Germany Indoor Farming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

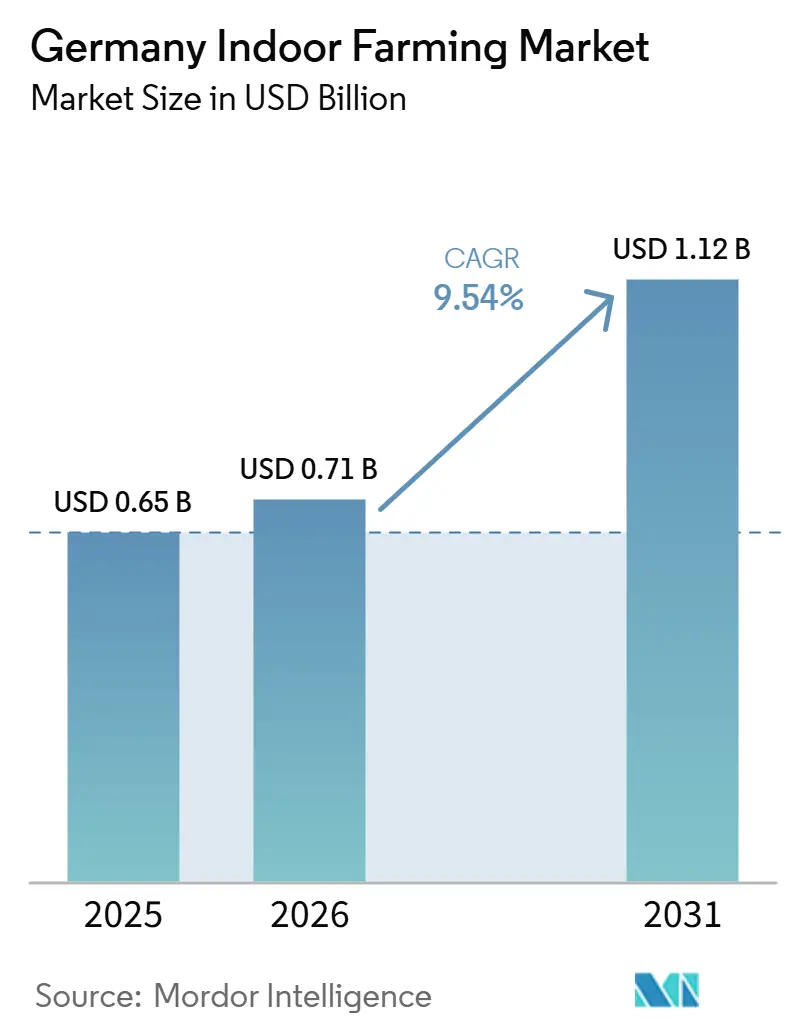

| Base Year Market Size (2025) | USD 0.65 Billion |

| Market Size (2026) | USD 0.71 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 9.54% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Indoor Farming Market Analysis by Mordor Intelligence

The Germany indoor farming market is forecasted to grow from USD 650 million in 2025 to USD 711.8 million in 2026, reaching USD 1,117.7 million by 2031, at a CAGR of 9.54% over 2026-2031. Growth is driven by growers, retailers, and infrastructure investors placing greater emphasis on local supply, stable output, and tighter crop quality control amid supply chain uncertainty. Dense urban demand in Berlin, Hamburg, Munich, and Cologne is supporting a broader market for pesticide-free produce, while weather-related pressure on field agriculture is making protected cultivation more relevant for high-value perishables. Financing conditions remain selective following Infarm's insolvency, and energy costs continue to be a major operating concern, directing capital toward operators with established retail contracts, stronger technology, or broader revenue support. Improved LED efficiency, stronger automation packages, and retailer-backed projects are improving project economics and reducing execution risk for new facilities. The availability of vacant retail and industrial buildings in urban corridors, combined with recurring drought-related crop losses in conventional agriculture, is expanding the long-term opportunity for the Germany indoor farming market.

Key Report Takeaways

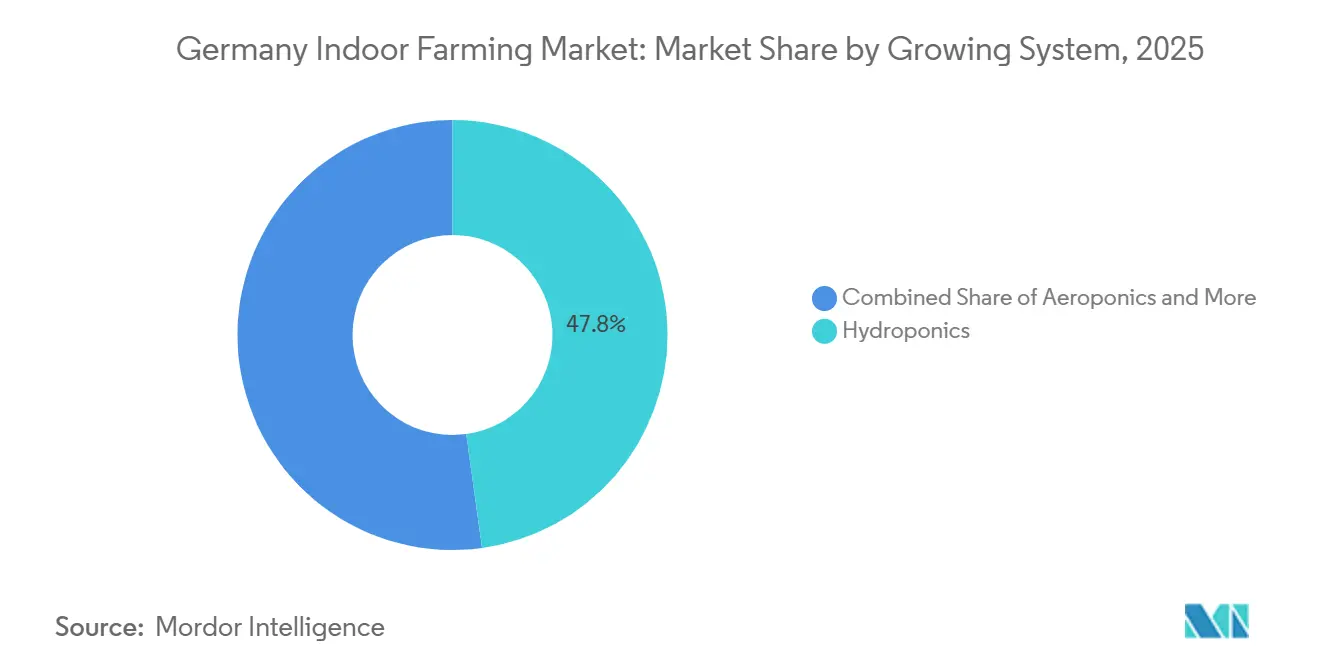

- By growing system, hydroponics held 47.8% share in 2025, while aeroponics is forecast to expand at a 15.8% CAGR between 2026 and 2031.

- By facility type, glass or poly greenhouses held 52.1% of Germany indoor farming market share in 2025, while indoor vertical farms are projected to grow at a 17.4% CAGR between 2026 and 2031.

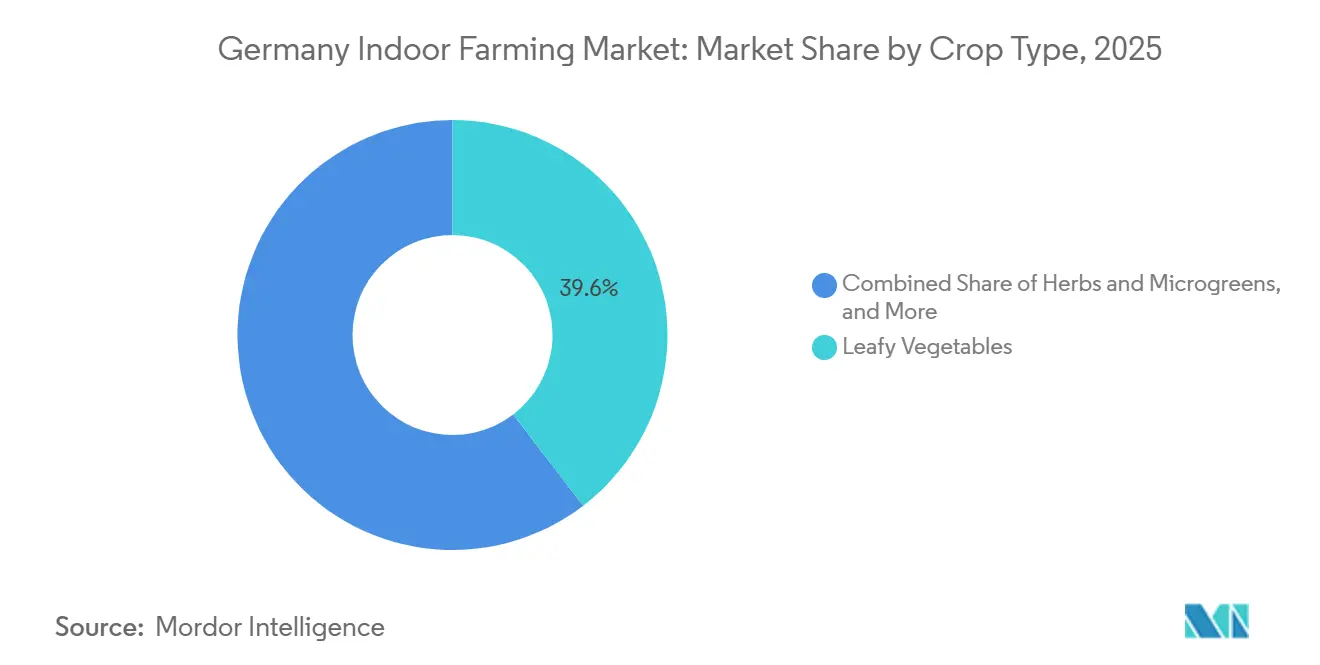

- By crop type, leafy vegetables accounted for 39.6% share of the Germany indoor farming market size in 2025, while herbs and microgreens are forecast to grow at a 14.2% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Indoor Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban demand for fresh, pesticide-free produce | +2.5% | Germany-wide, concentrated in Berlin, Hamburg, Munich, and Cologne retail corridors | Short term (≤ 2 years) |

| LED efficiency and climate control cost declines | +1.8% | Germany-wide, strongest in greenhouse clusters in North Rhine-Westphalia and Bavaria | Medium term (2-4 years) |

| Shrinking arable land and weather volatility | +1.4% | Northern and eastern Germany, where drought exposure and irrigation deficits are highest | Long term (≥ 4 years) |

| Year-round production strengthens grocery supply reliability | +1.2% | Germany-wide, especially urban grocery chains and food service buyers | Medium term (2-4 years) |

| Repurposing vacant industrial real estate | +0.7% | Germany-wide, accelerated in post-industrial Rhine-Ruhr and eastern German cities | Medium term (2-4 years) |

| Carbon and energy efficiency monetization | +0.6% | Germany-wide, ESG-driven regions near Energiewende transition hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban Demand for Fresh, Pesticide-Free Produce

Germany's organic food market is growing, indicating that demand for traceable and clean-label food extends beyond a small premium niche. Discount retailers now account for a substantial share of organic purchases, reflecting broad everyday adoption rather than occasional premium buying. This shift is relevant to indoor farming because leafy greens, herbs, and strawberries grown indoors can be sold through large supermarket channels where freshness, shelf life, and pesticide-free positioning carry commercial weight. Private-label contracts through discounters also give growers access to stable volume that was previously difficult to secure when indoor produce was sold primarily through specialty retail. As a result, the Germany indoor farming market is supported by recurring food demand tied to mainstream retail rather than a narrow high-end consumer segment.

LED Efficiency and Climate Control Cost Declines

Commercial horticultural LED fixtures sold in 2025 and 2026 routinely exceeded 3.5 µmol/J efficacy, which was linked to a 30%-40% reduction in electricity use for the same light intensity. Signify reinforced this trend in June 2025 with the launch of the Philips GrowWise smart spectrum algorithm, which the company stated can reduce energy use or increase crop growth by up to 6% through real-time light adjustment. In 2026, Ridder and Signify formalized integration under the Horti Lighting Protocol, giving growers a more direct route to connected control without extensive custom integration work. Additionally, NLight's centralized DC architecture claims a 10%-20% capital expenditure reduction for greenhouse lighting projects, which is significant in a market where power costs can determine project viability. While these developments do not eliminate energy risk, they narrow one of the largest cost gaps that has constrained smaller facilities. As a result, the Germany indoor farming market is seeing a clearer path toward commercially viable projects at more modest scales and in more urban settings.

Shrinking Arable Land and Weather Volatility

According to Destatis, Germany's grain cultivation area fell to its lowest point since 2010 during the 2024 harvest year due to weather-related difficulties during winter wheat sowing. In 2025, northwestern Europe, including Germany, experienced its driest spring in a century, with farmers in Schleswig-Holstein and Saxony-Anhalt reporting rainfall at nearly half of normal levels and potential yield losses of 20%-30%. A peer-reviewed study in Natural Hazards and Earth System Sciences estimated average annual direct biophysical crop revenue losses of EUR 781 million (USD 836 million) during drought years in Germany between 2016 and 2022, and placed the 2018 drought loss at EUR 1.7 billion (USD 1.9 billion). Fewer than 10% of Germany's agricultural land parcels are equipped with irrigation, leaving field output highly exposed to rainfall volatility. Controlled-environment agriculture will not replace large-scale field production for commodity crops, but it can provide a steady supply of high-value perishables when weather stress disrupts open-field output. For this reason, the Germany indoor farming market is becoming more relevant to buyers seeking year-round crop availability and reduced weather exposure in parts of their fresh produce sourcing mix.

Year-Round Production Strengthens Grocery Supply Reliability

The opening of REWE Green Farming Berlin in May 2026 demonstrated how a mainstream retailer is integrating indoor agriculture directly into store infrastructure. The rooftop greenhouse covers 2,760 square meters, is operated by ECF Farmsystems, and produces up to 900,000 salad mixes per year using a hydroponic system powered by 100% renewable electricity. REWE's Endless Summer project in Upper Bavaria, developed with Steiner in Kirchweidach, is a 4-hectare hydroponic lettuce system heated by geothermal energy, associated with annual CO2 savings of 3,000 tons. These projects indicate that supermarkets are moving beyond the role of buyer and are beginning to share infrastructure risk with growers. This shift can make revenue more predictable and help projects reach scale with stronger off-take visibility. As these models expand, the Germany indoor farming market is likely to favor operators that can consistently meet retailer standards throughout the year, rather than suppliers focused on short-run specialty output.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure and energy intensity | -2.4% | Germany-wide, more acute in eastern Germany where energy infrastructure lags and grid tariffs are less predictable | Short term (≤ 2 years) |

| Shortage of skilled horticulture and automation talent | -1.2% | Germany-wide, concentrated in expansion hubs such as Berlin and Rhine-Ruhr | Medium term (2-4 years) |

| Investment pullback after operator failures | -1.0% | Germany-wide, especially affecting new market entrants and growth-stage operators | Medium term (2-4 years) |

| Urban grid capacity constraints | -0.8% | Urban centers including Berlin, Hamburg, and Munich | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Energy Intensity

Capital expenditure for a medium-scale vertical farm is regularly increasing and energy costs account for 40%-70% of operating expenditure in fully enclosed systems, which explains why energy price volatility has had a strong effect on investor confidence. This burden is especially difficult for new operators that need to scale output before they can negotiate better procurement terms or spread overhead across larger volumes. Partial solutions are emerging, including Schneebergerhof's March 2026 greenhouse opening with direct wind and solar power supply. Dürr AG's EcoY system, launched in June 2025, uses grow-tube technology that can reduce water use by up to 95% and applies supplemental LED lighting only where natural daylight is insufficient. Even so, high upfront capital requirements and power intensity will continue to slow the Germany indoor farming market until lower-cost engineering and stronger energy integration become more widespread across commercial projects.

Shortage of Skilled Horticulture and Automation Talent

Controlled-environment farming requires growers who understand nutrient balance, crop timing, pest control, climate systems, sensors, and automation within the same operating environment. Germany's training system has not yet established standardized pathways for these combined roles, which means operators often recruit from adjacent disciplines and face higher staffing costs. Automation suppliers are addressing this challenge through software and remote-control tools, rather than labor replacement alone. Priva highlighted this direction in June 2026 with its Priva One platform, which combines climate control, irrigation, crop performance, and daily operations in a single crop-centric system. Ridder made a similar move with Hortimax Plus in June 2025, offering a lower-cost climate computer that provides growers an easier entry point into automation with room for later upgrades. Until training supply improves and more operators gain hands-on experience, the Germany indoor farming market will continue to face limits on expansion speed and operating consistency, even where equipment availability is improving.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Growing System: Hydroponics Leads, but Aeroponics Redefines the Efficiency Frontier

Hydroponics held 47.8% of the Germany indoor farming market in 2025, making it the clear operating base for commercial production. Its lead reflects a favorable cost-to-yield profile, a broader equipment supply base, and production methods that operators understand well enough to scale with lower execution risk. Aquaponics and soil-based systems remain present but are more limited in scope, as biological complexity is higher in aquaponics and yield intensity is lower in soil-based formats. Hybrid systems are drawing interest where crop flexibility matters, yet their market position remains modest as most operators prefer proven system designs during the current financing cycle.

Aeroponics is forecast to be the fastest-growing system between 2026 and 2031, at a CAGR of 15.8%, reflecting a shift in performance expectations. This outlook is linked to maturing precision misting technology and growing interest in water efficiency, particularly for high-value herbs, microgreens, and specialty strawberries. In June 2025, Körber Technologies and Veganz Group AG introduced the OrbiFarm platform, reporting trial yields up to 36 times higher than conventional cultivation in Fraunhofer testing, which has drawn strategic attention to the system even before broad commercial rollout. Closed-loop hydroponic systems use only 5% of the water required by conventional field cultivation[1]Source: Hanna Bonekämper, "Adaptive Reuse for Sustainable Urban Development: Vertical Farming in Former Department Stores. German Case Study," Frontiers in Built Environment, frontiersin.org., and aeroponics reduces water input further. In the Germany indoor farming market, this efficiency gap is increasingly relevant as buyers pay closer attention to resource use and supply stability. Hydroponics is anticipated to remain the dominant system in the near term, while aeroponics is likely to capture a larger share of new high-efficiency projects as commercial validation improves.

By Facility Type: Greenhouses Anchor the Market, While Vertical Farms Drive the Next Growth Cycle

Glass or poly greenhouses accounted for 52.1% of the Germany indoor farming market in 2025, placing them ahead of other facility types by revenue. They benefit from partial natural light use, lower construction costs per square meter compared to fully enclosed farms, and a workforce familiar with greenhouse operations. This makes greenhouses a practical choice for growers seeking cost control without sacrificing year-round production, and explains why greenhouse formats remain the primary revenue base even as vertical farms attract increasing attention.

Indoor vertical farms are forecast to grow at a CAGR of 17.4% between 2026 and 2031, making them the fastest-growing facility type in the current outlook. This growth is tied to stacking potential, high yield per land unit for selected leaf crops, and an expanding pool of vacant buildings available for repurposing in dense urban areas. A 2025 study examined a former Galeria Karstadt Kaufhof store in Wuppertal and found that its freight elevators, loading docks, and structural load capacity already met key indoor farming requirements. Container farms and deep-water culture systems continue to serve useful roles in distributed urban supply and high-volume leafy vegetable production, but hold smaller market shares than the two primary formats. The next facility cycle in the Germany indoor farming market is likely to combine greenhouse economics with targeted vertical farm deployment in urban locations where land scarcity and retail proximity outweigh higher energy costs.

By Crop Type: Leafy Vegetables Dominate, Herbs and Microgreens Accelerate

Leafy vegetables accounted for 39.6% of the Germany indoor farming market in 2025, reflecting their strong fit with controlled-environment cultivation and fast turnover. Controlled-environment lettuce can complete a growth cycle in 28–35 days, compared with 60–90 days under field conditions, which supports frequent harvest scheduling and steadier cash conversion. Leafy crops also align closely with retailer demand for consistent appearance, freshness, and shorter transport distances in urban markets. For these reasons, they remain the most commercially established crop group across both greenhouse and vertical farm operations.

Herbs and microgreens are forecast to be the fastest-growing crop type between 2026 and 2031, at a CAGR of 14.2%. This growth is driven by high value per kilogram, short growing cycles, and strong demand from food service and specialty retail, where freshness and uniformity are priorities. Basil, tarragon, and wheatgrass are particularly well suited to vertical farm layouts, as their compact canopies allow dense stacking with limited shading loss. Indoor-grown herbs also face less import pressure during German winter months, which helps local operators maintain shelf space when field supply tightens. The Germany indoor farming market also sees growing interest in flowers, ornamentals, functional plants, and pharmaceutical-grade herbs, although these remain smaller and more specialized segments of current revenue. One structural constraint across premium herb categories is that hydroponic and aeroponic output cannot carry organic labeling under current European Union rules unless grown in soil, which means many producers must compete on pesticide-free positioning, traceability, and availability instead. While this does not eliminate demand, it does influence packaging decisions and buyer negotiations in premium herb categories.

Geography Analysis

The Germany indoor farming market was valued at USD 711.8 million in 2026, making it one of the largest controlled-environment agriculture markets in continental Europe. This position is supported by dense urban demand, a sizable market for cleaner-label food, and a broad mix of greenhouse, automation, and engineering capabilities that many neighboring countries are still developing. According to BÖLW (Bund Ökologische Lebensmittelwirtschaft) Industry Report 2025, Germany's organic food market was valued at EUR 18.2 billion (USD 19.5 billion) in 2025, which supports stronger price realization for indoor-grown produce compared to many other European markets. Fraunhofer ISI identified the reuse of vacant retail and industrial properties as a viable route for urban agriculture in Germany, providing a physical expansion advantage beyond consumer demand alone. Together, these conditions place Germany in a stronger position than most continental peers to scale commercial indoor farming across multiple city and regional formats.

Within Germany, Berlin is the most active urban hub, combining sustainability-focused retailers, food technology activity, and visible showcase projects. The REWE Green Farming Berlin facility, which opened in May 2026, brought a 2,760-square-meter rooftop greenhouse into operation above a supermarket, establishing a clear reference point for urban retail-led cultivation. Bavaria is another important region, where the Kirchweidach geothermal lettuce project serves as a working model for renewable energy-integrated hydroponics at commercial scale. Northern and eastern Germany face the most visible field-agriculture stress, which increases local demand for protected cultivation among buyers seeking supply reliability. Weather-related pressure on the 2024 grain harvest and severe spring dryness in 2025 further reinforce the case for controlled-environment output in exposed supply chains.

The Rhine-Ruhr region offers the strongest real estate pipeline for conversion, combining dense demand with large industrial and warehouse footprints. These assets can reduce capital intensity per square meter compared with greenfield development when structure, access, and utilities are already in place. Hamburg is also pursuing a policy-led approach through the Innovationsareal Öjendorf urban agriculture zone, which allocated land through autumn 2026 for commercial horticultural operators. Taken together, these patterns indicate that growth in the Germany indoor farming market will not be concentrated in a single city, but will spread across Berlin, Bavaria, Rhine-Ruhr, and selected northern and western nodes where retail demand, infrastructure reuse, and renewable energy integration align.

Competitive Landscape

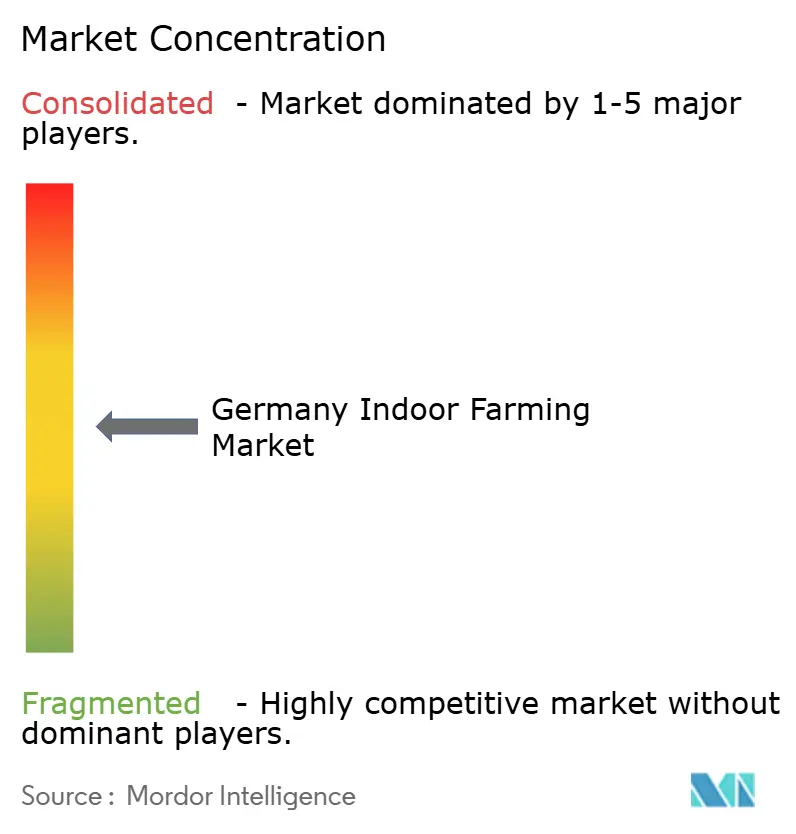

The Germany indoor farming market was moderately fragmented in 2025, with the top five players, Infarm Group GmbH, Signify N.V., Priva Holding B.V., Ridder Holding B.V., and KUBO Group B.V. holding a major share of the market. Market leadership is distributed across operators, lighting specialists, automation suppliers, greenhouse engineers, and input providers, rather than concentrated in a single dominant grower. Urban Crop Solutions and Agrotonomy are positioned among end to end farm operators, Signify and Valoya among lighting specialists, and Siemens AG, Bosch Rexroth AG, and Stulz GmbH among automation and climate control suppliers. In this structure, value is often captured through system integration, recurring service relationships, and long-term customer fit rather than scale alone. Partner networks and technical compatibility can be as important as brand recognition in winning projects.

Competition in the Germany indoor farming market is increasingly organized around ecosystems rather than stand-alone products. Signify's recognition at HortiContact 2026 for its Philips Unlock Lighting Intelligence system, along with its 2026 Horti Lighting Protocol integration with Ridder, illustrates how vendors are seeking to capture value through interoperable control layers and data-driven lighting management. Dürr AG's entry into vertical farming in June 2025 brought industrial ventilation and clean-air engineering capabilities from automotive production into indoor food systems. KUBO Group B.V. strengthened its position when its Ultra-Clima greenhouse tomato system received ISO based low CO2 recognition in 2025, providing a standards-backed sustainability credential for customers with stricter procurement requirements. These developments indicate that technical performance alone is no longer a sufficient differentiator, and that verified sustainability, integration compatibility, and energy responsiveness are gaining importance.

Partnerships are central to the Germany indoor farming market because no single supplier controls the full stack from crop genetics to lighting, automation, climate management, and retail placement. Identified white space includes technology as a service, infrastructure as a service, and specialty crop platforms for pharmaceutical herbs and nutraceutical applications, pointing to open competitive boundaries rather than closed ones. Körber Technologies and Veganz drew attention with the OrbiFarm aeroponic system and its reported trial yield gains, while REWE-backed infrastructure projects illustrated how retailers can become strategic counterparties rather than simple buyers. The market remains open enough for specialists to grow, but scale will likely favor companies that can combine engineering credibility, operating discipline, and reliable customer demand.

Germany Indoor Farming Industry Leaders

-

Infarm Group GmbH

-

Signify N.V. (Philips Horticulture LED Solutions)

-

Priva Holding B.V.

-

Ridder Holding B.V.

-

KUBO Group B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Schneebergerhof opened a high-tech greenhouse in Gerbach, Rhineland-Palatinate, Germany, equipped with direct wind and solar power supply. The facility grows tomatoes, salads, and herbs using 100% renewable energy. The Rhineland-Palatinate climate protection minister attended the public open day, indicating state-level policy alignment with energy-integrated indoor farming.

- June 2025: Dürr AG entered the vertical farming market with the commercial launch of its EcoY turnkey vertical farm system, developed with partner Clean Air Nurseries Agri Global. The patented grow-tube system stacks 80 seedlings vertically, uses up to 95% less water than conventional cultivation, and applies Dürr's industrial ventilation and climate control engineering from automotive applications to indoor food production. This marks a new-market entry for a major German engineering group.

- June 2025: Ridder Holding B.V. and Signify N.V. launched an integrated greenhouse automation and lighting solution connecting Ridder's Hortimax Pro climate computer with Signify's 4-channel GreenPower LED Toplighting Force under the Horti Lighting Protocol (HLP). The partnership delivers a plug-and-play connected control system for commercial growers, reducing integration complexity and enabling real-time lighting response to energy price signals and crop development stages.

Germany Indoor Farming Market Report Scope

Indoor farming refers to the cultivation of crops within controlled environments using systems such as hydroponics, aeroponics, aquaponics, soil-based setups, and hybrid methods to manage light, temperature, humidity, and nutrients more precisely.

The Germany indoor farming market is segmented by growing system (Aeroponics, Hydroponics, Aquaponics, Soil-Based, Hybrid), by facility type (Glass or Poly Greenhouses, Indoor Vertical Farms, Container Farms, Indoor Deep-Water Culture Systems, Other Facility Types), and by crop type (Fruits and Vegetables, Herbs and Microgreens, Flowers and Ornamentals, Other Crop Types). The market forecasts are provided in terms of value (USD).

| Aeroponics |

| Hydroponics |

| Aquaponics |

| Soil-Based |

| Hybrid |

| Glass or Poly Greenhouses |

| Indoor Vertical Farms |

| Container Farms |

| Indoor Deep-Water Culture Systems |

| Other Facility Types |

| Fruits and Vegetables | Leafy Vegetables |

| Tomato | |

| Strawberry | |

| Eggplant | |

| Other Fruits and Vegetables | |

| Herbs and Microgreens | Basil |

| Tarragon | |

| Wheatgrass | |

| Other Herbs and Microgreens | |

| Flowers and Ornamentals | Perennials |

| Annuals | |

| Ornamentals | |

| Other Flowers and Ornamentals | |

| Other Crop Types |

| By Growing System | Aeroponics | |

| Hydroponics | ||

| Aquaponics | ||

| Soil-Based | ||

| Hybrid | ||

| By Facility Type | Glass or Poly Greenhouses | |

| Indoor Vertical Farms | ||

| Container Farms | ||

| Indoor Deep-Water Culture Systems | ||

| Other Facility Types | ||

| By Crop Type | Fruits and Vegetables | Leafy Vegetables |

| Tomato | ||

| Strawberry | ||

| Eggplant | ||

| Other Fruits and Vegetables | ||

| Herbs and Microgreens | Basil | |

| Tarragon | ||

| Wheatgrass | ||

| Other Herbs and Microgreens | ||

| Flowers and Ornamentals | Perennials | |

| Annuals | ||

| Ornamentals | ||

| Other Flowers and Ornamentals | ||

| Other Crop Types | ||

Key Questions Answered in the Report

What is the projected value of Germany indoor farming by 2031?

The sector is forecast to reach USD 1,117.7 million by 2031 from USD 711.8 million in 2026.

Which growing system currently leads commercial adoption in Germany?

Hydroponics led with 47.8% share in 2025 because it combines a favorable cost-to-yield profile with a broad supplier base and familiar production methods.

Which facility type is expanding the fastest?

Indoor vertical farms are projected to grow at a 17.4% CAGR, supported by urban land limits and the reuse potential of vacant retail and industrial buildings.

Which crops generate the strongest current demand in controlled-environment farming?

Leafy vegetables led with 39.6% share in 2025, while herbs and microgreens are growing fastest at a 14.2% CAGR because of short cycles and premium pricing.

Page last updated on: