Germany Turning Machine and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

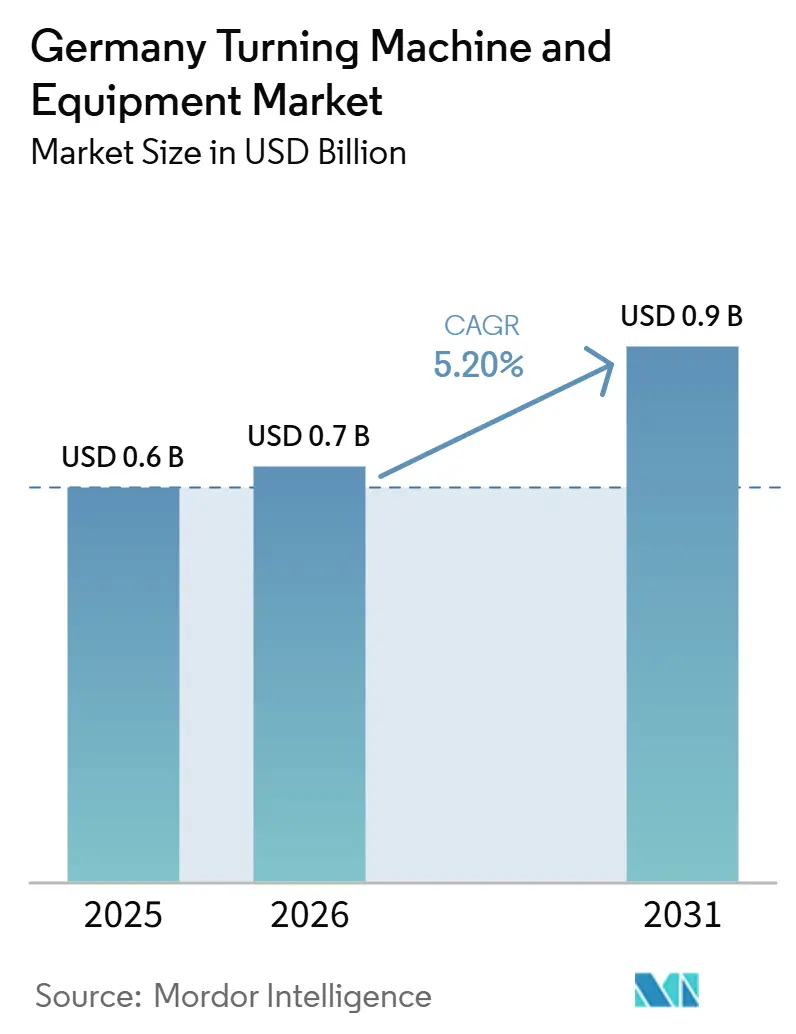

| Base Year Market Size (2025) | USD 0.6 Billion |

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 0.9 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Turning Machine and Equipment Market Analysis by Mordor Intelligence

The Germany Turning Machine and Equipment Market size is expected to grow from USD 0.6 billion in 2025 to USD 0.7 billion in 2026 and is forecast to reach USD 0.9 billion by 2031 at 5.20% CAGR over 2026-2031.

Germany remains one of the world’s leading machine tool exporting countries, supported by its strong precision engineering base, as domestic users in automotive, aerospace, medical technology, and industrial machinery still depend on precision turning systems with local engineering support and established service coverage. The broader German machine tool sector produced EUR 13.6 billion (USD 16.0 billion) in 2025, and the VDW expects output to edge up to EUR 13.7 billion (USD 16.1 billion) in 2026, which signals that the Germany turning machine and equipment market is benefiting from the first expected production rebound after two difficult order years. Federal spending on infrastructure, defense, digitalization, and mobility is creating a better investment backdrop. At the same time, medical technology manufacturing and broader machinery output continue to support equipment renewal and capacity additions in Germany turning machine and equipment market. Industry 4.0 adoption, retrofit activity, and the shift toward connected CNC platforms with robotic loading and inline measurement are also changing purchasing priorities, helping Germany's turning machine and equipment market move from stand-alone lathes toward integrated turning cells and multitasking systems. Order weakness in automotive, stronger competition from Asian suppliers, and a persistent skilled labor shortage still limit the pace of expansion. Yet, the late-2025 order recovery and steady demand from defense, medical, electronics, and machinery applications supports sustained investment in turning machine and equipment through 2031.

Key Report Takeaways

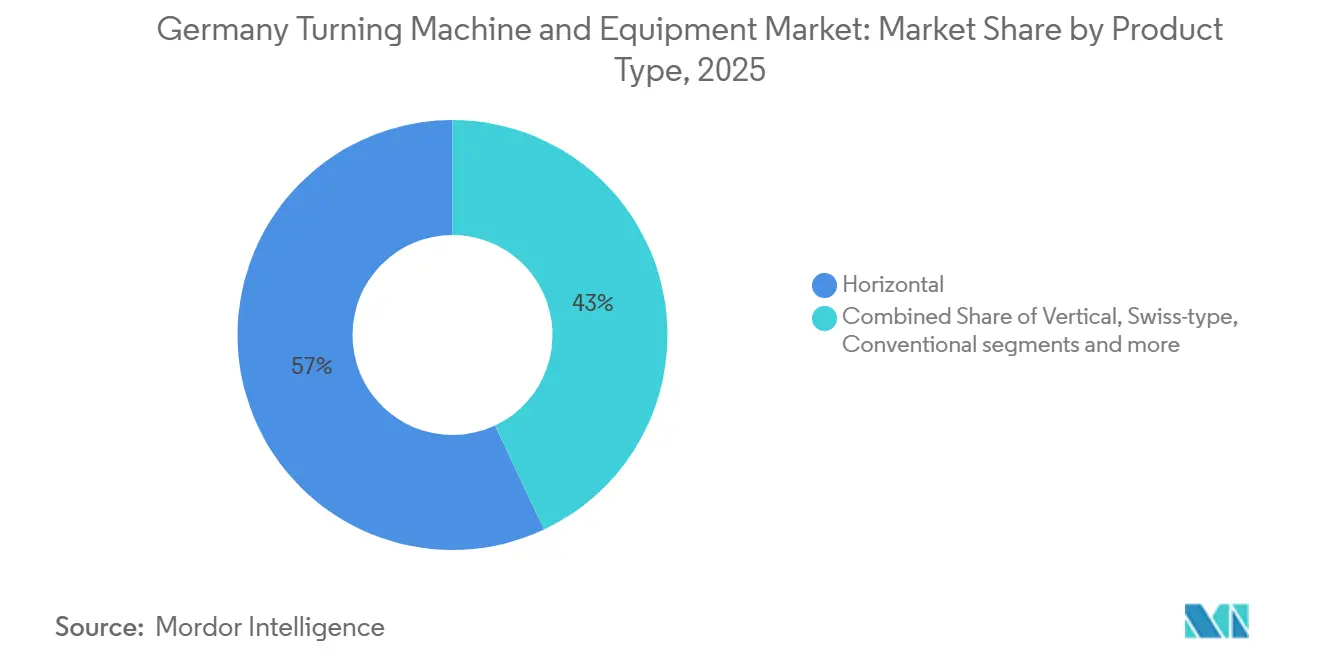

- By product type, the horizontal segment led with a 57% share in 2025, while the multitasking segment is forecast to post a 6.5% CAGR through 2031.

- By automation type, fully automatic CNC held 88% of the Germany turning machine and equipment market share in 2025 and is projected to expand at a 6.3% CAGR through 2031.

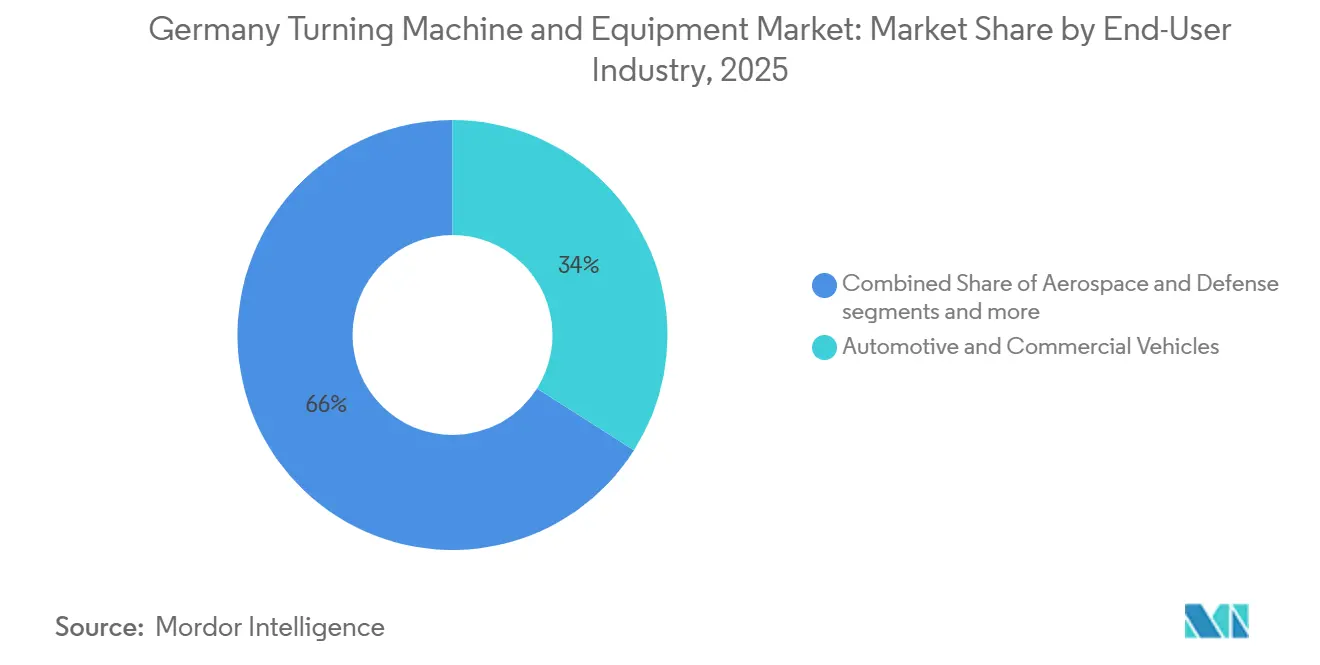

- By end-user industry, automotive and commercial vehicles accounted for 34% of the Germany turning machine and equipment market size in 2025, while aerospace and defense are forecast to record the highest CAGR at 6.7% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Turning Machine and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Germany's Strong Machine Tool Manufacturing Base | +1.2% | National, concentrated in Baden-Württemberg and Bavaria | Medium term (2-4 years) |

| Industry 4.0-Driven Machine Replacement | +1.0% | National, with early gains in Stuttgart, Munich, and Dortmund manufacturing clusters | Medium term (2-4 years) |

| Strong Demand from Industrial Machinery Manufacturing | +0.9% | National | Short term (≤ 2 years) |

| Export-Oriented Manufacturing Competitiveness | +0.8% | National, with spill-over to EU export markets | Medium term (2-4 years) |

| European Supply Chain Regionalization Supporting Domestic Machining Capacity Expansion | +0.7% | EU core, with primary gains in Germany, Poland, and the Czech Republic | Long term (≥ 4 years) |

| Growth in Medical Technology Manufacturing | +0.5% | National medtech clusters are concentrated in Bavaria, Baden-Württemberg, and Thuringia. | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Germany's Strong Machine Tool Manufacturing Base

Germany maintains one of the world’s most advanced and integrated precision-engineering ecosystems, and that foundation continues to give Germany a structural advantage in the turning machine and equipment market. Germany maintains strong domestic engineering capabilities, supported by significant investment in machinery R&D and innovation ecosystems. Buyers in aerospace, medical technology, and defense continue to value domestic sourcing because local builders can provide application engineering, co-development, and certified process integration with shorter response times than distant suppliers. The concentration of OEMs, tooling specialists, automation suppliers, and training institutions in Baden-Württemberg and Bavaria also supports repeat investment, as manufacturers can resolve process issues more quickly and upgrade production lines with less disruption. That cluster effect helps sustain demand in the Germany turning machine and equipment market even as broader capital spending becomes more selective.

Industry 4.0-Driven Machine Replacement

Digital modernization is now a practical purchasing issue rather than a pilot-stage concept in the Germany turning machine and equipment market.[1]itkom e.V., “Industrie 4.0 Studie 2025,” Bitkom, bitkom.org Bitkom reported in 2025 that 80% of German manufacturing companies planned to maintain or increase their Industry 4.0 spending, with process monitoring, automation, and machine connectivity named as priority areas. Depending on the machine condition and the scope of upgrades, retrofit investments can account for a significant share of the cost of a new machine. The VDW also stated during EMO 2025 that retrofit activity had moved into a more strategic role because users want connectivity and data visibility on machines that still have usable mechanical life. Germany’s installed base of older CNC lathes, therefore, creates a multi-year renewal pipeline for the Germany turning machine and equipment market, with demand coming from both new machine purchases and modular upgrade packages. Builders that can pair new platforms with automation cells, connectivity software, and retrofit support are gaining an edge, as customers seek lower integration risk and clearer productivity gains.[2]VDMA, “Ingenieur-Erhebung 2025,” Smart Production, smart-production.de

Strong Demand from Industrial Machinery Manufacturing

Industrial machinery manufacturing remains a steady demand source for the Germany turning machine and equipment market because it consumes large volumes of precision shafts, threaded parts, housings, and drive components. VDMA data showed that German machinery exports reached EUR 15.8 billion (USD 18.6 billion) in December 2025, a nominal increase of 2.7% year-over-year, underscoring the production scale that continues to support turning operations across many sub-industries. Producers in this sector depend on continuous machining output rather than occasional capacity additions, so turning machines and equipment often remain core production assets rather than discretionary purchases. Order conditions in machinery were also more resilient than in automotive during 2024 and 2025, which helped soften some of the weakness tied to powertrain-related turning demand. As machinery production shifts toward electrification-compatible systems, servo-hydraulic assemblies, and precision bearing applications, turning specifications are widening and favoring more capable equipment. This broadens the addressable workload base for the Germany turning machine and equipment market beyond traditional automotive part families.

Export-Oriented Manufacturing Competitiveness

Germany’s export model continues to shape the Germany turning machine and equipment market, as machine builders and end users both operate under strict productivity and quality requirements. German machine tool exports totaled EUR 1.43 billion (USD 1.63 billion) in 2025, which kept the country in the position of the world’s second-largest machine tool exporter despite weaker demand from the United States and China. Exports account for 70% of domestic machine tool production, so product competitiveness in turning centers directly affects revenue stability and technology reinvestment. The local-for-local production model also matters because 20% of total output is now produced at foreign sites, mostly in Europe, China, and the United States, thereby extending German technology standards into major manufacturing regions. That export discipline keeps pressure on suppliers to improve uptime, process integration, and tolerance performance, especially in aerospace, defense, electronics, and adjacent high-precision work. It also supports recurring domestic investment in premium CNC turning systems because local customers often want the same standards they are expected to meet in export markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Turning Systems | -1.2% | National, with disproportionate impact on SME job shops in rural Länder | Medium term (2-4 years) |

| Shortage of Skilled CNC Workforce | -1.0% | National, particularly acute in Lower Saxony, North Rhine-Westphalia, and Bavaria | Long term (≥ 4 years) |

| Competition from Asian Machine Tool Suppliers | -0.8% | National, with concentrated pressure in cost-sensitive mid-tier and job shop segments | Short term (≤ 2 years) |

| Cyclical Manufacturing Capital Expenditure | -0.7% | National, correlated to automotive and export manufacturing investment cycles. | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Turning Systems

The cost of advanced CNC turning systems continues to limit broader adoption in the Germany turning machine and equipment market, especially among small and medium-sized manufacturers. VDW reported that high costs and weak planning security were the main reasons many German manufacturers did not invest in new machine tools during 2025. This burden rises further when buyers also have to manage energy costs, logistics pressure, and tighter margins, which extends replacement cycles well beyond the technical optimum. The problem is more acute in lower-volume environments, such as aerospace prototyping or specialized defense work, where machine utilization may not be high enough to support rapid payback. Compliance demands such as CE conformity and quality management requirements add to the total ownership burden and can delay projects even when production needs are clear. As a result, the Germany turning machine and equipment market often sees customers choose staged retrofits, partial automation, or delayed purchases rather than full turnkey investments.

Shortage of Skilled CNC Workforce

The shortage of skilled CNC labor remains a structural limit on both machine utilization and new investment in the Germany turning machine and equipment market. DIHK found that 38% of mechanical engineering companies and 42% of metal production and processing firms struggled to fill open positions in late 2025, which places these industries among the most affected parts of German manufacturing. VDMA also noted that 20% of engineers in German machine and plant manufacturing are expected to retire within the next 10 years, while graduate pipelines in mechanical and manufacturing fields remain under pressure. CNC turning roles require familiarity with control systems such as Siemens, FANUC, and HEIDENHAIN, and these skills usually take years to develop through formal training and shop-floor experience. Germany’s Federal Employment Agency identified 163 bottleneck occupations in 2024, and machining-related positions remained prominent, which shows that the issue is not cyclical alone. Labor shortages encourage automation adoption but can also delay capacity expansion decisions due to a lack of qualified programming and operational personnel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Equipment Anchors Market Volume, While Multi-Tasking Systems Gain Momentum

The horizontal segment held 47.8% of the Germany turning machine and equipment market in 2025, which kept them as the largest product category across shaft, sleeve, and disc machining in automotive, energy, and general industrial applications. Their scale reflects a broad machining range, an established tooling ecosystem, and easier integration with pallet handling and robotic loading systems. The conventional segment continues to serve low-volume job shops and training environments, though its role is narrowing as CNC adoption deepens. The vertical segment remains relevant for large-diameter and heavy workpieces, where floor space efficiency and stable workpiece support are critical. Swiss-type machines continue to serve the production of small precision parts for medical devices, electronic connectors, and defense-related applications.

Multi-tasking turning centers are projected to record the fastest growth at a 6.5% CAGR from 2026 to 2031. Their expansion is tied to single-setup machining that combines turning, milling, drilling, and grinding, helping reduce cycle time, handling steps, and fixturing errors. German suppliers are actively strengthening this category through new product launches and broader compatibility with automation systems. The category is also gaining from demand among manufacturers that want complete machining capability without adding multiple standalone machines. This keeps multitasking systems well-positioned for further adoption through the forecast period.[3]European Commission, “Machinery Regulation EU 2023/1230,” European Commission, europa.eu

By Automation Type: Fully Automatic CNC Dominates Amid Persistent Workforce Constraints

Fully automatic CNC represented 88% of the Germany turning machine and equipment market in 2025, which reflects the mature automation profile of the country’s machining base. This high penetration is tied to decades of reinvestment by domestic builders and export-focused end users that need consistent output quality, lower scrap rates, and higher labor productivity. The DIHK labor shortage data has strengthened the case for automated turning cells because one operator can supervise more output when machines handle loading, monitoring, and repeat cycles with less manual intervention. EMAG’s MSC 5 DUO, presented for automated batch production, was explicitly positioned to address the twin pressures of skilled labor scarcity and cost inflation, which align with current buyer needs in the Germany turning machine and equipment market. The growing adoption of the VDW’s umati connectivity standard also enhances the value of fully automatic systems by improving data exchange with manufacturing execution systems and digital monitoring tools.

Fully automatic CNC is also expected to lead growth through 2031 with a 6.3% CAGR, indicating that the Germany turning machine and equipment market is moving further toward connected, unattended production models. Semi-automatic segment still has a role in prototyping, repair, and low-volume custom work where frequent human intervention remains useful. Manual turning machines are now largely limited to training centers and smaller repair workshops, and its share is likely to keep shrinking as digital standards become more important. As major control platforms and machine interfaces continue to modernize, the performance gap between fully automatic and lower-automation formats is likely to widen across the Germany turning machine and equipment market through the forecast period.

By End-User Industry: Automotive Maintains Scale as Aerospace and Defense Lead Growth

Automotive and commercial vehicles accounted for 34% of the Germany turning machine and equipment market in 2025, keeping the segment as the largest demand center despite a weaker recent investment appetite. The legacy turning workload in this segment still includes crankshafts, camshafts, connecting rods, and transmission parts produced at scale, so the installed base remains significant. At the same time, electrification is reducing some traditional powertrain demand, changing equipment needs rather than eliminating them. New EV-related requirements, such as rotor shafts, power electronics housings, and battery module components, are creating a different mix of turning applications with new process expectations. VDW identified automotive and its suppliers as the main source of domestic investment reluctance, although the 4% order recovery in Q4 2025 suggested that conditions had begun to stabilize.

Aerospace and defense is forecast to deliver the highest end-user CAGR of 6.7% through 2031, making it the clearest growth segment in the Germany turning machine and equipment market. This segment favors advanced turning capability because many parts require stable machining of difficult materials, repeat accuracy, and strong process control across smaller batch sizes. Safran Electronics & Defense announced an investment of EUR 50 million (USD 58.8 million) in June 2026 in a new defense precision manufacturing center in Ludwigsburg, which will directly expand the local supply chain for precision-turned components. Medical devices and surgical instruments also remain a stable source of demand because Germany’s medtech sector generated EUR 41 billion (USD 48.2 billion) in annual manufacturer revenue and continues to rely on high-precision turning for implants and instruments. In addition, electrical and electronics equipment, oil and gas, energy, and general industrial machinery represent secondary demand pillars that diversify the Germany turning machine and equipment market away from a single end-user cycle.

Geography Analysis

The demand in the Germany turning machine and equipment market is concentrated in Baden-Württemberg, Bavaria, and North Rhine-Westphalia because these Länder hold the densest mix of mechanical engineering, precision machining, and OEM production capacity. Baden-Württemberg remains the center of both turning machine production and domestic use because it combines leading builders such as INDEX-Werke and EMAG with strong automotive and precision parts ecosystems. Bavaria remains another strategically important region due to DMG MORI’s production facilities and concentration of advanced manufacturing sectors. DMG MORI opened a new training center in Pfronten in January 2026, totaling 4,500 sqm and with a capacity for 150 trainees, strengthening the region’s long-term skills pipeline for advanced CNC work. Bavaria’s High-Tech Agenda also supports the broader innovation environment, which favors the adoption of premium turning machine and equipment in the German market.

North Rhine-Westphalia is a major demand zone because it combines heavy industry, automotive supply activity, and a growing defense manufacturing presence across the Rhine-Ruhr corridor. Okuma opened its new Solution Center in Krefeld in March 2026 with 14 machines, including 8 fully automated systems, which shows the commercial importance suppliers attach to this part of Germany. Europe, including Germany, accounts for more than 60% of German machine tool sales, so suppliers use Germany both as a destination market and as a base for wider regional service and demonstration activity. The EU Machinery Regulation and CE compliance requirements also strengthen the position of suppliers that can deliver locally adapted and fully documented machines with lower approval risk.

Thuringia and Saxony are becoming more visible secondary demand centers as medtech and defense-related precision manufacturing expand in eastern Germany. Supply chain regionalization inside Europe is also encouraging multinational manufacturers to place more machining capacity in Germany, which adds demand above the normal replacement cycle. Citizen Machinery’s JPY 4 billion (USD 26.7 million) investment in a new European headquarters in Ostfildern, Baden-Württemberg, announced in October 2025, points to sustained long-term confidence in regional demand and local service needs. This pattern favors suppliers with established German sales, application support, and after-sales infrastructure, as buyers in the Germany turning machine and equipment market continue to value response time and process support as much as machine specifications.

Competitive Landscape

The Germany turning machine and equipment market remains moderately concentrated in the premium technology tier and fragmented across the mid-tier and specialty segments, where domestic, European, and Asian suppliers compete on different value propositions. German builders usually compete through application engineering depth, automation integration, digital connectivity, and long service support rather than on price alone. DMG MORI’s 2025 and 2026 expansion program, including new headquarters capacity in Munich and new training infrastructure in Pfronten, shows how leading suppliers are reinforcing their local technology and skills base rather than treating Germany as a mere sales market. INDEX-Werke’s introduction of new turn-mill and multi-spindle automation solutions at Open House 2026 follows a similar strategy, tying machine launches directly to robotic handling and in-process gauging. The EU Machinery Regulation also gives established suppliers in the Germany turning machine and equipment market an advantage because compliance, validation, and documentation now play a larger role in purchase decisions.

A major opportunity sits in the underconnected installed base, where many customers still need better links between turning machines, manufacturing execution systems, and shop-floor analytics. The VDW’s umati standard supports this transition by making data exchange more practical, which helps suppliers win projects with stronger digital readiness and lower integration effort. Cost-sensitive buyers still attract smaller European challengers such as CMZ and Biglia, which means the Germany turning machine and equipment market remains contested outside the top automation tier. Japanese players such as Okuma and Citizen Machinery also maintain a durable position through local solution centers, demonstration capacity, parts support, and long-term physical investment in Germany.

Competition, therefore, centers less on a single machine sale and more on total operating support across the machine life cycle in the Germany turning machine and equipment market. Buyers increasingly favor vendors that can combine application engineering, automation cells, digital interfaces, training, and retrofit pathways within a single service relationship. Strategic moves by DMG MORI, INDEX-Werke, Okuma, and Citizen show that local presence remains a decisive competitive lever even as import competition rises. This leaves the Germany turning machine and equipment market open to international suppliers, but it does not remove the advantage held by companies with strong German engineering, compliance, and after-sales depth.

Germany Turning Machine and Equipment Industry Leaders

DMG MORI

INDEX-Werke

EMAG GmbH & Co. KG

Spinner

WFL Millturn

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: DMG MORI opened a 1,400 sqm expansion at its Stipshausen facility, extending production, logistics, and R&D capacity for ULTRASONIC turning-milling technology, and launched the ULTRASONIC 80 Precision as a world premiere at the Ultrasonic Technology Days, targeting hard and brittle material machining for aerospace and medical device applications.

- June 2026: Safran Electronics & Defense announced an approximately EUR 50 million (USD 58.8 million) investment to build a new defense precision manufacturing center in Ludwigsburg, Baden-Württemberg, creating approximately 200 jobs and directly expanding Germany's precision-turned defense component supply chain.

- March 2026: Okuma Europe opened its new Solution Center in Krefeld, Germany, featuring 14 CNC machines, including 8 fully automated turning and machining systems. The facility serves as Okuma's European operational headquarters and serves customers across Germany and Benelux.

- March 2026: INDEX-Werke held Open House 2026 in Deizisau, launching the INDEX G160 turn-mill center, a compact, highly configurable turn-mill platform, and the Traub MS12-4 multi-spindle sliding and fixed headstock turning automatic, alongside the iXcenter robotic automation module enabling automated workpiece unloading and in-process gauging on multi-spindle turning machines.

Germany Turning Machine and Equipment Market Report Scope

The Germany Turning Machine and Equipment Market is Segmented by Product Type (Horizontal, Vertical, Swiss-Type, and More), by Automation Type (Manual, Semi-Automatic, and Fully Automatic CNC), and by End-User Industry (Automotive & Commercial Vehicles, Aerospace & Defense, Medical Devices & Surgical Instruments, Oil, Gas, & Energy, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal |

| Vertical |

| Swiss-Type |

| Multi-Tasking |

| Conventional |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive & Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices & Surgical Instruments |

| Oil, Gas, & Energy |

| Electrical, Electronics & Semiconductor Equipment |

| General Industrial Machinery |

| Others (Consumer Goods, Defense Ordnance) |

| By Product Type | Horizontal |

| Vertical | |

| Swiss-Type | |

| Multi-Tasking | |

| Conventional | |

| By Automation Type | Manual |

| Semi-Automatic | |

| Fully Automatic CNC | |

| By End-User Industry | Automotive & Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices & Surgical Instruments | |

| Oil, Gas, & Energy | |

| Electrical, Electronics & Semiconductor Equipment | |

| General Industrial Machinery | |

| Others (Consumer Goods, Defense Ordnance) |

Key Questions Answered in the Report

What is the 2031 outlook for turning machine and equipment demand in Germany?

The Germany turning machine and equipment market is projected to reach USD 0.9 billion by 2031, up from USD 0.7 billion in 2026, advancing at a 5.2% CAGR over 2026-2031.

Which product category currently leads equipment demand in Germany?

Horizontal segment led in 2025 with a 57% share, as it remains the core format for high-volume shaft, sleeve, and disc machining.

Which automation format is expanding fastest across German turning shops?

Fully automatic CNC is both the dominant and fastest-growing automation type, holding 88% share in 2025 and posting a projected 6.3% CAGR through 2031.

Why are German manufacturers replacing older turning machines now?

Replacement is being driven by Industry 4.0 investment, better machine connectivity, retrofit economics, and labor shortages that make automation more valuable.

Which end-user segment offers the strongest growth potential through 2031?

Aerospace and defense is expected to record the highest CAGR at 6.7% through 2031, supported by precision machining needs and new defense manufacturing investment.

What are the main factors limiting broader investment in advanced turning systems?

High acquisition costs, weak planning security, skilled labor shortages, and stronger competition from Asian suppliers continue to slow some purchase decisions.

Page last updated on: