Germany Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 2.10 Billion |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 2.20 Billion |

| Market Size (2031) | USD 2.9 Billion |

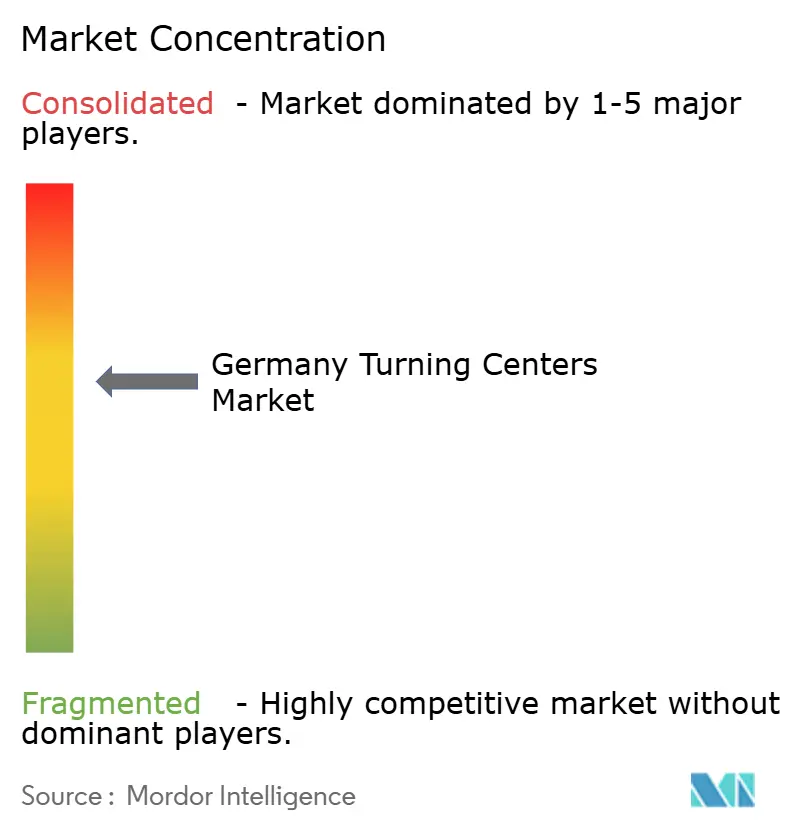

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Turning Centers Market Analysis by Mordor Intelligence

The Germany Turning Centers Market size is expected to grow from USD 2.10 billion in 2025 to USD 2.20 billion in 2026 and is forecast to reach USD 2.9 billion by 2031 at 5.68% CAGR over 2026-2031.

The Germany turning centers market entered 2026 with stronger order momentum after a difficult 2025, when German machine tool production fell 8% to USD 15.0 billion and domestic orders remained under pressure. The recovery pattern is supported by a 15% rise in German machine tool order intake in Q1 2026 and an 8% increase in exports to the United States in the same period, according to the German Machine Tool Builders’ Association (VDW), which has improved the near-term outlook for the Germany turning centers market. Demand is also being reshaped by changes in electric vehicle production, higher defense spending, and broader digital manufacturing programs that are pushing customers toward more capable, connected equipment. At the same time, the Germany turning centers market still faces high electricity costs, labor constraints, and tougher mid-market competition from Chinese suppliers, even while premium German OEMs remain well placed in aerospace, defense, and medical machining. The growth path to 2031 rests on the continued need for turning centers across Germany’s changing industrial base, where customers are balancing cost pressure with the need for tighter tolerances, digital integration, and shorter process chains.

Key Report Takeaways

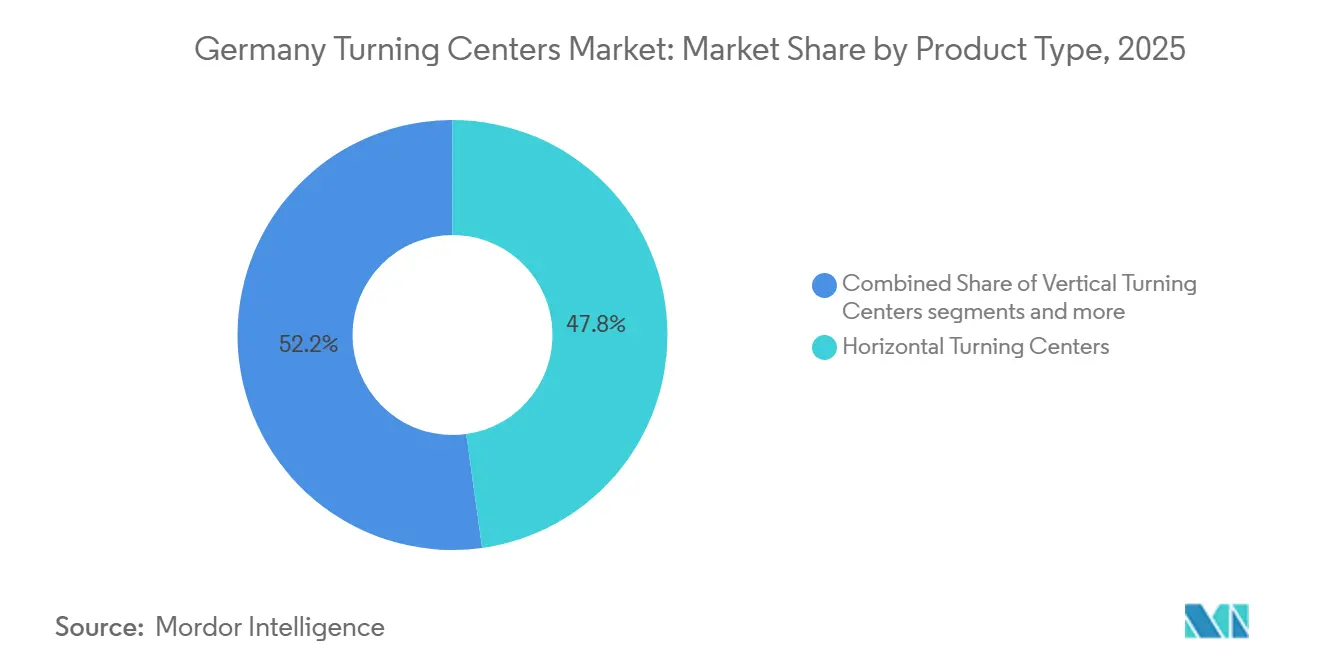

- By product type, horizontal turning centers accounted for 47.8% of the Germany turning centers market size in 2025, while multi-tasking turning centers are projected to expand at a 6.5% CAGR through 2031.

- By axis configuration, 4-axis turning centers accounted for 49.2% of the Germany turning centers market size in 2025, while 5-axis and above configurations are forecast to grow at a 7.8% CAGR through 2031.

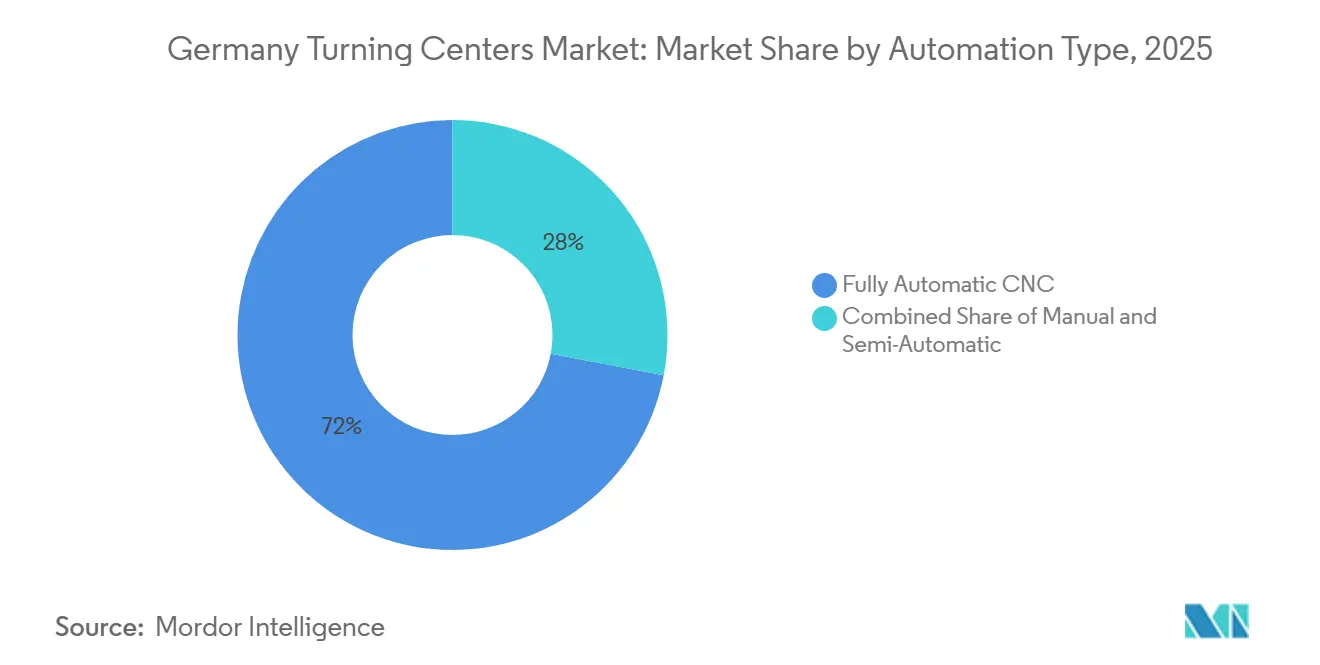

- By automation type, fully automatic CNC held 72% of the Germany turning centers market share in 2025, and the same segment is projected to grow at a 5.8% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles accounted for 45% of the Germany turning centers market size in 2025, while aerospace and defense are forecast to expand at a 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Transition Driving Drivetrain Turning Center Retooling | +1.4% | Germany, especially Munich, Stuttgart, and Berlin, with spillover to the wider EU supply chain | Medium term (2-4 years) |

| Increased Defense Spending Following NATO's 2% GDP Commitment | +1.1% | Germany, especially Bundeswehr procurement channels, has wider EU defense industrial effects. | Short term (≤ 2 years) |

| United States Export Growth Boosting Demand for German Turning Center OEMs | +0.9% | Germany and the North America export corridor | Short term (≤ 2 years) |

| Industry 4.0 Investments Supporting Premium Turning Center Upgrades | +0.8% | Germany and the DACH region, with wider platform spillover | Medium term (2-4 years) |

| Aerospace Recovery and Airbus Ramp-Up Sustaining 5-Axis Turn-Mill Demand | +0.7% | EU aerospace hubs, especially Hamburg and Toulouse, linked suppliers with North America. | Medium term (2-4 years) |

| Strong Domestic OEM Ecosystem Enabling Short Lead-Time Machine Procurement | +0.5% | Germany, especially Baden-Württemberg, Bavaria, and North Rhine-Westphalia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Transition Driving Drivetrain Turning Center Retooling

Electric drivetrain parts require tighter bore, cylindricity, and surface tolerances than many internal combustion components, which is changing procurement priorities in the Germany turning centers market.[1]SIPRI, “Trends in World Military Expenditure, 2025,” SIPRI, sipri.org This shift favors 4-axis and 5-axis turn-mill platforms because single-setup machining is becoming increasingly important for electric-drive housings and related precision parts in the Germany turning centers market. BMW Group’s move to convert its Munich plant to all-electric Neue Klasse production by the end of 2027 shows that this retooling cycle is already shaping plant-level investment decisions. The company’s additional EUR 200 million (USD 235.3 million) investment at Plant Landshut for electric-drive-unit central housings also shows that this demand is tied to real machining capacity rather than long-term planning. VDW’s customer structure data supports this transition because the automotive industry’s share of German machine tool output fell to 27.2%. In comparison, engineering rose to 30.1%, suggesting that newer precision applications in the Germany turning centers market are supplanting older powertrain demand. The result is not a simple loss of automotive demand, but a reallocation toward more complex machining work that needs better axis capability and stronger process control in the Germany turning centers market.[2]Bundestag, “2026 Budget, Defense Expenditure of 108 Billion Euros,” German Bundestag, bundestag.de

Increased Defense Spending Following NATO’s 2% GDP Commitment

Defense procurement is becoming a durable source of demand because many military systems require precision turned parts made from hardened alloys, titanium, and specialty steels. Germany’s military spending reached USD 114 billion in 2025, which was 24% higher than the prior year and equal to 2.3% of GDP, giving Germany's turning centers market a stronger non-automotive demand base. The 2026 defense budget reached EUR 108.2 billion (USD 127.3 billion) when the regular budget and the Sondervermögen special fund are combined. NATO’s June 2025 summit commitment to raise total defense and security spending to 5.0% of GDP by 2035 shows that elevated procurement activity is likely to persist beyond a single budget cycle. Germany’s state equipment investments rose 47.7% in 2025, reinforcing the view that physical capital formation tied to public-sector demand is already moving through the system. This gives the Germany turning centers market a second growth pillar, less tied to passenger vehicle capital expenditure and more tied to long-cycle industrial and security requirements.

United States Export Growth Boosting Demand for German Turning Center OEMs

The United States remained Germany’s largest machinery export market in 2025 at USD 27.7 billion, even though the full-year value was 8.0% lower than in 2024. That backdrop matters because export demand often stabilizes order books when domestic spending weakens in the Germany turning centers market. In Q1 2026, German machine tool exports to the United States rose 8%, the strongest regional result for the quarter and a clear sign of renewed traction for the Germany turning centers market. VDW’s commentary explains that the United States industry still needs German manufacturing technology because the domestic supply of advanced 5-axis turning and milling, multitasking, and medical precision applications remains limited. This creates a stable baseline export demand even when tariff concerns or policy noise affect sentiment in the Germany turning centers market. India’s emergence as Germany’s 3rd-largest machine tool export market in Q1 2026 also gives German OEMs another volume channel that can soften country-specific swings in the Germany turning centers market.

Industry 4.0 Investments Supporting Premium Turning Center Upgrades

Digital manufacturing investment is no longer discretionary for most large German manufacturers, which is supporting replacement demand in the Germany turning centers market.[3]Bitkom, “Industrie 4.0 Study 2025,” Bitkom, bitkom.org The German Association for Information Technology, Telecommunications, and New Media (BITKOM) found that 80% of German manufacturing companies planned to maintain or increase Industry 4.0 spending in 2025, and 96% said digital capabilities were essential for international competitiveness. Older turning machines that lack open communication protocols, digital twins, and real-time monitoring fit poorly into current smart factory layouts, so customers are replacing equipment earlier than normal in the Germany turning centers market. Germany’s Federal Ministry for Economic Affairs backed this direction with close to EUR 100 million (USD 117.6 million) in funded research programs under its Industrie 4.0-related initiatives. Acatech’s 2035 strategy work also shows that the digitalization of production is supported by a national technology roadmap rather than by isolated company spending. This keeps premium and connected platforms at the center of competitive positioning in the Germany turning centers market, especially where automation, traceability, and uptime are decisive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decline in Domestic Turning Center Demand | -0.9% | Germany, with secondary effects on wider EU machine tool order flows | Short term (≤ 2 years) |

| High Manufacturing Costs: Energy, Labor, and Regulatory Compliance | -0.8% | Germany, where electricity and labor costs remain elevated | Long term (≥ 4 years) |

| Intensifying Chinese Competition in Mid-Market and Emerging Export Channels | -0.7% | Global export markets, with direct pressure on Germany | Long term (≥ 4 years) |

| Skilled Worker Shortage Impacting Capacity Utilization | -0.6% | Germany, especially in mechanical engineering and precision manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Decline in Domestic Turning Center Demand

Although overall machine tool orders began recovering in Q1 2026, domestic demand remains below historical levels following the sharp contraction in 2025. German machine tool domestic new orders fell 16% in full-year 2025, while Q1 2025 recorded a 30% decline from a high prior-year base. Although export demand has improved, domestic investment remains cautious, particularly among automotive manufacturers. Capacity utilization in the German machine tool industry averaged 76% in 2025, which was 6.1 percentage points below the prior year and well below the long-run norm. VDW also noted that 12 of the largest German machine tool OEMs have foreign production sites, with 32% of output in China and 20% in the United States, indicating that investment has shifted outward when local demand is weak. The Germany turning centers market should improve from the 2025 trough in 2026, but a full return to the order environment seen in 2021 and 2022 still appears to be a medium-term event.

High Manufacturing Costs, Energy, Labor, and Regulatory Compliance

The cost base for German turning center manufacturing remains high, which limits the accessible customer pool for premium equipment in the Germany turning centers market. Germany’s industrial electricity price stood at EUR 17.99 cents per kWh (USD 21.2 cents per kWh) in January 2025 and stayed above the wider EU average. Even electricity-intensive companies with existing reductions paid EUR 10.04 cents per kWh (USD 118 cents per kWh) in September 2025, which was 57% above the comparable rate 5 years earlier. Labor costs add to that pressure because skilled machining roles remain difficult to fill, even though economic activity softened and some shortage measures improved. Upcoming machinery compliance requirements also add documentation and qualification work for advanced CNC systems with integrated software and sensors. These cost layers keep German OEMs focused on higher-margin configurations, but they also make price competition harder in the broader Germany turning centers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Machines Lead as Multi-Axis Centers Accelerate

Horizontal turning centers accounted for 47.8% of segment revenue in 2025, making them the largest product category in the Germany turning centers market. Their leadership reflects broad use in shaft turning, general industrial production, and established automation layouts across German plants. Existing workholding systems, operator familiarity, and line-level continuity support same-class replacement purchases, helping horizontal systems retain scale as end users shift more work to higher-complexity platforms. The installed base remains important, as many German shops balance new capability needs with proven process stability.

Multi-tasking turning centers are projected to grow at a CAGR of 6.5% from 2026 to 2031, making them the fastest-growing product type in the Germany turning centers market. This growth reflects demand for single-setup, complete machining in aerospace, medical, and precision automotive applications. Vertical turning centers remain important for large-diameter parts in the energy, heavy machinery, and defense industries. At the same time, Swiss-type and gang-slide machines continue to serve small precision parts for implants, electronics, and related applications. INDEX-Werke’s G160 5-axis turn-mill, designed for small, high-complexity parts with a 32,000 rpm spindle and 60 or 90 tool positions, and DMG Mori’s CTX 450 4A, with dual-spindle capability and up to 36 tool positions across two carriers for six-sided complete machining, show product development shifting toward compact, process-combining platforms. This supports a gradual migration pattern in which older horizontal assets remain productive. At the same time, new multitasking systems take on incremental jobs, allowing the Germany turning centers market to support both mature product classes and faster-growing turn-mill platforms simultaneously.

By Axis Configuration: 4-Axis Dominates While 5-Axis Gains Fast

4-axis turning centers accounted for 49.2% of revenue in 2025, making them the largest axis class in the Germany turning centers market. Their adoption remains strong among automotive suppliers, general industrial machinery manufacturers, and part families that require radial milling but not full simultaneous 5-axis motion. Many German shops already operate around 4-axis workflows, making like-for-like replacement attractive when uptime matters more than major process redesign. Cost discipline also supports this configuration, as it offers broader capabilities without the full price increase of more advanced systems. This keeps 4-axis platforms at the center of volume demand, supported by their relevance across a wide range of industrial applications, a large installed base, and manageable customer migration from 3-axis systems.

5-axis and above configurations are forecast to grow at a 7.8% CAGR from 2026 to 2031, the fastest rate among axis configurations in the Germany turning centers market. Rising demand from aerospace, defense, and medical applications is driving this growth, as these applications require fewer setups and tighter geometric accuracy. German OEM strengths in synchronized turn-mill software and B-axis integration remain difficult to replicate because they require deep application engineering. At the same time, 3-axis machines continue to serve batch production of simpler round parts where additional axes do not generate sufficient returns. WFL’s M70 MILLTURN, presented with workpiece handling capabilities of up to 8,000 mm in length and an 850 mm swing diameter, shows how axis-rich platforms address specialized, high-value large-component machining. Policy direction reinforces this trend, as the OECD’s 2025 Germany survey is expected to highlight manufacturing competitiveness as a national priority, supporting machines that deliver more operations per setup and stronger long-term productivity. The market mix is expected to shift toward higher-capability systems, even as 4-axis equipment remains the largest revenue pool.

By Automation Type: Fully Automatic CNC Anchors Market Share

Fully automatic CNC held 72% of revenue in 2025, giving them the largest share of the Germany turning centers market. This scale reflects Germany’s mature industrial automation landscape and the shift in new machine tool purchases toward CNC controls across most end users. Buyers increasingly compare control quality, connectivity, and adaptive functions rather than choose between CNC and non-CNC formats. As a result, this segment serves as both a maturity indicator and the primary platform for future differentiation, with software, integration quality, and service support carrying greater weight in purchase decisions.

Fully automatic CNC turning centers are also projected to be the fastest-growing automation segment in the Germany turning centers market, registering a CAGR of 5.8% from 2026 to 2031. BITKOM’s 2025 findings, which indicate that 44% of manufacturers plan to keep digital investment steady and 23% plan to increase it, support continued connected CNC upgrades. Semi-automatic machines still serve smaller job shops and training environments, while manual turning centers remain limited to training, specialty repair, and low-volume applications. However, rising labor costs, shorter automation payback periods, and the need for traceability and stable output are shifting competition toward control architecture, machine connectivity, unmanned operation, and adjacent automation functions. INDEX-Werke’s iXcenter robotic automation cell, which adds workpiece handling, measuring, deburring, and marking to multi-spindle turning operations, and Germany’s smart manufacturing framework, supported by Plattform Industrie 4.0 standards work, show how OEMs are extending automation beyond the base machine and strengthening the case for advanced systems in the Germany turning centers market.

By End-User Industry: Automotive Leads, Aerospace Rises Sharply

Automotive and commercial vehicles accounted for 45% of demand in 2025, making the segment the largest end user in the Germany turning centers market. The segment’s scale reflects Germany’s extensive OEM and Tier 1 supplier base across several industrial clusters. Demand is expected to remain resilient as fleet maintenance, selective upgrades, and early electric vehicle retooling help offset delays in larger-scale purchases. Despite uncertainty around electric platform transitions, automotive activity is likely to continue supporting utilization across many turning applications as its internal mix shifts toward newer component categories.

Aerospace and defense is forecast to grow at a CAGR of 7.2% from 2026 to 2031, making it the fastest-growing end user in the Germany turning centers market. Airbus targets 870 commercial aircraft deliveries in 2026, up from 793 in 2025, and is moving toward producing 70 to 75 A320 family aircraft per month by the end of 2027. This ramp is expected to support demand for 5-axis turn-mill capacity among suppliers manufacturing landing gear parts, structural elements, and engine-related housings. Medical devices, surgical instruments, oil and gas, energy, electronics, semiconductor equipment, and general industrial machinery keep the market diversified beyond automotive cycles. Quality and compliance requirements, including NADCAP and EN 9100, increasingly favor machines with strong process stability, robust documentation, service, validation, and long-term application support, shifting growth toward precision-focused applications over low purchase prices.

Geography Analysis

Germany is the only geography covered in this report, so regional demand patterns within the country shape the full revenue base of the Germany turning centers market. Baden-Württemberg and Bavaria remain the core demand centers because they host many of Germany’s precision machine tool OEMs and large customer clusters. These states are closely tied to automotive suppliers, aerospace machining, medical device manufacturing, and broader capital goods production. These states are also leading Germany's electric vehicle retooling, which is increasing demand for new component designs and more advanced turning center capabilities. Germany’s machine tool consumption fell 6% in 2025, and capacity utilization averaged 76%, underscoring why recovery in these industrial hubs matters so much for the Germany turning centers market.

Defense spending is adding a different regional demand pattern by directing procurement through military and industrial nodes in North Rhine-Westphalia and Bavaria. Germany’s 2026 defense budget reached EUR 108.2 billion (USD 127.3 billion), supporting equipment flows to manufacturers and maintenance networks that were less central in earlier planning cycles. This matters because the Germany turning centers market is no longer tied only to civilian automotive and general engineering programs. Eastern Germany is also becoming more relevant as policy and industrial investment support deeper manufacturing reinvestment. Destatis also reported that state equipment investments rose 47.7% in 2025, suggesting that public-sector demand is beginning to reach the capital goods base serving the Germany turning centers market.

North Rhine-Westphalia completes the main demand triad by contributing industrial machinery, energy equipment, and supplier volumes for broader German manufacturing. The machine tool sector employed around 64,500 people in 2025, so order decisions at the OEM level tend to spread quickly through the Mittelstand supply chain that underpins the Germany turning centers market. Germany Trade and Invest also highlighted machine tools as a backbone of European precision manufacturing, noting that sector R&D intensity exceeds 4% of revenue. India’s rise to the 3rd-largest export market for German machine tools in Q1 2026 provides German suppliers with another external demand channel, which can support capacity planning across several German regions.

Competitive Landscape

The Germany turning centers market shows moderate concentration in premium configurations, where German-headquartered OEMs remain strongest in 5-axis turn-mill and multitasking systems. That position rests on proprietary spindle designs, advanced control integration, and application engineering that has been built over many years. Japanese and Korean suppliers remain credible competitors in 3-axis and 4-axis categories, especially where customers balance performance and cost. Chinese manufacturers are gaining traction in the lower- to mid-priced segments, making pricing more difficult for mid-tier suppliers in the Germany turning centers market. VDW reported that China became the world’s leading machine tool exporter in 2025, with exports rising 18% to USD 9.5 billion, while German export volumes fell 10% to USD 7.7 billion.

Chinese export quality is also improving, as VDW noted a 40% increase in average export prices for Chinese metal-cutting machines in 2025. That does not erase Germany’s premium edge, but it narrows the competitive gap in less specialized configurations within the Germany turning centers market. INDEX-Werke’s High Dynamic Turning 2.0 is a useful example of how leading suppliers defend their position, because it adjusts the tool entry angle through synchronized control to support complex contour turning with fewer tool changes. DMG Mori’s MX strategy follows a similar logic by linking machine hardware with automation, monitoring, and connected services, turning the product into a broader production platform. VDW’s R&D review adds weight to this picture, as Germany ranked 4th in international machine tool patent applications, and more than 15% of revenue came from product innovations introduced in the previous 3 years.

White space remains most visible in automated medical machining cells, digital twin-ready defense maintenance systems, and compact multitasking machines for semiconductor-related parts. These areas fit the Germany turning centers market because they combine precision, traceability, and higher service intensity. Strategic moves by leading companies underline this direction. INDEX-Werke launched the G160 5-axis turn-mill center and the iXcenter automation cell in 2026, while DMG Mori introduced the CTX 450 4A in early 2026 and had already expanded its offer with the NLX 2500 second generation in late 2025. The competitive center of gravity in the Germany turning centers market is therefore moving toward software intelligence, process consolidation, and deeper automation rather than mechanical precision alone.

Germany Turning Centers Industry Leaders

DMG Mori

INDEX-Werke GmbH

EMAG GmbH & Co. KG

Spinner AG

Yamazaki Mazak

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: INDEX-Werke launches the G160 5-axis turn-mill center at its Open House 2026 (iXperience Center, Deizisau), the smallest model in the G-Series family. Designed for single-setup machining of small, high-complexity parts, it features a 32,000 rpm direct-drive spindle and a 60- or 90-tool magazine, targeting medical device, aerospace, and precision automotive sectors.

- March 2026: INDEX-Werke simultaneously introduces the iXcenter robotic automation cell for multi-spindle turning machines, enabling automated workpiece handling, measuring, deburring, and marking in unmanned extended-shift production, addressing Germany’s skilled worker shortage at the machine level.

- March 2026: Siemens announces an investment of over EUR 200 million (USD 235.3 million) to build a next-generation intelligent factory at its Amberg, Germany, campus by 2030, reinforcing domestic precision manufacturing capacity and signaling continued demand for advanced CNC turning equipment in Germany’s electronics industrial complex.

- January 2026: DMG Mori premieres the CTX 450 4A universal turning center, featuring dual-spindle capability and up to 36 tool positions across 2 tool carriers with 6 µm positioning accuracy, enabling complete 6-sided machining in a compact footprint for mid-size component producers.

Germany Turning Centers Market Report Scope

The Germany Turning Centers Market Report is Segmented by Product Type (Horizontal, Vertical, and More), Axis Configuration (3-Axis, 4-Axis, 5-Axis & Above), Automation Type (Manual, Semi-Automatic, Fully Automatic CNC), End-User Industry (Automotive, Aerospace & Defense, Medical, Oil & Gas, Electrical & Electronics, General Industrial, Others). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Turning Centers |

| Vertical Turning Centers |

| Multi-Tasking Turning Centers |

| Others |

| 3-Axis |

| 4-Axis |

| 5-Axis and Above |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive and Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices and Surgical Instruments |

| Oil, Gas, and Energy |

| Electrical, Electronics and Semiconductor Equipment |

| General Industrial Machinery |

| Others |

| By Product Type | Horizontal Turning Centers |

| Vertical Turning Centers | |

| Multi-Tasking Turning Centers | |

| Others | |

| By Axis Configuration | 3-Axis |

| 4-Axis | |

| 5-Axis and Above | |

| By Automation Type | Manual |

| Semi-Automatic | |

| Fully Automatic CNC | |

| By End-User Industry | Automotive and Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices and Surgical Instruments | |

| Oil, Gas, and Energy | |

| Electrical, Electronics and Semiconductor Equipment | |

| General Industrial Machinery | |

| Others |

Key Questions Answered in the Report

What is the expected value of Germany turning centers by 2031?

The Germany turning centers market is forecast to reach USD 2.9 billion by 2031, rising from USD 2.2 billion in 2026 at a 5.68% CAGR over 2026-2031.

Which product type leads demand in Germany?

Horizontal turning centers led product demand, with a 47.8% revenue share in 2025, supported by widespread use in automotive shafts, general engineering, and existing automation layouts.

Which axis configuration is growing the fastest?

5-axis and above machines are projected to expand at a 7.8% CAGR through 2031, driven by aerospace, defense, and medical applications that need fewer setups and tighter tolerances.

Why is aerospace and defense becoming more important for turning center demand in Germany?

Aerospace and defense is the fastest-growing end-user segment, with a 7.2% CAGR to 2031, supported by Airbus's production ramp-up and Germany’s much higher defense spending.

What is driving upgrades toward fully automatic CNC systems?

Fully automatic CNC held 72% share in 2025 and is still the fastest growing automation segment at 5.8% CAGR, helped by labor constraints, digital factory investment, and demand for connected machining.

What are the main risks to demand over the next few years?

The main restraints are weak domestic demand, high electricity and labor costs, stronger Chinese competition in the mid-market, and ongoing skilled worker shortages.

Page last updated on: