GM1 Gangliosidosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

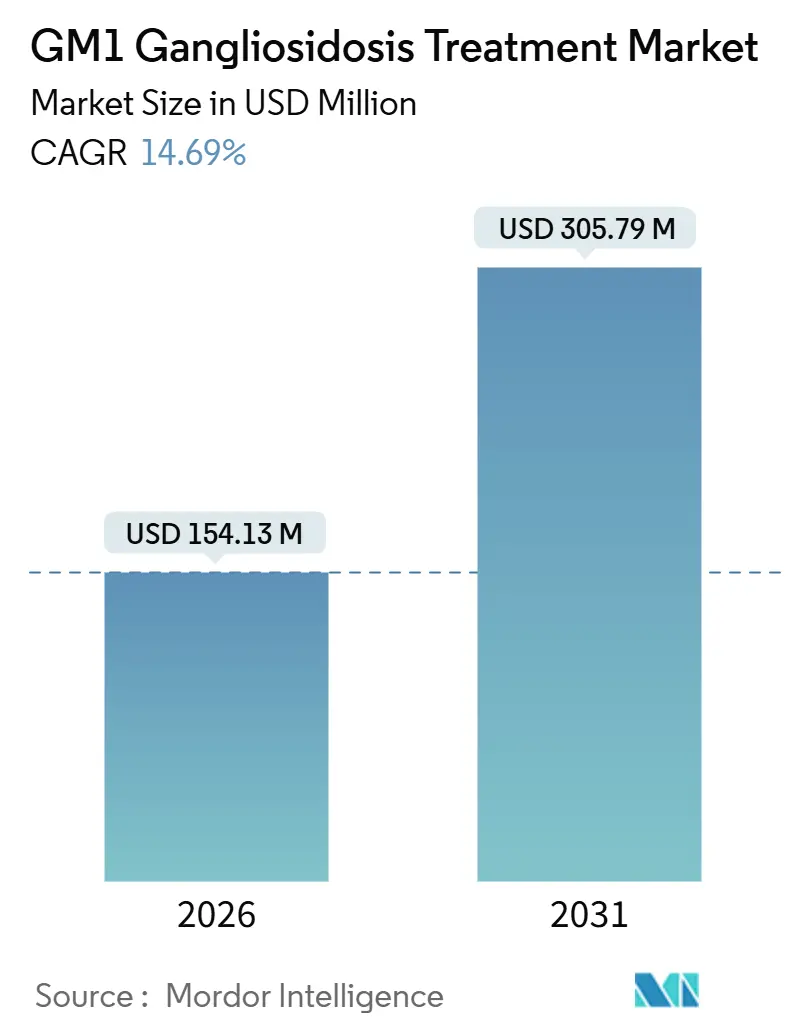

| Market Size (2026) | USD 154.13 Million |

| Market Size (2031) | USD 305.79 Million |

| Growth Rate (2026 - 2031) | 14.69% CAGR |

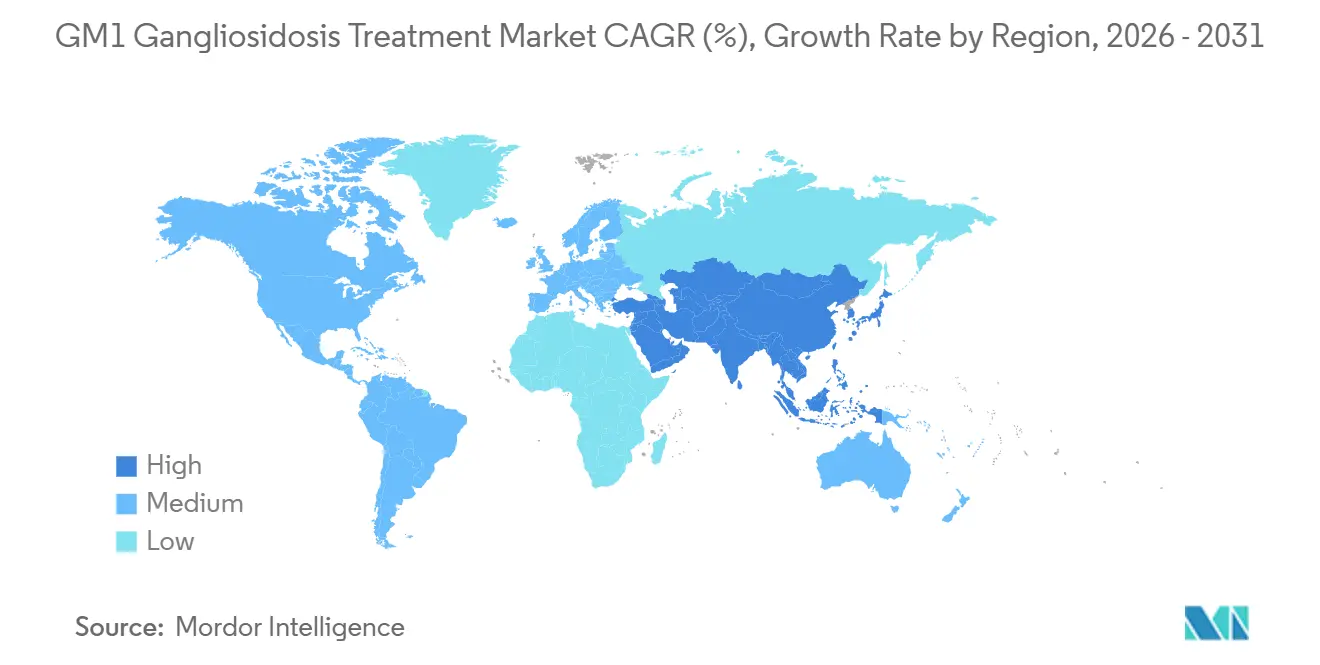

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GM1 Gangliosidosis Treatment Market Analysis by Mordor Intelligence

The GM1 Gangliosidosis Treatment Market size is estimated at USD 154.13 million in 2026, and is expected to reach USD 305.79 million by 2031, at a CAGR of 14.69% during the forecast period (2026-2031).

The growth trajectory aligns with pivotal advances in adeno-associated virus serotype 9 and AAVhu68 gene-therapy constructs that have delivered early reductions in cerebrospinal fluid GM1 ganglioside levels, while synchronized orphan-drug incentives across the United States, European Union, Japan, and China shorten development timelines and de-risk capital deployment. Newborn-screening pilots that integrate lysosomal-enzyme panels now detect presymptomatic cases, moving gene therapy into a prophylactic role that promises improved functional outcomes. In parallel, pharmacological-chaperone cocktails tailored to GLB1 missense mutations provide a genotype-specific alternative that sidesteps vector immunogenicity and can be administered orally. Investors are responding to this convergence of clinical validation and policy support, channeling record venture and grant funding into ultra-rare central nervous system programs, thereby accelerating trial activation and broadening the competitive field.

Key Report Takeaways

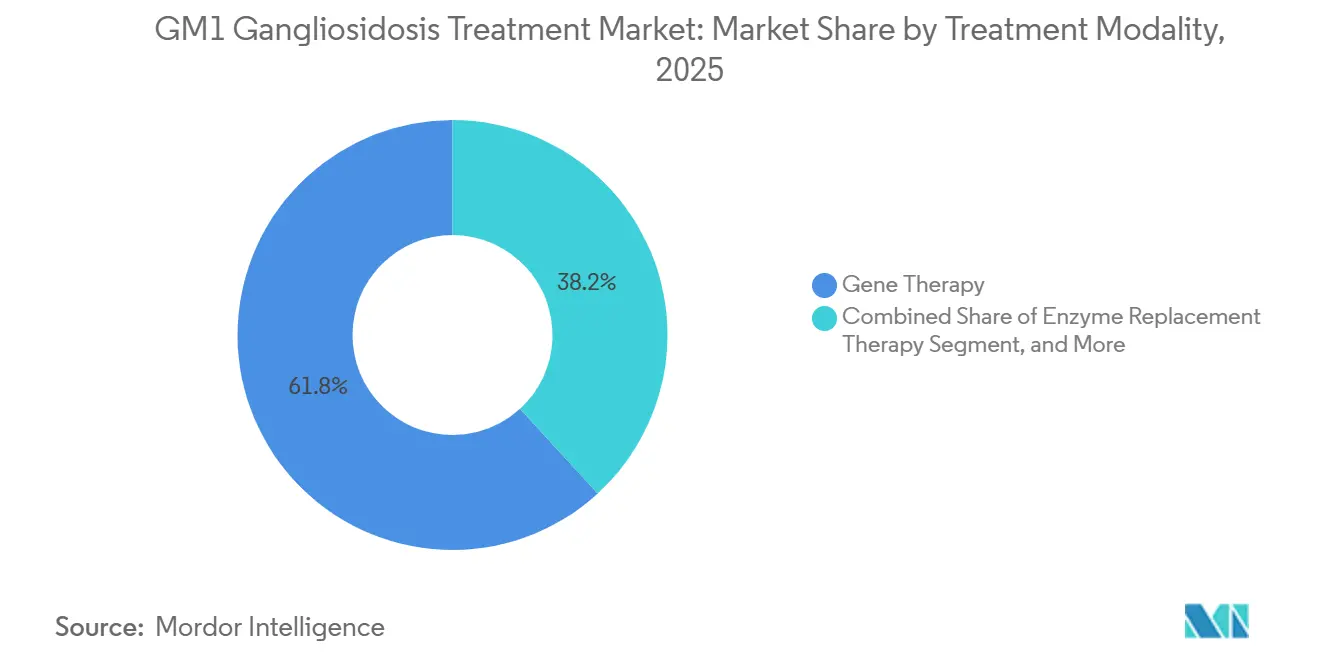

- By treatment modality, gene therapy held 61.81% of the GM1 gangliosidosis treatment market share in 2024, while enzyme-replacement therapy is projected to post the fastest 16.37% CAGR through 2031, led by blood-brain-barrier shuttle platforms.

- By clinical type, Type I infantile disease accounted for 48.57% of revenue in 2024; Type II juvenile cases are on track for a 17.98% CAGR through 2031.

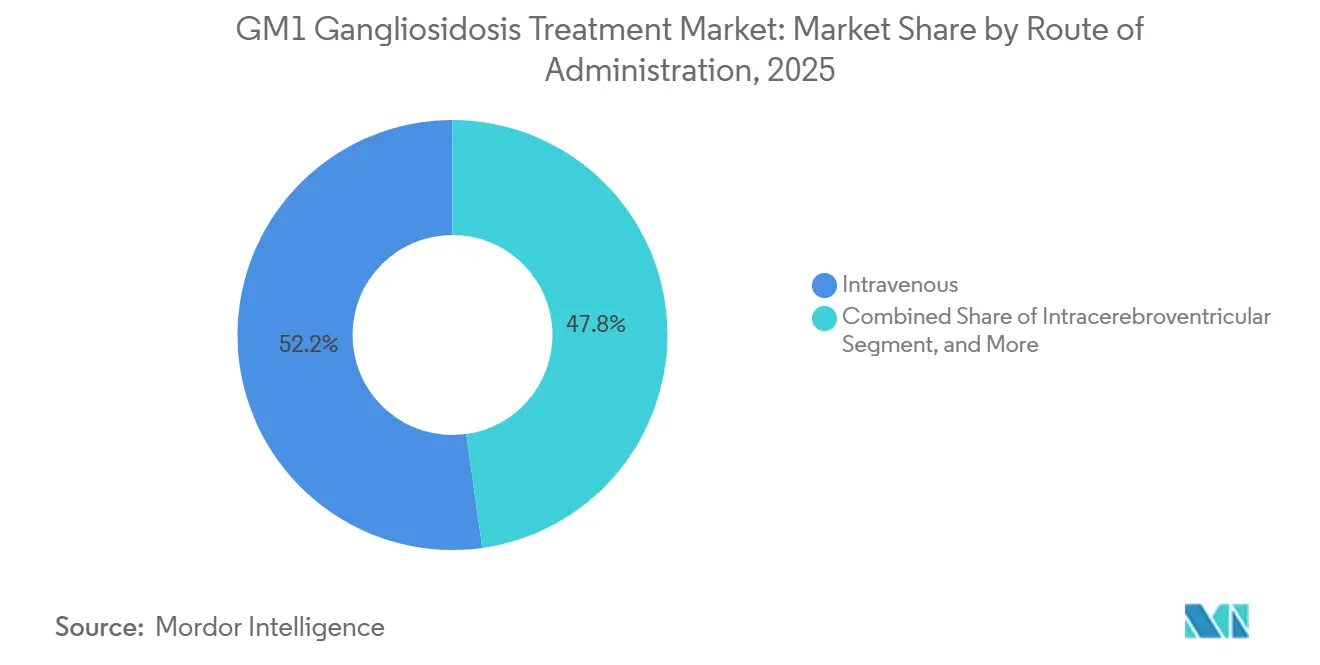

- By administration route, intravenous delivery accounted for 52.22% of procedures in 2024, but intrathecal and intracisternal approaches are poised for a 15.19% CAGR.

- By end-user, hospitals retained a 41.93% share in 2024, whereas specialty clinics and centers are forecast to expand at a 19.12% CAGR through 2031.

- By geography, North America contributed 42.03% of 2024 revenue; Asia-Pacific is expected to lead growth with an 18.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GM1 Gangliosidosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Newborn-Screening Adoption | +2.8% | North America (ScreenPlus NYC pilot), Europe (expanding panels), Asia-Pacific (China provincial pilots) | Medium term (2-4 years) |

| Clinical-Stage AAV9 And AAVhu68 Gene-Therapy Breakthroughs | +4.1% | Global, with trial concentration in United States, France, United Kingdom | Short term (≤ 2 years) |

| Orphan-Drug Incentives & Priority-Review Vouchers | +2.3% | United States, European Union, Japan (MHLW), China (NMPA) | Short term (≤ 2 years) |

| Increasing Venture & Grant Funding for Ultra-Rare CNS Disorders | +1.9% | North America, Europe, early spillover to Asia-Pacific | Medium term (2-4 years) |

| Emergence of Β-Gal Pharmacological-Chaperone Cocktails Tailored By GLB1 Genotype | +2.1% | Global, with research hubs in Japan, United States, Europe | Long term (≥ 4 years) |

| Hospital-Based Ex Vivo HSC-Editing Point-Of-Care Platforms | +1.5% | United States (academic medical centers), Europe (specialized hematology centers) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clinical-Stage AAV9 and AAVhu68 Gene-Therapy Breakthroughs

Passage Bio’s IMAGINE-1 study of PBGM01 achieved cerebrospinal-fluid GM1-ganglioside reductions exceeding 50% alongside stabilized motor scores in infantile patients, prompting an August 2024 out-licensing to GEMMA Biotherapeutics for USD 10 million upfront plus milestones. Intravenous AAV9-GLB1 therapy from the National Human Genome Research Institute normalized plasma biomarkers and extended survival, though 2 subjects experienced transient hepatotoxicity that resolved with corticosteroids, highlighting a dose-dependent liver risk. Conversely, Lysogene’s LYS-GM101 program closed after three deaths and no functional benefit, underscoring the gulf between biochemical correction and clinical efficacy. These divergent data sets are steering the field toward earlier intervention windows, combination immunomodulation, and refined capsid engineering.

Rising Newborn-Screening Adoption

New York City’s ScreenPlus pilot, launched in 2024, delivers presymptomatic GM1 detection within the first week of life through tandem-mass-spectrometry analysis of dried blood spots.[1]ScreenPlus NYC, “Pilot Newborn Screening Program,” screenplus.nyc Natural history evidence shows that infantile patients lose half of their baseline motor capacity by 12 months, so earlier identification materially widens the therapeutic window. Japan is reviewing a nationwide expansion of lysosomal-disease screening, underpinned by an orphan-drug subsidy pool of 650 million yen that would flow to qualifying treatments. Screening economics hinge on averting lifetime institutional-care expenditures, estimated at USD 548 billion annually across rare diseases in the United States, assuming durable therapy benefits beyond five-year follow-up.

Orphan-Drug Incentives and Priority-Review Vouchers

The United States Food and Drug Administration granted orphan designation to acetylleucine in 2024, including 7-year exclusivity, fee waivers, and eligibility for tradable priority review vouchers valued at nearly USD 100 million.[2]U.S. Food and Drug Administration, “CBER Research Focus Areas: Gene Therapy,” fda.gov China’s National Medical Products Administration now accepts overseas Phase 2 data and offers six-year data protection, while India’s 2021 National Policy for Rare Diseases allocates up to Rs 20 lakh for one-time curative therapies at centers of excellence. These incentives shorten regulatory cycles yet skew corporate resource allocation toward jurisdictions with richer subsidies, potentially widening access gaps.

Emergence of β-Gal Pharmacological-Chaperone Cocktails

N-octyl-4-epi-β-valienamine and related iminosugars restored enzyme activity in 22 of 94 GLB1 missense variants, arresting neurological decline in murine models when therapy began presymptomatically. Unlike viral vectors, chaperones stabilize endogenous enzyme conformation, avoiding capsid immunogenicity. Responsiveness, however, is mutation-specific, compelling upfront genotyping that existing reimbursement frameworks rarely fund. Azafaros Bio’s Phase 3 nizubaglustat program in GM2 gangliosidosis signals cross-application potential for GM1 patients with shared sphingolipid-burden profiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sky-High One-Time Therapy Prices | -3.2% | Global, most acute in United States Medicaid, emerging in Asia-Pacific markets | Short term (≤ 2 years) |

| Limited Patient Pool Complicating Pivotal-Trial Powering | -2.1% | Global, particularly severe in regions without newborn screening | Medium term (2-4 years) |

| Rising AAV9 Capsid Immunotoxicity Scrutiny from Regulators | -1.8% | United States (FDA CBER), European Union (EMA), Japan (PMDA) | Short term (≤ 2 years) |

| Scarcity Of Validated, Age-Appropriate Neurodevelopmental Endpoints | -1.4% | Global, with regulatory guidance gaps in pediatric CNS trials | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sky-High One-Time Therapy Prices

Bluebird Bio’s LENMELDY won U.S. approval in March 2024 at USD 4.25 million, setting a benchmark that GM1 gene-therapy sponsors may track. Medicaid covers 40% of U.S. rare-disease patients yet faces actuarial hurdles in recouping such upfront costs within typical 18-month member turnover. Installment-payment models remain largely conceptual due to statutory limits on multi-year obligations. China’s reduction in the value-added tax to 3% softens import prices but not the high fixed costs of clinical-grade AAV manufacturing. India’s crowdfunding schemes introduce socioeconomic disparities that privilege patients with media visibility.

Rising AAV9 Capsid Immunotoxicity Scrutiny

A 2024 meta-analysis covering 255 AAV trials logged 11 deaths and 30 clinical holds linked to toxicity, prominently dorsal-root-ganglion degeneration.[3]Nature Reviews Drug Discovery, “Clinical Trial Toxicity Meta-analysis,” nature.com The Food and Drug Administration now mandates 15-year follow-up for gene-therapy recipients and quarterly liver-function tests in pediatric cases, adding USD 50,000 to USD 100,000 in post-marketing obligations per patient. Pre-existing AAV9 antibodies exclude more than 10% of infants, necessitating costly serology screening and reducing trial enrollment. Selecta’s ImmTOR immune-tolerance platform, licensed to Takeda for up to USD 1.124 billion, exemplifies strategies to blunt capsid T-cell responses but introduces additional regulatory layers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Gene Therapy Leads, Enzyme Replacement Accelerates

Gene therapy controlled 61.81% of the GM1 gangliosidosis treatment market in 2024, driven by confidence in single-dose AAV vectors that sustain β-galactosidase production. Enzyme replacement now advances at a 16.37% CAGR as transferrin-receptor antibody shuttles raise central-nervous-system exposure twenty-fold compared with unconjugated enzymes. Pharmacological chaperones, though nascent, appeal to payors for their oral delivery format and lower manufacturing overhead. Substrate-reduction therapy remains a supplemental option, while symptomatic management still occupies a role in late-onset adults.

The GM1 gangliosidosis treatment market continues to see limited exploration of combination regimens. Coupling transient chaperone administration with gene transfer could stabilize nascent enzyme expression during the lag to peak vector output, yet no registered trial currently evaluates this strategy. Stakeholders agree that future competitive advantage will hinge on integrating multimodal care in single protocols.

By Clinical Type: Infantile Dominance, Juvenile Momentum

Infantile Type I GM1 disease accounted for 48.57% of 2024 revenue, reflecting a severe early decline and orphan-voucher attractiveness. The GM1 gangliosidosis treatment market share for infantile disease is expected to remain above 40% through 2031 despite shrinking incidence, because therapy pricing is highest in this cohort. Juvenile Type II presentations exhibit the fastest CAGR of 17.98%, buoyed by robust natural-history data that improve endpoint selection. Adult Type III cases remain a small fraction but offer extended treatment windows.

Two-thirds of Type I patients identified via newborn screening now initiate gene therapy before six months of age in trial settings, a shift that raises ethical questions around randomization to historical controls. For Type II disease, chaperone-responsive mutations cluster among individuals with residual enzyme activity, guiding therapy selection. Adult-onset programs may benefit from oral agents that avoid the surgical burden of CNS injections.

By Administration Route: Systemic Convenience, Intrathecal Efficiency

Intravenous infusion accounted for 52.22% of the administration volume in 2024, largely due to its ease of delivery in community infusion suites. The GM1 gangliosidosis treatment market size for intrathecal and intracisternal routes is projected to grow at a 15.19% CAGR, driven by 17-fold dose-sparing benefits that reduce the manufacturing cost per patient. Yet these procedures require pediatric neurosurgical expertise available at fewer than 50 global centers, creating access bottlenecks.

Central nervous system injection risk includes serious adverse events documented in 37.5% of procedures across lysosomal-storage trials, compared with 20% for systemic approaches. Oral administration, confined to chaperone and substrate-reduction therapies, is gaining favor in adult-onset disease for its home-care compatibility, though responsiveness hinges on specific GLB1 genotypes.

By End-User: Hospitals Hold Share, Specialty Clinics Surge

Hospitals maintained a 41.93% end-user share in 2024. Specialty clinics and centers, however, are advancing at a 19.12% CAGR as payors channel patients toward certified gene-therapy centers to standardize dosing, immunomodulation, and adverse-event reporting. Research institutes capture about 15% of procedures, leveraging federal grants and multinational registries to build longitudinal data sets. Home-care models remain limited to oral therapies but may expand if remote monitoring proves reliable.

The reimbursement ecosystem shapes end-user dynamics. U.S. hospitals benefit from diagnosis-related-group outlier payments that partly offset gene-therapy costs, whereas specialty clinics rely on fragmented fee codes that rarely cover multidisciplinary services. Europe’s reference networks support cross-border patient flow, yet inconsistent national tariffs impede financial sustainability for high-complexity centers.

Geography Analysis

North America generated 42.03% of 2024 revenue. Medicaid carve-outs and National Institutes of Health trials drive demand, though prior-authorization delays average 90–120 days. ScreenPlus and similar newborn-screening initiatives in Massachusetts and California are expected to lift the GM1 gangliosidosis treatment market size in the region by 14% through 2031.

Asia-Pacific is the fastest riser at an 18.72% CAGR. China’s acceptance of overseas Phase 2 data, value-added-tax cuts, and blended reimbursement pilots in Zhejiang and Shandong provinces is accelerating commercial entry. Japan’s 10-year re-examination period incentivizes domestic trials, while India’s Rs 5 crore center-of-excellence grants enhance genomic diagnostic capacity, albeit with reliance on philanthropic funding for therapies.

Brazil’s SUS high-cost drug list could eventually accommodate GM1 therapies if local data support cost-offset claims, while Gulf Cooperation Council states leverage sovereign investment in genome strategies yet lack disease-specific programs. The geographic growth gap reflects both policy incentives and disparities in diagnostic infrastructure.

Competitive Landscape

Fewer than 20 active developers create a moderately concentrated field. Passage Bio transferred PBGM01 to GEMMA Biotherapeutics, exemplifying reliance on niche acquirers positioned to shepherd ultra-rare assets to market. Bluebird Bio’s USD 4.25 million LENMELDY price sets a signal that will influence future negotiations over GM1 therapy. Takeda’s 2021 agreement with Selecta Biosciences underscores the strategic importance of immune-evasion platforms.

Differentiation centers on the administration route, capsid design, and genotype targeting. Developers exploring blood-brain-barrier shuttle enzymes or hospital-based lentiviral point-of-care platforms occupy white-space niches. China’s rapid review pathways and India’s crowdfunding environment lower entry barriers for smaller firms pursuing proof-of-concept programs.

GM1 Gangliosidosis Treatment Industry Leaders

Amicus Therapeutics Inc.

Sarepta Therapeutics Inc.

Bluebird Bio Inc.

Passage Bio Inc.

Takeda Pharmaceutical Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: National Human Genome Research Institute published interim intravenous AAV9-GLB1 data showing biomarker normalization and extended survival, though transient hepatotoxicity occurred in two infants.

- July 2025: Azafaros Bio initiated a Phase 3 trial of nizubaglustat for GM2 gangliosidosis, with potential cross-application to GM1 cases.

- August 2024: Passage Bio out-licensed PBGM01 to GEMMA Biotherapeutics for USD 10 million upfront plus milestones, allowing GEMMA to pursue pivotal trials.

- March 2024: Bluebird Bio received FDA approval for LENMELDY at USD 4.25 million, setting a pricing precedent for lysosomal storage disease gene therapies.

Global GM1 Gangliosidosis Treatment Market Report Scope

The GM1 Gangliosidosis Treatment Market is defined as the global healthcare industry segment focused on therapies, diagnostics, and management solutions for GM1 gangliosidosis, a rare, inherited lysosomal storage disorder caused by mutations in the GLB1 gene that lead to progressive neurodegeneration. It includes enzyme replacement therapy (ERT), gene therapy, substrate reduction therapy (SRT), pharmacological chaperones, and supportive care approaches.

The GM1 Gangliosidosis Treatment Market Report is Segmented by Treatment Modality (Gene Therapy, Enzyme Replacement Therapy, Pharmacological Chaperone Therapy, Substrate Reduction Therapy, Symptomatic Management), Clinical Type (Type I, Type II, Type III), Administration Route (Intravenous, Intrathecal/Intracisternal, Intracerebroventricular, Oral), End-User (Hospitals, Specialty Clinics and Centers, Research Institutes, Home-Care Settings), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Gene Therapy |

| Enzyme Replacement Therapy |

| Pharmacological Chaperone Therapy |

| Substrate Reduction Therapy |

| Symptomatic Management |

| Type I |

| Type II |

| Type III |

| Intravenous |

| Intrathecal / Intracisternal |

| Intracerebroventricular |

| Oral |

| Hospitals |

| Specialty Clinics & Centers |

| Research Institutes |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Gene Therapy | |

| Enzyme Replacement Therapy | ||

| Pharmacological Chaperone Therapy | ||

| Substrate Reduction Therapy | ||

| Symptomatic Management | ||

| By Clinical Type | Type I | |

| Type II | ||

| Type III | ||

| By Route of Administration | Intravenous | |

| Intrathecal / Intracisternal | ||

| Intracerebroventricular | ||

| Oral | ||

| By End-user | Hospitals | |

| Specialty Clinics & Centers | ||

| Research Institutes | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the GM1 gangliosidosis treatment market in 2026?

The GM1 gangliosidosis treatment market size reached USD 154.13 million in 2026 and is on a 14.69% CAGR, reaching USD 305.79 million by 2031.

Which therapy class currently leads sales?

Gene therapy accounted for 61.81% of 2024 revenue, driven by advancing AAV9 and AAVhu68 constructs.

What drives the fastest growth segment?

Enzyme-replacement therapy is projected to expand at a 16.37% CAGR, driven by receptor-mediated transcytosis platforms that improve central nervous system exposure.

Which region will see the highest CAGR?

Asia-Pacific is forecast to grow at 18.72% CAGR due to China’s fast-track reviews and expanding reimbursement pilots.

How do newborn-screening programs affect treatment demand?

Early detection through programs such as ScreenPlus moves diagnosis to presymptomatic stages, increasing eligibility for prophylactic gene therapy and boosting market uptake.

Page last updated on: