GPU Fabric Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 91.80 Billion |

| Market Size (2031) | USD 227.30 Billion |

| Growth Rate (2026 - 2031) | 22.64% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

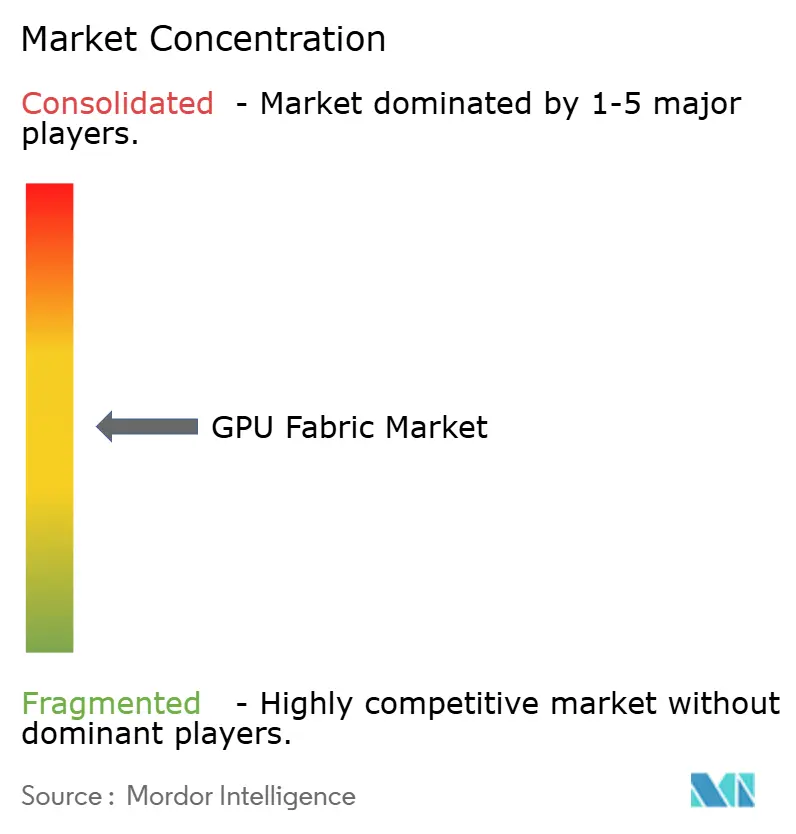

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Fabric Market Analysis by Mordor Intelligence

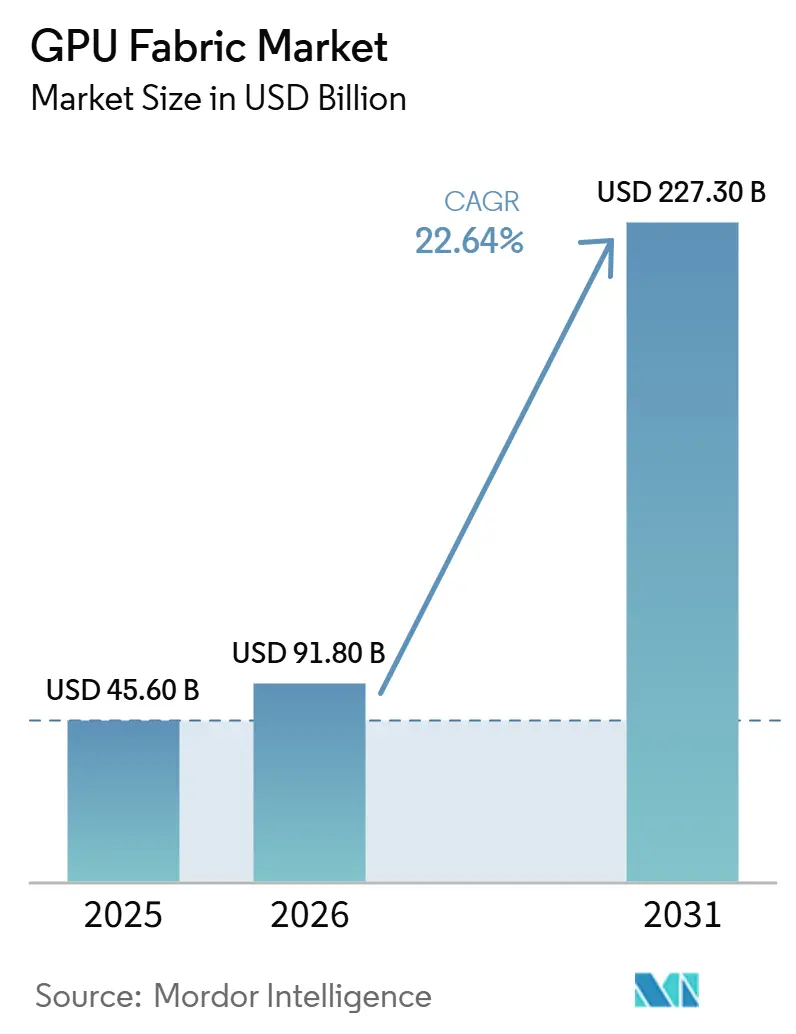

The GPU fabric market size is expected to increase from USD 45.60 billion in 2025 to USD 91.80 billion in 2026 and reach USD 227.30 billion by 2031, growing at a CAGR of 22.64% over 2026-2031. The sharp step-up between 2025 and 2026 shows that interconnect design has moved from a supporting hardware choice to a core infrastructure decision inside large AI clusters. Buyers are now paying closer attention to bandwidth balance, rack density, optical reach, and software control because idle accelerators raise costs quickly when GPU systems scale across many racks. The GPU fabric market is also being shaped by a broader shift toward rack-scale systems, denser switch layers, and more demanding inference traffic, which is changing how operators size both scale-up and scale-out deployments. Leading vendors are responding by opening parts of their ecosystems, investing in optics and switching partnerships, and tying fabric products more tightly to full-stack AI infrastructure. The GPU fabric market still faces supply and policy friction, but the direction of spending suggests that operators see better interconnect performance as a direct way to protect utilization and support larger deployments through 2031.

Key Report Takeaways

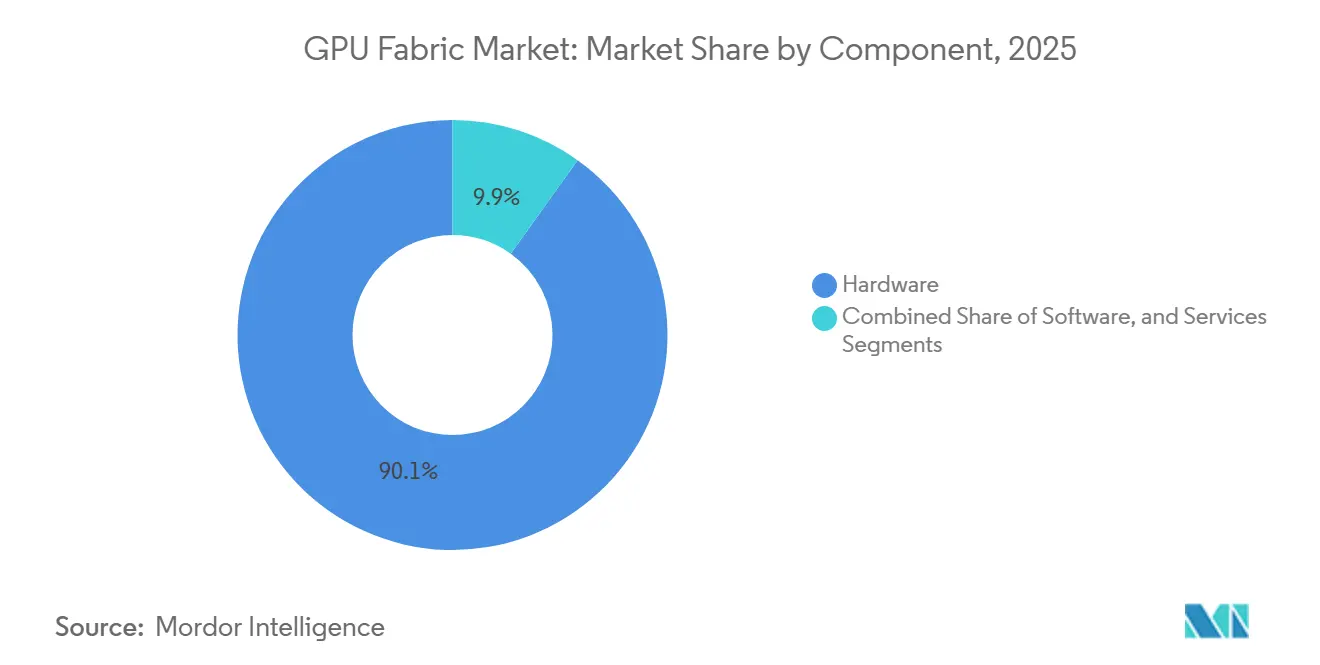

- By component, hardware held 90.11% share of the GPU fabric market in 2025, while services is projected to expand at a 24.21% CAGR through 2031.

- By fabric type, scale-out led with 49.33% share in 2025, while the GPU fabric market is expected to see the fastest expansion in scale-up fabric at a 24.62% CAGR through 2031.

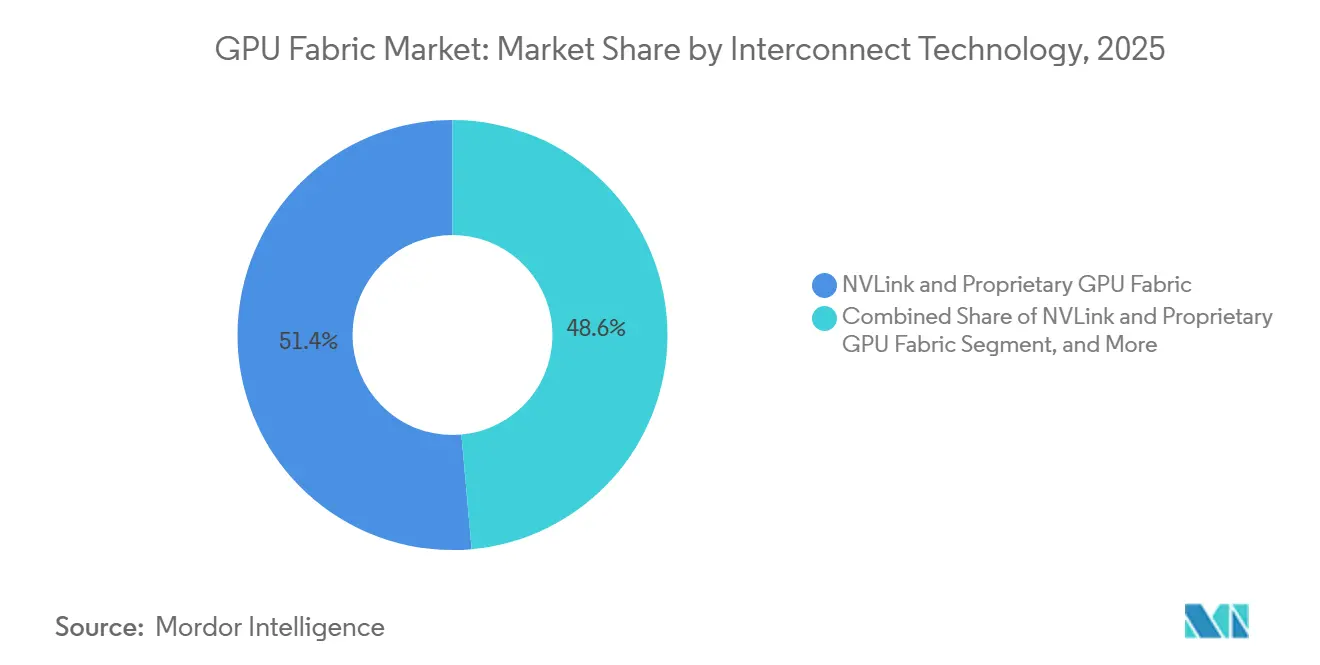

- By interconnect technology, NVLink and proprietary GPU fabric accounted for 51.42% share in 2025, while co-packaged optics-based fabric is projected to advance at a 24.53% CAGR through 2031.

- By application, AI training captured 62.12% share of the GPU fabric market in 2025, while AI inference is expected to grow at a 24.32% CAGR through 2031.

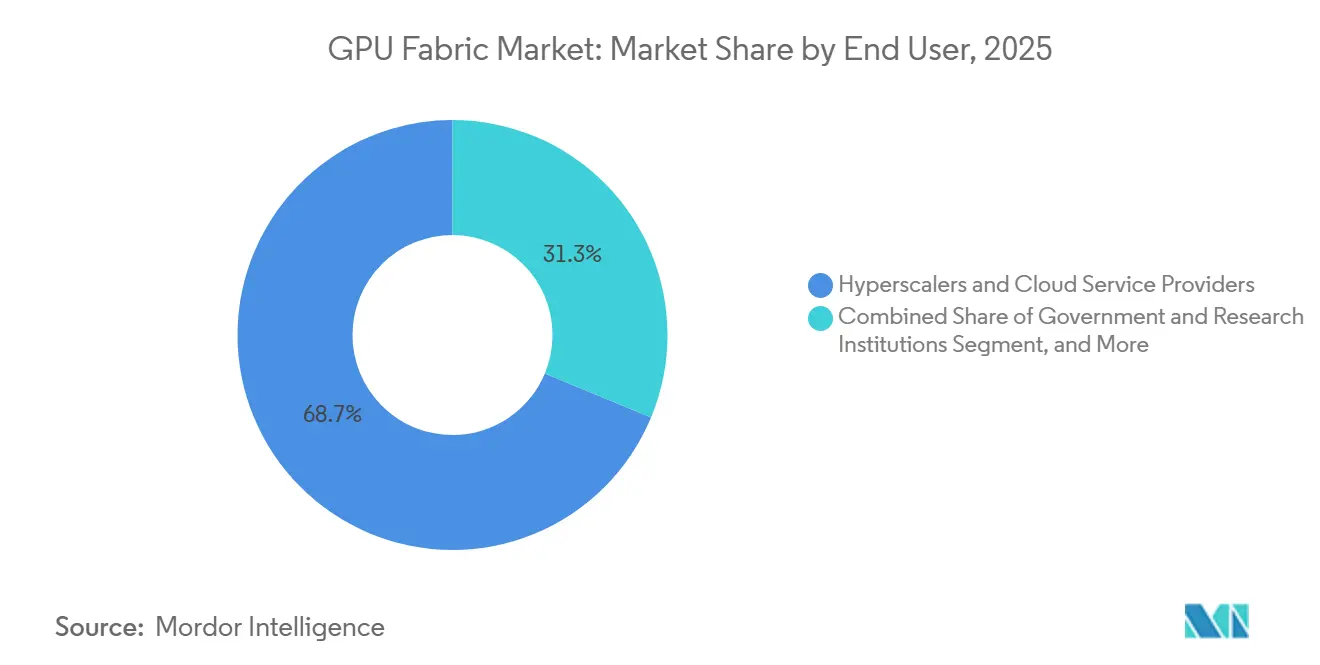

- By end user, hyperscalers and cloud service providers held 68.73% share in 2025, while government and research institutions are projected to expand at a 24.44% CAGR through 2031.

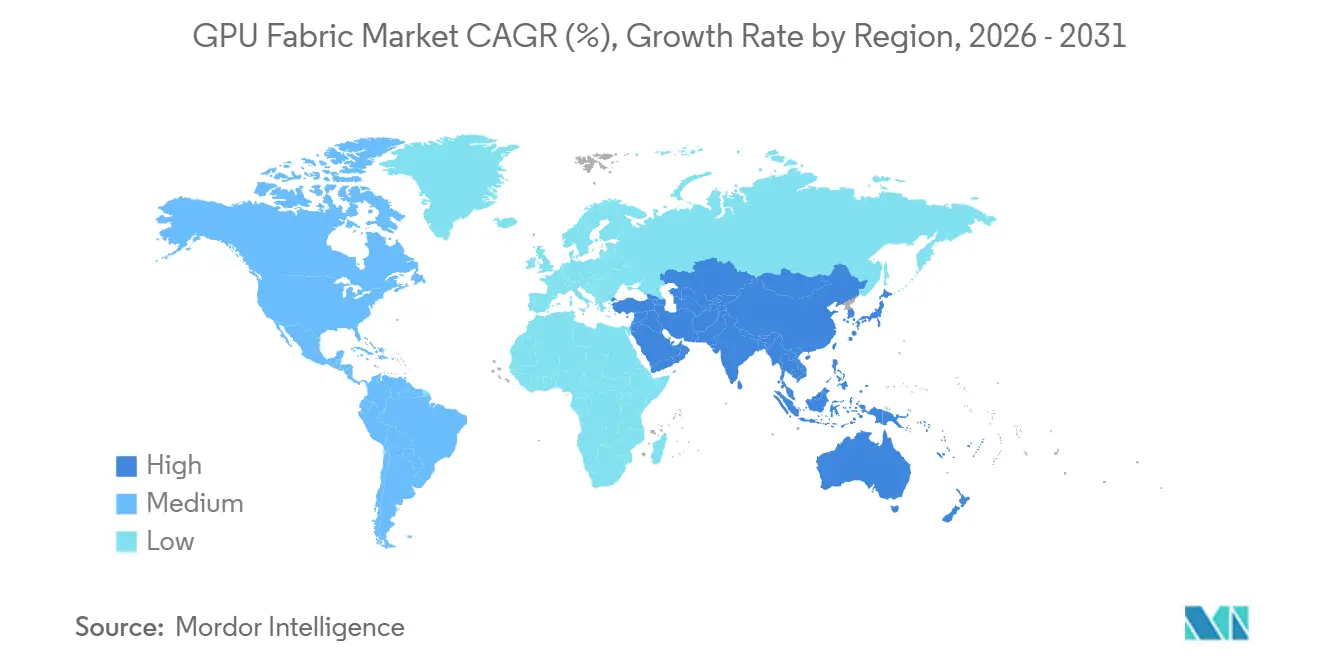

- By geography, North America held 38.44% share of the GPU fabric market in 2025, while Asia-Pacific is projected to expand at a 24.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Fabric Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Cluster Density In Hyperscale Data Centers | +6.5% | Global, highest in North America and Asia-Pacific core | Short term (≤ 2 years) |

| Expansion of High-Bandwidth GPU Interconnect Architectures | +5.2% | Global, with early scaling in North America, South Korea, and Japan | Short term (≤ 2 years) |

| Shift From Copper to Co-Packaged Optics for Higher Bandwidth | +4.1% | North America and East Asia, with spillover to Europe | Medium term (2-4 years) |

| Rising Sovereign AI and on-Premises GPU Deployments | +2.8% | Europe, Middle East, Canada, India, and Southeast Asia | Medium term (2-4 years) |

| Growth of Liquid-Cooled GPU Infrastructure | +1.5% | North America and Asia-Pacific, expanding to Europe | Medium term (2-4 years) |

| Rising Adoption of Ethernet and InfiniBand Converged Fabrics | +1.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising AI Cluster Density in Hyperscale Data Centers

Rising cluster density is changing how the GPU fabric market is planned, because the number of accelerators inside one rack and across connected racks is growing faster than legacy network designs can support. NVIDIA stated that its Vera Rubin platform ramps into full production in 2026 with rack-scale configurations built around 72 Rubin GPUs and expansion to 576 GPUs across 8 racks, which raises the importance of non-blocking bandwidth inside the cluster.[1]NVIDIA, “NVIDIA Vera Rubin Ramps Into Full Production to Power Agentic AI Factories Worldwide,” NVIDIA Investor Relations, investor.nvidia.com. That shift means the GPU fabric market is no longer driven only by the number of deployed GPUs, because effective utilization increasingly depends on whether traffic can move cleanly across dense domains without creating latency bottlenecks. Broadcom’s Tomahawk 6, shipped in 2026 with 102.4 Tbps capacity, shows that switch silicon is being built specifically for this density step rather than for traditional enterprise workloads. Arista also launched its 7060XE7 Series in 2026 with 1.6T systems validated by large cloud operators, which confirms that rack-scale AI traffic is now shaping real procurement decisions. As a result, the GPU fabric market is pulling more value toward switching, optics, and orchestration layers that can keep expensive accelerators active for longer parts of the workload cycle.

Expansion of High-Bandwidth GPU Interconnect Architectures

The GPU fabric market is also advancing because interconnect architectures are improving at several layers at the same time, from in-rack GPU links to multi-rack and multi-site connectivity. NVIDIA’s NVLink platform now supports 3.6 TB/s of bidirectional GPU-to-GPU bandwidth and extends through NVLink Switch across 576 GPUs at 260 TB/s, which materially raises the ceiling for scale-up design.[2]NVIDIA, “NVLink and NVLink Switch,” NVIDIA, nvidia.com. NVIDIA also introduced Spectrum-XGS Ethernet in 2025 to connect distributed data centers into unified AI super-factories, which widened the role of fabric from a local cluster function to a broader facility-level architecture. Broadcom’s Tomahawk 6 and Arista’s 7060XE7 portfolio show that the open standards side of the GPU fabric market is keeping pace with that shift by moving quickly to 1.6T class switching platforms. This matters because buyers increasingly want scale-up, scale-out, and scale-across options that work together rather than a single topology that forces tradeoffs between performance and flexibility. The GPU fabric market therefore benefits not only from more traffic volume, but also from a wider set of deployment choices that allow operators to match architectures to training, inference, and geographically distributed workloads.

Shift From Copper to Co-Packaged Optics for Higher Bandwidth

The move from copper-heavy designs toward co-packaged optics is becoming more important in the GPU fabric market as clusters push past the practical reach and power profile of older interconnect methods. NVIDIA said in 2026 that Spectrum-X Ethernet Photonics, described as the world’s first co-packaged optics Ethernet switches with 200G SerDes, had entered production as part of the Vera Rubin ramp. That production milestone matters because the GPU fabric market now needs higher bandwidth density and cleaner signal performance without adding excessive power or thermal burden to already crowded racks. NVIDIA’s March 2026 partnership expansion with Marvell also covered silicon photonics collaboration, which points to a broader effort to secure optical building blocks before the category scales further.[3]Marvell, “NVIDIA AI Ecosystem Expands as Marvell Joins Forces Through NVLink Fusion,” Marvell Technology, marvell.com. The shift will not replace existing copper or pluggable layers immediately, but it does change the design path for clusters that are expected to grow through multiple upgrade cycles. Over time, the GPU fabric market is likely to shift more spending toward integrated optical solutions because they help preserve bandwidth headroom as rack-level power and accelerator counts rise together.

Rising Sovereign AI and On-Premises GPU Deployments

Sovereign AI programs are widening the GPU fabric market beyond hyperscaler-led demand, because many governments and regulated enterprises want local control over compute, data, and system operation. IBM launched Sovereign Core in 2026 to support sovereign AI environments with governance and regional control features, which shows that buyers now want AI infrastructure frameworks built around jurisdictional requirements rather than only raw throughput. Palantir and NVIDIA also introduced the Sovereign AI OS Reference Architecture in 2026 for on-premises, edge, and sovereign cloud deployments, which supports the view that isolated and controlled environments are becoming a defined purchasing lane for the GPU fabric market. This trend changes buying behavior because sovereign deployments often favor dedicated rack-scale systems, auditable networking, and greater physical control over the interconnect path. It also creates demand from customers that are not always aligned with hyperscaler design standards, which opens space for more customized switching, management software, and on-prem integration services. The GPU fabric market therefore gains a second demand engine, one tied to compliance, national capacity building, and controlled deployment models rather than only public cloud expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Packaging and HBM Supply Constraints | -1.8% | Global, concentrated in Taiwan and South Korea | Short term (≤ 2 years) |

| Export Controls and Cross-Border Deployment Friction | -1.4% | Tier II and Tier III markets, China, Middle East, and parts of Asia-Pacific | Medium term (2-4 years) |

| High Power Density and Cooling Complexity | -0.8% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Proprietary Software Stack Lock-In Risks | -0.5% | Global, affecting enterprise and government buyers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Packaging and HBM Supply Constraints

The GPU fabric market still depends on how quickly complete AI systems can be manufactured, and that keeps advanced packaging and high-bandwidth memory availability at the center of deployment risk. NVIDIA’s 2026 production ramp for Vera Rubin, together with HPE and Dell announcements around dense Rubin systems, makes clear that next-generation platforms are moving into the field with much higher rack density and more demanding integration requirements. Even when switching, optics, and networking are ready, the GPU fabric market cannot monetize at full speed if core accelerator systems arrive later than planned. That mismatch pushes operators to stage interconnect spending, delay commissioning, and reserve infrastructure for hardware that is still in the queue. The effect is most visible in large clusters where one missing system tier can postpone utilization across multiple dependent fabric layers. For that reason, supply constraints at the accelerator package level still act as a practical ceiling on how fast the GPU fabric market can convert demand into live deployments.

Export Controls and Cross-Border Deployment Friction

Cross-border policy friction remains a clear restraint on the GPU fabric market because interconnect demand tracks the availability of the accelerators that sit behind each rack and cluster. CSIS noted that the AI diffusion framework places hard limits and compliance burdens on certain countries, which slows procurement and can delay eligibility for larger deployments. Al Jazeera also reported in June 2026 that U.S. restrictions extend to subsidiaries of Chinese companies located outside China, which broadens the geographic reach of export scrutiny. In practical terms, the GPU fabric market feels this through delayed rack buildouts, slower optics and switch purchases, and more cautious planning for sovereign or enterprise projects in affected regions. These rules do not remove demand, but they fragment timing and push some buyers toward alternative suppliers, modified specifications, or phased deployments. The result is a more uneven regional rollout pattern, even while core demand for AI infrastructure stays strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software And Services Gain More Weight Around Hardware-Led Spending

Hardware held 90.11% of the GPU fabric market share in 2025, which kept the component mix heavily tilted toward switches, NICs, cables, and optical modules. Services is projected to expand at a 24.21% CAGR through 2031, which shows that growth is moving beyond physical deployment into design support, optimization, monitoring, and managed operations. This structure means the GPU fabric market still derives most current revenue from installed hardware, but the operating complexity of AI clusters is shifting more value toward the layers that keep traffic balanced and utilization stable. In 2024, Juniper outlined how AI data center operators compare InfiniBand and RDMA over converged Ethernet in ways that increasingly tie switching outcomes to software policy and operational control rather than only hardware specifications. That is why the GPU fabric market is developing a wider services opportunity even though hardware remains the dominant spend bucket today.

The software segment is still the smallest by value, but it is becoming more central to how the GPU fabric industry differentiates performance across similar physical systems. NVIDIA’s full-stack approach around NVLink and Spectrum-X, Arista’s EOS operating model, and Juniper’s automation-led positioning all show that vendors want control of the operational layer where policy, telemetry, congestion management, and recovery are handled. Buyers are therefore less likely to treat services as a simple add-on, because troubleshooting a dense AI fabric can affect utilization across thousands of GPUs. Inference expansion adds to that shift since operators increasingly need dynamic traffic steering between different pools and deployment types rather than a fixed training topology. The GPU fabric market is also seeing more need for lifecycle support as companies mix proprietary and open systems inside one environment. Over time, the segment mix suggests that hardware will keep leading absolute revenue while software and services capture a larger share of strategic value inside the GPU fabric industry.

By Fabric Type: Scale-Up Becomes The Main Growth Engine While Scale-Out Keeps the Largest Base

Scale-out held 49.33% of the GPU fabric market size in 2025, which reflects the continued use of multi-node InfiniBand and Ethernet environments across large AI training estates. Scale-up is projected to expand at a 24.62% CAGR through 2031, which makes it the fastest-growing fabric type as rack-scale AI systems become more common. This split shows that the GPU fabric market is not abandoning scale-out, but it is giving more weight to configurations that keep more GPUs inside a tightly linked memory and bandwidth domain. NVIDIA’s NVLink platform supports scale-up architectures that connect 576 GPUs across 8 racks at 260 TB/s, which helps explain why rack-level density is pulling investment toward this segment. The performance appeal is strongest where latency-sensitive training and large model coordination benefit from more direct links and fewer external network hops.

Scale-across remains the smallest of the three, but it adds a meaningful strategic layer to the GPU fabric market because some operators want separate data centers to function more like one coordinated AI estate. NVIDIA introduced Spectrum-XGS Ethernet in 2025 for that purpose, which formalized scale-across as a commercial category rather than a conceptual extension of scale-out. The practical implication is that buyers now have clearer choices between rack-local performance, multi-rack expansion, and geographically distributed capacity. Scale-up should keep gaining as newer systems bundle more accelerators per rack, while scale-out remains essential for broad cluster growth and interoperability. Scale-across is likely to matter most in sovereign and resiliency-focused deployments where local sites still need to operate as parts of one larger compute estate. Taken together, these three layers show that the GPU fabric market is becoming more structurally diverse rather than converging on one standard architecture.

By Interconnect Technology: Proprietary Platforms Lead Today While Open Systems Broaden the Field

NVLink and proprietary GPU fabric accounted for 51.42% share in 2025, which placed closed and tightly integrated systems at the center of the interconnect mix. Co-packaged optics-based fabric is projected to expand at a 24.53% CAGR through 2031, showing that future growth is spreading into newer transport approaches even while proprietary links keep the largest current position. The GPU fabric market therefore combines a strong incumbent position at the scale-up layer with a rising set of alternatives in optics, Ethernet, and PCIe-based scaling. NVIDIA’s NVLink platform remains a reference point for high-bandwidth scale-up design because of its direct GPU-to-GPU bandwidth and switch-based domain expansion. That advantage supports continued leadership where buyers prioritize a tightly controlled and high-performance rack fabric.

At the same time, the GPU fabric market is opening in adjacent layers where buyers want multi-vendor options, broader compatibility, and more flexible cost structures. Broadcom’s Tomahawk 6 and Arista’s 7060XE7 systems show how fast Ethernet-based AI switching is moving up the performance curve. Marvell also introduced the Structera S PCIe 6.0 switch in 2026, which strengthens the position of PCIe-based scale-up paths in inference and heterogeneous system design. Co-packaged optics, while still early, addresses the physical and thermal pressure that comes with denser racks and longer high-speed reach. This means no single technology is positioned to solve every workload need inside the GPU fabric market. The segment is instead moving toward a layered model where proprietary links, Ethernet, PCIe, optics, and legacy high-performance networking all serve different parts of the deployment stack.

By Application: Inference Growth Changes How Fabrics are Designed and Operated

AI training held 62.12% share in 2025, which kept training as the largest application in the GPU fabric market. AI inference is projected to advance at a 24.32% CAGR through 2031, which makes it the faster-growing application and signals a broader change in traffic patterns. The GPU fabric market was built around large training clusters first, but the demand mix is now becoming more balanced as operators scale user-facing inference and enterprise AI services. NVIDIA’s 2026 announcements around Vera Rubin for science and broader AI factories show that large training systems remain essential, especially where synchronized model work and high-throughput communication are required. Training will therefore continue to anchor the revenue base, particularly in hyperscale and research deployments.

Inference, however, introduces a different operational profile for the GPU fabric market because lower latency, mixed hardware pools, and more distributed deployment footprints become more important. That is one reason Ethernet-based and PCIe-based designs are gaining attention, since not every inference deployment needs the same communication pattern as frontier model training. Marvell’s 2026 scale-up switch launch and Arista’s rack-scale Ethernet systems both point to this widening set of design options for production inference clusters. High-performance computing remains relevant as research institutions adopt newer direct liquid-cooled systems based on Rubin-class platforms. Edge and distributed AI also add to application diversity because they pull fabric requirements toward smaller, more operationally compatible deployments. The application mix now suggests that the GPU fabric market must support both training-heavy superclusters and more varied inference-led estates without assuming that one topology fits both.

By End User: Hyperscalers Still Lead While Sovereign Buyers Add a New Demand Layer

Hyperscalers and cloud service providers held 68.73% share in 2025, which kept them as the largest end-user group in the GPU fabric market by a wide margin. Government and research institutions are projected to expand at a 24.44% CAGR through 2031, which points to a second demand center forming beside cloud-led deployment. The current structure means hyperscalers still shape volumes, preferred architectures, and upgrade timing across the GPU fabric market. Arista’s 2026 announcement noted validation by Microsoft Azure, Oracle Cloud Infrastructure, Meta, and AMD, which confirms that the cloud ecosystem remains central to leading-edge switching adoption. Broadcom’s switch silicon leadership in open standards environments also reflects how strongly large cloud operators influence the competitive path of the GPU fabric market.

The fastest growth, though, comes from buyers that need tighter governance, on-prem deployment, or dedicated research systems. IBM Sovereign Core and the Palantir-NVIDIA Sovereign AI OS Reference Architecture both show that government and regulated organizations now have clearer infrastructure blueprints for controlled deployments. Enterprises remain an important middle group because many are expected to start with cloud-based AI services and later move selective workloads into private or hybrid environments. Telecom operators are still the smallest end-user segment, but they remain strategically relevant where edge inference and low-latency network functions intersect. This broadening end-user base reduces the risk that the GPU fabric market depends only on a few hyperscaler budget cycles. It also increases the need for vendors that can adapt systems to different policy, operating, and performance conditions without rebuilding the full stack each time.

Geography Analysis

North America held 38.44% of GPU fabric market share in 2025, which made it the largest regional base. The region leads because it combines hyperscaler concentration, mature AI infrastructure spending, and direct access to the leading vendors building rack-scale systems and open AI switching platforms. Arista’s 2026 launch was validated by major U.S. cloud operators, which shows how quickly North American deployments absorb next-generation Ethernet fabric hardware. NVIDIA’s 2026 Vera Rubin production ramp also reinforces North America’s role as the first large proving ground for dense scale-up AI infrastructure. Broadcom’s shipment of Tomahawk 6 adds to that lead because the region remains a primary destination for the switch silicon behind open standards AI cluster expansion.

Europe remains a meaningful part of the GPU fabric market because digital sovereignty and auditable AI deployment are strong purchasing themes across the region. IBM’s 2026 Sovereign Core release aligns well with this pattern, since European buyers often place greater weight on data control, residency, and governance across AI environments. The region also benefits from research computing demand and ongoing interest in dedicated national or institutional systems rather than only public cloud access. Europe may not match North America in hyperscaler scale, but it continues to support a wider mix of sovereign, enterprise, and research-led procurement in the GPU fabric market.

Asia-Pacific is projected to record the fastest regional CAGR at 24.42% through 2031, which gives it the strongest expansion outlook in the GPU fabric market. Growth across the region reflects aggressive infrastructure building in economies that want larger local AI capacity and stronger positions in the semiconductor supply chain. HPE and Dell both announced dense Rubin-based systems for 2026 availability, and that type of product roadmap supports the region’s need for newer on-prem and partner-led deployments as capacity expands. The GPU fabric market in Asia-Pacific also benefits from the region’s proximity to critical memory, packaging, and optical component ecosystems, even though those same supply chains can become points of pressure. South America and the Middle East and Africa remain smaller by current value, but they still matter as follow-on demand centers for sovereign, enterprise, and cloud-connected AI deployments. As a result, regional demand is becoming more distributed even while North America remains the largest installed base today.

Competitive Landscape

The GPU fabric market is moderately concentrated at the top, with NVIDIA holding the strongest position in proprietary scale-up interconnects while several other vendors compete across switching, optics, PCIe expansion, and software control. NVIDIA’s advantage comes from linking GPUs, switches, and system architecture into one stack, which keeps the company central to high-density rack designs and large training estates. At the same time, Broadcom sits in a critical middle position because its switch silicon supports many of the open standards alternatives that hyperscalers and system vendors continue to adopt. Arista has strengthened that open ecosystem through the 7060XE7 launch and software-led deployment model, which gives buyers a credible Ethernet-first path for AI fabrics. The result is a GPU fabric market where one vendor is strongest in the most tightly integrated layer, but no single supplier controls every important part of the deployment stack.

One notable strategic move came in 2025 when NVIDIA introduced NVLink Fusion, opening its interconnect to third-party silicon partners such as Marvell, Astera Labs, and MediaTek. That move matters because it extends NVIDIA’s influence even when buyers want semi-custom or non-NVIDIA compute elements inside a broader AI system. A second important move came in March 2026 when Marvell expanded its collaboration with NVIDIA across NVLink Fusion and silicon photonics, which tightened the link between scale-up interconnect and future optical infrastructure. A third move came from Broadcom and Arista as 102.4 Tbps silicon and 1.6T switching reached commercial rollout, giving open AI networks more credible performance at scale.

The next competitive layer in the GPU fabric market includes specialists building around PCIe expansion, optical transport, retimers, and sovereign deployment models. Marvell’s Structera S PCIe 6.0 switch gives the company a more direct role in scale-up design for AI data centers. Credo’s 2026 launch of 224G optical DSPs and a multiprotocol scale-up retimer shows that protocol-agnostic suppliers can gain when standards remain fragmented across the market. IBM and Palantir, while not core switch vendors, are helping define the sovereign and controlled deployment lane that could shape buyer preferences in government and regulated sectors. This leaves the GPU fabric market competitive in the middle tiers, especially where buyers want multi-vendor designs or operating flexibility. It also means that future leadership will depend not only on bandwidth leadership, but also on who can connect hardware, optics, management, and deployment models into a usable full-system proposition.

GPU Fabric Industry Leaders

NVIDIA Corporation

Broadcom Inc.

Arista Networks, Inc.

Cisco Systems, Inc.

Marvell Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA announced the Vera Rubin platform for scientific supercomputing (NVL4 architecture), with Dell Technologies, HPE, Supermicro, GIGABYTE, and Bull launching direct liquid-cooled Vera Rubin NVL4 rack systems; deployments at research institutions and national labs are planned for Q4 2026, extending GPU fabric addressable markets into the HPC and government research sectors.

- June 2026: Arista Networks launched the 7060XE7 Series, a portfolio of 1.6T rack-scale Ethernet switches based on Broadcom Tomahawk 6 silicon, delivering 100 Tbps switching capacity with 224G SerDes and validated by Microsoft Azure, Oracle Cloud Infrastructure, Meta, and AMD for production AI fabric deployments; air-cooled units are scheduled for Q4 2026.

- June 2026: Dell Technologies introduced the PowerEdge XE8812 server for NVIDIA Vera Rubin NVL4 architecture, achieving up to 144 GPUs per rack with 300 kW-plus power support and 100% direct liquid-cooled CPUs and GPUs, as part of the Dell AI Factory with NVIDIA expansion for HPC and sovereign AI deployments globally.

- June 2026: ZutaCore raised USD 100 million in a Series C round (investors include Mitsubishi Electric, Carrier Ventures, and Samsung Ventures) to scale its waterless, two-phase, direct-to-chip liquid cooling technology for AI data centers where rack power densities are entering the multi-megawatt range.

Global GPU Fabric Market Report Scope

The GPU Fabric Market refers to the industry ecosystem focused on designing and deploying high-speed, scalable interconnect architectures that enable efficient communication between Graphics Processing Units (GPUs) within clusters, data centers, and distributed computing environments.

The Global GPU Fabric Market Report is Segmented by Component (Hardware, Software, and Services), Fabric Type (Scale-Up, Scale-Out, and Scale-Across), Interconnect Technology (PCIe-Based Fabric, NVLink and Proprietary GPU Fabric, InfiniBand Fabric, Ethernet-Based Fabric, and Co-Packaged Optics Based Fabric), Application (AI Training, AI Inference, High-Performance Computing, Cloud and Data Center Workloads, and Edge AI and Distributed Computing), End User (Edge AI and Distributed Computing, Enterprises, Government and Research Institutions, and Telecom Operators), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Scale-Up GPU Fabric |

| Scale-Out GPU Fabric |

| Scale-Across GPU Fabric |

| PCIe-Based Fabric |

| NVLink and Proprietary GPU Fabric |

| InfiniBand Fabric |

| Ethernet-Based Fabric |

| Co-Packaged Optics Based Fabric |

| AI Training |

| AI Inference |

| High-Performance Computing |

| Cloud and Data Center Workloads |

| Edge AI and Distributed Computing |

| Hyperscalers and Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| Telecom Operators |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Fabric Type | Scale-Up GPU Fabric | |

| Scale-Out GPU Fabric | ||

| Scale-Across GPU Fabric | ||

| By Interconnect Technology | PCIe-Based Fabric | |

| NVLink and Proprietary GPU Fabric | ||

| InfiniBand Fabric | ||

| Ethernet-Based Fabric | ||

| Co-Packaged Optics Based Fabric | ||

| By Application | AI Training | |

| AI Inference | ||

| High-Performance Computing | ||

| Cloud and Data Center Workloads | ||

| Edge AI and Distributed Computing | ||

| By End User | Hyperscalers and Cloud Service Providers | |

| Enterprises | ||

| Government and Research Institutions | ||

| Telecom Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and future size of the GPU fabric market?

The GPU fabric market size is expected to increase from USD 45.60 billion in 2025 to USD 91.80 billion in 2026 and reach USD 227.30 billion by 2031, with a 22.64% CAGR over 2026-2031.

Which component category leads spending in GPU fabric deployments?

Hardware led the component mix with 90.11% share in 2025, mainly because switches, NICs, cables, and optical modules still account for most infrastructure spending.

Which fabric type is growing the fastest through 2031?

Scale-up fabric is projected to expand at a 24.62% CAGR through 2031, even though scale-out remained the largest fabric type in 2025 with a 49.33% share.

Why is AI inference becoming more important for interconnect design?

AI inference is projected to grow at a 24.32% CAGR through 2031, and that pushes operators toward lower-latency, more flexible fabric designs that can support mixed deployment environments.

Which end users are creating the strongest new demand outside hyperscalers?

Government and research institutions are projected to grow at a 24.44% CAGR through 2031, driven by sovereign AI, controlled deployments, and dedicated research infrastructure.

Which region offers the strongest growth outlook for suppliers?

Asia-Pacific is projected to record the fastest regional CAGR at 24.42% through 2031, while North America remained the largest regional base in 2025 with 38.44% share.

Page last updated on: