack architectures.

The HBM 8-Hi vs 12-Hi Stack Market Report is Segmented by Application (Servers, Networking, High-Performance Computing, Consumer Electronics, and Automotive and Transportation), Technology (HBM2, HBM2E, HBM3, HBM3E, and HBM4), Memory Capacity Per Stack (Up to 8 GB, 16 GB, 24 GB, 36 GB, and Above 36 GB), Processor Interface (GPU, CPU, AI Accelerator and ASIC, FPGA, and Other Processor Interfaces), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Servers |

| Networking |

| High-Performance Computing |

| Consumer Electronics |

| Automotive and Transportation |

| HBM2 |

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| Up to 8 GB |

| 16 GB |

| 24 GB |

| 36 GB |

| Above 36 GB |

| GPU |

| CPU |

| AI Accelerator and ASIC |

| FPGA |

| Other Processor Interfaces |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Application | Servers | |

| Networking | ||

| High-Performance Computing | ||

| Consumer Electronics | ||

| Automotive and Transportation | ||

| By Technology | HBM2 | |

| HBM2E | ||

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| By Memory Capacity Per Stack | Up to 8 GB | |

| 16 GB | ||

| 24 GB | ||

| 36 GB | ||

| Above 36 GB | ||

| By Processor Interface | GPU | |

| CPU | ||

| AI Accelerator and ASIC | ||

| FPGA | ||

| Other Processor Interfaces | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the HBM 8-Hi vs 12-Hi stack market?

The HBM 8-Hi vs 12-Hi stack market was valued at USD 2.85 billion in 2025, reached USD 3.62 billion in 2026, and is forecast to hit USD 10.70 billion by 2031 at a 24.20% CAGR.

Why are 8-Hi and 12-Hi HBM stacks both gaining traction?

The main reason is that platform vendors are optimizing for different outcomes. NVIDIA's path emphasizes bandwidth per pin with 8-Hi stacks, while AMDs path emphasizes capacity per package with 12-Hi stacks.

Which application drives most revenue in this space?

Servers led demand with 83.38% of 2025 revenue because AI training and inference systems remain the main commercial use case for high-layer HBM.

Which technology generation is growing the fastest?

HBM4 is the fastest-growing technology generation, with a forecast CAGR of 25.08% through 2031, supported by the move to wider interfaces and higher per-stack bandwidth.

Which memory capacity tier is expanding the fastest?

The above 36 GB tier is projected to grow at a 25.11% CAGR through 2031 as operators seek higher-capacity stacks for larger AI models and denser inference systems.

Which region matters most for supply and growth?

Asia-Pacific remained the largest region with 74.62% share in 2025 because production is concentrated in South Korea and Taiwan, while North America is the fastest-growing region because hyperscaler and policy-led investment continues to rise.

Page last updated on: