Germany Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

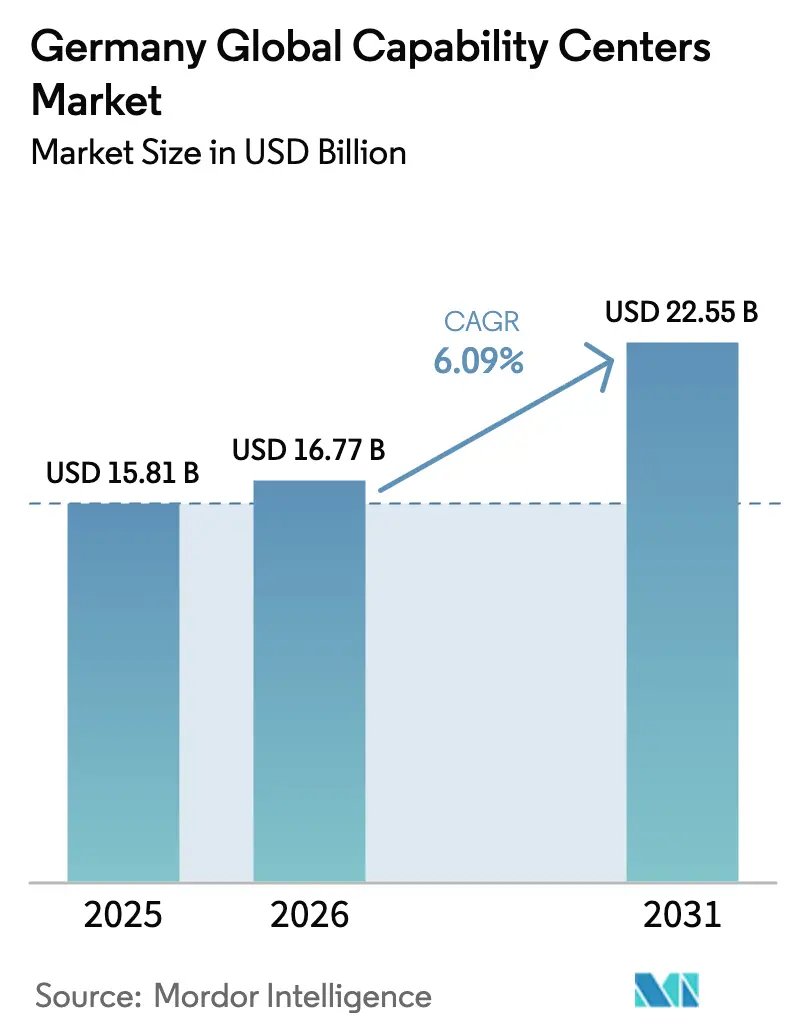

| Base Year Market Size (2025) | USD 15.81 Billion |

| Market Size (2026) | USD 16.77 Billion |

| Market Size (2031) | USD 22.55 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Global Capability Centers Market Analysis by Mordor Intelligence

The German Global Capability Centers market size is expected to grow from USD 15.81 billion in 2025 to USD 16.77 billion in 2026 and is forecast to reach USD 22.55 billion by 2031 at 6.09% CAGR over 2026-2031. Robust growth in engineering-intensive digital manufacturing, sovereign-cloud infrastructure build-outs, and post-Brexit realignment of EU shared services underpin the uptrend. Enterprises favor onshore centers that comply with the GDPR while tapping into Germany’s deep industrial expertise. Fresh capital outlays from hyperscale cloud vendors confirm infrastructure readiness, while generous R&D tax credits lower setup costs and maintain high investment momentum. Meanwhile, talent shortages and escalating sustainability mandates are driving demand for nearshore global capability centers models as firms seek resilient and compliant delivery footprints.

Key Report Takeaways

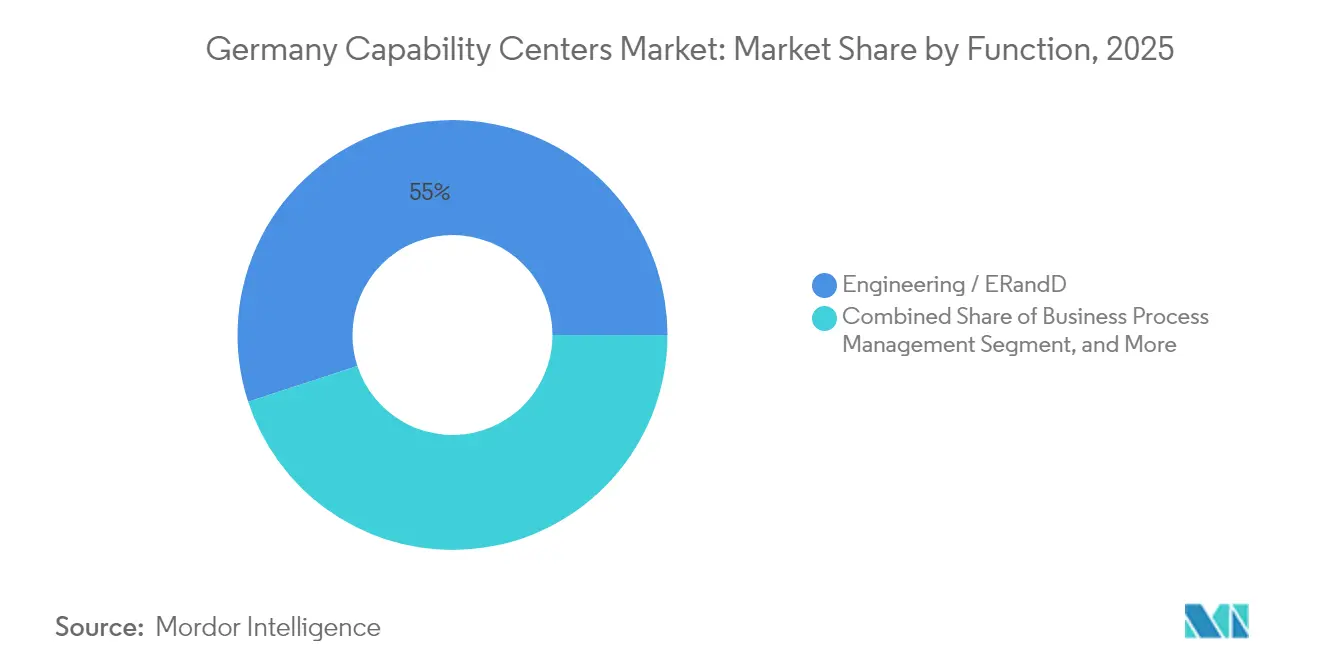

- By function, engineering and ER&D commanded 55.02% of Germany's Global Capability Centers market share in 2025; the cohort is expected to expand at a 6.44% CAGR through 2031.

- By engagement model, captive centers held a 61.78% revenue share of the German Global Capability Centers market size in 2025, while the hybrid build-operate-transfer model is projected to grow at a 7.11% CAGR through 2031.

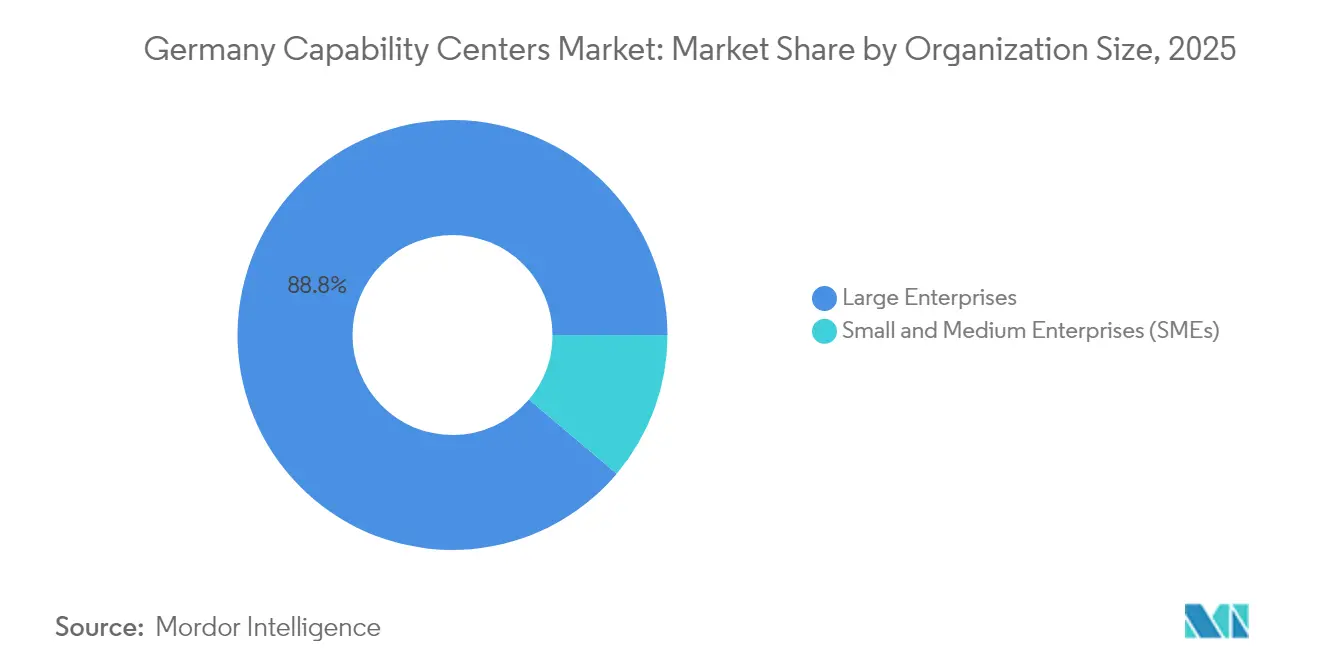

- By organization size, large enterprises led with 88.84% revenue share in 2025; small and medium enterprises are advancing at an 7.92% CAGR to 2031.

- By industrial vertical, manufacturing, automotive, and industrial accounted for 51.00% of the German Global Capability Centers market size in 2025; healthcare and life sciences are set to record the fastest growth, with a 6.74% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for nearshore digital transformation talent | +1.2% | Germany-wide, concentrated in Berlin, Munich, Frankfurt | Medium term (2-4 years) |

| Expansion of Industrie 4.0 requires localized ER&D hubs | +1.5% | Germany-wide, strongest in Baden-Württemberg, North Rhine-Westphalia | Long term (≥ 4 years) |

| Government R&D tax credits boosting captive investment | +0.8% | Germany-wide, enhanced benefits in eastern states | Short term (≤ 2 years) |

| Post-Brexit relocation of EU shared service activities to Germany | +1.1% | Germany-wide, concentrated in Frankfurt, Berlin | Medium term (2-4 years) |

| Accelerated cloud migration among Mittelstand enterprises | +0.9% | Germany-wide, rural areas lag behind urban centers | Medium term (2-4 years) |

| ESG compliance pressures favoring onshore data stewardship | +0.6% | Germany-wide, particularly financial services hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Nearshore Digital Transformation Talent

Germany’s 545,000-person digital skills gap is forcing companies to secure talent pipelines within the country rather than compete in the overheated freelance market, where senior developer day rates exceeded EUR 800 (USD 872) in 2024.[1]Boston Consulting Group, “Global Talent Shortage Reaches Record High,” BCG.COM Cultural proximity and time-zone overlap offset higher salaries, making the German Global Capability Centers market an increasingly viable choice for continuous product engineering. The government’s Skilled Immigration Act widens visa pathways, yet domestic capacity constraints persist, prompting firms to internalize capability centers for strategic roles. Captive hubs offer employers stronger retention levers, stable career paths, and faster security clearances compared to vendor models. The EUR 12 billion (USD 13.79 billion) Digital Pact earmarked for workforce upskilling adds further momentum.

Expansion of Industrie 4.0 Requiring Localized ER&D Hubs

Germany’s Future Investment Fund allocates EUR 10 billion (USD 11.49 billion) to advanced manufacturing, catalyzing local demand for engineering talent that must be physically close to production lines. Fraunhofer identified 847 Industrie 4.0 projects in 2024, 73% of which involved proprietary processes unsuitable for offshore teams. Automotive OEMs, such as BMW, have invested heavily in digital factories that depend on co-located software and hardware experts. Proximity eases TÜV certification, accelerates iteration cycles, and keeps sensitive data within German jurisdiction. These needs make the German Global Capability Centers market integral to the nation’s broader industrial digitalization road map.

Government R&D Tax Credits Boosting Captive Investment

The Forschungszulage now covers up to EUR 4 million (USD 4.6 million) of annual R&D spend per firm, with enhanced 35% rates for digital projects.[2]Federal Ministry of Finance, “Research and Development Tax Incentive,” BMF.BUND.DE When combined with regional investment grants of up to 40% in eastern states, total setup costs for a new center can decrease by 15-20%. These incentives are drawing development programs back onshore, particularly in the life sciences and automotive electronics sectors, where companies claim credits directly for in-house work. The reforms sharply improve the return on invested capital compared to vendor outsourcing, thereby deepening the Germany Global Capability Centers' market penetration among both multinationals and Mittelstand innovators.

Post-Brexit Relocation of EU Shared Service Activities to Germany

Frankfurt welcomed 127 financial institutions after the United Kingdom’s EU exit, turning the city into a continental compliance and risk hub. Deutsche Bank alone plans to shift 800 roles from London to Germany by 2024. Pharmaceutical and tech enterprises followed, favoring Germany’s GDPR rigor and direct regulatory access. This migration created immediate demand for multilingual finance, legal, and regulatory affairs teams embedded inside the German Global Capability Centers market, further anchoring it as Europe’s post-Brexit operations base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High labor cost versus Eastern Europe | -1.8% | Germany-wide, most pronounced in Munich, Frankfurt | Short term (≤ 2 years) |

| Scarcity of multilingual niche-skill talent | -0.9% | Germany-wide, acute in smaller cities | Medium term (2-4 years) |

| Stringent worker council regulations are slowing the ramp-up | -0.7% | Germany-wide, varies by state labor laws | Long term (≥ 4 years) |

| Competition from flexible freelance platforms | -0.5% | Germany-wide, strongest in tech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Labor Cost Versus Eastern Europe

Average German IT salaries of EUR 65,000-85,000 (USD 70,850-92,650) remain roughly 40-60% higher than pay rates in Poland or Hungary.[3]OECD, “Employment Outlook 2024,” OECD.ORG Social security contributions add 19.3% on top, inflating total employment cost and compressing margins for scale-sensitive functions. Although German productivity per hour is 15-20% higher than that of regional peers, the upfront payroll gap still deters some firms from undertaking deep back-office consolidation. High living expenses in Munich and Frankfurt intensify the challenge, making location selection and automation investments decisive for cost control within the German Global Capability Centers market.

Scarcity of Multilingual Niche-Skill Talent

Only 42% of German IT workers possess business-level English skills, versus 78% in the Netherlands. Linguistic limitations hinder multi-country support roles, forcing companies to cluster language-rich functions in cities such as Berlin or Munich. Shortfalls are sharper in emerging domains such as AI safety and quantum cryptography, where training materials appear sooner in English than in German. Although the government has earmarked EUR 2.5 billion (USD 2.87 billion) for language-focused upskilling, the payoff is years away, which will sustain tight labor supply and wage pressures within the German Global Capability Centers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: Engineering Leadership Drives Digital Manufacturing

Engineering and ER&D functions dominated the German Global Capability Centers market, accounting for a 55.02% share in 2025, and are projected to grow at a 6.44% CAGR through 2031. Close physical proximity to production lines ensures seamless integration with Industrie 4.0 equipment, enables rapid feedback loops, and satisfies stringent certification demands that offshore vendors cannot easily match. The German Global Capability Centers market size attributed to engineering exceeded USD 8.7 billion in 2025, driven by substantial investments from the automotive, industrial machinery, and process industries.

Information technology and digital services hold the second-largest slice, benefiting from the rapid adoption of enterprise cloud and the influx of post-Brexit financial workloads. Business process management has also matured, driven by the consolidation of standardized finance and procurement as firms seek operational efficiency. Knowledge process outsourcing remains a niche yet gains steady traction in regulatory analytics and intellectual property services, where German domain expertise is pivotal. Firms view engineering centers as strategic assets that protect intellectual property, secure compliance, and accelerate time-to-market, reinforcing the primacy of this segment within the German Global Capability Centers market.

By Engagement Model: Captive Dominance Meets Hybrid Innovation

Captive structures retained a 61.78% share in 2025 as German boards prioritize data sovereignty and direct governance over sensitive processes. This model enables companies to align their culture, enforce GDPR safeguards, and claim R&D tax incentives. However, hybrid build-operate-transfer vehicles are scaling fastest at 7.11% CAGR, allowing firms to de-risk entry while partners handle early-stage hiring, facilities, and compliance.

The German Global Capability Centers market size allocated to hybrid deals is forecast to surpass USD 6.47 billion by 2031, reflecting lessons learned from first-wave captives that grappled with ramp-up delays amid worker council negotiations. Managed service layers inside hybrid contracts address talent shortages and provide variable cost pools without sacrificing control. Traditional build-operate-transfer (BOT) continues to appeal to multinationals, allowing them to validate German cost structures before full insourcing. As regulations tighten and work councils gain influence, flexible engagement formats are expected to become hallmarks of mature Global Capability Center strategies.

By Organization Size: SME Growth Accelerates Digital Adoption

Large corporations still account for 88.84% of Germany's Global Capability Centers market revenues, leveraging scale economies and global footprints. Yet, small and medium enterprises are the fastest movers, recording an 7.92% CAGR, which is twice the pace of big enterprises. The KfW SME Digitalization report revealed that 67% of Mittelstand firms will expand technology outsourcing by 2027.

SMEs tend to gravitate toward modular Global Capability Center-as-a-service offerings that bundle cybersecurity, cloud management, and analytics under flexible subscription plans. They prioritize German-language support, regional data residency, and rapid compliance adaptation over exhaustive global scale. Vendors pitching turnkey centers in tier-two cities are lowering thresholds for entry, democratizing access to shared service models once reserved for multinationals. As government programs fund SME digitization, the German Global Capability Centers market will see a broader base of clients fueling demand for right-sized centers.

By Industry Vertical: Manufacturing Leads While Healthcare Accelerates

Manufacturing, automotive, and industrial companies held 51.00% of the German Global Capability Centers market in 2025, reflecting the sector’s reliance on embedded engineering competence and quality rigor. These firms tap Global Capability Centers for model-based design, digital twin development, and predictive maintenance algorithms that must align with German certification protocols.

However, the healthcare and life sciences sectors are the fastest climbers, with a 6.74% CAGR, as the EUR 4 billion (USD 4.6 billion) pharmaceutical strategy and the Berlin-Brandenburg cluster attract biotech and med-tech investments. Clinical-trial data stewardship, validated SaaS development, and pharmacovigilance demand GDPR-compliant environments, which the German Global Capability Centers market readily supplies. Financial services centers profit from post-Brexit scale-ups, while telecom and retail continue incremental digitization. The life sciences surge signals a future in which regulated industries drive incremental center formation, diversifying the sector mix of the German Global Capability Centers industry.

Geography Analysis

Germany’s federal structure is anchored by three distinct capability-center corridors, which together host the bulk of current facilities. The southern Bavarian and Baden-Württemberg cluster concentrates engineering-heavy operations linked to automotive and industrial equipment OEMs, thanks to proximity to suppliers and universities such as the Technical University of Munich. Berlin-Brandenburg forms the nation’s fastest-scaling digital and life-sciences hub, leveraging a vibrant start-up scene, multilingual talent pools, and below-average office rents that hovered around EUR 35-40 (USD 38-44) per square meter in 2024. [4]CBRE Germany, “Market Report 2024,” CBRE.DE Frankfurt and the surrounding Rhine-Main region complete the triad, specializing in banking, regulatory, and data-sovereignty services that followed Brexit-related moves by 127 financial institutions.

Targeted incentives shape location economics across these corridors. Eastern states, such as Saxony and Thuringia, provide investment grants of up to 40% of eligible project costs through the Joint Task for Regional Economic Development, a subsidy that narrows the labor-cost premium compared to Eastern Europe and accelerates greenfield builds for cloud and semiconductor projects. Western regions counter with superior fiber backbones, world-class logistics, and dense vendor ecosystems; as a result, ramp-up times for new Global Capability Center sites in Cologne or Düsseldorf are, on average, three months shorter than in less-connected cities. Nationwide, Germany’s central longitude supports continuous follow-the-sun delivery, with morning overlap in Asia and late-day handoffs to the Americas, an operational advantage that reduces overtime costs on multi-region programs.

Local specialization further differentiates sub-markets. Munich and Stuttgart dominate advanced driver-assistance and digital-twin engineering, attracting marquee investments such as BMW’s EUR 400 million (USD 459.56 million) digital factory in Regensburg, which pairs manufacturing lines with co-located software teams. Berlin’s bilingual workforce draws SaaS firms and biotech players that prize fast-growing AI expertise for drug discovery workloads. Hamburg’s port-centric economy drives the development of logistics analytics centers, while Hannover and Bremen leverage their historical aerospace expertise for simulation and certification services. Together, these localized strengths raise entry barriers for offshore competitors and solidify Germany’s position as Europe’s preferred onshore operations base for regulated, data-sensitive work.

Competitive Landscape

The German Global Capability Centers arena remains moderately concentrated, with the five largest service providers generating a significant share of revenue. Accenture, Deloitte, and Capgemini dominate the multi-process business services market, leveraging their long-standing client relationships with C-suite executives and comprehensive compliance toolkits. Indian technology majors Tata Consultancy Services, Infosys, and Wipro lead large-scale application services by blending onshore domain teams with mature offshore delivery, giving them cost leverage without breaching GDPR guardrails. German engineering consultancies, such as Bertrandt, EDAG, and IAV, are rapidly expanding their digital portfolios to defend core automotive relationships and capture higher-margin software work.

Investment by hyperscalers is redrawing the competitive map. Microsoft’s EUR 3.3 billion (USD 3.79 billion) program to add AI-optimized data centers in Berlin and Frankfurt, coupled with AWS’s EUR 7.8 billion (USD 8.96 billion) sovereign cloud build in Brandenburg, provides the secure infrastructure that mid-tier providers need to scale regulated workloads. Access to low-carbon, high-performance computing enables emerging specialists to differentiate themselves through GenAI accelerators, cyber-resilience blueprints, and advanced data governance services. Simultaneously, rising wage inflation is prompting all players to intensify their automation pipelines, which reduce manual effort in finance and HR processes by 25-35%, thereby preserving margins without offshoring sensitive data.

Strategic models are converging around hybrid delivery. Captive centers offer critical IP protection and R&D tax advantages, while managed-service overlays mitigate ramp-up risk and streamline labor-law compliance. Providers that master co-innovation frameworks, embedding product owners on-site while orchestrating global agile squads, win complex Industrie 4.0 and life-sciences deals that demand both physical proximity and cost efficiency. White-space opportunities persist in quantum-computing research, sustainable-manufacturing analytics, and reg-tech automation, niches where deep German domain knowledge and strict regulatory mandates create high entry barriers for generic outsourcers. Early movers securing talent and reference projects in these fields are well-positioned to capture a significant share of the market as it expands over the next five years.

Germany Global Capability Centers Industry Leaders

Accenture GmbH

Tata Consultancy Services Deutschland GmbH

Capgemini Deutschland GmbH

Cognizant Technology Solutions GmbH

IBM Deutschland Services GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Microsoft confirmed a EUR 3.3 billion (USD 3.79 billion) AI and cloud expansion spanning Berlin and Frankfurt to meet sovereign cloud rules.

- January 2025: AWS allocated EUR 7.8 billion (USD 8.96 billion) to Brandenburg sovereign cloud facilities for regulated workloads.

- December 2024: SAP earmarked EUR 500 million (USD 574.45 million) for AI research centers across Walldorf, Berlin, and Munich, adding 2,000 engineers.

- November 2024: Siemens Digital Industries launched a EUR 300 million (USD 344.67 million) software hub in Nuremberg for industrial IoT solutions.

Germany Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

What is the size of the German Global Capability Centers market in 2026?

The Germany Global Capability Centers market size is expected to reach USD 16.77 billion in 2026 and is projected to grow to USD 22.55 billion by 2031.

What is the main growth driver for capability centers in Germany?

The convergence of Industrie 4.0 manufacturing demands and sovereign-cloud requirements is the leading catalyst, propelling a 6.09% CAGR.

Which functional area captures the biggest share of German centers?

Engineering, ER&D functions lead with a 55.02% share, reflecting the need for on-site industrial digitalization expertise.

Why are hybrid build-operate-transfer models gaining traction?

Hybrid structures balance cost flexibility with Germany’s strict compliance needs, helping firms scale faster while retaining oversight.

Which industry vertical is expanding fastest inside German centers?

The healthcare and life sciences sector posts the highest 6.74% CAGR, boosted by the national pharmaceutical strategy and the Berlin-Brandenburg cluster.

How do Germany’s labor costs compare with Eastern Europe?

Salaries remain 40-60% higher than in Poland or Hungary, though productivity gains and tax incentives partially offset the premium.

Page last updated on: