Battery Sensor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

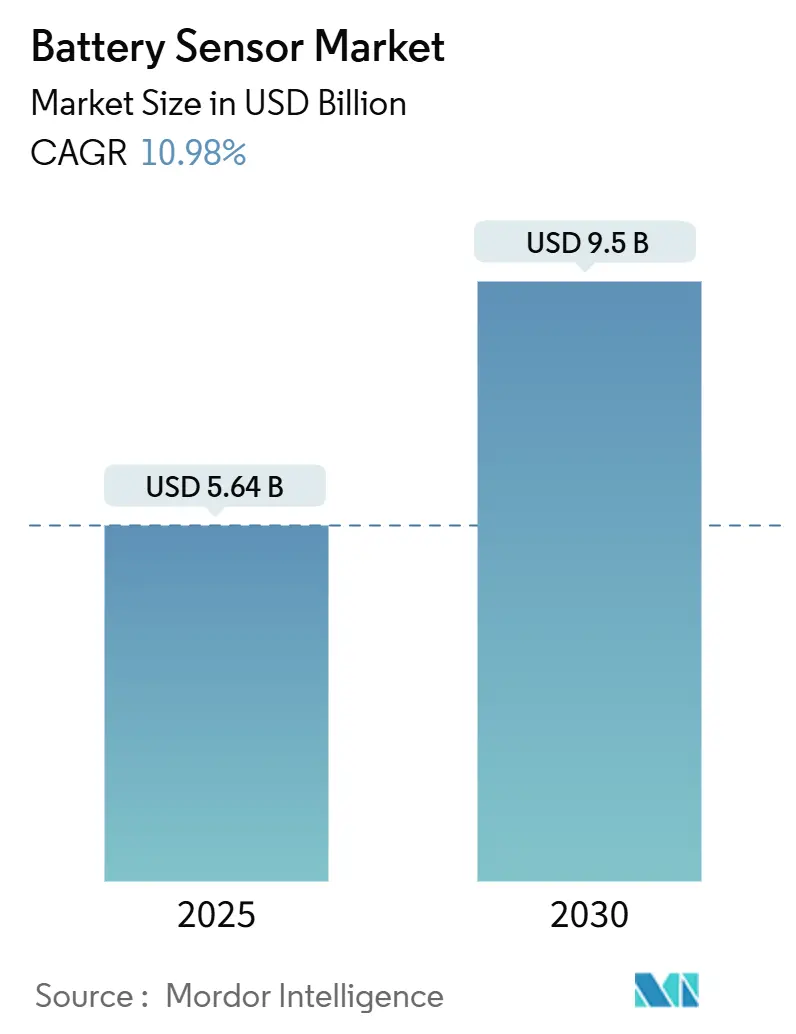

| Market Size (2025) | USD 5.64 Billion |

| Market Size (2030) | USD 9.5 Billion |

| Growth Rate (2025 - 2030) | 10.98% CAGR |

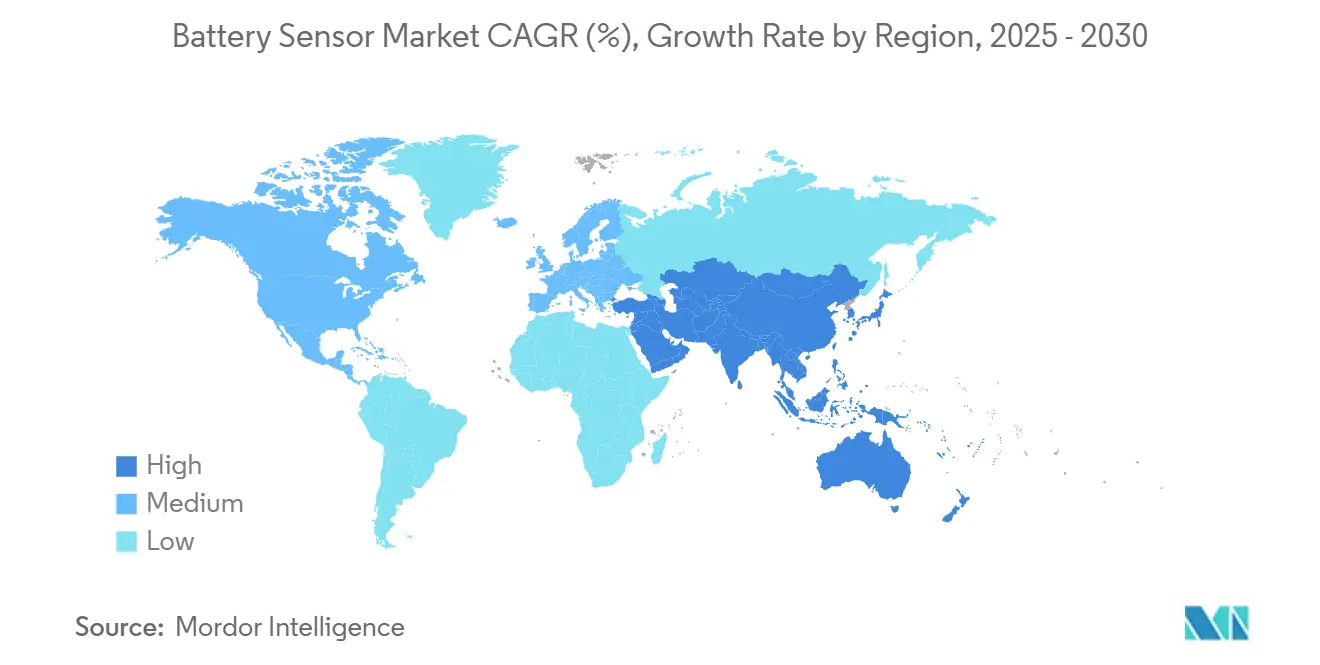

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Sensor Market Analysis by Mordor Intelligence

The battery sensor market size stood at USD 5.64 billion in 2025 and is forecast to reach USD 9.50 billion by 2030, advancing at a 10.98% CAGR. The expansion reflects accelerating electric-vehicle (EV) output, fast-rising utility-scale energy-storage installations, and the enforcement of ISO 21498 battery-monitoring standards across automotive and industrial settings. Intensifying competition around high-accuracy current-sensing solutions, rapid cost declines in Hall-effect devices, and the shift toward 800 V battery packs sustain momentum. Suppliers that package hardware, diagnostics, and analytics into integrated offerings are capturing premium price points as original-equipment manufacturers (OEMs) seek turnkey compliance and safety. Geographic demand concentrates where electrification policies intersect domestic battery manufacturing incentives, notably in North America, Europe, and China. Meanwhile, sovereign-wealth investments in the Gulf Cooperation Council (GCC) economies introduce a second growth pole that favors sensor designs tolerant of extreme ambient temperatures.

Key Report Takeaways

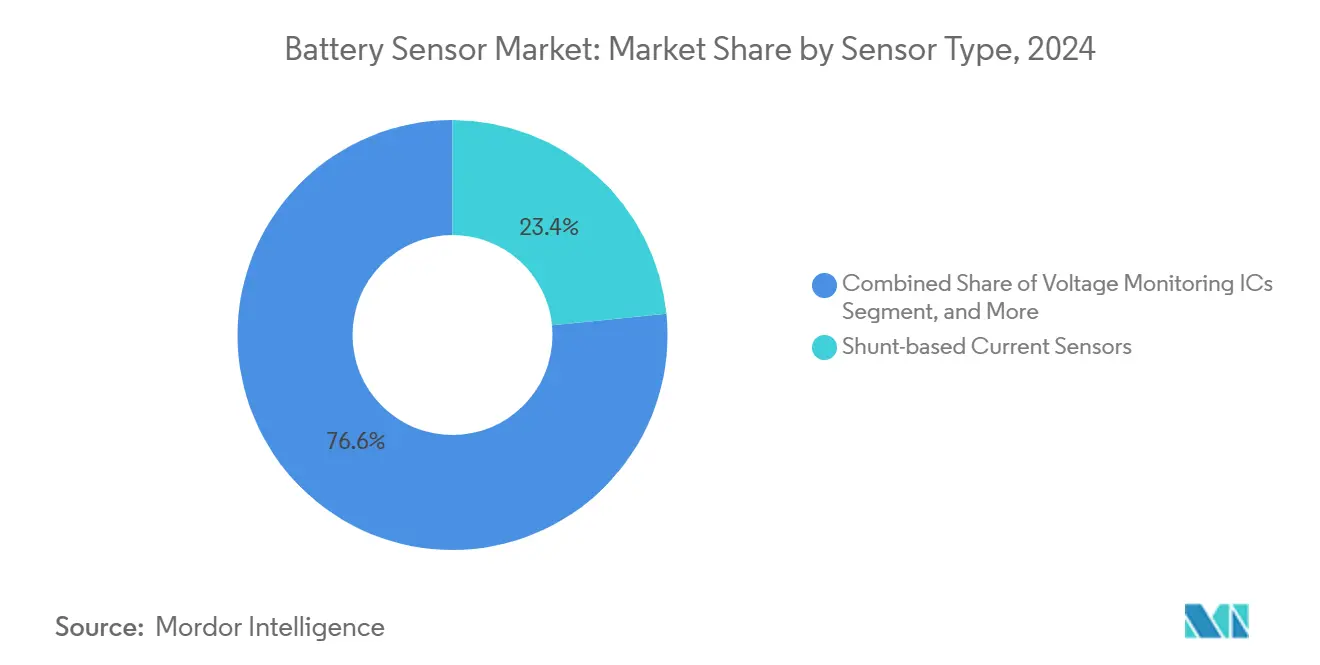

- By sensor type, shunt-based current sensors led with 23.43% of battery sensor market share in 2024 while fiber-optic sensors are projected to register an 11.21% CAGR to 2030.

- By technology, open-loop designs held 32.84% share of the battery sensor market size in 2024; wireless solutions are forecast to expand at a 12.32% CAGR through 2030.

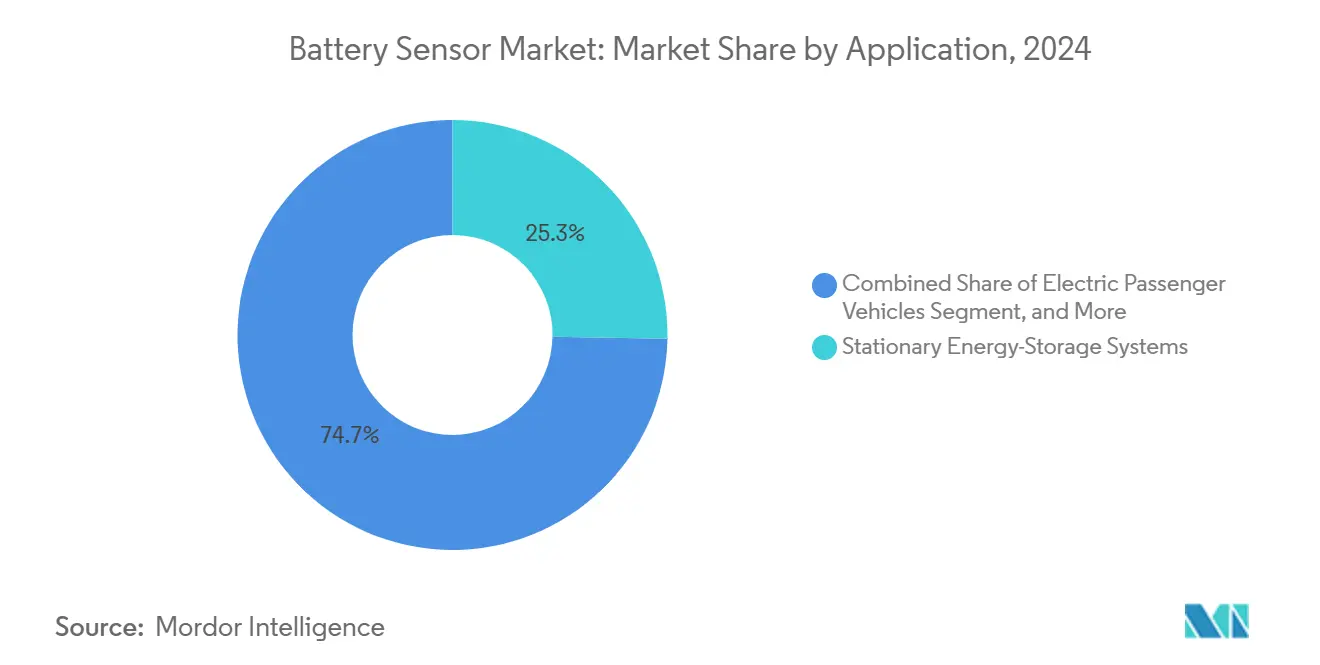

- By application, stationary energy-storage systems accounted for 25.28% of the 2024 battery sensor market size and are set to grow 11.56% annually to 2030.

- By end-user industry, the energy and utilities segment captured 22.98% revenue in 2024 and shows the fastest trajectory at 13.78% CAGR through 2030.

- By geography, North America led with 23.41% share in 2024, whereas the Middle East and Africa region is poised for the quickest gain at 11.89% CAGR through 2030.

Global Battery Sensor Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV production surge and stringent xEV battery-safety mandates | +3.2% | Global, concentrated in North America, Europe, China | Medium term (2-4 years) |

| Rapid growth of utility-scale energy-storage installations | +2.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Falling cost and accuracy gains in Hall-effect current sensors | +1.9% | China, Japan, Germany | Short term (≤ 2 years) |

| Standardization of ISO 21498 battery-monitoring interfaces | +1.5% | Global automotive markets | Medium term (2-4 years) |

| IIoT-driven predictive-maintenance analytics for batteries | +1.1% | Industrial hubs in developed markets | Long term (≥ 4 years) |

| Transition to wireless battery-sensor modules in 800 V packs | +0.8% | Premium EV programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV production surge and stringent xEV battery-safety mandates

Record EV assembly lines now specify sub-1%-accuracy current sensing, sub-2 mV voltage resolution, and cell-level temperature granularity to comply with UNECE R100 and SAE J2929 safety codes. BMW’s move to 800 V architecture illustrates how these thresholds elevate sensors from cost components to safety-critical systems. [1]BMW Group, “BMW Group accelerates transformation with Neue Klasse,” press.bmwgroup.com OEMs pay premiums for devices with Automotive Safety Integrity Level-D (ASIL-D) certification, driving tier-one suppliers toward redundant, self-diagnosing designs. This dynamic reinforces barriers to low-cost entrants and sustains higher average selling prices across the battery sensor market.

Rapid growth of utility-scale energy-storage installations

Grid operators approved multiple 200 MWh-plus lithium-ion facilities in Texas and California, each deploying upward of 50,000 discrete sensors to manage thermal gradients and balance currents. VERBUND’s 50 MWh Austrian project employs distributed fiber-optic arrays that cut cell-to-cell temperature variance by 8 °C, extending usable life 15–20%. [2]VERBUND, “VERBUND starts construction of largest battery storage facility in Austria,” verbund.comCapital-intensive assets justify advanced monitoring that limits downtime penalties exceeding USD 50,000 per day, underpinning double-digit growth in the energy-storage slice of the battery sensor market.

Falling cost and accuracy gains in Hall-effect current sensors

Process shrinks and package integration trimmed Hall-effect sensor prices 15–20% annually, while precision improved to sub-1% full-scale error. TDK’s closed-loop tunnel-magnetoresistance (TMR) family measures up to 1,200 A with negligible thermal drift, enabling precise state-of-charge computation. [3]TDK Corporation, “A TMR Sensor Solution Providing Ultra-High-Precision Monitoring of an EV Battery,” tdk.com As affordability improves, automakers retrofit entry-level EV trims and consumer-electronics makers integrate high-accuracy gas-gauge circuits, broadening the battery sensor market addressable base.

Standardization of ISO 21498 battery-monitoring interfaces

ISO 21498 harmonizes the communications stack between sensors and battery-management controllers, cutting integration cycles from as long as 24 to as short as 9 months. Suppliers with early-compliant offerings enjoy preferred-supplier status, and the standard’s embedded diagnostics clause is accelerating the pivot toward smart sensors with on-chip health-report channels. Automotive procurement teams now score bids partly on ISO 21498 readiness, nudging late movers to scramble for certification services.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wide temp-drift/offset errors in low-cost shunt solutions | -1.8% | India, Southeast Asia, Latin America | Short term (≤ 2 years) |

| Volatile pricing and supply of ferrite/permalloy magnetic cores | -1.2% | Global supply chains centered in China and Japan | Medium term (2-4 years) |

| Higher system complexity and power draw from drift-compensation algorithms | -0.9% | Automotive and industrial design hubs worldwide | Short term (≤ 2 years) |

| Lengthy qualification cycles for automotive-grade sensor compliance | -0.6% | Global automotive markets (OEM and Tier-1 suppliers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Wide temp-drift/offset errors in low-cost shunt solutions

Budget-grade shunts exhibit resistance-value drift beyond 5% across -40 °C to +125 °C automotive excursions, causing inaccurate state-of-charge readings that jeopardize thermal-runaway protection. Compensation firmware mitigates errors but adds bill-of-materials cost and processing overhead, negating shunts’ headline price advantage. Consequently, premium EV and industrial platforms color-code shunts only to non-critical subsystems, capping growth in cost-sensitive regions such as India and parts of Latin America.

Volatile pricing and supply of ferrite/permalloy magnetic cores

More than 70% of ferrite core production resides in China and Japan, exposing Hall-effect and TMR sensors to material disruptions. Rare-earth magnet prices fell 42% in 2024 but remain lumpy, complicating procurement forecasts. Supply instability elongates lead times up to six months and forces suppliers to dual-source or redesign around alternate alloys, shaving 1.2 percentage points from the forecast CAGR of the battery sensor market.

Segment Analysis

By Sensor Type: Fiber-optic designs accelerate market shift

Shunt-based current sensors retained 23.43% of the 2024 battery sensor market share, yet fiber-optic units are on course for an 11.21% CAGR, illustrating how electromagnetic-interference immunity shapes next-generation packs. The battery sensor market size for fiber-optic devices is projected to climb proportionally with multi-gigawatt storage farms, where a single string can run 100 m in length and require distributed temperature nodes at 1 m intervals. PARC and LG Chem demonstrated Bragg-grating arrays embedding 100+ points in one fiber, reducing harness weight by 70%.

Complementary uptake of Hall-effect arrays persists because galvanic isolation simplifies 800 V electrical design. Meanwhile NTC/PTC thermistors continue as baseline thermal safeguards, rated beyond 150 °C for under-hood reliability. MEMS pressure discs emerge for pouch-cell swelling detection, with NXP’s NBP8-9x family reporting micro-strain variations that precede gas venting by several cycles. Convergence of multiple sensing modalities inside single modules compresses board real estate and feeds unified analytics engines, a trend likely to capture additional battery sensor market value.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Wireless links reshape pack architecture

Open-loop architectures dominated 32.84% of 2024 revenue owing to simplicity, but wireless nodes will grow 12.32% a year as automakers chase harness weight reductions. NXP’s ultra-wideband transceivers eliminate 3 kg of cabling from a typical 100 kWh pack, trimming vehicle mass enough to extend driving range 2–3 km without added cells. The battery sensor market size for closed-loop isolated options remains robust in grid storage, where Revenue-per-Megawatt hinges on sub-0.5% measurement accuracy.

Analog outputs persist in price-sensitive inverters and scooters, but digital channels such as CAN-FD and SENT win share via built-in error-checking and over-the-air firmware update support. Predictive algorithms running at the edge leverage these digital datapaths to trigger pre-emptive balancing, cutting warranty returns by 15% in pilot fleets. Over the forecast, suppliers bundling secure wireless connectivity with on-board analytics stand to outpace peers limited to discrete measurement chips within the battery sensor market.

By Application: Stationary storage scales sensor volumes

Stationary energy-storage systems held 25.28% of 2024 revenue and will sustain 11.56% CAGR as utilities deploy 10 GWh-class, multi-site batteries for peak-shaving. Texas approval of 600 MWh “Trio” projects underscores sensor volumes that surpass 50,000 per site, anchoring the largest incremental chunk of the battery sensor market by absolute units. Passenger EVs still absorb the highest unit shipments but growth moderates as penetration levels mature.

Commercial EVs, particularly delivery vans, accelerate because fleet operators monetize total cost-of-ownership savings. Consumer electronics incorporate advanced gas gauges such as ADI’s LTC2941 to stretch run-time, illustrating downstream diversification. Industrial UPS and telecom back-up arrays adopt smart sensors to achieve 99.99% uptime by moving from calendar-based to asset-health-based replacement, enhancing the resilience narrative central to the battery sensor market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Utilities anchor future momentum

Utilities accounted for 22.98% revenue in 2024 and top the growth table with 13.78% CAGR as grid operators roll out energy-shifting assets and ancillary-services batteries. ACCURE’s partnership with Repsol embeds AI models that forecast capacity fade within 2% error, validating revenue-optimization use cases. Automobile OEMs remain vital, yet as EV adoption exceeds early-adopter phases in Europe and China growth rates plateau.

Industrial automation facilities, especially those operating continuous-process lines, deploy redundant battery backups requiring real-time health scoring. Telecommunications carriers equip 5G base-stations with ISO-21498-compliant monitoring to manage elevated duty cycles. Such breadth ensures the battery sensor market remains insulated from single-vertical downturns while sharpening segmentation strategies.

Geography Analysis

North America maintained 23.41% revenue leadership in 2024, reflecting Inflation Reduction Act credits that boost domestic battery manufacturing and thus co-located sensor demand. Joint ventures such as General Motors–Samsung SDI’s USD 3.5 billion plant illustrate vertically aligned supply-chain formation. Utility-scale deployments in Texas and California regularly exceed 200 MWh, necessitating multi-layer sensor meshes interfacing with regional grid-command centers. Canada’s nickel and lithium reserves and Mexico’s automotive sub-assembly capacity round out an integrated continental value network that accelerates innovation cycles within the battery sensor market.

Europe records strong momentum as the EU Battery Regulation mandates cradle-to-grave traceability, forcing sensor instrumentation through production, road use, and recycling stages. Germany pioneers adaptive sensor fusion for high-energy-density packs, France focuses on second-life battery applications, and the Nordics exploit abundant hydroelectricity to host cell-test facilities. Such policy coherence and advanced manufacturing combine to nurture specialized sensor niches tied to circular-economy metrics.

The Middle East and Africa showcase the fastest regional CAGR at 11.89% through 2030, propelled by sovereign-wealth funding of renewable megaprojects and aggressive EV adoption targets UAE aims for 50% EV share by 2050 and Saudi Arabia pursues 500,000 EVs by 2030. Harsh ambient temperatures spur demand for sensors validated to 125 °C steady-state operation, creating an addressable opportunity for ruggedized solutions. South Africa leverages mining logistics to implement batteries for peak-shaving across ore-haul railways, while Jordan’s 140% EV-sales surge catalyzes a supporting aftermarket for retrofit battery-health monitors. The confluence of climate, policy, and infrastructure quickens overall uptake inside the battery sensor market.

Competitive Landscape

The competitive field skews toward mid-level concentration as the top five suppliers command roughly 62% of global revenue, underpinned by deep patent portfolios and automotive-grade fabrication lines. Allegro MicroSystems, TDK, and Infineon lead in Hall-effect and TMR accuracy records, while Murata advances ceramic sensors suited to solid-state batteries. Chinese entities collectively hold 5,486 of 9,862 active battery-technology patents, affording domestic players defensive leverage in core intellectual property disputes.

Wireless sensing opens white space where semiconductor incumbents face competition from connectivity specialists integrating ultra-wideband links and digital-isolation blocks. Startups bundle cloud dashboards and subscription analytics, shifting revenue models from pure component sales to data-as-a-service. Partnerships such as Murata–QuantumScape and STMicro’s USD 950 million acquisition of NXP’s sensor unit signal consolidation aimed at closing technology gaps and assuring supply-chain control.

Regulatory rigor favors firms with Automotive SPICE and ISO 26262 workflows already in place, extending qualification cycles that deter price-focused entrants. Nonetheless, fiber-optic niche players and edge-AI software vendors infiltrate project-based awards in utility storage, indicating pockets of fragmentation. Collectively, these forces shape a battery sensor market whose strategic battleground shifts from discrete parts toward integrated, standards-compliant modules featuring embedded diagnostics.

Battery Sensor Industry Leaders

Allegro MicroSystems, Inc.

Asahi Kasei Microdevices Corporation

Melexis NV

LEM Holding SA

Sensata Technologies Holding plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: STMicroelectronics announced acquisition of NXP Semiconductors’ sensor business unit for USD 950 million, strengthening its MEMS-based portfolio for automotive and industrial batteries.

- July 2025: Samsung unveiled solid-state battery technology with 500 Wh/kg energy density, promising 600-mile EV range and 9 minute charging. Interesting Engineering.

- April 2025: Murata Manufacturing and QuantumScape initiated collaboration for high-volume ceramic film production aimed at solid-state batteries. Murata Manufacturing.

- April 2025: ITEN achieved 200 C discharge-rate breakthrough in solid-state lithium-ion chemistry, requiring high-speed current sensing. EE Journal.

Global Battery Sensor Market Report Scope

| Hall-effect Current Sensors |

| Shunt-based Current Sensors |

| Voltage Monitoring ICs |

| Temperature (NTC / PTC) Sensors |

| Fiber-Optic Battery Sensors |

| MEMS Pressure Sensors (Cell-level) |

| Closed-loop (Isolated) Sensors |

| Open-loop Sensors |

| Digital (I2C / CAN / SENT) Output |

| Analog Output |

| Wireless Battery Sensors |

| Electric Passenger Vehicles |

| Electric Commercial Vehicles |

| Hybrid and Plug-in Hybrid Vehicles |

| Stationary Energy-Storage Systems |

| Consumer Electronics |

| Industrial UPS and Backup |

| Automotive |

| Energy and Utilities |

| Consumer Electronics |

| Industrial and Manufacturing |

| Telecommunications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Sensor Type | Hall-effect Current Sensors | ||

| Shunt-based Current Sensors | |||

| Voltage Monitoring ICs | |||

| Temperature (NTC / PTC) Sensors | |||

| Fiber-Optic Battery Sensors | |||

| MEMS Pressure Sensors (Cell-level) | |||

| By Technology | Closed-loop (Isolated) Sensors | ||

| Open-loop Sensors | |||

| Digital (I2C / CAN / SENT) Output | |||

| Analog Output | |||

| Wireless Battery Sensors | |||

| By Application | Electric Passenger Vehicles | ||

| Electric Commercial Vehicles | |||

| Hybrid and Plug-in Hybrid Vehicles | |||

| Stationary Energy-Storage Systems | |||

| Consumer Electronics | |||

| Industrial UPS and Backup | |||

| By End-User Industry | Automotive | ||

| Energy and Utilities | |||

| Consumer Electronics | |||

| Industrial and Manufacturing | |||

| Telecommunications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the battery sensor market in 2025 and how fast is it growing?

The battery sensor market size reached USD 5.64 billion in 2025 and is on track to post a 10.98% CAGR to USD 9.50 billion by 2030.

Which sensor technology is expanding the quickest through 2030?

Wireless battery sensors register the fastest growth at 12.32% CAGR as OEMs adopt 800 V architectures that demand galvanic isolation and weight reduction.

What end-user sector shows the strongest demand momentum?

Utilities lead with a 13.78% CAGR because large-scale energy-storage projects require thousands of high-accuracy sensors for grid-integration and predictive-maintenance functions.

Why are fiber-optic battery sensors gaining popularity?

Fiber-optic designs are immune to electromagnetic interference and can embed 100+ sensing points along lengthy battery strings, making them ideal for utility-scale storage and high-voltage EVs.

Which region is expected to record the fastest growth?

The Middle East and Africa region is forecast to grow 11.89% annually, underpinned by sovereign-wealth investments in renewables and ambitious EV adoption targets.

What is driving consolidation among sensor suppliers?

Acquisition activity, exemplified by STMicroelectronics’ purchase of NXP’s sensor unit, reflects the need for broader portfolios that combine hardware, wireless connectivity, and analytics under evolving ISO 21498 standards.