Germany Robotics CNC Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

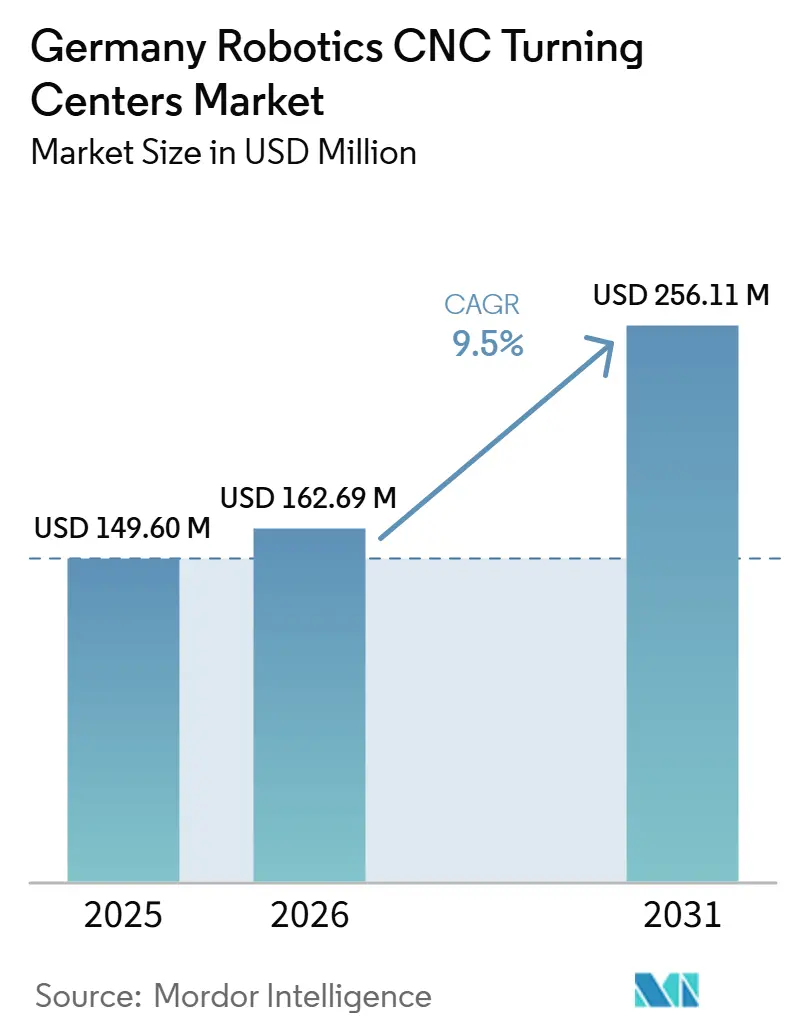

| Base Year Market Size (2025) | USD 149.60 Million |

| Market Size (2026) | USD 162.69 Million |

| Market Size (2031) | USD 256.11 Million |

| Growth Rate (2026 - 2031) | 9.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Robotics CNC Turning Centers Market Analysis by Mordor Intelligence

The Germany Robotics CNC Turning Centers Market size was valued at USD 149.60 million in 2025 and is estimated to grow from USD 162.69 million in 2026 to reach USD 256.11 million by 2031, at a CAGR of 9.5% during the forecast period (2026-2031).

The Germany robotics CNC turning centers market is moving faster than it did in 2020-2025, because EV production programs, open machine communication standards, and public support for AI-based robotics now reinforce one another. Germany’s machine tool sector generated EUR 14.8 billion (USD 17.4 billion) in 2024, with machines alone contributing EUR 10.3 billion (USD 12.1 billion), underscoring the industrial depth supporting robot-ready turning capacity. This industrial depth matters because the Germany robotics CNC turning centers market depends on a steady base of precision production, application engineering, and after-sales support rather than on isolated equipment demand. The Germany robotics CNC turning centers market is also benefiting from stronger interoperability, as UMATI (Universal Machine Technology Interface) and OPC UA (Open Platform Communications Unified Architecture) reduce integration friction across mixed-machine environments. At the same time, the Germany robotics CNC turning centers market faces tighter cost controls and a more demanding compliance path, pushing suppliers to compete on precision, software, modular automation, and service depth rather than price alone.

Key Report Takeaways

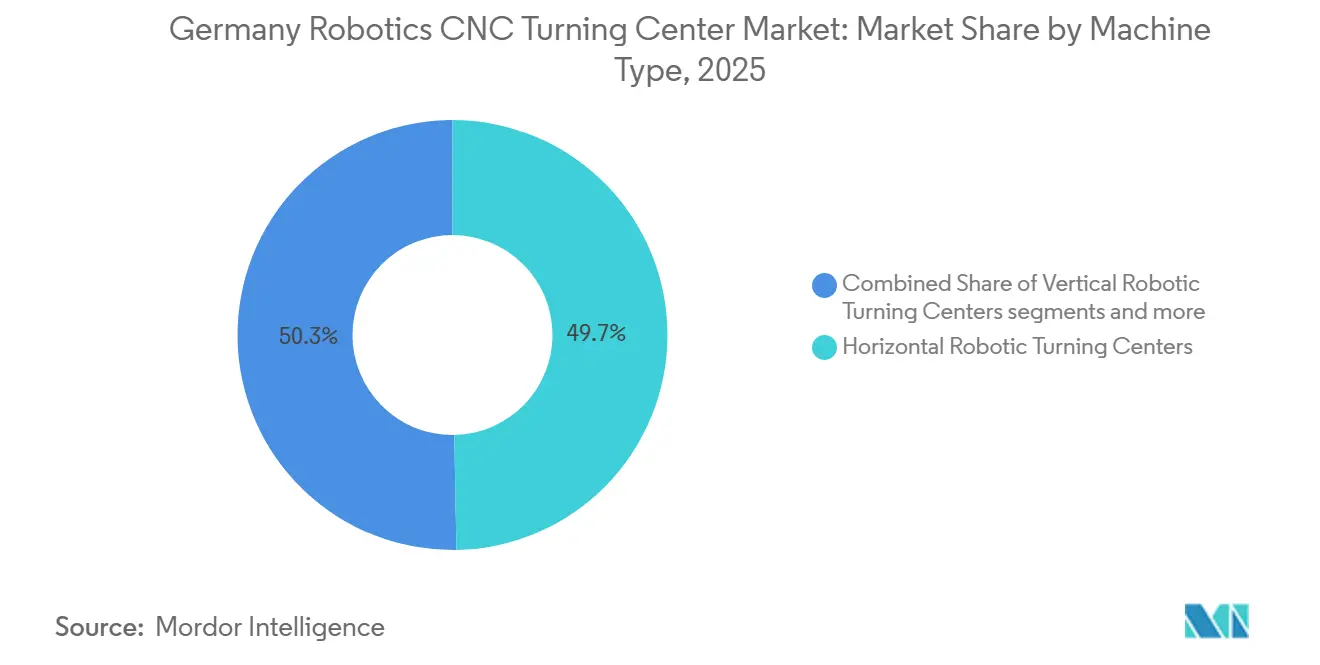

- By machine type, horizontal robotic turning centers held 49.71% of the Germany robotics CNC turning centers market share in 2025, while multi-tasking robotic turning centers are forecast to expand at 11.24% CAGR through 2031.

- By robot type, articulated robots held 56.2% of the Germany robotics CNC turning centers market share in 2025, while collaborative robots are projected to grow at 12.6% CAGR through 2031.

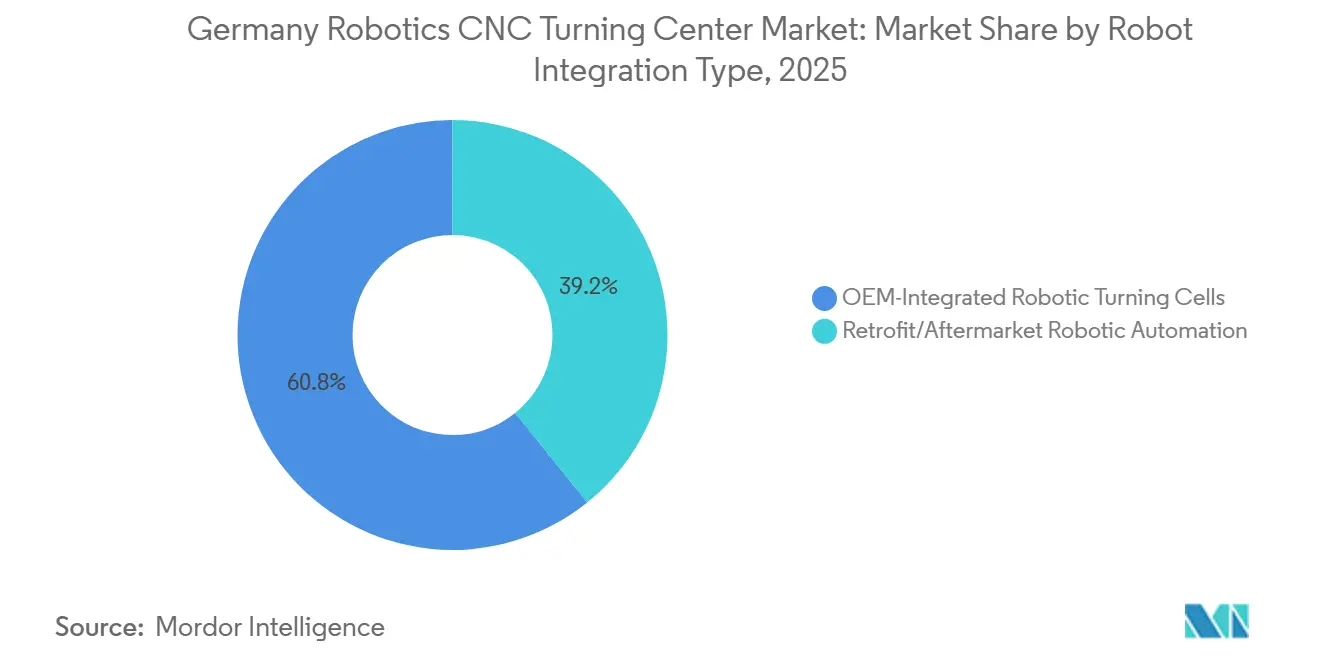

- By robot integration type, OEM-integrated robotic turning cells accounted for 60.8% of the Germany robotics CNC turning centers market share in 2025, while retrofit/aftermarket automation is projected to grow at 13.2% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles accounted for 38.1% of the Germany robotics CNC turning centers market size in 2025, while medical devices and surgical instruments are forecast to advance at 10.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Robotics CNC Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Automotive Demand for Robot-Tended EV Powertrain Turning | +2.6% | Bavaria, Baden-Württemberg, NRW | Medium term (2-4 years) |

| Strong Manufacturing Base Driving Investment in Advanced CNC Automation | +1.9% | Germany-wide, with spillover into EU export markets | Long term (≥ 4 years) |

| World-Leading Robot Density Supporting Mature Integration | +1.5% | Germany-wide, with a strong presence in Stuttgart, Munich, and the Rhine-Ruhr corridors | Long term (≥ 4 years) |

| Government R&D Funding Targeting Human-Robot Interaction | +1.1% | Nationwide, led by Munich, Karlsruhe, and Kaiserslautern research centers | Medium term (2-4 years) |

| German Machine Tool Builders Embedding Automation in Product Design | +0.8% | Baden-Württemberg and Bavaria, with global deployment through OEM networks | Long term (≥ 4 years) |

| UMATI Reducing Robot-CNC Integration Complexity | +0.6% | Global, with the strongest near-term relevance in Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strong Automotive Demand for Robot-Tended EV Powertrain Turning

The shift in automotive powertrain design toward electric drivetrains is lifting the Germany robotics CNC turning centers market. CNC turning centers with robotic loading are now central to the production of EV motor shafts, rotor cores, and gearbox assemblies. BMW Group launched pre-series production of the Neue Klasse central e-drive housing at Plant Landshut in October 2024 after a EUR 200 million (USD 235.3 million) investment, and the site had already received EUR 1 billion (USD 1.2 billion), since 2020, with EUR 500 million (USD 588.2 million) directed to electromobility. ZF Friedrichshafen also expanded its Saarbrücken plant for additional electric axle drive variants, with series production beginning in 2025. These programs are raising tolerance requirements and making robotic loading less of an efficiency option and more of a production requirement. The effect is spreading beyond Tier 1 suppliers, as Tier 2 precision turned parts manufacturers in Baden-Württemberg and Bavaria are also retrofitting robot cells to meet EV-related volume and quality targets.

Strong Manufacturing Base Driving Investment in Advanced CNC Automation

The Germany robotics CNC turning centers market is supported by one of the world's deepest machine tool production bases. Germany remained the second-largest machine tool producer in 2024, with a total output of EUR 14.8 billion (USD 17.4 billion) and a workforce of 65,500 across the sector. The country’s base of more than 1,200 machine tool and related companies, together with more than 50 recognized university research institutes, creates a self-reinforcing cycle between user demand and OEM innovation. German machine tool builders invest more than 4% of annual turnover in research and development, and 15% of turnover comes from newly developed products, which helps explain the strong level of process-integrated automation seen in the Germany robotics CNC turning centers market. A further layer comes from international production networks, as 12 larger German machine tool manufacturers now produce abroad, keeping domestic engineering centers closely linked to global automation rollouts. That linkage strengthens Germany’s role in control design, software integration, and cell architecture even when physical output is distributed across regions.

World-Leading Robot Density Supporting Mature Integration

The Germany robotics CNC turning centers market benefits from a robot base that is already large, dense, and experienced. Germany recorded 449 industrial robots per 10,000 manufacturing employees in 2024, which was the highest level in Europe and the 4th-highest globally.[1] International Federation of Robotics, “Robot Density Surges in Europe, Asia, and Americas,” IFR Press Release, ifr.org The country also installed 26,982 new industrial robots in 2024, which represented 32% of all annual robot installations in Europe. This installed base lowers adoption risk for the Germany robotics CNC turning centers market because engineers, integrators, and maintenance teams are already familiar with programming, safety, and uptime management. Germany also led Europe in robotics and automation foreign direct investment projects between 2019 and 2024, which signals continued confidence in the country as a location for robot-intensive manufacturing. High robot density also supports a broader peripheral ecosystem for grippers, vision systems, conveyor modules, and safety components, reducing both assembly time and friction from customization.

Government R&D Funding Targeting Human-Robot Interaction

The Germany robotics CNC turning centers market is also benefiting from public research funding directly relevant to flexible industrial production. The Federal Ministry of Education and Research established the Robotics Institute Germany on July 1, 2024, with a EUR 20 million (USD 23.5 million) budget for the period through June 2028, led by TUM, KIT, and DFKI. The program focuses on AI-based robotics, human-robot collaboration, intelligent manipulation, and autonomous task allocation, all of which translate well to robot-tended turning cells. In June 2026, the Federal Ministry for Research, Technology, and Space launched the Robo-Hubs initiative to connect academic robotics work with SME application needs, and production manufacturing was named as a priority area. This reduces part of the development burden for CNC OEMs and integrators, as some enabling capabilities are being built within the national research system. The result is a steadier pipeline of automation intelligence that can feed into the Germany robotics CNC turning centers market over the next several years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Sustainability and Regulatory Compliance Requirements Increasing Investment Complexity | -1.8% | EU-wide, with the most immediate effect in Germany | Medium term (2-4 years) |

| High Automation System Integration and Implementation Costs | -1.4% | Germany, especially among Mittelstand manufacturers in Baden-Württemberg, Bavaria, and NRW | Medium term (2-4 years) |

| Asian Manufacturers Erode Germany's International Market Share | -1.1% | Global export markets across Asia, Eastern Europe, and South America | Long term (≥ 4 years) |

| High Robot-Integrated Solution Costs Limit Mittelstand Adoption | -0.8% | Germany, especially firms with fewer than 250 employees | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Sustainability and Regulatory Compliance Requirements Increasing Investment Complexity

The Germany robotics CNC turning centers market faces a more stringent compliance burden as the EU Machinery Framework moves toward implementation in 2027. Regulation (EU) 2023/1230 will become mandatory from January 20, 2027, and adds new requirements around cybersecurity risk assessment, AI-related conformity evaluation, and digital technical documentation for machinery placed on the EU market.[2] European Parliament and Council of the European Union, “Regulation (EU) 2023/1230 on Machinery,” EUR-Lex, eur-lex.europa.eu This matters for robot-integrated turning cells because more of them now include adaptive control, vision-guided positioning, and software-based process intelligence. Germany also brought its national implementation framework into force through MaschinenDG on December 6, 2025, which established market surveillance powers and sanction provisions. Sustainability obligations add another cost layer through environmental management, energy-efficiency targets, and reduced fluid-disposal requirements. These factors stretch procurement timelines and make mid-cycle equipment replacement harder to justify, especially for smaller manufacturers with limited capital flexibility.

High Automation System Integration and Implementation Costs

The full-system cost of robot-integrated turning cells continues to constrain the Germany robotics CNC turning centers market. A typical cell can require USD 55,000 to USD 222,000 at 2025 average exchange rates, including the robot, tooling, fencing, inspection, programming, and commissioning. Actual integration costs also exceed initial budgets by 20% to 60% in many cases, due to protocol alignment and legacy machine interfaces that are more difficult than expected for Mittelstand manufacturers running only 3 to 5 CNC lathes, turning automation into a multi-year payback decision rather than a straightforward productivity upgrade. Robot-as-a-Service models, with monthly fees ranging from USD 550 to USD 3,300, ease some of the burden, but coverage remains uneven across regional manufacturing clusters. Cost uncertainty continues to delay buying decisions in the Germany robotics CNC turning centers market, especially when firms must train operators while supporting 2 generations of automation simultaneously.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Multi-Tasking Centers Challenge Horizontal Dominance

Horizontal robotic turning centers held 49.71% of the Germany robotics CNC turning centers market share in 2025. Their lead came from strong use in high-volume automotive shaft and bearing race production, where horizontal spindle architecture aligns well with bar feeders and gantry robot loading systems. This installed base keeps horizontal systems central to production programs that depend on repeatability, throughput, and stable automation layouts. The segment continues to benefit from its established role in large-scale industrial machining environments.

Multi-tasking robotic turning centers are the fastest-growing machine type in the Germany robotics CNC turning centers market, with a projected 11.24% CAGR during 2026-2031. Growth is being driven by rising demand in aerospace and medical device manufacturing, where complete machining in a single setup helps reduce part-handling errors, lower dimensional variation, and shorten the production sequence. OEM product development is also supporting this shift toward more capable platforms. DMG MORI’s January 2026 launch of the CTX 450 4A, with 36 tool positions, 6 μm positioning accuracy, and a compact 10 m² footprint, reflects this move toward higher-value and space-efficient turning platforms.

By Robot Type: Articulated Robots Anchor the Market, Cobots Expand the Addressable Base

Articulated robots held a 56.2% share in 2025, making them the leading robot type in the Germany robotics CNC turning centers market. They remain the default choice because they offer broad payload coverage, strong reach, and high compatibility with both direct spindle loading and gantry-assisted part presentation. Their programming environment is also mature because Germany’s automotive sector has used articulated robots at scale for many years. That maturity lowers engineering risk for new automation cells and keeps articulated robots central to large-volume installations. Gantry and Cartesian robots also retain a steady place where linear loading speed matters most, especially in throughput-driven component lines.

Cobots are expanding faster than any other robot type in the Germany robotics CNC turning centers market, with a forecast CAGR of 12.6% through 2031. Their adoption is rising in lower-risk loading tasks and in adjacent functions such as inspection support and tool-change assistance. That means cobots are widening the addressable base rather than replacing articulated robots in core production cells. IFR confirmed that Germany installed 26,982 industrial robots in 2024, the highest total in Europe, which supports ongoing reconfiguration and mixed robot deployment across plants. The German robotics CNC turning centers market is therefore evolving toward a layered robot mix where articulated units lead the main turning process, and cobots fill the flexibility gaps around it.

By Robot Integration Type: OEM Cells Lead, Retrofit Automation Accelerating

OEM-integrated robotic turning cells accounted for 60.8% of the Germany robotics CNC turning centers market in 2025, reflecting the preference among larger manufacturers for factory-engineered systems with aligned mechanical, control, and safety design. These buyers value one-source accountability because it simplifies commissioning and long-term service. OEM cells are especially strong where uptime, validation, and production continuity matter more than initial capex alone. At the same time, retrofit and aftermarket automation is the fastest-growing integration path, with a forecast CAGR of 13.2% through 2031. That growth reflects the logic of improving existing CNC turning assets when capital budgets are tighter and full machine replacement is harder to justify.

The retrofit channel is becoming more viable because interoperability standards have reduced part of the engineering burden in the Germany robotics CNC turning centers market. DMG MORI’s third-generation Robo2Go Turning, launched in January 2026 with up to 50% more workpiece storage capacity, shows how OEMs now treat robot automation as a core product layer rather than an optional add-on.[3]DMG MORI, “World Premiere, CTX 450 4A,” DMG MORI News, dmgmori.com At the same time, the UMATI framework and the November 2024 update to VDMA 40501-1 are improving plug-and-produce conditions across mixed machine populations. Independent systems integrators still lead most retrofit projects, which keeps the channel more open than the OEM-integrated side. That is why established suppliers are responding with certified integrator programs and modular robot kits for smaller shops that want lower customization risk.

By End-User Industry: Automotive Anchors Demand While Medical Devices Signal Premiumization

Automotive and commercial vehicles accounted for 38.1% of the market in 2025, making them the largest end-user segment in the Germany robotics CNC turning centers market. Germany’s role as Europe’s largest automotive manufacturing economy keeps this segment central, and the EV shift is adding fresh demand for precise turning of motor shafts, battery housing parts, and e-axle components. Production scale and tolerance requirements are both increasing, favoring robot-tended turning cells over manual loading. Aerospace and defense remain the next major demand source because titanium and nickel-alloy parts require consistent dimensional control over long machining cycles. Oil and gas, energy, electrical and electronics equipment, and general industrial machinery further diversify the customer base.

Medical devices and surgical instruments are projected to grow at a 10.9% CAGR through 2031, making them the fastest-expanding end-user segment in the Germany robotics CNC turning centers market. This growth is linked to Germany’s strong medtech position and the need for traceable, automated machining in line with ISO 13485 and EU MDR requirements. Buyers in this segment do not only need turning capability; they also need process control, measurement, and auditable data capture within the machining workflow. That pushes the German robotics CNC turning centers market toward higher-value cells with inspection and logging built into the process. The broader effect is premiumization, because sectors with stricter quality and documentation requirements are raising the technical standard for machines that were once specified mainly around cycle time.

Geography Analysis

The Germany robotics CNC turning centers market is concentrated most strongly in Baden-Württemberg, Bavaria, and North Rhine-Westphalia. Baden-Württemberg serves as the leading innovation hub because it brings together a dense base of machine tool OEMs, systems integrators, and automotive suppliers within a single regional cluster. Bavaria reinforces this position through BMW’s manufacturing base and the demand for aerospace and semiconductor machining in the greater Munich area. North Rhine-Westphalia adds a broad user base across commercial vehicles, steel processing, and heavy industrial machinery. Together, these corridors define where the Germany robotics CNC turning centers market sees the highest concentration of deployment capability, service support, and application engineering depth.

Germany’s machine tool sector employed 65,500 people in 2024, and research and development spending remained above 4% of turnover, with 15% of turnover coming from newly developed products. Lower Saxony and Hesse play a smaller but growing role in the Germany robotics CNC turning centers market, as they support automotive, chemical, pharmaceutical, and precision industrial demand. Saxony and Thuringia are also becoming more visible as secondary clusters, owing to federal support and lower real estate costs, which make them attractive for greenfield automation projects. As western clusters become tighter on space and labor, eastern regions are offering a practical expansion path for new robot-ready turning capacity.

The Germany robotics CNC turning centers market is also being shaped by how regional demand aligns with the EV investment cycle. Bavaria remains especially important because BMW’s Landshut and Munich operations continue to anchor precision component demand linked to electric drivetrains. Lower Saxony benefits from Volkswagen-linked demand for EV gearbox, axle, and fastening components. Baden-Württemberg continues to matter because of its OEM and supplier density, which allows new machine launches and integration services to move quickly into production environments. The VDW forecast of EUR 13.7 billion (USD 16.1 billion) in German machine tool production in 2026 points to a recovery supported by investments in mobility, climate, and digitalization. That recovery is likely to show first in regions where EV programs, service infrastructure, and advanced machining capacity already overlap most strongly.

Competitive Landscape

The Germany robotics CNC turning centers market has a moderately concentrated structure led by full-solution OEMs, but it still leaves room for robot suppliers, control specialists, and independent integrators. Domestic OEMs have an advantage because they can integrate spindle, control, safety, and robot design within a single engineering loop. That reduces commissioning time and simplifies the service relationship for customers who want a single accountable supplier. The strategic direction in the Germany robotics CNC turning centers market is platformization, where automation is sold as an extension of the machine rather than as a separate accessory. This is why leading suppliers are investing in standard robot packages, software layers, and validated installation layouts rather than relying solely on custom project work.

DMG MORI provides one of the clearest examples of this shift in the Germany robotics CNC turning centers market. Its third-generation Robo2Go Turning, launched in January 2026 with up to 50% greater storage capacity, shows how a premium OEM is pushing longer unattended operation and more compact deployment layouts. The January 2026 CTX 450 4A also points in the same direction, combining compact floor use with 36 tool positions and optional automation support. In October 2025, DMG MORI and HAIMER expanded their cooperation around digital tool management, which supports the data backbone needed for more automated turning cell operation.

The Germany robotics CNC turning centers market is also creating meaningful competitive space in retrofit and SME-focused modular cells. UMATI is lowering the interoperability barrier, helping smaller integrators build practical plug-and-play solutions around legacy turning centers. KUKA’s 2026 machine-tending demonstration with EMAG equipment, delivered through a Robot-as-a-Service model, also showed that robot suppliers are approaching CNC users more directly with capital-light offers. This matters because the retrofit channel still has no single dominant player, and smaller providers using vision systems, adaptive gripping, and simpler financing are pushing the minimum viable entry point downward. As a result, the Germany robotics CNC turning centers market is likely to stay competitive at both ends, with premium OEMs leading integrated cells and a broader field contesting the aftermarket automation opportunity.

Germany Robotics CNC Turning Centers Industry Leaders

DMG MORI AG

SPINNER Werkzeugmaschinenfabrik GmbH

EMAG GmbH & Co. KG

KUKA AG

INDEX-Werke GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: KUKA Robotics announced its participation at IMTS 2026, September 2026, Chicago, featuring live robotic machine-tending demonstrations pairing the KR CYBERTECH robot with EMAG's WPG 7 cylindrical grinding machine through Formic Automation's RaaS model, showcasing a capital-light, scalable adoption path for CNC machine tending.

- January 2026: DMG MORI unveiled the CTX 450 4A at its Pfronten in-house exhibition, a universal turning center with 36 tool positions, 6 μm positioning accuracy, and optional Robo2Go automation, targeting the Mittelstand segment with a compact 10 m² footprint designed for complete 6-sided machining of complex geometries.

- January 2026: DMG MORI released the third generation of its Robo2Go Turning system, expanding workpiece storage capacity by up to 50% and introducing optimized installation layouts, enabling longer lights-out production windows for small-to-medium batch sizes in Mittelstand turning operations.

- October 2025: DMG MORI and HAIMER GmbH expanded their strategic cooperation to accelerate toolroom digitization and global automation, establishing WinTool as the digital tool-management solution distributed through DMG MORI Technium worldwide and integrated with over 20 CAM systems and digital twin connectivity, advancing the data infrastructure underpinning automated turning-cell operation.

Germany Robotics CNC Turning Centers Market Report Scope

The Germany Robotics CNC Turning Centers Market is Segmented by Machine Type (Horizontal Robotic Turning Centers, Vertical Robotic Turning Centers, and More), by Robot Type (Articulated Robots, and More), by Robot Integration Type (OEM, Retrofit/Aftermarket Robotic Automation), and by End-User Industry (Oil, Gas, & Energy, Aerospace & Defense, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers |

| Multi-Tasking Robotic Turning Centers |

| Others |

| Articulated Robots |

| Collaborative Robots (Cobots) |

| Gantry/Cartesian Robots |

| OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation |

| Automotive & Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices & Surgical Instruments |

| Oil, Gas, & Energy |

| Electrical, Electronics & Semiconductor Equipment |

| General Industrial Machinery |

| Others |

| By Machine Type | Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers | |

| Multi-Tasking Robotic Turning Centers | |

| Others | |

| By Robot Type | Articulated Robots |

| Collaborative Robots (Cobots) | |

| Gantry/Cartesian Robots | |

| By Robot Integration Type | OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation | |

| By End-User Industry | Automotive & Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices & Surgical Instruments | |

| Oil, Gas, & Energy | |

| Electrical, Electronics & Semiconductor Equipment | |

| General Industrial Machinery | |

| Others |

Key Questions Answered in the Report

What is the forecast demand for Germany's robotics CNC turning centers by 2031?

The Germany robotics CNC turning centers market is forecast to reach USD 256.1 million by 2031, up from USD 162.7 million in 2026, with a 9.5% CAGR over 2026-2031.

Which robot type leads CNC turning automation in Germany?

Articulated robots led with 56.2% share in 2025 because they offer strong payload flexibility, reach, and well-established programming ecosystems.

Which integration route is growing the fastest in robotic turning cells?

Retrofit/aftermarket automation is growing the fastest, with a projected CAGR of 13.2% through 2031, as manufacturers look to upgrade existing CNC assets.

Why is automotive demand so important for robotic CNC turning in Germany?

Automotive and commercial vehicles held 38.1% share in 2025, and EV programs are raising demand for the precise turning of motor shafts, gearbox parts, and e-axle components.

What is driving the higher adoption of collaborative robots in German turning applications?

Collaborative robots are projected to grow at 12.6% CAGR through 2031 because they fit lower-risk loading, inspection support, and flexible shop-floor tasks that complement main production cells.

What is the biggest constraint on wider SME adoption?

High full-system costs remain the main hurdle, since a robot-integrated CNC turning cell can cost USD 55,000 to USD 222,000 before retraining and legacy integration work are factored in.

Page last updated on: