GMC Based Motion Controller Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

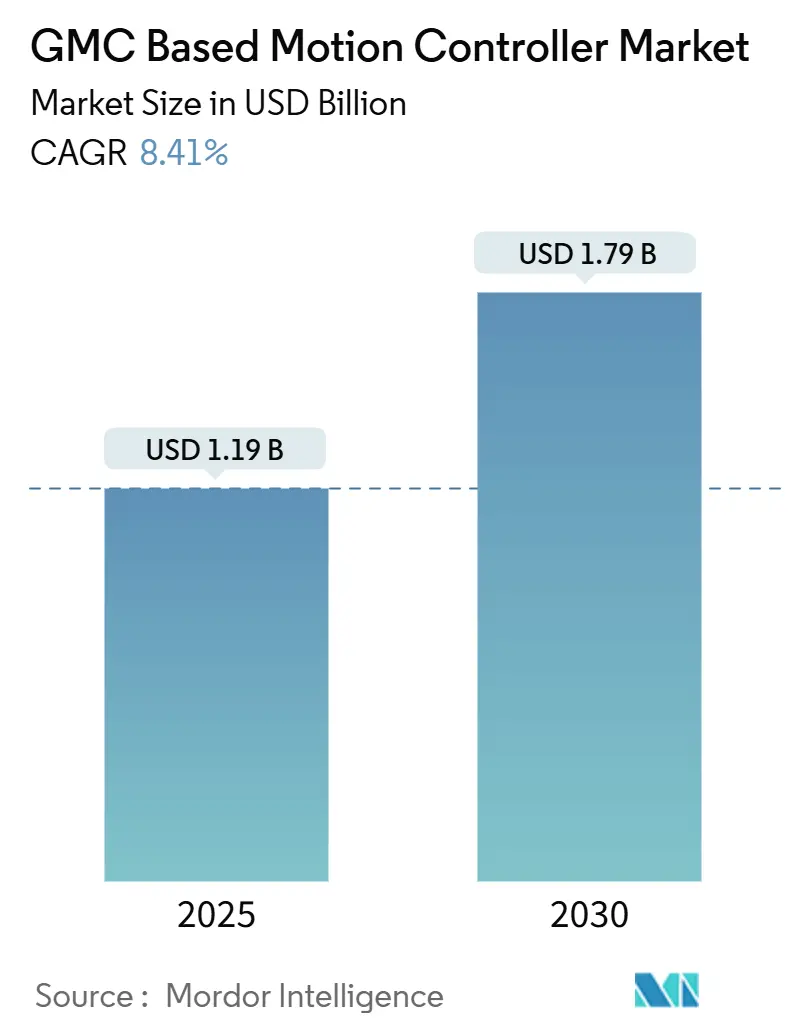

| Market Size (2025) | USD 1.19 Billion |

| Market Size (2030) | USD 1.79 Billion |

| Growth Rate (2025 - 2030) | 8.41% CAGR |

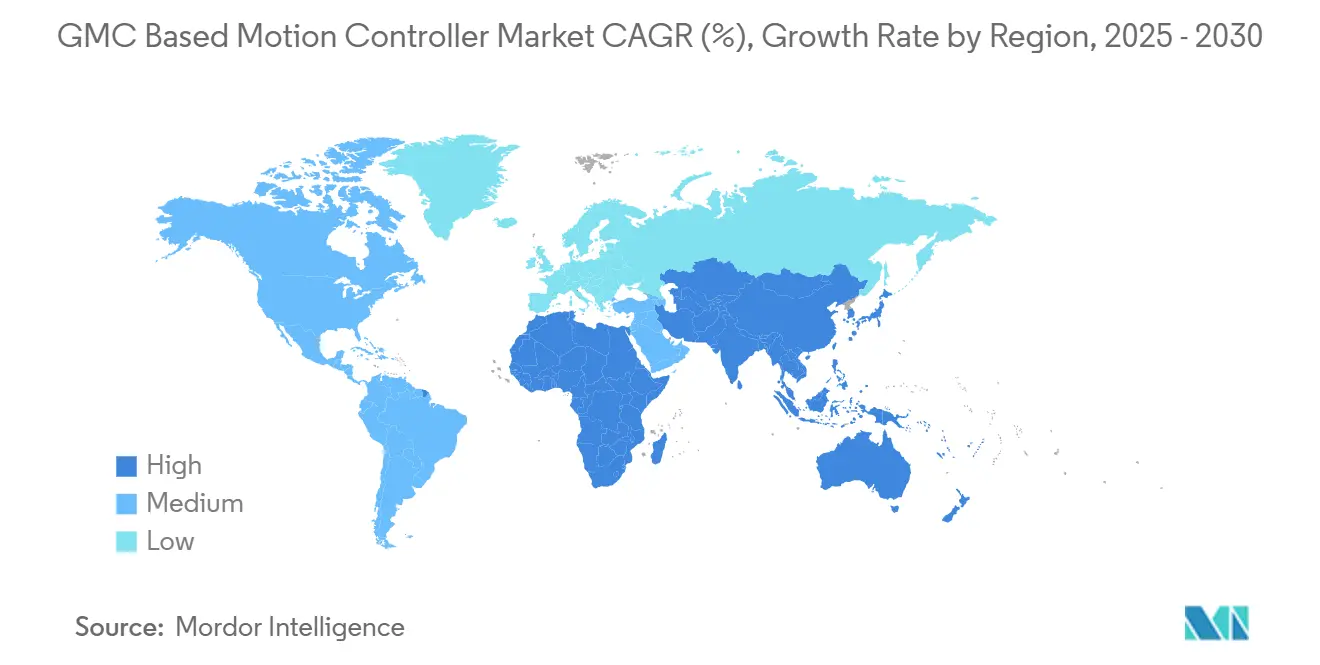

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

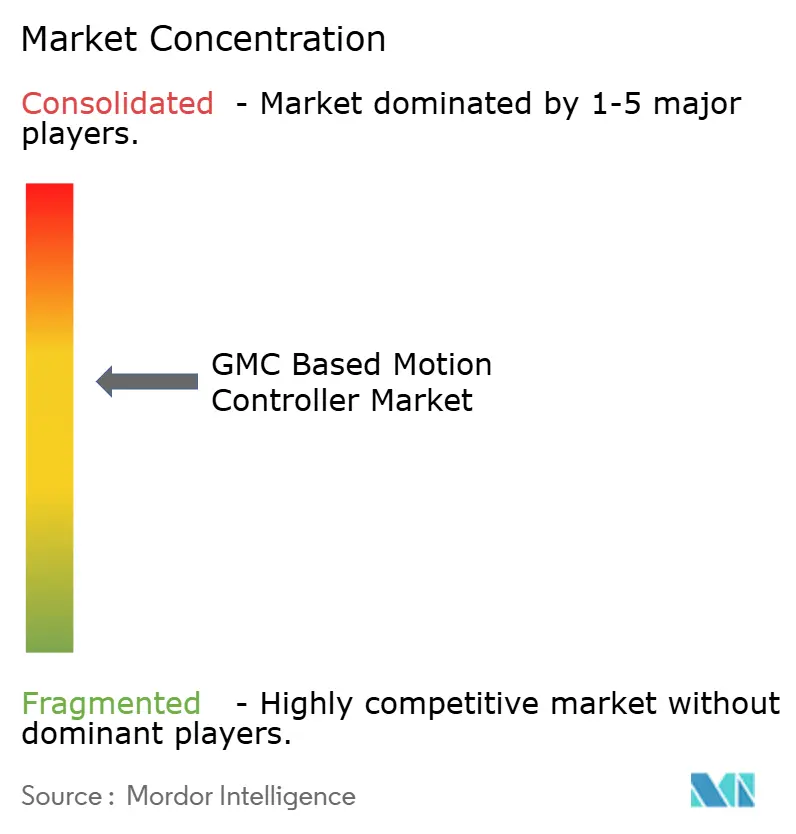

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GMC Based Motion Controller Market Analysis by Mordor Intelligence

The GMC-based motion controller market size is USD 1.19 billion in 2025 and is projected to reach USD 1.79 billion by 2030, advancing at an 8.41% CAGR over the forecast period. Demand accelerates as open Ethernet architectures displace proprietary field buses, EtherCAT secures a 43.91% protocol share, and digital twin workflows trim commissioning time by up to 40% in high-axis semiconductor and robotics cells. The rising density of robots in the Asia Pacific, the push for multi-axis precision in electric vehicle battery lines, and government incentives that promote the localization of controller assembly across India, Vietnam, and Thailand further propel adoption. Vendors now compete on ecosystem breadth, encompassing cloud analytics, AI-driven tuning, and TSN convergence, rather than solely on raw cycle time. Meanwhile, cybersecurity hardening and brownfield retrofit economics temper near-term growth.

Key Report Takeaways

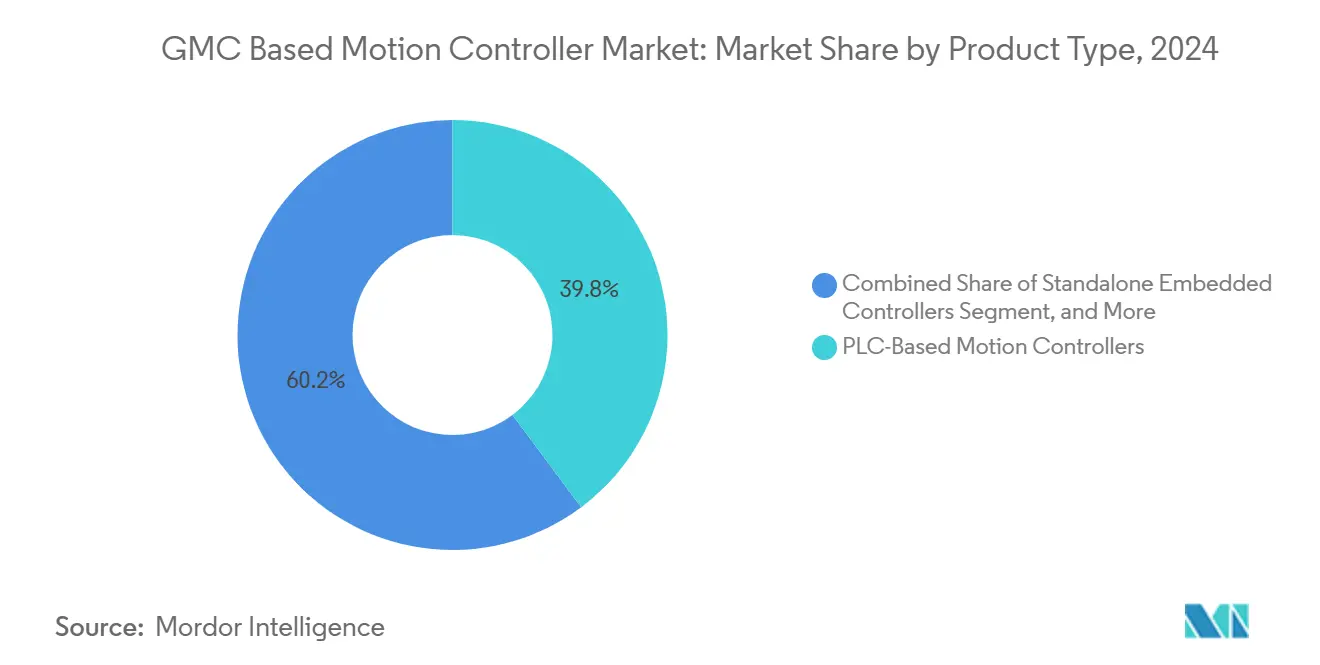

- By product type, PLC-based units held 39.78% of GMC based motion controller market share in 2024, while standalone embedded controllers recorded the quickest pace at a 9.23% CAGR through 2030.

- By axis count, installations above 10 axes represented the fastest-growing slice of the GMC-based motion controller market, with a 9.17% CAGR, whereas the 3-5 axis bracket retained the largest revenue share at 36.54% in 2024.

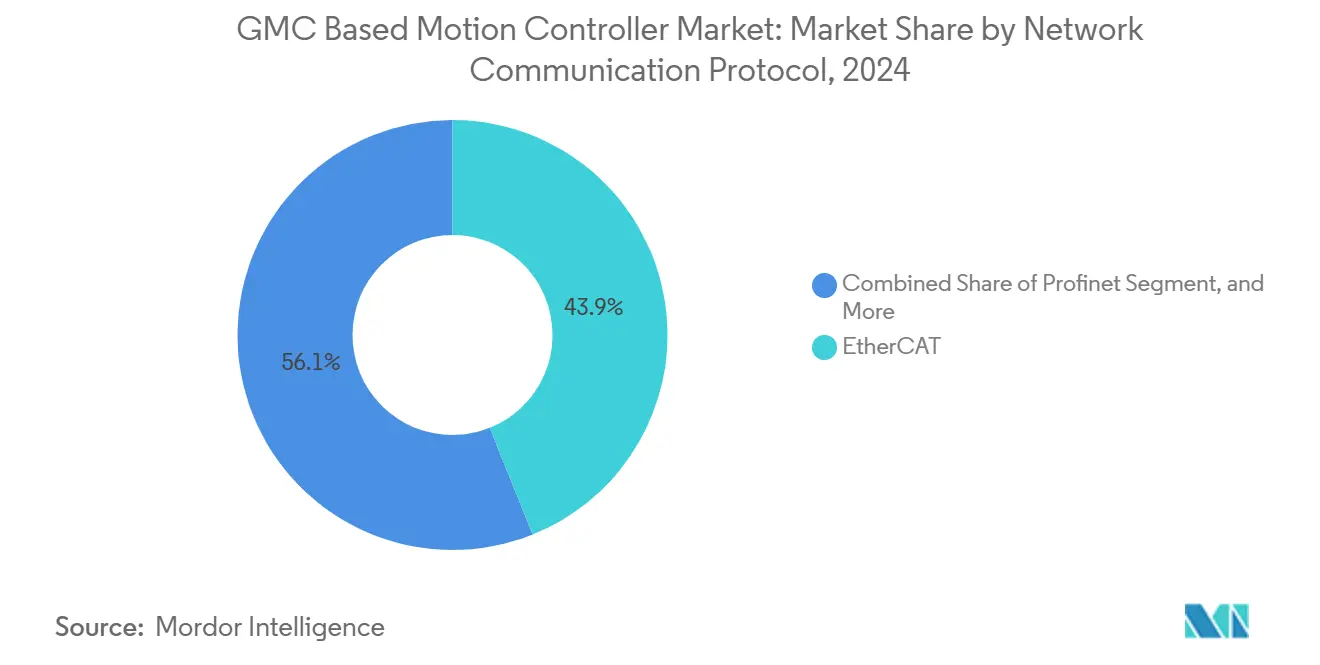

- By network protocol, EtherCAT captured 43.91% of the market in 2024 and is forecasted to rise at a 9.41% CAGR to 2030, outpacing Profinet and EtherNet/IP.

- By end-use industry, semiconductor and electronics equipment led 2024 growth with a 9.59% CAGR outlook, even as robotics and automation applications commanded 28.66% of overall demand.

- By geography, the Asia Pacific accounted for 42.89% of 2024 revenue, but Africa is poised for the fastest regional expansion, at a 9.47% CAGR, to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GMC Based Motion Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of EtherCAT-Enabled Architectures | +1.8% | Europe, Asia Pacific semiconductor hubs, North America automotive clusters | Medium term (2-4 years) |

| Rising Demand for Multi-Axis Synchronisation in Robotics | +1.5% | China, Japan, South Korea, spill-over to North America and Europe | Medium term (2-4 years) |

| Growing Shift Toward PC-Based Motion Control Platforms | +1.3% | North America and Europe advanced manufacturing, Asia Pacific high-tech OEMs | Long term (≥ 4 years) |

| Expansion of Compact Standalone Controllers for OEMs | +1.2% | Europe machinery builders, Asia Pacific collaborative robotics integrators | Short term (≤ 2 years) |

| Emergence of Digital Twin Workflows for Motion Optimisation | +1.0% | North America and Europe aerospace and semiconductor, Asia Pacific electronics manufacturing | Long term (≥ 4 years) |

| Supply-Chain Localisation Incentives in Asia Pacific | +0.9% | India, Vietnam, Thailand with spill-over in Mexico and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of EtherCAT-Enabled Architectures

EtherCAT surpassed 88 million installed nodes by 2024 and now anchors deterministic motion in semiconductor tools, packaging machines, and high-throughput robotics.[1]EtherCAT Technology Group, “Technology Overview,” ethercat.org On-the-fly frame processing synchronizes 32 servo axes within 1 microsecond across 100 meters of cable, trimming panel footprints by 40% compared with legacy buses. Planar-motor platforms, such as Beckhoff XPlanar, coordinate 256 movers for wafer handling at rates exceeding 300 wafers per hour, demonstrating the scalability of the protocol. IEC standardization, TSN convergence, and SIL 3 safety over the same wire enable OEMs to consolidate motion, vision, and safety traffic onto a single network, reducing wiring and changeover time for flexible packaging lines.

Rising Demand for Multi-Axis Synchronisation in Robotics

The global robot stock reached 4.28 million units in 2024, and annual installations topped 541,000, with half of them located in China.[2]International Federation of Robotics, “World Robotics 2024 – Industrial Robots,” ifr.org Multi-axis controllers now steer collaborative arms that insert gears, dispense adhesives, or drive screws with ±0.05 millimeter accuracy. AI-enhanced planners, funded by investments such as Mitsubishi Electric’s stake in Realtime Robotics, cut collision-free path computation for 12-axis cells to under 50 milliseconds. Electric-vehicle battery lines utilize 8-axis gantries for cell stacking, and pharmaceutical pick-and-place systems can exceed 600 packs per minute, both tasks that are impossible without tightly synchronized electronic camming.

Growing Shift Toward PC-Based Motion Control Platforms

Industrial PCs equipped with Intel Xeon or AMD EPYC processors utilize real-time Linux to achieve 250-microsecond cycle times, while hosting vision, analytics, and OPC UA servers. Siemens links its Sinumerik CNC to NVIDIA Omniverse, enabling machine-tool builders to fine-tune 5-axis paths in a virtual twin and reduce commissioning time by up to 6 months.[3]Siemens AG, “NVIDIA Omniverse Partnership,” siemens.com A single IPC can replace multiple racks, lowering hardware outlay by up to 30%. TwinCAT 3 turns off-the-shelf x86 hardware into sub-250-microsecond controllers, a draw for European OEMs that scale from single-axis labelers to complex rotary fillers.

Expansion of Compact Standalone Controllers for OEMs

Embedded controllers smaller than 100 cubic centimeters pack servo drives, motion processors, and I/O while consuming under 15 watts. Omron’s Sysmac NX7, launched in 2024, folds EtherCAT master, SIL 3 safety logic, and multi-axis control into a DIN-rail form-factor 40% cheaper than rack systems. ARM and RISC-V chips enable 1 kilohertz S-curve trajectories, allowing battery-powered mobile robots to operate continuously for an 8-hour shift. Medical device makers favor the compact design because fewer software modules simplify FDA and CE validation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Integration Costs for Brownfield Retrofits | -1.2% | North America and Europe legacy plants, moderate impact in Asia Pacific | Medium term (2-4 years) |

| Cybersecurity Vulnerabilities in Open Ethernet Networks | -0.9% | Critical infrastructure across all regions | Short term (≤ 2 years) |

| Shortage of Skilled Motion Engineers in Emerging Economies | -0.7% | India, Vietnam, Indonesia, South Africa, Kenya, Egypt, Brazil, Mexico | Long term (≥ 4 years) |

| Semiconductor Supply Instability for DSP and FPGA Chips | -0.6% | Global, with supply concentration in Taiwan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Integration Costs for Brownfield Retrofits

Retrofits often require USD 50,000-150,000 per machine because engineers must bridge analog 4-20 mA loops to EtherCAT via USD 2,000-5,000 gateways and compress installation into 72-hour shutdowns. Retraining technicians on IEC 61131-3 languages adds USD 10,000-20,000 per employee. SMEs in Europe and North America often postpone upgrades when the payback period stretches to five years, despite long-term energy and throughput gains. Digital twins could de-risk projects, yet most legacy sites lack accurate CAD models, forcing costly reverse engineering.

Cybersecurity Vulnerabilities in Open Ethernet Networks

Operational technology attacks increased by 75% in 2024, exploiting flaws in ThinManager, SIMATIC, and TwinCAT stacks that enable remote code execution. EtherCAT’s open Ethernet layer lacks mandatory authentication, so firms must add segmentation, intrusion detection, and encrypted tunnels, which can increase project costs by as much as USD 100,000. High-profile ransomware incidents at automotive and semiconductor plants caused losses above USD 50 million per event. IEC 62443 compliance requires secure boot and role-based access, yet 60% of installed controllers predate these features, leaving large swaths of equipment vulnerable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Embedded Controllers Extend OEM Flexibility

Standalone embedded units expanded at a 9.23% CAGR through 2030, as cobot, benchtop CNC, and AGV builders chose integrated designs that deliver sub-50-millisecond cycles in under-15-watt envelopes. PLC-based devices retained 39.78% of GMC based motion controller market share in 2024, as brownfield facilities prefer familiar ladder logic. PC-based platforms appeal to high-tech manufacturers who consolidate vision, analytics, and motion on x86 hardware, reducing the component count by 30%. Modular racks remain in glass coating and multi-spindle lathes, where scaling from 8 to 64 axes in one chassis offsets the higher cost.

The shift toward containerized motion, where Docker orchestrates real-time tasks on industrial PCs, hints at future over-the-air updates without downtime. Food and beverage lines still favor stainless steel PLC enclosures rated IP69K, whereas medical pipetting systems often employ embedded controllers to streamline CE documentation. Across all categories, compliance with IEC 61131-3 ensures program portability; however, vendor-specific motion extensions can preserve switching costs.

By Axis Count: Complex Robotics Lifts High-Axis Demand

Controllers with 10 axes or more advance at a 9.17% CAGR, as wafer handlers, battery assembly gantries, and composite layup machines coordinate 12-32 servos in nanometer precision regimes. The 3-5 axis bracket, accounting for 36.54% of 2024 revenue, remains prevalent in pick-and-place, CNC milling, and cartoners, where the cost per axis drives decisions. Six- to ten-axis devices power collaborative robots in electronics and machine tending, while one- to two-axis units occupy conveyors and index tables.

EtherCAT dominates high-axis projects because distributed clocks maintain jitter below 1 microsecond across 100 meters, an envelope that Profinet IRT cannot meet at a similar cost. Beckhoff’s planar motor platform orchestrates 256 movers, enabling over 300 wafers to be processed per hour, demonstrating scalability. Automotive battery lines transition from mechanical linkages to electronic camming for 8-axis welders, enabling 10-minute format changes versus the two hours required with shafts.

By Network Communication Protocol: EtherCAT Maintains the Lead

EtherCAT commanded a 43.91% share in 2024 and is projected to grow at a 9.41% CAGR, underpinned by on-the-fly processing that delivers sub-microsecond determinism for 32-axis systems. Profinet retains Siemens-centric users in the automotive and process industries, offering 31.25-microsecond cycles, but at 30-50% higher network hardware costs. EtherNet/IP dominates legacy North American PLC estates; however, millisecond-level determinism curtails precision motion applications. SERCOS III loses ground as suppliers ship dual-stack drives and OEMs consolidate on EtherCAT to cut inventory.

TSN-ready EtherCAT G permits motion, vision, and sensor traffic over a single cable, while SIL 3 Fail-Safe over EtherCAT removes hard-wired safety circuits, reducing panel wiring by 40%. Smaller protocols such as CC-Link IE TSN and POWERLINK address regional niches but lack the 7,200 certified devices and 6,900 member companies that sustain EtherCAT’s ecosystem.

By End-Use Industry: Semiconductor Equipment Sets the Pace

Semiconductor and electronics machinery is expected to grow at a 9.59% CAGR to 2030, as wafer stages now require nanometer positioning at throughputs exceeding 300 wafers per hour, which can only be achieved with EtherCAT-synchronized piezo drives. Robotics and automation applications accounted for 28.66% of 2024 demand, driven by China’s 276,000 robot installations and India’s 59% surge in deployments. Packaging lines exploit electronic line-shafts for 10-minute changeovers, machine tools rely on spline interpolation at 4 kilohertz, and printing presses drive 1,500-meter-per-minute webs with ±0.5 newton tension control.

Pharmaceutical filling lines reach 400 vials per minute and require auditable motion profiles to satisfy FDA PAT guidance. Food processors demand IP69K stainless controllers for wash-down but lag in growth. Textile, woodworking, and material-handling firms are adopting electric servos to replace pneumatics, achieving 30-50% energy savings and lower maintenance costs.

Geography Analysis

The Asia Pacific region accounted for 42.89% of 2024 revenue, driven by China’s 276,000 annual robot installations, India’s subsidy-driven electronics push, and Korea’s 932 robots per 10,000 workers. Regional incentives waive import duties and grant R and D tax credits, prompting Delta, Schneider, and Inovance to add domestic motion-controller lines. Vietnam’s contract-manufacturing hubs demand four-week lead times that distant suppliers struggle to match. Australia’s autonomous haul trucks rely on motion-controlled electric drives, which reduce diesel consumption by 35%.

Africa is projected to post a 9.47% CAGR through 2030, as Angola, Kenya, and South Africa automate their mines, ports, and energy sites. Service centers opened in Johannesburg and Nairobi support multi-kilometer conveyor synchronization that reduces energy consumption by 20%. Suez Canal modernization utilizes gantry cranes to position containers within 10 millimeters, thereby shortening vessel dwell time.

North America and Europe grow below the global mean, yet they offer high absolute opportunities through reshoring and labor scarcity. Yaskawa’s USD 200 million Ohio expansion aligns with USMCA content rules, while EU safety mandates favor incumbents with SIL 3 certificates. Middle East free zones lure vendors with 10-year tax holidays, while South America sees a selective uptake in Brazilian automotive and Argentine agricultural sectors amid currency fluctuations.

Competitive Landscape

The top five suppliers, ABB, Siemens, Rockwell Automation, Mitsubishi Electric, and Bosch Rexroth, held a combined share of 45-50% in 2024, indicating moderate market concentration. ABB and Schneider formed an edge-to-cloud analytics alliance in September 2025 to predict servo bearing failures weeks in advance, thereby reducing unplanned downtime.

Rockwell partnered with NVIDIA to integrate Jetson Orin AI into mobile-robot controllers, reducing path-planning latency to 50 milliseconds. Yaskawa earmarked USD 200 million to boost Ohio manufacturing and satisfy reshoring orders tied to local-content rules.

Smaller firms such as Trio Motion Technology, Galil, and ACS win medical and scientific OEMs by offering open C++ or Python APIs. Siemens links Sinumerik to Omniverse for digital twins, compressing tool-builder projects by six months. Cloud-delivered firmware, license-key feature unlocks, and OT cybersecurity tie-ins reshape competition; suppliers lacking IT partnerships risk obsolescence as software-defined motion gains traction.

GMC Based Motion Controller Industry Leaders

ABB Ltd.

Mitsubishi Electric Corporation

Siemens AG

Rockwell Automation, Inc.

Bosch Rexroth AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ABB and Schneider Electric formed a strategic alliance to build an edge-to-cloud motion-analytics platform that captures servo-drive data, uses machine-learning models to predict bearing failures two to four weeks ahead, and schedules maintenance automatically—an approach aimed at pharmaceutical and food-processing plants where every hour of unplanned downtime can cost more than USD 50,000.

- July 2025: Siemens AG confirmed it will finalize the acquisition of ebm-papst’s Intelligent Drive Technology division, a move that adds integrated motor-drive solutions for HVAC, refrigeration, and industrial-ventilation systems to Siemens’ lineup and bolsters its position in energy-efficient motion control; financial terms were not disclosed.

- March 2025: Beckhoff posted EUR 1.17 billion (USD 1.29 billion) sales despite semiconductor downturn, while investing EUR 80 million in R and D.

Global GMC Based Motion Controller Market Report Scope

The GMC Based Motion Controller Market Report is Segmented by Product Type (PLC-Based Motion Controllers, PC-Based Motion Controllers, Standalone Embedded Controllers, Modular Rack-Mount Controllers), Axis Count (1-2 Axis, 3-5 Axis, 6-10 Axis, Above 10 Axis), Network Communication Protocol (EtherCAT, Profinet, Ethernet/IP, SERCOS III, Other Network Communication Protocol), End-Use Industry (Packaging Machinery, Semiconductor and Electronics Equipment, Robotics and Automation, Machine Tools, Printing and Paper, Other End-Use Industry), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| PLC-Based Motion Controllers |

| PC-Based Motion Controllers |

| Standalone Embedded Controllers |

| Modular Rack-Mount Controllers |

| 1-2 Axis |

| 3-5 Axis |

| 6-10 Axis |

| Above 10 Axis |

| EtherCAT |

| Profinet |

| Ethernet/IP |

| SERCOS III |

| Other Network Communication Protocol |

| Packaging Machinery |

| Semiconductor and Electronics Equipment |

| Robotics and Automation |

| Machine Tools |

| Printing and Paper |

| Other End-Use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | PLC-Based Motion Controllers | ||

| PC-Based Motion Controllers | |||

| Standalone Embedded Controllers | |||

| Modular Rack-Mount Controllers | |||

| By Axis Count | 1-2 Axis | ||

| 3-5 Axis | |||

| 6-10 Axis | |||

| Above 10 Axis | |||

| By Network Communication Protocol | EtherCAT | ||

| Profinet | |||

| Ethernet/IP | |||

| SERCOS III | |||

| Other Network Communication Protocol | |||

| By End-Use Industry | Packaging Machinery | ||

| Semiconductor and Electronics Equipment | |||

| Robotics and Automation | |||

| Machine Tools | |||

| Printing and Paper | |||

| Other End-Use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How fast is the GMC based motion controller market expected to grow to 2030?

Revenue is forecast to rise from USD 1.19 billion in 2025 to USD 1.79 billion by 2030, reflecting an 8.41% CAGR.

Which network protocol is gaining the most share in motion control applications?

EtherCAT leads with 43.91% share in 2024 and is forecast to grow at a 9.41% CAGR as multi-axis systems demand sub-microsecond determinism.

What segment shows the quickest growth by product type?

Standalone embedded controllers expand at 9.23% CAGR thanks to compact cobots, mobile robots, and benchtop CNC machines.

Why are semiconductor equipment builders driving demand?

Wafer-handling stages now require nanometer positioning at throughputs above 300 wafers per hour, achievable only with EtherCAT-synchronized motion platforms.

Which region is the fastest growing for motion controllers?

Africa leads with a 9.47% CAGR to 2030 as mining, port, and energy projects adopt modular controller platforms.

What is the primary restraint holding back retrofit projects?

High initial integration costs—USD 50,000-150,000 per machine—extend payback periods to up to five years, delaying upgrades in older plants.

Page last updated on: