Green Chemistry In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 32.20 Billion |

| Market Size (2031) | USD 55.44 Billion |

| Growth Rate (2026 - 2031) | 11.48% CAGR |

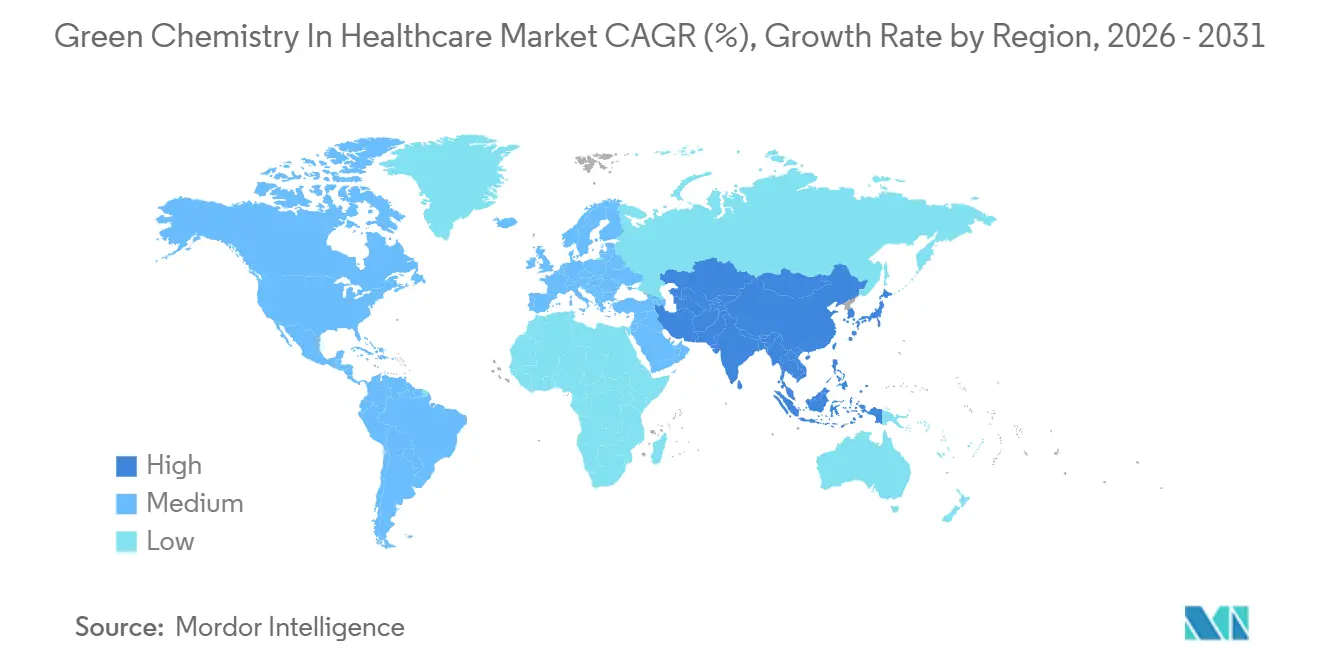

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green Chemistry In Healthcare Market Analysis by Mordor Intelligence

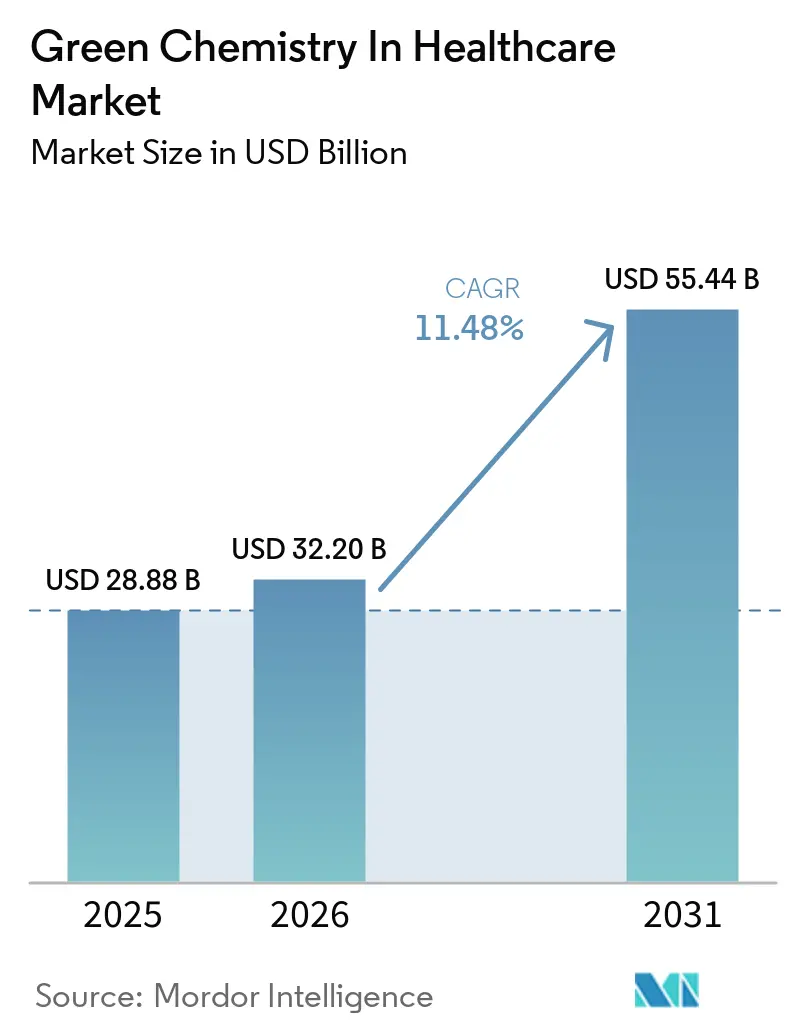

The Green Chemistry In Healthcare Market size is projected to expand from USD 28.88 billion in 2025 and USD 32.20 billion in 2026 to USD 55.44 billion by 2031, registering a CAGR of 11.48% between 2026 to 2031.

The acceleration of green chemistry in the healthcare market is driven less by voluntary program adoption and more by binding regulatory compulsion, led by the European Union’s 2026 pharmaceutical legislation that embeds environmental sustainability into marketing authorization frameworks. Reinforcements from residual solvent controls, such as the ICH Q3C(R9) reclassification of key solvents to stricter categories, are compressing timelines for substitution and removal strategies in drug substance routes. In the U.S., the EPA’s methylene chloride rule eliminates a widely used reagent from most pharmaceutical operations under TSCA in 2025, accelerating route redesign and solvent replacement. Procurement-led mandates are amplifying these shifts by tying supplier selection to measured environmental performance and decarbonization progress across Scope 1, 2, and 3, which further aligns capital allocation with pre-competitive sustainability baselines in the green chemistry in the healthcare market. The transition is supported by maturing enabling technologies and drop-in solutions, including bio-based HPLC solvents validated for analytical precision alongside continuous-flow platforms that make hazardous or heat-sensitive steps safer and more efficient at scale.

Key Report Takeaways

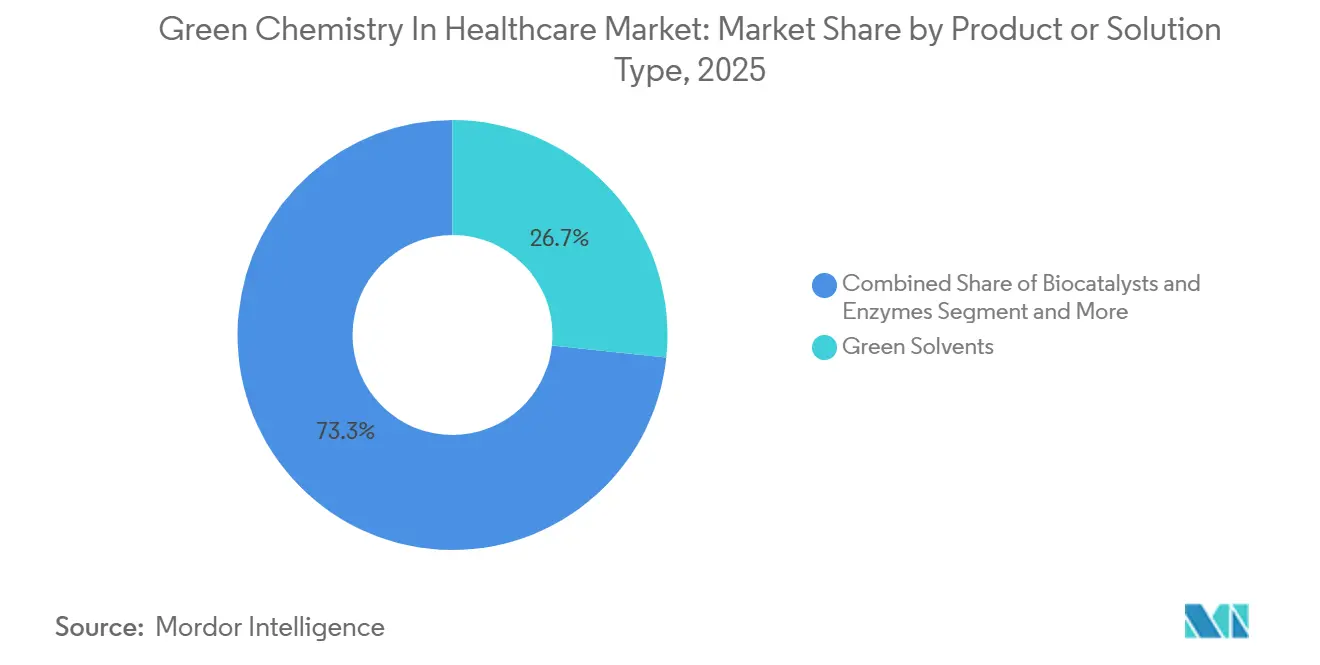

- By product/solution type, green solvents led with 26.67% revenue share in 2025, while biocatalysts & enzymes is forecast to expand at a 12.91% CAGR through 2031 in the green chemistry in healthcare market.

- By application, API synthesis accounted for 38.49% share in 2025, while biologics & vaccines is projected to grow at a 13.45% CAGR through 2031 in the green chemistry in healthcare market.

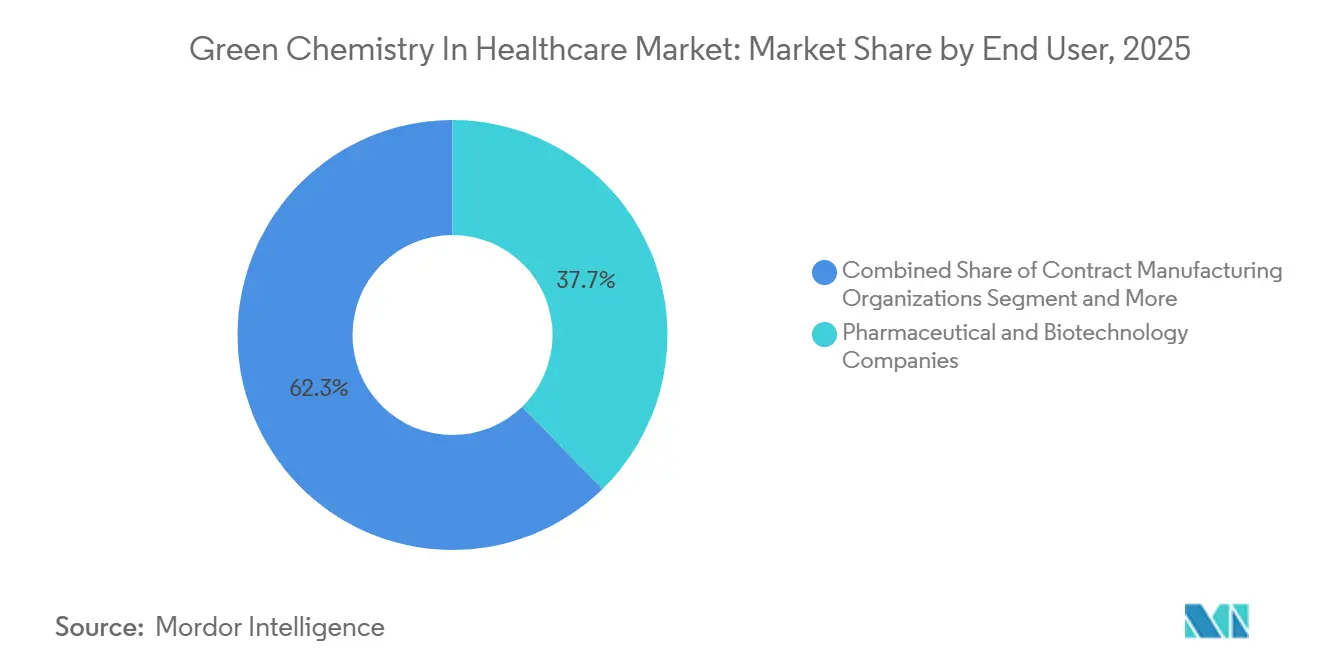

- By end user, pharmaceutical & biotechnology companies held 37.71% share in 2025, while CMOs/CDMOs are the fastest-growing at a 12.62% CAGR through 2031.

- By geography, North America led with 36.54% share in 2025, while Asia-Pacific is expected to register a 14.28% CAGR to 2031 in the green chemistry in healthcare market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Green Chemistry In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Pressure on Hazardous Solvents, Waste, and Emissions | +3.2% | Global, with strictest enforcement in EU & North America | Short term (≤ 2 years) |

| High Cost of Traditional API Manufacturing and Waste Disposal | +2.5% | Global, acute in high-labor-cost markets (US, EU, Japan) | Medium term (2-4 years) |

| ESG, Sustainability, and Net-Zero Commitments By Pharma and CDMOs | +2.8% | Global, led by EU & North America, expanding to APAC | Long term (≥ 4 years) |

| Maturation of Enabling Technologies (Flow, Biocatalysis, Analytics) | +2.1% | APAC manufacturing hubs, technology transfer to emerging markets | Medium term (2-4 years) |

| Procurement-Led Solvent Selection and Greener Sourcing Mandates | +1.4% | EU, expanding to UK & Germany | Short term (≤ 2 years) |

| Emergence of Mechanochemistry and Solvent-Free Processing in Route Design | +0.9% | Academic-industry partnerships in EU, Japan, pilot in US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure on Hazardous Solvents, Waste, and Emissions

The EU’s pharmaceutical legislation reform that takes effect in 2026 embeds environmental sustainability into the core of marketing authorization, pushing sponsors to include solvent use, lifecycle carbon, and environmental performance as part of their regulatory dossiers.[1]European Medicines Agency, “Reform of the EU Pharmaceutical Legislation,” European Medicines AgencyTightening solvent controls intensified in 2024 when ICH Q3C(R9) reclassified several common reagents into more stringent classes, raising the burden of proof for permitted daily exposures and driving substitution or enhanced removal strategies during API purification.[2]European Medicines Agency, “ICH Q3C (R9) Guideline on Impurities: Residual Solvents,” European Medicines Agency In parallel, the U.S. EPA’s methylene chloride rule under TSCA prohibits manufacture and most industrial uses by May 2025 except under narrow Workplace Chemical Protection Programs, which effectively eliminates an entrenched solvent from most pharmaceutical workflows.[3]U.S. Environmental Protection Agency, “Methylene Chloride Regulation Under TSCA,” U.S. Environmental Protection Agency These actions shrink fallback options for legacy solvent-intensive routes, accelerating adoption of bio-renewable alternatives such as Cyrene and 2-methyltetrahydrofuran that can meet performance needs in common couplings while reducing product carbon footprints. China’s new Ecological and Environmental Code, effective August 2026, raises accountability and enforcement risks for pharmaceutical executives, with penalties for falsified emissions reporting and standards for new projects, which shifts green route design from a discretionary practice to a hard compliance requirement across APAC operations.[4]ChemNet, “Ecological and Environmental Code to take effect in August,” ChemNet

High Cost of Traditional API Manufacturing and Waste Disposal

Hazardous pharmaceutical waste management imposes multi-step compliance obligations in the U.S., including manifesting, certified transport, and disposal at RCRA-permitted facilities, where non-compliance can result in significant penalties, which strengthens the cost case for waste-reducing routes that improve Process Mass Intensity.[5]Secure Waste, “EPA Final Rule on Hazardous Waste Pharmaceuticals,” Secure Waste The February 2025 technical corrections to hazardous waste regulations clarified triggers that can reclassify small quantity generators to large quantity generators at low acute waste thresholds, raising recurring compliance costs for organizations that operate multiple sites. Continuous processing provides a structural solution by reducing facility footprints and enabling better in-line controls for impurity profiles and solvent usage, which lowers energy and safety burdens compared to batch for select transformations. Capital challenges for smaller firms are being addressed through targeted investments from established players, including greenfield and retrofit programs in biotechnology and advanced manufacturing that expand access to greener operations. Industry initiatives that de-risk transitions through drop-in solutions, such as bio-based HPLC solvents that require no method redevelopment, help accelerate lab and QC integration while easing validation workloads upstream of manufacturing changes.

ESG, Sustainability, and Net-Zero Commitments By Pharma and CDMOs

Novartis, in April 2026, committed to achieving net-zero greenhouse gas emissions across the value chain by 2040, paired with interim milestones that include large absolute reductions in Scope 1 and 2 and material Scope 3 cuts by 2030, which makes supplier decarbonization a contract-level requirement. The same program requires API suppliers to deliver water-use reduction plans in water-stressed regions and ensure zero water-quality impact from manufacturing effluents, driving deeper process redesign and environmental controls at partner sites. Large CDMOs are also codifying environmental performance, as seen in WuXi Biologics’ reporting of up to 70% water savings and up to 80% product carbon footprint reduction per gram of protein through single-use platforms and process intensification at commercial scale. Sun Pharma reported substantial operational progress through a network of Zero Liquid Discharge facilities and increasing renewable energy share, indicating that major exporters are aligning to global sustainability baselines. Policy reinforcement through mandatory reporting rules in Europe increases the need for auditable, quantitative disclosures, which elevates green chemistry from a marketing theme to an enterprise performance metric across the green chemistry in healthcare market.

Maturation of Enabling Technologies (Flow, Biocatalysis, Analytics)

Continuous flow reactors have moved into mainstream deployment for complex reactions where heat and mass transfer control, safety, and multiphase handling are critical, with industrial platforms now supporting multi-step synthesis in a single unit while lowering energy demand. Biocatalysis has achieved step-change performance for oligonucleotides and small molecules, with Codexis reporting kilogram-scale enzymatic siRNA production and customer batches that achieve improved yields and lower waste versus phosphoramidite routes. Enzymatic control of stereochemistry in oligonucleotides, discussed publicly by Codexis, adds a quality lever that traditional chemistries struggle to match, which supports potency gains with cleaner impurity profiles. At the same time, drop-in innovations like bio-based HPLC solvents let labs and QC functions decarbonize without revalidating methods, creating rapid adoption paths for analytical operations that interface with manufacturing release. Together, these advances compress the gap between pilot proof-of-concept and industrial deployment, supporting a faster transition to low-solvent, energy-efficient processes across the green chemistry in healthcare market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Transition and Retrofitting Costs | -1.7% | Smaller CDMOs in APAC, Latin America; legacy EU/US plants | Medium term (2-4 years) |

| Regulatory and Validation Burden for Process Changes | -1.1% | FDA/EMA jurisdictions, cascading to ICH-aligned markets | Short term (≤ 2 years) |

| Bio-Based Feedstock Availability and Price Volatility Risks | -0.8% | Global, acute in regions dependent on agricultural commodities | Medium term (2-4 years) |

| Data Gaps/Greenwashing Risk; Need for Auditable LCA/PMI Metrics | -0.6% | EU, expanding to U.S. reporting | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Transition and Retrofitting Costs

Capital expenditure to retrofit batch facilities for continuous operations or to add biocatalytic infrastructure can be prohibitive for smaller CDMOs and generic manufacturers, extending timelines for green process adoption. Real-world transition programs underscore multi-year arcs, illustrated by Codexis’ 2025 lease and subsequent retrofit toward kilogram-scale enzymatic production capability by the end of 2027. While sustainability-linked financing and grants can lower the hurdle rate, access remains uneven across regions and company sizes, producing staggered adoption across the green chemistry in the healthcare market. Incremental expansions by incumbents demonstrate scale economics that smaller firms cannot easily match, such as Evonik’s EUR 80 million investment to add advanced fermentation and downstream capabilities for drug substances. As large players standardize green process equipment and analytics across global networks, suppliers without comparable capital flexibility may defer upgrades until procurement penalties outweigh retrofit costs.

Regulatory and Validation Burden for Process Changes

Post-approval process changes require comparability, impurity-profile assessment, and often stability bridging, which slows adoption of novel unit operations that minimize solvents or energy use. The absence of extensive precedents for GMP-qualified mechanochemical equipment and for solvent-minimized unit ops in filings adds uncertainty to implementation timelines for conservative sponsors. By contrast, regulator engagement with enzymatic oligonucleotide synthesis demonstrates that compelling data packages can unlock adoption, which suggests a path for other high-impact green changes as analytical frameworks mature. Drop-in solutions that preserve methods and performance, such as bio-based HPLC solvents, present a lower regulatory burden and are therefore seeing faster uptake in analytical and QC areas. The interplay of validation workload and available regulatory precedents will continue to determine the pace of change across the green chemistry in healthcare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product/Solution Type: Biocatalysts Command Fastest Growth as Enzyme Economics Shift

Green Solvents captured 26.67% of the green chemistry in healthcare market share in 2025, reflecting fast adoption of drop-in replacements in labs and upstream development that must comply with tighter solvent controls. In April 2026, Merck launched bio-based HPLC solvents that are designed as direct substitutes for fossil equivalents, enabling analytical teams to decarbonize without changing validated methods. BASF’s Intermediates division converted its acid chlorides and chloroformates production at Ludwigshafen to 100% renewable electricity credits, reporting meaningful product carbon footprint reduction while also modernizing assets for added volume. EU-backed industrialization of Cyrene expanded supply for a cellulose-derived dipolar aprotic solvent that helps replace NMP and DMF in medicinal chemistry while improving worker safety and lifecycle profiles. ICH Q3C(R9) tightened the exposure limits for several widely used reagents, which makes solvent substitution and enhanced removal a near-term priority during route design and API purification. The U.S. methylene chloride rule removes a common fallback option for process validation, pushing teams to re-examine dipolar aprotics and greener reaction media earlier in development.

The biocatalysts & enzymes segment is projected to expand at a 12.91% CAGR through 2031 for the green chemistry in the healthcare market size as enzyme discovery, evolution, and process engineering converge to deliver industrial performance. Codexis reported progression from gram to kilogram-scale enzymatic siRNA production, with customers executing multi-kilogram batches using its ligase-catalyzed routes, which shows scalability and reduced waste compared to phosphoramidite chemistry. In small molecules, industrial KREDs and transaminases have delivered route shortcuts and safer reductions at commercial scale, with published cases demonstrating high stereopurity and elimination of hazardous hydride reagents. Process-intensification technologies complement these gains, with advanced-flow reactors enabling safer handling of reactive intermediates while controlling heat and mass transfer with precision. Renewable and biomass-balanced inputs are increasingly available for core intermediates, adding certified low-PCF feedstocks that reduce lifecycle burdens when paired with green catalytic steps. Green auxiliaries and excipients, backed by medicine-specific carbon accounting methodologies, are also gaining traction for formulation teams that need credible, audit-ready metrics for supplier selection.

By Application: Biologics & Vaccines Surge as Single-Use Systems Demonstrate PCF Advantages

API Synthesis held a 38.49% share in 2025 as the application with the largest environmental baseline and the greatest exposure to solvent regulation, removal controls, and waste compliance. Flow systems support reaction safety, high heat-flux steps, and hazardous intermediates, which enable greener designs that are hard to replicate in traditional batch at scale. Residual solvent rules compel earlier and broader adoption of alternative solvents in route development, which improves PMI and simplifies regulatory submissions downstream. Labs and QC organizations are also decarbonizing with bio-based HPLC solvents that retain analytical performance, which shortens the transition cycle for broader enterprise programs. The U.S. methylene chloride rule boosts the case for complete route redesign where legacy steps were anchored to now-prohibited reagents.

Biologics & Vaccines is advancing at a 13.45% CAGR through 2031 in the green chemistry in the healthcare market as single-use platforms, perfusion, and renewable electricity converge to lower resource intensity. WuXi Biologics has reported up to 70% water savings and up to 80% product carbon footprint reduction per gram of protein through integrated platform changes, which signals a maturing playbook for scaling greener biologics. Amgen’s fully electric Ohio site and modular designs show how facility-level electrification and on-site renewables are moving from pilots to standard features in new builds. Procurement mandates from large buyers favor CDMOs that can evidence renewable electricity across contracted production and demonstrate water stewardship programs in stress areas. On the formulation side, eco-design commitments and packaging changes with timelines to remove plastics signal steady reductions in downstream waste, which complements process-side improvements.

By End User: CMOs/CDMOs Accelerate Adoption to Secure Procurement Advantage

Pharmaceutical & Biotechnology Companies held 37.71% of the green chemistry in the healthcare market share in 2025, supported by direct regulatory accountability and investor scrutiny that ties sustainability to capital access. Enterprise green chemistry frameworks are now part of R&D and manufacturing governance, with recognition programs and awards reinforcing tangible reductions in energy, water, and waste. Novartis’ 2040 net-zero commitment and supplier requirements on water and effluent management formalize sustainability as a sourcing criterion for API partners. Public disclosures from major exporters reporting ZLD operations and rising renewable energy shares signal convergence toward stricter baselines that align with EU and U.S. expectations. The regulatory foundation in Europe that embeds environmental performance into marketing approvals further hardwires green process requirements into innovator-roadmaps and partner expectations.

CMOs/CDMOs are the fastest-growing end-user group at a 12.62% CAGR through 2031 as buyers use environmental scoring and contract clauses to direct volumes to greener capacity. WuXi Biologics’ “Green CRDMO” practices, including single-use systems and high-productivity upstream platforms, demonstrate how CDMOs can deliver step-change reductions in resource use while meeting commercial-scale quality requirements. Capacity investments at leading providers signal a sustained shift toward biotechnology-based routes and greener manufacturing toolkits. Membership moves into green chemistry roundtables and consortia, indicating strategic prioritization of sustainable process development capabilities that can satisfy sponsor audits. Procurement programs that call for renewable electricity and water stewardship plans in specific regions solidify the economic case for CDMO investments in decarbonization and advanced solvent management.

Geography Analysis

North America commanded 36.54% of the green chemistry in healthcare market size in 2025, supported by early regulatory action and high levels of disclosure that align with investor expectations. The EPA’s final rule for methylene chloride under TSCA, effective May 2025 for most industrial uses, precipitated rapid assessments and substitutions for legacy steps that depended on the solvent. Progress on solvent-class reclassification and impurity control frameworks also informs U.S. route designs that target lower PMI and cleaner purification profiles in alignment with global expectations. North American sites are scaling continuous-flow strategies that enhance control of hazardous or exothermic reactions while shrinking energy loads, which supports green objectives without sacrificing throughput. Drop-in bio-based HPLC solvents for analytical labs further reduce carbon equivalents with no method redevelopment, making decarbonization in R&D and QC faster and less risky.

Asia-Pacific is the fastest-growing region at a 14.28% CAGR through 2031, driven by China’s regulatory enforcement, expanding production networks, and rapid technology transfer. China’s Ecological and Environmental Code, effective August 2026, imposes accountability for environmental data integrity, establishes red lines for new projects, and strengthens penalties for unlawful emissions, which heightens the value of solvent-reducing routes and certified inputs. Provisions that legalize carbon trading expand economic incentives for early movers able to beat benchmarks and sell surplus allowances. APAC manufacturing hubs continue to integrate advanced-flow reactors and in-line analytical systems that enable safer, high-efficiency transformations across key intermediates. Broader availability of biomass-balanced intermediates and certified low-PCF inputs in regional supply chains strengthens the case for adopting greener routes at scale in export-focused plants.

Europe’s market is being reshaped by the EU’s 2026 pharmaceutical legislation that embeds environmental sustainability into marketing authorization decisions and drives submissions to include lifecycle performance evidence. The One Substance One Assessment initiative, which begins pooling chemical data and assessments across multiple EU agencies, will expand cross-check visibility and raise the bar for consistency in environmental claims. Industrial scale-up of greener solvents such as Cyrene within the EU demonstrates progress from development to reliable supply, which supports regional route conversions and substitution for hazardous dipolar aprotics. Packaging and eco-design commitments from European manufacturers point to ongoing reductions in downstream waste and plastic use over near-term timelines. As audited ESG reporting expands, procurement teams in Europe will continue to favor suppliers with documented renewable energy sourcing, water stewardship, and certified inputs, which reinforces the momentum of green chemistry in the healthcare market.

Competitive Landscape

The green chemistry in the healthcare market remains moderately fragmented, with chemical majors, API innovators, and CDMOs competing on demonstrated reductions in carbon, water, and waste rather than price alone. Industrial leaders are using capital programs to hardwire sustainability into production, as shown by investments in fermentation and downstream biotechnology platforms for drug substance manufacturing in Central Europe that add flexible capacity aligned with green process goals. Analytical operations are decarbonizing through drop-in solvent portfolios that preserve precision, helping organizations realize quick wins while they concurrently evaluate deeper manufacturing changes. On the process side, continuous-flow reactors that support dangerous or sensitive transformations have matured into configurable systems with integrated heat, mass transfer, and safety control, enabling greener processes with industrial reliability. Biocatalysis continues to scale, with kilogram-level enzymatic oligonucleotide manufacturing indicating that greener, high-selectivity enzymatic routes are now production-viable.

Green Chemistry In Healthcare Industry Leaders

BASF SE

Evonik Industries AG

Solvay S.A.

Codexis, Inc.

Corning, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Merck launched a bio-based solvent portfolio for high-performance liquid chromatography (HPLC), including acetonitrile, methanol, and ethanol derived from renewable feedstocks. The products were designed as drop-in replacements for conventional solvents without compromising performance. The portfolio reduced CO₂ equivalents, supporting sustainable laboratory and pharmaceutical processes. The launch reinforced Merck’s focus on green chemistry solutions in healthcare.

- March 2026: Codexis reported progress in enzymatic RNA manufacturing, including a technology transfer agreement and a successful 10 g siRNA run using fully enzymatic synthesis. The company also completed a 3 kg batch via a ligase-based route for a customer program. In parallel, Codexis advanced development of a GMP manufacturing facility expected to be operational by the end of 2027. The update highlighted its expansion in sustainable biocatalytic manufacturing.

- March 2026: Codexis entered into an agreement to manufacture 50 g of siRNA using its ECO Synthesis Manufacturing Platform for an innovator’s preclinical cardiovascular program. The platform utilized enzyme-driven processes to improve efficiency and reduce chemical waste. The collaboration demonstrated growing adoption of green chemistry technologies in nucleic acid therapeutics. It further strengthened Codexis’ position in sustainable pharmaceutical manufacturing.

Global Green Chemistry In Healthcare Market Report Scope

As per the scope of the report, green chemistry in healthcare refers to the application of green chemistry principles specifically within pharmaceutical, biotechnology, and medical device manufacturing. It focuses on designing drug, biologic, and diagnostic production processes that reduce or eliminate hazardous solvents, reagents, and waste, while improving safety and environmental performance. It emphasizes safer solvents, biocatalysis, renewable feedstocks, and cleaner synthesis routes to make healthcare manufacturing more sustainable.

The green chemistry in the healthcare market is segmented by product/solution type, application, end user, and geography. By product/solution type, the market is segmented into Green Solvents, biocatalysts & enzymes, renewable/bio‑based feedstocks, process‑intensification technologies, and green auxiliaries & additives. By application, the market is segmented into API synthesis, biologics & vaccines manufacturing, formulation & dosage forms, and diagnostics & medical devices. By end user, the market is segmented into pharmaceutical & biotechnology companies, contract manufacturing organizations, hospitals & healthcare facilities, and research & academic institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Green Solvents |

| Biocatalysts & Enzymes |

| Renewable/Bio-based Feedstocks |

| Process-intensification Technologies |

| Green Auxiliaries & Additives |

| API Synthesis |

| Biologics & Vaccines Manufacturing |

| Formulation & Dosage Forms |

| Diagnostics & Medical Devices |

| Pharmaceutical & Biotechnology Companies |

| Contract Manufacturing Organizations (CMOs/CDMOs) |

| Hospitals & Healthcare Facilities |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product/Solution Type | Green Solvents | |

| Biocatalysts & Enzymes | ||

| Renewable/Bio-based Feedstocks | ||

| Process-intensification Technologies | ||

| Green Auxiliaries & Additives | ||

| By Application | API Synthesis | |

| Biologics & Vaccines Manufacturing | ||

| Formulation & Dosage Forms | ||

| Diagnostics & Medical Devices | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Contract Manufacturing Organizations (CMOs/CDMOs) | ||

| Hospitals & Healthcare Facilities | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What changes in 2026 make green chemistry a compliance priority in healthcare and pharma?

EU pharmaceutical legislation embeds environmental sustainability into marketing authorizations starting in 2026, requiring lifecycle and solvent metrics in submissions. Tightened residual solvent rules and the U.S. methylene chloride regulation further constrain legacy options and accelerate substitution.

Which parts of healthcare manufacturing show the fastest sustainability gains now?

Biologics and vaccines operations report large reductions in water use and product carbon footprint with single-use platforms and high productivity perfusion. New facilities are electrifying operations with on-site renewables to cut energy and emissions.

How are enabling technologies like flow chemistry and biocatalysis changing process design?

Advanced-flow reactors allow safer scale-up of hazardous or heat sensitive steps with tighter control and lower energy needs. Enzymatic oligonucleotide routes have reached kilogram scale with higher yields and less waste than traditional methods.

How do large buyers influence supplier adoption of greener processes?

Procurement programs require renewable electricity, water stewardship, and audited Scope 1-3 disclosures, which favor suppliers that document verifiable improvements. Certified low-carbon inputs such as biomass-balanced intermediates expand options for route redesign with traceable reductions.

What solvent regulations matter most for near-term route redesign?

ICH Q3C(R9) reclassified several solvents to stricter classes, raising proof burdens for permitted exposure and pushing substitution or enhanced removal in API steps. The U.S. rule on methylene chloride removes a common reagent from most industrial use, which advances earlier redesign decisions.

What are the biggest hurdles to implementing greener processes at scale?

Upfront retrofit costs for continuous and biocatalytic infrastructure and multi-year build timelines slow adoption for smaller suppliers. Drop-in solutions like bio-based HPLC solvents gain faster traction in labs and QC because they avoid method revalidation.

Page last updated on: