Market Overview

| Study Period | 2019 - 2030 |

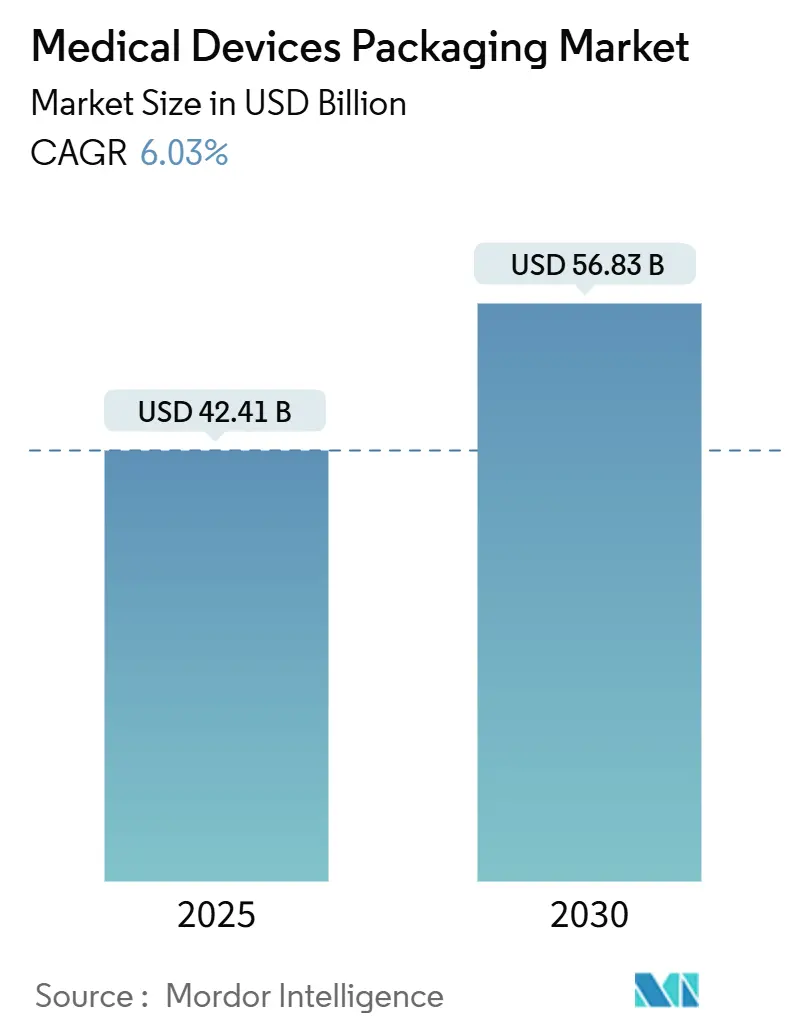

| Market Size (2025) | USD 42.41 Billion |

| Market Size (2030) | USD 56.83 Billion |

| Growth Rate (2025 - 2030) | 6.03% CAGR |

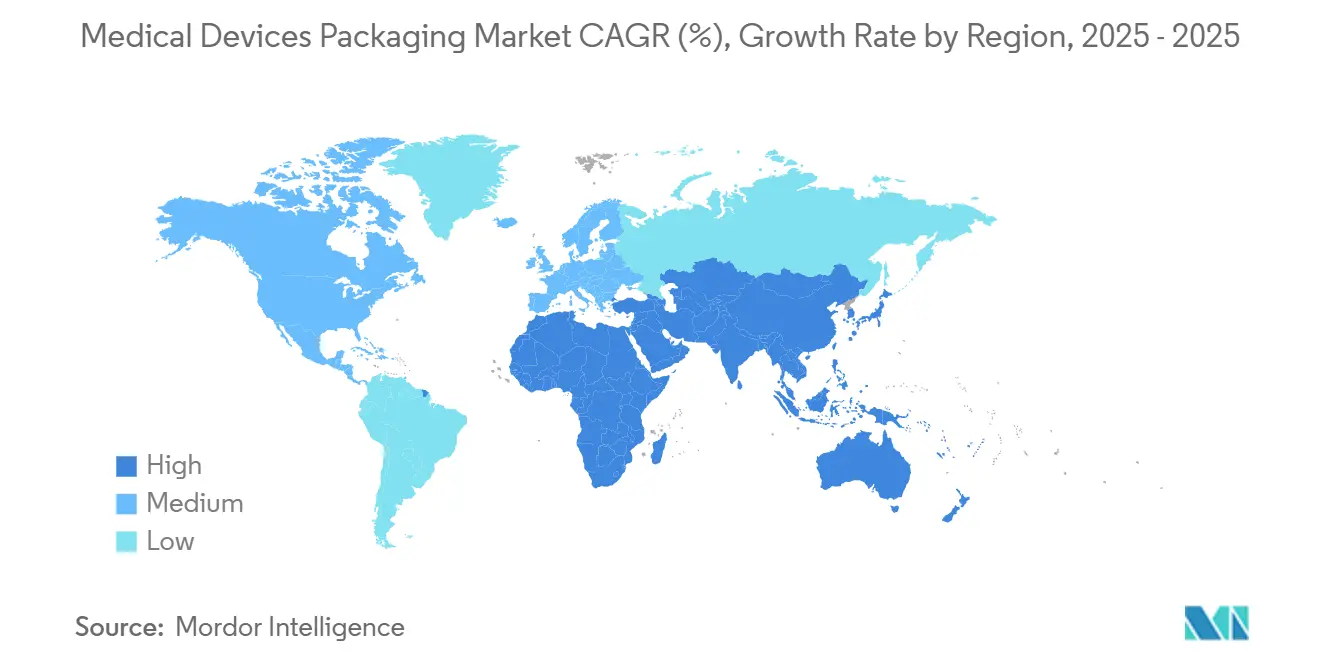

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Devices Packaging Market Analysis by Mordor Intelligence

The medical device packaging market size is USD 42.41 billion in 2025 and is forecast to reach USD 56.83 billion by 2030, advancing at a 6.03% CAGR. This momentum is underpinned by tighter sterility standards, rapid adoption of smart-label technologies, and a steady pipeline of minimally invasive and wearable devices that demand high-performance barrier formats. Material innovation remains a core growth lever because polymers such as cyclic olefin copolymers and liquid-crystal polymers withstand high-temperature sterilization while enabling RFID integration. Contract sterilization networks continue to expand, which raises demand for standardized primary packs that perform consistently across multiple facilities. At the same time, raw-material cost volatility and limited ethylene oxide capacity are forcing converters to redesign packs for alternative sterilization methods, creating both cost pressures and innovation windows. Geographically, North America preserves market leadership yet Asia-Pacific delivers the fastest incremental revenue, thanks to hospital build-outs in China and India and policy-backed local manufacturing.

Key Report Takeaways

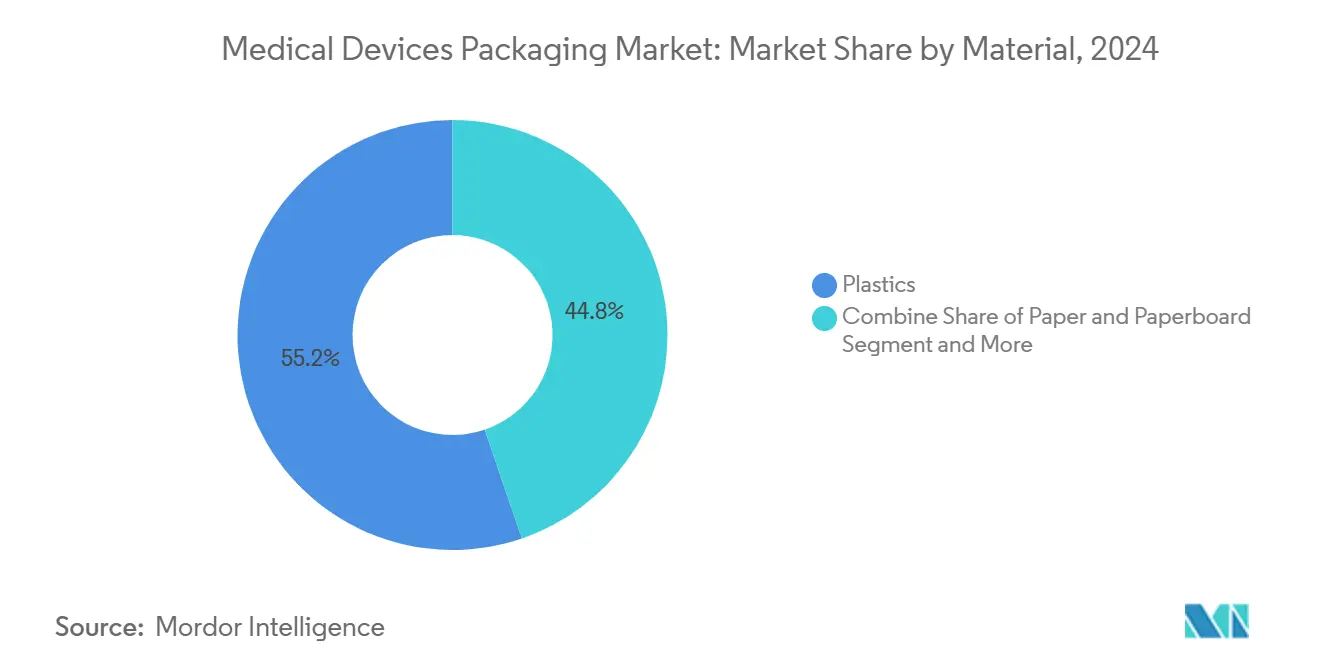

- By material, plastics captured 55.23% of the medical device packaging market share in 2024 while bio-enhanced grades lifted the segment to an 8.22% CAGR through 2030.

- By product type, pouches and bags led with 36.32% revenue share in 2024; boxes and cartons are projected to expand at a 9.32% CAGR to 2030.

- By application, sterile packaging accounted for a 66.23% share of the medical device packaging market size in 2024 and is advancing at an 8.78% CAGR.

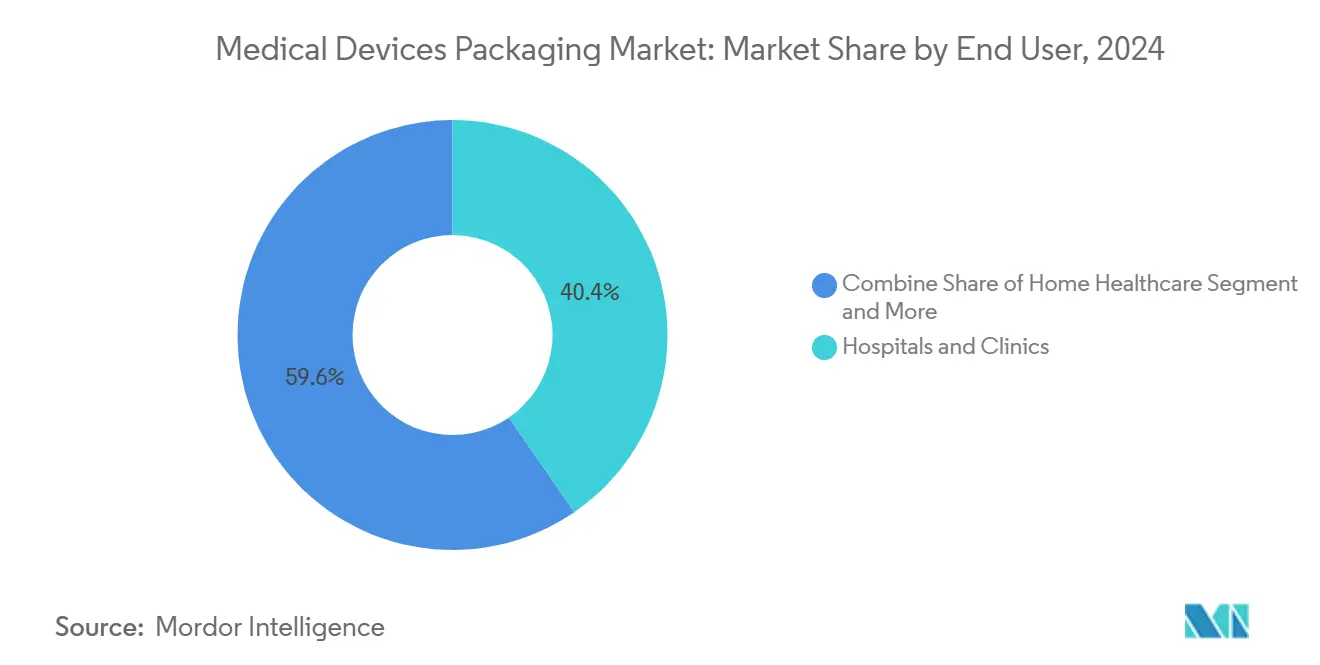

- By end user, hospitals and clinics held 40.43% share in 2024, whereas contract manufacturing and sterilization organizations are set to grow at a 10.32% CAGR.

- By packaging level, primary packs dominated with 52.12% share in 2024, while tertiary formats post the highest 8.12% CAGR on the back of longer global supply routes.

- By geography, North America led with 35.43% share in 2024; Asia-Pacific exhibits the quickest 10.83% CAGR through 2030.

Global Medical Devices Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for extended-shelf-life formats | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Growth in minimally-invasive and wearable devices | +1.5% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Stricter global sterility regulations (ISO 11607, EU MDR, FDA) | +0.8% | Global, with immediate impact in EU and North America | Short term (≤ 2 years) |

| Integration of RFID/UDI smart-label traceability | +0.6% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Carbon-footprint disclosure pushing mono-materials | +0.4% | EU-led, expanding to North America and APAC | Long term (≥ 4 years) |

| Expansion of outsourced contract sterilization networks | +0.9% | Global, with rapid growth in APAC | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising Demand for Extended-Shelf-Life Formats

Healthcare providers want devices that remain usable for five to seven years because pandemic preparedness and rural outreach stretch replenishment cycles. Barrier films incorporating ethylene vinyl alcohol and metallized polyester now deliver that longevity, and DuPont’s 2025 Costa Rica expansion—adding 16,000 ft² solely for sterile Tyvek packs—underscores the global push for superior barriers. Accelerated-aging and real-time stability protocols are becoming routine, shifting material choice toward premium polymers despite higher purchase prices.

Growth in Minimally-Invasive and Wearable Devices

New laparoscopic tools and connected wearables feature complex geometries and sensitive electronics that require gentle yet sterile containment. Thermoformed trays with custom cavities dominate for small surgical sets, whereas flexible pouches embedded with temperature-sensitive inks suit smart patches destined for home use. Packaging scientists are also mitigating adhesive migration to ensure skin safety for wearable sensors, a challenge cited by device integrators interviewed across APAC clinics.

Stricter Global Sterility Regulations

Revised ISO 11607 test batteries and the European Union Medical Device Regulation now oblige comprehensive seal-strength and microbial-barrier verification. A 2024 FDA alert following joint-implant oxidation linked to defective packs reinforced regulator focus on oxygen ingress. [1]Food and Drug Administration, “Risks: Exactech Joint Replacement Devices With Defective Packaging,” fda.govManufacturers consequently invest in in-house validation labs, which raises CapEx yet speeds approvals for next-generation barrier systems.

Integration of RFID/UDI Smart-Label Traceability

UDI mandates compel device makers to embed electronic identifiers that survive sterilization and distribution. RFID-enabled primary packs now track temperature excursions, vibration, and humidity in real time, a capability gaining traction as China’s device market heads toward USD 210 billion by 2025. [2]Cambridge Network, “Insights Into China’s Medical Device Market for 2025,” cambridgenetwork.co.uk Blockchain pilots further deter counterfeits, offering brand holders immutable provenance records.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory compliance cost burden | -0.7% | Global, with highest impact in EU and North America | Short term (≤ 2 years) |

| Volatile medical-grade polymer prices | -1.1% | Global, with severe impact in cost-sensitive APAC markets | Short term (≤ 2 years) |

| Scarcity of bio-based and PCR resins | -0.5% | Global, with acute impact in EU due to sustainability mandates | Medium term (2-4 years) |

| Cold-chain e-commerce seal-failure recalls | -0.3% | Global, with concentration in North America and EU e-commerce | Short term (≤ 2 years) |

Source: Mordor Intelligence

Regulatory Compliance Cost Burden

Validation outlays have risen 25-30% under the EU MDR because each pack configuration must pass biocompatibility, accelerated-aging, and distribution-simulation batteries. Smaller converters are consolidating platforms to curb test repetition, yet this can compromise application fit. The complexity fuels a niche consulting segment that guides dossier compilation at premium fees.

Volatile Medical-Grade Polymer Prices

Medical-grade polyethylene and polypropylene have risen 15-20% since 2024 amid supply dislocations and refinery curtailments. Post-consumer recycled resin remains scarce, making sustainable pledges costlier to fulfill. Companies respond with multi-year offtake agreements that lock pricing but tie up working capital, an acute pain point for mid-tier converters across Southeast Asia.

Segment Analysis

By Material: Plastics Dominate Through Innovation

Plastics retained 55.23% of the medical device packaging market in 2024, and the segment leads growth with an 8.22% CAGR through 2030. Advanced polymers such as cyclic olefin copolymers enable steam and plasma sterilization without warping, whereas liquid-crystal polymers support smart circuitry embedment. As a result, the medical device packaging market records steady migration away from legacy glass and metal for primary packs. Paperboard continues in secondary roles where cost efficiency trumps barrier performance. Bio-based plastics, though under 5% of volume, post double-digit expansion riding on hospital sustainability scorecards and Asia-Pacific’s emergence as a biopolymer hub.

Rising demand for multi-layer films that withstand gamma and e-beam sterilization fuels capital investment in co-extrusion lines across the United States and Malaysia. Polymer suppliers leverage vertical integration to guarantee medical-grade resin purity, positioning themselves as assured partners for validated barrier systems. These dynamics are expected to uphold plastics’ commanding share of the medical device packaging market through the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Pouches Lead While Boxes Accelerate

Pouches and bags delivered 36.32% of 2024 revenues owing to their versatility across single-use disposables and electronic catheters. However, kit complexity in orthopedic and cardiovascular interventions lifts demand for rigid boxes and cartons, causing this format to pace at a 9.32% CAGR. Consequently, multilayer cartons lined with Tyvek are gaining share where outer rigidity and inner sterility must coexist. Trays remain indispensable for delicate scopes, while thermoformed blisters secure small items such as diagnostic strips.

Third-party sterilizers increasingly request flat pouches equipped with optimized peelability that speeds operating-room presentation. In parallel, carton suppliers integrate transparent apertures so clinicians can verify instrument sets without breaking seals. These usability tweaks reinforce product-type diversification within the medical device packaging market.

By Application: Sterile Packaging Maintains Dominance

Sterile systems supplied 66.23% of 2024 revenue and grow 8.78% annually because every minimally invasive instrument and implant requires validated microbial barriers. Accelerated adoption of single-procedure kits intensifies volume, and active packs with oxygen scavengers now protect moisture-sensitive bio-electronics. Non-sterile formats, while smaller, retain utility for hospital durable equipment and diagnostic analyzers that undergo on-site disinfection.

Active and smart packs represent the fastest sub-segment. Embedded sensors confirm cold-chain compliance for battery-powered neuro-stimulators, improving patient safety and trimming recall exposure. These high-value features propagate quickly across the medical device packaging market as reimbursement models reward supply-chain traceability.

By End User: Hospitals Lead, Contract Organizations Surge

Hospitals and clinics consumed 40.43% of packaged devices in 2024 by virtue of direct procurement authority and surgical throughput. Yet contract manufacturing and sterilization organizations expand at a 10.32% CAGR, reflecting OEM outsourcing strategies that prioritize core R&D over capital-heavy packaging lines. Standardized pack formats enable these service providers to manage multi-customer loads efficiently, channeling volume growth back into the broader medical device packaging market.

Home-health adoption of wearable injectors also rises, prompting suppliers to design intuitive opening features and large-print instructions. Diagnostic centers demand tamper-evident cartons for contrast agents, further diversifying downstream requirements and spurring pack differentiation.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Level: Primary Focus, Tertiary Growth

Primary packs formed 52.12% of 2024 revenue because they guard device sterility throughout shelf life. They range from chevron pouches for sutures to rigid trays for cardiovascular stents, each requiring laser-coded lot details. Secondary packs assist global labeling obligations and logistics handling, whereas tertiary formats record an 8.12% CAGR as OEMs ship consolidated kits across continents.

Stackable corrugated shippers with edge-crush certification now dominate export flows from Vietnam and Costa Rica. Blockchain-ready parcel labels track shock events and temperature excursions, ensuring traceability until last-mile hospital receipt. Such tertiary upgrades add new value streams within the medical device packaging market.

Geography Analysis

North America led with 35.43% share in 2024, propelled by the United States’ robust device innovation base and FDA’s clear validation pathways. Canadian hospital-modernization programs boost demand for cost-effective packs, while Mexico’s maquiladora clusters integrate cross-border packaging lines that meet both FDA and COFEPRIS standards. Material circularity targets drive trial runs of recyclable high-density polyethylene film across several US hospital systems, initiatives supported by Amcor’s expanded closed-loop projects.

Asia-Pacific advances at a 10.83% CAGR, anchored by China, Japan, and India. China’s forecast USD 210 billion device market prompts label-localization investments and UDI-compliant printing, drawing converters into provincial hubs such as Suzhou. Japan’s ageing demographic multiplies the need for home-use kits preserved in long-life pouches, while India’s Make-in-India incentives attract joint ventures that erect extrusion and die-cutting capacity near Ahmedabad.

Europe remains mature yet innovation-driven. The EU MDR compels multi-language labeling and proof of recyclability, and Germany’s orthopedic cluster partners with packaging labs to prototype mono-material sterility systems. Post-Brexit divergence obliges dual certification for exporters targeting both EU and UK markets. The Middle East and Africa record steady gains as Gulf states commission new hospitals, whereas South America’s growth stems from Brazil’s domestic pacemaker lines that now source Tyvek trays from local converters.

Competitive Landscape

The medical device packaging market is fragmented but consolidation is accelerating as scale and regulatory breadth become decisive. Amcor completed an USD 8.4 billion stock merger with Berry Global in 2025, producing a healthcare-focused packaging titan with USD 24 billion annual revenue and USD 650 million synergy targets. DuPont deepened vertical integration through multiple component acquisitions, most recently Spectrum Plastics Group in 2025, which expands polymer-processing reach for specialty barrier packs. Sonoco sharpened its portfolio by divesting thermoformed and flexibles operations to Toppan for USD 1.8 billion, redirecting capital to high-growth performance hubs in India.

Technology leadership is now a competitive prerequisite. DuPont’s Costa Rica extension embeds ISO 11607 testing suites within production, accelerating customer validations for Tyvek-based systems. Emerging disruptors such as Viant Medical doubled revenue to nearly USD 1 billion after acquiring Integer’s Advanced Surgical and Orthopedics unit, offering OEMs design-through-package turnkey services. RFID and blockchain pilots differentiate full-service suppliers from commodity film extruders, and those without digital capabilities risk relegation to price-competing tiers.

White-space growth resides in bio-based substrates and thin-film barrier coatings that enable mono-material recyclability without compromising sterility. Start-ups fielding compostable films lure early-adopter European hospitals, while incumbents funnel R&D to balance sustainability with validated performance thresholds. The competitive race hinges on who brings compliant, data-rich, and low-carbon packs to scale fastest.

Medical Devices Packaging Industry Leaders

-

Amcor PLC

-

Wipak Group

-

Smurfit WestRock

-

Sonoco Products Company

-

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: DuPont expanded its Costa Rica healthcare plant by 16,000 ft², creating the region’s first sterile‐pack operation.

- February 2025: Pacur bought France-based Carolex SAS to strengthen European PETG sheet capacity for rigid medical packs.

- January 2025: DuPont completed its acquisition of Spectrum Plastics Group, adding polymer processing and device assembly competencies.

- July 2024: DuPont bought Donatelle Plastics for USD 313 million, expanding electrophysiology and drug-delivery specialties.

Global Medical Devices Packaging Market Report Scope

The study tracks the demand for major medical device packaging products, such as pouches, bags, trays, boxes, clamshells, and other products. The pricing for the raw material, that is, plastic, paper, and paperboard, is taken into consideration along with the consumption, import, and export trends, as well as average prices to arrive at the market revenue.

The medical devices packaging market is segmented by material type (plastic, paper and paper boards, and other material types), product type (pouches and bags, trays, boxes, clam shells, and other products), application (sterile packaging and non-sterile packaging), geography(North America [United States and Canada], Europe [United Kingdom, Germany, France, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], Latin America [Brazil, Argentina, and Rest of Latin America], Middle East, and Africa [United Arab Emirates, South Africa, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material | Plastics | |||

| Paper and Paperboard | ||||

| Metals and Foils | ||||

| Glass | ||||

| Bio-based Plastics | ||||

| By Product Type | Pouches and Bags | |||

| Trays | ||||

| Boxes and Cartons | ||||

| Blister Packs | ||||

| Other Product Types | ||||

| By Application | Sterile Packaging | |||

| Non-sterile Packaging | ||||

| Active / Smart Packaging | ||||

| By End User | Hospitals and Clinics | |||

| Diagnostic and Imaging Centers | ||||

| Home Healthcare | ||||

| Contract Manufacturing and Sterilization Orgs | ||||

| By Packaging Level | Primary | |||

| Secondary | ||||

| Tertiary | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Australia and New Zealand | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

By Material

| Plastics |

| Paper and Paperboard |

| Metals and Foils |

| Glass |

| Bio-based Plastics |

By Product Type

| Pouches and Bags |

| Trays |

| Boxes and Cartons |

| Blister Packs |

| Other Product Types |

By Application

| Sterile Packaging |

| Non-sterile Packaging |

| Active / Smart Packaging |

By End User

| Hospitals and Clinics |

| Diagnostic and Imaging Centers |

| Home Healthcare |

| Contract Manufacturing and Sterilization Orgs |

By Packaging Level

| Primary |

| Secondary |

| Tertiary |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the medical device packaging market?

The market stands at USD 42.41 billion in 2025 and is projected to grow to USD 56.83 billion by 2030.

Which material segment leads the medical device packaging market?

Plastics hold the lead with 55.23% share in 2024 and continue growing thanks to high-performance polymer adoption.

Why is Asia-Pacific the fastest-growing region?

Infrastructure expansion in China and India, coupled with government support for local manufacturing, is driving a 10.83% CAGR for the region.

How are smart labels changing device packaging?

RFID and UDI labels enable real-time traceability, environmental monitoring, and faster recalls, becoming standard for high-value devices.

What challenges do manufacturers face with raw materials?

Medical-grade polymer prices have risen 15-20% since 2024, compelling firms to lock long-term supply contracts and explore bio-based alternatives.

Which end-user segment is expanding fastest?

Contract manufacturing and sterilization organizations are forecast to grow at a 10.32% CAGR as OEMs outsource packaging and validation services.

Page last updated on: July 7, 2025