Colombia Grains Market Analysis by Mordor Intelligence

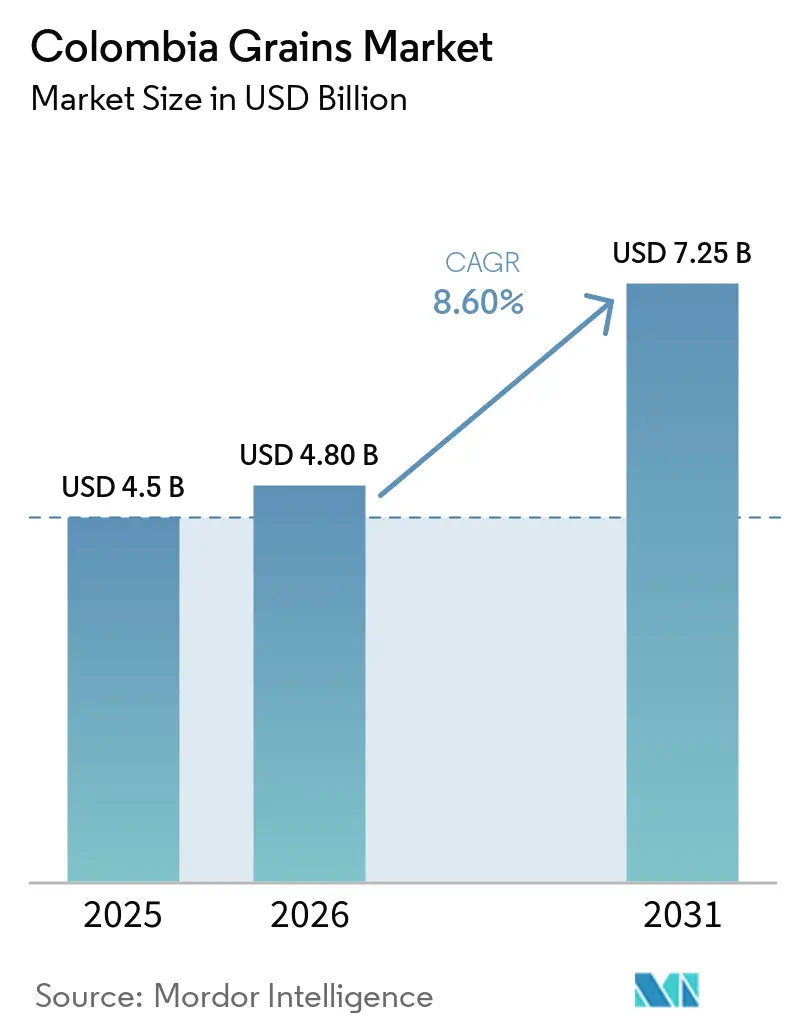

The Colombia grains market is projected to grow from USD 4.5 billion in 2025 and USD 4.8 billion in 2026 to USD 7.25 billion by 2031, with a CAGR of 8.6% during the period from 2026 to 2031. The market is highly dependent on imports, making it susceptible to factors such as currency fluctuations, port efficiency, and government policies that influence import costs and supply stability. Demand is largely driven by the livestock sector, particularly poultry and swine, while urban consumption supports the growth of processed foods. Government interventions, including subsidies, play a significant role in stabilizing domestic production and affecting profitability across the value chain. Upgrades to port infrastructure are enhancing logistics efficiency, benefiting larger players more than smallholders. Market competition is concentrated among major processors and global traders, while challenges such as crop diseases, climate variability, and an aging farming population pose risks to long-term supply resilience.

Key Report Takeaways

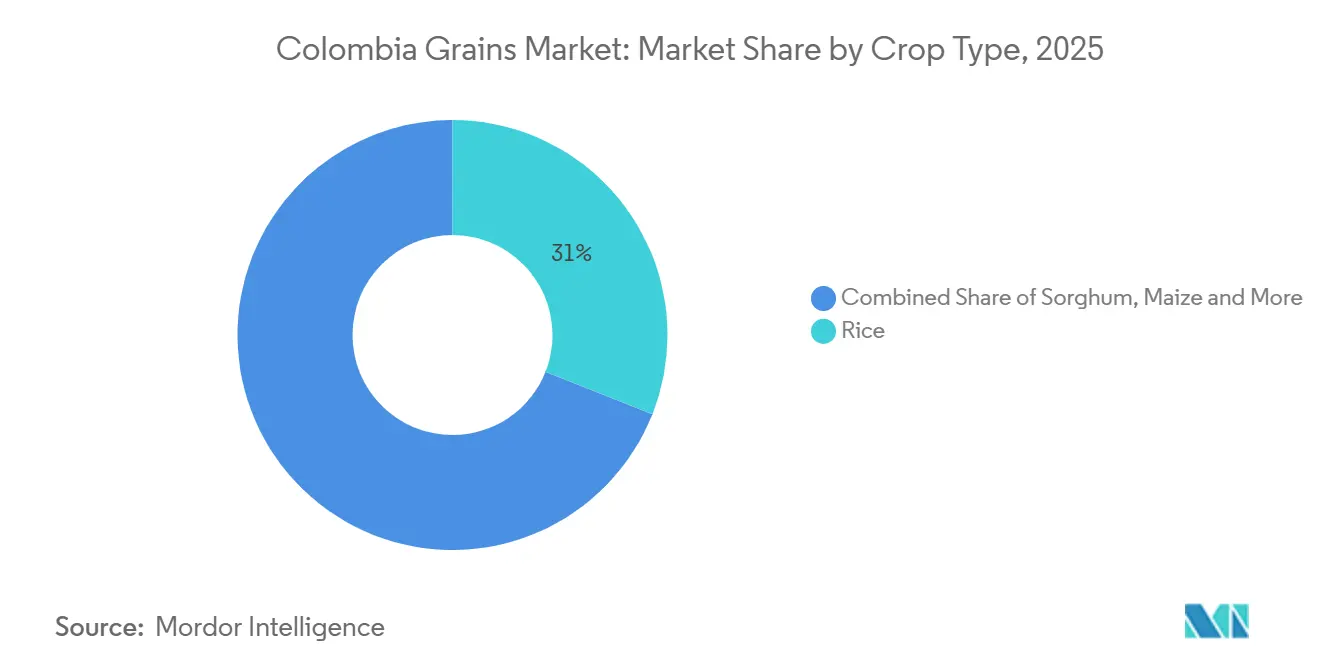

- By crop type, rice led with the largest 31% of the Colombia grain market share in 2025, while sorghum market size is forecast to expand at the fastest 10.7% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Colombia Grains Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust demand from poultry and swine sectors | +2.1% | National, with concentration in Santander, Antioquia, and Valle del Cauca | Medium term (2-4 years) |

| Growth of rice-based processed foods in urban centers | +1.3% | National, with early gains in Bogota, Medellín, and Cali | Medium term (2-4 years) |

| Government import tariff quota programs | +0.9% | National | Short term (≤ 2 years) |

| Port infrastructure upgrades at Buenaventura and Cartagena | +1.5% | National, with logistics spillover to Pacific and Caribbean corridors | Long term (≥ 4 years) |

| Pivot to drought-tolerant hybrid seeds | +0.7% | National, with early adoption in Tolima, Huila, and Meta | Long term (≥ 4 years) |

| Carbon-credit revenues for regenerative grain cultivation | +0.4% | National, pilot projects in Valle del Cauca and Cauca | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Demand from Poultry and Swine Sectors

Grain consumption in Colombia remains heavily driven by demand from the poultry and swine sectors, particularly for yellow maize used in compound feed. According to the United States Department of Agriculture, in 2025, around 95% of Colombia's corn imports are allocated to animal feed, highlighting the sector's reliance on imported grain[1]Source: United States Department of Agriculture Foreign Agricultural Service (USDA FAS), “Grain and Feed Update Colombia,” usda.gov. Feed producers are enhancing conversion efficiency, optimizing grain usage per unit of output, while managing costs. The strong consumer preference for poultry as an affordable protein source continues to sustain production levels, ensuring steady feed demand and stable grain import needs within the domestic market.

Growth of Rice-Based Processed Foods in Urban Centers

Urbanization is driving increased demand for value-added rice products in Colombia, such as pre-cooked and fortified options distributed through modern retail channels. This trend is prompting millers to prioritize product differentiation, branding, and quality improvements to achieve higher profit margins. According to a researcher from the University of Arkansas and Humboldt University of Berlin, a consumer study in 2025, zinc-biofortified rice commands an 18.8% price premium compared to standard rice, indicating a willingness to pay for enhanced nutritional benefits. Changing lifestyles and a growing preference for convenience foods are accelerating the shift toward processed rice, fostering revenue diversification and intensifying competition focused on innovation rather than scale.

Government Import Tariff Quota Programs

The tariff-rate quota framework established under trade agreements is influencing grain import patterns in Colombia by lowering duties and enhancing cost predictability for importers. Through the United States Department of Agriculture (USDA) framework, Colombia permits specific volumes of corn imports to enter duty-free under tariff-rate quotas for the last three years, facilitating stable procurement planning for feed mills and processors[2]Source: United States Department of Agriculture Foreign Agricultural Service (USDA FAS), “Colombia Trade Agreement and Grain Market Analysis,” fas.usda.gov. This structured liberalization intensifies competition for domestic producers, while government support programs are designed to stabilize farm income and maintain production levels. This approach reflects a balance between promoting trade openness and ensuring agricultural resilience.

Port Infrastructure Upgrades at Buenaventura and Cartagena

Investments in port infrastructure at Buenaventura and Cartagena are enhancing grain logistics by increasing operational efficiency within import and distribution networks. The implementation of upgraded bulk handling systems and modern storage facilities facilitates faster unloading, improved inventory management, and more effective coordination with inland transportation. These advancements help mitigate congestion risks and improve supply chain reliability for feed manufacturers and processors. Integrated operators with extensive logistics networks gain the most from these enhancements, whereas smaller participants encounter challenges in achieving similar efficiencies due to scale limitations, capital constraints, and restricted control over end-to-end supply chain operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High incidence of Fusarium and Fall Armyworm outbreaks | −1.2% | Cordoba, Sucre, and Meta | Short term (≤ 2 years) |

| Exchange-rate driven price volatility of imported wheat | −0.8% | Nationwide | Short term (≤ 2 years) |

| Aging smallholder farmer population | −0.6% | Nationwide, acute in Tolima and Huila | Medium term (2–4 years) |

| Shallow domestic crop-insurance penetration | −0.5% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Incidence of Fusarium and Fall Armyworm Outbreaks

Recurring outbreaks of Fall Armyworm and the rising incidence of Fusarium-related fungal diseases pose significant challenges to Colombia's grain market, particularly impacting maize and wheat cultivation. Persistent pest infestations have compelled farmers to rely more heavily on chemical crop protection measures, leading to increased production costs and reduced operational efficiency in grain-producing regions. Additionally, Fusarium contamination is adversely affecting grain quality, storage stability, and market acceptance due to heightened concerns over food and feed safety standards. These crop health risks undermine productivity stability, diminish farmer profitability, and constrain the long-term growth potential of Colombia's grain market.

Exchange-Rate Driven Price Volatility of Imported Wheat

Colombia's reliance on imported wheat continues to make its domestic grain market vulnerable to exchange rate fluctuations and external price changes. In 2024, the depreciation of the Colombian peso against the United States dollar raised import costs for wheat millers and food processors, leading to pricing pressures throughout the value chain and reducing procurement stability. Small and medium-sized processors, in particular, faced challenges in managing abrupt cost increases due to limited financial risk mitigation capabilities. These factors have disrupted purchasing strategies, strained operating margins, and impeded stable growth in Colombia grain market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Rice Anchors Value, Sorghum Surges From Low Base

Rice accounted for the largest 31% of Colombia grain market share in 2025, driven by its role as a staple food across the country. This segment benefits from extensive domestic cultivation and a well-established milling industry, primarily located in key producing regions such as Tolima and Huila. Major rice processors and millers exert significant influence over paddy procurement and pricing, reinforcing the segment's commercial framework. Additionally, government support measures, including subsidies for small-scale rice farmers, contribute to production stability and sustained cultivation levels within Colombia's grain market.

Colombia grain market size for Sorghum is projected to grow at the fastest 10.7% CAGR from 2026 to 2031, fueled by rising demand from the livestock feed industry and increasing interest in alternative feed grains. Adoption of hybrid seed varieties and improved agronomic practices are enhancing productivity and crop quality. Furthermore, feed manufacturers are increasingly considering sorghum as a gluten-free alternative to maize in feed formulations. This shift may diversify feed ingredient usage and mitigate mycotoxin-related risks within Colombia's grain industry.

Geography Analysis

Tolima, Huila, and Norte de Santander form the core rice-producing belt, benefiting from irrigation facilities and proximity to milling infrastructure that ensure steady paddy production. The Llanos region, particularly Meta and Casanare, remains a key area for maize cultivation. However, planting decisions are increasingly shaped by cost considerations and crop profitability. Regional production patterns are influenced by climatic conditions and infrastructure availability, resulting in uneven output across departments. This geographic distribution necessitates reliance on inter-regional trade and imports to address supply shortages, especially when domestic production falls short of meeting consumption demands for major grain categories.

Port connectivity plays a critical role in grain logistics, with the Pacific and Caribbean corridors linking inland production areas to import routes. Buenaventura facilitates supply chains in the western regions, while Cartagena improves access for northern and central areas, reducing transit times and enhancing supply reliability. Variations in freight costs across regions affect sourcing decisions and competitiveness for both domestic producers and importers. Inadequate rural infrastructure in interior regions hampers the efficient transportation of grains, leading to higher post-harvest losses and discouraging investments in productivity-enhancing inputs. These structural challenges exacerbate cost disparities between regions and hinder the development of an integrated supply chain.

Infrastructure and institutional support vary significantly across regions, impacting production efficiency and market access within Colombia's grain market. Processing companies strategically locate facilities near major production areas to enhance aggregation efficiency and mitigate procurement challenges. However, disparities in transport quality and connectivity lead to higher delivered grain costs compared to regional standards. Regional infrastructure differences contribute to inconsistencies in supply chain performance. Enhancing rural road infrastructure and optimizing logistics networks are essential to improving competitiveness, minimizing inefficiencies, and ensuring a stable and reliable grain supply across diverse agricultural regions.

Competitive Landscape

The grain market demonstrates a mixed competitive structure, characterized by consolidated rice milling operations and a more fragmented import and feed-processing segment. Prominent millers utilize their scale, brand portfolios, and distribution networks to sustain their market positions, while smaller competitors focus on localized sourcing and competitive pricing strategies. Vertical integration across procurement, processing, and distribution allows larger firms to better manage input cost fluctuations. This dynamic creates significant entry barriers for smaller participants and strengthens the position of established processors in securing a reliable raw material supply from farmers.

Procurement strategies increasingly incorporate contract farming and input support programs, enabling processors to stabilize supply chains and influence agricultural practices. These programs often involve the provision of seeds, fertilizers, and technical support in return for guaranteed offtake agreements. However, price volatility in raw materials can expose weaknesses in these systems, particularly when farmers encounter unfavorable contract terms during market downturns. Simultaneously, global trading firms play a vital role in coordinating imports, optimizing logistics, and improving storage efficiency to ensure consistent grain availability across supply chains.

Industry consolidation and operational scale are influencing the competitive landscape of Colombia's grain market. The United States Department of Agriculture (USDA) estimates Colombia's corn imports at 6.95 million metric tons for the 2024/2025 marketing year, highlighting the significant role of large trading firms in managing bulk supply chains [3]Source: United States Department of Agriculture Foreign Agricultural Service (USDA FAS), “Grain and Feed Annual Colombia,” fas.usda.gov. Technology adoption shows notable variation, with larger firms implementing automation and quality control systems, while smaller operators continue to use traditional methods. Trade liberalization is intensifying competition, driving a transition toward value-added products and diversified revenue streams to maintain profitability.

Recent Industry Developments

- July 2025: The Government of Colombia has implemented a regulated pricing mechanism for paddy aimed at stabilizing producer incomes and enhancing price transparency throughout the value chain. This policy establishes region-specific minimum prices and enforces stricter monitoring of transactions.

- January 2025: The Government of Colombia introduced temporary adjustments to import duties on wheat, barley, and yellow corn under the Andean Price Band System (APBS). This initiative aimed to stabilize domestic prices and control inflation.

- August 2024: CAF (Development Bank of Latin America and the Caribbean), the GCF (Green Climate Fund), and the Colombian government have implemented a USD 99.9 million "Sustainable Agrifood Colombia" project aimed at the grain sector. The project focuses on adopting climate-resilient practices to support rice and corn producers. In collaboration with associations such as Federación de Azúcar and Fenalce, the initiative includes real-time climate monitoring to enhance productivity.

Colombia Grains Market Report Scope

Grains are small, hard seeds obtained from cereal crops like wheat, rice, and corn, widely used as staple foods globally. They are high in carbohydrates and supply essential nutrients, functioning as a primary energy source for human consumption and as critical inputs in animal feed and food processing industries. The Colombia grain market report is segmented by crop type (rice, maize, sorghum, wheat, barley, oat). The report includes production analysis (volume), consumption analysis (value and volume), import market analysis (value and volume), export market analysis (value and volume), wholesale price trend analysis and forecast, regulatory framework, list of key players, logistics and infrastructure analysis, and seasonality analysis. The market forecasts are provided in terms of value (USD) and volume (metric tons) for all the above segments.

By Crop Type

| Rice | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Wheat | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Maize | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Sorghum | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Oat | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Barley | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

By Geography

| Production Analysis | Production Volume | |

| Area Harvested and Yield | ||

| Consumption Analysis (Value and Volume) | ||

| Import Value and Volume | ||

| Key Supplying Markets | ||

| Export Value and Volume | ||

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Seasonality Analysis |

| By Crop Type | Rice | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Wheat | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Maize | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Sorghum | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Oat | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Barley | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| By Geography | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

Key Questions Answered in the Report

How large is the Colombia grain market in 2026?

The Colombia grain market size stands at USD 4.8 billion in 2026 and is projected to reach USD 7.25 billion by 2031, reflecting an 8.6% CAGR from 2026 to 2031.

How dependent is Colombia on grain imports?

Colombia imports 85–88% of total grain demand, relying almost entirely on external supplies for wheat and yellow maize.

Which crop holds the largest share of grain value in Colombia?

Rice leads with the largest 31% of Colombia grain market share in 2025, driven by sustained household consumption.

What segment is growing fastest through 2031?

Sorghum market size is forecast to expand at the fastest 10.7% CAGR through from 2026 to 2031.

Page last updated on: