Digestive Health Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 74.86 Billion |

| Market Size (2031) | USD 112.46 Billion |

| Growth Rate (2026 - 2031) | 8.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Digestive Health Products Market Analysis by Mordor Intelligence

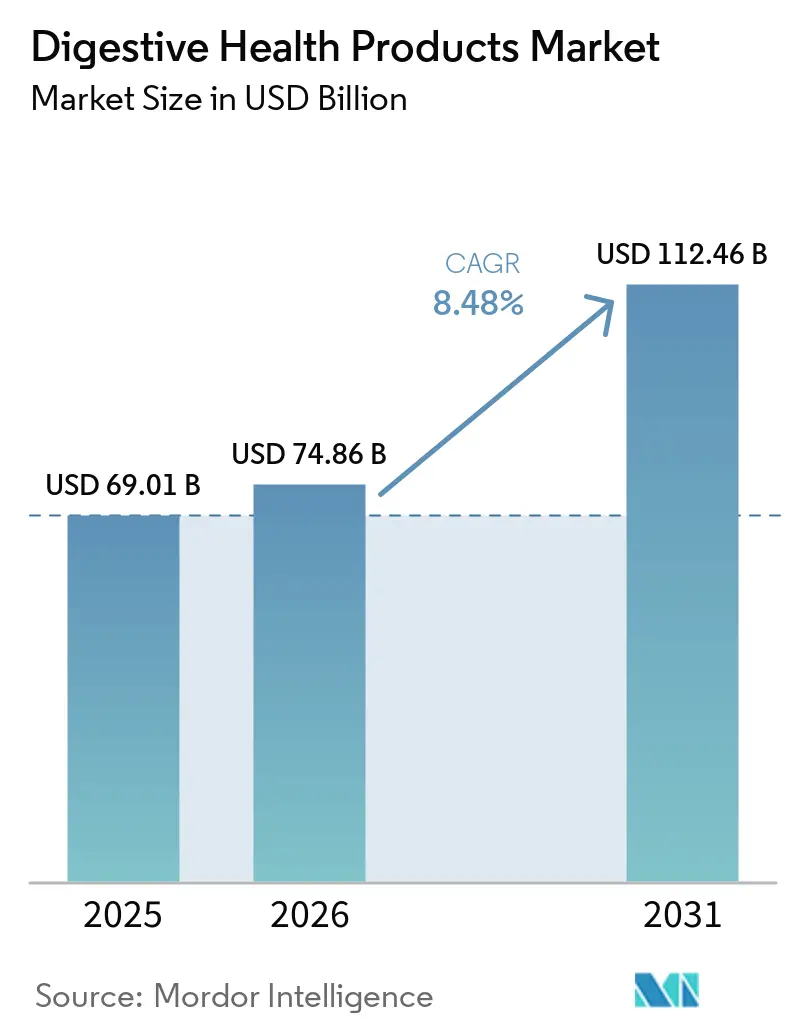

The global digestive health products market size is expected to grow from USD 69.01 billion in 2025 to USD 74.86 billion in 2026, and is forecast to reach USD 112.46 billion by 2031, at an 8.48% CAGR over 2026-2031. As consumers increasingly prioritize preventive healthcare, the global digestive health products market is experiencing consistent growth. Recognizing gut health as a critical component of overall well-being, this shift is further driven by increased awareness of the gut-brain axis, the challenges associated with aging demographics, and medical developments such as weight-loss medications, which frequently result in gastric discomfort and create opportunities for complementary digestive health solutions. A study published by Frontiers in Nutrition (2025) underscores the scale of the issue, estimating that over 40% of the global population is affected by gastrointestinal dysfunction. Specifically, the prevalence of functional dyspepsia in China is reported at 23.5%, significantly exceeding the global average[1]Source: Frontiers in Nutrition, "High-potency multi-strain probiotic formulations for safety and improvement of gastrointestinal function and intestinal health: a randomized controlled clinical trial", frontiersin.org. Industry advancements are focused on probiotics, functional food products, and dietary supplements, while digital retail platforms are transforming consumer accessibility. Despite obstacles such as regulatory inconsistencies and supply chain restructuring, the market demonstrates resilience, reflecting consumers' strong dedication to digestive health as an integral part of their broader wellness objectives.

Key Report Takeaways

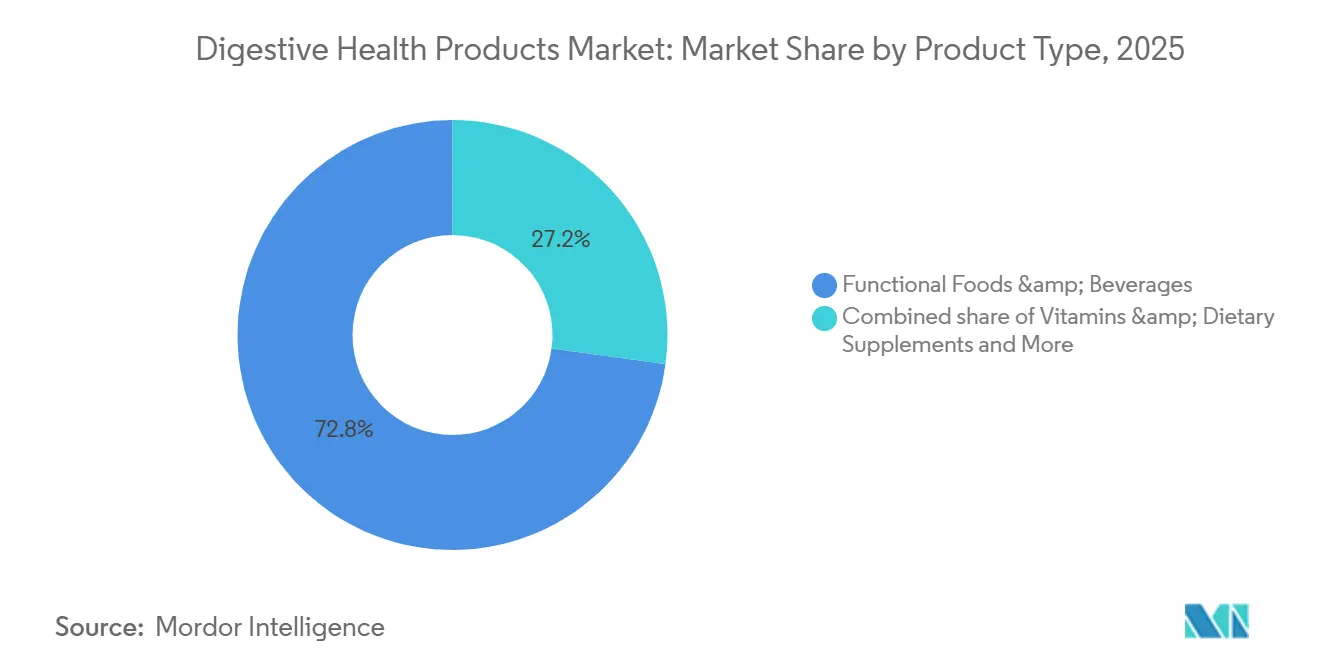

- By product type, functional foods and beverages led with 72.84% of the global digestive health products market share in 2025, whereas the vitamins and dietary supplements segment is projected to grow at a 9.46% CAGR through 2031.

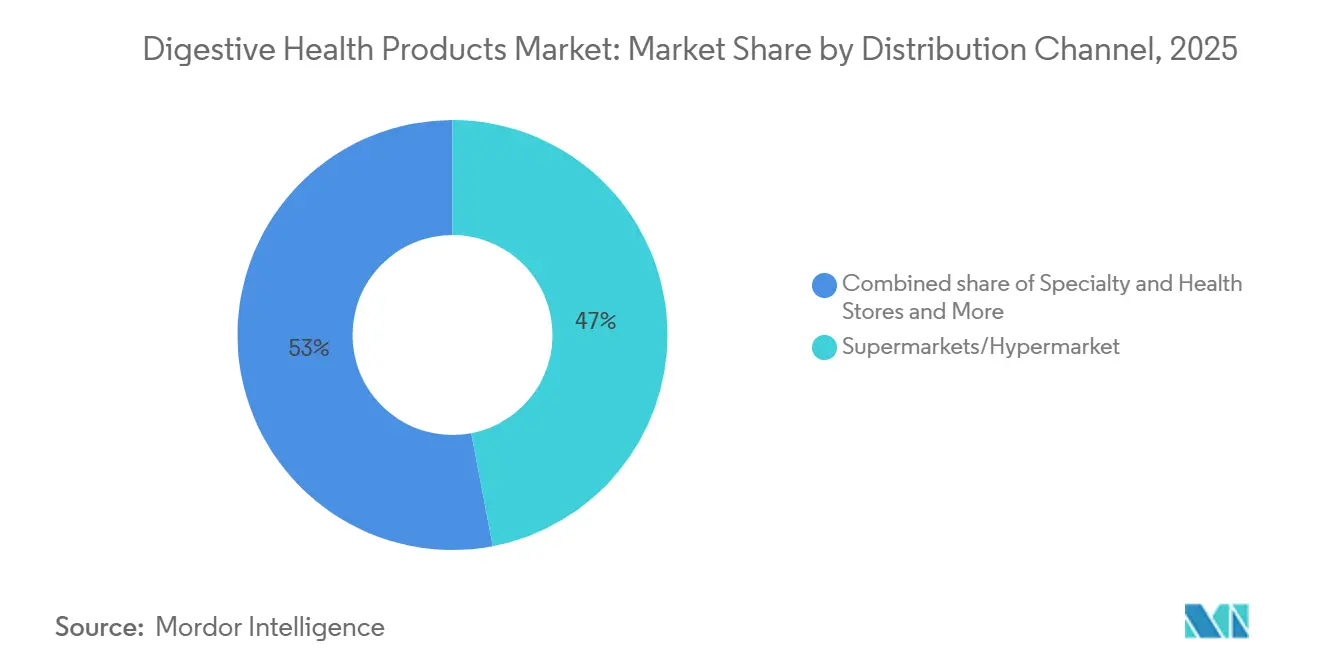

- By distribution channel, supermarkets/hypermarkets accounted for 47.01% revenue share in 2025; online retail is the quickest-growing route with a 12.01% CAGR through 2031.

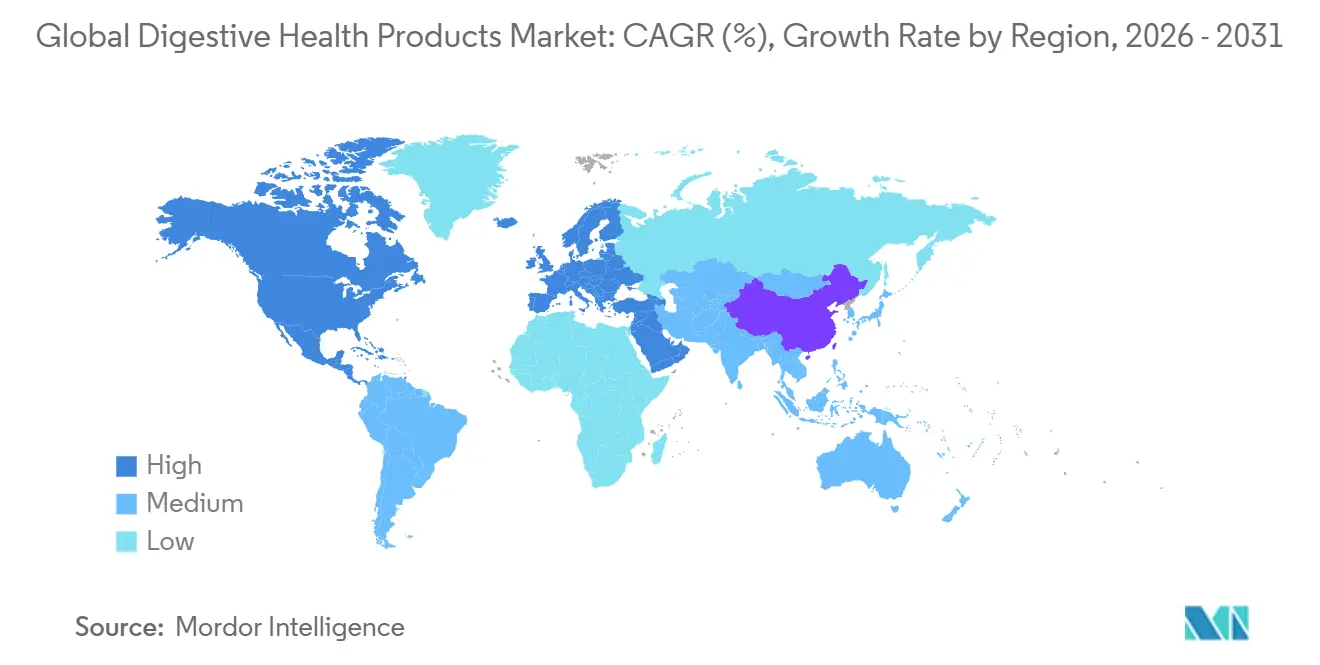

- By geography, North America commanded 36.78% of the global digestive health products market size in 2025, yet Asia-Pacific represents the fastest-growing region with a 10.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digestive Health Products Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of digestive disorders | +2.3% | Global | Medium term (2–4 years) |

| Growing consumer awareness of the gut-brain axis connection | +1.4% | Global, with early momentum in North America and European Union | Short term (≤ 2 years) |

| Aging global population driving demand for digestive support | +1.0% | Aais-Pacific core (Japan, China), Europe, North America | Long term (≥ 4 years) |

| Shift toward preventive healthcare and wellness | +1.2% | Global | Short-medium term (≤ 4 years) |

| Growing popularity of plant-based and clean-label products | +0.8% | North America and European Union, spill-over to Asia-Pacific | Medium term (2–4 years) |

| Rapid expansion of e-commerce and direct-to-consumer channels | +1.0% | Asia-Pacific core, spill-over to all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of digestive disorders

Propelled by the increasing prevalence of digestive disorders, the global market for digestive health products has established a strong and sustainable demand for both preventive and supportive solutions. As gastrointestinal diseases are increasingly recognized as significant contributors to global health challenges, consumers and healthcare systems are progressively adopting nutritional interventions to mitigate strain and improve health outcomes. According to the World Health Organization (WHO) in 2024, diarrhoeal disease ranks as the third leading cause of death among children aged 1–59 months. Each year, it results in approximately 443,832 fatalities among children under five and an additional 50,851 deaths among those aged 5 to 9[2]Source: World Health Organization, "Diarrhoeal disease", who.int. This alarming reality, despite the preventable and treatable nature of the disease, highlights the critical need for digestive health solutions. These solutions play a pivotal role not only in managing chronic conditions but also in addressing preventable risks through enhanced nutrition, access to safe water, and improved hygiene practices. Collectively, these factors underscore the shifting dynamics of the digestive health category, positioning these products as indispensable tools in modern wellness strategies and public health frameworks.

Growing consumer awareness of the gut-brain axis connection

As consumer awareness of the gut-brain connection increases, the digestive health products market is undergoing a significant transformation, extending its relevance beyond traditional digestive health. What began as an interest in the relationship between gut health and mental well-being has evolved into a consumer expectation. Customers are now actively seeking products that not only support digestive balance but also address stress management, enhance sleep quality, and improve cognitive performance. This shift is legitimizing digestive health claims across adjacent wellness categories. Companies with clinically substantiated claims are leveraging this trend to secure premium market positioning. For example, Yakult's Yakult 1000 series, which incorporates the Lacticaseibacillus paracasei strain Shirota, includes functional claims for stress relief and improved sleep quality. By the fiscal year 2025 (FY2025), the product is expected to achieve daily sales of 3.12 million bottles in Japan. This highlights how clinically validated gut-brain claims can drive both high sales volumes and a strong willingness to pay a premium. Simultaneously, structural dietary deficiencies, such as widespread fiber insufficiency, exacerbate the risks of gut imbalances, thereby expanding the market for fiber-based solutions. Overall, the growing emphasis on the gut-brain axis is driving a significant evolution, embedding digestive health products more deeply into holistic wellness strategies.

Shift toward preventive healthcare and wellness

Consumers are increasingly incorporating gut health products into their daily routines, reflecting a significant shift toward preventive healthcare and wellness. This transition highlights a broader lifestyle transformation, where foods, beverages, and supplements designed to improve digestion are now regarded as integral wellness practices. A key driver of this trend is the growing demand for clean-label products. A 2025 survey conducted by the Kaiser Family Foundation revealed that 58% of United States respondents support stricter regulations on food chemicals[3]Source: Global Wellness Institute "Nutrition for Healthspan Initiative Trends for 2025", globalwellnessinstitute.org. This consumer preference is prompting companies to innovate with transparent and natural product formulations. Simultaneously, regulatory authorities are enforcing stricter compliance standards. Regulations such as the European Food Safety Authority’s (EFSA) health claims framework and the United States Food and Drug Administration’s (FDA) Good Manufacturing Practices (GMP) standards are eliminating unverified products from the market and necessitating robust scientific validation. As a result, generic "gut health" claims are losing relevance, while products that can substantiate specific benefits, such as fiber fermentation, strengthening the mucus barrier, or supporting neuroenteric signaling, are gaining increased credibility and consumer trust. This evolving market landscape underscores the growing integration of digestive health products into modern lifestyles, fundamentally reshaping competitive dynamics.

Rapid expansion of e-commerce and direct-to-consumer channels: structural re-routing of consumer spending

As e-commerce and direct-to-consumer (DTC) channels continue their rapid expansion, they are fundamentally transforming the digestive health products market, with digital platforms becoming pivotal growth drivers. Online retail, supported by mobile-first commerce strategies and health-focused digital platforms, is enabling products to achieve rapid scalability, particularly when paired with accessible distribution formats. For instance, in the Asia-Pacific region, Yakult's Y1000 Toshitsu Off, a low-sugar variant, exemplified how health-conscious innovations can achieve significant market penetration through convenience stores and digital channels. In Western markets, subscription-based supplement delivery services and brand-owned DTC platforms are building extensive consumer data repositories, eroding the traditional advantages of physical retailers that relied on pharmacist recommendations and strategic shelf placements. Simultaneously, regulatory oversight is becoming more stringent: the United States Food and Drug Administration (FDA) is intensifying enforcement of digital health claims, while the European Union (EU), under Regulation (EC) No 1924/2006, is tightening restrictions on permissible marketing language in online platforms. This regulatory shift raises the compliance threshold, posing significant challenges for smaller DTC players that lack robust clinical evidence to substantiate their gut-health claims. Overall, the growth of e-commerce and DTC models is not only redirecting consumer spending but also redefining the competitive dynamics within the digestive health products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and inconsistent regulatory frameworks | -1.2% | European Union, Asia-Pacific, North America | Medium-long term (2–5 years) |

| Consumer skepticism and lack of product standardization | -0.8% | Global | Medium term (2–4 years) |

| Misleading health claims eroding consumer trust | -0.6% | North America and European Union | Short-medium term (≤ 4 years) |

| High product development and clinical validation costs | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent and inconsistent regulatory frameworks

The global digestive health products market faces a significant challenge in the form of a fragmented and stringent regulatory environment, which not only increases operational costs but also hampers innovation. Companies, particularly those operating in the probiotics and botanicals segments, encounter substantial hurdles due to the absence of harmonized global standards. This regulatory inconsistency forces businesses to navigate varying regional requirements, resulting in considerable compliance expenses. For instance, in the European Union (EU), fewer than half of the member states permit the use of the term “probiotic” on product labels. This regulatory disparity necessitates costly, region-specific packaging and customized claims strategies. Furthermore, the differing regulatory frameworks in the United States (United States), European Union (EU), and India exacerbate the complexity of cross-border product launches, often delaying market entry and reducing the return on research and development (research and development) investments. Lengthy approval processes, such as those required for multi-strain synbiotic formulations in the European Union (EU), further strain working capital and extend the time required to generate revenue. While incremental progress has been observed, such as the approval of new claims for specific ingredients and ongoing consultations regarding botanicals, achieving full regulatory harmonization remains a distant objective. These regulatory inconsistencies act as a structural barrier to market growth, disproportionately affecting mid-sized manufacturers and increasing the baseline investment necessary to compete effectively.

Consumer skepticism and lack of product standardization

Consumer skepticism and a lack of product standardization have created a significant trust deficit in the global digestive health products market. Issues such as inaccurate labeling, inconsistent strain identification, contamination risks, and diminished probiotic viability by the end of the shelf life have particularly eroded confidence in the supplement segment. The situation is exacerbated by the absence of harmonized international manufacturing standards for live biotherapeutic products, leaving a significant portion of the market without stringent external validation. Although independent verification is offered by third-party certification frameworks such as the United States Pharmacopeia (USP), National Sanitation Foundation (NSF) International, and the European Food Safety Authority (EFSA)’s novel food authorization process, compliance remains voluntary for many food supplements. As a result, a substantial number of products circulate without rigorous quality assurance. Informed consumers are increasingly seeking clinical-grade substantiation. While generic “gut health” claims might entice initial trials, they often fail to foster brand loyalty. Additionally, high-dose probiotic products can lead to discomfort, further fueling skepticism and curtailing repeat purchases. These challenges hinder sustainable penetration rates, underscoring the necessity of credibility and transparency for long-term growth in the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Supplements Outpacing a Dominant Functional Food Base

In 2025, functional foods and beverages dominated the global digestive health products market, capturing 72.84% of total revenue. This dominance is supported by the extensive penetration of probiotic dairy products, particularly yogurt and fermented milk, across Europe and the Asia-Pacific region. In these markets, such products have transitioned from niche functional offerings to essential health staples. The segment is undergoing rapid diversification, with younger consumer demographics increasingly favoring kombucha, prebiotic sodas, and fiber-infused beverages, driven more by the emerging gut-brain axis narrative than by traditional digestive symptom relief. While dairy remains the leading category, significant growth opportunities exist in underpenetrated areas such as cereals, snacks, and baked goods, especially considering the widespread fiber intake deficiency highlighted by the 2025 Dietary Guidelines Advisory Committee.

In contrast, supplements represent the fastest-growing category, with a projected CAGR of 9.46% from 2026 to 2031. This growth trajectory is driven by advancements in clinical research, enabling brands to utilize strain-specific probiotic evidence for more precise differentiation compared to broadly marketed food products. Probiotics lead this segment, followed by prebiotics and enzymes, while postbiotics are emerging as a disruptive sub-category due to their inherent stability and simplified supply chain logistics. Clinical trials demonstrating measurable improvements in gut barrier integrity and immune system markers are strengthening consumer trust and gaining regulatory approval. Additionally, adherence to compliance frameworks such as International Organization for Standardization (ISO) 22000, Good Manufacturing Practices (GMP) certification, and United States Pharmacopeia (USP) verification is becoming a baseline expectation. These standards position supplements as the segment most aligned with scientific rigor and the demands of premium consumer markets.

By Distribution Channel: Online Retail Challenging Supermarket Primacy

In 2025, supermarkets and hypermarkets accounted for the largest distribution share at 47.01%. These channels function as both impulse-purchase points for functional dairy products and trusted retail spaces, often located near pharmacies, for dietary supplements. This strategic positioning is particularly robust in regions where pharmacist endorsements strengthen physical retail relationships, thereby enhancing consumer trust. Convenience stores and grocery outlets continue to serve as key maintenance channels for established brands. Meanwhile, specialty and health-focused stores cater to clinically driven consumers seeking high-potency or condition-specific formulations, enabling premium pricing for innovative product formats such as postbiotics and synbiotics. Together, these physical retail channels form the backbone of the category’s traditional distribution network, leveraging consumer trust and accessibility to sustain their market dominance.

Online retail stores represent the fastest-growing distribution channel, with a projected CAGR of 12.01% from 2026 to 2031. Subscription-based business models and brand-owned direct-to-consumer (DTC) platforms are enabling manufacturers to establish direct relationships with consumers. This approach not only secures repeat-purchase revenue streams but also provides access to valuable consumer data, which is difficult for physical retailers to replicate. In the Asia-Pacific region, social commerce platforms such as Douyin, Shopee, and Lazada are driving rapid trial-to-purchase conversions in markets underserved by specialty retail stores. In Western markets, digital-first strategies are narrowing the gap with traditional pharmacy-driven sales channels. However, this rapid growth is accompanied by strategic challenges: online platforms often amplify misinformation, with nutrition professionals identifying social media as a significant source of misleading health claims. Consequently, while e-commerce is fundamentally altering consumer spending patterns and reshaping competitive dynamics, establishing credibility and adhering to regulatory compliance standards are becoming critical factors for achieving sustainable growth.

Geography Analysis

In 2025, North America dominated the global digestive health products market, capturing a 36.78% share. This dominance was driven by high per-capita healthcare expenditure, a well-established functional food segment, and heightened consumer awareness of probiotics and dietary fiber. The region's diverse distribution channels, spanning mass retail, pharmacies, specialty stores, and digital-first subscription brands, have facilitated the coexistence of multiple value tiers, thereby driving revenue growth. Brand-led innovation and marketing strategies centered on storytelling continue to strengthen the category. For example, campaigns for products such as Tums Gummy Bites and Benefiber demonstrate how investments in consumer engagement can secure market share, even in a highly competitive environment. Additionally, increasing clinical demand, particularly in Canada, where the prevalence of inflammatory bowel disease (IBD) is rising, is expanding the market's scope from lifestyle supplements to medically oriented nutritional solutions.

Asia-Pacific is experiencing rapid growth and is projected to expand at a CAGR of 10.41% from 2026 to 2031. This growth is driven by China's market scale, Japan's aging population, the expanding urban middle class in India, and the rapid penetration of e-commerce in Southeast Asia. China's large population affected by gastrointestinal diseases, coupled with a high prevalence of functional dyspepsia, underscores the structural demand for both food-based and supplement formats. Japan's demographic profile, with one-third of its population aged 65 or older, sustains demand for digestive enzymes and probiotics designed to address age-related gastrointestinal slowdown. Meanwhile, the rise of digital-first distribution channels in Southeast Asia is accelerating product trials and adoption, positioning the region as a critical growth driver for global market players.

Europe represents a high-value yet structurally complex market, characterized by the highest global prevalence of digestive disorders and a substantial consumer base seeking functional solutions. Germany and Italy lead in terms of market size, with probiotics holding a significant share in both dietary supplements and food formats. Regulatory oversight continues to play a pivotal role, with the European Food Safety Authority's (EFSA) health claim authorizations and timelines for novel food approvals influencing product development cycles and investment strategies. While compliance costs remain substantial, the region's sophisticated consumers, who are willing to pay a premium for clinically validated products, make Europe a strategically important geography. The challenge lies in balancing regulatory complexities with the region's premium market potential.

Competitive Landscape

The global digestive health products market is fragmented, with large multinational food and pharmaceutical groups dominating mass distribution channels. At the same time, specialized probiotic and nutraceutical companies compete by leveraging clinical specificity and direct-to-consumer strategies. A significant strategic development occurred in January 2024 with the merger of Novozymes and Chr. Hansen, resulting in the formation of Novonesis, a biosolutions leader valued at EUR 3.7 billion. Novonesis boasts an extensive probiotic strain library, marking a consolidation at the ingredient level. In contrast, the branded product segment remains fragmented, with established players like Danone revitalizing legacy brands such as Activia’s “Gut Glow-Up” and Activia Proactive to attract younger demographics and consumers using glucagon-like peptide-1 (GLP-1) medications. Additionally, Haleon’s acquisition of Tianjin TSKF Pharmaceutical highlights the strategy of global players deepening local partnerships to drive growth in high-potential markets.

Emerging disruptors are reshaping the premium segment of the market by utilizing precision nutrition technologies. Innovations such as gut microbiome sequencing, artificial intelligence (AI)-driven strain screening, and personalized synbiotic formulations are accelerating product development timelines while creating competitive advantages grounded in clinical data rather than marketing scale. Companies like BioGaia have shifted to direct market entry in countries such as Germany and Austria, moving away from distributor partnerships to capture higher profit margins and gain deeper consumer insights. Simultaneously, regulatory gaps are creating new opportunities. In the GLP-1 companion nutrition space, early entrants like Arla Foods Ingredients and Novonesis are positioning themselves with protein-and-probiotic concepts and co-development partnerships.

Looking forward, the competitive dynamics of the market are increasingly defined by intellectual property and clinical innovation rather than traditional factors such as shelf placement or advertising expenditure. Key differentiators now include patent filings, substantiated health claims, and regulatory-compliant product innovations. This evolution underscores a market where scientific credibility, rigorous research, and strategic partnerships will determine market leadership. Meanwhile, smaller challengers continue to exploit their agility and direct-to-consumer business models to establish niche positions within the market.

Digestive Health Products Industry Leaders

-

Nestlé S.A.

-

Danone S.A.

-

Yakult Honsha Co., Ltd.

-

Abbott Laboratories

-

Novonesis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Arla Foods Ingredients unveiled innovative solutions tailored for users of GLP-1 anti-obesity medications. These high-protein, nutrient-rich application concepts were showcased at Vitafoods Europe, held from May 5th to 7th, 2026, in Barcelona. This launch specifically addresses the 76% of GLP-1 users who face gastric discomfort, a demographic currently lacking a dominant brand in digestive health.

- March 2026: On March 23, 2026, Abbott finalized its acquisition of Exact Sciences Corporation, valuing the transaction at approximately USD 23 billion. This strategic acquisition strengthens Abbott's position in gastrointestinal (GI) health diagnostics while significantly expanding its market opportunities. The integration of Cologuard, a colorectal cancer screening product that has facilitated over 20 million tests since its introduction in 2014, effectively doubles Abbott's total addressable market to exceed USD 120 billion.

- September 2025: BASF SE finalized the divestiture of its Food and Health Performance Ingredients Business to Louis Dreyfus Company B.V. (LDC). The transaction encompasses the transfer of approximately 300 employees, a production facility situated in Illertissen, Germany, and a portfolio of health ingredient lines, including plant sterol esters, conjugated linoleic acid (CLA), and omega-3 oils. This strategic move enables BASF SE to concentrate on its core competencies in vitamins and carotenoids, while LDC strengthens its position in the plant-based health ingredients market.

Global Digestive Health Products Market Report Scope

Digestive health products are foods, beverages, and supplements specifically formulated to support the proper functioning of the gastrointestinal system. They include categories such as probiotics, prebiotics, postbiotics, enzymes, fiber-enriched products, and functional foods like yogurts, fermented milk, kombucha, and fiber-infused snacks. These products aim to maintain gut balance, improve nutrient absorption, strengthen the intestinal barrier, and address issues such as bloating, indigestion, or irregular bowel movements.

The market is segmented on the basis of product type, distribution channel, and geography. By product type, the market is segmented into functional foods and beverages, supplements, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, specialty and health stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Functional Foods and Beverages | Dairy and Dairy-based Products |

| Functional Beverages | |

| Cereals, Snacks and Bakery | |

| Other Functional Food and Beverages Product | |

| Supplements | Probiotics |

| Prebiotics | |

| Enzymes | |

| Botanicals | |

| Other Supplement Type | |

| Other Product Type |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Specialty and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Columbia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Functional Foods and Beverages | Dairy and Dairy-based Products |

| Functional Beverages | ||

| Cereals, Snacks and Bakery | ||

| Other Functional Food and Beverages Product | ||

| Supplements | Probiotics | |

| Prebiotics | ||

| Enzymes | ||

| Botanicals | ||

| Other Supplement Type | ||

| Other Product Type | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty and Health Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Columbia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global digestive health products market?

The market was valued at USD 69.01 billion in 2025 and is projected to reach USD 112.46 billion by 2031, reflecting a CAGR of 8.48% between 2026 and 2031.

Which product category holds the largest share of the market?

Functional foods and beverages dominate the market, accounting for 72.84% of revenue in 2025, driven by probiotic dairy products and expanding functional beverage formats.

Which product category is expected to grow the fastest?

Supplements are the fastest-growing segment, forecasted to expand at a CAGR of 9.46% from 2026 to 2031, supported by clinical-grade probiotic, prebiotic, and postbiotic innovations.

What is the leading distribution channel for digestive health products?

Supermarkets and Hypermarkets held the largest share at 47.01% in 2025, reflecting their role as trusted retail spaces for both functional foods and supplements.

Which region is the largest and which is the fastest-growing?

North America led with 36.78% of global revenue in 2025, while Asia-Pacific is the fastest-growing region, projected to expand at a CAGR of 10.41% from 2026 to 2031.

Page last updated on: