GPU Advanced Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

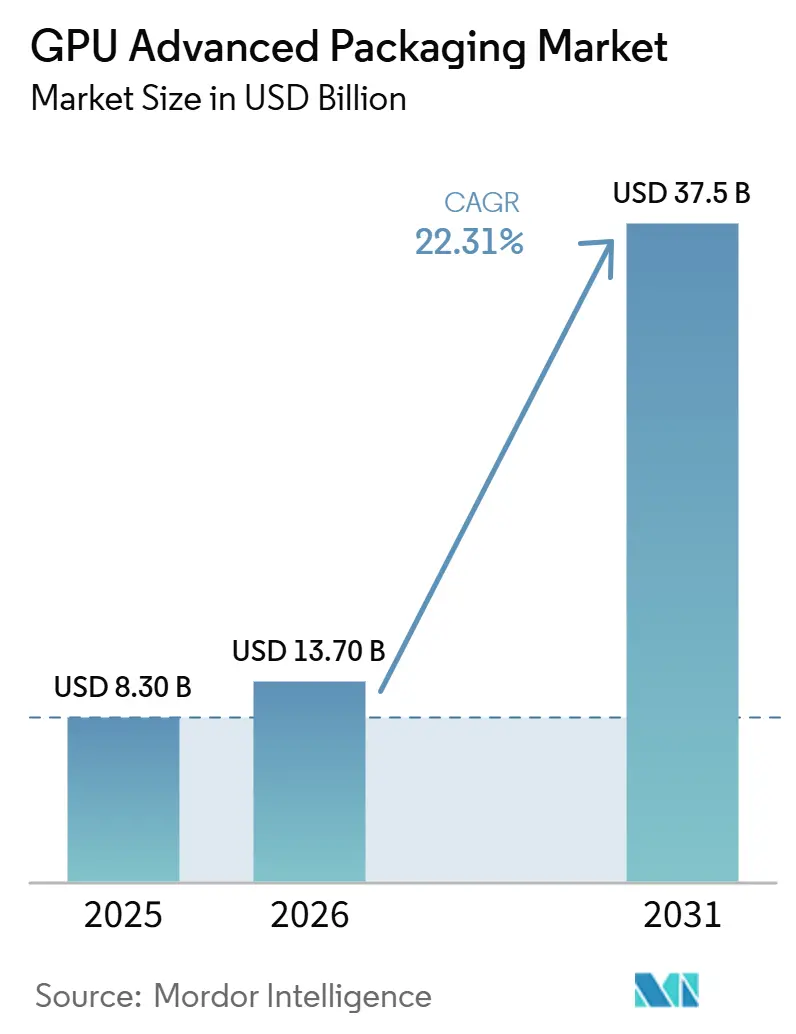

| Market Size (2026) | USD 13.70 Billion |

| Market Size (2031) | USD 37.5 Billion |

| Growth Rate (2026 - 2031) | 22.31% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Advanced Packaging Market Analysis by Mordor Intelligence

The GPU advanced packaging market size is expected to increase from USD 8.30 billion in 2025 to USD 13.70 billion in 2026 and reach USD 37.50 billion by 2031, growing at a CAGR of 22.31% over 2026-2031. Growth is tied to the fact that packaging now shapes how many AI GPUs can actually be delivered, because compute demand is rising faster than advanced packaging supply. The market is also being lifted by the move from monolithic GPU designs toward multi-die layouts that need more complex integration, more precise assembly, and tighter coordination between logic, memory, and thermal design. AI training remained the main demand center in 2025, while AI inference started to build a broader volume base that will keep demand more balanced across deployment types through 2031. Asia-Pacific remained the core manufacturing base in 2025, while North America is expanding faster as public incentives and supply chain security concerns push more packaging capacity closer to end customers. Competition remains concentrated at the leading edge, and this leaves room for foundries, OSATs, and captive packaging providers to compete on capacity access, process depth, and customer diversification rather than on price alone.

Key Report Takeaways

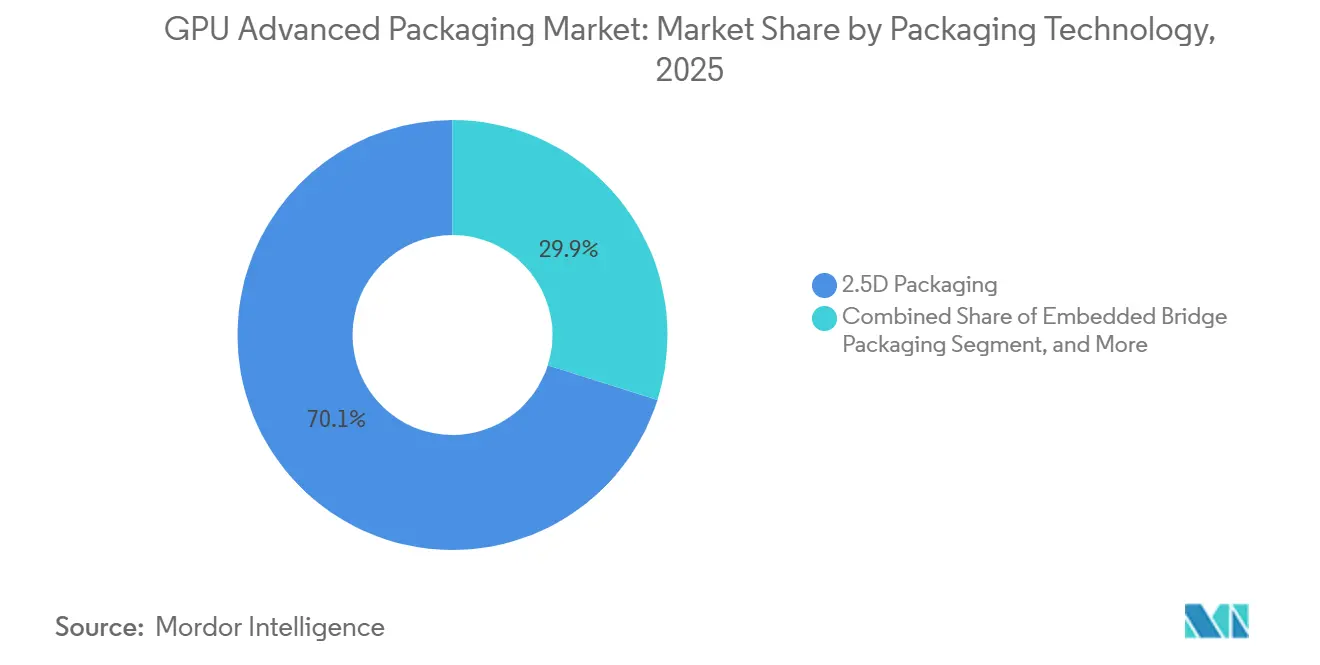

- By packaging technology, 2.5D silicon-interposer packaging accounted for 70.11% of the GPU advanced packaging market size in 2025, while hybrid 2.5D + 3D packaging is projected to expand at a 23.21% CAGR through 2031.

- By GPU configuration, chiplet-based GPU packages held 55.33% share in 2025, while GPU packages with stacked cache and I/O dies are projected to expand at a 23.62% CAGR through 2031.

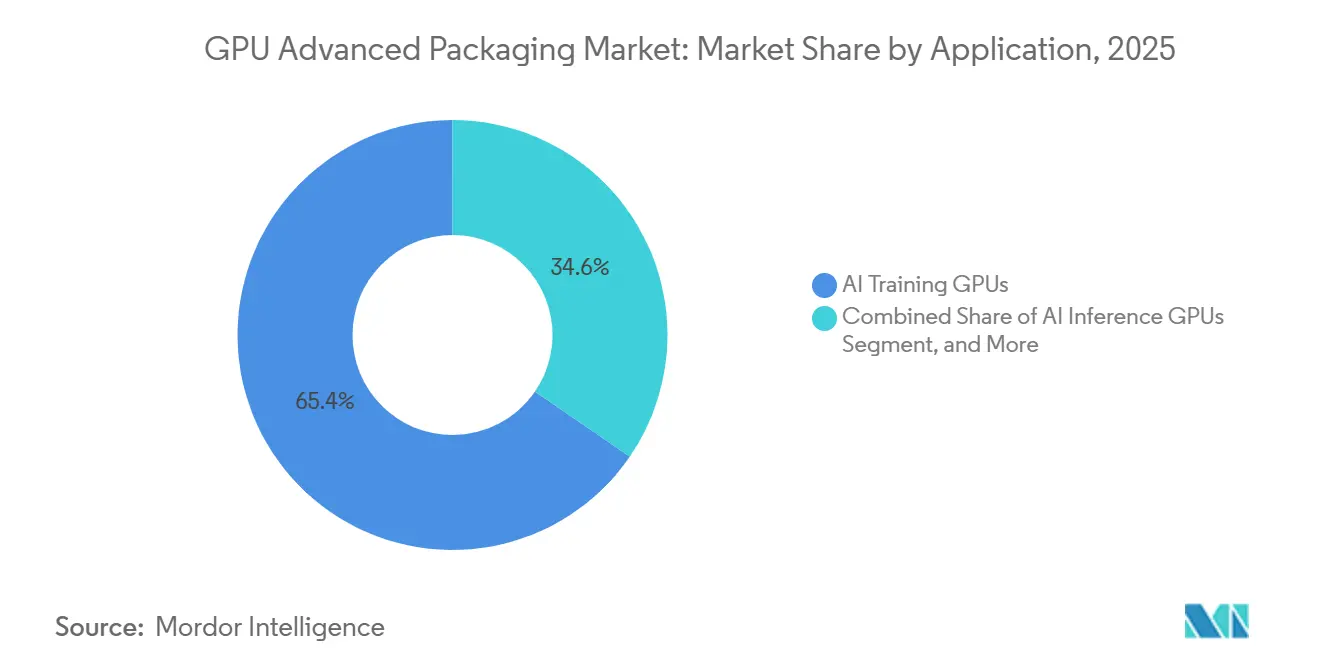

- By application, AI training GPUs held 65.42% share of the GPU advanced packaging market size in 2025, while AI inference GPUs are projected to expand at a 23.53% CAGR through 2031.

- By packaging service provider, foundry-led packaging held 79.12% of the GPU advanced packaging market share in 2025, while OSAT-led packaging is projected to expand at a 23.32% CAGR through 2031.

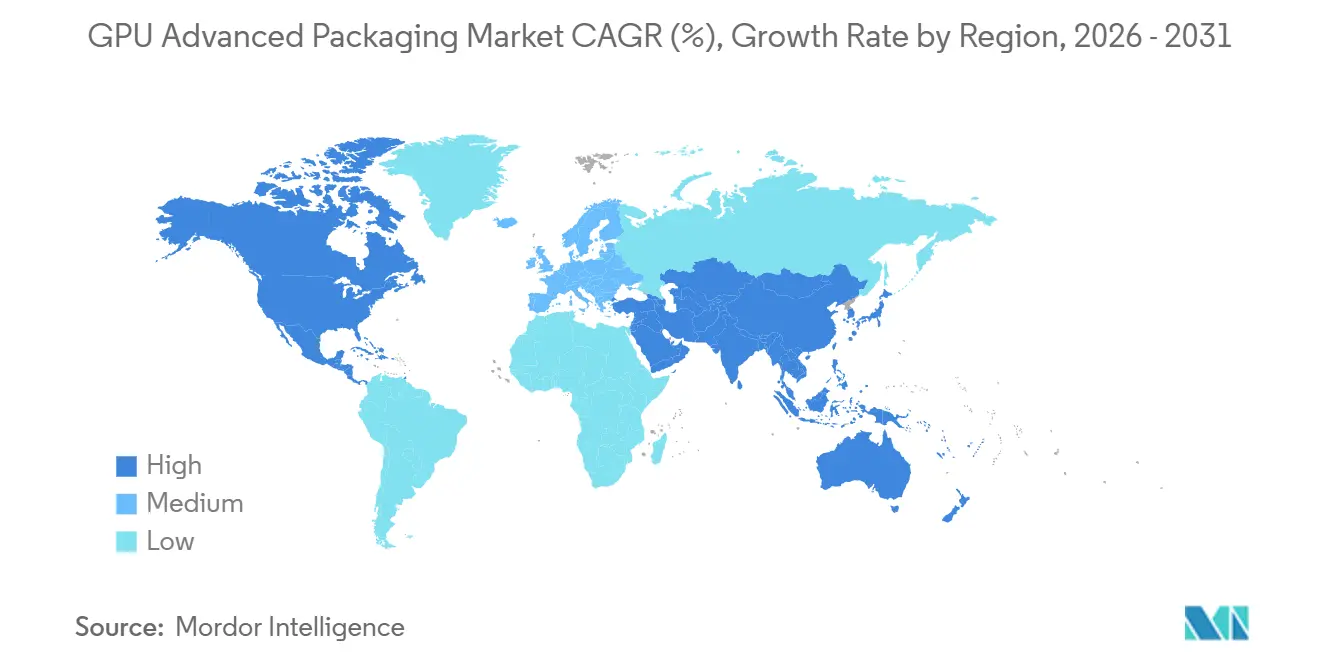

- By geography, Asia-Pacific held 68.44% of the GPU advanced packaging market share in 2025, while North America is projected to expand at a 23.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Advanced Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI GPU and HBM Integration Needs | +6.2% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Growth of Chiplet-Based GPU Architectures | +4.8% | Global, early gains in Taiwan, South Korea, and United States | Medium term (2-4 years) |

| Capacity Expansion By Foundries and OSATs | +4.0% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Government Incentives For Domestic Packaging Supply Chains | +2.6% | North America and Europe | Medium term (2-4 years) |

| Hybrid Bonding Adoption for Higher Interconnect Density | +2.0% | Global, with early gains in Taiwan, Japan, and South Korea | Long term (≥ 4 years) |

| Power and Thermal Efficiency Pressure in Data Center GPUs | +1.7% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising AI GPU and HBM Integration Needs Drive Packaging Demand

The GPU advanced packaging market is expanding because AI accelerators now need tight integration between GPU logic and high-bandwidth memory inside the same package. This requirement raises the value of interposers, die placement, thermal path design, and package level power delivery, because each one directly affects usable performance in training and inference systems. SK hynix stated in 2025 that its iHBM solution placed cooling features directly in the D2D PHY area, where heat concentration is highest, and this reduced thermal resistance by 30% in demanding package environments.[1]SK hynix, “SK hynix Unveils ‘iHBM’ Thermal Solution to Boost AI Performance,” SK hynix Newsroom That shift matters because memory stacking is no longer just a component choice, and it now changes how the full GPU package is engineered, qualified, and priced. As HBM stacks become denser, packaging decisions move earlier in the design cycle and stay tied to long customer qualification programs, which supports stronger revenue visibility for advanced package suppliers. The result is that the packaging layer has become one of the main technical gates for AI system deployment, rather than a downstream assembly step.

Growth of Chiplet-Based GPU Architectures Expands Packaging Complexity

The GPU advanced packaging market is also gaining from the wider use of chiplet-based GPU layouts that break large functions into smaller tiles and then reconnect them inside one package. This design path helps vendors work around reticle limits and yield pressure, but it also increases the need for dense die-to-die interconnects, tighter alignment, and more complex assembly flows. An IEEE Journal of Solid-State Circuits study published in 2025 described a scalable heterogeneous 2.5D system with 300 MB SRAM, 20 Tb/s bandwidth, and simultaneous inferencing across 20 chiplets, which shows how far multi-chip designs are moving beyond simple side-by-side integration.[2]Srivatsa Srinivasa et al., “A 300MB SRAM, 20Tb/s Bandwidth Scalable Heterogeneous 2.5D System Inferencing Simultaneous Streams Across 20 Chiplets with Workload-Dependent Configurations,” IEEE Journal of Solid-State Circuits Intel also noted in its November 2025 Foveros Direct 3D technology brief that hybrid bonding supports very fine pitch interconnects and denser vertical integration, reinforcing why advanced packaging is central to next-generation compute architecture. In practical terms, chiplet adoption broadens the mix of packages needed across AI training, HPC, and high-end inference products, instead of keeping demand tied to one package format. That broadening effect gives the GPU advanced packaging market a wider and more durable demand base as product roadmaps become more modular.

Government Incentives for Domestic Packaging Supply Chains Shift Investment

The GPU advanced packaging market is benefiting from public policy that treats packaging as critical semiconductor infrastructure rather than as a lower priority backend activity. The U.S. Department of Commerce announced USD 1.4 billion in final awards in January 2025 for advanced packaging, including USD 1.1 billion to Natcast and USD 100 million each to Applied Materials and Absolics for ecosystem development. The same policy direction supported preliminary terms for up to USD 400 million toward Amkor Technology's planned USD 2 billion advanced packaging campus in Peoria, Arizona, which is intended to establish high-volume domestic OSAT capability. These measures matter because they reduce customer dependence on a single regional cluster and create a clearer path for defense, national security, and hyperscale buyers that want packaging capacity closer to home. They also encourage equipment, substrate, and material suppliers to align their own investment plans with new packaging buildouts in the United States and Europe. Over the forecast period, that policy support should widen the supplier base that can participate in the GPU advanced packaging market without changing the fact that Asia-Pacific remains the main production center.

Power and Thermal Efficiency Pressure Makes Packaging a Design Lever

The GPU advanced packaging market is being pushed forward by power density and heat removal limits that cannot be solved by silicon design alone. Dense multi-die packages bring logic, memory, and I/O into a smaller footprint, so package materials, vertical paths, and cooling features have a direct effect on system stability and throughput. SK hynix highlighted this in its iHBM work by focusing on the hottest area of the package and lowering thermal resistance by 30%, which points to the commercial value of package-led thermal improvement. Research published in 2025 on hybrid bonding manufacturing challenges also noted that alignment precision and thermal budget constraints become harder to sustain as packaging moves toward finer pitch and more advanced heterogeneous integration.[3]“Manufacturing Challenges of Hybrid Bonding for Chiplets Heterogeneous Integration,” ASME Journal of Electronic Packaging This means package engineering now affects not only yield, but also power efficiency, sustained clocks, and long-term reliability in AI deployment settings. As a result, buyers in the GPU advanced packaging market increasingly view packaging competence as part of compute performance, not as a separate manufacturing service.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CoWoS and Comparable Advanced Packaging Capacity Bottlenecks | -3.2% | Global, most severe in Taiwan | Short term (≤ 2 years) |

| High Capex and Yield Risk in 2.5D and 3D Lines | -2.4% | Global | Medium term (2-4 years) |

| Thermal Management Complexity in Dense Multi-Die Packages | -1.6% | Global | Medium term (2-4 years) |

| Glass and Panel-Level Ecosystem Readiness Gaps | -1.0% | Global, early bottlenecks in Taiwan, Japan, and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CoWoS And Comparable Capacity Bottlenecks Limit Revenue Conversion

The GPU advanced packaging market still faces a supply ceiling because demand for leading-edge package formats remains heavily concentrated in a narrow set of qualified platforms and production lines. Even when end demand is strong, revenue cannot fully convert if substrate availability, interposer capacity, memory integration, and final package throughput do not scale together. The U.S. Department of Commerce framed advanced packaging as a strategic gap in the semiconductor supply chain when it announced large public awards for domestic ecosystem buildout, which supports the view that current supply remains structurally constrained. This constraint matters most for flagship AI programs, because those products rely on the most advanced packaging flows and cannot easily switch to lower-complexity alternatives once design qualification is complete. It also reinforces customer concentration around a few suppliers that already operate at the leading edge, which limits bargaining power for GPU designers that need fast volume ramps. Until more qualified lines come online across regions and providers, the GPU advanced packaging market will continue to face periods when demand runs ahead of practical package output.

High Capex and Yield Risk Raise the Barrier to New Capacity

The GPU advanced packaging market is restrained by the fact that the most advanced 2.5D and 3D flows require precision equipment, long validation cycles, and disciplined yield learning before they become economically dependable. Hybrid bonding work published in 2025 showed that manufacturing challenges remain significant in heterogeneous integration, especially when pitch shrinks and process tolerances become tighter. Intel's 2025 Foveros Direct 3D technology brief also underscored how advanced vertical stacking depends on exact process control, which confirms that scaling these flows is not only a matter of buying more tools. For new entrants, this creates a difficult balance between building enough capacity to matter and maintaining yields that support customer qualification. For existing leaders, it explains why they prioritize selective expansion and customer co-development rather than open capacity access for every program. The result is a slower supply response than headline demand would suggest, and that keeps the GPU advanced packaging market exposed to periodic bottlenecks despite strong long-term momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Technology: 2.5D Interposers Anchor Volume, Hybrid Stacking Accelerates

2.5D silicon-interposer packaging held 70.11% of the market in 2025, which kept it as the volume anchor of the GPU advanced packaging market. That position reflects its role as the default integration route for advanced GPU and HBM combinations, where the package must support dense interconnects, large memory footprints, and stable thermal behavior. The installed base of qualified design flows also matters, because customers already rely on this format for high-value programs and cannot easily absorb long requalification cycles during active product ramps. In effect, 2.5D kept its lead because it offers the best balance between bandwidth density, customer familiarity, and near-term production readiness for top AI deployments.

The GPU advanced packaging market is also shifting toward hybrid 2.5D + 3D packaging, which is projected to expand at a 23.21% CAGR through 2031. This segment is gaining because it combines horizontal integration and vertical stacking in a way that can push beyond the practical limits of pure interposer designs. The direction is consistent with broader industry work on fine-pitch hybrid bonding, denser vertical links, and more advanced heterogeneous integration. Fan-out and redistribution-layer approaches continue to fit programs that need thinner form factors or more controlled cost, while embedded bridge solutions are building a role where customers want a credible path outside the largest interposer-based platforms. Over time, this means the GPU advanced packaging industry is moving from one dominant package choice toward a more segmented technology mix that maps to workload needs, thermal limits, and customer budgets.

By GPU Configuration: Chiplets Reshape the Design Foundation for AI Accelerators

Chiplet-based GPU packages commanded 55.33% of the configuration mix in 2025, and this made them the leading configuration in the GPU advanced packaging market. The share reflects a structural shift in design logic, because breaking functions into smaller dies helps vendors manage yield, reticle boundaries, and product scaling across multiple performance tiers. It also aligns with research results that show chiplet-rich 2.5D systems can deliver very high bandwidth and broader configuration flexibility across many active dies. That mix gives chiplet layouts a stronger long-term foundation than single large dies in the highest-value AI accelerator classes.

GPU packages with stacked cache and I/O dies are projected to expand at a 23.62% CAGR through 2031, making them the fastest-growing configuration in the GPU advanced packaging market size discussion for emerging design layers. This growth is tied to the need to lift bandwidth and reduce latency without expanding package footprint beyond what current board, power, and cooling systems can handle. Very fine pitch hybrid bonding supports that direction by enabling closer vertical links and more compact heterogeneous stacks. Monolithic GPU packages still matter in gaming, visualization, and other cost-sensitive areas where disaggregation does not always pay off. Even so, the broader design center of gravity inside the GPU advanced packaging market is moving toward more layered and more modular package structures as AI compute demand intensifies.

By Application: AI Training Dominates, Inference Broadens the Demand Base

AI training GPUs accounted for 65.42% of application revenue in 2025, which kept them as the dominant use case in the GPU advanced packaging market. This lead came from large cluster buildouts, where performance goals justified complex packages with high memory density and stringent package level engineering. Training workloads also tend to favor the most advanced package formats because system operators value raw throughput, scaling efficiency, and stable operation under sustained load. That concentration has made training programs a major anchor for supplier planning, capacity allocation, and customer qualification across the market.

AI inference GPUs are projected to expand at a 23.53% CAGR through 2031, and this makes them the fastest-growing application in the GPU advanced packaging market. The shift matters because inference brings a wider deployment base, including enterprise systems, edge installations, and more specialized accelerators that still need advanced package performance. Package decisions become more sensitive to energy efficiency, thermals, and system cost in this segment, which broadens the commercial logic for hybrid and more application-specific packaging architectures. HPC remains a steady middle layer of demand, while gaming and professional visualization continue to rely on less packaging intensity per unit in many cases. As inference scales, the GPU advanced packaging market gains a second major volume engine that complements training rather than replacing it.

By Packaging Service Provider: Foundries Lead, OSATs Build a Larger Role

Foundry-led packaging held 79.12% of the service provider mix in 2025, which gave this group the largest position in the GPU advanced packaging market. That concentration reflects strong customer dependence on leading-edge package platforms that sit close to advanced logic manufacturing and benefit from tightly linked co-development cycles. It also explains why the highest-value AI programs remain concentrated among a small number of qualified suppliers, even while broader capacity expansion is underway. In commercial terms, foundries kept the lead because they controlled the deepest combination of process integration, design support, and production readiness for advanced GPU packages.

OSAT-led packaging is projected to expand at a 23.32% CAGR through 2031, making it the fastest-growing provider category in the GPU advanced packaging market. Customers want more than one route to advanced packaging, and that gives OSATs a stronger role in programs that do not need the most exclusive process stack. Public support for domestic packaging expansion also strengthens the case for OSAT growth, especially where governments and end users want more regional diversity in supply. IDM and captive packaging remains a third path that can gain relevance when integrated device makers use their own package technologies to serve internal programs or selected external customers. Taken together, the GPU advanced packaging industry is still concentrated, but the provider structure is widening enough to create a more layered competitive field by the end of the forecast period.

Geography Analysis

The GPU advanced packaging market remained concentrated in Asia-Pacific in 2025, with the region holding 68.44% share of global demand and supply activity. This lead came from the region's combination of foundry depth, memory supply, substrate capability, and OSAT scale, which gives customers shorter feedback loops between design, assembly, and qualification. South Korea remains important because advanced memory and package co-development are tightly linked, and NVIDIA and SK hynix formalized that linkage further through their June 2026 multiyear technology partnership for AI memory platforms. Asia-Pacific also benefits from a mature supplier web that can support multiple package technologies at commercial scale, from interposer-based flows to more experimental next-generation formats. This keeps the GPU advanced packaging market centered in the region even as other geographies increase their investment pace.

North America is projected to grow at a 23.42% CAGR through 2031, and this makes it the fastest-growing regional layer of the GPU advanced packaging market size outlook. That expansion is being supported by direct public funding, pilot infrastructure, and new domestic packaging plans intended to strengthen semiconductor resilience. The U.S. Department of Commerce's January 2025 package of USD 1.4 billion in final awards placed advanced packaging at the center of broader chip policy, rather than treating it as a secondary part of the supply chain. Preliminary support for Amkor's planned Arizona campus extends that policy into commercial capacity and signals that the United States wants a functioning high-volume OSAT base onshore. For customers in defense, hyperscale computing, and national infrastructure, the value of local capacity is not only cost related, but also tied to assurance, lead times, and risk management.

Europe, South America, and the Middle East and Africa remain smaller in direct manufacturing scale, but they still shape the GPU advanced packaging market through equipment, materials, and downstream demand. Europe is especially relevant in process equipment and ecosystem development, where suppliers help advance next-generation packaging formats that feed into global production chains. LPKF and Onto Innovation announced a collaboration in April 2025 to accelerate mass production of glass core substrates, and that supports Europe's role in enabling future package architectures rather than in dominating high-volume GPU assembly. South America and the Middle East and Africa remain more important as end markets for AI infrastructure deployments than as major packaging production hubs. Even without large local manufacturing footprints, those deployments still add to demand for advanced-packaged GPUs shipped from the main supply regions.

Competitive Landscape

The GPU advanced packaging market remains highly concentrated at the leading edge, because a small number of providers control the package technologies and qualification depth required for flagship AI products. Foundry-led players still hold the strongest position in the highest-value programs, while OSATs and captive providers are trying to build more credible alternatives for overflow demand and second-tier advanced deployments. This structure keeps the market competitive in strategy and investment, even when it is not fully open in capacity access. It also means customer relationships tend to be deeper and longer than in more standardized packaging categories.

Strategic moves in 2025 and 2026 show how companies are trying to widen their role in the GPU advanced packaging market. Applied Materials announced in May 2026 that it would acquire NEXX from ASMPT, which adds large-area panel-level electrochemical deposition capability to its advanced packaging portfolio and strengthens its position in fine-pitch package tooling. NVIDIA and SK hynix also announced a multiyear technology partnership in June 2026, linking future AI systems more closely to advanced memory and package integration planning across several product families. In parallel, U.S. policy support for Amkor's planned Arizona campus shows that governments are influencing competitive structure by helping new regional capacity reach commercial scale. These moves do not break concentration at the top, but they do widen the field of companies that can shape future package roadmaps.

Competition is also broadening at the ecosystem layer, where equipment, materials, and enabling process suppliers are becoming more important to the GPU advanced packaging market. LPKF's 2025 collaboration around glass substrate processing highlights how next-generation package formats need ecosystem coordination long before they become high-volume commercial products. Intel's continued emphasis on advanced 3D packaging methods also reinforces that packaging differentiation is now part of platform strategy, not a narrow backend function. Over the forecast period, leadership will depend on who can combine process maturity, customer qualification, and ecosystem control across memory, substrates, thermal solutions, and assembly. That is why the GPU advanced packaging market is likely to stay concentrated at the frontier even as more participants enter adjacent parts of the value chain.

GPU Advanced Packaging Industry Leaders

Taiwan Semiconductor Manufacturing Company Limited

Intel Corporation

Samsung Electronics Co., Ltd.

ASE Technology Holding Co., Ltd.

Amkor Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK Hynix announced a multiyear technology partnership on June 7, 2026, to co-develop advanced memory for AI factories, covering HBM supply for NVIDIA Vera Rubin AI supercomputers, Vera CPUs, RTX Spark-powered PCs, and Jetson Thor robotics platforms, extending co-integration commitments across GPU packaging programs scheduled through the end of the decade.

- May 2026: Applied Materials announced a definitive agreement to acquire NEXX from ASMPT Limited on May 3, 2026, adding large-area panel-level electrochemical deposition equipment to its advanced packaging portfolio to enable fine-pitch I/O wiring for larger-body AI GPU packages, and the NEXX team will join Applied's Semiconductor Products Group.

- May 2026: AMD announced an investment of more than USD 10 billion in Taiwan's advanced packaging ecosystem over three years, partnering with ASE and SPIL on EFB-based 2.5D packaging for its MI450X GPU and EPYC Venice CPU programs within the Helios rack-scale platform, with multi-gigawatt deployments targeted for late 2026.

- May 2026: ASE Technology and WUS Printed Circuit announced a strategic collaboration to build an advanced AI packaging hub in Kaohsiung's Nanzih Technology Industrial Park, incorporating FOCoS and FC BGA technologies for AI, cloud computing, and autonomous driving applications; facility completion is scheduled for September 2029.

Global GPU Advanced Packaging Market Report Scope

The Global GPU Advanced Packaging Market refers to the industry segment focused on the design, development, and deployment of cutting-edge semiconductor packaging technologies tailored for Graphics Processing Units (GPUs). Advanced packaging solutions, including 2.5D/3D integration, chiplet architectures, fan-out wafer-level packaging, and heterogeneous integration, are critical for enhancing GPU performance, power efficiency, and scalability in applications such as artificial intelligence (AI), machine learning (ML), high-performance computing (HPC), gaming, and data center workloads.

The GPU Advanced Packaging Market Report is Segmented by Packaging Technology (2.5D Packaging, 3D Packaging, Fan-Out / RDL-Based Packaging, Embedded Bridge Packaging, and Hybrid 2.5D + 3D Packaging), GPU Configuration (Monolithic GPU Packages, Chiplet-Based GPU Packages, GPU Packages with HBM Integration, and GPU Packages with Stacked Cache / I/O Dies), Application (AI Training GPUs, AI Inference GPUs, HPC GPUs, Professional Visualization GPUs, Gaming and Consumer GPUs, and Edge, Industrial, and Automotive GPUs), Service Provider (Foundry-Led Packaging, OSAT-Led Packaging, and IDM / Captive Packaging), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 2.5D Packaging |

| 3D Packaging |

| Fan-Out / RDL-Based Packaging |

| Embedded Bridge Packaging |

| Hybrid 2.5D + 3D Packaging |

| Monolithic GPU Packages |

| Chiplet-Based GPU Packages |

| GPU Packages with HBM Integration |

| GPU Packages with Stacked Cache / I/O Dies |

| AI Training GPUs |

| AI Inference GPUs |

| HPC GPUs |

| Professional Visualization GPUs |

| Gaming and Consumer GPUs |

| Edge, Industrial, and Automotive GPUs |

| Foundry-Led Packaging |

| OSAT-Led Packaging |

| IDM / Captive Packaging |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Packaging Technology | 2.5D Packaging | |

| 3D Packaging | ||

| Fan-Out / RDL-Based Packaging | ||

| Embedded Bridge Packaging | ||

| Hybrid 2.5D + 3D Packaging | ||

| By GPU Configuration | Monolithic GPU Packages | |

| Chiplet-Based GPU Packages | ||

| GPU Packages with HBM Integration | ||

| GPU Packages with Stacked Cache / I/O Dies | ||

| By Application | AI Training GPUs | |

| AI Inference GPUs | ||

| HPC GPUs | ||

| Professional Visualization GPUs | ||

| Gaming and Consumer GPUs | ||

| Edge, Industrial, and Automotive GPUs | ||

| By Packaging Service Provider | Foundry-Led Packaging | |

| OSAT-Led Packaging | ||

| IDM / Captive Packaging | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 to 2031 outlook for GPU advanced packaging revenue?

The GPU advanced packaging market size is expected to increase from USD 13.70 billion in 2026 to USD 37.50 billion by 2031 at a 22.31% CAGR.

Which packaging technology leads GPU advanced packaging demand?

2.5D silicon-interposer packaging led with 70.11% share in 2025, showing that it remained the main volume platform for advanced GPU and HBM integration.

Which GPU configuration is growing the fastest through 2031?

GPU packages with stacked cache and I/O dies are projected to expand at a 23.62% CAGR, reflecting stronger interest in dense vertical integration.

Why is AI training still the largest use case?

AI training GPUs held 65.42% of application revenue in 2025 because large model training clusters still require the highest package complexity and memory density.

Which region is expanding the fastest?

North America is projected to grow at a 23.42% CAGR through 2031 as public funding and domestic supply chain programs support new packaging capacity.

Why are packaging bottlenecks still important in this field?

Bottlenecks matter because advanced package output depends on qualified process flows, substrates, memory integration, and yield control, so demand cannot always convert into shipments even when customer orders are strong.

Page last updated on: