Hard Seltzer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

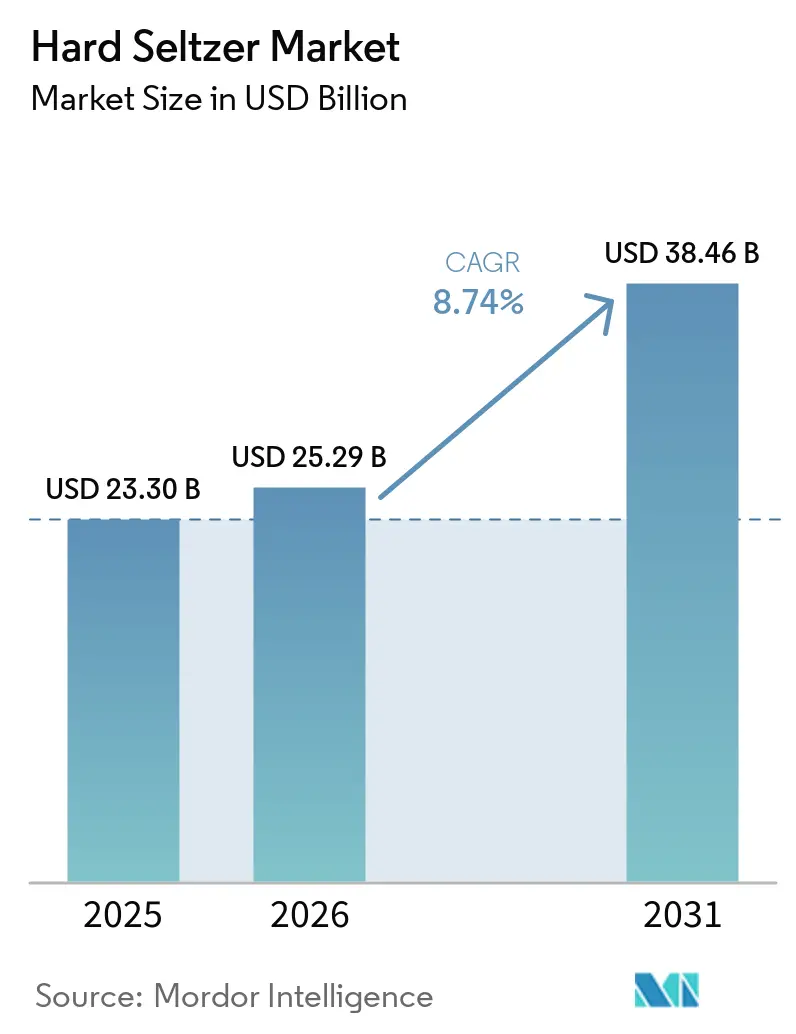

| Market Size (2026) | USD 25.29 Billion |

| Market Size (2031) | USD 38.46 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hard Seltzer Market Analysis by Mordor Intelligence

The hard seltzer market size was valued at USD 23.30 billion in 2025 and estimated to grow from USD 25.29 billion in 2026 to reach USD 38.46 billion by 2031, at a CAGR of 8.74% during the forecast period (2026-2031). The hard seltzer market is expanding because consumers are moving away from heavier, full-calorie beer toward lighter ready-to-drink options that align with moderation, calorie awareness, and simple ingredient expectations, a trend also reflected in academic work on healthier beverage choices. The hard seltzer market is also being reshaped by product moves that bring the category closer to cocktail occasions, with higher-ABV launches, variety packs, and spirits-based extensions widening its appeal across retail and social settings. Competitive behavior in the hard seltzer market now reflects that shift, as leading suppliers are using portfolio simplification, selective acquisitions, and innovation around flavor and alcohol base to defend shelf space and pricing power. The biggest near-term pressure on the hard seltzer market comes from spirits-based RTD cocktails, while tax classification changes in markets such as Australia and parts of Europe are making product-base strategy more important for margins and long-run positioning.

Key Report Takeaways

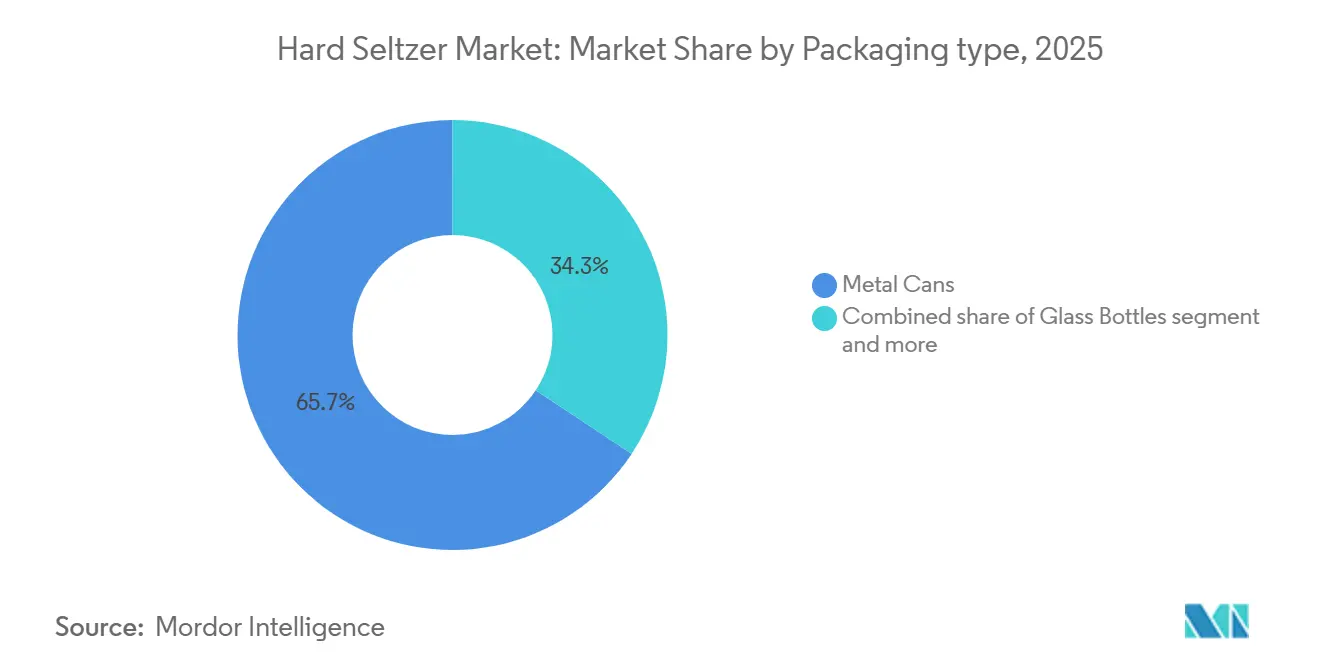

- By packaging type, metal cans accounted for 65.68% of the hard seltzer market in 2025 and are expected to remain the fastest-growing format, expanding at a CAGR of 8.87% during 2026-2031.

- By ABV content, the 1% to 5% ABV segment accounted for 58.28% of revenue in 2025, while the above-5% ABV tier is anticipated to expand at a CAGR of 9.28% during 2026-2031.

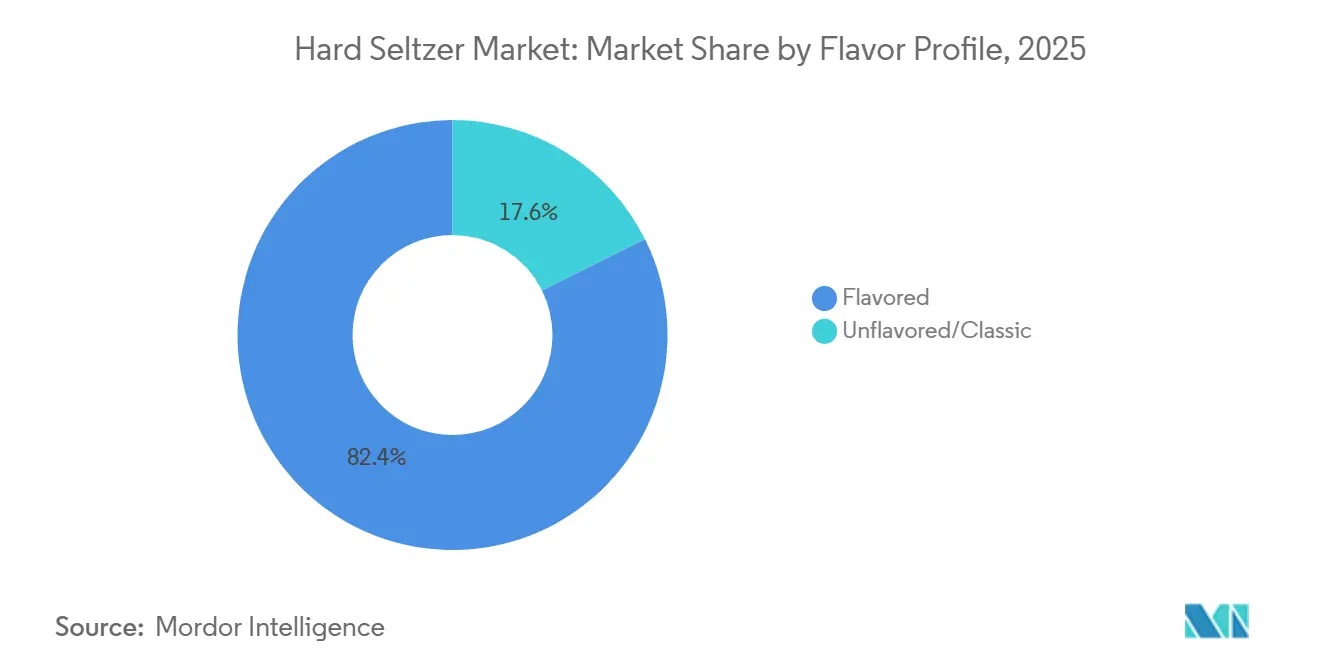

- By flavor profile, flavored products accounted for 82.36% of revenue in 2025, while unflavored or classic products are expected to grow at a CAGR of 9.12% during 2026-2031.

- By distribution channel, off-trade represented 76.42% of revenue in 2025, while on-trade is expected to record the highest growth at a CAGR of 9.78% during 2026-2031.

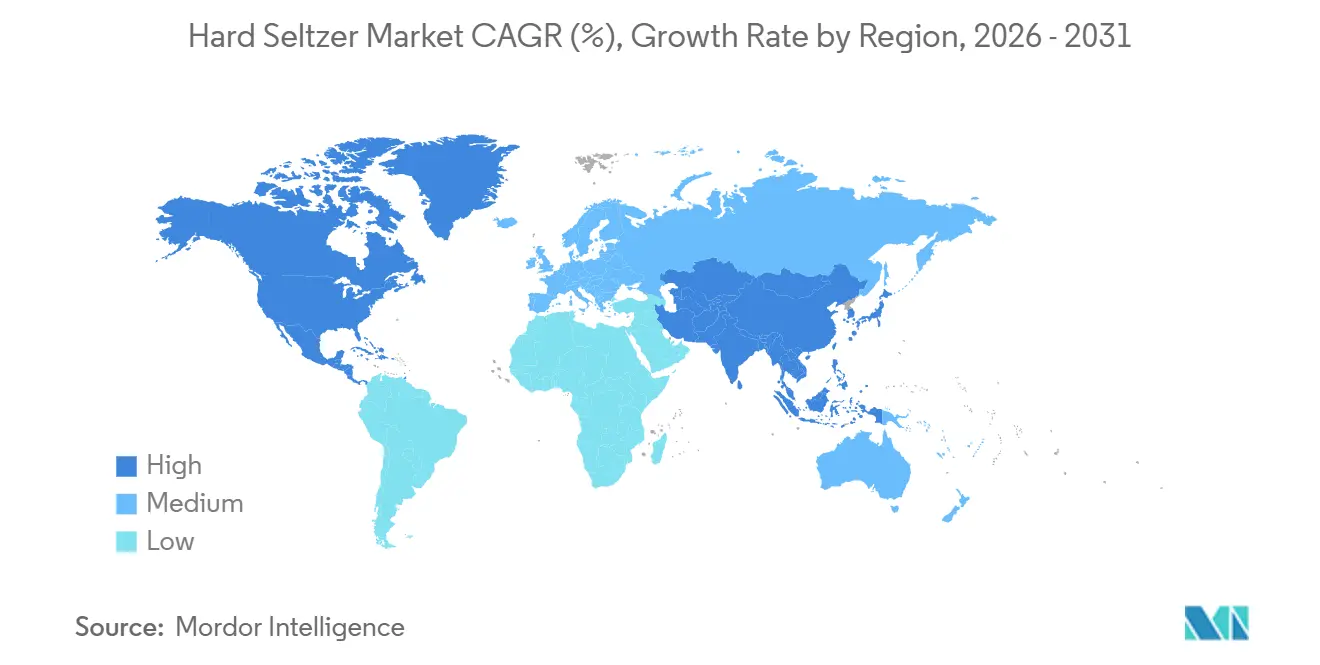

- By geography, North America held 48.74% of the hard seltzer market share in 2025, while Asia-Pacific is expected to grow at a CAGR of 9.56% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hard Seltzer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Better-for-you alcohol substitution | +2.1% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| RTD convenience and outdoor occasion fit | +1.8% | Global, especially North America, Europe, and Australia | Short term (≤ 2 years) |

| Flavor innovation and variety-pack premiumization | +1.6% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Spirits-based hard seltzer premiumization | +1.2% | North America, Australia, and the UK | Medium term (2-4 years) |

| Use of recyclable and lightweight aluminum cans aligning with sustainability | +0.9% | Global, with Europe and North America leading compliance requirements | Medium term (2-4 years) |

| Growing cocktail culture and Western lifestyle influence encouraging consumption | +0.7% | Asia-Pacific core, with spillover to South America and the Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Better-for-you alcohol substitution underpins long-run demand

Structural consumer reorientation toward health and transparency is the most durable demand driver the hard seltzer category commands. Yale School of Management research published in January 2024 found that consumers associate seltzer's hydration proximity with credible wellness claims, and that "skinny can" packaging creates measurable positive purchase intent among health-motivated shoppers, particularly among women, where the format functions as a proxy signal for caloric moderation. The harder-to-quantify second-order dynamic is that as GLP-1 medications normalize moderation behaviors across older Gen X and Millennial cohorts, hard seltzer transcends its original occasion profile, a summer refreshment, to become a lifestyle-aligned weekly consumption pattern displacing wine and craft beer on multiple occasions. Brands with on-label clarity around calorie count, sugar content, and ingredient sourcing will be best positioned to convert this secular moderation trend into sustained volume growth.

RTD convenience and outdoor occasion fit drive off-shelf velocity

Portability in aluminum cans generates purchase velocity across outdoor, sporting, and convenience occasions that neither glass-bottled wine nor draught beer can access effectively. Simon-Kucher's State of Beverage Report, surveying 3,000 US consumers in 2024, recorded a net spend intent increase of +16% for seltzers and sparkling beverages, the strongest positive trajectory of any tracked alcoholic or non-alcoholic category, with the growth disproportionately driven by consumers expanding on-the-go and sport/workout consumption occasions. A less obvious implication of this portability advantage is its seasonality disruption effect: the same can format that drives summer peaks is also enabling year-round penetration in cold-climate markets, where single-serve aluminum formats have displaced regional craft ciders as the default session alternative at indoor leisure and live-event venues. The portability tailwind also compounds with the breadth of off-trade distribution, since the format's presence across grocery, mass retail, warehouse clubs, and convenience channels means that impulse-triggered outdoor demand converts directly into incremental retail sales.

Flavor innovation and variety-pack premiumization sustain category relevance

Flavor differentiation has evolved from a growth accelerator into a category-survival mechanism, as basic fruit profiles approach saturation in the North American core. Brands are leveraging nostalgia, global flavor trends, and cocktail inspiration to re-engage existing buyers and recruit new cohorts. White Claw's ClawTails launch in April 2025, a 7% ABV line featuring Strawberry Cosmo, Mango Margarita, Blackberry Mojito, and Tropical Mai Tai, and its expansion to spirit-based formulations for Summer 2026 reflects the category's repositioning around cocktail ritual. High Noon's January 2025 rollout of 2 permanent variety packs, the Beach Pack (12-pack, MSRP USD 25.99) and Day Pack (8-pack, MSRP USD 19.99), incorporated Kiwi and Raspberry as new permanent flavors, illustrating how variety-pack architecture functions as a retail shelf-management tool that compels incremental purchase[1]Source: Spirit of Gallo, “High Noon Unveils Two New Permanent Variety Packs,” Spirit of Gallo, spiritofgallo.com. Tropical and margarita-inspired profiles are consistently outperforming the broader category: Topo Chico Hard Margarita Variety Pack generated USD 12.1 million in incremental US off-premise sales shortly after its 2025 launch, while pineapple held 6% of US RTD launches in 2024, and lemon-led variants dominated new introductions across 10 global markets in the same year.

Spirits-based hard seltzer premiumization expands the addressable market

The spirits-based reformulation of hard seltzer is a category re-segmentation that positions the format within the high-growth USD 4 billion spirits RTD corridor rather than the stagnating malt-based seltzer pool. According to DISCUS's 2025 Annual Economic Briefing, premixed cocktails and spirits RTDs grew 16.4% year-over-year in the United States to nearly USD 4 billion, while malt-based seltzers conceded 14 percentage points of category share over the same window[2]Source: Distilled Spirits Council of the United States, “Annual Economic Briefing 2025,” Distilled Spirits Council of the United States, distilledspirits.org. High Noon Sun Sips held 65.2% of the spirits-based seltzer sub-segment while posting 31.2% dollar growth in US off-premise, and NÜTRL scaled at +96% dollar growth in the same measurement period; spirit-based hard seltzer innovations rose from 22% of all new hard seltzer launches in 2021 to 40% by 2024. The strategic advantage is structural: spirits-based hard seltzers compete for spirits shelf space in most US state retail frameworks rather than beer shelf space, bypassing the same-store cannibalization dynamics that limit malt-based seltzer growth. Brands already commanding spirits credentials, through real vodka, tequila, or rum bases, can sustain retail price points 15-25% above equivalent malt-based products while leveraging the same convenience-format equity that built the category.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spirits-based RTD cocktail substitution | -2.2% | North America primary, with exposure in Australia and the UK | Short term (≤ 2 years) |

| Aluminum, CO2, and freight cost volatility | -1.5% | Global, with North America most exposed | Short term (≤ 2 years) |

| Fluctuations in excise duties and trade regulations | -0.8% | Europe, the UK, Australia, and Asia-Pacific | Medium term (2-4 years) |

| Social stigma and cultural resistance toward alcohol consumption | -0.5% | Middle East and Africa, South and Southeast Asia, Japan, and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

RTD cocktail substitution accelerates malt-seltzer attrition

The premium spirits RTD segment is proving to be the most disruptive competitive force the hard seltzer category has faced since its peak in 2021. US off-premise spirits-based RTDs grew 25.7% in 2025, contributing USD 650 million in revenue that largely offset broader spirits category declines, while the malt-based hard seltzer core contracted approximately 4.5% in US off-premise in the same year, according to the Boston Beer 2025 Annual Report filed with the SEC[3]Source: The Boston Beer Company, “Annual Report 2025,” U.S. Securities and Exchange Commission, sec.gov. The substitution dynamic is compounded by a state-level distribution asymmetry: spirits-based RTDs face regulatory barriers in states restricting liquor-aisle spirits sales, yet DISCUS identified eliminating these structural inequities as a 2026 federal and state policy priority, meaning the channel advantage that currently protects malt-based hard seltzer is time-limited. Consumer perception research cited by Beverage Industry in 2025 indicates that spirits-based RTDs are being increasingly experienced as authenticity upgrades by core hard seltzer drinkers, a substitution path that accelerates as brand loyalty to malt-based formats erodes and newer cohorts enter the category via spirits-adjacent entry points.

Aluminum, CO2, and freight cost volatility compress category-wide margins

Input cost volatility has become a structural margin headwind for hard seltzer producers, whose per-unit economics are tightly indexed to aluminum pricing. Iranian missile strikes on Emirates Global Aluminum (EGA) and Aluminum Bahrain (Alba) smelters on March 28, 2026, removed approximately 3.2 million metric tons of annual aluminum capacity from global supply, with EGA predicting a 12-month restart timeline. Combined with the US Section 232 tariff doubling from 25% to 50% in June 2025, which drove the US Midwest Premium to USD 0.60 per pound (a 190% spike from USD 0.21 per pound), aluminum prices reached USD 2.43 per pound in March 2026 and surpassed USD 2.70 per pound in early April, against a 15-year average of USD 1.15 per pound. Molson Coors disclosed USD 30 million in incremental aluminum costs in Q1 2026 versus the prior year and guided to continued inflation in Q2. Hard seltzer brands with limited domestic aluminum sourcing face the most acute pressure, while those, like AB InBev, that have vertically integrated into can manufacturing are materially better insulated. The secondary cost vector, CO2 and freight, interacts nonlinearly: higher aluminum prices incentivize lightweighting and can lead to downsizing, which in turn raises per-unit filling and logistics costs, creating a feedback loop that ultimately reaches the consumer via retail price inflation and SKU rationalization at the shelf.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Metal Cans Sustain Structural Dominance

Metal cans accounted for 65.68% of hard seltzer packaging revenue in 2025 and remain the category's defining format; their share is unlikely to erode materially through 2031, given their alignment with circular-economy frameworks and portability economics. The Aluminum Association and Can Manufacturers Institute reported in December 2024 that the average US aluminum beverage can contains 71% recycled content, 3× the 23% for glass, and that recycled aluminum can complete the can-to-new-can lifecycle in under 60 days. The International Aluminium Institute's Eunomia-commissioned study, released at COP30 in November 2025, found the global aluminum beverage can recycling rate at 74.8%, outpacing PET bottles (47%) and glass (42%), reinforcing the format's premium sustainability positioning at a time when EU CBAM compliance costs are rising.

Metal cans are forecast to grow at 8.87% CAGR through 2026-2031, a dynamic unusual in that the largest segment is also the fastest-growing, structurally limiting the addressable space for glass and flexible format innovators. Glass bottles retain a niche role in on-premise and premium gifting occasions in Europe, while pouches and multi-serve containers are gaining incremental traction in outdoor and event settings, particularly in markets where deposit-return scheme infrastructure raises the recycling cost calculus for competing formats.

By ABV Content: High-ABV Formats Redefine the Category's Growth Ceiling

The 1% to 5% ABV tier accounted for 58.28% of hard seltzer revenue in 2025, anchoring the category's foundational appeal among health-conscious, moderation-oriented drinkers seeking session-appropriate alternatives to full-strength beer and wine. The above-5% ABV tier, however, is expanding at a CAGR of 9.28%, the fastest of any ABV segment, as cocktail-adjacent, higher-indulgence products generate incremental trial from consumers unwilling to pay spirits-RTD price premiums but seeking comparable intensity. Boston Beer's 2025 Annual Report confirmed that Truly Unruly at 8% ABV ranked number one among high-ABV beer brand growth drivers in the US, and that its Lemonade variety pack expanded hard seltzer shelf space at national retail from its April 2025 launch.

White Claw Surge, also at 8% ABV, approached 10 million cases as of early 2025, per Mark Anthony Brands' president's public disclosures. The behavioral driver behind above-5% growth is the convergence of two distinct consumer types: cocktail-strength seekers who find standard-strength seltzers insufficiently satisfying, and value-oriented drinkers who maximize alcohol per dollar in an inflationary retail environment. Both groups are expanding faster than the category's historical core demographic.

By Flavor Profile: Flavored Varieties Dominate While Unflavored Accelerates Unexpectedly

Flavored hard seltzers dominated with 82.36% of market value in 2025, establishing the sub-category as the commercial engine of the hard seltzer segment. Within flavored variants, the innovation frontier has shifted from basic citrus profiles toward tropical, botanical, and cocktail-inspired formulations: Global Drinks Intel's category intelligence recorded that pineapple held 6% of US RTD launches in 2024, while tropical and margarita-inspired profiles, including Topo Chico Hard Margarita Variety Pack (+USD 12.1 million in incremental off-premise sales) and Simply Spiked Tropical Variety Pack (+USD 11 million in incremental sales), emerged as 2025 growth drivers.

The counter-intuitive structural signal is that Unflavored/Classic hard seltzer is forecast to grow at 9.12% CAGR through 2026-2031, the fastest of any flavor segment. A sub-cohort of highly health-motivated consumers is actively seeking ingredient-transparent plain carbonated bases, particularly as regulatory attention on natural flavor additives intensifies. A new format class, "hard refreshers" using sea-salt or coconut-water bases, is beginning to bridge the unflavored-flavored boundary, capturing functional wellness messaging without the sugar associations of flavored variants. Beverages in this niche attracted measurable incremental off-premise dollar gains in 2025, per Beverage Industry trade data.

By Distribution Channel: Off-Trade Anchors Revenue While On-Trade Builds Brand Equity

Off-trade channels retained a commanding 76.42% share of hard seltzer revenue in 2025, reflecting the category's structural reliance on packaged retail velocity in grocery, convenience, and warehouse club formats. The on-trade channel is forecast to grow at 9.78% CAGR through 2026-2031, the fastest distribution growth vector, reflecting that bar and restaurant placement has evolved from a secondary objective to a strategic brand equity investment. Simon-Kucher's 2024 US consumer survey confirmed that on-premise discovery occasions generate disproportionate brand affinity and trading-up behavior, and Boston Beer's Q3 2025 earnings transcript noted that Sun Cruiser became the leading RTD spirits brand in on-premise bars and restaurants measured evidence that category leaders are actively routing premium innovation through on-trade first.

Within off-trade, specialty liquor stores perform a premium positioning function: San Juan Seltzer commands the highest average case price among the top-20 US hard seltzer brands at USD 53.94, achieved in part through specialty channel exclusivity. Approximately half of US on-premise accounts currently carry a hard seltzer SKU, per Mark Anthony Brands' 2025 disclosures, leaving substantial white space in stadium venues, concert arenas, and hotel bars where RTD cocktail competitors encounter less category competition.

Geography Analysis

North America held 48.74% of global revenue in 2025, while Asia-Pacific is projected to advance at a 9.56% CAGR through 2031, making the regional profile of the hard seltzer market clear from the start. North America remains the largest base because its retail system is well-suited to canned RTDs, its off-premise network is deep, and the category already has broad consumer familiarity. The United States continues to shape most regional performance, and brand strategy there is increasingly focused on higher-ABV products, cocktail-style flavors, and spirits-adjacent extensions that can defend shelf space against faster-growing RTD substitutes. This also means the hard seltzer market in North America is moving from early category creation to portfolio management, where success depends less on novelty and more on pack architecture, pricing discipline, and route-to-market strength. Canada and Mexico add support to the regional base, but the core strategic story is still U.S.-led.

Asia-Pacific is the fastest-growing region because urbanization, rising disposable income, and Western drinking influence are helping create a larger audience for lighter premixed alcohol. Australia stands out not only for its demand potential but also for its regulation, as the ATO’s draft ruling on hard seltzer classification showed how tax treatment can materially affect product economics and future formulation choices. Across Japan, South Korea, India, and Australia, the hard seltzer market is gaining relevance in modern retail, social occasions, and premium convenience channels rather than through traditional beer routines alone. That gives the region a different growth pattern from North America, with more room for imported brand building, local flavor adaptation, and category education.

Europe remains smaller in absolute terms, but it holds strategic value because premium positioning is stronger there and regulatory classification can reshape the competitive field. The UK’s Finance Act 2025 revised alcohol duty treatment for spirits and other fermented products, while France and Germany continue to illustrate how product classification can alter the cost base for hard seltzers and related premix products. South America is still early in penetration, yet AB InBev reported strong Beyond Beer momentum in Brazil and triple-digit growth in Peru during Q1 2026, which suggests that the hard seltzer market can still open new pockets of demand in the region. The Middle East and Africa remain the most constrained geography because legal and cultural barriers limit alcohol demand in many countries, although South Africa remains a more practical entry point for selective RTD expansion. Taken together, the hard seltzer market is moving from a North America-heavy category into a broader regional story, but that expansion will not be uniform and will depend heavily on tax structure, channel fit, and local drinking culture.

Competitive Landscape

The hard seltzer market remains moderately concentrated, with a small number of large beverage groups shaping category visibility, shelf access, and product direction. White Claw remains the most recognizable name in the category through Mark Anthony Group, while Boston Beer, AB InBev, Molson Coors, and other multi-brand operators continue to contest share through adjacent RTD and flavored alcohol portfolios. This structure gives larger players clear advantages in distribution, marketing, and innovation funding, yet it still leaves room for smaller labels where flavor, channel, or local positioning is distinct. In other words, the hard seltzer market is concentrated enough to reward scale, but not so concentrated that challenger brands lose all room to grow.

Company strategy since 2025 shows how competition is changing. Boston Beer used its 2025 portfolio focus to concentrate behind Truly Unruly and other brands with better momentum, a move that aligned investment with higher-ABV and more differentiated demand pockets. White Claw launched ClawTails in 2025 to bring cocktail-style flavors and a 7% ABV to the category, signaling a deliberate move toward more indulgent drinking occasions. Mark Anthony Group then announced plans to acquire The Finnish Long Drink in April 2026, which widened its exposure to spirits-based RTDs beyond its legacy White Claw base. AB InBev also completed the acquisition of 85% of BeatBox Beverages in February 2026 and reported 37% Beyond Beer revenue growth in Q1 2026, showing a broad multi-format approach to future category competition.

The main battleground in the hard seltzer market is no longer simple entry-level flavor novelty. Competition now turns on alcohol base choice, ABV laddering, premium flavor direction, can format, and the ability to adapt quickly to shifting regulation. Larger companies are better placed when packaging costs rise or when excise treatment changes because they can reformulate, reprice, or redirect distribution with less disruption. Smaller brands still have openings, especially where local provenance, premium menus, or focused retail partnerships can matter more than national scale. The hard seltzer market is therefore likely to reward companies that can balance brand familiarity with product flexibility, because the category is now competing on identity as much as on refreshment.

Hard Seltzer Industry Leaders

Mark Anthony Brands

The Boston Beer Company

Diageo PLC

Molson Coors Beverage Company

Anheuser-Busch InBev

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AB InBev designated its NÜTRL Vodka Seltzer as the official hard seltzer sponsor of the 2026 FIFA World Cup (June–July, hosted across Canada, Mexico, and the US), with planned in-stadium activations and a national consumer sweepstake featuring match tickets. The sponsorship elevates NÜTRL's brand visibility in the three largest North American markets simultaneously, building on the brand's 96% dollar growth trajectory.

- April 2026: White Claw launched a spirit-based Clawtails line for Summer 2026, featuring Mango Margarita (tequila-based), Blackberry Mojito (rum-based), Strawberry Cosmo (vodka-based), and Tropical Mai Tai (rum-based) at 7% ABV, signaling the brand's strategic pivot from malt-based seltzer toward cocktail-positioned, spirits-based formulations.

- February 2026: AB InBev completed the acquisition of 85% of BeatBox Beverages (a high-ABV, Tetra Pak-packaged RTD brand) for approximately USD 490 million, extending its RTD portfolio into the above-7% ABV tier and gaining access to Gen Z's nostalgia-driven high-ABV purchasing behavior.

- April 2025: White Claw launched ClawTails, a malt-based 7% ABV cocktail-inspired line (Strawberry Cosmo, Mango Margarita, Blackberry Mojito, Tropical Mai Tai) developed using the Cold Wave Filtered process, rolling out in 12-oz variety 12-packs and 19.2-oz single cans; ClawTails achieved USD 23.7 million in NIQ-tracked off-premise sales across 2025.

Global Hard Seltzer Market Report Scope

Hard seltzer is an alcoholic beverage made from carbonated water, alcohol, and flavorings, typically offering a lighter taste and lower calories than traditional alcoholic drinks. The hard seltzer market is segmented by packaging type, ABV content, flavor profile, distribution channel, and geography. By packaging type, the market includes metal cans, glass bottles, and other packaging formats such as pouches, kegs, and multi-serve containers. Based on ABV content, the market is categorized into 1% to 5% ABV and above 5% ABV. By flavor profile, the market includes unflavored/classic and flavored variants, with flavored products further segmented into citrus, berry, tropical, botanical, herb, and other flavors. Based on distribution channel, the market is divided into on-trade and off-trade, with the off-trade segment further comprising specialty liquor stores and other off-trade channels. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD billion).

| Metal Cans |

| Glass Bottles |

| Other Packaging (Pouches, Kegs, Multi-Serve Containers) |

| 1% to 5% ABV |

| Above 5% ABV |

| Unflavored/Classic | |

| Flavored | Citrus |

| Berry | |

| Tropical | |

| Botanical & Herb | |

| Others |

| On-Trade | |

| Off-Trade | Specialty Liquor Stores |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Packaging Type | Metal Cans | |

| Glass Bottles | ||

| Other Packaging (Pouches, Kegs, Multi-Serve Containers) | ||

| By ABV Content | 1% to 5% ABV | |

| Above 5% ABV | ||

| By Flavor Profile | Unflavored/Classic | |

| Flavored | Citrus | |

| Berry | ||

| Tropical | ||

| Botanical & Herb | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty Liquor Stores | |

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in hard seltzer demand through 2031?

Growth is being supported by a move toward lighter alcohol choices, wider RTD adoption, and continued flavor and pack innovation, with the category forecast to reach USD 38.46 billion by 2031 at an 8.74% CAGR.

Which region leads current revenue and which one is growing fastest?

North America led with 48.74% of revenue in 2025, while Asia-Pacific is projected to record the fastest growth at a 9.56% CAGR through 2031.

Why are metal cans so important in this category?

Metal cans held 65.68% of packaging revenue in 2025 and remain dominant because they combine portability, high recycled content, and strong fit with off-trade and event-driven consumption.

How important is on-trade compared with off-trade sales?

Off-trade remained the main revenue base with 76.42% share in 2025, but on-trade is expected to grow faster at a 9.78% CAGR because it helps build trial and brand visibility.

Page last updated on: