Global Point Of Care Diagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

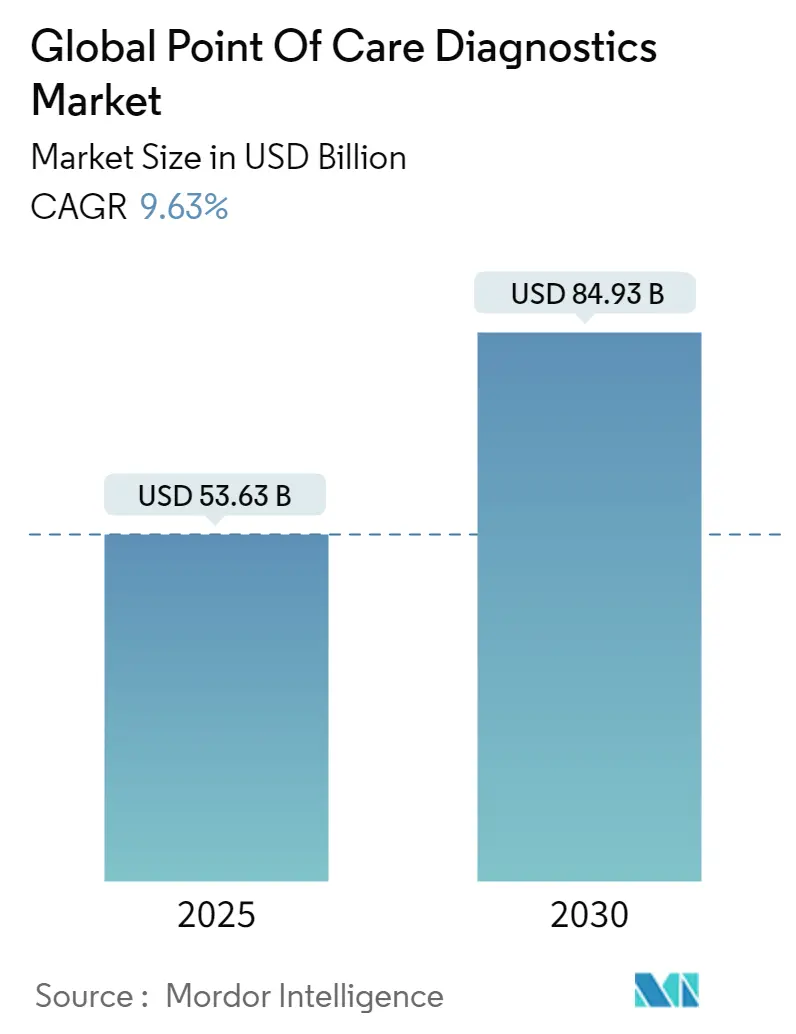

| Market Size (2025) | USD 53.63 Billion |

| Market Size (2030) | USD 84.93 Billion |

| Growth Rate (2025 - 2030) | 9.63% CAGR |

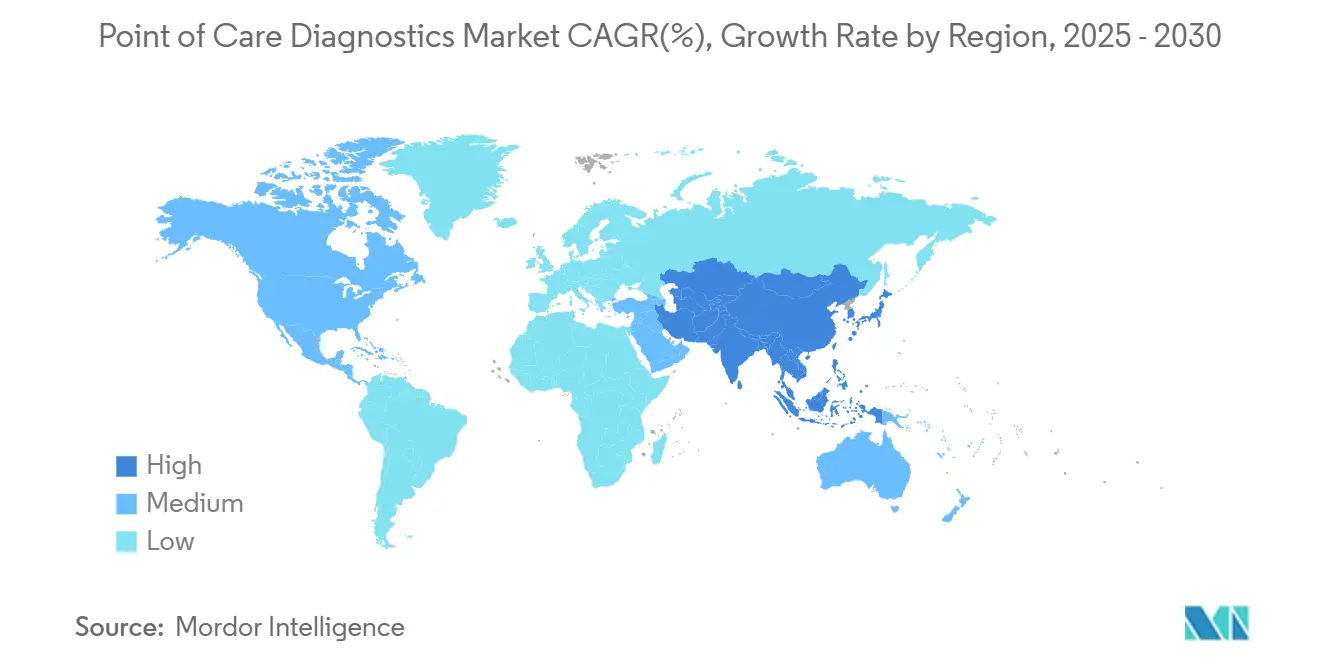

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Point Of Care Diagnostics Market Analysis by Mordor Intelligence

The Global Point Of Care Diagnostics Market size is estimated at USD 53.63 billion in 2025, and is expected to reach USD 84.93 billion by 2030, at a CAGR of 9.63% during the forecast period (2025-2030).

The steady growth reflects an industry shift toward immediate, near-patient testing that trims time-to-treatment and lowers overall care costs. Decentralized testing, miniaturized electronics, and smartphone connectivity are converging to drive adoption across both clinical and home settings. Market leaders continue to invest in four-in-one molecular respiratory panels, Bluetooth-enabled glucose sensors, and handheld cardiac biomarker readers—all technologies that improve decision speed and broaden access. Regional performance varies: North America leverages mature reimbursement and robust R&D, whereas Asia-Pacific benefits from expanding health coverage and a rising chronic disease burden. Competitive intensity is accelerating as approvals for multiplex molecular cartridges shorten development cycles, while phased Laboratory Developed Test (LDT) rules favor firms with strong quality systems.

Key Report Takeaways

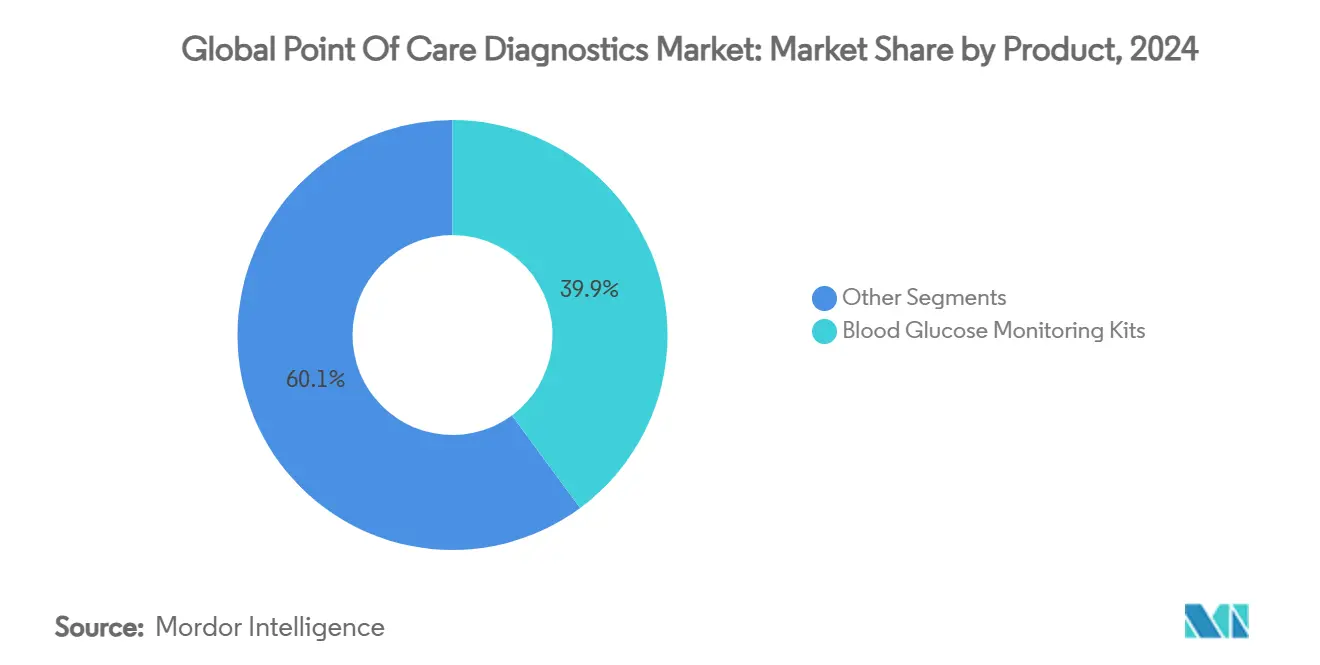

- By product category, Blood Glucose Monitoring Kits held 39.9% of point-of-care diagnostics market share in 2024; Infectious Disease Testing Kits are projected to advance at a 10.1% CAGR to 2030.

- By platform, Lateral Flow Assays led with 32.4% revenue share in 2024, while Molecular Diagnostics platforms are forecast to post the highest 11.8% CAGR through 2030.

- By sample type, blood specimens accounted for 68.15% of the point-of-care diagnostics market size in 2024; nasal/throat swab specimens are poised to grow at a 10.7% CAGR between 2025-2030.

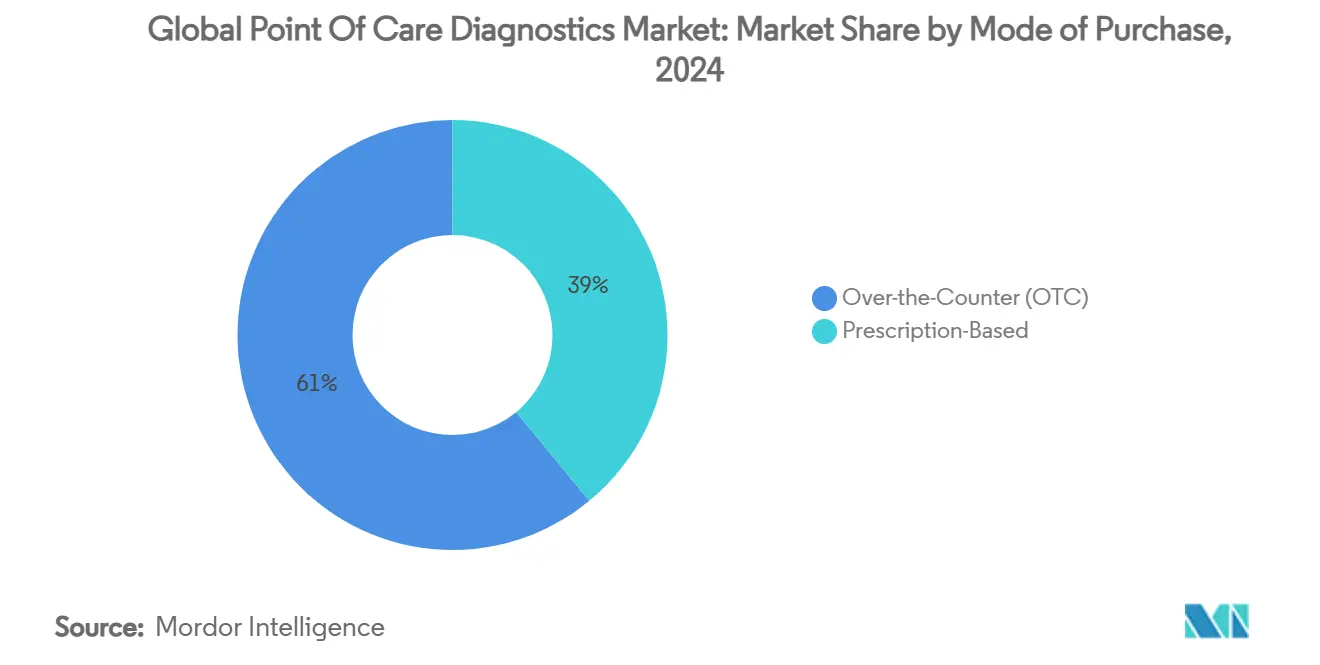

- By mode of purchase, OTC products commanded 60.98% share of the point-of-care diagnostics market in 2024; prescription-based kits record a projected 11.09% CAGR to 2030.

- By end user, hospitals & clinics represented 47.7% market share in 2024, while home-care settings expand at a 10.3% CAGR to 2030.

- By geography, North America retained 43.6% revenue share in 2024; Asia-Pacific is forecast to exhibit the fastest 10.67% CAGR through 2030.

Global Point Of Care Diagnostics Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Glucose Self-Management Becoming a Standard of Care in diabetes | +2.1% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Surge in CLIA-Waived Molecular POC Platforms for Respiratory Pathogens | +2.8% | North America and Europe, limited in Asia-Pacific | Short term (1-2 years) |

| Rising Prevalence of Chronic and Infectious Diseases | +1.7% | Global, highest impact in Asia-Pacific and emerging markets | Long term (4-6 years) |

| Increasing Number of Regulatory Approvals for Novel Immunoassay Techniques | +1.4% | North America leading, Europe following, Asia-Pacific emerging | Medium term (3-5 years) |

| Technological Advancements and Rising Usage of Home-based POC Devices | +2.3% | Global, highest adoption in developed markets | Medium term (2-5 years) |

| National Newborn Screening Mandates Accelerating Bedside Bilirubin Testing in Europe | +0.4% | Europe-specific, potential expansion to other developed regions | Short term (1-3 years) |

Source: Mordor Intelligence

Glucose Self-Management Becoming a Standard of Care in Diabetes

Continuous glucose monitoring is moving from clinic to consumer wearables as leading systems pair real-time data with GLP-1 therapy to enhance glycemic control. Abbott’s FreeStyle Libre portfolio, when used with GLP-1 drugs, delivered an additional 1.5% HbA1c reduction over six months, demonstrating the clinical benefit of integrated monitoring[1]Abbott Content Team, “Abbott Enters U.S. Consumer Biowearables Market With Lingo and Libre Rio,” abbott.com . Academic groups are fast-tracking non-invasive optics; RMIT University’s infrared sensor pinpoints glucose across four discrete wavelengths, eliminating fingersticks [2]Science X, “Continuous Non-Invasive Glucose Sensing on the Horizon With the Development of a New Optical Sensor,” phys.org. Early-stage trials in Raman spectroscopy, in-ear PPG, and magnetohydrodynamic fluidics reaffirm strong correlation to capillary values, signaling a move toward painless, always-on monitoring that boosts adherence and supports population-level diabetes management.

Surge in CLIA-Waived Molecular POC Platforms for Respiratory Pathogens

Syndromic PCR cartridges that detect SARS-CoV-2, Influenza A/B, and RSV in 20 minutes are reshaping triage workflows. Roche’s cobas liat quad-plex panel received EUA and cut antiviral initiation delays, with 99% of influenza-positive patients treated at first encounter. Interfacing these devices with cloud dashboards turns once-isolated tests into networked infection-surveillance nodes, improving bed management during peak respiratory seasons.

Rising Prevalence of Chronic and Infectious Diseases

Global diabetes cases reached 537 million adults in 2024, intensifying demand for reliable glucose self-testing solutions doi.org. Simultaneously, resurging infectious threats such as syphilis—up 80% in the United States between 2018-2022—drive rapid serology kit uptake; Labcorp’s First to Know OTC test offers a 15-minute self-screen option that facilitates immediate care linkage. These parallel disease burdens anchor sustained growth in the point-of-care diagnostics market.

Increasing Number of Regulatory Approvals for Novel Immunoassay Techniques

The U.S. FDA cleared the first at-home syphilis antibody assay and the first POC Hepatitis C RNA test, providing blueprints for future rapid immunoassays that compress diagnosis and treatment into a single visit [3]U.S. Food and Drug Administration, “FDA Permits Marketing of First Point-of-Care Hepatitis C RNA Test,” fda.gov . Fast-track pathways reduce uncertainty, encouraging device makers to invest in multiplex cartridges targeting antimicrobial resistance and sexually transmitted infections.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product Recalls | -1.0% | Global, highest visibility in North America | Short term (immediate-2 years) |

| Stringent Regulatory Policies and Reimbursement Issues | -1.8% | Highest in North America, moderate in Europe, lower in Asia-Pacific | Long term (3-6 years) |

| Quality-Control Non-Compliance Penalties in US Physician-Office Labs | -0.7% | US-specific, potential spillover to other markets | Medium term (2-4 years) |

| Supply-Chain Cold-Chain Gaps for Molecular Cartridges in Africa | -0.3% | Africa and emerging markets with limited infrastructure | Long term (4-7 years) |

Source: Mordor Intelligence

Product Recalls

In 2024 Abbott identified three FreeStyle Libre 3 sensor lots that over-reported high glucose values, prompting a voluntary correction and temporary market disruption. Recall visibility influences prescribers’ brand trust and forces contingency testing, muting near-term growth despite overall demand.

Stringent Regulatory Policies and Reimbursement Issues

The July 2024 LDT final rule reclassifies all in-vitro diagnostics as medical devices, initiating a five-phase roll-in from adverse-event reporting to full premarket review over four years. Compliance costs rise as CLIA fee hikes and personnel standards add operational overhead, while payers lag in defining codes for novel multiplex panels, stretching reimbursement timelines.

Segment Analysis

By Product: Glucose Monitoring Leads, Infectious Disease Kits Accelerate

Blood Glucose Monitoring Kits retained 39.87% of point-of-care diagnostics market share in 2024, buoyed by the worldwide diabetes epidemic. Continuous sensors and connected meters keep sales resilient, with the point-of-care diagnostics market size for glucose monitoring expected to expand steadily alongside type 2 diabetes incidence. Infectious Disease Testing Kits posted the fastest 10.1% CAGR outlook for 2025-2030, propelled by four-pathogen respiratory panels and at-home syphilis antibody tests. The FDA authorization of the First to Know Syphilis Test underscores regulatory support for consumer infectious-disease self-screening, accelerating segment momentum.

Demand is also diversifying: multiplex molecular strips now blend bacterial, viral, and fungal targets, letting primary-care clinics manage differential diagnoses on-site. Product pipelines show convergence, with companies integrating cardiac troponin, HbA1c, and CRP into comprehensive metabolic and sepsis panels that fit the same palm-sized reader, extending lifetime value per instrument.

Note: Segment shares of all individual segments available upon report purchase

By Platform: Molecular Diagnostics Upsets Lateral Flow Dominance

Lateral Flow Assays captured 32.4% revenue in 2024 thanks to low unit cost and easy distribution, yet their market weight is gradually ceding ground. Molecular platforms—projected at 11.8% CAGR—extend sensitivity, vital for variant-prone viruses and low-copy pathogens. The point-of-care diagnostics market size for molecular cartridges is forecast to double this decade as pharmacies adopt CLIA-waived analyzers.

Manufacturers focus on higher multiplex density without compromising run-time. QuidelOrtho’s Savanna console delivers PCR-grade accuracy from a single swab in 25 minutes, matching clinic cycle times. Meanwhile, cloud-linked analyzers push auto-result posting into electronic medical records, creating fertile ground for population-level antimicrobial stewardship dashboards.

By Sample Type: Blood Remains Cornerstone, Respiratory Specimens Surge

Blood-based assays comprised 68.15% of 2024 revenue, covering glucose, lipids, cardiac markers, and hemoglobin variants. Innovation now centers on capillary micro-volume handling and room-temperature whole-blood chemistry, minimizing preprocessing. Yet respiratory specimens are the growth story: nasal/throat swabs carry a 10.7% CAGR through 2030 as syndromic panels expand.

Self-collection kits broaden sampling beyond clinics—BD’s HPV solution lets women obtain vaginal samples in pharmacies, powering high-throughput molecular screening programs. Simultaneously, spin-disk microfluidics from SpinChip produce quantitative results out of fingerprick blood in 10 minutes, tightening links between sampling, analysis, and treatment.

By Mode of Purchase: OTC Channels Reshape Access

OTC products held 60.98% revenue share in 2024, reflecting stronger patient agency and retail clinic expansion. Chain pharmacies stock pregnancy, glucose, cholesterol, and rapid infection tests on adjacent shelves, making the point-of-care diagnostics market an everyday consumer category. Prescription kits, however, are set to outpace with 11.09% CAGR as molecular test complexity warrants professional interpretation and insurer coverage.

Regulatory shifts encourage OTC migration of once-clinical assays. Abbott’s Lingo CGM and Roche’s forthcoming at-home HPV test highlight the blurred boundary between consumer health and clinical diagnostics. Meanwhile, digital companion apps guide lay users in specimen collection, reducing invalid tests and building real-time epidemiological datasets.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals & Clinics Lead, Home-Care Gains Speed

Hospitals and clinics managed 47.7% of 2024 revenues, where immediate triage value justifies premium cartridges. Emergency departments rely on eight-minute troponin readers to rule out myocardial infarction and release low-risk patients sooner, cutting bed occupancy. In parallel, home-care settings grow at 10.3% CAGR as payers incentivize remote supervision. The point-of-care diagnostics market size for home testing devices climbs with broadband telehealth adoption.

Integration with smartphones and cloud dashboards enables virtual coaching. Libre Rio transmits CGM data straight into provider portals, while electrical-sensing blood analyzers schedule refill prompts when chronic-care labs exceed thresholds—mechanisms that align with value-based reimbursement

Geography Analysis

North America commands 43.6% of 2024 revenue, underpinned by policy initiatives, robust venture backing, and early-adopter health systems. The final LDT rule reshapes investment calculus; firms that already handle Medical Device Reporting glide through phase-in stages, consolidating competitive advantage. Strategic M&A—BD’s USD 4.2 billion Critical Care acquisition—adds AI-enabled monitors that feed real-time alerts to intensivists, marrying analytics with bedside diagnostics.

Asia-Pacific is the fastest climber, forecast at a 10.67% CAGR. Health ministries in India, China, and Southeast Asia are scaling remote vital-sign hubs to offset clinician shortages. Investment projections of USD 138 billion by 2027 in regional life-sciences infrastructure spur local cartridge manufacturing, reducing import dependency. Public-private collaborations—such as BD’s cervical cancer partnership with Kenya’s Ministry of Health—show how multinationals tailor solutions for resource-limited environments, often leapfrogging legacy lab models.

Europe balances stringent regulation with technological depth. CE-marked cobas 6800/8800 2.0 systems boost throughput by optimizing walk-away times, letting central labs handle surges without staff increases. Additionally, CE approvals for Bluetooth-enabled cardiac monitors extend arrhythmia surveillance for six years, aligning with EU digital-health reimbursement frameworks. In the Middle East and Africa, infection diagnostics dominate donor funding, while South America sees rising awareness of early cancer screening. Supply-chain cold-chain gaps persist, but rooftop solar refrigeration pilots in Nigeria indicate pathways to stabilize PCR reagent logistics.

Competitive Landscape

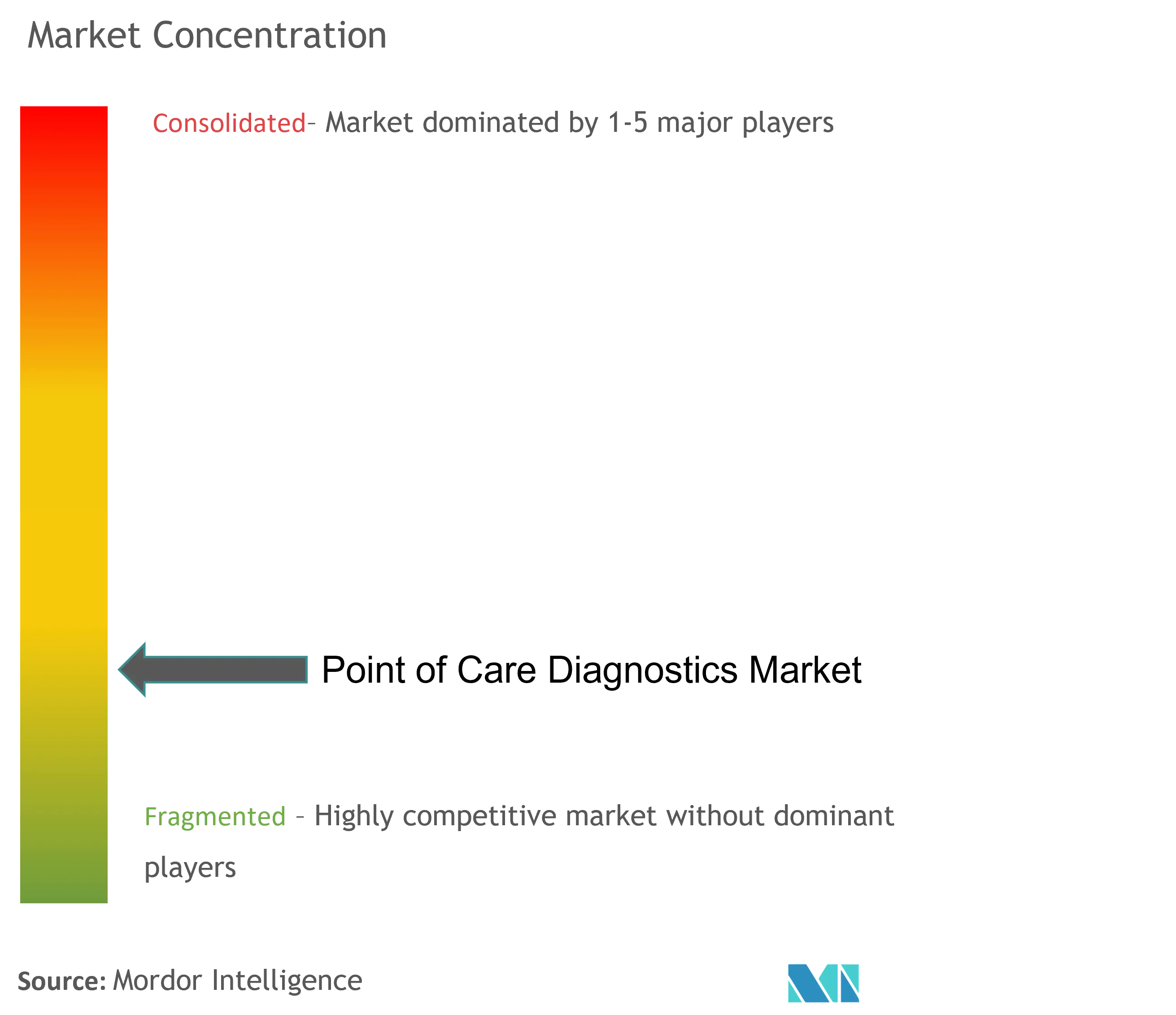

The point-of-care diagnostics market shows moderate concentration. Abbott, Roche, Siemens Healthineers, and Danaher’s Cepheid division together hold an estimated upper-medium share, while dozens of specialists compete in niche assays. Larger firms leverage scale and regulatory muscle; Roche’s USD 350 million purchase of LumiraDx’s platform expands its decentralized menu from coagulation to COVID-19.

Technology remains the key differentiator. Siemens Healthineers’ handheld high-sensitivity troponin device shrinks diagnosis time to eight minutes using magnetic nanoparticles while keeping lab-grade precision. bioMérieux’s acquisition of SpinChip brings centrifugal microfluidics that return immunoassay results from fingerstick blood within 10 minutes, broadening the firm’s sepsis and antimicrobial stewardship offerings

Partnerships with digital-health players multiply value. Chronus Health integrates machine-learning edge analytics, enabling electrical-sensing chips to classify analytes without optics or reagents. QuidelOrtho’s revamped R&D leadership signals a push toward broader multiplex menus across both immunoassay and molecular domains, a move expected to intensify competition among mid-tier innovators.

Global Point Of Care Diagnostics Industry Leaders

-

F. Hoffmann-La Roche Ltd

-

Abbott Laboratories

-

Siemens Healthineers AG

-

Becton, Dickinson and Company

-

Qiagen Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: bioMérieux acquired SpinChip Diagnostics for EUR 138 million to strengthen its 10-minute whole-blood immunoassay platform.

- January 2025: Beckman Coulter Diagnostics introduced new RUO blood-based biomarker immunoassays for neurodegenerative disease research.

- May 2025: Roche received FDA Breakthrough Device Designation for its Elecsys pTau217 plasma biomarker test to aid early Alzheimer’s diagnosis.

- December 2024: Roche secured CE Mark for updated cobas 6800/8800 systems 2.0 that increase laboratory throughput.

Global Point Of Care Diagnostics Market Report Scope

As per the scope of the report, point of care (POC) diagnostics have many advantages over traditional methods as it allows patient diagnosis at different places other than only hospitals and clinics, including remote areas, such as in the physician's office, an ambulance, the home, the field, or in the hospital.

The Point of care Diagnostics Market is segmented by Product (Glucose Monitoring Kit, Cardio-metabolic Monitoring Kit, Pregnancy and Fertility Testing Kit, Infectious Disease Testing Kit, Cholesterol Test Strip, Hematology Testing Kit, and Other Products), End-User (Hospital and Critical Care Setting, Ambulatory Care Setting, Research Laboratory, and Others) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Product | Glucose Monitoring Kits | ||

| Infectious Disease Testing Kits | |||

| Cardiometabolic (Cardiac Marker) Testing Kits | |||

| Coagulation Monitoring Kits | |||

| Pregnancy & Fertility Testing Kits | |||

| Blood Gas / Electrolyte & Metabolite Testing Kits | |||

| Hematology Testing Kits | |||

| Tumor / Cancer Marker Testing Kits | |||

| Urinalysis Testing Kits | |||

| Cholesterol Test Strips | |||

| By Platform | Lateral Flow Assays | ||

| Dipsticks & Test Strips | |||

| Microfluidics-Based Platforms | |||

| Immunoassays (CLIA & FIA) | |||

| Molecular Diagnostics (PCR, INAAT) | |||

| By Sample Type | Blood | ||

| Urine | |||

| Saliva | |||

| Nasal / Throat Swab | |||

| Other Specimens (Sweat, Tear, CSF) | |||

| By Mode of Purchase | Over-the-Counter (OTC) | ||

| Prescription-Based | |||

| By End User | Hospitals & Clinics | ||

| Home-Care Settings | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Glucose Monitoring Kits |

| Infectious Disease Testing Kits |

| Cardiometabolic (Cardiac Marker) Testing Kits |

| Coagulation Monitoring Kits |

| Pregnancy & Fertility Testing Kits |

| Blood Gas / Electrolyte & Metabolite Testing Kits |

| Hematology Testing Kits |

| Tumor / Cancer Marker Testing Kits |

| Urinalysis Testing Kits |

| Cholesterol Test Strips |

| Lateral Flow Assays |

| Dipsticks & Test Strips |

| Microfluidics-Based Platforms |

| Immunoassays (CLIA & FIA) |

| Molecular Diagnostics (PCR, INAAT) |

| Blood |

| Urine |

| Saliva |

| Nasal / Throat Swab |

| Other Specimens (Sweat, Tear, CSF) |

| Over-the-Counter (OTC) |

| Prescription-Based |

| Hospitals & Clinics |

| Home-Care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the point-of-care diagnostics market?

The market is valued at USD 53.63 billion in 2025 and is projected to reach USD 84.93 billion by 2030.

Which product segment leads the point-of-care diagnostics market?

Blood Glucose Monitoring Kits lead, holding 39% market share in 2024 as continuous sensors anchor diabetes management.

Which region shows the fastest growth?

Asia-Pacific is the fastest-growing region, forecast at a 10.67% CAGR for 2025-2030.

What is driving the shift toward home-based testing?

Healthcare decentralization, patient preference, and connected devices like Abbott’s new CGMs support a 10.3% CAGR for home-care settings.

How are new regulations affecting the market?

The FDA’s phased LDT rule increases compliance demands but clarifies approval pathways, favoring companies with established quality systems and accelerating innovation.

Page last updated on: July 11, 2025