HBM3E Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

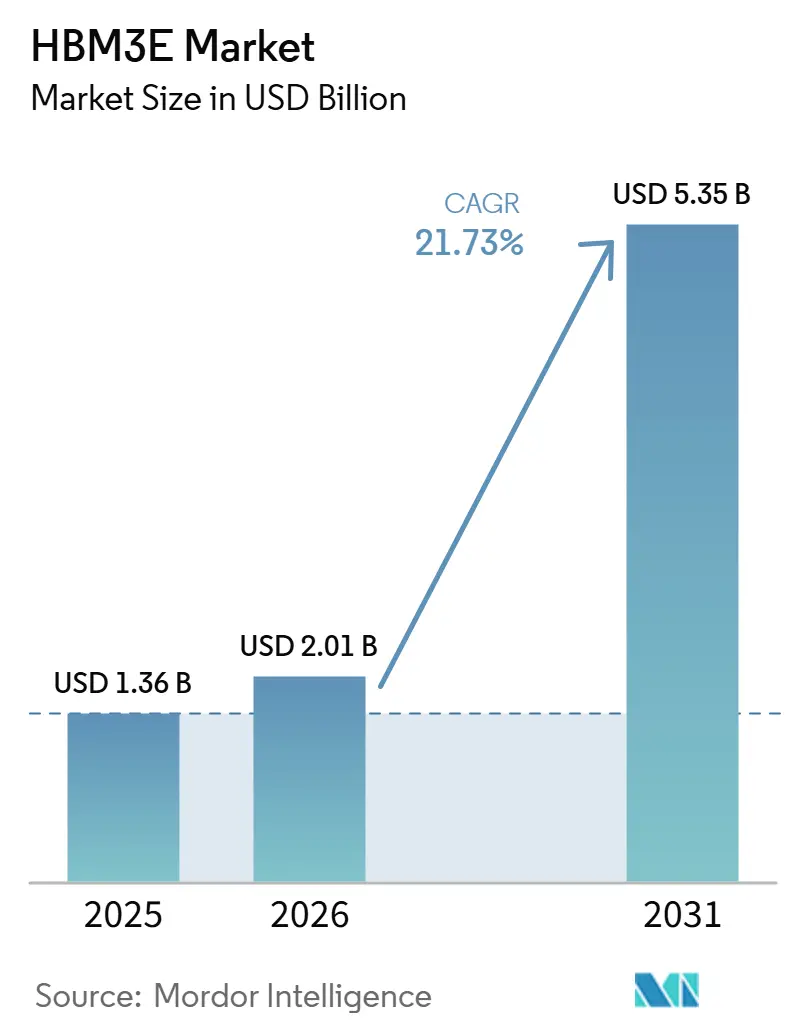

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 5.35 Billion |

| Growth Rate (2026 - 2031) | 21.73% CAGR |

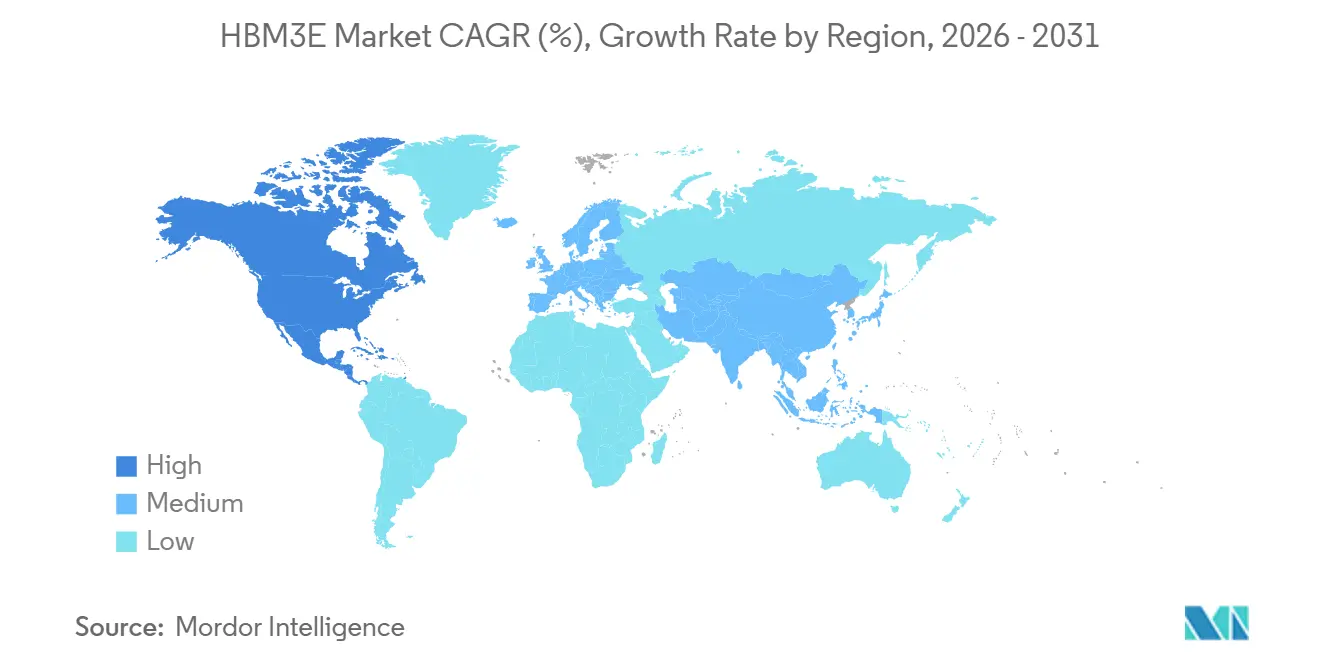

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

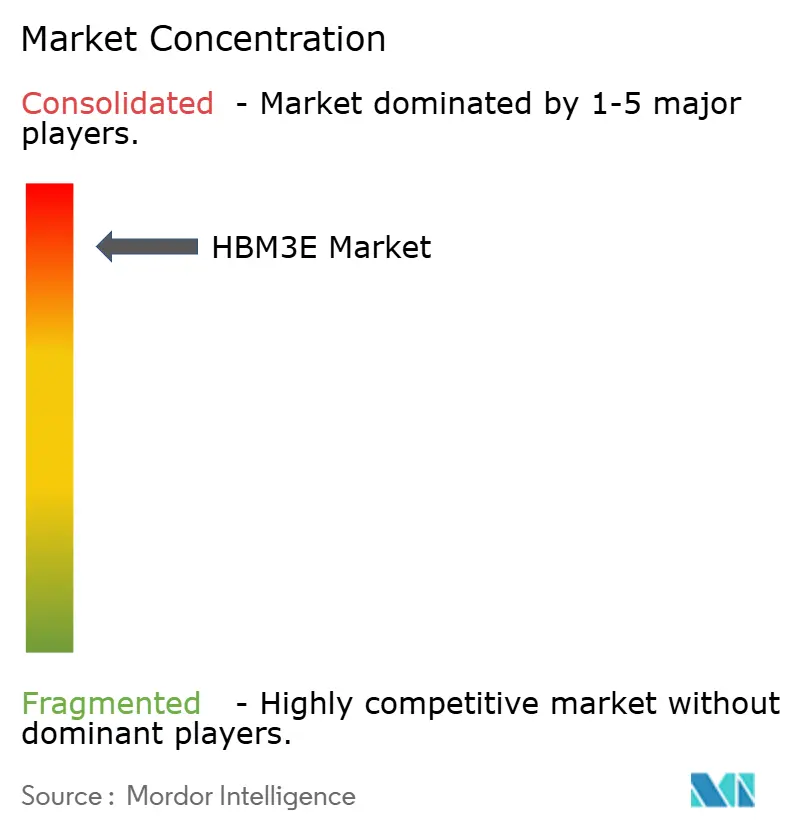

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM3E Market Analysis by Mordor Intelligence

The HBM3E market size is expected to increase from USD 1.36 billion in 2025 to USD 2.01 billion in 2026 and reach USD 5.35 billion by 2031, growing at a CAGR of 21.73% over 2026-2031. Growth in the HBM3E market is being driven by a sharp increase in memory capacity per accelerator, with NVIDIA Blackwell Ultra B300 carrying 288 GB of HBM3E compared with 80 GB on H100, which is lifting demand even without a matching rise in accelerator unit shipments. The HBM3E market is also benefiting from hyperscalers shortening standard server replacement cycles as they move from H100- and H200-class systems to newer platforms that offer better inference economics. The market remains protected by a strong technology lock, as no alternative memory architecture is positioned to meet the bandwidth and density requirements of flagship AI accelerators at production yields within the forecast period. Competitive behavior in the HBM3E market is defined by qualification timing, access to advanced packaging, and the ability to lock into multiyear platform roadmaps with major AI chip vendors. At the same time, tight CoWoS packaging capacity and export controls on China-linked demand are limiting how much of this demand can translate into realized revenue during the forecast period.

Key Report Takeaways

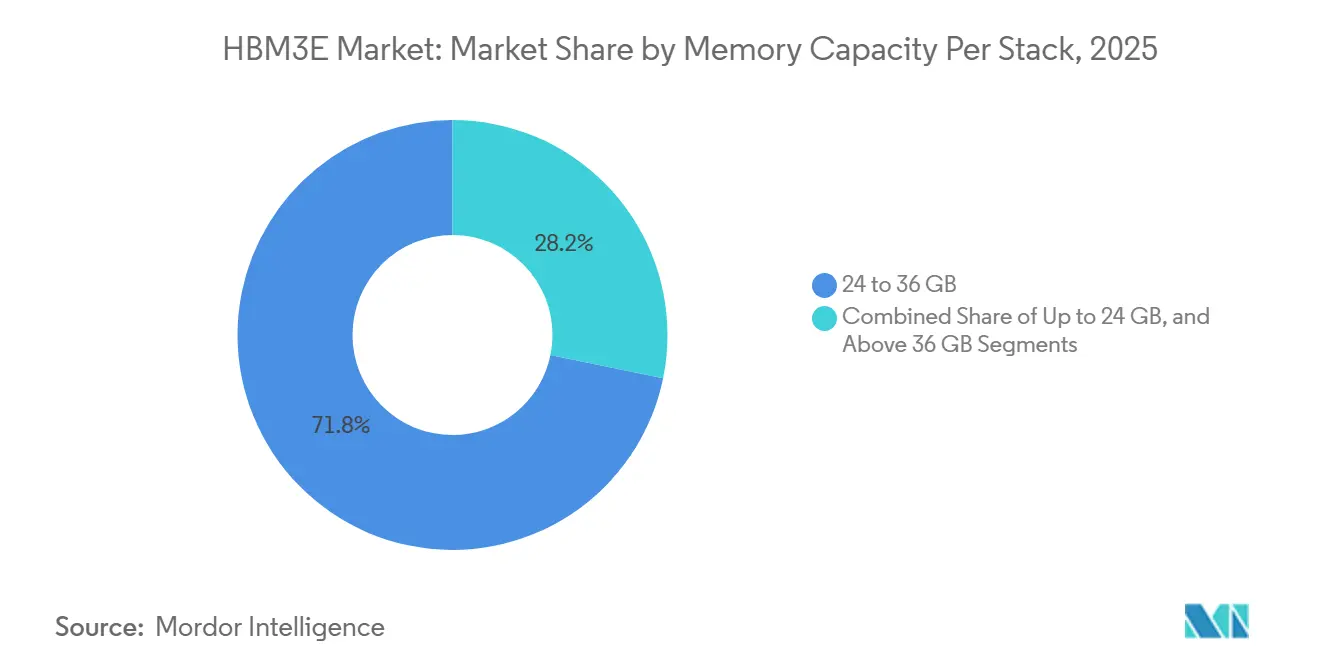

- By memory capacity per stack, 24-36 GB held 71.78% of the HBM3E market share in 2025, while capacities above 36 GB are projected to expand at a 22.38% CAGR through 2031.

- By processor interface, GPU accounted for 76.93% of revenue in 2025, while AI accelerators and ASICs are expected to record the fastest 22.73% CAGR through 2031 in the HBM3E market.

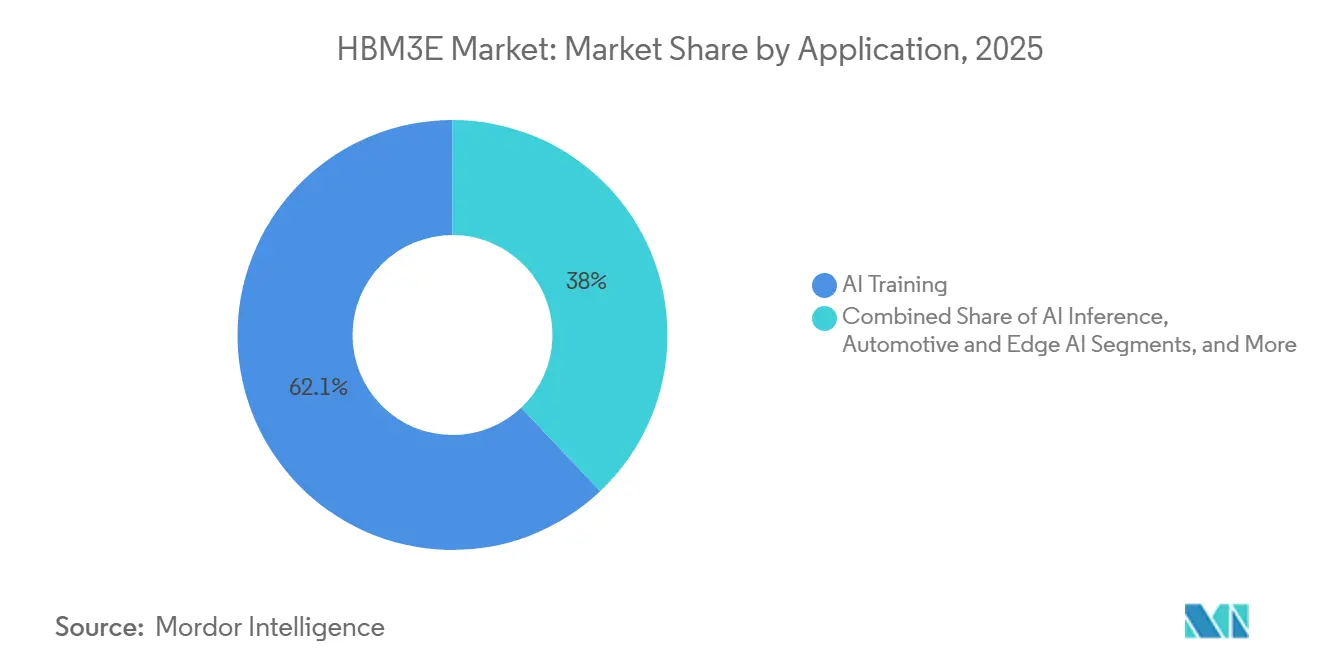

- By application, AI training accounted for 62.05% of the HBM3E market size in 2025, while AI inference is projected to expand at a 23.12% CAGR through 2031.

- By end-use industry, cloud service providers contributed 74.22% of revenue in 2025, while enterprise IT is projected to grow at a 22.91% CAGR through 2031 in the HBM3E market.

- By geography, Asia-Pacific accounted for 61.36% of revenue in 2025, while North America is projected to record the fastest CAGR of 22.64% through 2031 in the HBM3E market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM3E Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AI Accelerator Bandwidth Escalation | +7.2% | Global | Short term (≤ 2 years) |

| HBM3E Qualification Advantage In Premium GPU Supply Chains | +4.5% | Asia-Pacific and North America | Short term (≤ 2 years) |

| Intensifying Demand For 12-High And Higher Stack Density | +3.8% | Global | Medium term (2-4 years) |

| HBM3E Adoption In Hyperscale AI Server Refresh Cycles | +2.9% | North America and APAC core, spill-over to Europe | Short term (≤ 2 years) |

| Second-Source Qualification Pressure Across AI OEMs | +2.1% | North America and Asia-Pacific | Medium term (2-4 years) |

| Advanced Packaging Yield Optimization From Memory-Compute Co-Design | +1.6% | Global, with early gains in South Korea and Taiwan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid AI Accelerator Bandwidth Escalation

AI accelerators now require memory bandwidth levels not seen in earlier commercial computing systems. The HBM3E standard itself was designed for per-pin data rates beyond 9 Gbps across a 1,024-bit interface and 16 independent channels, which shows why this memory class sits at the center of current AI system design. As model sizes and context windows expand, data movement pressure rises faster than many conventional memory subsystems can handle, which keeps bandwidth at the center of system bottlenecks.[1]Micron Technology, Inc., “Accelerating Large Language Model Inference With Micron HBM3E,” Micron Technology, micron.com That pattern gives the HBM3E market a structural demand base, as buyers respond to architectural constraints rather than only to short-term budget cycles. It also explains why the HBM3E market continues to advance even as AI infrastructure spending rotates between training and inference. The result is a durable pull for high-bandwidth memory in premium AI platforms over the forecast period.

HBM3E Qualification Advantage In Premium GPU Supply Chains

The HBM3E market has been shaped by a qualification process that functions as a high commercial barrier for memory suppliers. SK Hynix began the world's first mass production of 12-layer HBM3E in September 2024, giving it an early position in premium accelerator programs. Micron stated in June 2025 that its 36 GB 12-high HBM3E was designed into AMD Instinct MI350 Series solutions and was qualified on multiple leading AI platforms. NVIDIA and SK Hynix then announced a multiyear technology partnership in June 2026 that covered co-development of memory for Vera Rubin AI supercomputers, Vera CPUs, RTX Spark-powered PCs, and Jetson Thor robotic platforms. These moves show that the HBM3E market rewards suppliers that qualify early and stay inside customer roadmaps across successive platform generations. They also narrow the window for later entrants seeking to displace incumbent suppliers in premium GPU supply chains.

Intensifying Demand For 12-High And Higher Stack Density

The HBM3E market is moving steadily from 8-high products toward 12-high and higher stack density configurations. SK Hynix said its 12-layer HBM3E mass production delivered 36 GB per stack at 9.6 Gbps per pin and up to 1.0 TB/s per stack, marking a major step toward production-ready density and bandwidth. JEDEC's HBM3E standard also supports the performance envelope needed for this density shift in advanced AI systems. Samsung's May 2026 announcement on HBM4E samples shows that suppliers are already preparing for the next density step beyond current HBM3E volumes, which keeps the race for taller stacks active across the value chain. This raises manufacturing complexity because taller stacks require more aggressive die thinning, more difficult thermal control, and tighter package integration. The HBM3E market therefore benefits from higher content per device, while near-term supply remains constrained by the difficulty of scaling these higher-density products.

HBM3E Adoption In Hyperscale AI Server Refresh Cycles

The HBM3E market is also being lifted by hyperscalers that are refreshing AI server fleets faster than traditional enterprise replacement cycles. Microsoft launched Maia 200 in January 2026 as a custom inference accelerator built on TSMC's 3 nm process, with 216 GB of HBM3E and 7.0 TB/s bandwidth, demonstrating that proprietary hyperscaler silicon is now a direct source of demand for HBM3E. SK Hynix's 2026 market outlook also said Google selected SK Hynix as the first HBM3E supplier for the TPU v7p and v7e series, indicating a second large procurement path outside the core NVIDIA cycle. This spreads demand across more customers and silicon types, reducing the risk associated with any one platform change. It also means the HBM3E market is no longer dependent only on merchant GPU demand, because custom ASIC programs now carry their own memory roadmaps. That wider customer mix supports revenue continuity through multiple refresh cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Advanced Packaging Capacity For CoWoS And Similar Interposers | -1.8% | Global | Short term (≤ 2 years) |

| Export Controls And Customer Concentration Risk In China-Linked Demand | -1.4% | Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Thermal And Power-Integrity Constraints In Dense AI Boards | -0.8% | Global | Medium term (2-4 years) |

| Qualification Delays In High-Power 12-High HBM3E Stacks | -1.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Advanced Packaging Capacity For CoWoS And Similar Interposers

The HBM3E market remains constrained by advanced packaging capacity, especially in CoWoS and related 2.5D integration flows. TSMC repeatedly described AI-related capacity as very tight across its investor communications, even as the company expanded both front-end and back-end support for AI demand. TSMC also noted that CoWoS capacity doubled in 2025 but remained fully allocated, indicating that packaging additions have not been sufficient to clear the backlog. This matters because HBM3E stacks cannot become revenue until they are integrated with compute dies through advanced packaging lines. Equipment lead times then make the constraint harder to solve quickly, since new bonders and precision placement tools take time to reach volume use. The HBM3E market, therefore, faces a real conversion gap between memory demand and shippable accelerator systems.

Export Controls And Customer Concentration Risk In China-Linked Demand

The HBM3E market also faces policy restraints from export controls that limit access to part of the addressable customer base. The United States Bureau of Industry and Security said in December 2024 that HBM2e, HBM3, HBM3E, and HBM4 fell under ECCN 3A090.c, with a global license requirement for exports to Macau and Country Group D:5 destinations. That rule removes a portion of China-linked demand from normal market access and adds compliance friction for transactions tied to sensitive end users. The effect is stronger because the customer base is already concentrated among a small number of advanced AI buyers. It also limits demand visibility in regions where end-use verification can be more complex than in established OECD supply chains. The HBM3E market, therefore, grows from a narrower accessible base than raw technology demand alone would suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Capacity Per Stack: 12-High Configuration Anchors Market Structure

The 24 to 36 GB segment held 71.78% of revenue in 2025, making it the largest memory capacity tier in the HBM3E market. This range is centered on 36 GB 12-high products that support flagship AI accelerators from NVIDIA and AMD, which explains why it became the commercial core of the HBM3E market. JEDEC's HBM3E standard supports this configuration with a wide interface and higher per-pin data rates, which makes the segment suitable for dense AI workloads. The up to 24 GB segment remained relevant in 2025 for legacy AI server deployments, networking use cases, and cost-sensitive inference systems where absolute bandwidth is less critical. Even so, the HBM3E market is shifting its center of gravity away from those lower-capacity products as customers move toward larger memory footprints per accelerator.

SK Hynix's world-first mass production of 12-layer HBM3E in September 2024 demonstrated that 12-high products had already moved from development into scaled commercial production.[2]SK hynix Inc., “SK hynix Begins World-First Mass Production Of 12-Layer HBM3E,” SK hynix Korean Newsroom, news.skhynix.co.kr That production shift matters because the HBM3E market now depends on stack height as much as on wafer volume when suppliers try to expand revenue. Above 36 GB is projected to grow at a 22.38% CAGR through 2031, which reflects demand for 16-high and other future high-density formats in next-generation systems. Samsung's May 2026 announcement of a HBM4E sample shipment shows that suppliers are already preparing for even denser memory packages, reinforcing the direction of travel toward taller stacks. The HBM3E market share held by 24 to 36 GB in 2025 reflects the current deployment reality, while products above that range are driving future growth.

By Processor Interface: Custom Silicon Disrupts GPU Dominance

GPU accounted for 76.93% of revenue in 2025, which kept graphics processors as the main interface category in the HBM3E market. That share reflects the concentration of current HBM3E procurement in NVIDIA Blackwell systems and AMD Instinct platforms, both of which anchor large training clusters and advanced inference infrastructure. The HBM3E market still leans heavily on merchant GPU roadmaps because those platforms drive the largest volume commitments from hyperscalers and advanced AI system buyers. CPU and FPGA interfaces remained smaller in 2025 because their use cases were narrower and more specialized. Even so, the HBM3E market is no longer defined only by GPU demand, because custom silicon programs are now moving into the same memory class.

AI accelerators and ASICs are projected to expand at a 22.73% CAGR through 2031, making them the fastest-growing processor interfaces in the HBM3E market. Microsoft's Maia 200 launch in January 2026 clearly showed this shift, with a custom inference accelerator integrating 216 GB of HBM3E and 7.0 TB/s bandwidth. SK Hynix also said Google selected it as the first HBM3E supplier for TPU v7p and v7e, which confirms that hyperscaler ASIC programs are becoming a meaningful second channel for demand. This shift reduces dependence on one vendor cycle and gives the HBM3E market a broader customer base across both merchant and proprietary AI silicon. It also means future interface mix will likely become less GPU-heavy even if GPU unit volumes keep rising.

By Application: Inference Momentum Reshapes The Demand Mix

AI training accounted for 62.05% of revenue in 2025, which made it the leading application in the HBM3E market. That position was tied to frontier model pretraining, where dense GPU clusters run for long periods, and place sustained pressure on memory bandwidth and capacity. Micron's technical material on HBM3E highlighted how this memory class supports large language model inference and advanced AI workloads through high bandwidth and lower data movement friction. High-performance computing also remained a steady application base, since HBM architectures were already validated in scientific and research computing before the current AI wave. The HBM3E market, therefore, entered 2026 with training still at the center of revenue, but with a wider application base forming around it.

AI inference is projected to grow at a 23.12% CAGR through 2031, which makes it the fastest-growing application in the HBM3E market. Microsoft's Maia 200 launch was a clear sign of that shift, as it was positioned as an inference accelerator rather than a general training-first platform. Inference also broadens the HBM3E market by enabling more ASIC-based deployments and a broader range of customer architectures. Networking, telecommunications, automotive, and edge AI are still smaller application areas, yet they add to the breadth of long-term demand as AI workloads move closer to the network edge and to specialized onboard systems. The HBM3E market size linked to inference is therefore rising not only because inference volumes are increasing, but also because the number of hardware routes serving those workloads is expanding.

By End Use Industry: Enterprise Deployment Narrows Cloud Concentration

Cloud service providers accounted for 74.22% of revenue in 2025, making this segment the clear leader in the HBM3E market. That concentration reflected the buying power of hyperscalers, which could secure supply through large advance commitments and integrate HBM3E into both GPU and custom ASIC roadmaps. Microsoft's Maia 200 launch and Google's TPU-related HBM3E sourcing show how large cloud operators are shaping direct memory demand through their own silicon programs and merchant platforms. This made the cloud the anchor customer group for the HBM3E market in 2025. It also raised the barrier for smaller buyers, who often lacked the same access to long-duration supply agreements.

Enterprise IT is projected to grow at a 22.91% CAGR through 2031, making it the fastest-growing end-use segment in the HBM3E market. That growth reflects a gradual move by large enterprises toward owned AI infrastructure for private inference and model tuning when data control and latency matter more than flexible cloud access. The HBM3E market is also seeing interest from telecommunications, automotive, aerospace and defense, healthcare imaging, financial services, and scientific research, even if these remain smaller demand pools today. Those sectors value high-bandwidth, compact packages for specialized workloads, helping extend demand beyond hyperscaler concentration. The HBM3E market will therefore remain cloud-led through the forecast period, while enterprise adoption slowly broadens the end-user mix.

Geography Analysis

Asia-Pacific accounted for 61.36% of revenue in 2025, making it the leading regional bloc in the HBM3E market. South Korea remains the production hub because SK Hynix and Samsung operate the bulk of the HBM wafer and stacking capacity used in the current cycle. Hynix's 2026 market outlook also described the strong HBM pull into Taiwan, where advanced packaging lines connect memory stacks with AI accelerator logic dies. Taiwan then adds the packaging layer through TSMC, whose CoWoS lines remain a critical checkpoint for system output.[3]Taiwan Semiconductor Manufacturing Company, “Investor Relations Earnings Call Transcripts And Quarterly Reports,” TSMC Investor Relations, investor.tsmc.com This Korea-Taiwan production link explains why the Asia-Pacific held the largest share of the HBM3E market size in 2025.

North America is projected to grow at a 22.64% CAGR through 2031, making it the fastest-growing geography in the HBM3E market. The region benefits from concentrated AI infrastructure spending by hyperscalers and from strong demand visibility around advanced accelerator deployments. Microsoft's Maia 200 launch in January 2026 showed that North American demand is not limited to merchant GPU purchases, as custom silicon programs are also driving HBM3E consumption. Micron's June 2025 statement on AMD platform integration also reinforced North America's role in shaping product qualification and customer alignment for the HBM3E market. The region, therefore, combines end demand, platform influence, and strategic supply planning to support above-market growth.

Europe, South America, the Middle East, and Africa accounted for the remaining share of the HBM3E market in 2025, with each region still contributing at a single-digit level. In Europe, demand is mainly driven by scientific computing, advanced research infrastructure, and expanding data center footprints supporting AI workloads. South America remains at an earlier stage, with adoption concentrated in a small number of countries where cloud and digital infrastructure investment is beginning to scale. The Middle East and Africa are emerging as a demand region through sovereign AI programs and GPU cluster deployments, although export control compliance adds another layer of complexity for procurement tied to sensitive destinations.

Competitive Landscape

The HBM3E market is one of the most concentrated segments of the semiconductor value chain, as SK Hynix, Samsung Electronics, and Micron Technology make up the qualified supply base for leading AI platforms. Competition in the HBM3E market is driven less by price and more by qualification timing, stack yield, thermal control, and access to advanced packaging. SK Hynix strengthened its position through world-first 12-layer HBM3E mass production in September 2024, which gave it a strong early edge in premium accelerator programs. That position became harder to challenge when NVIDIA and SK Hynix announced a multiyear technology partnership in June 2026 covering memory for several future product families. The HBM3E market, therefore, rewards suppliers that can convert early technical readiness into long-duration roadmap control.

Micron has used platform qualification as its main route to gain ground in the HBM3E market. In June 2025, Micron said its 36 GB 12-high HBM3E was designed into AMD Instinct MI350 Series solutions and qualified on multiple leading AI platforms. Micron also continued to reinforce its product positioning through technical messaging around HBM3E performance for AI workloads. Samsung has remained active by advancing next-generation memory samples, including its May 2026 announcement of industry-first HBM4E sample shipments. These actions show that the HBM3E market is being contested through platform access today and through preparation for denser follow-on products tomorrow.

The broader HBM3E market also depends on companies outside the memory fabrication industry. TSMC remains essential because CoWoS integration determines how quickly memory output becomes a deployable accelerator supply. SEMI's 2025 co-optimization work also showed that future competitiveness will depend on tighter coordination among thermal, electrical, and mechanical design across die, package, and system levels.[4]Seung Kang, “Co-Optimization Of Semiconductor Systems For AI Accelerators,” SEMI, semi.org This means the HBM3E market will continue to favor companies that can align memory design, packaging readiness, and customer qualification within the same product cycle. It also leaves little room for new entrants that cannot match incumbent suppliers across all of those execution points.

HBM3E Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SK Hynix shipped samples of its 12-layer HBM4E to major global customers, according to a June 17, 2026, company press release. The company stated that it leveraged mass production and supply expertise built during HBM3E production to deliver HBM4E samples on schedule and that it will work closely with partners to deliver mass production "in a timely manner."

- June 2026: Samsung Electronics officially confirmed the supply of its 12-layer HBM3E chips to AMD, integrated into the AMD Instinct MI350X and MI355X accelerator platforms launched at AMD's media event in June 2026. The confirmation marked Samsung's first publicly acknowledged HBM3E supply to a named AI chip customer following its NVIDIA 12-layer qualification in September 2025.

- June 2026: NVIDIA Corporation and SK Hynix announced a multiyear technology partnership on June 7, 2026, covering co-development of memory for NVIDIA Vera Rubin AI supercomputers, Vera CPUs, RTX Spark-powered PCs, and Jetson Thor robotic platforms. The agreement also includes the use of NVIDIA CUDA-X libraries and NVIDIA PhysicsNeMo to accelerate semiconductor chip design simulations at SK Hynix's fabs.

- January 2026: Microsoft Corporation launched Maia 200, a custom inference accelerator built on TSMC's 3 nm process, integrating 216 GB of HBM3E at 7.0 TB/s bandwidth and 272 MB of on-chip SRAM. Microsoft stated that Maia 200 delivers 30% better performance per dollar than the latest-generation hardware in its fleet at launch date.

- June 2025: Micron Technology announced the integration of its HBM3E 36 GB 12-high product into AMD Instinct MI350 Series solutions, marking dual-source qualification alongside Samsung and establishing Micron as a qualified supplier across multiple leading AI platforms. Micron's investor relations confirmed the product was "qualified on multiple leading AI platforms" as of this date.

Global HBM3E Market Report Scope

The HBM3E Market is Segmented by Memory Capacity Per Stack (Up to 24 GB, 24-36 GB, and Above 36 GB), Processor Interface (GPU, CPU, AI Accelerator, ASIC, FPGA, and Other Interfaces), Application (AI Training, AI Inference, High-Performance Computing (HPC) Servers, Networking and Telecommunications, Automotive and Edge AI, and Other Applications), End Use Industry (Cloud Service Providers, Enterprise IT, Telecommunications, Automotive, Aerospace and Defense, and Other End-user Industries), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Up to 24 GB |

| 24 to 36 GB |

| Above 36 GB |

| GPU |

| CPU |

| AI Accelerator and ASIC |

| FPGA |

| Other Interfaces |

| AI Training |

| AI Inference |

| High-Performance Computing (HPC) Servers |

| Networking and Telecommunications |

| Automotive and Edge AI |

| Other Applications |

| Cloud Service Providers |

| Enterprise IT |

| Telecommunications |

| Automotive |

| Aerospace and Defense |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Capacity Per Stack | Up to 24 GB | |

| 24 to 36 GB | ||

| Above 36 GB | ||

| By Processor Interface | GPU | |

| CPU | ||

| AI Accelerator and ASIC | ||

| FPGA | ||

| Other Interfaces | ||

| By Application | AI Training | |

| AI Inference | ||

| High-Performance Computing (HPC) Servers | ||

| Networking and Telecommunications | ||

| Automotive and Edge AI | ||

| Other Applications | ||

| By End Use Industry | Cloud Service Providers | |

| Enterprise IT | ||

| Telecommunications | ||

| Automotive | ||

| Aerospace and Defense | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the HBM3E space?

The HBM3E market size stands at USD 2.01 billion in 2026 and is forecast to reach USD 5.35 billion by 2031, at a 21.73% CAGR over 2026 to 2031.

Which memory capacity tier leads HBM3E demand?

The 24 to 36 GB segment led in 2025 with 71.78% of revenue, supported by strong adoption of 12-high 36 GB configurations in premium AI accelerators.

Which processor interface is growing fastest for HBM3E adoption?

AI accelerator and ASIC is the fastest-growing interface, with a projected 22.73% CAGR through 2031 as hyperscalers expand custom silicon programs.

Why is AI inference becoming more important for HBM3E suppliers?

AI inference is projected to grow at a 23.12% CAGR through 2031, broadening demand beyond training clusters and increasing the role of custom accelerator deployments.

Which end-user group still dominates purchases?

Cloud service providers remained the largest end-user group in 2025, accounting for 74.22% of revenue because hyperscalers continue to drive the biggest procurement programs.

Which region is growing fastest and which one leads revenue?

Asia-Pacific led revenue in 2025 with 61.36%, while North America is projected to grow the fastest at a 22.64% CAGR through 2031.

Page last updated on: