Germany Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

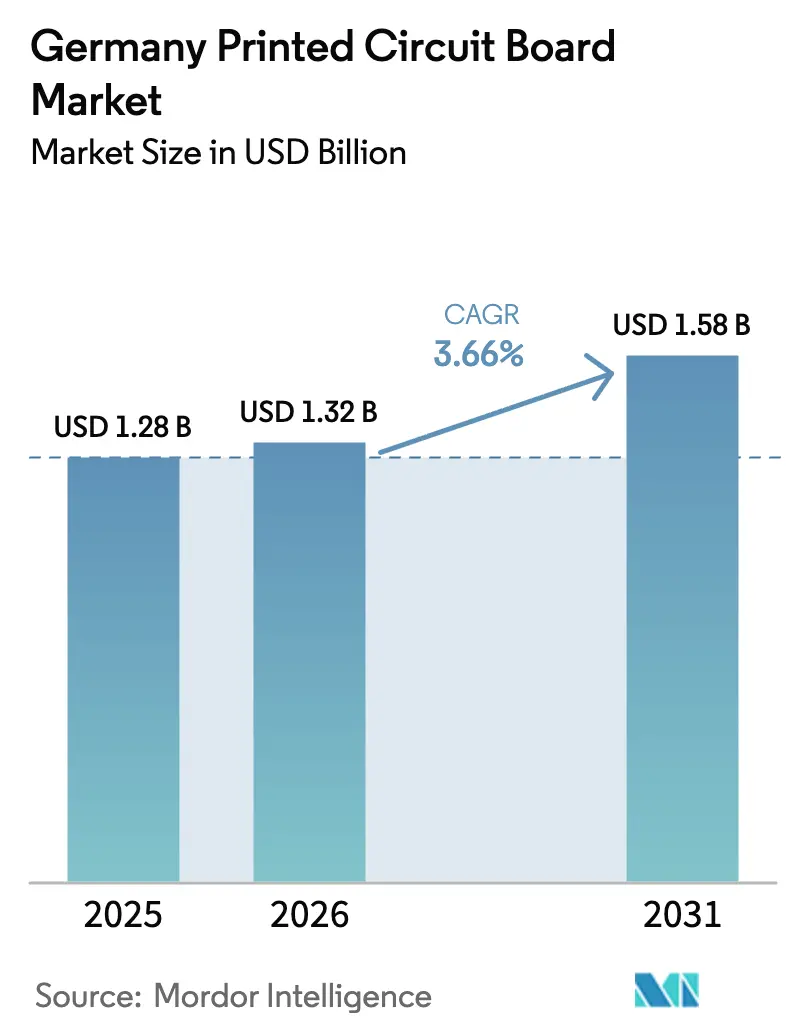

| Base Year Market Size (2025) | USD 1.28 Billion |

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

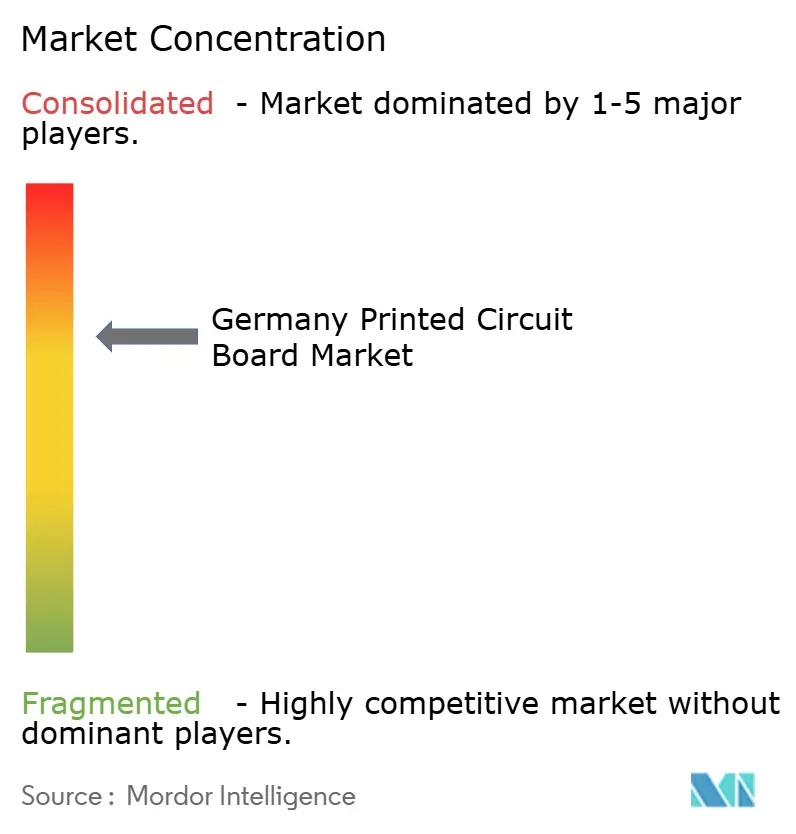

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Printed Circuit Board Market Analysis by Mordor Intelligence

The Germany printed circuit board market size is expected to increase from USD 1.28 billion in 2025 to USD 1.32 billion in 2026 and reach USD 1.58 billion by 2031, growing at a CAGR of 3.66% over 2026-2031. Demand is advancing in step with the country’s electrification push, 5G infrastructure build-out, and a growing need for rapid-prototype services. Price pressure in commodity multilayer boards tempers revenue gains, yet domestic fabricators benefit from a mix shift toward high-complexity products, IC substrates, and rigid-flex assemblies that preserve margins. Germany captures almost one-third of European PCB value output, confirming its role as the region’s anchor for advanced substrate manufacturing, material R&D, and quick-turn engineering support.

Key Report Takeaways

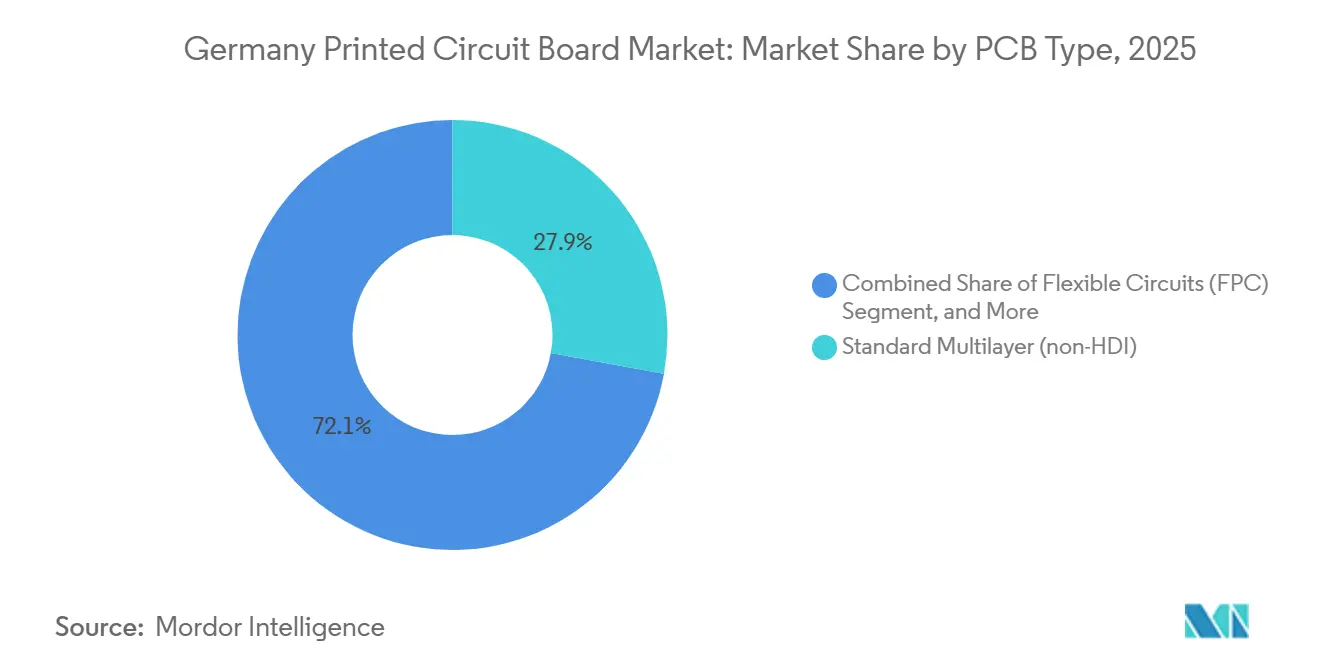

- By PCB type, standard multilayer PCBs led with 27.89% of the Germany PCB market share in 2025, while flexible circuits are projected to expand at a 5.07% CAGR through 2031.

- By substrate material, glass epoxy FR-4 commanded 41.63% of the Germany PCB market in 2025, whereas high-speed, low-loss laminates are forecast to grow at a 4.68% CAGR through 2031.

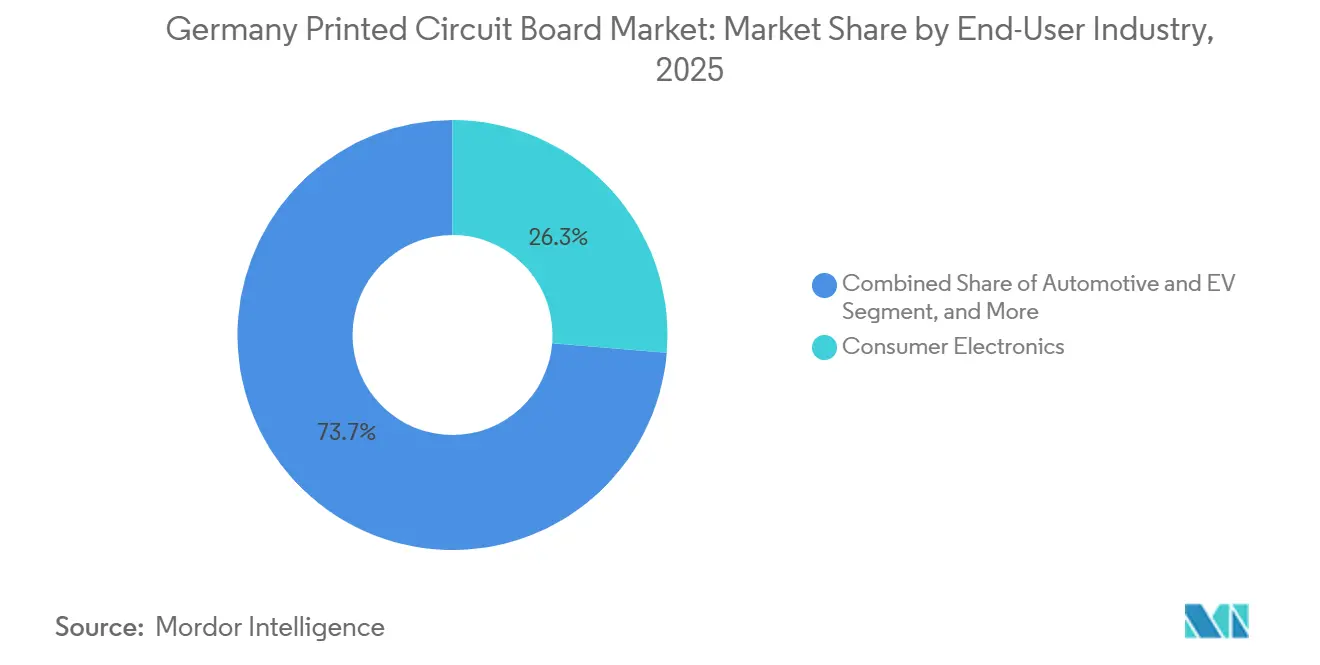

- By end-user industry, consumer electronics accounted for 26.31% of the Germany PCB market in 2025, while automotive and EV applications are projected to record the fastest 5.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of ADAS in German Automotive Sector | +1.2% | Germany and Central Europe automotive supply chain | Medium term (2-4 years) |

| Expansion of 5G Infrastructure Driving High-Frequency Boards | +0.9% | Urban and industrial corridors across Germany | Short term (≤ 2 years) |

| Growth in EV Production Requiring High-Thermal PCBs | +1.1% | Bavaria and Baden-Württemberg EV clusters | Medium term (2-4 years) |

| Miniaturization in Consumer Wearables Boosting Flex PCBs | +0.6% | Medical device hubs across Western Europe | Long term (≥ 4 years) |

| EU Chips Act Incentives for Domestic PCB Capacity | +0.5% | Saxony and Brandenburg semiconductor zones | Long term (≥ 4 years) |

| Industrie 4.0 Retrofit Kits Creating Quick-Turn Demand | +0.4% | SME manufacturing clusters in North Rhine-Westphalia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of ADAS in the German Automotive Sector

Automakers are embedding multiple radar, lidar, and camera modules in every new model, each employing rigid-flex or HDI substrates that integrate power management and high-speed serial connections inside a confined footprint. BMW plans to assemble 3 million battery-electric vehicles by 2027, with each platform consolidating formerly distributed electronic control units onto boards with more than 12 layers. Domestic fabricators able to deliver prototype lots within 10 working days secure preference, as vehicle programs now run on compressed 24-month cycles. Sensor boards alone lift PCB content by EUR 50 to EUR 80 per vehicle (USD 56.5 million to USD 90.4 million) and serve as both a heat spreader and a mechanical frame. As penetration of ADAS rises toward 95% of new cars, PCB throughput for automotive Tier 1 suppliers scales in tandem.[1]Germany Trade and Invest, “Automotive Electronics Sector Report 2024,” gtai.de

Expansion of 5G Infrastructure Driving High-Frequency Boards

Millimeter-wave base stations and massive MIMO antenna arrays require boards fabricated from low-loss laminates with dissipation factors below 0.003 at 28 GHz. Operators specify Rogers RO4000 and Isola Astra MT77 for front-end modules, materials priced 3-4 times above FR-4, yet essential to keep insertion loss under 0.5 dB. Data-center networks migrating to 800-gigabit Ethernet deploy motherboards with 20-24 layers and controlled-impedance traces routed to a ±5% window. Fabricators investing in laser direct imaging and automated optical inspection to achieve sub-75-micron line widths and generate early revenue. Research by the Fraunhofer Institute shows that 6G packaging will demand substrates with dielectric stability from −40 °C to +125 °C, reinforcing a shift toward advanced resin systems.[2]Fraunhofer IZM, “6G Packaging Technologies Research 2024,” izm.fraunhofer.de

Growth in EV Production Requiring High-Thermal PCBs

Battery management systems and traction inverters dissipate heat at densities above 10 W/cm², prompting the adoption of metal-core and ceramic-filled substrates capable of conducting more than 3 W/m · K. Webasto committed EUR 1 billion (USD 1.13 billion) to high-voltage heaters and battery thermal modules, each quoting PCBs that meet IPC Class 3 workmanship and IATF 16949 quality gates. Fraunhofer IPA measured polyimide composites with boron nitride fillers, achieving 5 W/m-K while retaining dielectric strength over 20 kV/mm, a benchmark for next-generation traction electronics. These designs rely on domestic suppliers that guarantee traceability for every laminate batch.[3]Fraunhofer IPA, “High-Thermal Laminate Materials Study 2024,” ipa.fraunhofer.de

Miniaturization in Consumer Wearables Boosting Flex PCBs

Wearable health devices and smartwatch modules require bend radii of less than 1 mm and dynamic flex life exceeding 100,000 cycles. Würth Elektronik’s PURE.flex line ships single-layer circuits with a coverlay thickness as low as 12.5 µm, enabling antennas for Bluetooth Low Energy and NFC. Liquid crystal polymer substrates limit moisture uptake to 0.04%, important for implantable sensors subject to bodily fluids. Collaboration with FELA on s.mask solder-mask technology increases elongation to over 50%, so traces survive repetitive bending. These capabilities underpin a 5.07% CAGR for flexible circuits and diversify Germany PCB market revenue into health-tech niches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper Prices Elevating Production Costs | −0.7% | All German PCB fabricators | Short term (≤ 2 years) |

| Stringent Environmental Regulations on Chemicals | −0.5% | EU-wide with Germany in the vanguard | Medium term (2-4 years) |

| Skilled Labor Shortage in Advanced PCB Fabrication | −0.4% | Precision manufacturing regions across Germany | Long term (≥ 4 years) |

| Chip-Level Component Shortages Slowing OEM Builds | −0.3% | Automotive, industrial, and telecom corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Copper Prices Elevating Production Costs

Copper accounts for up to 30% of multilayer material costs, and quarterly swings exceeding 20% erode margins when long-term customer contracts limit mid-cycle price resets. Smaller shops with turnover under EUR 50 million rely on spot buys, leaving them exposed to margin compression from 25% down to 15% during price spikes. Asian manufacturers possess vertically integrated smelters that temper input cost volatility, deepening the competitive gap. German players respond by pivoting toward high-complexity builds in which laminate and copper account for a smaller share of the selling price and where engineering value can be monetized.

Stringent Environmental Regulations on Chemicals

REACH and RoHS mandate elimination of brominated flame retardants and hexavalent chromium finishes, adding 3%-5% to process costs for mid-sized German plants. Documenting every laminate’s chemical profile now requires supply-chain traceability to raw-material lots, alongside annual certification budgets that can exceed EUR 100,000 (USD 113,000). Exemption extensions for aerospace solder alloys move through 18-24-month regulatory reviews, creating uncertainty for mixed-technology programs. Larger firms amortize compliance spend over a greater volume, but SMEs divert scarce cash from automation projects, slowing productivity gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Drive Momentum

The Germany printed circuit board (PCB) market for flexible circuits is forecast to expand at a 5.07% CAGR, outpacing the overall market by 1.41 percentage points. Sensor clusters, medical wearables, and foldable displays increasingly rely on polyimide-based interconnects to eliminate bulky wiring, reduce weight, and withstand continuous flexing. Rigid-flex assemblies that integrate stiff and pliant zones meet packaging constraints inside advanced driver-assistance modules and avionics trays. Domestic vendors leverage laser direct imaging to maintain line widths under 75 µm and provide 48-hour prototype cycles that automotive Tier 1 suppliers require. Meanwhile, standard multilayer boards retained 27.89% of the German PCB market share in 2025, yet face sustained price erosion as Asian contractors discount high-volume bids by 15%-25%.

German shops, therefore, steer commodity orders to partner fabs abroad and allocate domestic capacity to short-run, high-layer-count builds that keep gross margins over 30%. A second growth pocket lies in rigid-flex architectures that shrink cable harnesses by 30%-40% in robotics arms and MRI gantries. Würth Elektronik’s Advanced Solution Center delivers s.mask-enabled prototypes within five days, compressing customer validation cycles. Metal-core boards power LED luminaires, and ceramic substrates host RF power amplifiers used in 5G macro sites. Collectively, specialty boards lift the blended selling price in the German PCB market, cushioning declines in commoditized multilayer revenue.

By Substrate Material: Low-Loss Laminates Ascend

Glass epoxy FR-4 held 41.63% of the Germany printed circuit board (PCB) market share in 2025 because industrial and automotive designs below 1 GHz value its cost efficiency and mechanical stability. The shift to 5G and 800 GbE backplanes lifts demand for high-speed, low-loss laminates, which are projected to post a 4.68% CAGR to 2031. Rogers RO4000 and Isola Astra MT77 maintain dissipation factors below 0.003 at 28 GHz, enabling insertion loss under 0.5 dB per inch, far superior to FR-4’s 1 dB. German fabricators retool with plasma treating and vacuum lamination to manage resin flow on these premium materials.

Packaging resins such as Ajinomoto build-up film underpin flip-chip ball-grid-array and fan-out wafer-level packages, areas receiving EUR 10 billion (USD 11.3 billion) in German co-financing under the EU Chips Act. Polyimide remains the incumbent substrate for flexible circuits because its glass transition temperature exceeds 250 °C, an essential metric for solder reflow profiles on automotive under-hood boards. Liquid crystal polymer’s ultra-low moisture uptake meets implantable device standards, though limited converter capacity restricts scale. Research reported by Fraunhofer IZM projects sub-terahertz communications above 100 GHz will necessitate even tighter dielectric tolerances, opening space for novel resin chemistries that domestic laminate suppliers aim to commercialize by 2028.

By End-User Industry: Automotive Electrification Commands Investment

Automotive and EV lines are set to grow at 5.23% annually, injecting the largest incremental value into the Germany printed circuit board market. Battery management, traction inverters, and ADAS sensor clusters lift board content from EUR 120 to EUR 320 per vehicle, depending on platform architecture. German automakers demand domestic sourcing for prototypes and pre-series lots to safeguard intellectual property and speed design turns. Consumer electronics still capture 26.31% of 2025 revenue, anchored in premium audio, gaming accessories, and smart-home hubs produced by medium-sized contract manufacturers. Computing and data-center demand centers on 24-layer motherboards with tight impedance control to manage PCIe Gen 5 signaling at 32 GT/s. Telecom operators expand millimeter-wave coverage, driving RF board consumption higher, while industrial power electronics use metal-core substrates to dissipate more than 10 W/cm² in solar inverters and uninterruptible power supplies. Healthcare remains a reliable niche, requesting IPC Class 3 workmanship and ISO 10993 material compliance for implantables. Aerospace and defense programs specify rigid-flex assemblies with 100% lot traceability and employ conformal coatings that withstand −55 °C to +125 °C mission profiles. Each vertical accentuates the Germany printed circuit board market’s tilt toward high-mix, technology-intensive builds that fetch premium pricing.

A broader diffusion of demand across secondary sectors now reinforces the revenue base. Consumer electronics accounted for 26.31% of the Germany printed circuit board market in 2025, yet its future trajectory hinges on premium audio gear and smart-home controllers rather than on smartphones assembled abroad. Industrial and power applications are projected to advance at 3.4% as energy-storage systems, motor drives, and factory-automation controls adopt boards with metal-core or ceramic substrates that dissipate continuous heat loads above 10 W/cm². Healthcare shipments, although smaller in volume, rise at 4.1% as remote patient-monitoring and minimally invasive surgical tools specify flexible circuits that survive autoclave cycles at 134 °C. Aerospace and defense procurement cycles lengthen to 15-plus years, but programs demand IPC-6012 Class 3A certification, anchoring domestic volume in high-reliability builds. Finally, the telecom vertical, spanning small-cell radios and data-center switches, continues to shift toward low-loss laminates and 20-plus-layer stack-ups, entrenching local expertise in controlled-impedance routing. The diversified pull across these industries shields the Germany printed circuit board (PCB) market from sharp swings in any single end-user segment while rewarding plants that maintain multi-disciplinary engineering teams.

Geography Analysis

Germany accounts for 31.8% of European PCB output, with Bavaria and Baden-Württemberg clustering automotive electronics and EV platforms that require quick-turn prototypes and high-layer-count boards. Saxony and Brandenburg emerge as advanced packaging hubs, buoyed by EU Chips Act subsidies that lure IC substrate investments aligned with semiconductor fabs. North Rhine-Westphalia hosts thousands of small and mid-size enterprises installing Industrie 4.0 retrofit kits, a segment valued at EUR 4.9 billion to EUR 7.2 billion (USD 5.5 billion to USD 8.1 billion) by Platform Industrie 4.0, and these programs keep fast-cycle board demand local.

Eastern Europe, especially Poland, Czechia, and Hungary, attracts offshore green-field plants from Asian contractors, offering 40% lower labor costs than Germany for high-volume automotive builds. German shops counter by concentrating on low-volume, high-complexity orders and by automating laser drilling, direct imaging, and optical inspection to offset technician shortages. DACH as a block, Germany, Austria, and Switzerland collectively hold 51.8% of European capacity because automotive, medical, and industrial OEMs favor proximity for tight design loops and just-in-time delivery, preserving regional share despite lower-wage alternatives.

Western European states, including France, Italy, and Spain, still import most multilayer and HDI boards, yet coherent REACH and RoHS enforcement favors German exporters that already meet the strictest chemical thresholds. Future growth pockets in Germany align with semiconductor clustering around Dresden, where foundries require IC substrates with line widths below 10 µm. Skilled labor remains a constraint, as 33.8% of electronics firms reported open technician roles, driving deeper investment in cobots and machine-vision inspection to sustain throughput. Over the long term, regional specialization in Germany in quick-turn and advanced laminates, and in Eastern Europe in volume commodity builds, should stabilize the continental supply chain and allow the German PCB market to focus on margin-rich technologies.

Competitive Landscape

The Germany printed circuit board (PCB) market is moderately fragmented; the top five fabricators account for about 43% of domestic revenue, leaving ample room for above 30 SMEs specializing in prototypes and niche technologies. AT&S posted EUR 1.59 billion (USD 1.80 billion) for the first nine months of fiscal 2024-25, yet faces multilayered price pressure, leading to a EUR 100 million (USD 113 million) cost-reduction initiative and the divestiture of its Korea plant. These funds are redirected to IC substrate expansion in Kulim and Leoben, reinforcing a long-term strategic pivot toward data-center and smartphone packaging. Schweizer Electronic recorded EUR 139.2 million (USD 157.3 million) in the same period and shifted to a fab-light model that outsources high-volume orders while retaining its embedded-component edge for premium automotive contracts.

Würth Elektronik leverages its component distribution arm to bundle PCBs, connectors, and passives, creating one-stop procurement that appeals to industrial automation customers. Rapid-turn specialists such as KSG Leiterplatten and FELA guarantee 48-hour lead times for prototypes, helping win programs that compress design cycles to less than 4 weeks. Technology investments across the tier include wide adoption of plasma desmear systems that remove chemical etchants restricted under REACH, and AOI cameras that resolve defects below 10 µm. Plants holding IPC-6012 Class 3 and IATF 16949 certifications meet the baseline entry criteria for both automotive and medical contracts, with additional ISO 13485 certification required for implantables. A white-space opportunity lies in flip-chip ball-grid-array substrates, an area EU funding now supports; German laminators are partnering with machine suppliers to close capability gaps in 2.5D interposers and through-silicon via formation.

Despite elevated competitive intensity, German vendors defend their share by bundling engineering services, material science support, and end-of-life repair agreements that offshore rivals seldom match. Price competition persists in the commodity multilayer, but margin protection arises from packaging boards where gross returns exceed 30%. The blended corporate strategy converges on high-mix, low-volume production aligned with Germany’s innovation-led manufacturing economy.

Germany Printed Circuit Board Industry Leaders

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft

Schweizer Electronic AG

Würth Elektronik GmbH & Co. KG

KSG Leiterplatten GmbH

FELA GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: AT&S finalized the sale of its Ansan, Korea plant, redirecting proceeds toward IC substrate capacity in Leoben, Austria.

- November 2025: Würth Elektronik inaugurated a laser direct imaging line in Niedernhall, adding 12 µm registration capability for HDI builds.

- October 2025: The ifo Institute reported that 10.4% of German electronics firms faced semiconductor shortages, prolonging PCB lead times for automotive and telecom customers.

- May 2025: AT&S confirmed EUR 1.59 billion (USD 1.80 billion) revenue for the first three quarters of fiscal 2024-25 and activated a EUR 100 million (USD 113 million) cost-reduction program.

Germany Printed Circuit Board Market Report Scope

The Germany Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer (non-HDI), Rigid 1-2 Sided, High-Density Interconnect (HDI), Flexible Circuits (FPC), IC Substrates (Package Substrates), Rigid-Flex, Other PCB Types), Substrate Material (Glass Epoxy (FR-4), High-Speed Low-Loss, Polyimide (PI), Packaging Resins (BT / ABF), Other Substrate Materials), and End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare / Medical, Aerospace and Defense, Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the projected value of the Germany PCB market in 2031?

It is expected to reach USD 1.58 billion by 2031, rising at a 3.66% CAGR from 2026.

Which PCB type is forecast to grow the fastest in Germany?

Flexible circuits are projected to expand at a 5.07% CAGR through 2031, driven by automotive sensors and medical wearables.

Which end-user vertical adds the most incremental demand?

Automotive and EV applications deliver the highest growth, with a 5.23% CAGR as electrification and ADAS adoption accelerate.

How large is Germany’s share of European PCB output?

Germany accounts for 31.8% of European PCB production by value, underscoring its role as the region’s fabrication hub.

What impact do copper price swings have on German PCB makers?

A 20%-25% quarterly copper price jump can compress gross margins from 25% to 15% for small fabricators without hedging instruments.

Which regulatory frameworks most affect German PCB production?

REACH and RoHS impose strict chemical restrictions, adding 3%-5% to production costs for compliance and testing.

Page last updated on: