Grain Dryers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.56 Billion |

| Market Size (2031) | USD 2.09 Billion |

| Growth Rate (2026 - 2031) | 6.00% CAGR |

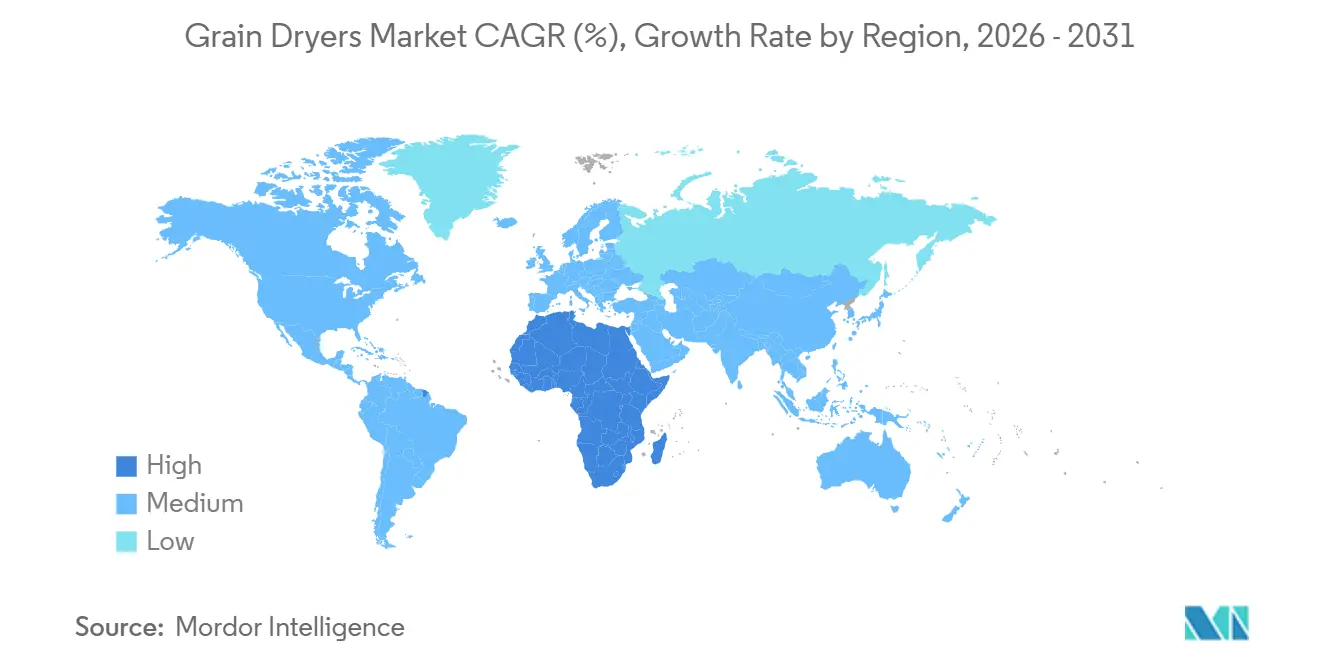

| Fastest Growing Market | Africa |

| Largest Market | North America |

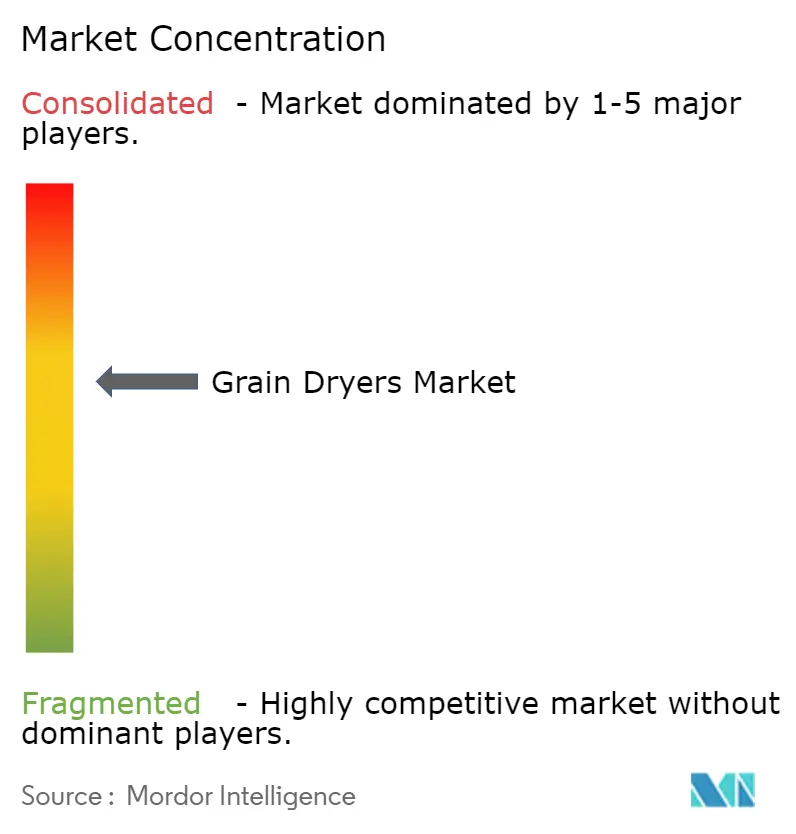

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grain Dryers Market Analysis by Mordor Intelligence

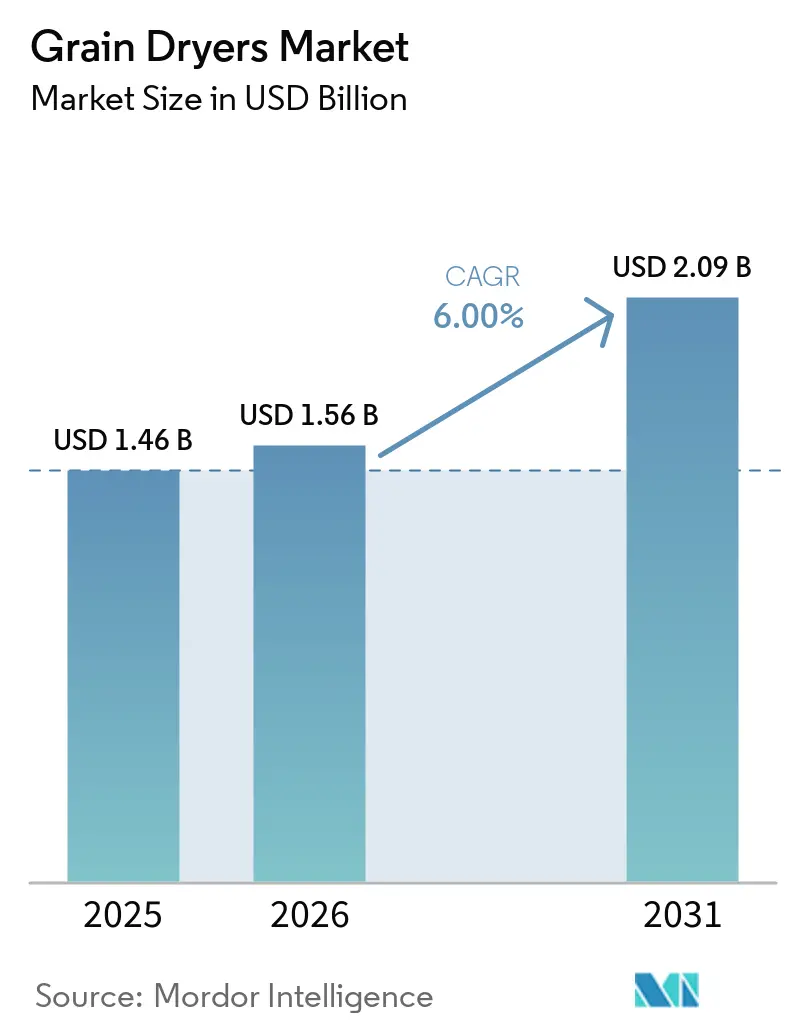

The grain dryers market size is projected to grow from USD 1.46 billion in 2025 to USD 1.56 billion in 2026 and USD 2.09 billion by 2031, registering a CAGR of 6.0% during the forecast period from 2026 to 2031. This growth is driven by rising investments in post-harvest infrastructure, increasing focus on reducing grain losses, and the growing adoption of automated drying technologies across commercial and on-farm facilities. Integration of Internet of Things (IoT)-enabled monitoring systems and digital moisture control technologies is supporting the shift toward more efficient and continuous drying operations. Additionally, growing demand for energy-efficient and solar-assisted dryers is encouraging technology upgrades in emerging agricultural economies. Expansion of grain storage and handling infrastructure, along with increasing adoption of modular drying systems by mid-scale producers, is further supporting market growth globally.

Key Report Takeaways

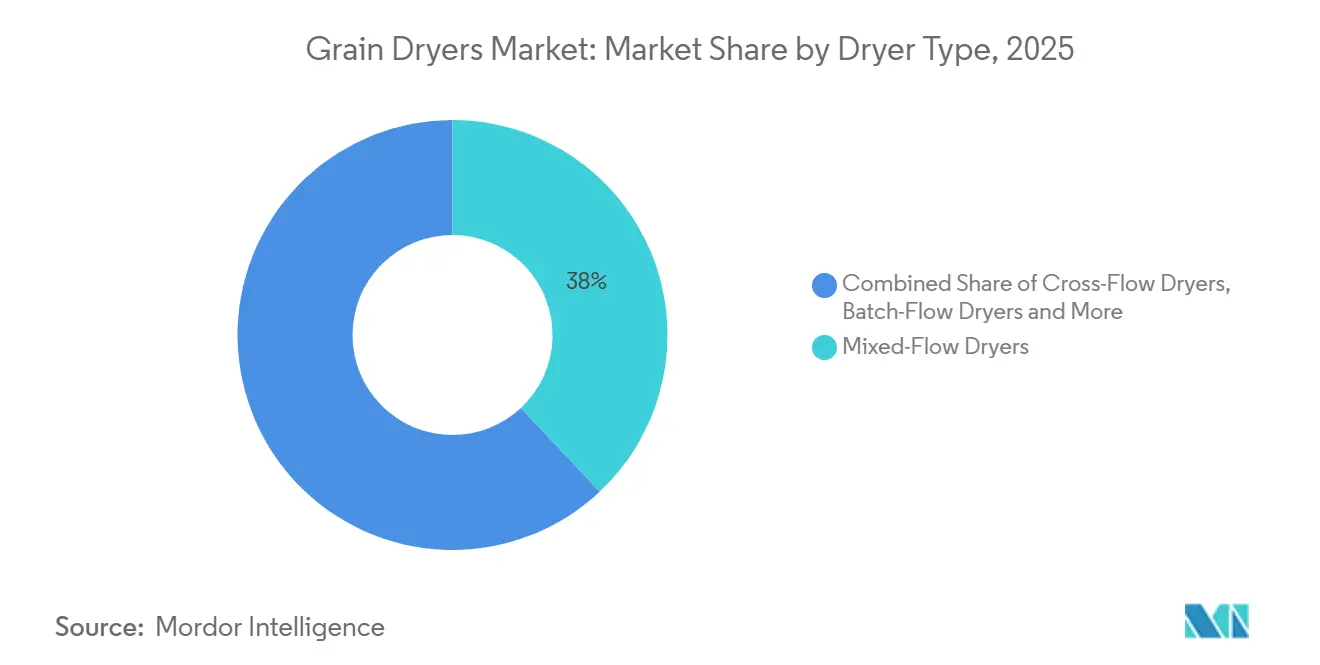

- By dryer type, mixed-flow units accounted for the largest share of the grain dryers market in 2025, at 38%. The microwave-assisted dryers market size is projected to grow at the fastest 9.8% CAGR from 2026 to 2031.

- By mode of operation, continuous-flow systems held the largest 52% of the grain dryers market share in 2025. The solar-assisted market size is projected to grow at the fastest 11.2% CAGR from 2026 to 2031.

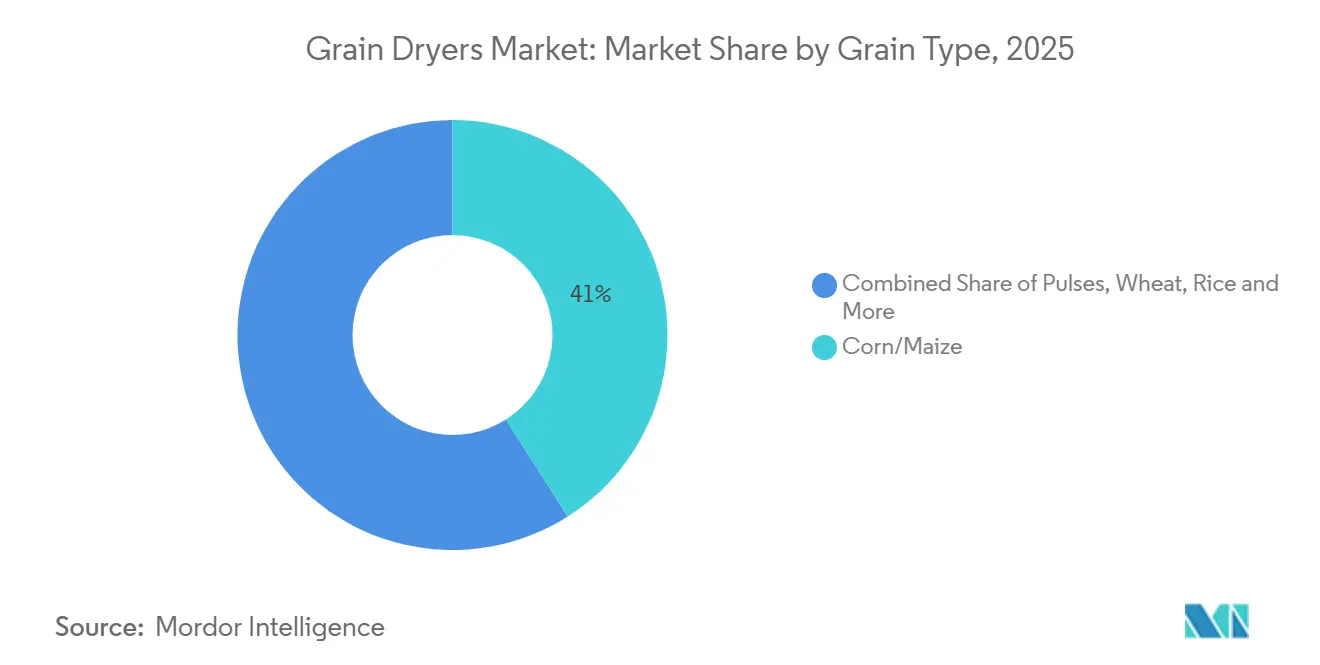

- By grain type, corn accounted for the largest share of the grain dryers market in 2025, at 41%. The pulses segment market size is projected to grow at the fastest 8.7% CAGR from 2026 to 2031.

- By end user, commercial grain elevators accounted for the largest 48% of the grain dryers market share in 2025. The on-farm facilities market size is projected to grow at the fastest 8.9% CAGR from 2026 to 2031.

- By geography, North America accounted for the largest 42% of the grain dryers market share in 2025. The Africa market size is projected to grow at the fastest 7.3% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Grain Dryers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of continuous-flow dryers in commercial elevators | +1.2% | North America, South America, and Asia-Pacific | Medium term (2–4 years) |

| Electrification reduces energy cost volatility | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Post-harvest loss reduction mandates in developing countries | +1.1% | Asia-Pacific and Africa | Short term (≤ 2 years) |

| Rapid adoption of IoT-enabled grain-handling automation | +0.8% | Global | Medium term (2–4 years) |

| Green hydrogen burner pilots in Europe and Australia | +0.5% | Europe and Australia | Long term (≥ 4 years) |

| Rising use of microwave-assisted hybrid dryers for specialty grains | +0.7% | North America, Europe, and Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Continuous-Flow Dryers in Commercial Elevators

Commercial grain elevators are increasingly utilizing continuous-flow dryers to improve operational efficiency and handle higher throughput during compressed harvest periods. In contrast to traditional batch systems, continuous-flow dryers enable uninterrupted grain processing, addressing the large-scale handling requirements of modern elevator operations. This transition is driven by the need to minimize intake congestion, reduce transport vehicle turnaround times, and maintain consistent grain quality across substantial volumes.

Electrification Reduces Energy Cost Volatility

The electrification of grain drying systems is becoming increasingly prominent as operators seek to decrease dependence on fossil fuels and enhance operational efficiency. Traditional dryers rely on propane and natural gas, resulting in variable operating costs. In contrast, electric and hybrid systems provide more stable, predictable energy costs. These systems also enable precise control of drying conditions, improving grain quality and minimizing losses. According to Renewable and Sustainable Energy Reviews (2024), the energy efficiency of grain dryers ranges from 26% to 80%, depending on the type of dryer [1]Source: M. H. T. Mondal et al., “Comprehensive energy analysis and environmental sustainability of industrial grain drying,” Renewable and Sustainable Energy Reviews, 2024, sciencedirect.com. Which underscoring the demand for more efficient and controlled drying technologies.

Post-Harvest Loss Reduction Mandates in Developing Countries

Government initiatives and food security programs in developing economies are promoting the use of grain dryers to reduce post-harvest losses and improve grain preservation. Efficient drying systems play a critical role in minimizing moisture-related spoilage, fungal contamination, and pest infestation during grain storage and transportation. A 2024 study by researchers from the University of Southern Queensland found that cereal grains experience an estimated 19% post-harvest weight loss, highlighting the impact of inadequate storage and drying infrastructure [2]Source: B. Nath et al., “Research and technologies to reduce grain postharvest losses,” Foods, 2024, mdpi.com. Developing economies are increasingly supporting the adoption of mechanized, energy-efficient grain-drying technologies through agricultural modernization and rural infrastructure programs. These initiatives are driving investments in grain dryers across both smallholder farming systems and commercial grain handling operations.

Rapid Adoption of IoT-Enabled Grain-Handling Automation

The integration of Internet of Things (IoT)-enabled automation is revolutionizing grain drying operations by improving process control, efficiency, and reliability. Contemporary grain dryers are equipped with sensors and digital monitoring systems that enable real-time tracking of key parameters, including moisture levels, temperature, and airflow. This enables operators to optimize drying conditions, lower energy consumption, and ensure consistent grain quality. Additionally, IoT-enabled systems provide remote monitoring and predictive maintenance capabilities, reducing downtime and minimizing operational disruptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital costs amid tight farm margins | -0.8% | Global, acute in North and South America | Short term (≤ 2 years) |

| Inconsistent grain quality standards in emerging markets | -0.5% | Africa, Asia-Pacific, and South America | Medium term (2–4 years) |

| Limited three-phase power in rural Africa | -0.3% | Sub-Saharan Africa | Medium term (2–4 years) |

| Supply risks of stainless-steel heat exchangers due to nickel constraints | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Costs Amid Tight Farm Margins

High initial investment costs continue to pose a significant challenge to the adoption of grain dryers, especially among small and medium-scale farmers. Declining farm profitability further constrains producers' ability to invest in capital-intensive equipment like advanced drying systems. According to the United States Department of Agriculture Economic Research Service, net farm income declined to USD 140.7 billion in 2024, a reduction of USD 9.5 billion compared to 2023 [3]Source: United States Department of Agriculture Economic Research Service (USDA ERS), “Farm Sector Income Forecast,” ers.usda.gov. This decline in income directly impacts farmers' capacity to allocate funds for post-harvest infrastructure, delaying the adoption of efficient grain drying technologies and hindering market growth.

Inconsistent Grain Quality Standards in Emerging Markets

Inconsistent grain quality standards in emerging markets pose challenges to the adoption of advanced grain drying technologies. Differences in acceptable moisture levels, grading systems, and testing infrastructure create uncertainty regarding drying requirements and operational practices. This lack of standardization often leads to inefficient drying processes, such as over-drying or under-drying, which negatively affect grain quality and raise operational costs. Small and mid-scale operators, in particular, struggle to justify investments in modern dryers due to the absence of clear and uniform regulatory benchmarks, hindering the broader adoption of precision drying systems in these regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dryer Type: Hybrid Systems Target Premium Crops

Mixed-flow units held the largest 38% of the grain dryers market share in 2025. This dominance is attributed to their fuel-efficient airflow design and capability to handle multiple grain types while ensuring consistent drying performance. These systems offer balanced heat distribution and operational flexibility, making them suitable for both commercial elevators and mid-scale facilities. Rotary and cross-flow dryers continue to address high-moisture grain applications, while batch systems remain relevant for small farms with seasonal usage needs. The versatility and cost efficiency of mixed-flow systems drive their widespread adoption across various agricultural regions.

The hybrid/microwave-assisted dryers market is projected to grow at the fastest CAGR of 9.8% from 2026 to 2031. This growth is driven by increasing demand for precision drying solutions that maintain grain quality while reducing energy consumption. Hybrid systems allow operators to switch between drying modes, enhancing efficiency across different crop types. These technologies are particularly significant for seed processors and high-value crop segments where controlled moisture levels are essential. Advancements in modular configurations and energy-efficient designs are further supporting adoption, establishing hybrid systems as a key growth segment within drying technologies.

By Mode of Operation: Solar Systems Scale in Off-Grid Regions

Continuous-flow systems held the largest 52% of the grain dryers market share in 2025. Their market leadership stems from their capability to handle large grain volumes continuously, minimizing operational downtime and enhancing throughput efficiency. These systems are predominantly utilized in commercial grain elevators, where uninterrupted drying is crucial during peak harvest seasons. Their compatibility with automated grain handling infrastructure facilitates streamlined operations and ensures consistent moisture control. Continuous-flow dryers are particularly favored in regions characterized by large-scale grain production and advanced logistics networks.

The solar-assisted market size is projected to grow at the fastest 11.2% CAGR from 2026 to 2031. Market growth is primarily driven by the rising demand for energy-efficient and off-grid drying solutions in areas with limited power infrastructure. Solar-assisted systems help reduce reliance on conventional fuels, offering cost-effective drying options for smallholder farmers. These systems are increasingly adopted in Asia-Pacific and Africa, where decentralized drying solutions are essential. Integration with hybrid backup systems is enhancing reliability, while advancements in solar thermal technologies are improving efficiency and driving adoption in emerging agricultural markets.

By Grain Type: Pulses Demand Specialized Protocols

Corn accounted for the largest 41% of the grain dryers market share in 2025. This dominance is attributed to high global production volumes and the necessity for efficient drying to maintain storage quality and prevent spoilage. Corn drying requires high-capacity systems capable of managing large throughput, making it a significant driver for commercial drying infrastructure. Additionally, other grains such as wheat and rice contribute to market demand, with region-specific drying requirements influencing equipment selection and operational practices across various agricultural markets.

The pulses segment market size is projected to grow at the fastest 8.7% CAGR from 2026 to 2031. This growth is driven by increasing demand for plant-based protein and the expanded cultivation of pulses across multiple regions. Pulses require specialized drying conditions to preserve quality attributes, including color and protein composition. This has led to the adoption of advanced drying technologies with precise temperature and moisture control. As dietary preferences shift toward plant-based foods, the demand for efficient and gentle drying solutions is projected to support sustained growth in this segment.

By End User: On-Farm Segment Captures Basis Premiums

Commercial grain elevators accounted for the largest 48% of the grain dryers market share in 2025. Their dominance is driven by the need to manage large volumes of grain efficiently during harvest seasons. These facilities require high-capacity drying systems integrated with storage and transportation infrastructure to maintain consistent throughput. Commercial operators prioritize reliability and efficiency, leading to strong adoption of advanced drying technologies. Their role in centralized grain handling and distribution reinforces their position as the primary end users of grain drying equipment.

The on-farm facilities market size is projected to grow at the fastest 8.9% CAGR from 2026 to 2031. Growth is driven by increasing farmer preference for greater control over post-harvest operations and pricing. On-farm drying systems enable producers to reduce dependency on external facilities and improve operational flexibility. Adoption is supported by financing options and technological advancements that make systems more accessible to mid-scale farmers. This trend reflects a shift toward decentralized drying infrastructure, allowing producers to enhance efficiency and optimize grain quality management.

Geography Analysis

North America accounted for the largest 42% of the grain dryers market share in 2025, driven by advanced agricultural infrastructure and high mechanization levels. The region's large-scale farming operations and well-developed grain handling systems create a consistent demand for efficient drying solutions. The strong adoption of automated technologies and integrated storage systems further supports the demand for high-capacity dryers. Additionally, access to financing programs and ongoing technological advancements contribute to equipment upgrades, reinforcing North America's leadership in grain drying capacity and operational efficiency.

The Africa market size is projected to grow at the fastest 7.3% CAGR from 2026 to 2031, supported by increasing focus on reducing post-harvest losses and improving food security. Adoption is driven by development programs that promote decentralized, solar-based drying solutions. While infrastructure limitations and restricted access to electricity pose challenges, rising investments and growing awareness are fostering gradual adoption. These efforts are expanding drying capacity within smallholder farming systems and improving post-harvest management practices in emerging agricultural economies.

Regional variations reveal disparities in infrastructure and investment across markets. Developed regions demonstrate high adoption rates of advanced drying technologies, while emerging regions focus on expanding basic capacity to meet rising demand. According to the Brazilian Institute of Geography and Statistics (IBGE), Brazil's agricultural storage capacity reached 231.1 million metric tons in the first half of 2025, coinciding with continued record growth in grain production. The growing gap between grain production and available storage infrastructure underscores the increasing need for additional grain drying and storage facilities. Addressing this imbalance is essential to reducing post-harvest losses, enhancing supply chain efficiency, and supporting agricultural productivity in key grain-producing regions.

Competitive Landscape

The market is moderately concentrated, with key players such as AGCO Corporation, Buhler Holding AG, Cimbria A/S, Sukup Manufacturing Co., and Alvan Blanch Development Company Limited maintaining a significant presence in large-scale commercial drying systems and integrated grain handling solutions. Major companies emphasize high-capacity equipment and advanced technologies, while regional manufacturers address localized demand with cost-effective solutions. Competitive positioning is determined by factors such as product performance, distribution networks, and after-sales service capabilities across various agricultural markets.

Competition is intensifying as companies prioritize innovation, partnerships, and geographic expansion. Investments in automation and energy-efficient technologies are driving product differentiation. Manufacturers are focusing on modular systems to enhance flexibility and scalability for farms of different sizes. Expansion into emerging markets and collaborations with cooperatives are bolstering market presence. Sustainability-focused innovations, such as hybrid and renewable energy-based drying systems, are increasingly shaping competitive strategies and driving technological advancements across both developed and emerging regions.

Competitive dynamics in the grain handling value chain are influenced by strategic investments and capacity expansion efforts. Companies are prioritizing the enhancement of integrated drying and storage capabilities to improve operational efficiency and throughput. This approach aligns with a broader trend toward vertical integration, enabling better supply chain control and minimizing operational challenges. Investments in infrastructure and technology are facilitating improved grain quality management and process optimization. These initiatives are strengthening supply chain resilience and addressing the growing demand for efficient post-harvest handling solutions in major agricultural regions.

Grain Dryers Industry Leaders

AGCO Corporation

Buhler Holding AG

Cimbria A/S

Sukup Manufacturing Co.

Alvan Blanch Development Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Cooperative Producers, Inc. has announced the expansion of its grain handling facility in Red Cloud, Nebraska. The project includes the construction of a new grain storage building with a capacity of 2 million bushels, along with a 30,000-bushel-per-hour dump pit and receiving leg.

- October 2025: Delta Grain Company has announced a USD 3.76 million expansion of its grain handling operations in Leflore County, Mississippi. This expansion will add 2.15 million bushels of storage capacity. It follows the company’s 2024 investment in a 10,000-bushel-per-hour grain dryer to enhance drying and grain processing efficiency.

- August 2024: AGCO Corporation, under its GSI brand, introduced a mixed-flow grain dryer designed to improve drying efficiency and grain quality in high-capacity operations.

Global Grain Dryers Market Report Scope

Grain dryers are devices designed to remove excess moisture from harvested grains, ensuring safe storage and minimizing spoilage risk. They operate by circulating heated air through the grains, reducing moisture levels to preserve quality and extend shelf life. The grain dryers market report is segmented by dryer type (mixed-flow dryers, cross-flow dryers, batch dryers, rotary dryers, and microwave-assisted dryers), by mode of operation (continuous-flow, recirculating batch, and solar-assisted), by grain type (corn, wheat, rice, soybean, and pulses and other crops), by end user (commercial grain elevators, on-farm facilities, and seed processors), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Mixed-Flow Dryers |

| Cross-Flow Dryers |

| Batch Dryers |

| Rotary Dryers |

| Microwave-Assisted Dryers |

| Continuous-Flow |

| Recirculating Batch |

| Solar-Assisted |

| Corn |

| Wheat |

| Rice |

| Soybean |

| Pulses and Others |

| Commercial Grain Elevators |

| On-Farm Facilities |

| Seed Processors |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | Nigeria |

| South Africa | |

| Rest of Africa |

| By Dryer Type | Mixed-Flow Dryers | |

| Cross-Flow Dryers | ||

| Batch Dryers | ||

| Rotary Dryers | ||

| Microwave-Assisted Dryers | ||

| By Mode of Operation | Continuous-Flow | |

| Recirculating Batch | ||

| Solar-Assisted | ||

| By Grain Type | Corn | |

| Wheat | ||

| Rice | ||

| Soybean | ||

| Pulses and Others | ||

| By End User | Commercial Grain Elevators | |

| On-Farm Facilities | ||

| Seed Processors | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the grain dryers market in 2026?

The grain dryers market size is valued at USD 1.56 billion in 2026.

What is the projected growth rate to 2031?

Revenue is projected to climb to USD 2.09 billion by 2031 at a 6.0% CAGR from 2026 to 2031.

Which dryer type is growing the fastest?

Microwave-assisted units are advancing at the fastest 9.8% CAGR from 2026 to 2031.

Why are pulses attracting new dryer investment?

Rising demand for plant-based protein and the heat sensitivity of pulses are driving the fastest CAGR of 8.7% for pulse drying systems during 2026–2031.

Page last updated on: