GM2 Gangliosidosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

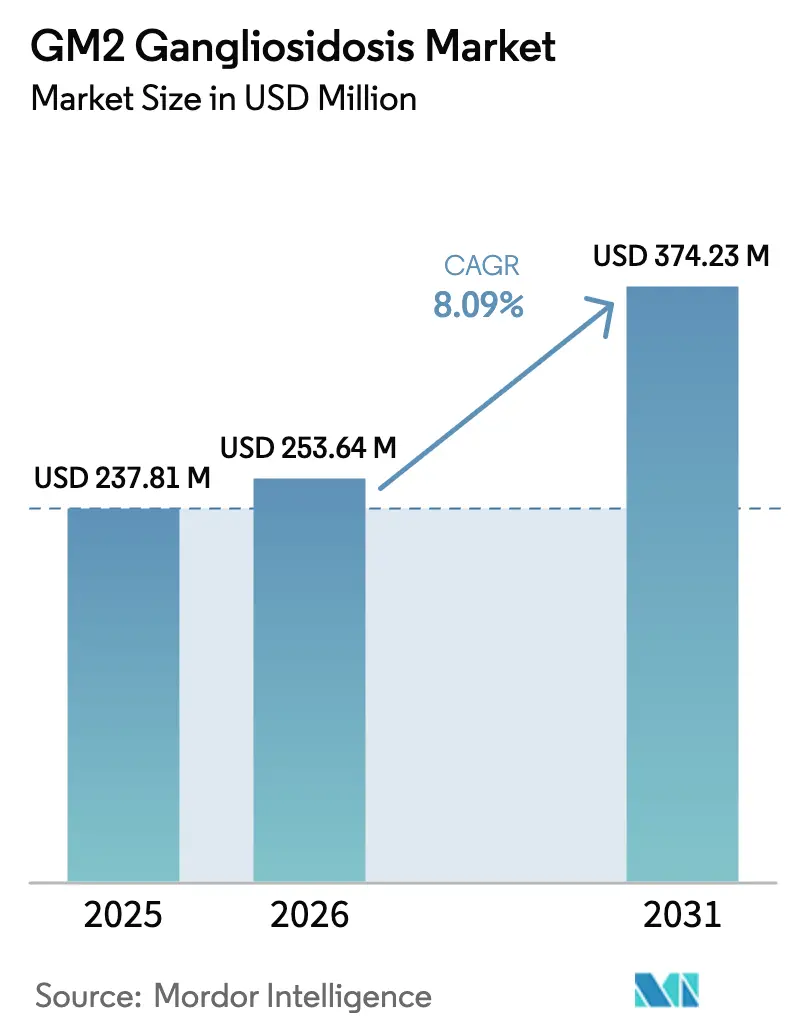

| Market Size (2026) | USD 253.64 Million |

| Market Size (2031) | USD 374.23 Million |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

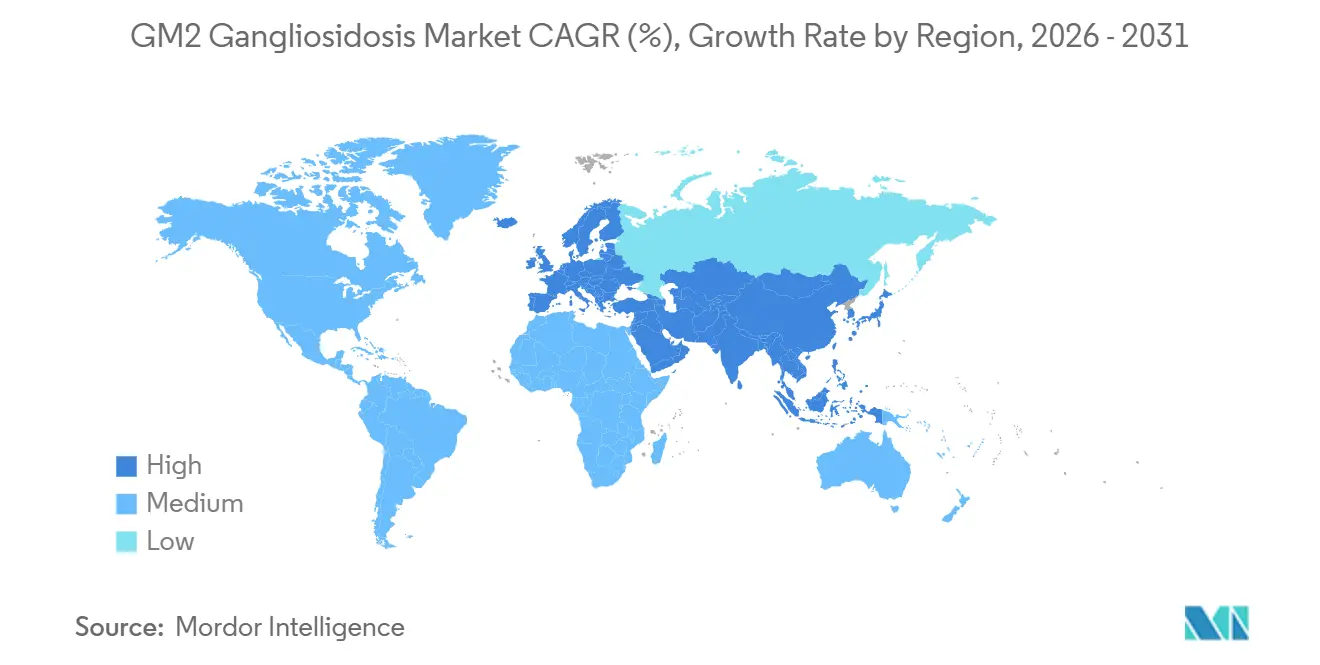

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

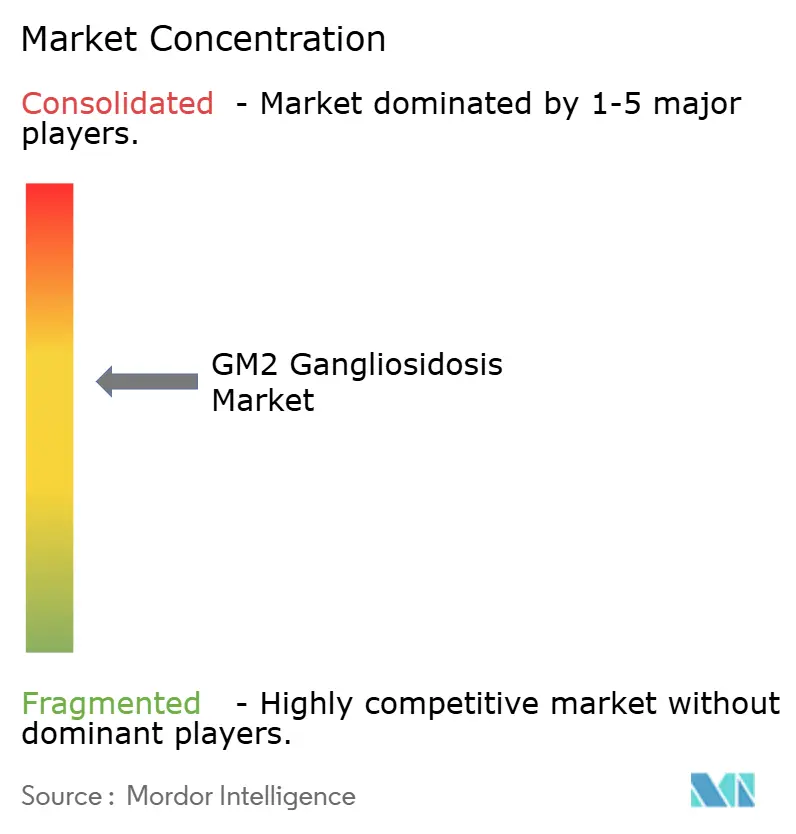

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GM2 Gangliosidosis Market Analysis by Mordor Intelligence

GM2 Gangliosidosis Market size in 2026 is estimated at USD 253.64 million, growing from 2025 value of USD 237.81 million with projections showing USD 374.23 million, growing at 8.09% CAGR over 2026-2031.

Three forces underpin this trajectory: rapid innovation in blood-brain-barrier-penetrant gene-therapy vectors, regulatory pathways that compress approval timelines for ultra-rare lysosomal diseases, and newborn-screening mandates that move diagnosis into the presymptomatic window. Gene therapy already accounts for 54.13% of therapeutic revenue in 2025, yet oral pharmacological chaperones are on an accelerated path because they avoid the high-dose manufacturing burden of viral vectors. Clinical data from a 2025 bilateral-thalamic plus cerebrospinal-fluid infusion study confirmed dose-dependent enzyme restoration, although immune management remains essential to sustain efficacy.[1]Xue-Li Chen, “Phase 1/2 Dual-Vector rAAVrh8 Trial for GM2 Gangliosidosis,” Nature Medicine, nature.com New investments in high-titer manufacturing, priority-review vouchers, and early-access schemes together broaden the commercial runway for the GM2 gangliosidosis market while white-space opportunities in substrate-reduction therapy invite additional entrants.[2]Peter Marks, “Rare Pediatric Disease Priority Review Voucher Program,” U.S. Food and Drug Administration, fda.gov

Key Report Takeaways

- By therapeutic modality, gene therapy led with 54.13% of the GM2 gangliosidosis market share in 2025, while pharmacological chaperone therapy is forecast to expand at an 11.46% CAGR through 2031.

- By disease type, Tay-Sachs disease accounted for 61.67% of revenue in 2025, whereas the AB-variant subtype is projected to grow at an 11.84% CAGR to 2031.

- By delivery route, intrathecal administration captured 47.26% of the GM2 gangliosidosis market share in 2025, and intracerebral delivery is advancing at a 12.24% CAGR through 2031.

- By end user, hospitals held 52.66% of GM2 gangliosidosis market share in 2025, while research and academic institutes record the fastest growth at a 10.63% CAGR through 2031.

- By geography, North America retained 39.53% share of the GM2 gangliosidosis market in 2025, and Asia-Pacific is forecast to post the highest regional growth at a 10.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GM2 Gangliosidosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in gene-therapy vectors | +2.1% | Global | Medium term (2-4 years) |

| Orphan-drug incentives and priority-review vouchers | +1.3% | North America, EU5, Japan | Short term (≤ 2 years) |

| Growing newborn-screening mandates | +1.5% | North America, selected EU, Australia | Long term (≥ 4 years) |

| CRISPR-edited HSC ex-vivo programs | +0.9% | North America, EU5 | Long term (≥ 4 years) |

| Cross-border early-access schemes | +0.7% | EU5 | Short term (≤ 2 years) |

| BBB-penetrant substrate-reduction small molecules | +1.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancements in Gene-Therapy Vectors Targeting GM2 Gangliosidosis

Bicistronic AAV9 constructs that deliver both HEXA and HEXB extended Sandhoff-mouse survival from four to eighteen months, normalizing motor scores and curbing GM2 accumulation across cortex and cerebellum.[3]Andrés F. Leal, “GM2 Gangliosidoses: Clinical Features, Pathophysiological Aspects, and Current Therapies,” International Journal of Molecular Sciences, mdpi.com JCR Pharmaceuticals advanced JR-479, a transferrin-receptor-targeted recombinant β-hexosaminidase A that balances central-nervous-system uptake with systemic distribution, reducing infusion reactions in preclinical models. A 2025 Phase 1/2 dual-vector rAAVrh8 trial delivered vectors via bilateral thalamic injection plus cerebrospinal-fluid infusion and restored up to 80% of wild-type enzyme activity in target regions, although transient pleocytosis required corticosteroid and rituximab prophylaxis. NIH scientists reported adenine base editing of the HEXA c.533G>A mutation with minimal off-target edits, paving the way for precision therapies that avoid double-strand breaks. Collectively, these advances shorten translation cycles and add 2.1 percentage points to forecast growth of the GM2 gangliosidosis market.

Orphan-Drug Incentives and Priority-Review Vouchers

Between 2020 and 2025 the FDA granted multiple orphan designations for GM2-targeting therapies, conferring seven-year exclusivity, clinical-trial tax credits, and PDUFA fee waivers that reduce late-stage trial costs by roughly 30%. Rare Pediatric Disease vouchers, resold for USD 80–110 million, offset capital outlays and draw venture investment. EMA’s PRIME and Japan’s SAKIGAKE programs deliver enhanced scientific advice and shorter assessment windows, moving commercial launch forward by two to eighteen months. These combined levers add 1.3 percentage points to CAGR by derisking the GM2 gangliosidosis market.

Growing Newborn-Screening Mandates for Lysosomal Disorders

HRSA added two lysosomal storage disorders to the Recommended Uniform Screening Panel in 2025, signaling that GM2 screening could follow within four years. CDC molecular-assessment teams are training state laboratories on tandem-mass-spectrometry and sequencing workflows, scaling technical readiness. Early detection moves therapy into the presymptomatic phase, with preclinical data showing four-fold survival extension when gene therapy is administered within the first three months of life. Australia’s statewide panels for Pompe and Fabry diseases prove operational feasibility and payer acceptance, reinforcing the 1.5-percentage-point lift to CAGR.

CRISPR-Edited HSC Ex-Vivo Programs Entering the IND Phase

FDA approval of Lenmeldy in 2024 validated autologous lentiviral correction for lysosomal diseases and set reimbursement benchmarks for future ex-vivo approaches. Base-editing platforms reached 43% correction efficiency for HEXA c.533G>A in patient fibroblasts with indel rates below 2%. Ex-vivo workflows avoid pre-existing anti-AAV antibodies, yet manufacturing remains patient-specific, costs exceed USD 500,000 per slot, and throughput averages eighty patients yearly per site. These factors still contribute 0.9 percentage points to CAGR by widening the therapeutic toolbox in the GM2 gangliosidosis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-low prevalence limiting commercial ROI | –1.8% | Global | Long term (≥ 4 years) |

| High cost and complexity of CNS gene-vector delivery | –1.2% | Global | Medium term (2-4 years) |

| Manufacturing bottlenecks for high-titer AAV serotypes | –0.9% | North America, EU5 | Short term (≤ 2 years) |

| Regulatory uncertainty around in-vivo gene editing | –0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-Low Prevalence Limiting Commercial ROI

Infantile Tay–Sachs incidence is roughly 1 per 100,000 U.S. births, translating to fewer than forty new cases each year. Even at a USD 2.1 million one-time price, annual revenue peaks near USD 100 million against development outlays of USD 1.5–2.0 billion, depressing internal rates of return and steering capital to larger rare-disease segments. The constraint removes 1.8 percentage points from projected CAGR for the GM2 gangliosidosis market.

High Cost and Complexity of CNS Gene-Vector Delivery

Intrathecal infusion requires specialized neurosurgical facilities, lumbar puncture or Ommaya reservoir placement, and immunosuppression costing USD 30–40 thousand per patient in drugs alone. Intracerebral stereotactic delivery adds device and operating-room charges of USD 200 thousand and lengthens procedure times to six hours. These hurdles shave 1.2 percentage points from growth because only a few centers can deliver therapy at scale in the GM2 gangliosidosis market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Modality: Gene Therapy Holds Lead, Chaperones Acceler

Gene therapy generated 54.13% of GM2 gangliosidosis market share in 2025, reflecting the first-mover status of intrathecal AAV9 programs and validated reimbursement precedents. The GM2 gangliosidosis market size contribution from pharmacological chaperones is smaller but rises fastest at an 11.46% CAGR because non-inhibitory molecules like NCGC326 combine blood-brain-barrier penetration with oral convenience. Enzyme replacement faces diffusion limits yet J-Brain Cargo fusions may close that gap, while substrate-reduction agents such as miglustat act as adjuncts for patients unable to receive viral vectors.

Stem-cell transplant remains investigational; ex-vivo lentiviral correction improved Sandhoff-mouse survival but shows variable engraftment in humans. Strategic pairing of one-time gene therapy with chronic oral maintenance is likely to define future modality mix as the GM2 gangliosidosis market matures.

By Disease Type: Tay-Sachs Dominates, AB Variant Gains Momentum

Tay-Sachs disease accounted for 61.67% of revenue in 2025 due to concentrated prevalence in Ashkenazi Jewish populations and established carrier-testing programs. Sandhoff disease follows, complicated by peripheral organ involvement. AB-variant GM2 gangliosidosis grows at 11.84% CAGR as next-generation sequencing reclassifies cases once labeled atypical Tay-Sachs.

Precision medicine advances, from HEXA base editing to GM2A gene addition, align with these subtype needs. As newborn panels broaden, the GM2 gangliosidosis market size mix is expected to tilt toward earlier-onset forms, lifting demand for therapies that benefit most from presymptomatic administration.

By Delivery Route: Intrathecal Still Leads, Intracerebral Surges

Intrathecal infusion retained 47.26% of GM2 gangliosidosis market size in 2025 because pediatric neurologists favor lumbar access and Ommaya reservoirs. Intracerebral administration grows at 12.24% CAGR, propelled by thalamic-delivery data that reached 80% wild-type enzyme levels in targeted tissue.

Intravenous Trojan-horse fusion proteins may widen access if human trials confirm the 20-fold uptake seen in primates, while oral delivery stays confined to substrate-reduction and chaperone regimens. Hybrid approaches blending thalamic injection with cerebrospinal-fluid infusion aim to balance distribution and dose economy as the GM2 gangliosidosis market evolves.

By End User: Academic Institutes Outpace Hospitals

Hospitals held 52.66% of GM2 gangliosidosis market share in 2025 because symptomatic patients need multidisciplinary support. Research and academic institutes grow at 10.63% CAGR as they double as trial centers and vector-manufacturing hubs, aided by CMS payment codes that reimburse outpatient gene-therapy administration at average sales price plus 6%.

Specialty clinics handle chronic oral regimens but lack neurosurgical capacity, while home-care adoption will rise once subcutaneous enzyme formats mature. Concentration of manufacturing and follow-up at academic sites will therefore continue, reshaping care delivery in the GM2 gangliosidosis market.

Geography Analysis

North America generated 39.53% of GM2 gangliosidosis market revenue in 2025. U.S. academic centers run the majority of gene-therapy trials, and separate CMS payment codes encourage hospitals to add clean-room capacity. HRSA’s evolving newborn-screening list could raise diagnosed cases by 60% within four years and further enlarge the GM2 gangliosidosis market.

Europe ranked second. France, Germany, and the United Kingdom each employ early-access schemes that shorten the gap between Phase 2 readouts and real-world use. Statutory insurers have reimbursed investigational therapies under compassionate provisions, an approach that accelerates revenue capture.

Asia-Pacific posts the fastest CAGR at 10.02% through 2031. Japan’s SAKIGAKE pathway and South Korea’s outcomes-based reimbursement agreements lower entry barriers, while China’s 2024 gene-therapy guidelines and earlier approvals of Zolgensma and Hemgenix confirm regulatory momentum. Australia’s statewide lysosomal panels validate operational roll-out, and India’s nascent centers of excellence set the stage for future clinical participation.

Middle East & Africa and South America remain the smallest contributors because of limited neurosurgical infrastructure and reimbursement constraints that cap therapy prices below USD 500,000. Cross-border referral to North America or Europe continues until domestic capacity matures, leaving substantial white space for the GM2 gangliosidosis market in these regions.

Competitive Landscape

The GM2 gangliosidosis market is moderately concentrated with eighteen profiled companies. Multinationals like Novartis and BioMarin operate end-to-end plants, while asset-light innovators outsource vector supply to CDMOs such as Lonza and Catalent. The October 2024 USD 1.5 billion acquisition of Poseida by Roche underscores big-pharma appetite for non-viral platforms that can expand rare-disease franchises.

Vector-engineering races center on novel AAV9 capsids, serotypes like AAV-DJ, and lipid nanoparticles that evade pre-existing antibodies and permit repeat dosing. Regulatory precedents, notably the March 2024 Lenmeldy approval, favor ex-vivo approaches with defined guidance, while in-vivo editing faces long follow-up obligations.

Strategic licensing, long-term manufacturing deals, and priority-review-voucher monetization shape funding flows. As dosing moves earlier in life and payer models mature, companies that combine scalable production with precision genomic tools are positioned to gain share in the GM2 gangliosidosis market.

GM2 Gangliosidosis Industry Leaders

Sio Gene Therapies

Taysha Gene Therapies

REGENXBIO

Passage Bio

Neurogene Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: NIH researchers applied adenine base editing to correct the HEXA c.533G>A mutation in patient-derived fibroblasts, achieving high on-target efficiency with minimal indels

- November 2024: Roche acquired Poseida Therapeutics for USD 1.5 billion, adding non-viral delivery and CAR-T manufacturing expertise relevant to ex-vivo correction programs

- March 2024: FDA approved Lenmeldy, an autologous lentiviral stem-cell gene therapy for metachromatic leukodystrophy, validating ex-vivo workflows for lysosomal indications

Global GM2 Gangliosidosis Market Report Scope

GM2 gangliosidosis, a rare and fatal disorder, arises from an autosomal recessive metabolic anomaly. At its core is a deficiency of the enzyme beta-hexosaminidase. This shortfall results in a toxic buildup of GM2 ganglioside within neurons, progressively damaging nerve cells in both the brain and spinal cord.

The GM2 Gangliosidosis Market Report is segmented by Therapeutic Modality, Disease Type, Delivery Route, End User, and Geography. By Therapeutic Modality, the market is segmented into Gene Therapy, Enzyme Replacement Therapy, Substrate-Reduction Therapy, Pharmacological Chaperone Therapy, and Stem-Cell Transplant. By Disease Type, the market is segmented into Tay-Sachs Disease, Sandhoff Disease, and AB Variant GM2. By Delivery Route, the market is segmented into Intrathecal, Intravenous, Intracerebral, and Oral. By End User, the market is segmented into Hospitals, Specialty Clinics, Research & Academic Institutes, and Home-Care Settings. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Gene Therapy |

| Enzyme Replacement Therapy |

| Substrate-Reduction Therapy |

| Pharmacological Chaperone Therapy |

| Stem-Cell Transplant |

| Tay-Sachs Disease |

| Sandhoff Disease |

| AB Variant GM2 |

| Intrathecal |

| Intravenous |

| Intracerebral |

| Oral |

| Hospitals |

| Specialty Clinics |

| Research & Academic Institutes |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Modality | Gene Therapy | |

| Enzyme Replacement Therapy | ||

| Substrate-Reduction Therapy | ||

| Pharmacological Chaperone Therapy | ||

| Stem-Cell Transplant | ||

| By Disease Type | Tay-Sachs Disease | |

| Sandhoff Disease | ||

| AB Variant GM2 | ||

| By Delivery Route | Intrathecal | |

| Intravenous | ||

| Intracerebral | ||

| Oral | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Research & Academic Institutes | ||

| Home-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What revenue level is expected for GM2 gangliosidosis therapies by 2031?

The GM2 gangliosidosis market size is projected to reach USD 374.23 million by 2031.

Which treatment class currently leads spending?

Gene therapy accounts for 54.13% of 2025 sales in the GM2 gangliosidosis market.

Which modality grows fastest through 2031?

Pharmacological chaperones expand at an 11.46% CAGR, the highest among all modalities.

Why does Asia-Pacific outpace other regions?

Japan’s SAKIGAKE pathway and China’s 2024 gene-therapy guidelines accelerate approvals, driving a 10.02% CAGR.

What remains the biggest restraint on growth?

Ultra-low prevalence limits commercial return, reducing forecast CAGR by 1.8 percentage points.

Page last updated on: