GLP-1 Nutritional Support Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.88 Billion |

| Market Size (2031) | USD 6.94 Billion |

| Growth Rate (2026 - 2031) | 12.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GLP-1 Nutritional Support Market Analysis by Mordor Intelligence

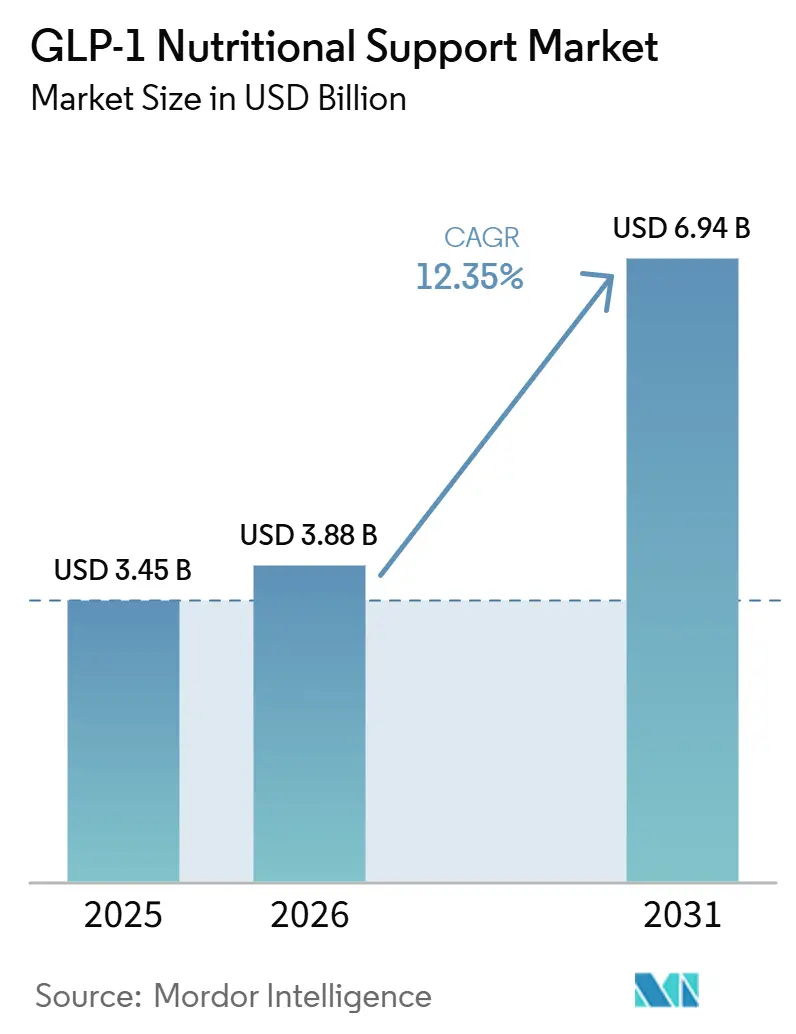

The GLP-1 Nutritional Support Market size is expected to grow from USD 3.45 billion in 2025 to USD 3.88 billion in 2026 and is forecast to reach USD 6.94 billion by 2031 at 12.35% CAGR over 2026-2031.

The market is expanding because GLP-1 prescriptions moved beyond a narrow diabetes base and became more common in weight management by late 2025, which widened the pool of users who need help with protein intake, muscle retention, and micronutrient balance. The GLP-1 nutritional support market is also benefiting from clinical guidance that now treats higher protein intake and closer nutrition support as a practical part of GLP-1 care rather than an optional add-on. Oral GLP-1 expansion is changing how the GLP-1 nutritional support market develops because self-managed users are more likely to buy companion nutrition through retail and digital channels instead of waiting for clinic-led recommendations. Competition in the GLP-1 nutritional support market is shifting toward companies that can combine clinical positioning, compact high-protein formats, and broad channel access, which is raising the standard for product design and evidence support. The main opportunity in the GLP-1 nutritional support market lies in products that are easy to consume during reduced appetite, gentle on digestion, and credible enough for use in physician, pharmacy, and telehealth pathways.

Key Report Takeaways

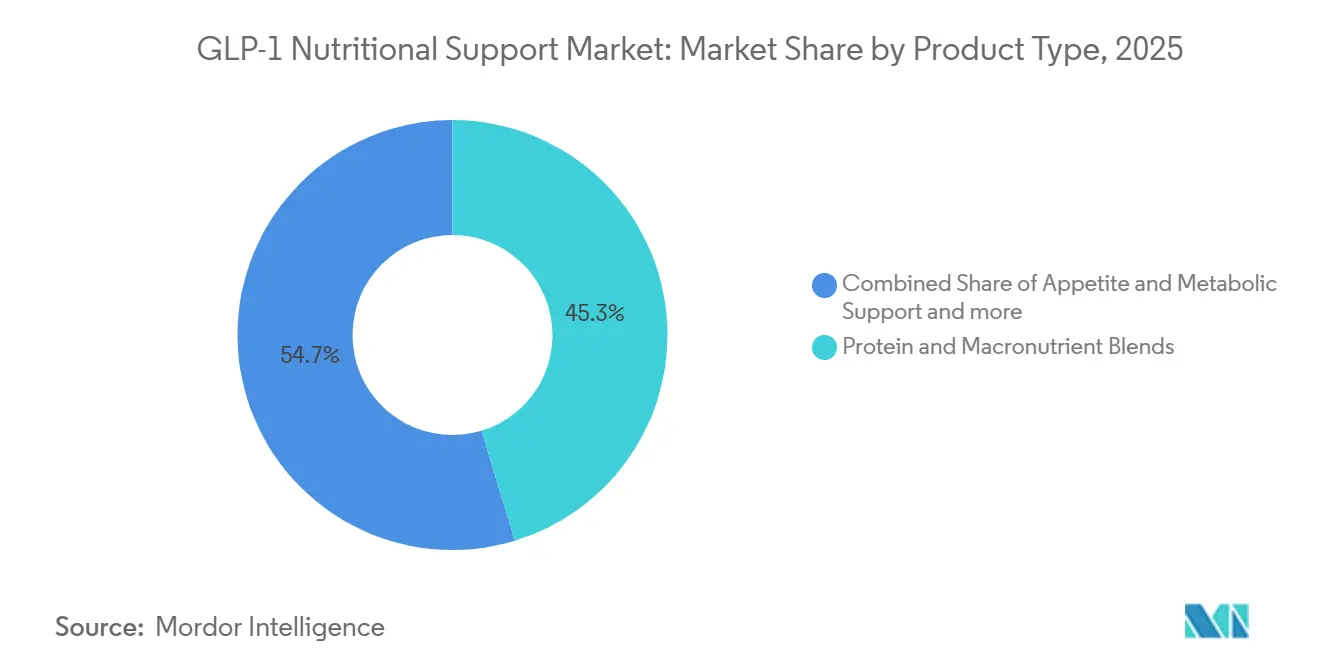

- By product type, Protein and Macronutrient Blends led with 45.31% share in 2025, while Appetite and Metabolic Support is forecast to grow at 14.38% CAGR through 2031.

- By dosage form, Powders held 39.24% share in 2025, while Ready-to-Drink Shakes are projected to expand at 14.52% CAGR through 2031.

- By age group, the 35-54 segment held 35.52% share in 2025, while the 18-34 segment is projected to grow at 15.25% CAGR through 2031.

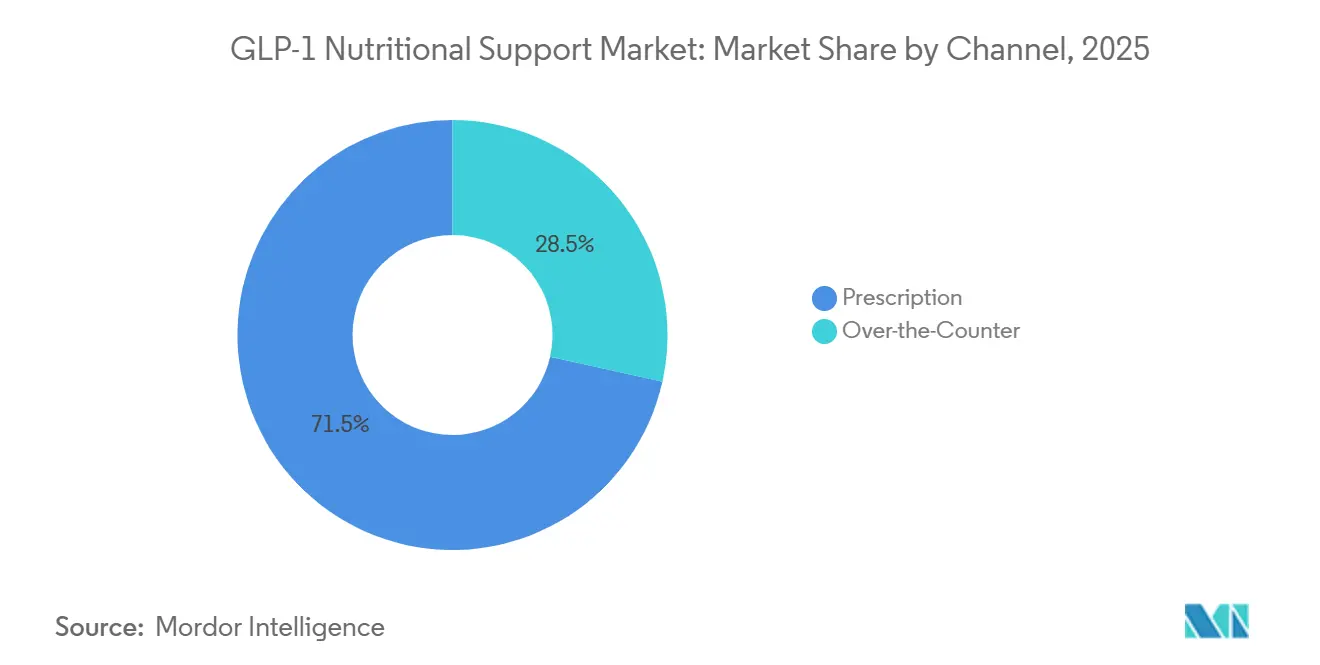

- By channel, Prescription held 71.52% share in 2025, while OTC is projected to grow at 13.25% CAGR through 2031.

- By distribution channel, Pharmacies held 38.36% share in 2025, while Online Stores are projected to grow at 16.55% CAGR through 2031.

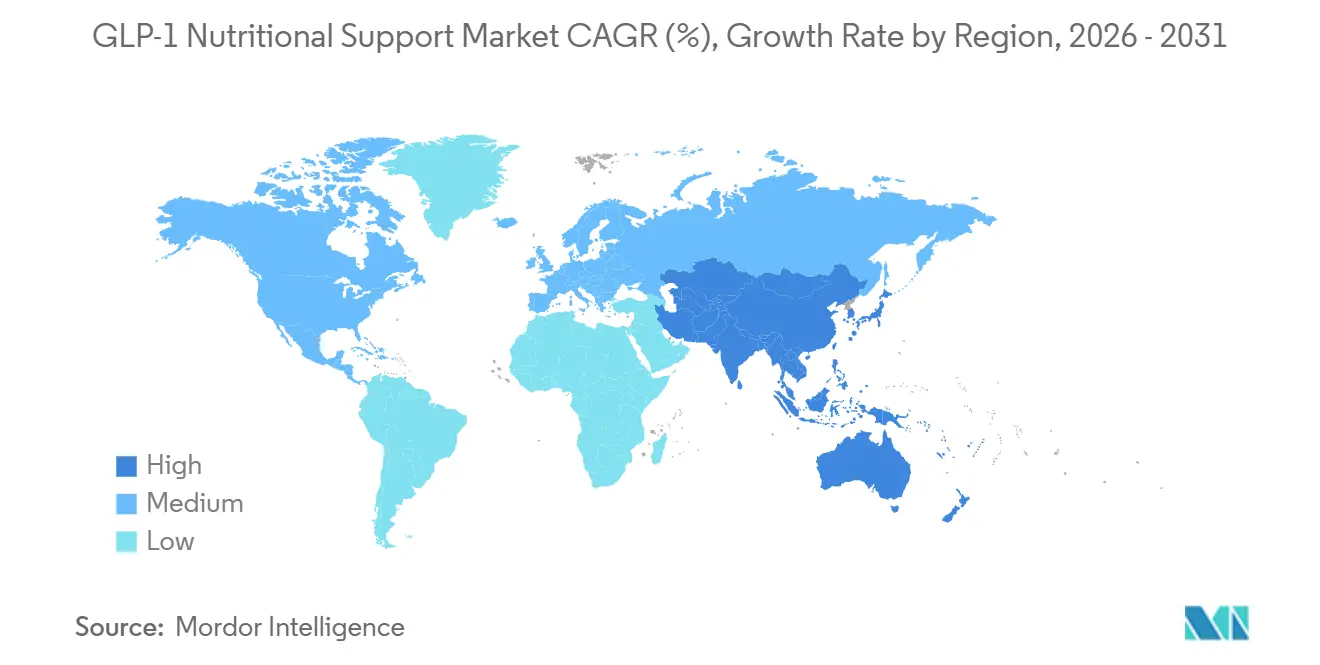

- By geography, North America held 39.22% share in 2025, while Asia-Pacific is projected to grow at 16.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GLP-1 Nutritional Support Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising GLP-1 Adoption in Weight Management | +4.5% | Global | Short term (≤ 2 years) |

| Need for Lean-Mass Preservation and Protein Repletion | +3.2% | Global, core in North America and Europe | Medium term (2-4 years) |

| Clinical Nutrition Protocols Expanding Adjunct Demand | +1.8% | North America and Europe | Medium term (2-4 years) |

| Oral GLP-1 Expansion Increasing At-Home Nutrition Support Use | +2.1% | Global, with spillover to Asia-Pacific and Latin America | Medium term (2-4 years) |

| Retail and DTC Bundling of GLP-1-Friendly Nutrition | +1.5% | North America core, Europe emerging | Short term (≤ 2 years) |

| Digital Dietitian Guidance Normalizing Structured Nutrition | +1.2% | North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising GLP-1 Adoption In Weight Management

The GLP-1 nutritional support market is getting its clearest demand lift from the rise in GLP-1 prescribing for weight management. Anti-obesity medication prescribing grew 10.1% from September 2025 to December 2025, and GLP-1 prescriptions moved above 7% of all prescriptions in the United States by December 2025[1]Truveta Research, “GLP-1 RA Prescription Trends: January 2019–December 2025,” Truveta, truveta.com. Medicare Part D gross spending on GLP-1 medicines reached USD 27.5 billion in 2024, which showed how deeply these therapies had already entered mainstream care pathways. That increase matters for the GLP-1 nutritional support market because each new user creates practical needs around muscle retention, lower-volume nutrition, and better tolerance during reduced food intake. As prescription use becomes more routine, the GLP-1 nutritional support market moves closer to a repeat-use wellness category rather than a niche clinical add-on.

Need For Lean-Mass Preservation And Protein Repletion

The GLP-1 nutritional support market is also gaining from clear evidence that weight loss on GLP-1 therapy often includes meaningful lean tissue loss. The 2025 joint advisory reported that 38%-40% of total weight lost during GLP-1 therapy can come from lean body mass, and the STEP 1 semaglutide trial recorded 5.3 kg of lean tissue loss within a 13.6 kg total reduction. Research presented at ENDO 2025 found higher muscle loss risk among older adults, women, and people with lower protein intake, and it also linked greater lean mass loss with less HbA1c improvement[2]H. Haines, “Consuming More Protein May Protect Patients Taking Anti-Obesity Drug from Muscle Loss,” Endocrine Society ENDO 2025 Press Release, endocrine.org. The same advisory set protein targets at 1.2-1.6 g/kg/day and flagged deficiencies in iron, calcium, magnesium, zinc, and several vitamins, which gives the GLP-1 nutritional support market a strong clinical reason to favor targeted protein and micronutrient products. A 2025 study in Diabetes, Metabolic Syndrome and Obesity further supported this direction by linking oral nutritional supplements with improved lean mass preservation, especially among younger adults and longer-duration users.

Clinical Nutrition Protocols Expanding Adjunct Demand

The GLP-1 nutritional support market is becoming more protocol driven as nutrition support gets drawn into formal treatment pathways. A 2026 scoping review in Obesity Reviews found that caloric intake fell 24%-39% across 12 telehealth GLP-1 trials, yet only 3 of the 12 studies included a registered dietitian, which left a visible care gap around practical nutrition support. That gap is commercially important because patients still need structured help with protein adequacy, micronutrient intake, and meal planning even when the drug is prescribed successfully. In January 2026, the Nutrition+ randomized study led by Joslin Diabetes Center with Abbott Nutrition began testing whether a high-protein diabetes-specific formula can preserve lean mass in patients starting GLP-1 receptor agonists. The GLP-1 nutritional support market stands to benefit if trial-backed products gain stronger footing in clinics, hospitals, and telehealth programs where nutrition recommendations are becoming more standardized.

Oral GLP-1 Expansion Increasing At-Home Nutrition Support Use

The GLP-1 nutritional support market is being reshaped by oral GLP-1 therapies because these formats make treatment easier to start and easier to manage at home. The December 2025 approval of oral semaglutide and the April 2026 approval of orforglipron lowered a major barrier for users who prefer not to start injectable treatment. Eli Lilly has submitted orforglipron to regulators in more than 40 countries and is ramping production at Huntsville, Alabama, which indicates that broader oral access is expected rather than temporary. This shift supports the GLP-1 nutritional support market because nutrition choices move closer to the patient when therapy becomes less clinic dependent. It also favors compact, self-selected products that can support protein intake, satiety management, and micronutrient adequacy without requiring intensive professional supervision.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gastrointestinal Tolerance Limits Repeat Use | -1.3% | Global | Short term (≤ 2 years) |

| High Cost of GLP-1 Therapy Constrains Addressable Demand | -1.8% | Global, most severe in emerging markets | Long term (≥ 4 years) |

| Label Credibility and Claim Compliance Risks | -1.0% | North America and Europe | Medium term (2-4 years) |

| Low Adherence to Long-Term Nutrition Routines | -1.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gastrointestinal Tolerance Limits Repeat Use

The GLP-1 nutritional support market faces a repeat-use challenge because nausea, constipation, and slowed gastric emptying can make even useful nutrition products harder to tolerate. This issue is shaping formulation choices more than simple flavor or branding decisions because products must stay gentle while still delivering meaningful protein and micronutrient density. Nestlé Health Science addressed that need with whey protein microgel technology in BOOST Advanced, which was designed for adults on a GLP-1 weight loss journey. Danone made a similar adjustment with Oikos Fusion by using a compact 7 fl oz format that reflects the low-volume needs of users with reduced appetite. These responses show that the GLP-1 nutritional support market can grow, but repeat demand will stay weaker for products that feel too heavy, too large, or too hard to digest during active therapy.

High Cost Of GLP-1 Therapy Constrains Addressable Demand

The GLP-1 nutritional support market is capped by the size of the active medication user base, and that base is still limited by the cost of therapy. The 2025 joint advisory noted that annual list prices for GLP-1 anti-obesity medicines in the United States remained at USD 12,000-16,000, or USD 7,000-8,000 with manufacturer coupons. The same body of evidence showed that real-world persistence stayed at only 33%-50% after 1 year and fell to 15% after 2 years, which directly narrows the repeat customer pool for companion nutrition. That pattern matters because the GLP-1 nutritional support market depends on continued medicine use rather than on one-time trial purchases. Lower-cost oral options may ease this restraint over time, but the GLP-1 nutritional support market will still remain sensitive to affordability until access broadens more clearly across payer and income groups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Formulations Anchor Clinical Demand

Protein and Macronutrient Blends captured 45.31% of the GLP-1 nutritional support market share in 2025, which kept them well ahead of other product types in the current mix. That position reflects a practical clinical need because the 2025 joint advisory set protein intake at 1.2-1.6 g/kg/day for GLP-1 users, a level many patients will struggle to reach through reduced food intake alone. The leading products in this category are built around concentrated delivery rather than general wellness messaging, which explains why companies are emphasizing large protein loads in compact servings. Nestlé's BOOST Advanced delivers 35 g of protein per serving, Abbott's Ensure Max Protein 42 g exceeds many mainstream thresholds, and these formats fit the clinical direction of the GLP-1 nutritional support market[3]Abbott, “Muscles, the New Flex: Abbott Launches Two New Ensure Max Protein Shakes to Tap into Growing Muscle Health Movement,” Abbott Mediaroom, abbott.mediaroom.com.

Appetite and Metabolic Support is projected to expand at 14.38% CAGR through 2031, which makes it the fastest-growing sub-segment in this product set. Growth is tied to the shift toward self-managed therapy, especially as oral GLP-1 access broadens and users look for more complete support rather than protein alone. Fiber Supplements and Digestive Health Formulations are also moving up because constipation and altered gastric motility are now treated as practical nutrition issues rather than side notes. Micronutrient Blends remain relevant because the joint advisory identified risks around iron, calcium, magnesium, zinc, and vitamins A, D, E, K, B1, and B12 during GLP-1 therapy. The GLP-1 nutritional support industry is therefore moving toward clinically specific formulations that can address muscle retention, digestive comfort, and nutrient adequacy within one patient journey.

By Dosage Form: RTD Shakes Gain Share On Low-Volume Precision Nutrition

Powders held 39.24% share in 2025, which shows that the GLP-1 nutritional support market still relies heavily on formats with broad distribution, lower cost per serving, and familiar use in pharmacy and clinical settings. Powders also fit prescription-led pathways because they are easy to position inside managed nutrition programs where dosing and protein targets are discussed directly with clinicians. Their shelf stability and formulation flexibility make them useful for protein blends, fiber support, and specialized mixes that need a broader nutrient load. This established base explains why powders remain the largest dosage form even as newer, more convenient options pick up speed.

Ready-to-Drink Shakes are projected to grow at 14.52% CAGR, which makes them the strongest growth pocket within the GLP-1 nutritional support market size outlook for dosage forms. The reason is simple because many users eat less, want fewer steps, and respond well to single-serve products that do not require measuring, mixing, or cleanup. Danone's Oikos Fusion combines 23 g of protein with a compact 7 fl oz serving, and that design matches the low-volume pattern that GLP-1 therapy often creates. Capsules and Tablets remain important for micronutrient delivery, while Gummies and Chews are gaining ground with younger users who prefer alternatives to standard pill formats. Across the GLP-1 nutritional support industry, dosage-form development is now centered on convenience, tolerance, and nutrient density rather than on broad meal replacement logic.

By Age Group: Mid-Career Users Lead While Younger Cohorts Accelerate

The 35-54 age group held 35.52% share in 2025, which made it the largest user cohort in the GLP-1 nutritional support market. This outcome matches the high concentration of obesity and type 2 diabetes treatment in middle-aged adults, where both metabolic burden and prescription activity are especially high. It also reflects a group that is more likely to face lean mass concerns during weight loss, which makes structured protein and micronutrient support more clinically relevant. The GLP-1 nutritional support market therefore draws steady demand from users who are not simply dieting, but managing chronic metabolic risk with medication and companion nutrition.

The 18-34 age group is projected to grow at 15.25% CAGR through 2031, which gives it the fastest expansion rate among age bands. Oral semaglutide in December 2025 and orforglipron in April 2026 lowered the barrier for younger users who prefer simpler, self-directed treatment formats. A 2025 DMSO study also found that oral nutritional supplements delivered stronger lean-mass preservation benefits among younger adults and longer-duration users, which supports earlier uptake in this cohort. The 55-74 and 75+ groups remain smaller today, yet they are becoming more important because cardiovascular use cases and sarcopenia risk raise the need for bone and muscle support together. The Vitamin Shoppe's GLP-1 Support Muscle & Bone SKU reflects that direction by combining the age-related need for protein support with bone-health positioning.

By Channel: Prescription Commands Share As OTC Carves Its Path

The Prescription channel held 71.52% share in 2025, which confirms that physician and pharmacist influence still shapes most purchase decisions in the GLP-1 nutritional support market. This channel led because patients entering GLP-1 therapy often look for credible products that fit a clinical plan, especially when appetite changes and lean-mass concerns appear early. Prescription-led demand also tends to favor higher-protein and more specialized products, which supports premium pricing and tighter product selection. These features help explain why the GLP-1 nutritional support market remains more clinically framed than many broader supplement categories.

The OTC channel is projected to grow at 13.25% CAGR through 2031 as retail launches widen access for users outside formal nutrition programs. At the same time, claim discipline is becoming more important because the Federal Trade Commission issued a final order against NextMed in December 2025 over deceptive GLP-1 advertising claims. That action signals that OTC brands must clearly position themselves as nutrition support rather than as drug-like weight loss solutions. The Vitamin Shoppe's Whole Health Rx model shows how the boundary can still blur by linking prescription access with supplement recommendations in one consumer path. The GLP-1 nutritional support market should therefore see OTC growth, but the winners are likely to be companies that combine wider access with careful compliance.

By Distribution Channel: Digital Commerce Redefines The Purchase Journey

Pharmacies held 38.36% share in 2025, which kept them as the leading distribution route in the GLP-1 nutritional support market because prescription-led buying still dominates. Pharmacies remain important because they sit close to drug dispensing, clinician advice, and repeat refill behavior, which gives them a natural role in early companion nutrition decisions. They also support trust, especially for first-time users who want guidance on protein products, digestive support, and micronutrient supplementation. This makes pharmacies a strong anchor channel even as digital options accelerate.

Online Stores are projected to grow at 16.55% CAGR, which represents the fastest channel growth within the GLP-1 nutritional support market size outlook for distribution. Digital channels fit this category well because users often prefer auto-ship models, easy product comparison, and direct access to compact protein and support formats. Telehealth-linked recommendations strengthen that pattern because product discovery can happen inside the same digital journey as diagnosis, prescription, and follow-up support. Supermarkets are also becoming more relevant as large brands use existing shelf relationships to normalize GLP-1-friendly products in everyday retail settings, including Danone's Walmart launch for Oikos Fusion at USD 2.12 per bottle. The GLP-1 nutritional support industry is therefore moving from a pharmacy-centered purchase path to a more blended model where digital convenience and mainstream retail visibility both matter.

Geography Analysis

North America held 39.22% of the GLP-1 nutritional support market share in 2025, which made it the leading regional cluster in the current landscape. The region benefits from strong GLP-1 penetration in the United States, where prescriptions exceeded 7% of all dispensed prescriptions by December 2025. That prescription base supports the GLP-1 nutritional support market because a larger active user pool creates repeat demand for protein support, digestive support, and micronutrient products. North America also has the deepest concentration of launches from major nutrition companies, including Abbott, Nestlé Health Science, Danone, and The Vitamin Shoppe, which keeps product availability high across both clinical and retail channels. Canada is moving in the same direction as U.S. clinical use expands, while Mexico remains earlier stage because affordability still limits broader uptake. Europe remains the second major area of development, and its regulatory setting favors more carefully substantiated nutrition positioning, which suits clinically framed products better than loose wellness claims.

Asia-Pacific is projected to grow at 16.15% CAGR through 2031, which gives it the fastest regional growth profile in the GLP-1 nutritional support market. The region is gaining momentum because access to GLP-1 therapy is widening in large population markets, and that expands the base for companion nutrition products. India is an important part of this story because rapid drug access expansion is creating room for localized nutrition offerings tied directly to GLP-1 and GIP therapy. Japan adds another layer of growth because its Functional Food Claims system supports formalized positioning for metabolic health products, and Kobayashi Pharmaceutical launched Salacia 100 Premium in March 2026 as the first supplement approved to support normal HbA1c levels in the country. China, South Korea, and Australia also strengthen the regional outlook through urban adoption, established supplement habits, and strong interest in higher-protein nutrition.

South America and the Middle East and Africa remain smaller in current revenue terms, but they still matter to the GLP-1 nutritional support market because obesity prevalence and premium healthcare pockets support long-run demand formation. Brazil stands out in Latin America because supplement companies are already testing GLP-1-specific positioning, including Vitafor's GLP-1 Support Multivitamínico launch in August 2025, even though household use remains concentrated in higher-income groups. The broader population need is visible because PAHO reported that 67.5% of adults in Latin America had excess weight, which leaves a large future base for medication and companion nutrition adoption. In MEA, the GCC offers the clearest entry point because high private healthcare coverage, elevated obesity prevalence, and established premium nutrition distribution create a favorable setting for early category development.

Competitive Landscape

The GLP-1 nutritional support market is moderately fragmented, and competition now spans large nutrition multinationals, pharma-linked entrants, and purpose-built companion brands. Nestlé Health Science, Abbott, Danone, Herbalife, and Glanbia bring scale, established distribution, and formulation resources that smaller brands cannot easily match. At the same time, specialist moves from the Dr. Reddy's and Nestlé Health Science joint venture, Medifast's OPTAVIA ASCEND line, and newer companion products show that the category still has room for focused entrants. The GLP-1 nutritional support market is therefore not controlled by a single brand group, but it is moving toward a higher evidence and product-design standard. That change favors companies that can connect clinical credibility, ingredient depth, and broad access in one offering.

Abbott strengthened its position with PROTALITY in January 2024 and followed with additional Ensure Max Protein launches in December 2025, which shows a sustained effort to own muscle-health positioning around weight loss support. Nestlé Health Science moved with BOOST Advanced in June 2025, using expert-led positioning and a digestion-conscious protein system tailored to adults on GLP-1 therapy. Danone entered with Oikos Fusion in August 2025 and highlighted a patented nutrient blend of whey, leucine, and vitamin D, which suggests a stronger attempt to build defensible differentiation around muscle retention. These moves show that the GLP-1 nutritional support market is no longer a simple extension of general meal replacement. It is turning into a more specialized field where compact delivery, tolerance, and evidence support all affect share gains.

Ingredient suppliers hold an important behind-the-scenes role in the GLP-1 nutritional support market because many end products depend on strong protein systems, premixes, and formulation support. Glanbia has been especially direct on this point, with management stating that GLP-1 is a tailwind for the whole business and pointing to stronger protein consumption among GLP-1 users. The market is also opening room for integrated care models, as shown by The Vitamin Shoppe's Whole Health Rx platform and Medifast's move to link GLP-1 access with OPTAVIA nutrition coaching. Herbalife's relatively stable FY2025 net sales versus Medifast's weaker revenue path suggests that companies positioned as complementary to GLP-1 use have held up better than those forced into a late pivot.

GLP-1 Nutritional Support Industry Leaders

Nestlé Health Science

Abbott Laboratories

Glanbia

Herbalife

ADM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Arla Foods Ingredients developed new solutions to meet the needs of consumers using GLP-1 anti-obesity medications. Featuring the high-quality Nutrilac and Lacprodan BLG-100 protein solutions, these formats deliver all essential amino acids that support muscle health in nutrient-dense formats.

- January 2026: Abbott Nutrition, in collaboration with Joslin Diabetes Center, initiated the Nutrition+ randomized controlled trial (NCT07271043) to evaluate whether a high-protein diabetes-specific formula preserves lean muscle mass in patients initiating GLP-1 receptor agonist therapy — the first large-scale academic trial of this design.

Global GLP-1 Nutritional Support Market Report Scope

As per the scope of the report, GLP-1 nutritional support refers to dietary strategies or supplements that aim to enhance the activity or levels of Glucagon-Like Peptide-1 (GLP-1), a hormone involved in regulating blood sugar levels, appetite, and digestion. These supports are often used to assist in managing conditions such as diabetes, obesity, or metabolic disorders by promoting satiety, improving glycemic control, and supporting overall metabolic health.

The GLP-1 nutritional support market is segmented by product type into protein and macronutrient blends, fiber supplements, micronutrient blends, digestive health formulations, appetite and metabolic support, and other product types; by dosage form into powders, ready-to-drink shakes, capsules and tablets, gummies and chews, and other dosage forms; by age group into 18 to 34 years, 35 to 54 years, 55 to 74 years, and 75 years and above; by channel into prescription and over-the-counter; by distribution channel into online stores, pharmacies, supermarkets, and other distribution channels; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Protein and Macronutrient Blends |

| Fiber Supplements |

| Micronutrient Blends |

| Digestive Health Formulations |

| Appetite and Metabolic Support |

| Other Product Types |

| Powders |

| Ready-to-Drink Shakes |

| Capsules and Tablets |

| Gummies and Chews |

| Other Dosage Forms |

| 18 to 34 Years |

| 35 to 54 Years |

| 55 to 74 Years |

| 75 Years and Above |

| Prescription |

| Over-the-Counter |

| Online Stores |

| Pharmacies |

| Supermarkets |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Protein and Macronutrient Blends | |

| Fiber Supplements | ||

| Micronutrient Blends | ||

| Digestive Health Formulations | ||

| Appetite and Metabolic Support | ||

| Other Product Types | ||

| By Dosage Form | Powders | |

| Ready-to-Drink Shakes | ||

| Capsules and Tablets | ||

| Gummies and Chews | ||

| Other Dosage Forms | ||

| By Age Group | 18 to 34 Years | |

| 35 to 54 Years | ||

| 55 to 74 Years | ||

| 75 Years and Above | ||

| By Channel | Prescription | |

| Over-the-Counter | ||

| By Distribution Channel | Online Stores | |

| Pharmacies | ||

| Supermarkets | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the GLP-1 nutritional support market by 2031?

The GLP-1 nutritional support market is projected to reach USD 6.94 billion by 2031, rising from USD 3.88 billion in 2026 at a 12.35% CAGR.

Which product category leads revenue generation in this space?

Protein and Macronutrient Blends led with 45.31% share in 2025 because GLP-1 users need concentrated protein support for lean-mass preservation.

Which dosage form is growing the fastest for GLP-1 companion nutrition?

Ready-to-Drink Shakes are projected to grow at 14.52% CAGR through 2031 because they fit reduced appetite, smaller portions, and no-prep use.

Which region leads current demand and which one grows the fastest?

North America led with 39.22% share in 2025, while Asia-Pacific is projected to record the fastest growth at 16.15% CAGR through 2031.

Why are companies focusing so heavily on protein-rich formulations?

Clinical guidance and published studies show that 38%-40% of total weight loss during GLP-1 therapy can come from lean body mass, which makes high-protein support more important.

What is changing the competitive landscape most rapidly?

Product launches from Abbott, Nestlé Health Science, and Danone, along with telehealth-linked models from The Vitamin Shoppe and Medifast, are pushing the category toward more clinical and evidence-backed positioning.

Page last updated on: