Green IT Software For Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 3.95 Billion |

| Growth Rate (2026 - 2031) | 16.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green IT Software For Healthcare Market Analysis by Mordor Intelligence

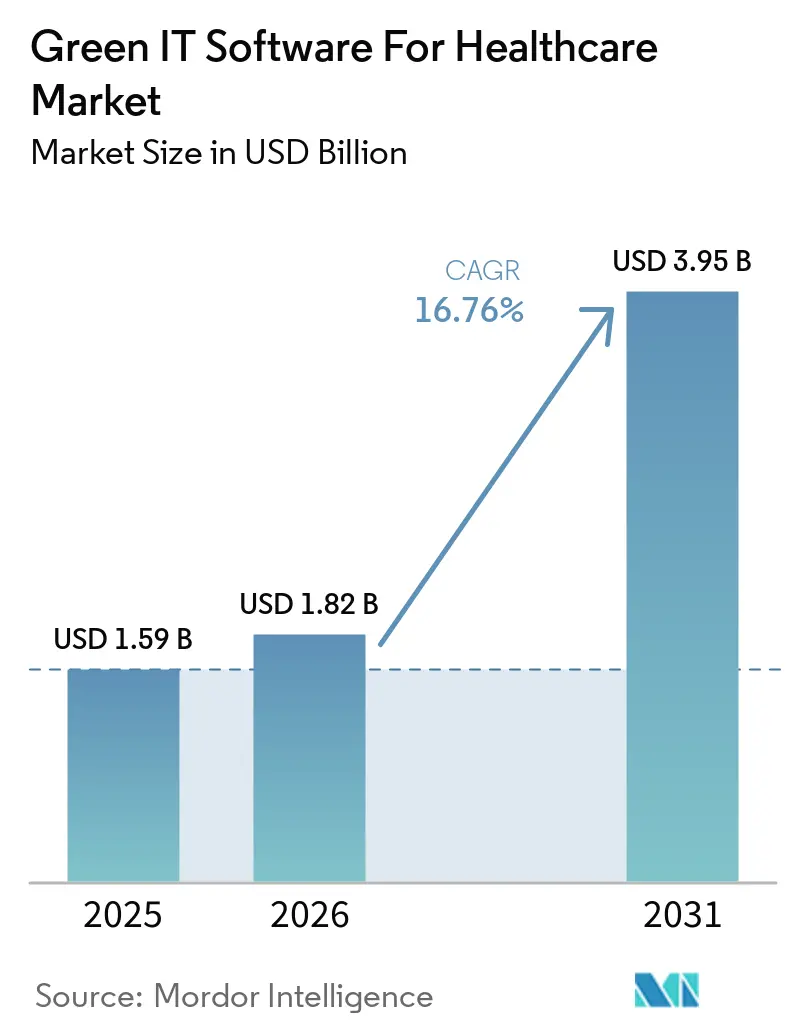

The Green IT Software For Healthcare Market size is expected to increase from USD 1.59 billion in 2025 to USD 1.82 billion in 2026 and reach USD 3.95 billion by 2031, growing at a CAGR of 16.76% over 2026-2031. Demand is rising because hospitals, payers, and other healthcare organizations now face tighter pressure to measure the energy and emissions impact of their digital estates in a more consistent way. The expansion of electronic health records, imaging platforms, remote monitoring, and AI-enabled workflows has made IT sustainability a board-level issue instead of a narrow facilities matter. Procurement-linked carbon reporting rules are also changing buying behavior, because software that supports audit-ready disclosures is becoming part of vendor qualification and compliance activity. Green IT software for the healthcare market is also gaining support from cloud migration and the need to understand the carbon cost of AI workloads within clinical operations. Competition remains spread across specialist carbon platforms and large enterprise software providers, leaving room for vendors that can connect healthcare workflows, emissions tracking, and regulatory reporting into a single usable system.

Key Report Takeaways

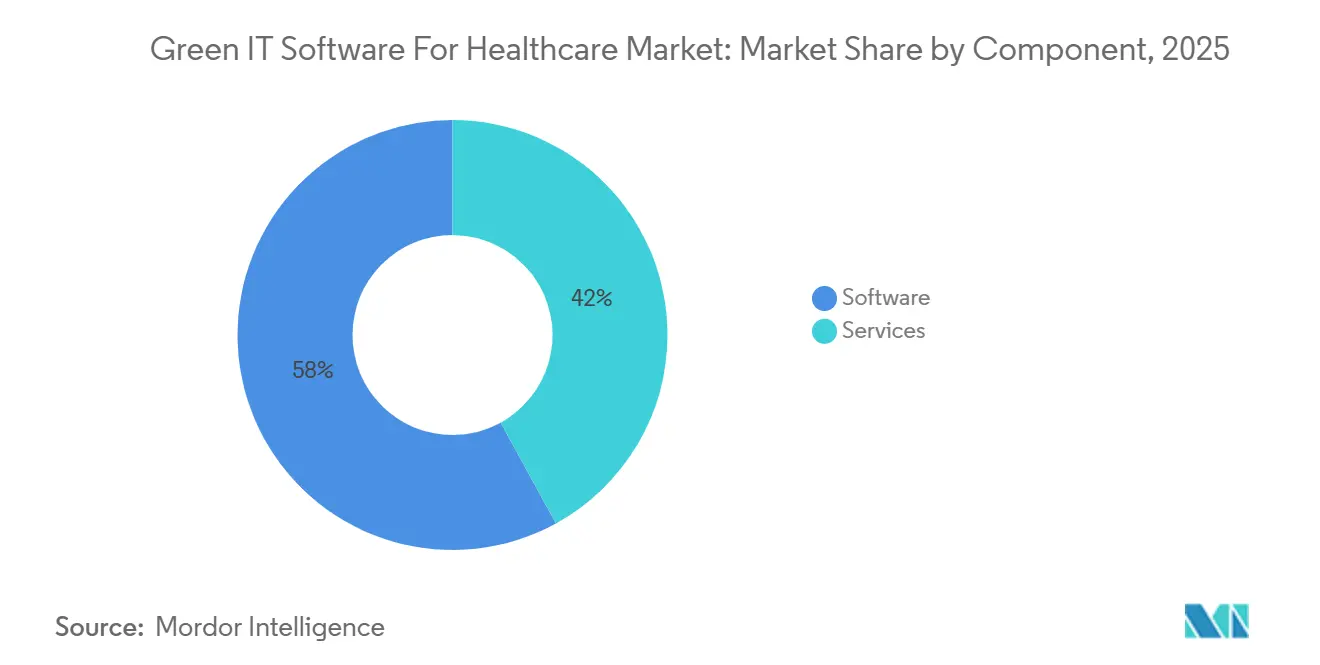

- By component, software held 58% share in 2025, while services are projected to expand at an 18.12% CAGR through 2031 in the Green IT software for healthcare market.

- By deployment mode, cloud-based deployment captured 64% of the market in 2025, while hybrid deployment is projected to grow at a 17.50% CAGR through 2031.

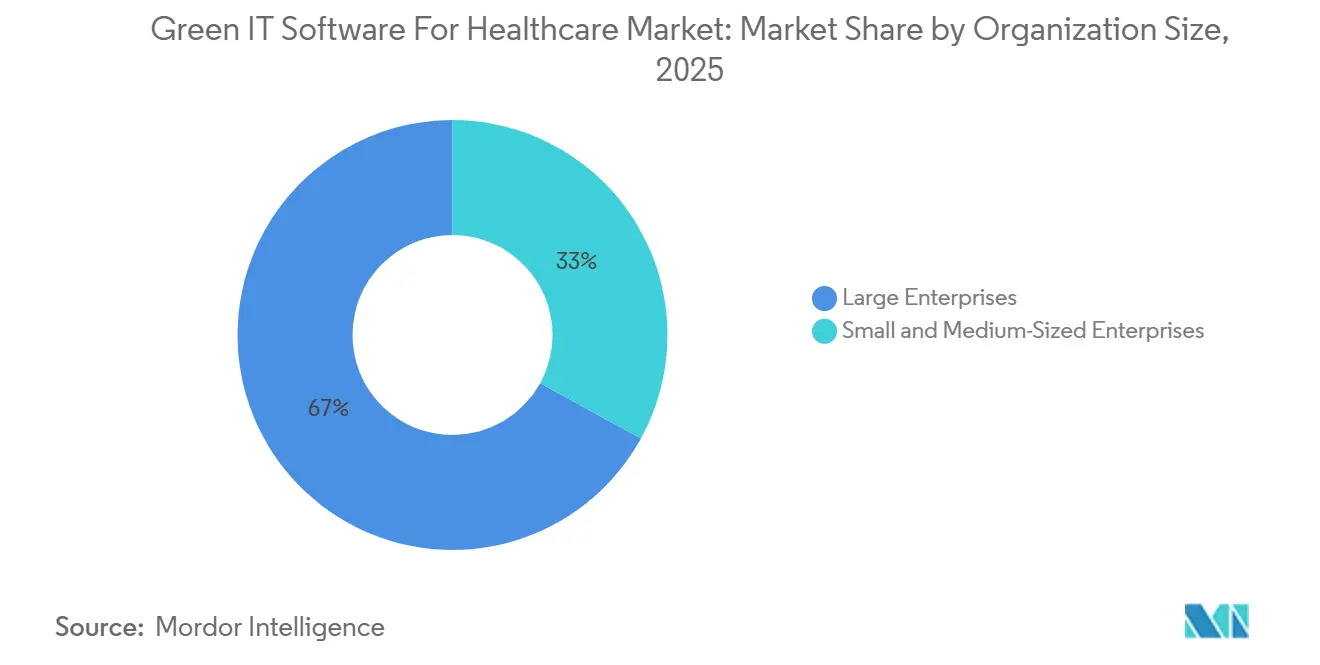

- By organization size, large enterprises held 67% share in 2025, while SMEs are projected to expand at a 17.27% CAGR through 2031.

- By application, ESG reporting and regulatory compliance led the application landscape and are projected to grow at a 19.12% CAGR through 2031.

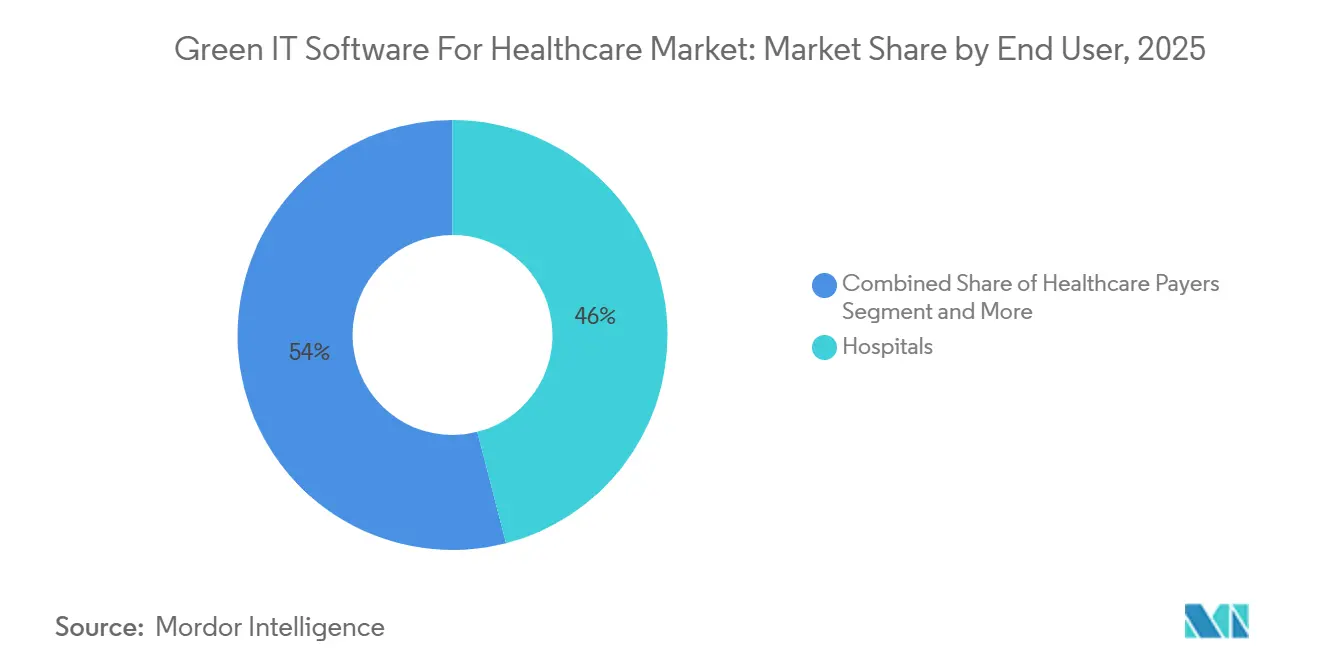

- By end user, hospitals held 46% share in 2025, while healthcare payers are projected to advance at an 18.80% CAGR through 2031.

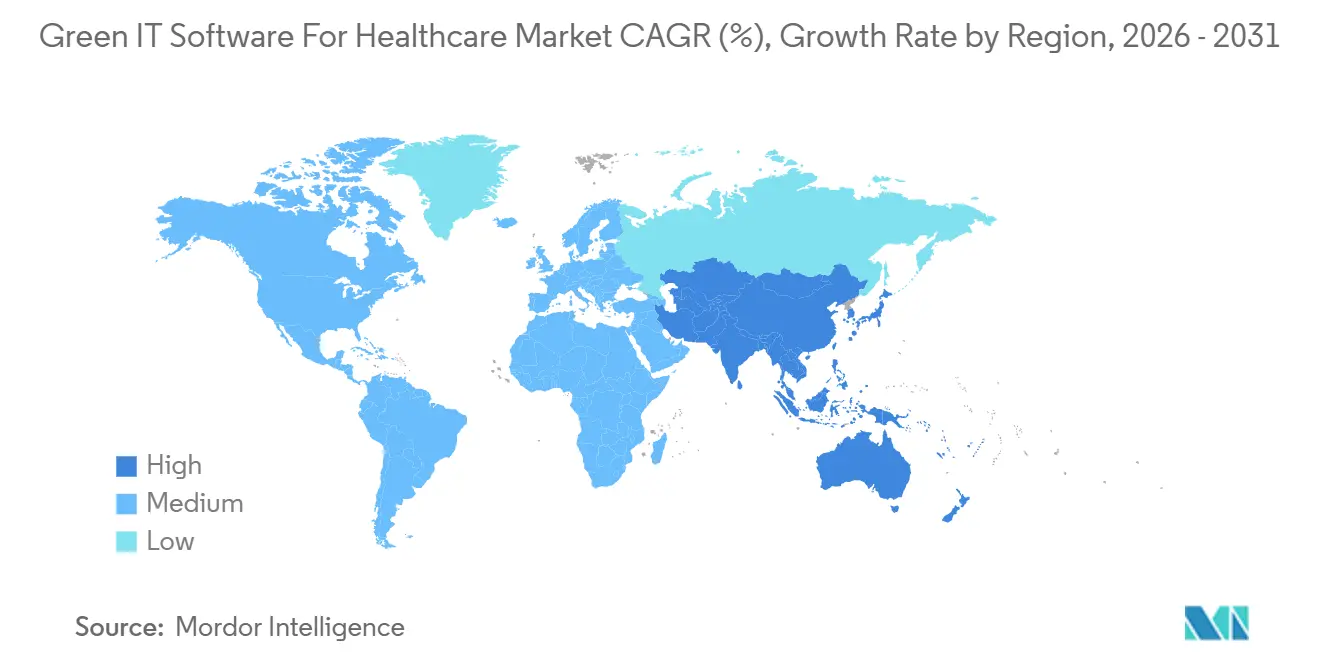

- By geography, North America held 38% share in 2025, while Asia-Pacific is projected to expand at a 17.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Green IT Software For Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Energy Cost Pressure Across Healthcare Digital Estates | +3.2% | Global | Short term (≤ 2 years) |

| Carbon Reporting Requirements Tied to Health System Procurement | +3.0% | North America and Europe | Short term (≤ 2 years) |

| Cloud Migration Demand for Lower-Emission IT Operations | +2.6% | Global | Medium term (2-4 years) |

| Need for Sustainable AI and Data Center Workloads in Healthcare | +2.3% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Hospital ESG Budget Linking IT Efficiency to Clinical Resilience | +1.5% | North America and Europe | Medium term (2-4 years) |

| Growing Preference for Audit-Ready Sustainability Analytics | +1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Energy Cost Pressure Across Healthcare Digital Estates

Rising power use across imaging storage, clinical servers, and connected digital workflows is making the Green IT software for healthcare market more urgent for provider boards. A 2025 study in European Radiology showed that long-term CT data storage consumes significant electricity across storage systems, servers, and network infrastructure, providing hospitals with a clear operating baseline for sustainability action. As digital care expands, energy management and carbon tracking increasingly sit within the same operating workflow rather than in separate teams. That shift favors platforms that can integrate asset selection, workload placement, and reporting outputs into a single system. The immediate effect is a stronger demand for software that can show where energy is consumed and how operational changes can lower both cost and emissions.

Carbon Reporting Requirements Tied To Health System Procurement

Procurement rules are moving the Green IT software for the healthcare market from optional spending to contract-linked spending. From April 6, 2026, NHS Supply Chain required suppliers to complete the Evergreen Sustainable Supplier Assessment Level 1 and to hold a PPN 006-compliant Carbon Reduction Plan covering Scope 1, Scope 2, and relevant Scope 3 emissions. [1]British Healthcare Trades Association, “Evergreen Sustainable Supplier Assessment Level 1 for NHS Tenders From April 2026,” British Healthcare Trades Association, bhta.com That requirement matters because it pushes carbon data collection into ordinary vendor qualification, renewal, and tender activity. The Journal of Medical Internet Research also documented that unproven generative AI in UK primary care creates a reporting gap because AI-related emissions are not consistently captured in current disclosures. As procurement standards and disclosure expectations tighten together, platforms that support audit-ready reporting gain a clearer path into healthcare budgets.

Cloud Migration Demand For Lower-Emission IT Operations

Cloud migration is changing the Green IT software landscape for the healthcare market, as carbon efficiency now sits alongside cost and resilience in IT planning. A 2025 European Radiology study reported that conventional European data centers average a power usage effectiveness of 1.8, while hyperscale cloud providers can operate below 1.2. That gap gives health systems a measurable reason to shift sustainability analytics and related workloads away from energy-intensive local estates. Kurashiki Central Hospital migrated its electronic health record environment to the Nutanix Cloud Platform in March 2025, demonstrating how cloud modernization and sustainability goals can be advanced within the same program. [2]Journal of Medical Internet Research, “Carbon Reporting Practices in the NHS, Emissions and Omissions Relating to Artificial Intelligence,” Journal of Medical Internet Research, jmir.org Green IT software for the healthcare market benefits providers by providing tools to compare pre- and post-migration emissions and document the results for internal oversight.

Need For Sustainable AI And Data Center Workloads In Healthcare

AI adoption is creating a new demand layer within Green IT software for the healthcare market, as model training and inference add a distinct energy burden to healthcare IT. The Journal of Medical Internet Research reported that a single complex AI query can use as much energy as charging a smartphone 11 times and require 20 mL of cooling water, while ChatGPT can consume 15 times the energy of a conventional web search. [3]Nutanix, “Kurashiki Central Hospital Case Study,” Nutanix, nutanix.com UC Berkeley’s SAHAI framework responded to this issue by outlining model-level carbon accounting for clinical AI deployments. That approach matters because generic ESG tools usually report enterprise emissions at a higher level and do not isolate AI workload intensity inside clinical settings. Vendors that can attribute emissions by model, workload type, and usage frequency are positioned to stand apart as healthcare AI deployment widens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Sustainability Data Across Clinical and Nonclinical Systems | -2.5% | Global | Medium term (2-4 years) |

| Weak Green IT ROI Benchmarking for Mid-Sized Providers | -2.0% | North America and Europe | Medium term (2-4 years) |

| Cybersecurity and Privacy Controls Raising Implementation Complexity | -1.6% | Global | Short term (≤ 2 years) |

| Integration Difficulty With Legacy EMR and Facility Systems | -1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Sustainability Data Across Clinical And Nonclinical Systems

Fragmented data remains the largest barrier inside the Green IT software for healthcare market because sustainability records are spread across clinical, facilities, procurement, and enterprise software systems. Hospitals often keep energy, asset, and operating data in separate environments, which slows the creation of a consistent emissions baseline. That weak starting point makes reporting more difficult and lengthens platform deployment cycles, especially when organizations want a single view across multiple sites. Sana Kliniken AG’s 2025 shift to Osapiens for ESG data management underscores why large operators are formalizing enterprise systems rather than relying on disconnected workflows. Until data models and interfaces become more standardized, the Green IT software for the healthcare market will face slower adoption across multisite providers and mid-sized institutions.

Weak Green IT ROI Benchmarking For Mid-Sized Providers

ROI benchmarking remains uneven in the Green IT software for healthcare market, especially for mid-sized providers that lack the scale of national hospital networks. Large systems can spread software, integration, and governance costs across broader infrastructure and across more reporting obligations. Smaller providers often need a clearer payback case before approving platform purchases, especially when budgets compete with clinical technology spending. This gap extends sales cycles because vendors must prove value through narrower use cases such as compliance readiness, cloud optimization, or equipment lifecycle planning. The result is a market where demand exists, but conversion is slower outside the largest and best-resourced organizations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Reflects A More Mature Buying Pattern

Software held 58% of the market in 2025, while services are projected to grow at an 18.12% CAGR through 2031. Software remained the structural anchor because healthcare buyers need a documented and continuously updated platform rather than a one-time consulting exercise. That position is reinforced by disclosure requirements that demand repeatable data collection, audit support, and workflow consistency across reporting periods. In the Green IT software for the healthcare industry, this makes software the base layer that other implementation and advisory services sit around.

Services are still set for the fastest expansion because integration, configuration, validation, and reporting support remain essential for many buyers in the Green IT software for healthcare market. As disclosure scope widens to include supply chain data, AI-related emissions, and multi-framework reporting, organizations need more help turning software outputs into usable compliance records. SAP announced in May 2026 that its new sustainability AI agents can cut packaging compliance hours by more than 50% and reduce scenario simulation time from 1 day to 20 minutes, demonstrating how vendors are automating work that previously required deeper service engagement. [4]SAP SE, “Autonomous Enterprise, New Sustainability AI Agents,” SAP News Center, news.sap.com This pattern suggests services demand will remain strong in the near term, but more of that work will gradually be shaped by automation.

By Deployment Mode: Cloud Leadership And Hybrid Growth Define Adoption

Cloud-based deployment captured 64% of the Green IT software for healthcare market size in 2025, while hybrid deployment is projected to grow at a 17.50% CAGR through 2031. Cloud remained the largest mode because it aligns with the push to move sustainability analytics away from energy-intensive local infrastructure. Hybrid is growing faster because many healthcare organizations still need local connections to clinical systems, building controls, and sensitive data environments. In the Green IT software for healthcare market, durable demand is created for architectures that combine central reporting tools with controlled local data access.

On-premises deployment is losing relative weight, but it still has a role where strict latency, privacy, and internal control requirements remain. Kurashiki Central Hospital’s March 2025 move to the Nutanix Cloud Platform demonstrated how healthcare providers can modernize core systems while supporting broader IT sustainability goals. The practical effect is that buyers are not choosing between legacy and cloud in a simple way, because many are moving through staged transition models instead. The Green IT software for the healthcare market, therefore, favors vendors that can support mixed environments without disrupting existing clinical operations.

By Organization Size: Large Enterprises Lead While SMEs Move Faster From A Smaller Base

Large enterprises held 67% of the Green IT software market share in 2025, while SMEs are projected to expand at a 17.27% CAGR through 2031. Large organizations lead because they have larger capital budgets, internal sustainability teams, and direct exposure to formal reporting obligations. They also benefit from deeper enterprise data stacks, which can lower deployment friction when new emissions tools are added. The Green IT software for the healthcare industry, therefore, remains tilted toward larger operators at the current stage of adoption.

SME growth is rising because procurement pressure now flows down from major health systems to smaller suppliers and service partners in the Green IT software for healthcare market. When large buyers ask vendors for structured carbon plans and disclosure support, smaller organizations must respond even if they do not yet need a full enterprise platform. The April 2026 NHS Supply Chain requirement for Evergreen Sustainable Supplier Assessment Level 1 provides this downstream pressure with a concrete operational trigger. That dynamic favors lighter subscription models, compliance-focused modules, and offerings that solve a defined reporting problem without requiring a broad enterprise rollout.

By Application: Reporting Stays Central As Platforms Add Decision Support

ESG reporting and regulatory compliance are projected to grow at a 19.12% CAGR through 2031 and remain the lead application for the Green IT software for healthcare market. This application acts as the core layer because most healthcare organizations start their sustainability software journey with disclosure, audit preparation, and policy alignment. Carbon footprint management remains close behind, as Scope 1 and Scope 2 measurement still underpin most reporting programs. IT infrastructure sustainability is also gaining ground as the expansion of AI and digital storage makes workload-level emissions more visible in routine operations.

The direction of travel is toward integrated reporting, benchmarking, and workflow automation in the Green IT software market for healthcare. Fujitsu launched an AI-powered non-financial ESG disclosure analysis service in May 2026, using sustainability data from more than 1,000 listed Japanese companies, demonstrating how reporting tools are moving beyond collection toward comparative analysis. SAP’s sustainability AI agents point to the same shift because they focus on faster scenario modeling and lower manual compliance effort. The result is a market that increasingly values tools that explain, benchmark, and operationalize disclosures rather than simply store emissions data.

By End User: Hospitals Anchor Demand While Payers Accelerate

Hospitals accounted for 46% of end-user demand in 2025, while healthcare payers are projected to grow at a 18.80% CAGR through 2031. Hospitals remained the largest users because they operate the heaviest physical IT estates, including imaging archives, local servers, connected devices, and network infrastructure. Payers are growing faster because their needs are often more software-centric and less dependent on physical estate optimization. In the Green IT software for healthcare market, it makes payer deployments easier to start and easier to scale from a reporting standpoint.

A 2025 European Radiology study provided a precise view of hospital IT energy use by showing the role of storage systems, servers, and networks in long-term CT data retention. [5]Springer Nature, “Greenhouse Gas Emissions Due to Long-Term Data Storage of CT With Reformats and Strategies for Mitigation,” European Radiology, springer.com That evidence helps explain why hospital demand continues to shape the commercial center of the Green IT software for healthcare market. Life sciences organizations remain financially important because they need structured emissions data across broader value chains and formal ESG programs. The Green IT software for the healthcare industry is also widening gradually into ambulatory care centers and diagnostic settings as procurement rules and parent-system requirements spread beyond major hospital groups.

Geography Analysis

North America accounted for 38% of the Green IT software market share in the healthcare market in 2025. The region led because it combines a strong base of enterprise software vendors, large integrated health systems, and mature digital infrastructure. The United States remained the core demand center because sustainability programs increasingly intersect with cloud modernization, bond scrutiny, and enterprise reporting needs. Mayo Clinic and Microsoft announced a strategic collaboration in June 2026 to develop a frontier AI model for healthcare, underscoring how large U.S. care systems and technology firms are advancing digital workloads that require stronger carbon oversight. The Green IT software for the healthcare market is therefore more operationally mature in North America than in most other regions.

Europe remained the second-largest regional bloc in the Green IT software for healthcare market. Demand in the region is being shaped by mandatory sustainability reporting, procurement-linked disclosure expectations, and wider pressure for auditable enterprise data. Large health systems are moving from fragmented sustainability workflows to formal software environments that can support repeatable reporting cycles. Sana Kliniken AG’s 2025 adoption of osapiens for ESG data management showed how major hospital operators are putting these requirements into enterprise systems. The region’s buying pattern favors platforms that can combine governance, emissions accounting, and operational integration without creating another disconnected reporting layer.

Asia-Pacific is projected to expand at a 17.85% CAGR through 2031, making it the fastest-growing region in the Green IT software for healthcare market. Growth is being supported by rising disclosure expectations, cloud modernization, and local software development linked to ESG reporting needs. Fujitsu’s May 2026 launch of an AI-powered ESG disclosure analysis service and Kurashiki Central Hospital’s earlier cloud migration illustrate how reporting and digital infrastructure changes are advancing at the same time in Japan. South America, the Middle East, and Africa remain smaller in current value, but adoption is still moving forward where multinational healthcare groups extend enterprise sustainability programs across local operations.

Competitive Landscape

The Green IT software for healthcare market remains moderately fragmented, with no single vendor holding a decisive position across all use cases. Competition is split between purpose-built climate platforms and larger enterprise software companies that already operate inside healthcare data environments. Purpose-built vendors bring depth in carbon accounting methods and disclosure workflows, while incumbents bring broader integration capabilities and established customer relationships. That split matters because healthcare buyers often need both technical emissions logic and practical links to enterprise systems. The Green IT software for healthcare market still leaves room for several vendor types because compliance, cloud transition, AI oversight, and facility-linked reporting do not yet sit neatly inside one standard product model.

One clear strategy is to automate sustainability work inside broader software platforms in the Green IT software for healthcare market. SAP said in May 2026 that its sustainability AI agents can reduce packaging compliance hours by more than 50%, cut scenario simulation time from 1 day to 20 minutes, and lower packaging compliance errors by more than 20%. Fujitsu followed a similar path in May 2026 with an AI-powered ESG disclosure analysis service that helps organizations compare their disclosures against peers and evaluation criteria. These moves show that vendors are competing not only on data capture, but also on speed, workflow automation, and interpretation. The Green IT software for healthcare market increasingly rewards platforms that reduce manual reporting effort and shorten the path from raw data to board-ready output.

Another strategy is to tie green IT capabilities to wider digital health and cloud programs inside the Green IT software for healthcare market. SAP and Fresenius announced a strategic partnership in January 2026 to build a scalable AI-supported healthcare platform using SAP Business Suite and SAP Business AI, which links sustainability-oriented data management to broader care process digitization. Mayo Clinic and Microsoft also announced a June 2026 collaboration to develop a frontier AI model for healthcare, reinforcing the need for stronger visibility into the energy and carbon impact of advanced digital workloads. The Green IT software for healthcare market therefore still offers white space for specialists that can connect audit-ready reporting with clinical system data, cloud architecture, and AI workload measurement.

Green IT Software For Healthcare Industry Leaders

Watershed, Inc.

Persefoni AI, Inc.

Sweep SAS

Normative AB

Plan A Earth GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Mayo Clinic and Microsoft Corporation announced a strategic collaboration to develop a frontier AI model for healthcare, to be hosted on Azure Foundry and made available globally. The deployment of inference-scale clinical AI at this volume raises direct accountability questions about data center energy and carbon footprinting that green IT platforms will be called upon to address.

- May 2026: SAP SE announced sustainability AI agents reaching general availability by end of 2026, delivering greater than 50% reduction in packaging compliance hours, scenario simulation time cuts from 1 day to 20 minutes, and over 20% fewer packaging compliance errors. The development accelerates automation of green IT reporting workflows within healthcare supply chains.

- May 2026: Fujitsu launched an AI-powered non-financial ESG disclosure analysis service, leveraging sustainability data from over 1,000 listed companies in Japan to help organizations benchmark their ESG disclosures against peers and rating agency criteria.

- January 2026: SAP SE and Fresenius announced a strategic partnership to build a scalable, AI-supported healthcare platform using SAP Business Suite and SAP Business AI, targeting connected, data-driven healthcare processes and digital innovation across the care chain.

Global Green IT Software For Healthcare Market Report Scope

The Green IT Software for Healthcare Market is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises and SMEs), Application (Carbon Footprint, Energy Optimization, ESG Reporting, and IT Infrastructure), End User (Hospitals, Ambulatory, Imaging, Payers, and Life Sciences), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Carbon Footprint Management |

| Energy and Resource Optimization |

| ESG Reporting and Regulatory Compliance |

| IT Infrastructure Sustainability Management |

| Hospitals |

| Ambulatory Care Centers |

| Diagnostic and Imaging Centers |

| Healthcare Payers |

| Life Sciences Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Application | Carbon Footprint Management | |

| Energy and Resource Optimization | ||

| ESG Reporting and Regulatory Compliance | ||

| IT Infrastructure Sustainability Management | ||

| By End User | Hospitals | |

| Ambulatory Care Centers | ||

| Diagnostic and Imaging Centers | ||

| Healthcare Payers | ||

| Life Sciences Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and future size of the Green IT software for healthcare market?

The Green IT software for healthcare market is valued at USD 1.82 billion in 2026 and is projected to reach USD 3.95 billion by 2031, growing at a 16.76% CAGR over 2026-2031.

What is driving demand for green IT software in healthcare organizations?

The main demand drivers are procurement-linked carbon reporting, growth in digital health infrastructure, cloud migration, and the rising energy burden of AI and data-heavy clinical systems.

Which application area is growing the fastest in this space?

ESG reporting and regulatory compliance is the fastest-growing application, with a projected 19.12% CAGR through 2031, because healthcare organizations need more formal and audit-ready disclosure tools.

Which deployment model is most widely used today?

Cloud-based deployment led with a 64% share in 2025, reflecting the push to move sustainability analytics away from energy-intensive local infrastructure.

Why do hospitals remain the largest end users?

Hospitals held 46% of end-user demand in 2025 because they operate large imaging archives, servers, and connected digital systems that create a sizable IT energy and emissions footprint.

Which region is growing the fastest and why?

Asia-Pacific is projected to grow at a 17.85% CAGR through 2031, supported by rising ESG disclosure needs, cloud modernization, and expanding use of AI-enabled reporting tools.

Page last updated on: