Market Overview

| Study Period | 2020 - 2030 |

|---|---|

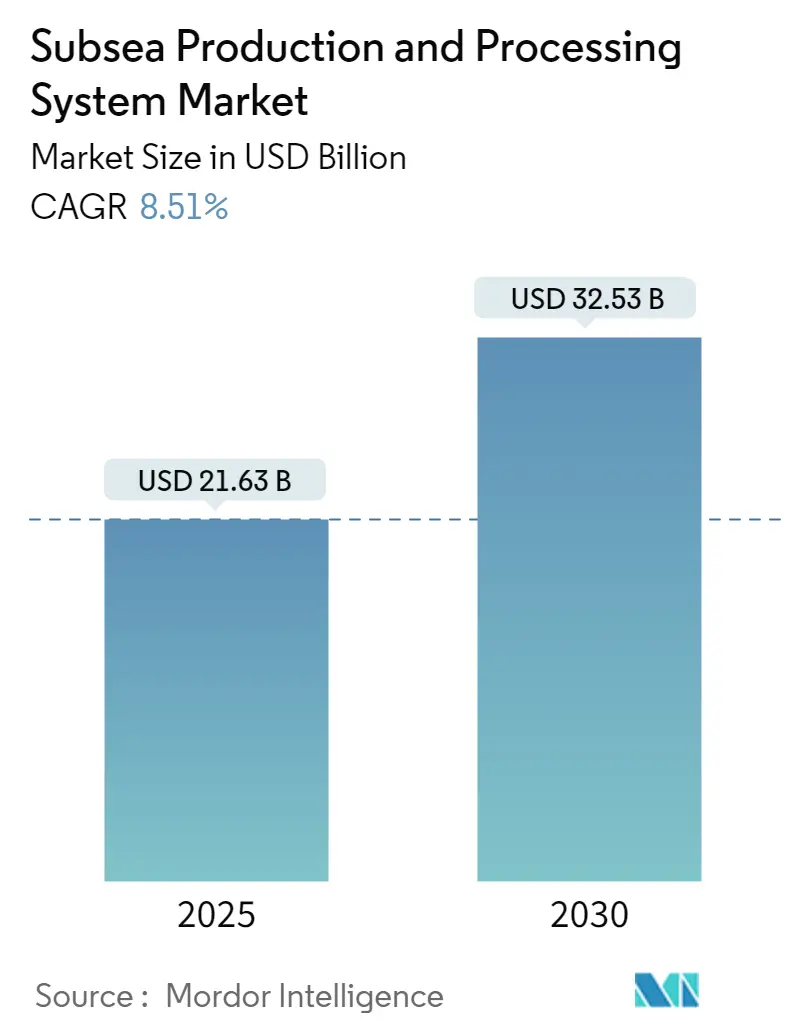

| Market Size (2025) | USD 21.63 Billion |

| Market Size (2030) | USD 32.53 Billion |

| Growth Rate (2025 - 2030) | 8.51% CAGR |

| Fastest Growing Market | Middle-East and Africa |

| Largest Market | Middle East and Africa |

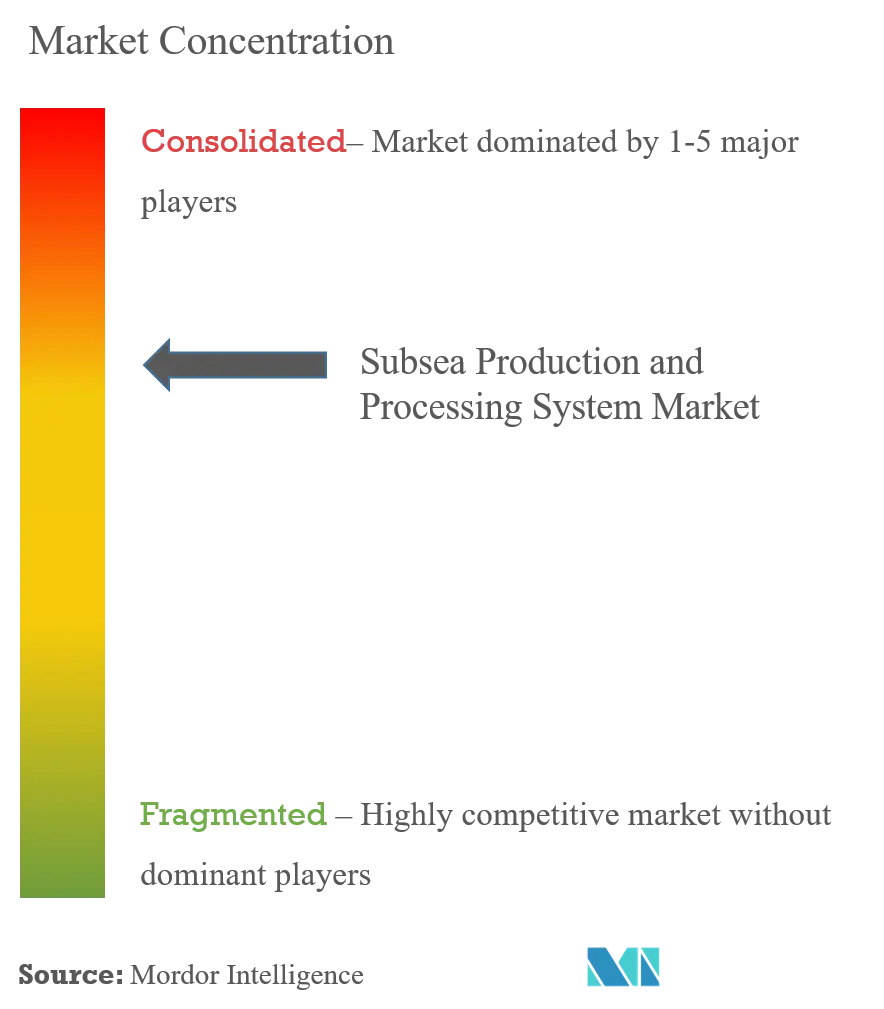

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subsea Production and Processing System Market Analysis by Mordor Intelligence

The Subsea Production and Processing System Market size is estimated at USD 21.63 billion in 2025, and is expected to reach USD 32.53 billion by 2030, at a CAGR of 8.51% during the forecast period (2025-2030).

The subsea production and processing systems industry is experiencing significant technological advancement and innovation, particularly in deepwater and ultra-deepwater applications. In May 2023, Baker Hughes launched a groundbreaking subsea technology called MS-2 Annulus Seal, demonstrating the industry's commitment to improving operational efficiency and reducing installation costs. This technological evolution is complemented by the increasing adoption of automated systems and digital solutions, enabling more efficient monitoring and control of subsea systems while minimizing human intervention in harsh underwater environments.

The industry is witnessing a substantial shift toward sustainable and environmentally conscious operations, with companies investing in technologies that reduce environmental impact while maintaining production efficiency. Qatar's ambitious plan to increase its LNG production capacity from 77 million tonnes per annum to 126 million tonnes per annum by 2027 exemplifies the industry's focus on expanding capacity while implementing advanced subsea technologies. This transformation is further evidenced by the development of all-electric subsea systems and the integration of renewable energy solutions in offshore operations.

Strategic partnerships and collaborations are reshaping the competitive landscape, as companies seek to combine expertise and resources for more efficient project execution. In March 2023, ONGC's collaboration with TotalEnergies to establish a holistic framework for exchanging technical strengths in deep-water offshore operations highlights this trend. Similarly, QatarEnergy's March 2023 agreement with ExxonMobil for stakes in two offshore explorations in Canada demonstrates the industry's growing emphasis on international partnerships to access new markets and technologies.

The market is experiencing a notable shift in geographical focus, with significant developments in emerging regions. CNOOC's ambitious production targets of 650 million barrels of oil equivalent in 2023, increasing to 690-700 million barrels in 2024, reflect the growing importance of Asia-Pacific in the global subsea oil and gas market. This regional diversification is accompanied by increasing investments in subsea infrastructure, particularly in areas with substantial offshore reserves, such as Brazil, where approximately 94% of oil reserves are located offshore, with 80% concentrated near Rio de Janeiro, driving the demand for advanced subsea equipment and offshore production systems.

Global Subsea Production and Processing System Market Trends and Insights

Rising Deepwater Oil & Gas Exploration and Production Activities in the Americas, Asia-Pacific, and Middle East & Africa Region

The global energy landscape is experiencing a significant transformation, with oil and natural gas expected to contribute approximately half of the 5% projected increase in global energy demand by 2030. This rising demand, coupled with technological advancements and operational optimizations, has led to a substantial reduction in offshore upstream project costs, particularly in deepwater production and ultra-deepwater developments. The industry has witnessed increased investment in offshore exploration and production activities, especially in previously unexplored regions. For instance, in March 2023, ONGC collaborated with TotalEnergies to establish a holistic framework for exchanging technical strengths in deep-water offshore, specifically focusing on the development of deep-water blocks in Mahanadi and Andamans off India's east coast.

The Middle East and African region has emerged as a prominent hub for offshore exploration activities, demonstrated by a significant 57% increase in offshore rig deployment as of March 2023 compared to October 2020. This surge in activity is complemented by major developments across other regions. In the Americas, Shell and TotalEnergies have strengthened their presence in Brazil's offshore sector, with Shell Brazil now holding more than 30 oil & gas contracts in the country. Similarly, in the Asia-Pacific region, BP's acquisition of two offshore exploration blocks - Agung I and Agung II in Indonesia - represents the industry's growing interest in developing previously unexplored areas with significant resource potential.

The industry is witnessing a strategic shift towards deepwater exploration as companies seek to capitalize on the current market conditions. This is evidenced by recent developments in 2023, such as Oil and Natural Gas Corp (ONGC)'s USD 4 billion investment plan for exploration activities and the establishment of technical collaborations with global energy majors. The trend is particularly notable in the Middle East & Africa region, where companies are investing heavily in subsea infrastructure to support major LNG projects, addressing both the growing demand for natural gas and the need for cleaner energy alternatives. These investments are driving technological innovations in subsea systems, enabling operators to access and develop resources in increasingly challenging environments while maintaining operational efficiency and environmental compliance.

Furthermore, the subsea oil and gas industry is evolving with advancements in subsea technology, which are crucial for enhancing the efficiency of offshore processing. As companies continue to explore and develop deepwater resources, the integration of subsea systems is becoming increasingly vital to ensure sustainable and efficient operations.

Understand The Key Trends Shaping This Market

Download PDF

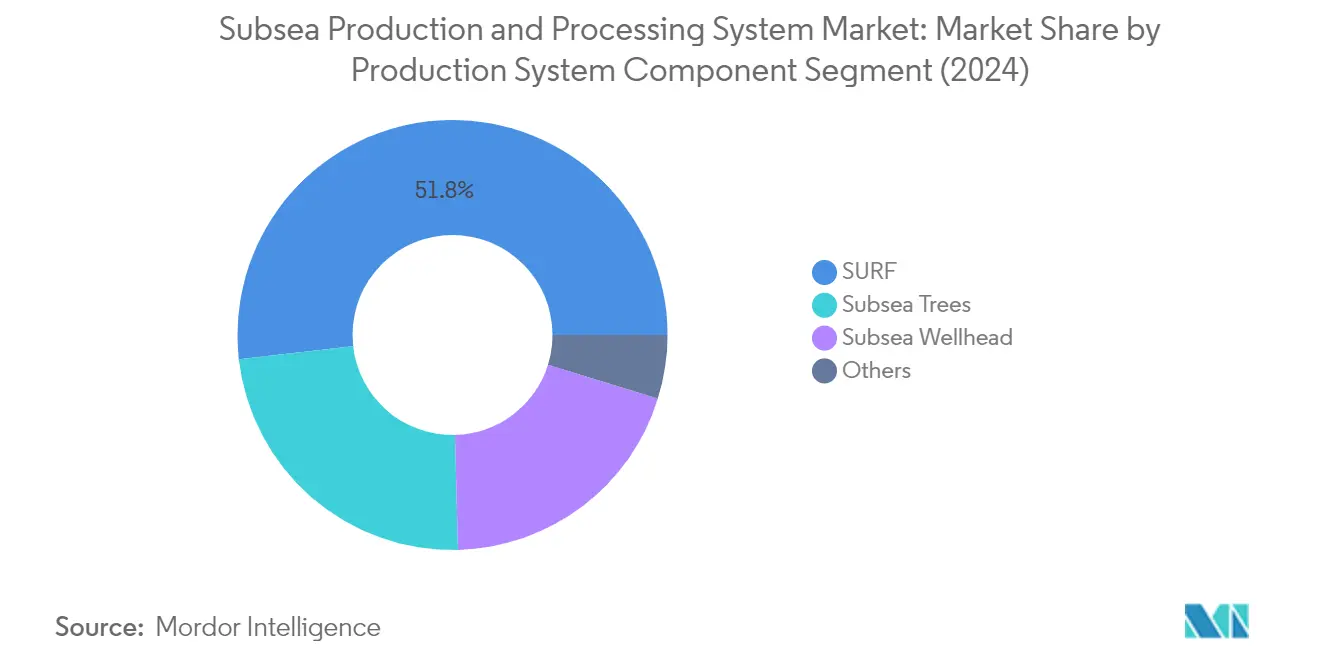

Segment Analysis: Production System Component

SURF Segment in Subsea Production and Processing System Market

The Subsea Umbilicals, Risers, and Flowlines (SURF) segment dominates the global subsea production and processing system market, holding approximately 52% market share in 2024. This significant market position is driven by the critical role SURF systems play in connecting surface and seafloor oil & gas equipment for controls, power, and heat transmission. The segment's dominance is further strengthened by the increasing deployment of these systems in deepwater and ultra-deepwater projects, particularly in regions like Brazil, the Gulf of Mexico, and West Africa. SURF systems are essential for providing electric and fiber-optic signals, electrical power, and hydraulic and chemical injection fluids to subsea units, while also supporting subsea boosting and subsea compression operations. The segment's robust performance is also attributed to the growing focus on flow assurance and the prevention of wax and hydrate formation in subsea production systems.

Subsea Trees Segment in Subsea Production and Processing System Market

The subsea trees segment is projected to exhibit the highest growth rate of approximately 9% during the forecast period 2024-2029. This accelerated growth is primarily driven by technological advancements in subsea tree systems, including the development of high-pressure high-temperature (HPHT) capabilities and improved reliability features. The segment's growth is further supported by increasing investments in deepwater and ultra-deepwater exploration and production activities, particularly in regions like the Gulf of Mexico, Brazil, and West Africa. The adoption of advanced subsea tree technologies, such as vertical and horizontal tree systems with enhanced monitoring and control capabilities, is also contributing to the segment's rapid expansion. Additionally, the industry's focus on cost optimization and operational efficiency through standardized and modular tree designs is expected to fuel the segment's growth trajectory.

Remaining Segments in Production System Component

The subsea wellhead and other production system components segments complete the market landscape, each serving crucial functions in subsea operations. The subsea wellhead segment plays a vital role as the primary pressure barrier for subsea wells, providing essential anchoring and suspension points for casing strings. This segment continues to evolve with innovations in materials and design, particularly for high-pressure applications. The other production system components segment, though smaller in market share, encompasses critical elements such as subsea manifold, flowline connectors, and subsea control systems, which are essential for maximizing reservoir recovery and extending field life. These segments are witnessing continuous technological advancements, particularly in areas of reliability, safety, and operational efficiency.

Segment Analysis: Processing System Type

Boosting Segment in Subsea Production and Processing System Market

The subsea boosting segment continues to dominate the subsea production and processing system market, holding approximately 33% market share in 2024. This significant market position is attributed to the segment's crucial role in supplying sufficient energy to well streams, ensuring fluids reach processing facilities efficiently. Subsea boosting systems are particularly valuable in scenarios where wellhead pressure falls below pipeline resistance or when natural reservoir pressure is insufficient. The technology enables production with back pressure at the wellhead as low as 50 psi, making even low-energy reservoirs commercially viable. Major oil and gas operators have widely adopted these systems, recognizing their effectiveness in extending field life while reducing carbon emissions compared to alternative methods like gas lifts. The segment's dominance is further reinforced by its ability to increase recovery rates, accelerate production, improve flow assurance, and significantly lower both CAPEX and OPEX in subsea operations.

Gas Compression Segment in Subsea Production and Processing System Market

The subsea compression segment is emerging as the fastest-growing segment in the subsea production and processing system market, projected to grow at approximately 12% during 2024-2029. This remarkable growth is driven by the increasing adoption of subsea compression systems as a sustainable alternative to conventional compressor solutions installed on sea-level platforms. The segment's expansion is supported by successful implementations like the Åsgard gas field project, which demonstrated the technology's reliability with over 100,000 operational hours without intervention. The growth is further accelerated by the segment's ability to significantly reduce environmental impact, as subsea compression systems require smaller infrastructure footprints compared to platform-based solutions. Additionally, the remote operation capabilities of these systems minimize health and safety risks, making them increasingly attractive to operators focusing on both operational efficiency and environmental responsibility.

Remaining Segments in Processing System Type

The subsea separation and injection segments continue to play vital roles in the subsea production and processing system market. The subsea separation segment focuses on crucial functions like separating multiphase fluids on the seabed and managing water content, while the injection segment specializes in enhancing the efficiency and productivity of existing wells through fluid injection processes. Both segments contribute significantly to the market's overall functionality by offering solutions for water treatment, flow assurance, and production optimization. These segments are particularly valuable in deepwater applications where traditional surface processing facilities may be impractical or cost-prohibitive. Their continued evolution and integration with other subsea technologies demonstrate the market's commitment to comprehensive subsea processing solutions.

Segment Analysis: Water Depth

Deepwater and Ultra-Deepwater Segment in Subsea Production and Processing System Market

The Deepwater and Ultra-Deepwater segment dominates the global subsea production and processing system market, commanding approximately 72% of the market share in 2024. This segment's prominence is driven by the increasing exploration and production activities in deep waters as companies move further offshore to access untapped reserves. The segment has witnessed substantial growth due to technological advancements in subsea systems that enable efficient operations at extreme depths, improved safety measures, and enhanced recovery rates. The development of sophisticated subsea processing equipment, including subsea boosting systems, subsea separation units, and subsea compression technologies, has made deepwater operations more economically viable. Major oil and gas companies are increasingly investing in deepwater projects, particularly in regions like Brazil's pre-salt areas, the Gulf of Mexico, and West Africa. The segment is expected to maintain its strong growth trajectory with a projected growth rate of approximately 10% from 2024 to 2029, driven by the rising global energy demand and the need to exploit deeper water resources as shallow water reserves mature.

Shallow Water Segment in Subsea Production and Processing System Market

The Shallow Water segment continues to play a vital role in the subsea production and processing system market, particularly in regions with extensive continental shelves. This segment is characterized by lower operational complexities and reduced installation costs compared to deepwater operations. The segment maintains its significance through the development of marginal fields and the optimization of existing shallow water infrastructure. Companies are implementing advanced technologies to enhance recovery from mature shallow water fields, including the deployment of smart well systems and improved monitoring capabilities. The shallow water segment also benefits from shorter project execution timelines and lower technical risks, making it attractive for operators looking to maintain steady production levels. Recent technological innovations have focused on making shallow water operations more cost-effective through standardized equipment designs and simplified installation procedures. The segment continues to attract investments in regions like the Middle East, Southeast Asia, and parts of the North Sea, where shallow water resources remain abundant and economically viable.

Subsea Production and Processing System Market Geography Segment Analysis

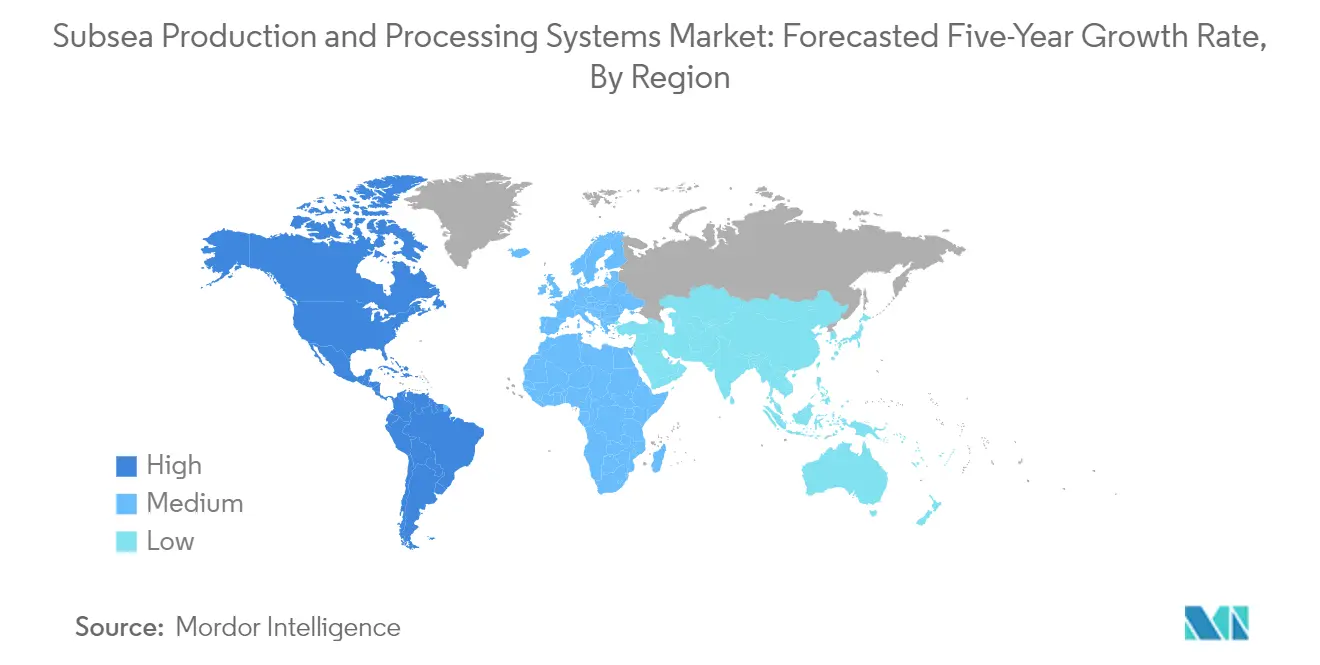

Subsea Production and Processing System Market in North America

The North American subsea systems market, accounting for approximately 16% of the global market share in 2024, is primarily driven by extensive activities in the Gulf of Mexico. The region's market dynamics are significantly influenced by the United States' strategic focus on offshore energy development, particularly through the five-year proposal for offshore hydrocarbon development in existing production areas. The market is characterized by continuous technological advancements in deepwater exploration and production capabilities, with major operators implementing cutting-edge subsea processing systems. The presence of established industry players and robust subsea infrastructure support has created a conducive environment for market growth. Environmental regulations and safety standards continue to shape investment decisions and operational strategies in the region. The market also benefits from ongoing efforts to enhance recovery rates from mature fields through advanced subsea processing systems. Despite the growing focus on renewable energy, the subsea sector remains crucial for energy security and economic development in North America.

Subsea Production and Processing System Market in Europe

The European subsea systems market has demonstrated resilience with approximately 0.4% growth from 2019 to 2024, primarily driven by activities in the North Sea region. The market landscape is characterized by a strong focus on technological innovation and sustainable development practices, particularly in Norway and the United Kingdom. European operators are increasingly investing in advanced subsea equipment solutions to maximize recovery from mature fields while minimizing environmental impact. The region's market is distinguished by its stringent regulatory framework and high environmental standards, which have fostered the development of more efficient and environmentally conscious subsea technology. Collaboration between industry players and research institutions has resulted in breakthrough innovations in subsea processing capabilities. The market benefits from well-established infrastructure and a skilled workforce, supporting complex subsea operations. Integration of digitalization and automation in subsea systems has become a key trend, enhancing operational efficiency and safety standards across the region.

Subsea Production and Processing System Market in Asia-Pacific

The Asia-Pacific subsea systems market is projected to grow at approximately 4% during 2024-2029, driven by increasing offshore exploration and production activities. The region's market is characterized by rapid technological adoption and growing investment in deepwater projects, particularly in countries like China, India, and Australia. Rising energy demand and the push for energy security have catalyzed offshore development activities across the region. The market benefits from increasing collaboration between national oil companies and international technology providers, facilitating knowledge transfer and technological advancement. Local manufacturing capabilities for subsea equipment are expanding, reducing dependency on imports and creating a more robust supply chain. Government initiatives supporting offshore exploration and development have created a favorable environment for market growth. The region's diverse geological conditions have necessitated the development of customized subsea solutions, driving innovation in the sector.

Subsea Production and Processing System Market in South America

The South American subsea production and processing system market is predominantly driven by Brazil's extensive offshore operations, particularly in the pre-salt areas. The region's market is characterized by significant investments in deepwater and ultra-deepwater projects, with a strong focus on technological advancement in subsea processing systems capabilities. National oil companies play a crucial role in market development, often partnering with international technology providers to enhance operational capabilities. The market benefits from continuous exploration activities and new field discoveries, creating sustained demand for subsea systems. Local content requirements have fostered the development of domestic manufacturing capabilities, strengthening the regional supply chain. The adoption of advanced subsea technologies has been crucial in optimizing production from challenging deepwater environments. Regulatory frameworks supporting offshore development have created a stable environment for long-term investments in the sector.

Subsea Production and Processing System Market in Middle East & Africa

The Middle East & Africa subsea production and processing system market is experiencing significant transformation driven by increased offshore exploration and development activities. The region's market is characterized by a growing focus on subsea technology adoption, particularly in countries like Saudi Arabia and the United Arab Emirates. National oil companies are increasingly investing in subsea infrastructure to enhance offshore production capabilities and maintain their competitive position in global energy markets. The market benefits from technological partnerships with international players, facilitating the adoption of advanced subsea solutions. Local manufacturing capabilities are expanding, supported by government initiatives to increase domestic content in the oil and gas sector. The region's diverse offshore environments have necessitated the development of specialized subsea solutions, driving innovation in the sector. Growing focus on gas development projects has created new opportunities for subsea processing systems deployment.

Competitive Landscape

Top Companies in Subsea Production and Processing System Market

The market is dominated by established players like Aker Solutions ASA, Baker Hughes Company, Halliburton Company, National Oilwell Varco Inc., Schlumberger Limited, and Oceaneering International. These companies are heavily investing in technological innovations, particularly in developing advanced subsea systems, processing systems, and digital solutions for remote operations. The industry has witnessed a strong focus on creating integrated subsea infrastructure solutions that combine production and processing capabilities while reducing environmental footprint. Companies are forming strategic alliances and joint ventures to pool technical resources and enhance their market presence, as exemplified by recent partnerships between major players like Aker Solutions, Schlumberger, and Subsea 7. Product development strategies are increasingly centered around creating configurable platforms and standardized solutions that offer flexibility for customization while maintaining cost efficiency.

Consolidated Market with Strong Global Players

The subsea production and processing system market exhibits a highly consolidated structure dominated by multinational corporations with extensive global footprints. These companies typically operate across the entire value chain, from equipment manufacturing to installation and maintenance services, giving them significant competitive advantages. The market has seen considerable consolidation through strategic mergers and acquisitions, with companies seeking to expand their technological capabilities and geographical reach. The high barriers to entry, including substantial capital requirements, technical expertise, and stringent regulatory compliance, have contributed to maintaining the oligopolistic nature of the market.

The competitive landscape is characterized by long-term relationships between suppliers and oil & gas operators, with contracts often spanning multiple years and involving comprehensive service agreements. Major players have established strong regional presences through local manufacturing facilities and service centers, particularly in key markets like the Middle East & Africa and Asia-Pacific. The industry has witnessed a trend toward vertical integration, with companies expanding their capabilities to offer end-to-end solutions, from front-end engineering to lifecycle services.

Innovation and Integration Drive Future Success

Success in the market increasingly depends on companies' ability to develop technologically advanced, cost-effective solutions while maintaining strong relationships with key stakeholders. Incumbent players are focusing on expanding their digital capabilities, developing all-electric subsea equipment systems, and improving the efficiency of their processing solutions to maintain their market positions. The ability to offer integrated solutions that combine multiple subsea technology functions while reducing installation and operational costs has become a crucial differentiator. Companies are also investing in research and development to address the growing demand for environmentally sustainable solutions and improved recovery rates from subsea wells.

For new entrants and smaller players, success lies in identifying and exploiting niche market segments or specialized technological solutions. The increasing focus on deepwater and ultra-deepwater exploration presents opportunities for companies with specialized expertise in these areas. The market's future will be shaped by the ability to adapt to evolving regulatory requirements, particularly regarding environmental protection and safety standards. Companies must also consider the concentration of buying power among major oil and gas operators, who often prefer established suppliers with proven track records. The development of alternative energy sources poses a long-term challenge, making it essential for companies to diversify their capabilities and adapt to changing market demands.

Subsea Production and Processing System Industry Leaders

Schlumberger Limited

Halliburton Company

Baker Hughes Company

Aker Solutions Asa

Oceaneering International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: One Subsea announced it had won a tender to provide the equipment for the Búziosfield in the Santos Basin pre-salt. The contract offers the delivery of 16 wet Christmas trees (ANMs) in phase 10 of the field's exploration.

- February 2023: Aker Solutions announced securing a contract from Eni Angola SpA. - Sucursal de Angola, an AzuleEnergy Holdings Limited subsidiary. The contract is to deliver the static and dynamic subsea umbilicals for the Agogo field development in offshore Angola.

- February 2023: TechnipFMC received a contract for subsea production systems by Equinor for Irpaoil and gas development on the Norwegian Continental Shelf. Under the contract, the company will likely supply and install support for subsea trees, control systems, structures, connections, and tooling.

Global Subsea Production and Processing System Market Report Scope

The subsea production and processing systems are deployed in wells situated on the seafloor, in shallow or deep water. Subsea processing emerged as a feasible option for fields in harsh environments where processing equipment on the water's surface may be jeopardized. It is generally termed a floating production system, where petroleum is extracted at the seabed. The same can be tied back to an existing production platform or an onshore facility.

The Subsea Production and Processing System market is segmented by a production system component (subsea trees, subsea umbilicals, risers, & flowlines, subsea wellhead, and others), processing system type (boosting, separation, injection, and gas compression), water depth (shallow water and deep and ultra-deepwater), and geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers the market size and forecasts for the global subsea production and processing system Market in revenue (USD) for all the above segments.

Production System Component

| Subsea Trees |

| Subsea Umbilicals, Risers, & Flowlines |

| Subsea Wellhead |

| Other |

Processing System Type

| Boosting |

| Separation |

| Injection |

| Gas Compression |

Water Depth

| Shallow Water |

| Deepwater and Ultra-Deepwater |

Geography

| North America |

| Europe |

| Asia-Pacific |

| South America |

| Middle-East and Africa |

| Production System Component | Subsea Trees |

| Subsea Umbilicals, Risers, & Flowlines | |

| Subsea Wellhead | |

| Other | |

| Processing System Type | Boosting |

| Separation | |

| Injection | |

| Gas Compression | |

| Water Depth | Shallow Water |

| Deepwater and Ultra-Deepwater | |

| Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle-East and Africa |

Key Questions Answered in the Report

How big is the Subsea Production and Processing System Market?

The Subsea Production and Processing System Market size is expected to reach USD 21.63 billion in 2025 and grow at a CAGR of 8.51% to reach USD 32.53 billion by 2030.

What is the current Subsea Production and Processing System Market size?

In 2025, the Subsea Production and Processing System Market size is expected to reach USD 21.63 billion.

Who are the key players in Subsea Production and Processing System Market?

Schlumberger Limited, Halliburton Company, Baker Hughes Company, Aker Solutions Asa and Oceaneering International Inc. are the major companies operating in the Subsea Production and Processing System Market.

Which is the fastest growing region in Subsea Production and Processing System Market?

Middle-East and Africa is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Subsea Production and Processing System Market?

In 2025, the Middle East and Africa accounts for the largest market share in Subsea Production and Processing System Market.

What years does this Subsea Production and Processing System Market cover, and what was the market size in 2024?

In 2024, the Subsea Production and Processing System Market size was estimated at USD 19.79 billion. The report covers the Subsea Production and Processing System Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Subsea Production and Processing System Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: