Gynecomastia Procedures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

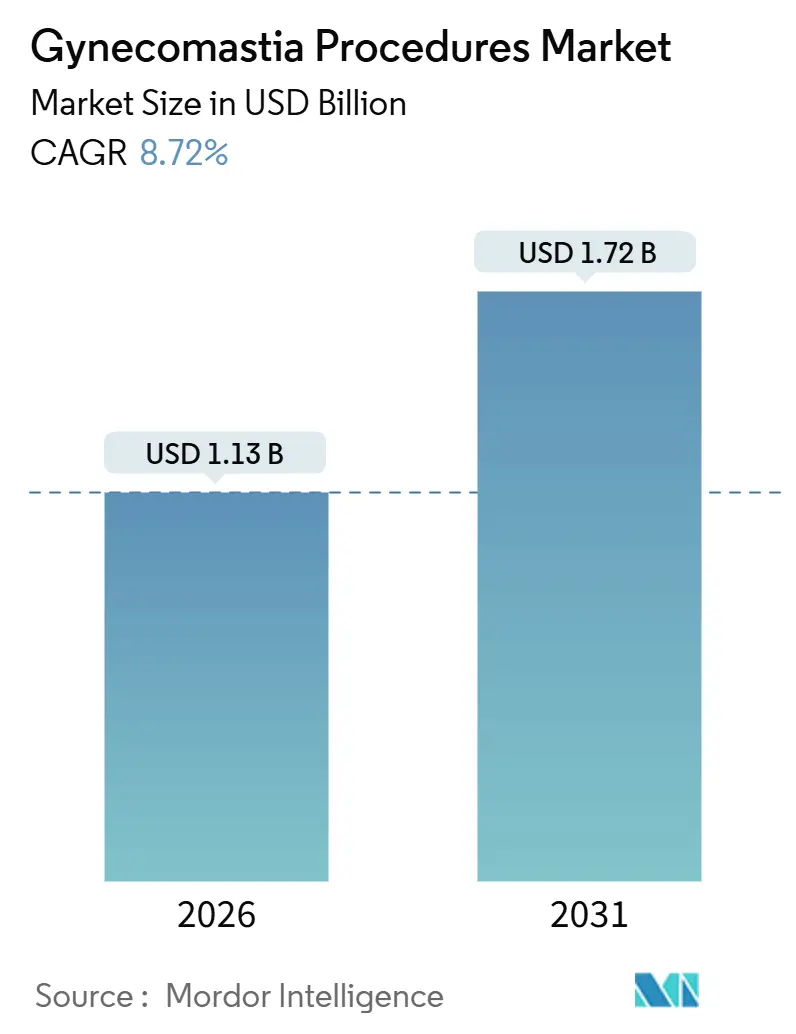

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 8.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gynecomastia Procedures Market Analysis by Mordor Intelligence

The Gynecomastia Procedures Market size is estimated at USD 1.13 billion in 2026, and is expected to reach USD 1.72 billion by 2031, at a CAGR of 8.72% during the forecast period (2026-2031).

Demand is climbing because social-media exposure reshapes male body ideals, obesity prevalence fuels glandular and fat-related cases, and energy-assisted technologies shorten recovery times while commanding premium fees. Procedure counts keep rising—26,430 cases were logged in the United States during 2024—yet revenue momentum stems chiefly from a shift toward outpatient facilities that lower infection risk and enable higher patient throughput. Device makers that bundle training and maintenance with capital equipment leases strengthen their pricing power, while payers continue to restrict reimbursement, placing most of the costs on patients. Middle-income men increasingly rely on third-party financing, expanding the market for gynecomastia procedures despite high out-of-pocket costs. Geographic growth is concentrated in Asia-Pacific, where rising disposable income, medical tourism corridors, and easing cultural stigma are unlocking new demand.

Key Report Takeaways

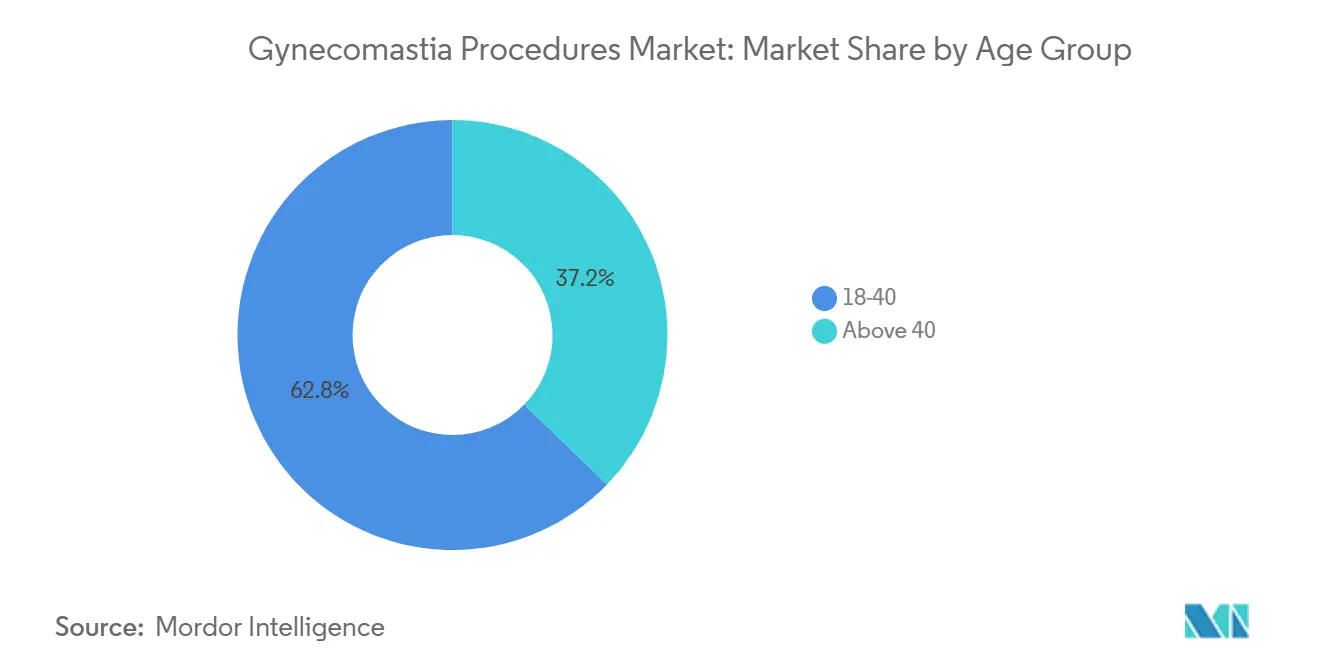

- By age group, the 18-40 cohort held 62.76% market share of the gynecomastia procedures market in 2025, while the above-40 segment is set to expand at a 10.43% CAGR through 2031.

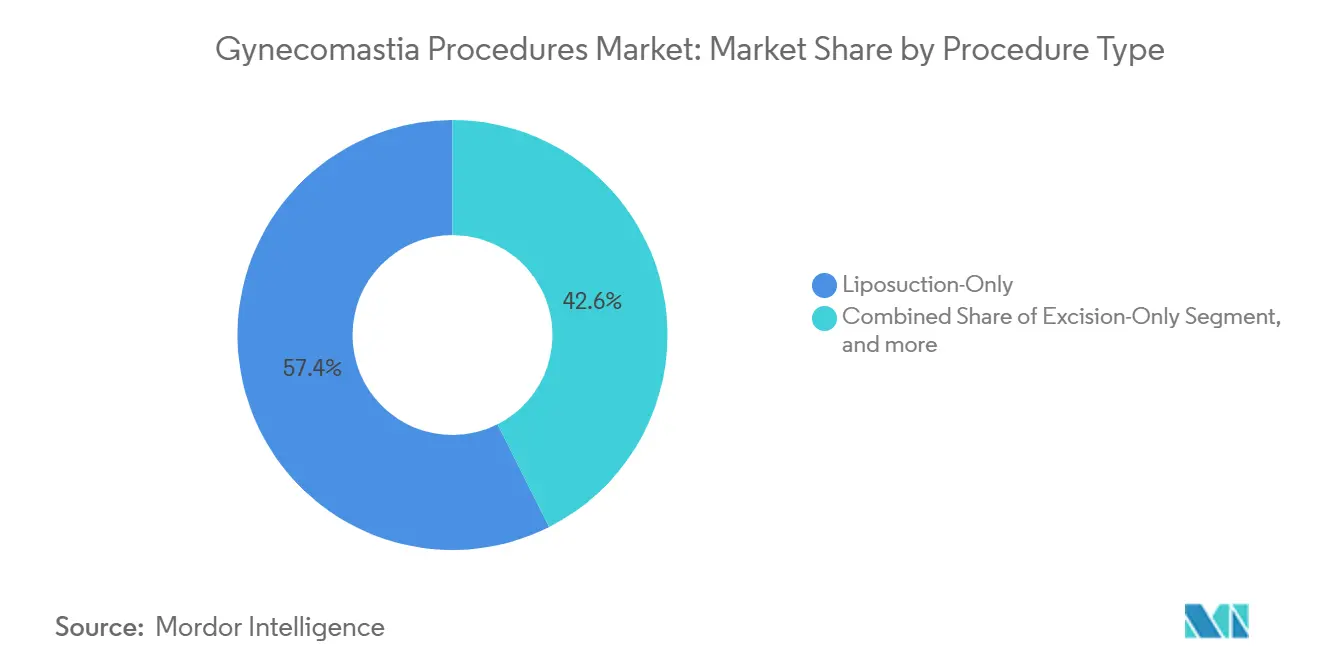

- By procedure type, liposuction-only techniques captured 57.43% of the gynecomastia procedures market in 2025; energy-assisted methods are advancing at a 9.67% CAGR through 2031.

- By end user, hospitals accounted for 58.98% of the gynecomastia procedures market in 2025, whereas ambulatory surgery centers are expected to grow at a 10.76% CAGR through 2031.

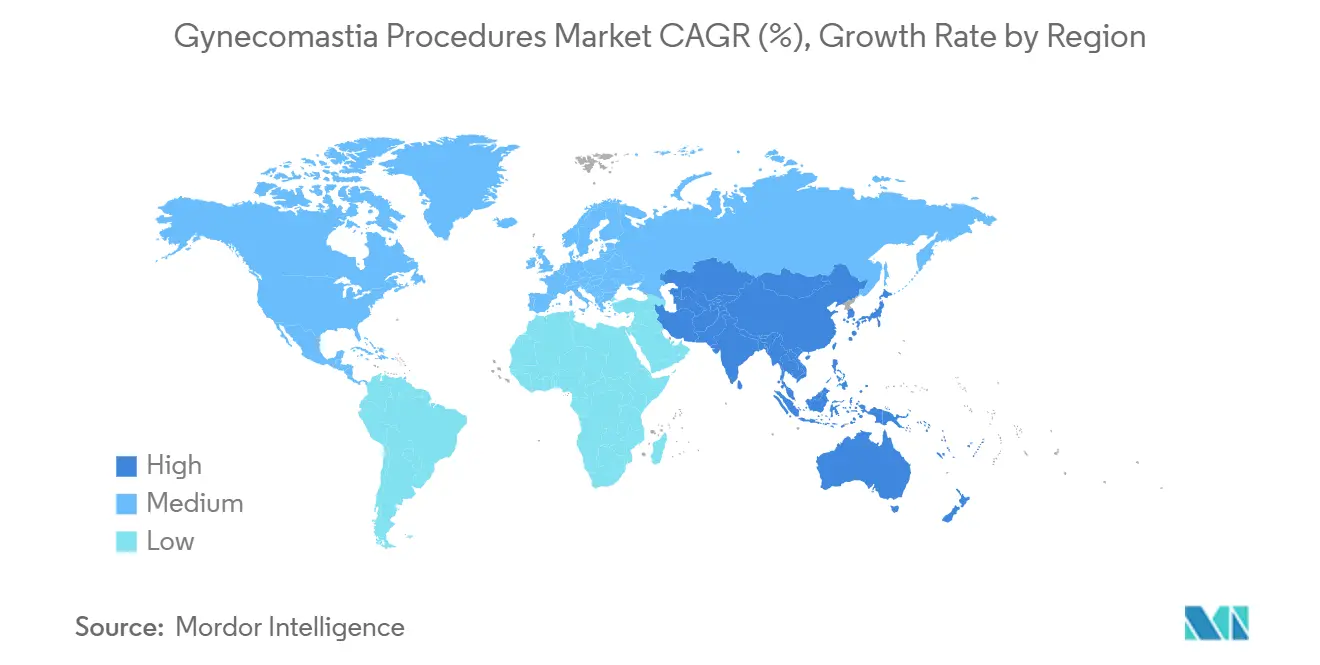

- By geography, North America commanded 42.11% of the gynecomastia procedures market share in 2025; Asia-Pacific is forecast to post the fastest 9.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gynecomastia Procedures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Male Body Image Consciousness | +2.1% | Global, strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| Increase in Hormonal and Obesity-Related Gynecomastia Incidence | +2.5% | North America & Middle East, rising in Latin America | Long term (≥ 4 years) |

| Technological Advancements in Minimally Invasive Chest Contouring | +1.9% | North America & Europe, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Outpatient Cosmetic Surgery Facilities | +1.3% | North America & Asia-Pacific | Medium term (2-4 years) |

| Rise in Disposable Income and Medical Tourism | +1.6% | Asia-Pacific, Middle East & Latin America | Medium term (2-4 years) |

| Proliferation of Social Media Influencers Promoting Male Cosmetic Surgery | +1.1% | Global, led by Gen Z users in North America & Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Male Body Image Consciousness

Seventy-two percent of Generation Z respondents in a 2024 survey stated that Instagram and TikTok content influenced their interest in cosmetic surgery[1]American Academy of Facial Plastic and Reconstructive Surgery, “2024 Annual Survey Results,” aafprs.org. Influencer testimonials normalize gynecomastia correction and tilt patient journeys away from physician referrals toward direct-to-consumer research. The 18-40 cohort values rapid recovery and scar minimization, driving preference for radiofrequency-assisted devices. Employers in client-facing sectors quietly reward polished appearance, adding intangible career incentives. Clinics note that peer comparisons now eclipse traditional word of mouth, underscoring a structural demand pull across the gynecomastia procedures market.

Increase in Hormonal and Obesity-Related Gynecomastia Incidence

Obesity affected 41.9% of U.S. adults between 2017 and 2020, and the CDC projects prevalence will breach 50% by 2030. Elevated aromatase activity converts androgens to estrogens, enlarging glandular tissue, while anabolic-steroid misuse and drugs such as spironolactone add to the incidence. Although 35%–65% of men experience some breast enlargement during their lifetime, only a small fraction pursue surgery, leaving a sizable unmet need. Rapid weight loss from GLP-1 agonists unmask residual glandular tissue, creating follow-on demand for chest contouring. These trends collectively boost case volume and average revenue in the gynecomastia procedures market.

Technological Advancements in Minimally Invasive Chest Contouring

Radiofrequency systems, such as InMode’s BodyTite, generated USD 145.5 million in Q3 2024 revenue, demonstrating strong surgeon uptake[2]InMode Ltd., “Q3 2024 Earnings Presentation,” inmodemd.com. Ultrasonic devices like VASER fragment fat while sparing neurovascular structures, cutting ecchymosis rates. Laser platforms provide similar outcomes yet longer operative times. Energy-assisted approaches deliver 85%–95% patient satisfaction scores versus 70%–80% for liposuction-only techniques, though higher capital costs slow penetration in emerging markets. Manufacturers now pair leases with hands-on training to accelerate adoption, magnifying technology’s contribution to the gynecomastia procedures market.

Expansion of Outpatient Cosmetic Surgery Facilities

The U.S. ambulatory surgery center sector is projected to reach USD 45.8 billion by 2030, with cosmetic procedures driving high-margin growth. Gynecomastia correction suits ASC workflows because most cases finish in under two hours and rarely need overnight monitoring. Infection rates stand at 0.6% in ASCs versus 1.9% in hospitals, encouraging both patients and payers to favor outpatient settings. Indian platform Pristyn Care has expanded to 45+ cities, showcasing how standardized protocols and telemedicine trim acquisition costs and broaden access. The migration toward ASCs enlarges addressable volume and shapes pricing across the gynecomastia procedures market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedural Costs and Limited Reimbursement | -1.4% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Surgical Complications and Revision Risk | -0.8% | Global | Short term (≤ 2 years) |

| Limited Surgeon Expertise in Emerging Markets | -0.9% | Asia-Pacific, Middle East-Africa & Latin America | Long term (≥ 4 years) |

| Cultural Stigma and Low Awareness | -0.7% | Europe & Middle East-Africa, pockets of Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedural Costs and Limited Reimbursement

Fees range from USD 6,000 to USD 12,000 in the United States, yet fewer than 15% of commercial plans cover the procedure. Insurers that do reimburse demand endocrinology evaluations, photographs, and proof of conservative management, delaying approval up to one year. Third-party financing carries APRs of 12%–24%, discouraging middle-income patients. Medical tourism offers USD 2,500–USD 4,500 packages in Turkey and Mexico, but perceived quality gaps limit uptake. In low-income countries, elective surgery competes with basic healthcare, setting a cost ceiling that constrains the market for gynecomastia procedures.

Surgical Complications and Revision Risk

Hematoma occurs in 1%–2% of cases, seroma in 5%–10%, and infection in <1%. Contour irregularities and asymmetry drive 5%–15% revision rates, adding USD 3,000–USD 6,000 in extra costs. Nipple hypoesthesia persists in 2%–5% of patients. Surgeon skill disparities in emerging markets lead to higher complication rates, eroding consumer trust. Limited outcome registries hamper benchmarking, making provider selection opaque. These factors temper growth within segments of the gynecomastia procedures market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Age Group: Younger Cohorts Drive Volume, Older Segment Accelerates

The 18-40 bracket accounted for 62.76% of the gynecomastia procedures market in 2025, reflecting high media exposure and disposable income. Men in this cohort favor minimally invasive methods scheduled during holiday breaks to limit workplace absence. Above 40 patients, however, will expand at a 10.43% CAGR through 2031 as hormonal shifts and obesity converge. Clinical data indicate greater comorbidity prevalence, leading to longer preoperative workups. Yet older men often bundle chest correction with abdominal contouring, lifting average transaction values by up to 35%. Telemedicine follow-up has reduced geographic barriers, broadened referral networks, and sustained the gynecomastia procedures market.

Older patients represent a growing secondary wave as GLP-1-induced weight loss reveals residual glandular tissue. Surgeons report increased demand from men over 50 who historically avoided elective procedures. Comprehensive body makeovers trigger cross-selling of flank and back liposuction, deepening revenue per case. These dynamics suggest that demographic aging, rather than eroding volume, reinvigorates premium tiers of the gynecomastia procedures market.

By Procedure Type: Energy-Assisted Platforms Gain Share Despite Liposuction Dominance

Liposuction-only methods accounted for 57.43% of procedures in 2025, driven by speed and affordability, especially in price-sensitive regions. Excision-only approaches stay niche, reserved for dense glandular tissue. Combined liposuction–excision techniques provide comprehensive correction but entail longer operative times. Endoscopic and energy-based systems are forecast to grow 9.67% annually, leveraging radiofrequency and ultrasound to improve skin retraction while reducing drainage. A 2024 Aesthetic Surgery Journal study documented 18% shorter operative times and 32% less postoperative drainage with suction-assisted methods versus suction-only methods, underscoring technology’s role in expanding the gynecomastia procedures market at the procedure level.

Seven new energy-based platforms secured FDA 510(k) clearance between 2024 and early 2026, intensifying competition and nudging capital prices downward. Manufacturers increasingly bundle workshops and proctored cases into leases, closing the skill gap that once slowed adoption. Procedure premiums of USD 1,500–USD 3,000 remain acceptable to image-conscious patients who value lower revision risk. These factors collectively translate to durable share gains for energy-assisted modalities in the gynecomastia procedures market.

By End-User: Ambulatory Centers Capture Growth as Hospitals Retain Volume

Hospitals performed 58.98% of gynecomastia procedures in 2025, with complex revisions and comorbidity management as the primary focus. Academic centers also perform training cases, reinforcing the hospital's share. However, OR fees of USD 1,200–USD 2,000 per hour and 8- to 12-week scheduling lead times push straightforward cases into ASCs, which are growing at a 10.76% CAGR. Infection rates below 1% and transparent bundled pricing resonate with self-pay patients, bolstering ASC momentum within the gynecomastia procedures market.

Specialist cosmetic-surgery clinics form the fastest-moving channel. Chains such as Pristyn Care standardize consent, imaging, and follow-up, trimming variability and enabling data-driven quality improvements. The shift is sharpest in regions where regulations allow a wide range of procedures under local anesthesia, notably North America and the Asia-Pacific. Hospitals still dominate Europe and the Middle East, where public systems funnel elective surgery to state facilities and private ASC licensing is restrictive. This duality keeps the gynecomastia procedures market competitively balanced across care settings.

Geography Analysis

North America generated 42.11% of 2025 revenue in the gynecomastia procedures market, anchored by high per-capita spending and early uptake of energy-based devices. U.S. case counts rose 2% year over year to 26,430 in 2024, and the American Society of Plastic Surgeons anticipates 3%–4% annual growth to 2028[3]American Society of Plastic Surgeons, “2024 Plastic Surgery Statistics Report,” plasticsurgery.org. Reimbursement remains sparse, yet financing plans and employer wellness allowances widen access. InMode derived 58% of its Q3 2024 revenue from North America, underscoring technology leadership. Canada shows similar trends, though provincial plans seldom pay for surgery, making private clinics the dominant channel.

Asia-Pacific is set to log a 9.54% CAGR through 2031, the fastest globally. China’s 400-million-strong urban middle class views cosmetic surgery as a career enhancement; male procedures climbed 12% in 2024. India’s Pristyn Care prices gynecomastia at USD 1,800–USD 3,500, leveraging same-day discharge to attract patients who would otherwise delay surgery. Thailand and South Korea ride medical tourism, while Singapore enforces FDA-like device standards, creating a quality tier. Off-label energy-device use in less-regulated markets widens outcome dispersion, prompting savvy patients to vet surgeon credentials thoroughly. Collectively, favorable demographics and shifting attitudes reinforce Asia-Pacific’s role as growth engine of the gynecomastia procedures market.

Europe, the Middle East and Africa, and South America display moderate expansion. The United Kingdom’s NHS funds surgery only for severe cases, funneling demand to private clinics where fees range from GBP 4,000 to GBP 7,000 (USD 5,200 to USD 9,100). Germany and France support robust private markets, yet cultural conservatism tempers male uptake. The Middle East leverages free-zone incentives—such as those in Dubai, which attracted multiple international clinic chains in 2025—to cultivate medical tourism. South America offers lower prices (USD 2,500–USD 4,500 in Brazil and Colombia), but it also faces currency volatility that deters cross-border patients. Africa remains underpenetrated outside South Africa’s private sector due to surgeon shortages and competing health priorities. These regional nuances ensure that the gynecomastia procedures market maintains heterogeneous growth trajectories.

Competitive Landscape

Competition in the gynecomastia procedures market spans device makers, pharmaceutical suppliers, and integrated clinic networks. InMode, Cutera (acquired for USD 1.1 billion in May 2024), Cynosure, Alma Lasers, and Lumenis vie for surgeon allegiance by bundling capital leases with training and service. BodyTite holds an estimated 22% share of energy-assisted procedure volume in North America, supported by key opinion leader endorsements. AbbVie’s Allergan Aesthetics posted USD 1.27 billion Q3 2024 revenue, led by CoolSculpting, yet lacks a surgical chest-contouring product, leaving strategic whitespace. Johnson & Johnson’s Mentor unit supplies implants for severe revisions but focuses chiefly on women’s health.

Clinic chains add another competitive layer. Pristyn Care’s franchise model standardizes workflows across 45+ Indian cities, while U.K. provider Spire Healthcare promotes gynecomastia correction alongside orthopedics to optimize OR utilization. North American single-specialty centers market directly via social media, offering flat-fee packages that include imaging, surgery, and garments. Transparency on complication rates and satisfaction scores differentiates leaders, though registry participation remains voluntary. Emerging opportunities include multi-site protocols that combine chest contouring with abdominal etching and pectoral implants in one session, as well as bioresorbable scaffolds aimed at reducing seroma—currently a 5%–10% complication.

Gynecomastia Procedures Industry Leaders

InMode Ltd.

Cynosure LLC

Alma Lasers Ltd.

MicroAire Surgical Instruments LLC

Cutera Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: BioZen started developing the world's first approved medical cure for gynecomastia, aiming to provide a non-surgical treatment option. This innovative approach is currently in development or awaiting approval.

- March 2024: Cleveland Clinic Abu Dhabi announced that it has pioneered a new reconstructive technique to enhance surgical outcomes for patients with gynecomastia. This innovative approach aims to improve aesthetic results and reduce complications. The development signifies a significant advancement in gynecomastia treatment at the institution.

Global Gynecomastia Procedures Market Report Scope

As per scope of the report, gynecomastia procedures are surgical or non-surgical treatments aimed at reducing excess breast tissue in males. Surgical options include liposuction and gland removal, while non-surgical methods involve medication or laser therapy. These procedures help restore a flatter, more masculine chest contour.

The Gynecomastia Procedures Market is Segmented by Age Group (18-40 and Above 40), Procedure Type (Liposuction-Only, Excision-Only, Combined Lipo + Excision, and Endoscopic / Energy-Assisted Lipolysis), End-User (Hospitals, Ambulatory Surgery Centers, and Specialist Cosmetic Surgery Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| 18-40 |

| Above 40 |

| Liposuction-Only |

| Excision-Only |

| Combined Lipo + Excision |

| Endoscopic / Energy-Assisted Lipolysis |

| Hospitals |

| Ambulatory Surgery Centers (ASCs) |

| Specialist Cosmetic Surgery Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Age Group | 18-40 | |

| Above 40 | ||

| By Procedure Type | Liposuction-Only | |

| Excision-Only | ||

| Combined Lipo + Excision | ||

| Endoscopic / Energy-Assisted Lipolysis | ||

| By End-User | Hospitals | |

| Ambulatory Surgery Centers (ASCs) | ||

| Specialist Cosmetic Surgery Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current value of the gynecomastia procedures market?

The gynecomastia procedures market size stands at USD 1.13 billion in 2026 and is projected to reach USD 1.72 billion by 2031.

Which age group undergoes most gynecomastia surgeries?

Men aged 18-40 account for 62.76% of procedures owing to social-media influence and disposable income.

Which region is growing fastest for gynecomastia surgery demand?

Asia-Pacific is forecast to expand at a 9.54% CAGR through 2031 due to rising incomes, medical tourism, and easing cultural stigma.

Why are energy-assisted devices gaining popularity?

Radiofrequency and ultrasound platforms tighten skin and reduce bleeding, lifting satisfaction rates to 85%Ð95% and lowering revision risk.

What limits insurance coverage for gynecomastia correction?

Most insurers classify the surgery as cosmetic unless severe symptoms are documented, so fewer than 15% of U.S. claims win approval.

Page last updated on: