Hadron Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.67 Billion |

| Growth Rate (2026 - 2031) | 8.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hadron Therapy Market Analysis by Mordor Intelligence

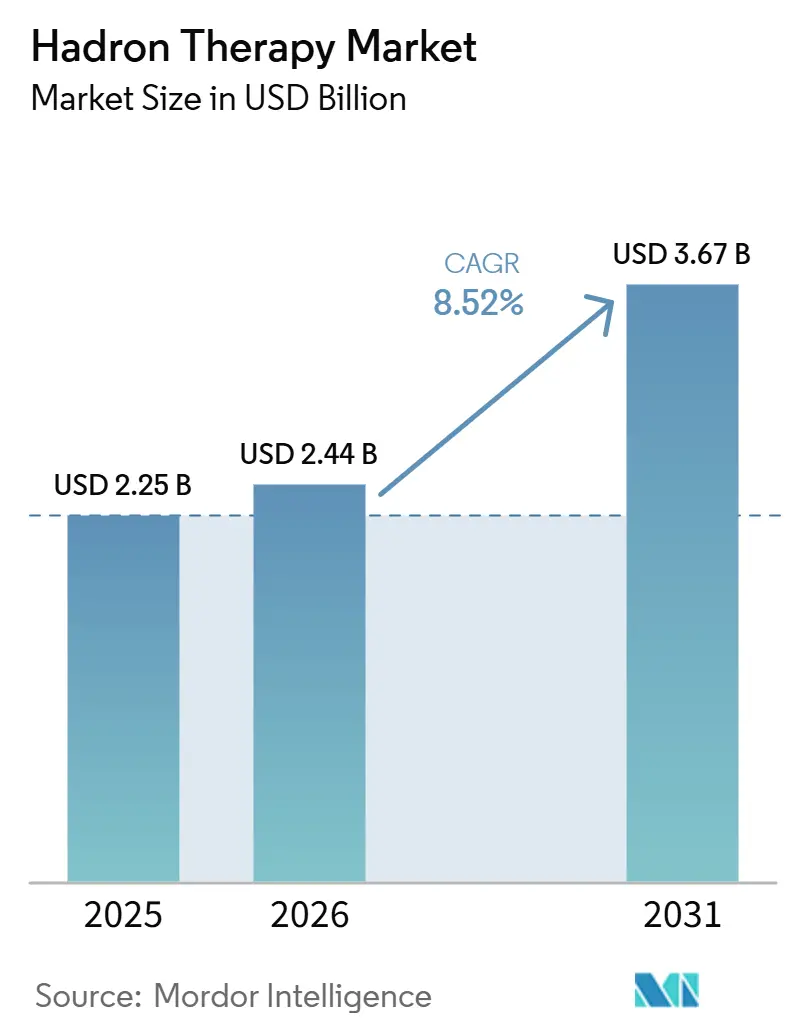

The Hadron Therapy Market size was valued at USD 2.25 billion in 2025 and is estimated to grow from USD 2.44 billion in 2026 to reach USD 3.67 billion by 2031, at a CAGR of 8.52% during the forecast period (2026-2031).

The hadron therapy market continues to expand because proton therapy remains the main clinical platform, with a broad treatment base and an installed network of more than 120 operational centers worldwide by the end of 2024. Treatment delivery standards are also moving higher, as pencil beam scanning now anchors most new installations and shifts procurement toward intensity-modulated proton therapy that can manage moving targets within a 5% dose inhomogeneity threshold. The hadron therapy market is also benefiting from compact single-room platforms, because they shorten construction timelines and lower the entry barrier for health systems that could not support older multi-room designs. Competitive positioning is increasingly tied to service depth, upgrade pathways, and the ability to support new treatment approaches such as FLASH, rather than system hardware alone. The hadron therapy market still faces clear access limits in reimbursement, capital intensity, and workforce readiness, yet demand remains supported by pediatric care, re-irradiation use cases, and the need for more precise treatment in radioresistant disease.

Key Report Takeaways

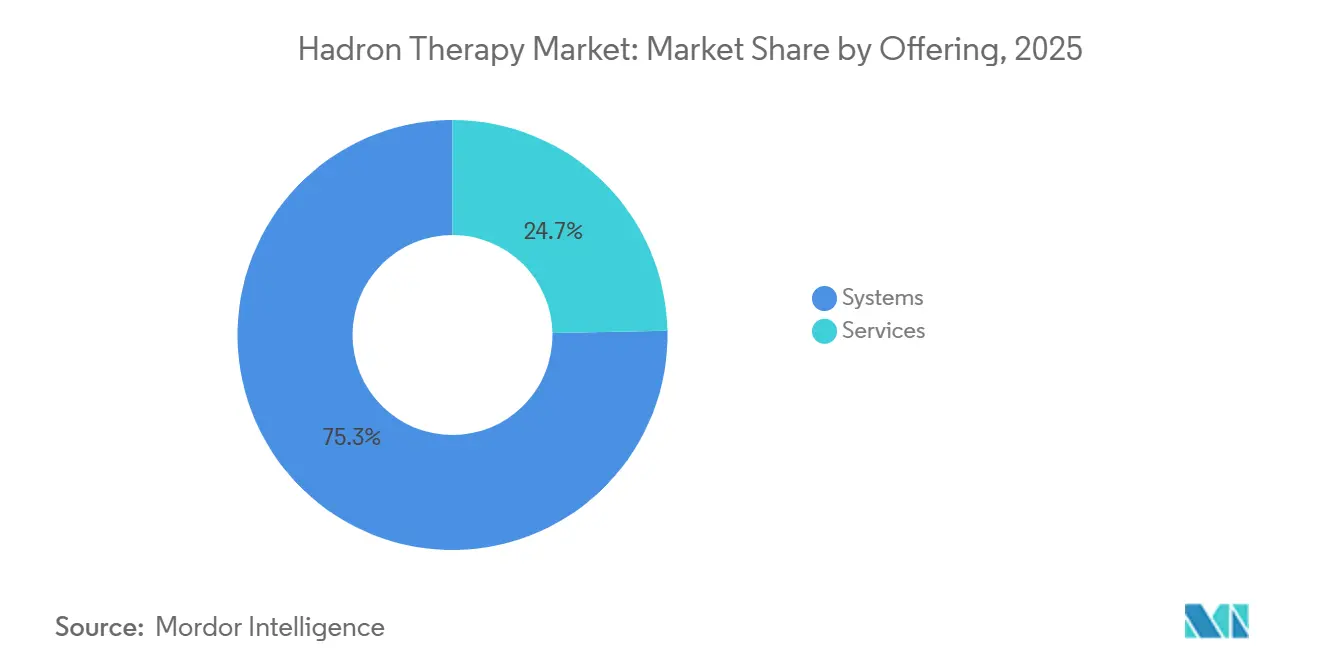

- By offering, systems led with 75.31% revenue share in 2025, while services are projected to expand at 10.38% CAGR through 2031.

- By system configuration, multi-room facilities held 56.24% share in 2025, while single-room facilities are forecast to grow at 11.52% CAGR through 2031.

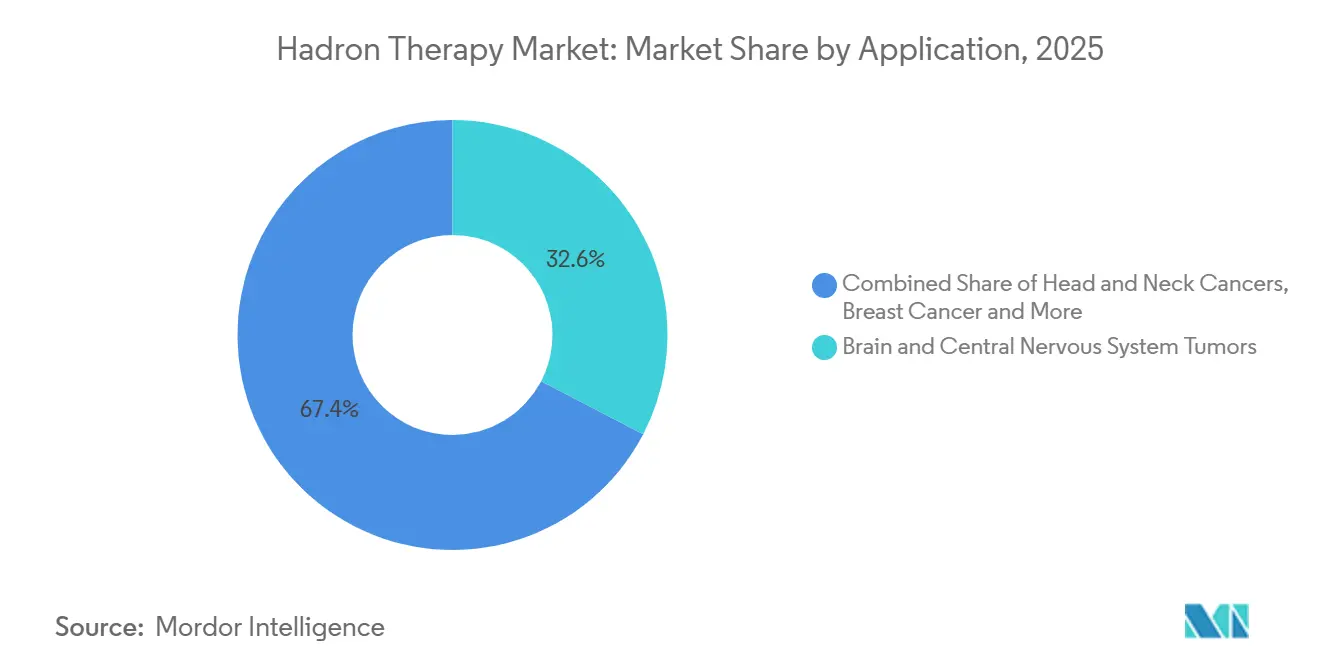

- By application, brain and central nervous system tumors accounted for 32.64% share in 2025, while head and neck cancers are projected to advance at 11.62% CAGR through 2031.

- By end user, hospitals held 50.26% share in 2025, while cancer treatment centers are projected to grow at 10.95% CAGR through 2031.

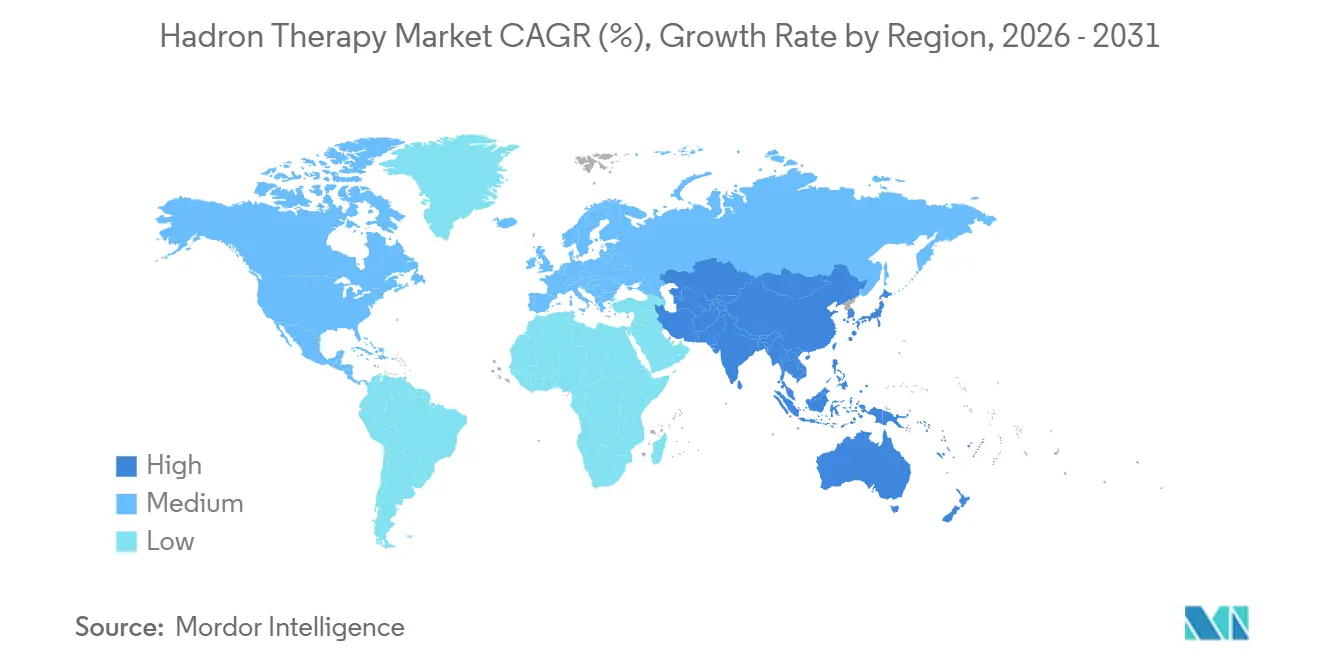

- By geography, North America retained 38.61% share in 2025, while Asia-Pacific is projected to expand at 10.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hadron Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference for Precise Tumor Targeting in Radioresistant Cancers | +2.1% | Global, with concentration in North America, Europe, and Japan | Long term (≥ 4 years) |

| Expanding Proton Therapy Installations in Oncology Centers | +2.0% | Global, accelerated in APAC and North America | Medium term (2-4 years) |

| Increasing Clinical Adoption in Pediatric and Re-Irradiation Cases | +1.1% | North America and Europe, with spill-over to APAC | Medium term (2-4 years) |

| Technology Upgrades in Compact Accelerators and Beam Delivery Systems | +1.3% | Global, with early gains in North America, China, and Japan | Short term (≤ 2 years) |

| Insurance Coverage Expansion for Selected Indications | +0.9% | North America, Japan, with emerging impact in Europe and South Korea | Medium term (2-4 years) |

| Growing Demand for Multidisciplinary Cancer Care Infrastructure | +0.8% | Global, especially GCC, China, and South and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Precise Tumor Targeting in Radioresistant Cancers

Radioresistant tumors remain a major demand anchor in the hadron therapy market because photon-based treatment often struggles to deliver durable control without damaging nearby tissue. Carbon ion therapy has shown a relative biological effectiveness of 2 to 3 versus X-rays, which supports its use in chordomas, chondrosarcomas, uveal melanoma, and other difficult histologies. Clinical practice at the Heidelberg Ion Beam Therapy Center also shows how this advantage translates into real use, with more than 7,300 patients treated since 2009 and strong experience in skull-base chordomas and salivary gland carcinomas that are difficult to manage with photon platforms[1]Universitätsklinikum Heidelberg, “Radiobiology Contributions and Perspectives in Hadron Therapy, With a Focus on Carbon Ions,” FAU CRIS, cris.fau.de. Capacity is still scarce on the heavy-ion side, because fewer than 20 centers globally provide carbon ion treatment, and that supply gap keeps new project interest active in the United States, China, and GCC markets. The hadron therapy market therefore gains from a treatment need that is clinically defined, geographically under-served, and hard to substitute with standard radiation modalities. The 2025 Hadrontherapy for Life white paper also points to a more coordinated global network, which should strengthen referral patterns and protocol consistency over time.

Expanding Proton Therapy Installations in Oncology Centers

The hadron therapy market is moving into a broader buyer base because the global installed base of proton centers has already passed 120 and more facilities remain in planning or construction. Compact single-room systems are central to this shift, since they allow health systems to enter proton therapy without the full cost and footprint of older multi-room programs. This change is visible in current project activity, where IBA has signed new contracts across North America, Portugal, Taiwan, and Brazil, while Mevion has moved a compact unit into clinical use at Stanford Medicine. Vendors are also structuring longer service relationships, as shown by Hitachi’s 20-year private finance arrangement with the University of Tsukuba, which shifts value creation beyond one-time equipment sales. Construction timelines are shortening from the previous 3 to 5 years toward 1 to 2 years for compact systems, and that improves the odds that the project pipeline converts into revenue during the forecast period. In the hadron therapy market, faster commissioning also matters because it reduces the period between capital approval and patient treatment.

Increasing Clinical Adoption in Pediatric and Re-Irradiation Cases

Pediatric treatment remains one of the strongest clinical foundations for the hadron therapy market because the long-term toxicity burden of photon radiotherapy is well established in younger patients. A 2025 study in Pediatric Blood & Cancer found that IMPT craniospinal irradiation reduced mean esophageal dose to 4.73 Gy from 9.06 Gy with IMRT and reduced hippocampal mean dose to 14.7 Gy from 17.2 Gy with VMAT. Those reductions matter in practice because they support lower late toxicity risk in children who may live for decades after treatment. Re-irradiation is also expanding as a meaningful use case, since survivors who previously received radiation are returning with local recurrence and need a second treatment option that avoids severe normal tissue exposure. Registry evidence from the KiProReg study in Germany confirmed the feasibility of proton re-irradiation in relapsed high-risk neuroblastoma without high-grade acute toxicity, and a 2025 paper in the International Journal of Particle Therapy also documented the feasibility of proton re-irradiation for recurrent pediatric brain tumors near the brainstem. The hadron therapy market benefits from this pattern because each expansion in survivorship creates a larger future pool of re-irradiation candidates.

Technology Upgrades in Compact Accelerators and Beam Delivery Systems

Technology progress is widening the clinical and commercial reach of the hadron therapy market through smaller accelerators, higher dose-rate capability, and more efficient beam delivery. Research teams in China have developed compact superconducting cyclotrons with a 2.2 meter diameter and a weight below 50 tons, which is far smaller than earlier synchrotron installations. Brookhaven work reported in 2025 also showed proton beam transport across the full 50 MeV to 250 MeV range through a nine-magnet array, which supports future racetrack accelerator designs that could fit into normal hospital settings. Beam delivery is also improving, and Siemens Healthineers secured a U.S. patent in December 2025 for methods that improve the placement of energy layers and spots of proton beams in target regions. FLASH is now part of the upgrade cycle as well, with clinical and preclinical work showing very high dose-rate delivery can be integrated into advanced particle therapy pathways[2]“Pioneering Proton FLASH-Minibeam Therapy, First Experimental Demonstration of Feasibility on a Clinical Proton System,” ASTRO Annual Meeting 2025, am25.astro.org. In the hadron therapy market, these upgrades matter because they improve throughput, expand installation options, and support premium system differentiation without changing the core treatment rationale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity of Facility Build-Out and Equipment Procurement | -1.8% | Global, most acute in LMICs, MEA, and smaller European markets | Long term (≥ 4 years) |

| Limited Reimbursement for Broad Indication Coverage | -1.2% | Global, most pronounced in middle-income countries and U.S. Medicare Advantage segments | Medium term (2-4 years) |

| Shortage of Trained Clinical and Physics Workforce | -0.7% | Global, concentrated in emerging APAC markets, MEA, and South America | Medium term (2-4 years) |

| Long Validation Cycles for Clinical Evidence in New Indications | -0.5% | Global, particularly relevant for gastrointestinal, lung, and gynecological indications in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of Facility Build-Out and Equipment Procurement

Capital intensity remains one of the clearest barriers in the hadron therapy market because full proton programs usually require USD 150.00 million to USD 200.00 million, while carbon ion facilities often exceed USD 300.00 million in project value. Even compact single-room systems still require a high upfront commitment, and users must also absorb construction, commissioning, and integration costs before clinical revenue begins. The burden does not end at installation, because service contracts, imaging links, replacement cycles, and specialist staffing keep annual operating costs high for large centers. Hitachi’s private finance structure with the University of Tsukuba shows that vendors can soften the upfront burden, but such models still depend on financially strong institutions and long service commitments. This is why the hadron therapy market remains concentrated in well-capitalized health systems, while large parts of Latin America, sub-Saharan Africa, and lower-income Asian markets still face long adoption timelines. The capital issue also shapes vendor strategy, since compact designs and phased entry models now matter almost as much as beam performance.

Limited Reimbursement for Broad Indication Coverage

Reimbursement remains uneven in the hadron therapy market even where clinical support is strong, and this directly affects patient access and project economics. CMS still applies Coverage with Evidence Development to a range of particle therapy indications, which means reimbursement can depend on trial or registry participation rather than routine approval. The National Association for Proton Therapy reported in 2025 that Medicare Advantage approvals could vary sharply by disease area, with some central nervous system cases approved at much lower rates than thoracic indications[3]National Association for Proton Therapy, “Prior Authorization for Proton Therapy in 2025, What Providers Need to Know,” National Association for Proton Therapy, proton-therapy.org. Japan presents a more supportive model because public coverage had expanded to 9 defined particle therapy indications by April 2025, but Europe still shows national variation that limits equal access across otherwise advanced healthcare systems. The hadron therapy market therefore grows faster where reimbursement policy aligns with referral behavior and slower where each case still faces high administrative friction. This gap also delays investment decisions because developers need dependable patient throughput before committing to long-lived assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Proton Therapy Systems Anchor Revenue; Services Outpace Equipment Growth

Systems held 75.31% of hadron therapy market share in 2025, which shows how strongly revenue still centers on the core treatment platform rather than on adjunct services or heavy-ion equipment. This position reflects decades of clinical use, broader indication coverage, and the fact that most new facility starts outside specialized heavy-ion centers still choose proton systems first. In the hadron therapy industry, that installed base also creates a replacement and upgrade cycle that keeps system vendors closely tied to existing customers. Varian and IBA continue to benefit from this pattern because treatment centers are not only buying new capacity, they are also refreshing older capability with more efficient delivery, imaging, and planning support. Heavy-ion systems remain a smaller part of the hadron therapy market, yet they carry high clinical value because they serve radioresistant disease settings that proton therapy cannot fully match. Japan’s National Institutes for Quantum Science and Technology is still advancing the next-generation Quantum Knife platform, which shows that the heavy-ion segment remains active even if it is far more selective than the proton segment.

Services are projected to grow at 10.38% CAGR through 2031, making them the fastest-moving part of this segmentation in the hadron therapy market. That pace reflects a structural shift in vendor economics, because operations support, maintenance, training, and long-duration lifecycle contracts now carry more strategic value than before. Hitachi’s long-term financing and service structure at the University of Tsukuba illustrates how suppliers are turning the installed base into recurring revenue rather than relying only on large one-time equipment sales. IBA’s Proton Therapy Academy supports the same direction, since training has become part of market access in a field where technical and clinical staffing are still limited. In the hadron therapy industry, service quality is now closely linked to customer retention because centers need uptime, workflow support, and future upgrade readiness over multi-decade operating periods. This is why the hadron therapy market is gradually shifting from a pure equipment model to a blended equipment and platform support model.

By System Configuration: Single-Room Platforms Redefine the Market's Physical Boundaries

Multi-room facilities held 56.24% of the configuration market in 2025, which keeps them as the largest installed format in the hadron therapy market. Their position is tied to large academic cancer centers that need multiple gantries, high patient throughput, and research-grade flexibility for complex treatment protocols. Shared accelerator infrastructure still makes economic sense for institutions that treat large patient volumes and can keep utilization high across several rooms. European heavy-ion centers such as Heidelberg and Marburg also show why large formats continue to matter, because multi-ion capability and specialized workflows still need broader physical infrastructure. In the hadron therapy market, multi-room systems therefore remain the reference model for flagship centers, national programs, and institutions that combine treatment with long-run research activity.

Single-room facilities are forecast to grow at 11.52% CAGR through 2031, making them the faster-moving configuration in the hadron therapy market. This growth reflects not only lower capital needs, but also the practical fact that compact systems can use existing clinical space more effectively than older designs. Mevion’s S250-FIT reached its first clinical treatment at Stanford Medicine in June 2026, and that installation used a renovated conventional LINAC vault rather than new bunker construction. P-Cure also completed a LINAC vault conversion at Hadassah Medical Center, which reinforces the idea that proton therapy can now fit into spaces that once served conventional radiotherapy. Health systems are increasingly viewing single-room sites as phased market entry rather than as a lower-end substitute, because modular upgrades can later support newer delivery modes within the same footprint. The hadron therapy market is therefore expanding its physical boundaries, since compact systems allow treatment access to move beyond the small set of institutions that could once fund purpose-built complexes.

By Application: Brain and CNS Dominates; Head and Neck Accelerates on Re-Irradiation Demand

Brain and central nervous system tumors accounted for 32.64% of the hadron therapy market size in 2025, making them the largest application in the hadron therapy market. This leadership reflects long clinical experience in skull-base disease, pediatric medulloblastoma, and other settings where sparing nearby normal tissue is especially important. Decades of published outcomes have made this group one of the most established referral channels for proton and particle therapy. The stability of this application also matters commercially because it supports utilization at both mature academic centers and newer clinical programs. In the hadron therapy market, CNS cases remain a dependable volume base because they fit the modality’s central value proposition of precise dose delivery near sensitive structures. Breast and prostate indications also remain relevant because the modality’s appeal there is tied less to raw tumor control and more to long-term toxicity reduction, especially in patients with long expected survival.

Head and neck cancers are projected to grow at 11.62% CAGR through 2031, making them the fastest-growing application in the hadron therapy market. Growth in this segment is closely linked to re-irradiation, where conventional photon retreatment can expose critical tissues to unacceptable cumulative dose. The treatment rationale is also strengthened by anatomy, because many head and neck cases sit close to structures that benefit directly from the Bragg peak’s steep dose fall-off. IBA’s ConformalFLASH human feasibility study now focuses on head and neck re-irradiation, which shows how next-generation clinical development is already aligning with this demand pocket. Gastrointestinal tumors are another important growth frontier, and Japan’s public insurance coverage across several gastrointestinal indications gives that country an important role in validating larger-scale use. The hadron therapy market is therefore gaining momentum in applications where dose precision is not only desirable but often decisive for treatment feasibility after prior radiation or in anatomically constrained sites.

By End User: Hospitals Retain Scale Advantage; Cancer Treatment Centers Accelerate

Hospitals held 50.26% share in 2025, which keeps them as the largest end-user group in the hadron therapy market. Their scale comes from existing oncology infrastructure, established referral networks, and the ability to support advanced imaging, surgery, and systemic therapy under one institutional structure. Hospitals also remain the main home for older multi-room programs, which still account for a large portion of global treatment capacity. Current upgrade activity supports this position, with large health systems such as MD Anderson continuing to reinvest in proton infrastructure through new contracts with established suppliers. In the hadron therapy industry, hospitals still provide the broadest deployment base because they can spread capital and staffing commitments across a wider clinical portfolio. Academic and research institutes remain smaller in number, yet they are strategically important because they host investigational work in FLASH, adaptive treatment, and multi-ion protocols that later shape wider commercial adoption.

Cancer treatment centers are projected to grow at 10.95% CAGR through 2031, which makes them the faster-growing end-user category in the hadron therapy market. Their appeal lies in focused operational design, because they can build staffing, workflow, and patient throughput around particle therapy rather than balancing many unrelated service lines. This model becomes more practical as compact systems reduce the physical and financial burden of entry. Dedicated centers also have a clearer incentive to optimize utilization, since proton therapy is not one department among many but a central revenue and care platform. The hadron therapy market is likely to see more of these specialized sites in regions where referral demand exists but large academic expansions are slower. Smaller end-user groups, including research-oriented facilities and defense-linked medical programs, still contribute visible project activity and show that procurement demand remains geographically diverse.

Geography Analysis

North America retained 38.61% of hadron therapy market share in 2025, which kept it as the largest regional contributor in the hadron therapy market. The region’s lead comes from its dense concentration of academic cancer centers, mature referral channels, and reimbursement structures that support selected pediatric, skull-base, and head and neck indications. The United States remains the core driver because many of the region’s flagship programs are now in modernization mode rather than initial build-out mode. Current projects at major institutions, including MD Anderson, show that replacement demand is still a meaningful revenue source for suppliers with deep installed bases. Reimbursement still limits wider use in the hadron therapy market, yet policy shifts and payer scrutiny are now shaping clinical mix and utilization as much as raw installation counts.

Asia-Pacific is projected to grow at 10.65% CAGR through 2031, making it the fastest-growing region in the hadron therapy market. China and Japan drive that pace, though they do so from different starting points. Japan already has a dense and clinically mature ecosystem, with 18 proton and 6 carbon ion facilities as of 2024, and that installed base treated around 6,000 particle therapy patients per year. Public insurance support is also broader there, with 9 defined indications under coverage by April 2025, which helps sustain referral flow and utilization. China is pushing the hadron therapy market forward through aggressive capacity build-out, with more than 30 proton and heavy-ion facilities either operational or under construction by 2026 and an approved pipeline under the national five-year plan. This combination of mature Japanese demand and fast Chinese expansion gives Asia-Pacific the strongest volume growth path in the forecast period.

Europe remains a major pillar of the hadron therapy market because it combines established proton programs with some of the world’s most important heavy-ion centers. Germany’s Heidelberg and Marburg facilities are especially important since they concentrate synchrotron-based expertise and carbon ion capability within a very small global supply base. The region is also adding new depth, as IBA now moves to install Portugal’s first proton therapy center at IPO-Porto. Outside the main established markets, South America and parts of the Middle East are becoming the next expansion layer in the hadron therapy market because they can adopt newer compact configurations without carrying legacy infrastructure constraints.

Competitive Landscape

The hadron therapy market is moderately consolidated, with IBA SA, Siemens Healthineers AG, and Hitachi High-Tech still forming the main competitive center through their long presence in large-scale particle therapy installations. Their advantage is rooted in installed base depth, service capability, financing options, and the credibility to support multi-year projects with complex commissioning requirements. IBA remains especially visible in the current cycle because it has added contracts or approvals across MD Anderson, Taiwan, Portugal, Brazil, and the ConformalFLASH study path in the current period. Hitachi continues to defend its position through long-term project structures in Japan, where service duration and institutional relationships are central to procurement outcomes. In the hadron therapy market, these established vendors still hold the clearest edge when buyers need execution certainty for high-value, long-life assets.

Competition is widening from below as compact system specialists challenge the older multi-room model in the hadron therapy market. Mevion’s first clinical treatment on the S250-FIT at Stanford Medicine gives that shift a strong proof point because it shows proton therapy can move into renovated LINAC space rather than only into newly built bunkers. P-Cure’s vault conversion work reinforces the same message, even though the commercial path for that model is still early. On the high-end side, heavy-ion capability remains scarce enough that any credible effort to reduce footprint or simplify deployment could alter future competitive boundaries. That is why the hadron therapy market now shows opportunity at both ends, compact entry systems for wider access and advanced multi-ion platforms for difficult tumor types. The competitive field is therefore no longer defined only by who can build the largest center, but also by who can lower complexity without weakening clinical value.

Technology and intellectual property are also becoming sharper points of separation in the hadron therapy market. Siemens Healthineers received a U.S. patent in December 2025 for methods that improve proton beam energy-layer and spot placement, while its wider FLASH work shows that modality development is now part of strategic positioning rather than a side program. IBA is using ConformalFLASH to push a proton-specific differentiation path that links compact deployment, advanced delivery, and a high-value head and neck use case. At the same time, the drop in CR3 supplier concentration to 72% in 2026 shows that the hadron therapy market is becoming less tightly held than it was earlier in the decade. This easing of concentration does not remove incumbent strength, but it does show that new entrants and narrower platform specialists are gaining room to compete.

Hadron Therapy Industry Leaders

Ion Beam Applications SA

Hitachi, Ltd.

Mevion Medical Systems, Inc.

Siemens Healthineers AG

Sumitomo Heavy Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: IBA (Ion Beam Applications S.A.) received FDA Investigational Device Exemption approval for ConformalFLASH proton therapy (C-FLASH-01), enabling the first-in-human feasibility study at the Abramson Cancer Center, University of Pennsylvania, targeting head and neck re-irradiation in 10 patients; the study is expected to launch in summer 2026 in collaboration with RaySearch Laboratories for treatment planning.

- June 2026: Mevion Medical Systems announced the world's first clinical proton therapy treatment using the MEVION S250-FIT at Stanford Medicine Cancer Center, installed within a renovated conventional LINAC vault without new bunker construction; subsequent installations are planned at BayCare, Atlantic Health, Dana-Farber Cancer Institute, and Istituto Nazionale Tumori IRCCS Fondazione G. Pascale in Italy.

Global Hadron Therapy Market Report Scope

As per the scope of the report, hadron therapy is a type of radiation therapy that uses protons or other heavier charged particles (hadrons) to precisely target and destroy cancer cells. It leverages the unique physical properties of hadrons, such as their ability to deliver a high dose of radiation directly to a tumor with minimal damage to surrounding healthy tissue, primarily through a phenomenon called the Bragg peak. This targeted approach makes hadron therapy particularly effective for treating tumors located near critical structures or in cases where conventional radiation therapy may pose significant risks.

The hadron therapy market is segmented by offering into systems and services. The systems segment includes proton therapy systems, synchrotron-based systems, cyclotron-based systems, and heavy-ion therapy systems. By system configuration, the market is segmented into multi-room facilities and single-room facilities. By application, the market is segmented into breast cancer, brain and central nervous system tumors, prostate cancer, head and neck cancers, gastrointestinal cancers, lung cancer, and other applications. By end user, the market is segmented into hospitals, cancer treatment centers, academic and research institutes, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Systems | Proton Therapy Systems |

| Synchrotron-Based Systems | |

| Cyclotron-Based Systems | |

| Heavy-Ion Therapy Systems | |

| Services |

| Multi-Room Facilities |

| Single-Room Facilities |

| Breast Cancer |

| Brain and Central Nervous System Tumors |

| Prostate Cancer |

| Head and Neck Cancers |

| Gastrointestinal Cancers |

| Lung Cancer |

| Other Applications |

| Hospitals |

| Cancer Treatment Centers |

| Academic and Research Institutes |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Systems | Proton Therapy Systems |

| Synchrotron-Based Systems | ||

| Cyclotron-Based Systems | ||

| Heavy-Ion Therapy Systems | ||

| Services | ||

| By System Configuration | Multi-Room Facilities | |

| Single-Room Facilities | ||

| By Application | Breast Cancer | |

| Brain and Central Nervous System Tumors | ||

| Prostate Cancer | ||

| Head and Neck Cancers | ||

| Gastrointestinal Cancers | ||

| Lung Cancer | ||

| Other Applications | ||

| By End User | Hospitals | |

| Cancer Treatment Centers | ||

| Academic and Research Institutes | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of hadron therapy by 2031?

The hadron therapy market is forecast to reach USD 3.67 billion by 2031, rising from USD 2.25 billion in 2025 at an 8.52% CAGR over 2026-2031.

Which treatment platform currently leads revenue generation?

Systems lead revenue generation, holding 75.31% share in 2025 because they have the broadest installed base and the widest clinical use.

Why are head and neck cancers growing so quickly in this space?

Head and neck cancers are projected to grow at 11.62% CAGR through 2031, mainly because re-irradiation needs are rising and dose sparing is critical in this anatomy.

Which region is expanding the fastest?

Asia-Pacific is the fastest-growing region with a 10.65% CAGR through 2031, supported by China's capacity build-out and Japan's mature clinical ecosystem.

What is the biggest barrier to wider adoption?

High capital intensity remains the biggest barrier, since full proton programs usually require USD 150.00 million to USD 200.00 million and carbon ion centers often exceed USD 300.00 million.

How is competition changing among suppliers?

The field remains moderately consolidated, but compact system entrants, service-led strategies, and FLASH-focused upgrades are reducing reliance on the traditional multi-room incumbent model.

Page last updated on: