Germany Plastic Waste Management Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

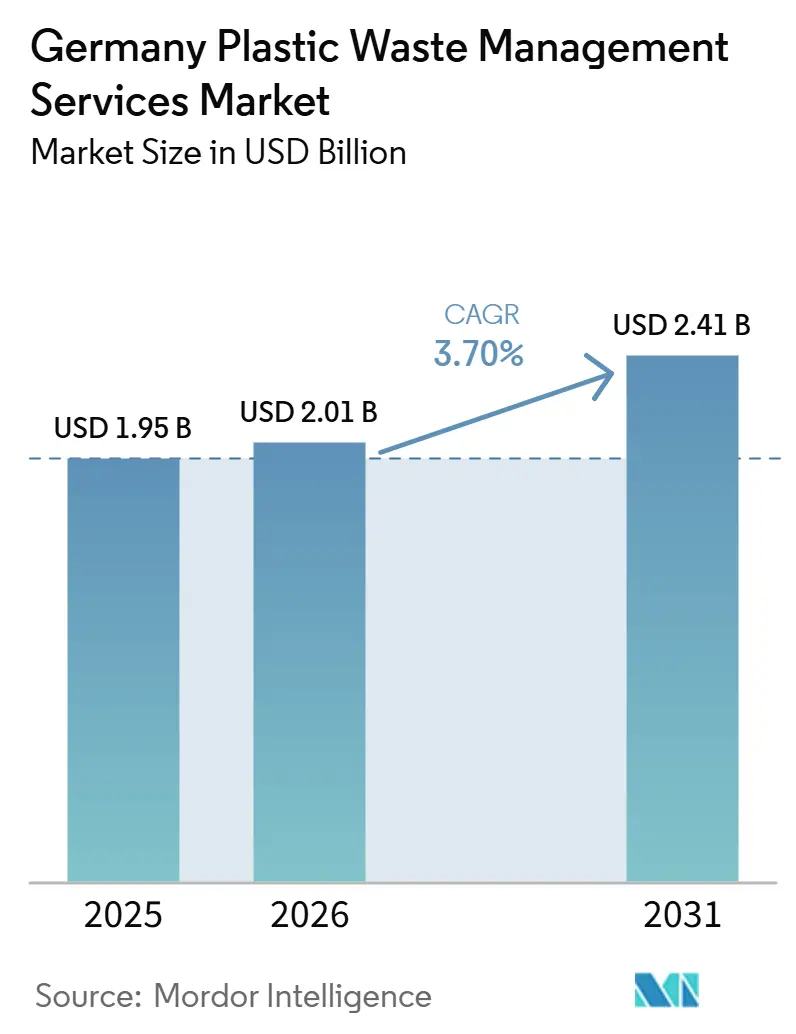

| Base Year Market Size (2025) | USD 1.95 Billion |

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 3.70% CAGR |

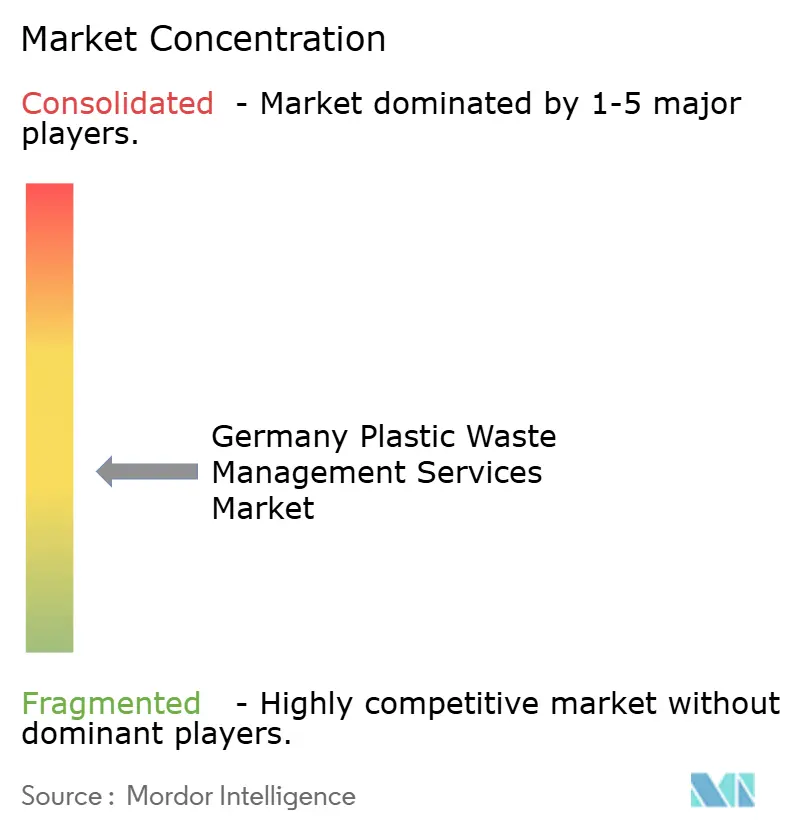

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Plastic Waste Management Services Market Analysis by Mordor Intelligence

The Germany Plastic Waste Management Services Market size is projected to expand from USD 1.95 billion in 2025 and USD 2.01 billion in 2026 to USD 2.41 billion by 2031, registering a CAGR of 3.70% between 2026 to 2031.

Germany’s expansion path remains steady because separate collection rules, recycled-content requirements, and a mature dual-system setup continue to create recurring demand for regulated waste services. At the same time, the national system recovered 5.5 million tons of packaging waste in 2025. Mechanical recycling rates for plastic packaging rose from 42% in 2018 to 70.8% in 2025, indicating that the Germany plastic waste management services market is now moving more towards service quality, deeper domestic processing, and throughput improvement than towards basic collection buildout. The policy backdrop is also tightening, as the PPWR entered into force in 2025 and will apply fully from August 12, 2026, while recycled-plastic obligations proposed under the End-of-Life Vehicles Regulation are extending demand into automotive supply chains. At the same time, German demand for recycled plastics is set to outpace domestic supply by 2030, which raises the value of collection, sorting, and upgrading contracts across the Germany plastic waste management services market. Competition remains moderately concentrated among a small top tier. Still, the strongest opportunities are shifting toward higher-value treatment, traceability, and near-virgin recycle production rather than basic hauling and commodity sorting.

Key Report Takeaways

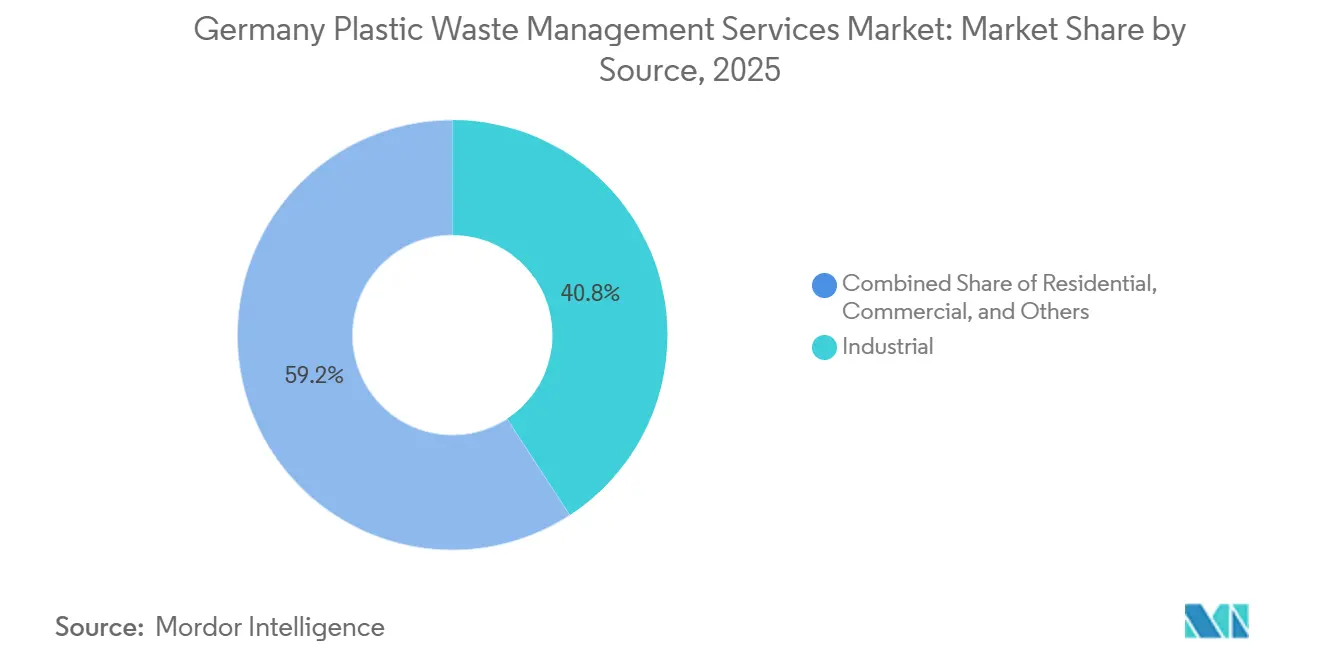

- By source, industrial waste accounted for 40.8% of the Germany plastic waste management services market share in 2025, while commercial streams are projected to be the fastest-growing at 4.1% CAGR through 2031.

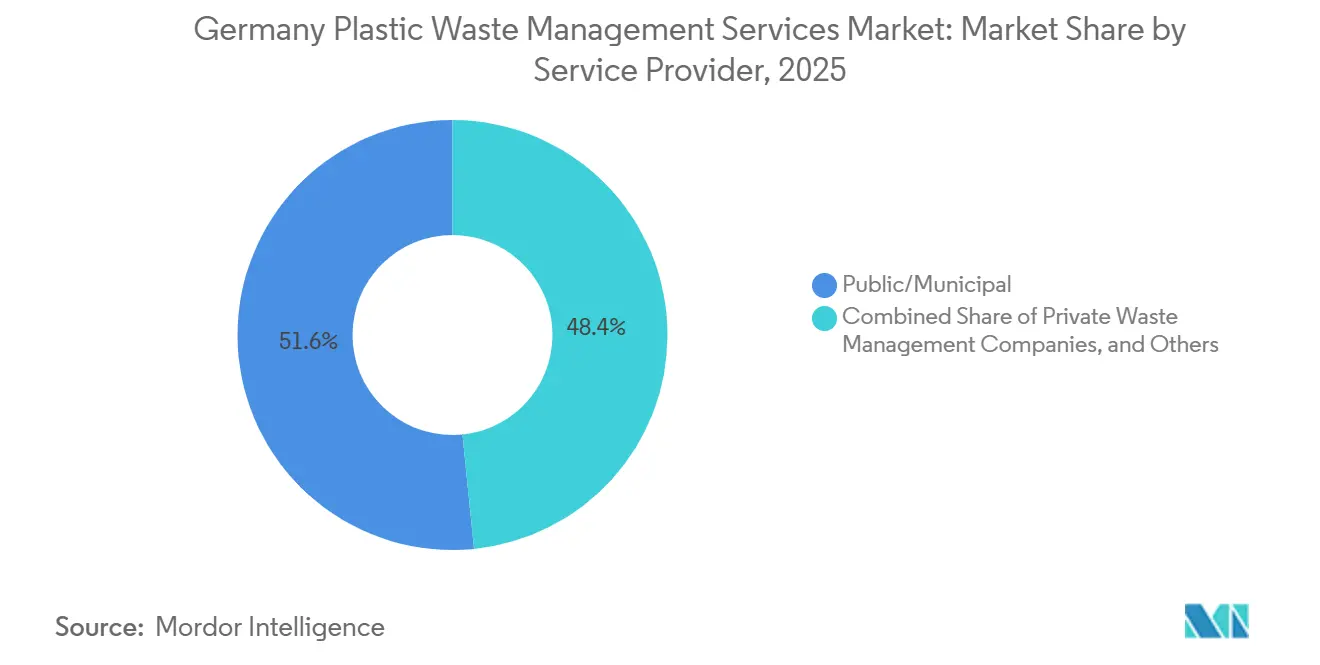

- By service provider, the public/municipal segment accounted for 51.60% of the Germany plastic waste management services market size in 2025, and the private waste management companies segment is expected to register 5.0% CAGR through 2031.

- By service type, collection, transportation, sorting, and segregation accounted for 41.7% in 2025, while disposal/treatment registered 5.4% CAGR over 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Plastic Waste Management Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Germany's Dual-System Collection Network And High Household Participation | +0.9% | National, with operational intensity in North Rhine-Westphalia, Bavaria, and Baden-Württemberg | Short term (≤ 2 years) |

| VerpackDG Recycling Quotas And Packaging Compliance Escalation | +0.7% | National, with compliance pressure centered on packaging producers and retail chains | Medium term (2-4 years) |

| Extended Producer Responsibility-Led Demand For Certified Waste Management Services | +0.6% | National, with spillover to EU-linked processing networks | Medium term (2-4 years) |

| Expansion Of Advanced Sorting, Washing, And Polymer-Upgrading Infrastructure | +0.5% | National, with investment clusters in Ruhr, Saxony-Anhalt, and logistics hubs | Long term (≥ 4 years) |

| Digital Waste Traceability, Route Optimization, And Reporting Automation | +0.3% | National, with early gains in major urban waste corridors | Medium term (2-4 years) |

| Demand Pull From Automotive And Packaging Recycled-Content Procurement | +0.4% | National, with strong pull from automotive regions such as Bavaria, Baden-Württemberg, and Lower Saxony | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Germany's Dual-System Collection Network and High Household Participation

Germany’s Yellow Bag and Yellow Bin system remains the foundation for recurring service demand in the Germany plastic waste management services market. In 2025, 43 dedicated sorting facilities processed 2.6 million tons of lightweight packaging, and total lightweight packaging recovery exceeded 90% of the volumes participating in dual systems. That level of household participation keeps collection routes efficient and gives operators a dependable flow of post-consumer plastics. The next growth step is less about adding household coverage and more about bringing harder commercial and industrial streams into formal contracts, especially because only 3.2 million of Germany’s 5.6 million tons of annual plastic waste currently enter recycling channels. Separate collection duties under German packaging rules also keep collection services non-discretionary, which supports stable contract renewal patterns across the market.

VerpackDG Recycling Quotas and Packaging Compliance Escalation

Germany’s Packaging Act has already raised plastic packaging recycling obligations, with a 63% mechanical recycling requirement in place today, a 65% threshold due by the end of 2025, and a 70% requirement due by the end of 2030. Dual systems cleared the 50% lightweight packaging recycling threshold in 2024, reaching 52.55%, confirming that compliance is possible but increasingly dependent on processing quality and downstream capacity.[1]Federal Ministry of Justice, “Verpackungsgesetz (VerpackG),” Gesetze im Internet, gesetze-im-internet.deThis is changing the commercial mix in the Germany plastic waste management services market because logistics-heavy contracts alone are no longer enough to secure future quota performance. Operators are under pressure to add more domestic polymer-upgrading capacity so that sorted output can move into higher-value recycling channels rather than lower-value recovery routes. The PPWR will add another layer from August 2026, as recyclability design standards and recycled-content rules will increase the need for auditable compliance support.

Extended Producer Responsibility-Led Demand for Certified Waste Management Services

Extended producer responsibility is widening demand beyond standard packaging take-back in the Germany plastic waste management services market. Effective January 1, 2025, the Single-Use Plastics Fund Act requires producers of covered single-use plastic products to register, report volumes, and pay an annual levy to support municipal cleanup and waste management costs. That creates a new services layer around reporting, certified handling, and fund-linked waste administration for municipalities and producer responsibility organizations. The effect extends further into procurement, as post-consumer recycled plastic content in German manufacturing conversions rose from 6.2% in 2018 to 14.4% in 2024. As more producers commit to traceable recycled content, certified waste management, and auditable output quality, simple tonnage collection alone becomes less valuable.

Expansion of Advanced Sorting, Washing, and Polymer-Upgrading Infrastructure

Investment is moving toward equipment and process upgrades that can deliver cleaner fractions and higher-value recyclates across the Germany plastic waste management services market. STADLER’s rebuilt Bremen plant restored 120,000 tons per year of lightweight packaging throughput. It was designed to deliver 12 high-purity mono-material fractions, demonstrating a shift toward better output quality rather than just more volume. Interzero and OMV are also building a sorting facility for chemical-recycling feedstock with a planned capacity of up to 260,000 tons per year, signaling stronger commercial interest in upgrading mixed plastics. Fraunhofer IOSB has shown how inline sensor monitoring can improve real-time quality control in sorting plants, thereby supporting more consistent recyclate output. The operators that secure food-contact, automotive-grade, or similarly certified output will be in a stronger position as recycled-content rules tighten further.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Processing Costs For Mixed And Contaminated Plastic Waste | -0.5% | National, with the strongest pressure in areas facing heavier residual contamination in household collections | Short term (≤ 2 years) |

| Rising Energy And Operating Costs | -0.6% | National, and most severe in energy-intensive mechanical and chemical recycling operations | Short term (≤ 2 years) |

| Labor Shortages In Waste Collection And Recycling Operations | -0.4% | National, with sharper shortages in rural districts and aging labor markets | Medium term (2-4 years) |

| Volatility In Virgin Polymer Prices Affecting PCR Competitiveness | -0.4% | National, with pressure strongest on mid-scale recyclers serving packaging and consumer goods | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Processing Costs for Mixed and Contaminated Plastic Waste

Mixed and contaminated plastic waste continues to limit margins in the Germany plastic waste management services market. ZSVR data for 2025 showed that only 52.55% of total lightweight packaging collection volumes met the recycling threshold, which means a large share of collected material still moved into costlier alternative treatment paths. Commercial and industrial plastics can add another layer of difficulty because coated films, laminates, and multi-material formats often need more pre-treatment before viable polymer separation. This increases labor, sorting, and cleaning intensity even when collection volumes look attractive on paper. Until eco-design standards under the PPWR translate into simpler packaging formats and cleaner incoming streams, many operators will continue to face pressure on commodity sorting economics.

Rising Energy and Operating Costs

Energy remains one of the clearest cost constraints for the Germany plastic waste management services market. BVSE has stated that German plastic recyclers face a structural energy-cost disadvantage compared to competitors elsewhere in Europe and has called for broader industrial support for electricity. BDE and BKV also argued in 2025 that recycling operations meet the energy-intensity thresholds relevant to electricity price relief under the EU clean industry framework. This matters because washing, drying, and compounding post-consumer plastics remain power-intensive steps that cannot be scaled efficiently when utility costs stay high. If recyclate prices remain weak while energy inputs stay elevated, mid-scale processors will find it harder to reinvest in advanced capacity, which can slow domestic growth.[2]BVSE, “Industriestrompreis greift zu kurz: Kunststoffrecycling darf nicht weiter benachteiligt werden,” BVSE, bvse.de

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Industrial Volumes Lead as Commercial Streams Attract New Investment

Industrial waste remained the largest source segment in 2025, accounting for 40.80% of the market share, while commercial waste is forecast to expand at 4.1% CAGR through 2031. Industrial generators produce recurring plastic waste from manufacturing, chemical processing, packaging conversion, and automotive assembly, providing processors with a steadier contract base than fragmented, smaller generators. Those waste streams are often more homogeneous, including off-cuts, purge material, and mono-material wraps, so they fit long-term feedstock agreements well. The Germany plastic waste management services industry benefits from these cleaner industrial streams because more predictable input quality supports better yields and a more stable downstream offtake.

Residential waste remains the most visible collection stream through Yellow Bags and Yellow Bins. Still, its revenue growth is more limited because collection density is already high and the network is mature. That keeps much of the near-term expansion in the Germany plastic waste management services market tied to commercial and mixed business waste rather than new household route buildout. A BKV-commissioned study identified 1 million tons of untapped plastic waste in Germany’s mixed commercial and construction streams, which explains why this source group is drawing fresh collection interest. The others segment, including institutional, agricultural, and construction plastics, can also deliver niche margins when operators build specialized take-back logistics, while Germany’s post-consumer recycled plastic conversion reached 1,727kt in 2024, equal to 14.4% of total conversion, which supports stronger demand for reliable recycled feedstock.

By Service Provider: Municipal Operators Anchor Infrastructure as Private Sector Expands Value-Added Capacity

Public and municipal operators remained the largest service provider segment in 2025, accounting for 51.60% of the market share as household waste responsibility still primarily rests with local public authorities and their contracted systems. Their position is reinforced by control over curbside collection infrastructure, long contract cycles, and stable access to household streams. That gives them a durable base in the Germany plastic waste management services market, even as private capital moves faster into new treatment niches. At the same time, public procurement rules and budget cycles can slow investment in advanced polymer-upgrading capacity, limiting how quickly some municipal operators can move into higher-value processing.

Private waste management companies are projected to grow at a 5% CAGR through 2031, the fastest pace within this segmentation. Their advantage is speed, because they can align plant investment more directly with packaging and automotive demand for certified recycled content and traceable material flows. PreZero’s 2026 partnership with BMW Group reflects that shift by linking waste services to circular material solutions for future automotive component supply. Producer responsibility organizations in the other segments are also gaining weight as EPR frameworks expand, and the Germany plastic waste management services industry is placing greater emphasis on reporting, audit trails, and fee administration alongside physical waste handling.[3]Federal Ministry of Justice, “Einwegkunststofffondsgesetz (EWKFondsG),” Gesetze im Internet, gesetze-im-internet.de

By Service Type: Segregation Infrastructure Leads as Treatment Attractiveness Grows

Collection, transportation, sorting, and segregation remained the largest service type in 2025. Its leading position comes from the labor and asset intensity of nationwide route management, collection fleets, transfer handling, and 43 dedicated lightweight packaging sorting plants. German packaging law keeps this part of the Germany plastic waste management services market structurally necessary, as packaging placed on the market must participate in a certified take-back system. STADLER’s rebuilt Bremen plant, with 120,000 tons per year of throughput and 12 high-purity mono-material fractions, shows that fresh investment in this segment is focused on resilience and cleaner output.

Disposal and treatment are forecast to expand at a 5.4% CAGR through 2031, making it the fastest-growing service category in the Germany plastic waste management services market outlook. Within this segment, recycling and resource recovery are drawing more strategic investment than landfill or standard incineration because they offer better value capture from mixed or difficult plastics. Interzero and OMV are developing a chemical recycling feedstock sorting facility with a capacity of up to 260,000 tons per year, which shows how high-value treatment contracts are taking on a larger role in the Germany plastic waste management services market. Landfill has little room left as a meaningful growth path, as Germany’s plastic waste landfill rate was only 0.6% in 2024. Advisory, audit, and training services are also expanding, as PPWR compliance will require more design-for-recyclability checks and documentation.

Geography Analysis

Germany recovered 5.5 million tonnes of packaging waste in 2024, achieving an overall recovery rate of 90%, confirming the scale and maturity of the national platform supporting the Germany plastic waste management services market. That maturity means growth is tied less to basic geographic white space and more to how regional infrastructure adapts to tighter rules and better output requirements. North Rhine-Westphalia remains one of the main operational centers because the Ruhr industrial belt combines dense commercial waste volumes with major operator footprints. Bavaria is also central because its automotive and manufacturing base generates steady industrial plastic streams and future demand for certified recyclates. Saxony-Anhalt is gaining importance as a location for advanced recycling projects and feedstock processing capacity linked to higher-value treatment.

In 2025, 83.2% of sorted plastic packaging was recovered domestically, and 16.5% was processed in other EU member states, keeping most of the Germany plastic waste management services market share within national borders while still relying on cross-border balancing capacity. Eastern German states attract recycling projects because lower land costs and available brownfield sites make them suitable for investment in processing. Those same states often have weaker local commercial waste generation because economic density is lower than in western industrial regions. From May 2026, the European Digital Waste System requires electronic declarations and tracking for cross-border waste flows, and that is raising the value of digital compliance support for operators that move sorted fractions across borders. The effect is especially relevant for service providers that need to document material movements between domestic sorting assets and external EU recovery partners.

The Bremen lightweight packaging plant rebuild restored 120,000 tons per year of regional sorting capacity. It showed that location strategy is now centered on improving output quality and resilience rather than simply adding collection coverage. TOMRA is expanding a German feedstock plant designed to process 80,000 tons of mixed plastics annually from unseparated waste, which adds another layer of regional sorting capability. These developments show that geography in the Germany plastic waste management services market is less about untapped national demand and more about where higher-purity processing can be built most efficiently. Dense consumer participation, strong industrial clusters, and EU-linked compliance obligations keep Germany as the clearest testing ground for advanced plastic waste service models in Europe.

Competitive Landscape

The Germany plastic waste management services market remains moderately concentrated at the top, with Remondis, PreZero, ALBA Group, and Interzero anchoring major positions across dual systems, sorting infrastructure, and downstream recyclate sales. Competitive strength is no longer defined solely by collection scale, as certified output quality and audit-ready reporting are becoming equally important. Remondis and Jokey Group highlighted this shift when they launched a PP food-packaging closed-loop pilot in the Ruhr region and filed a joint Novel Technology application with EU and national authorities. That move aimed to position the companies early for future food-contact PP recyclate demand under tighter packaging rules. The Germany plastic waste management services market is, therefore, rewarding firms that can combine plant operations, certification, and regulatory compliance into a single offering.

PreZero is pushing further into value-added circular contracts through its 2026 partnership with the BMW Group, which links waste management to data-driven recycled-material solutions for automotive components. Interzero and OMV are also moving downstream through a sorting facility for chemical recycling feedstock with a planned capacity of up to 260,000 tons per year. REMONDIS subsidiary RE Plano implemented STEINERT AI-based sorting at Bochum in 2026 to improve the quality of closed-loop PE and PP recyclate, demonstrating how digital sorting performance is becoming part of competitive positioning. These moves show that competition is shifting from hauling reach alone toward polymer purity, traceability, and end-use suitability. The firms that secure cleaner feedstock, stronger reporting systems, and better downstream offtake relationships will have a clearer edge as compliance pressure rises.

The clearest white space remains in commercial and industrial streams, where formal collection penetration still lags behind household systems. Chemical recycling support services and compliance advisory work also offer room for newer specialists, especially where mechanical recycling cannot handle multilayer or mixed plastic inputs. Technology providers such as TOMRA are becoming indirect competitors because advanced sorting assets can shape who controls feedstock quality and commercial relationships. Even with a visible top tier, municipal operators, producer responsibility organizations, and regional recyclers keep the Germany plastic waste management services market from reaching a very high concentration.

Germany Plastic Waste Management Services Industry Leaders

Remondis SE & Co. KG

ALBA Group

Veolia Environnement S.A.

PreZero International

Interzero

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: PreZero formalized its circular-material partnership with the BMW Group to develop scalable, data-driven recycled-material solutions for automotive components, aligned with future ELVR recycled-content targets.

- February 2026: STADLER completed reconstruction of Sortierkontor Nord's (SKN) Bremen lightweight packaging plant, restoring 120,000 tonnes per year throughput and upgrading fire protection and automated battery extraction capabilities.

- February 2026: EEW Energy from Waste secured a long-term district heating supply contract with Stadtwerke Pirmasens from its Saar waste-to-energy facility, formalizing a multi-year arrangement previously renewed annually.

- June 2026: Remondis and Jokey Group launched a PP food-packaging closed-loop pilot in the Ruhr region. They submitted a joint "Novel Technology" application to the EU Commission and national authorities for recognition of food-contact PP recyclate under EFSA guidelines.

Germany Plastic Waste Management Services Market Report Scope

The Germany Plastic Waste Management Services Market Report is Segmented by Source (Residential, Commercial, Industrial, and Others), by Service Provider (Public/Municipal, Private Waste Management Companies, and Others), and by Service Type (Collection, Transportation, Sorting & Segregation, Disposal / Treatment, and Others). The Market Forecasts are Provided in Terms of Value (USD).

| Residential |

| Commercial (retail, office, etc.) |

| Industrial |

| Others (institutional, agricultural, etc) |

| Public/Municipal |

| Private Waste Management Companies |

| Others - Producer Responsibility Organizations (PROs), etc. |

| Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill |

| Recycling & Resource Recovery | |

| Incineration & Waste-to-Energy | |

| Others (Chemical Treatment, etc.) | |

| Others (Consulting, Audit & Training, etc.) |

| By Source | Residential | |

| Commercial (retail, office, etc.) | ||

| Industrial | ||

| Others (institutional, agricultural, etc) | ||

| By Service Provider | Public/Municipal | |

| Private Waste Management Companies | ||

| Others - Producer Responsibility Organizations (PROs), etc. | ||

| By Service Type | Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill | |

| Recycling & Resource Recovery | ||

| Incineration & Waste-to-Energy | ||

| Others (Chemical Treatment, etc.) | ||

| Others (Consulting, Audit & Training, etc.) | ||

Key Questions Answered in the Report

What is the expected value of Germany's plastic waste management services by 2031?

The German plastic waste management services market is projected to reach USD 2.41 billion by 2031, up from USD 2.01 billion in 2026, at a 3.7% CAGR over 2026-2031.

What is driving demand for plastic waste services in Germany?

Demand is being supported by separate collection mandates, tighter packaging recycling quotas, PPWR compliance, and rising recycled-content needs across packaging and automotive supply chains.

Which source segment is growing the fastest?

Commercial waste is forecast to grow at 4.1% CAGR through 2031 as smaller generators move into formal compliance systems and untapped mixed commercial streams are targeted for collection.

Why do municipal operators still lead service provision?

Municipal operators remain central because they control much of the household collection base and benefit from long contract cycles tied to local public responsibility for waste services.

Which service category shows the fastest growth outlook?

Disposal and treatment are projected to grow at 5.4% CAGR through 2031 as higher-value recycling and resource recovery attract more investment than landfill or standard incineration.

How is competition changing among major operators?

Competition is shifting toward certified recyclate quality, digital traceability, and downstream material partnerships, as shown by moves from Remondis, Interzero, and PreZero in food-grade, chemical recycling, and automotive-linked circular contracts.

Page last updated on: