Greece Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

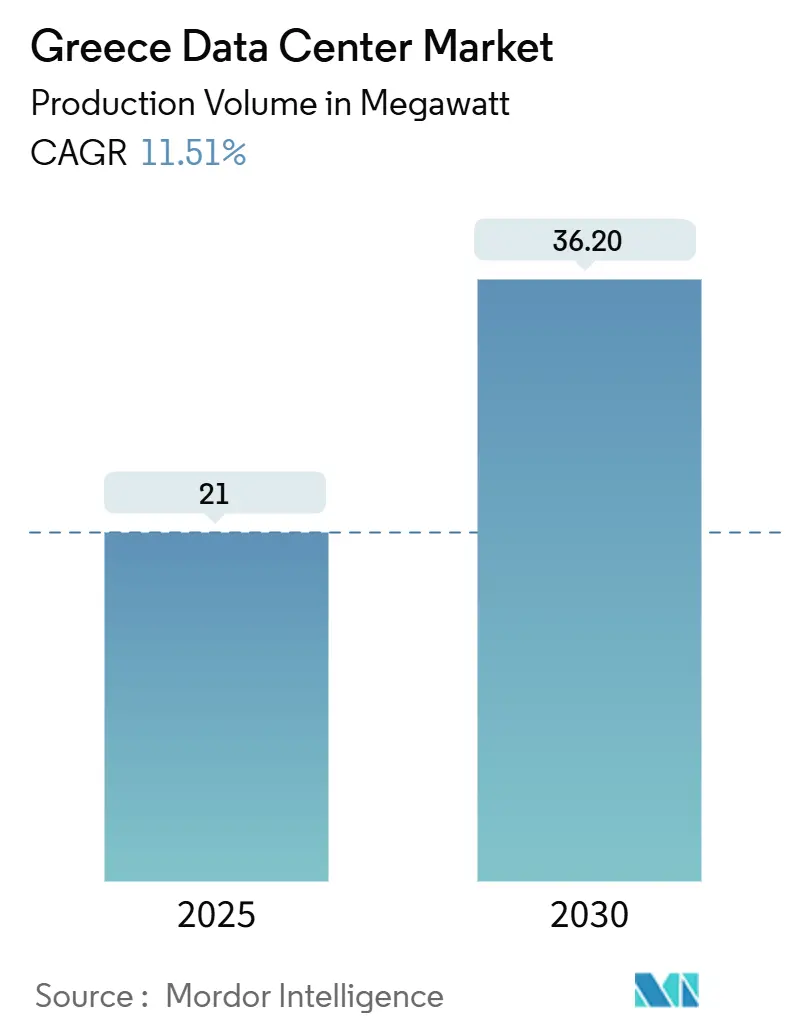

| Market Volume (2025) | 21 megawatt |

| Market Volume (2030) | 36.20 megawatt |

| Growth Rate (2025 - 2030) | 11.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Data Center Market Analysis by Mordor Intelligence

The Greece data center market size stands at 21 MW in 2025 and is projected to reach 36.2 MW by 2030, reflecting an 11.51% CAGR. The Greece data center market benefits from EU Recovery and Resilience Facility funding, new submarine cable landings, and a cloud-first public-sector mandate that collectively accelerate demand for colocation and hyperscale capacity. Latency advantages created by BlueMed, Blue-Raman, and MEDUSA cables attract global cloud and content providers that require fast traffic routes between Europe, Africa, and Asia. Operators are intensifying renewable-energy procurement to offset Europe’s highest wholesale electricity prices, and earthquake-resilient construction standards are prompting design innovation that supports high-density deployments. As the Greece data center market matures, competitive strategies center on scale, grid access, and advanced cooling, positioning the country as a Mediterranean digital hub.

Key Report Takeaways

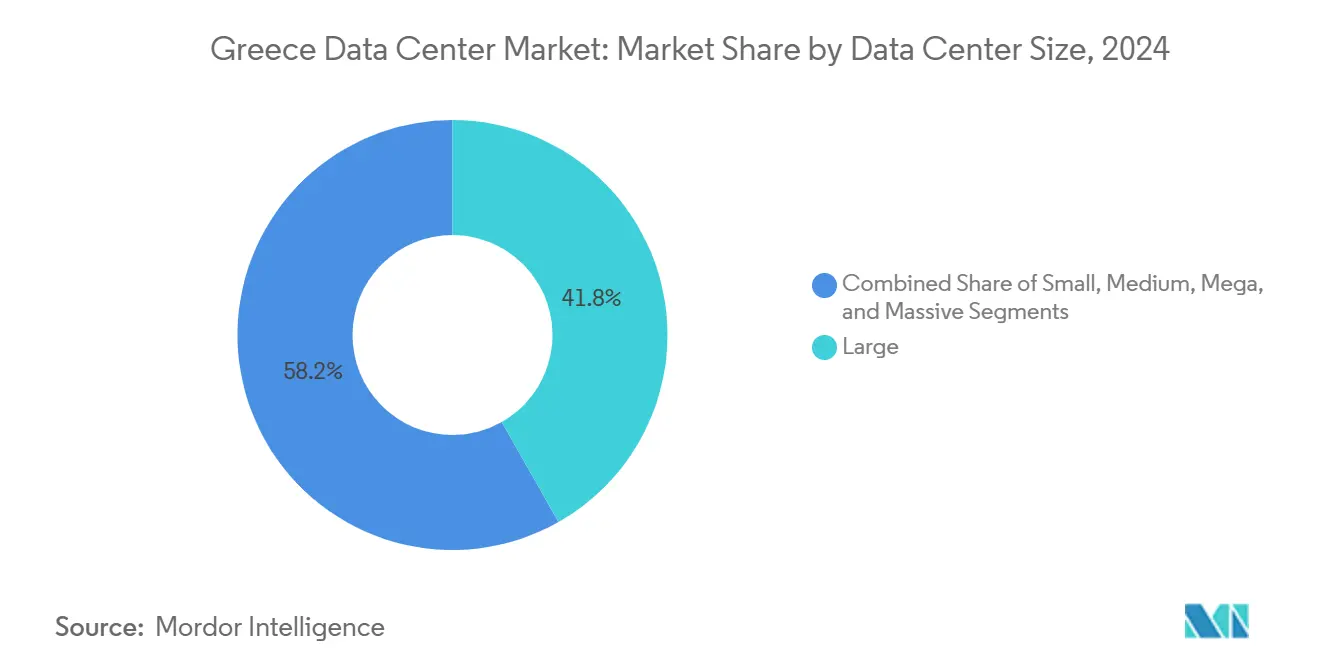

- By data-center size, large facilities held 41.8% of the Greece data center market share in 2024, while mega sites are forecast to advance at an 18.9% CAGR through 2030.

- By tier standard, Tier III installations captured 52% share of the Greece data center market size in 2024, and Tier IV facilities are expanding at a 17.3% CAGR through 2030.

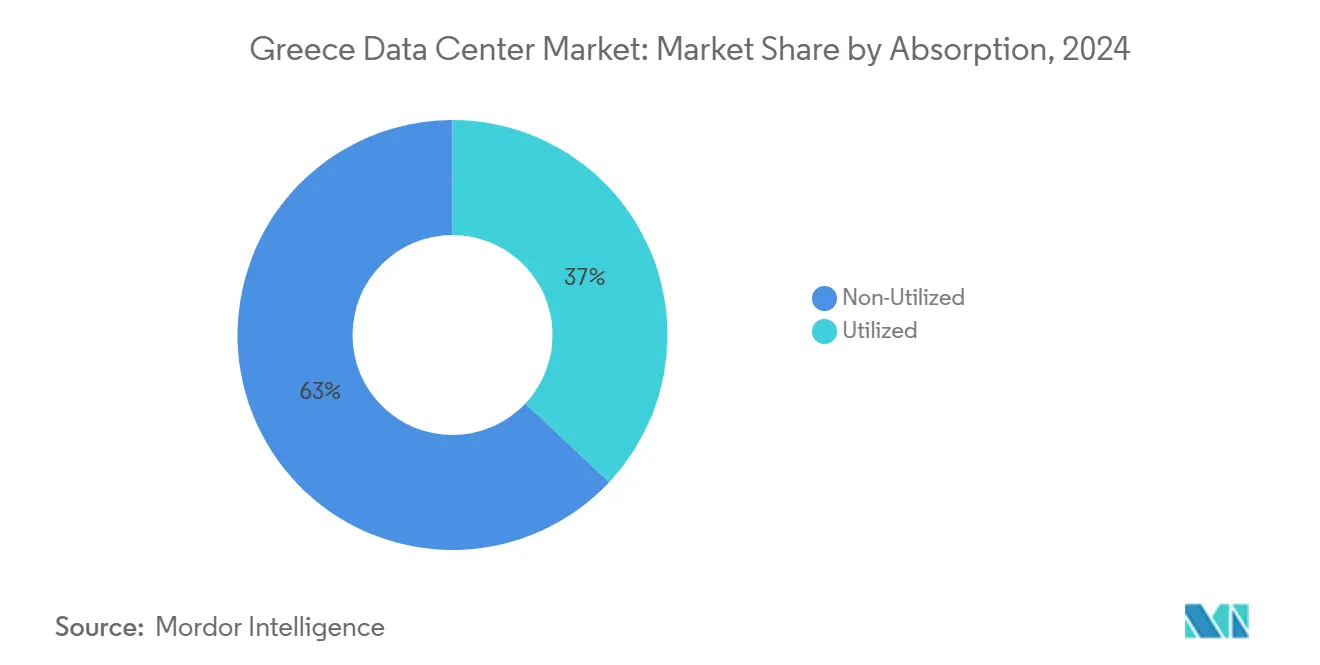

- By absorption, utilized capacity accounted for 37% of the Greece data center market size in 2024 and is tracking a 15.5% CAGR to 2030.

- By hotspot, Athens commanded 68% of the Greece data center market share in 2024, whereas Thessaloniki is accelerating at a 16.7% CAGR through 2030.

Greece Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National cloud-first strategy and EU RRF funds | +2.80% | Athens and Thessaloniki | Medium term (2-4 years) |

| Rapid fibre rollout and neutral IXPs | +1.90% | Athens-Thessaloniki corridor | Short term (≤2 years) |

| 5G-driven mobile-data boom | +1.50% | Urban centers | Medium term (2-4 years) |

| Surge in AI/ML workloads from shipping and fintech | +2.10% | Athens and Piraeus | Long term (≥4 years) |

| Mediterranean submarine-cable landings | +1.70% | Crete and other coastal nodes | Long term (≥4 years) |

| Repatriation of Greek-origin data | +1.20% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Cloud-First Strategy Accelerates Infrastructure Demand

Government policy allocates EUR 6.4 billion (USD 7.41 billion) toward 450 digitization projects that anchor long-term demand for colocation space.[1]International Trade Administration, “Greece Digital Transformation Plan,” trade.gov Ministries are migrating workloads to cloud-native environments to meet the 2025 digitization deadline. The portal already processes 275 million annual transactions, underscoring the rising compute intensity. Public-sector migration stabilizes utilization rates, encouraging operators to invest ahead of demand. Because domestic data residency is mandatory, the Greece data center market gains strategic importance for EU institutions seeking alternatives to non-European hyperscalers. The policy, therefore, establishes a predictable revenue base while enhancing national digital sovereignty.

Submarine Cable Infrastructure Creates Latency Arbitrage Opportunities

BlueMed, Blue-Raman, and MEDUSA cables collectively bypass congested Egyptian pathways, offering up to 50% lower latency for Middle East European traffic.[2]Sparkle, “Sparkle to Build Blue and Raman Submarine Cable Systems,” tisparkle.comGoogle’s Blue cable adds diverse routes, while Grid Telecom’s new landing station in Crete deepens regional reach. These routes enable operators to charge premium rack rates for latency-sensitive workloads, such as gaming and finance. The resulting traffic aggregation reinforces the Greece data center market as a preferred hand-off point between three continents. Improved connectivity also supports edge deployments that shorten data paths for new 5G and IoT services.

5G Network Expansion Drives Edge Computing Requirements

OTE and Vodafone have committed more than EUR 1 billion (USD 1.16 billion) each to extend fibre and 5G coverage, enabling 1 Gbps mobile speeds in Athens and Thessaloniki. Network-function virtualization increases data-centre compute demand, and micro-data-centre rollouts at tower sites lower latency for AR/VR and smart-city applications. FTTH investments create fibre-rich zones that colocation providers can monetize through carrier-neutral meet-me rooms. As smartphone and IoT traffic scales, the Greece data center market absorbs new edge capacity rather than expanding central sites alone.

Surge in AI/ML Workloads in Maritime and Financial Sectors

Greek shipping firms that manage 20% of global tonnage now deploy AI for predictive maintenance and route optimization. Banks adopt machine-learning tools for fraud detection, exemplified by Piraeus Bank’s flash-storage upgrade. Demokritos is building an AI hub that requires GPU clusters, anchoring specialized high-performance colocation. High-density racks and liquid cooling become essential, and operators able to guarantee 99.995% uptime capture these premium contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-grid congestion and high wholesale prices | -2.10% | Athens metro | Short term (≤2 years) |

| Earthquake-related construction standards raise CAPEX | -1.30% | All seismic zones | Medium term (2-4 years) |

| Scarcity of utility-scale green-energy PPAs | -0.90% | National | Long term (≥4 years) |

| Complex archaeological permitting delays | -0.70% | Athens and Thessaloniki | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power Grid Constraints Create Operational Cost Pressures

Wholesale electricity averaged EUR 0.1038 per kWh in 2024, the highest rate in Europe, which squeezes margins for facilities exceeding 10 MW.[3]Institute of Energy for Southeast Europe, “Greece’s Wholesale Electricity Prices Are Highest in Europe,” iene.eu IPTO is deploying EUR 4.1 billion (USD 4.74 billion) to modernize transmission lines, yet relief will take years. To hedge volatility, operators pursue on-site solar and long-term PPAs, following Microsoft’s photovoltaic strategy in Attica. High power costs favor players with scale and energy-buying leverage, intensifying consolidation within the Greece data center market.

Seismic Construction Standards Increase Development Costs

Law 5069/2023 mandates earthquake-resistant designs that add up to 20% to build costs for Zone 5 sites. Horizontal layouts required by 14-meter height limits increase land purchases in high-priced Athens districts. Smaller entrants lacking structural-engineering expertise struggle to compete, while established operators turn compliance into a reliability differentiator for financial and government clients demanding fault tolerance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Size: Mega Facilities Drive Hyperscale Consolidation

Mega facilities represent the fastest-growing slice of the Greece data center market, expanding at an 18.9% CAGR as hyperscale operators seek single-campus capacities above 20 MW. Large sites still dominate volumes, holding 41.8% of the Greece data center market size in 2024. Microsoft’s three-building complex in Attica typifies mega builds that integrate on-site solar to offset grid congestion.

The Greece data center market favors mega campuses because they unlock economies of scale in power procurement, cooling design, and operations staffing. Operators deploy liquid-to-chip cooling to support AI clusters, and larger electrical backbones facilitate 1.5 kW-plus per square foot densities. Massive facilities above 50 MW remain rare but are planned by Data4 for delivery in 2027, foreshadowing future hyperscale clustering near new submarine-cable landings in Crete.

By Tier Standard: Tier IV Growth Reflects Mission-Critical Demand

Tier III data centers commanded 52% of the Greece data center market size in 2024, striking a cost-reliability balance that satisfies most enterprise applications. Demand for Tier IV, however, is climbing at 17.3% CAGR on the back of fintech and sovereign-cloud workloads that cannot tolerate downtime.

Financial institutions require dual active-active architectures, pushing suppliers to build fault-tolerant mechanical and electrical systems. The Greece data center market therefore sees rising orders for concurrently maintainable generators, 2N UPS topology, and geophysical monitoring. Although capital intensive, Tier IV projects secure longer contracts and higher margin, offsetting build-cost premiums triggered by seismic codes.

By Absorption: Utilized Capacity Optimization Precedes Expansion

Utilized capacity made up 37% of total absorption in 2024 and is set to grow at 15.5% CAGR as operators prioritize rack density and hot-aisle containment over greenfield builds. Higher utilization raises return on invested capital and aligns with investor calls for disciplined expansion.

Hyperscale tenants negotiate wholesale rooms from 5 MW upward, encouraging landlords to retrofit existing halls with 80 kW cabinets capable of direct-to-chip cooling. Retail colocation continues to serve SMEs, yet its share slips as cloud on-ramp traffic accelerates. Non-utilized footprints, despite offering growth runway, face scrutiny over stranded capital, reinforcing a lean-deployment mindset across the Greece data center market.

By Hotspot: Thessaloniki Emerges as Cost-Effective Alternative

Athens retained 68% share of installed capacity in 2024 thanks to dense fibre, cable landings, and financial-sector demand. Grid bottlenecks and real-estate prices, however, nudge new projects northward. Thessaloniki, growing at 16.7% CAGR, offers lower land costs and proximity to Balkan users that value single-digit millisecond latency.

Operators also eye Crete for edge sites that capitalize on fresh submarine-cable routes. Island deployments pair well with solar-plus-battery microgrids, helping the Greece data center market align with renewable-energy targets. Geographic diversification spreads seismic risk and shortens content delivery paths, enhancing national network resilience.

Geography Analysis

Athens remains Greece’s principal colocation hub, supported by submarine-cable landings, financial-services density, and government IT procurement. Microsoft’s EUR 1 billion (USD 1.16 billion) program underscores sustained confidence despite higher costs and permitting complexity. AWS Direct Connect at Digital Realty’s campus further upgrades the city’s interconnection fabric, enabling enterprises to secure deterministic routes into public clouds. Continuous infill expansion, however, is tempered by grid congestion that elevates total cost of ownership.

Thessaloniki’s 16.7% CAGR mirrors its emerging role as a Balkan gateway. The metro leverages IPTO’s grid-modernization corridor and benefits from wind-rich hinterlands that support renewable PPAs. University research clusters generate skilled labor supply while lower real-estate prices attract disaster-recovery and back-office functions migrating from Athens. The city’s mounting share helps balance the Greece data center market geographically, reducing systemic exposure to Attica’s seismic risk.

Rest-of-Greece activity ranges from Crete’s cable-landing edge nodes to island micro-data-centers that host tourism and e-government workloads. Renewable developers bundle solar farms with containerized compute, offering sub-EUR 0.05 per kWh power where transmission capacity exists. Such provincial deployments advance national digital-inclusion goals and provide resilience against localized power or network outages.

Competitive Landscape

International entrants are consolidating a market once dominated by local telco data halls. Digital Realty’s Lamda Hellix buyout created the largest platform, now augmented by AWS on-ramp services. Microsoft’s hyperscale campus signals a shift toward cloud-led ecosystems that spur supplier clustering in cooling, power, and security services. IPTO’s joint venture with Serverfarm formalizes utility collaboration, potentially accelerating substation approvals and lowering interconnection fees.

Scale is the principal competitive lever within the Greece data center market. Operators with 20 MW-plus campuses secure bulk power at better rates and justify investments in liquid cooling that supports AI training jobs. Meanwhile, smaller Greek telcos focus on edge suites and managed services, defending share through localized support and metro fibre bundles. Strategic alliances with cable consortia give operators differentiated SLAs built on guaranteed sub-10 ms round-trip times to Milan and Marseille.

Innovation pivots around sustainability and automation. Liquid-to-chip cooling deployed by Digital Realty lifts rack densities to 100 kW while trimming water consumption. Early-stage players explore immersion cooling and AI-based energy-management platforms that flatten peak loads. Renewable-energy developers eye co-location as an offtake hedge, blending solar or wind output with predictable data-center demand curves. The resulting ecosystem raises entry barriers, pushing the Greece data center market toward moderate concentration.

Greece Data Center Industry Leaders

Digital Realty (Lamda Hellix)

Microsoft

Google

Telecom Italia Sparkle

OVHcloud

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Digital Realty's Athens Data Center Campus was selected by AWS for a new AWS Direct Connect location.

- June 2025: The Blue-Raman submarine-cable project received additional EU Global Gateway funding support.

- December 2024: IPTO and Serverfarm formed a joint venture to develop hyperscale data centers in Greece.

- May 2024: Digital Realty unveiled liquid-to-chip cooling support for high-density deployments.

- May 2024: Sparkle activated the BlueMed submarine cable connection to Chania, Crete.

- April 2024: National Research Center Demokritos announced plans for a new data center and AI hub.

Greece Data Center Market Report Scope

Greece Data Center Market is Segmented by Data Center Size (Small, Medium, Large, Mega, Massive), Tier Standard (Tier I and II, Tier III, and Tier IV), Absorption (Non-Utilized, Utilized (Colocation Type (Hyperscale, Retail, Wholesale), End-User (BFSI, Cloud Service Providers, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End-Users)), and Hotspot (Athens, Thessaloniki, Rest of Greece). The Market Forecasts are Provided in Terms of Volume (MW Capacity).

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Athens |

| Thessaloniki |

| Rest of Greece |

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| By Hotspot | Athens | ||

| Thessaloniki | |||

| Rest of Greece | |||

Key Questions Answered in the Report

How large is the Greece data center market in 2025?

It stands at 21 MW and is projected to reach 36.2 MW by 2030.

Which Greek city hosts most data-center capacity?

Athens holds 68% of installed power and remains the primary hub.

Why are mega data centers gaining momentum in Greece?

Hyperscale operators favor single campuses above 20 MW to achieve power-purchase leverage and support AI-ready cooling.

What is the main challenge facing operators?

High wholesale electricity prices and grid congestion raise operating costs, especially in Attica.

How fast is the Thessaloniki cluster growing?

Capacity in Thessaloniki is advancing at a 16.7% CAGR through 2030.

Which tier of facility is expanding fastest?

Tier IV data centers are growing at a 17.3% CAGR due to demand for 99.995% uptime.

Page last updated on: