Germany Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

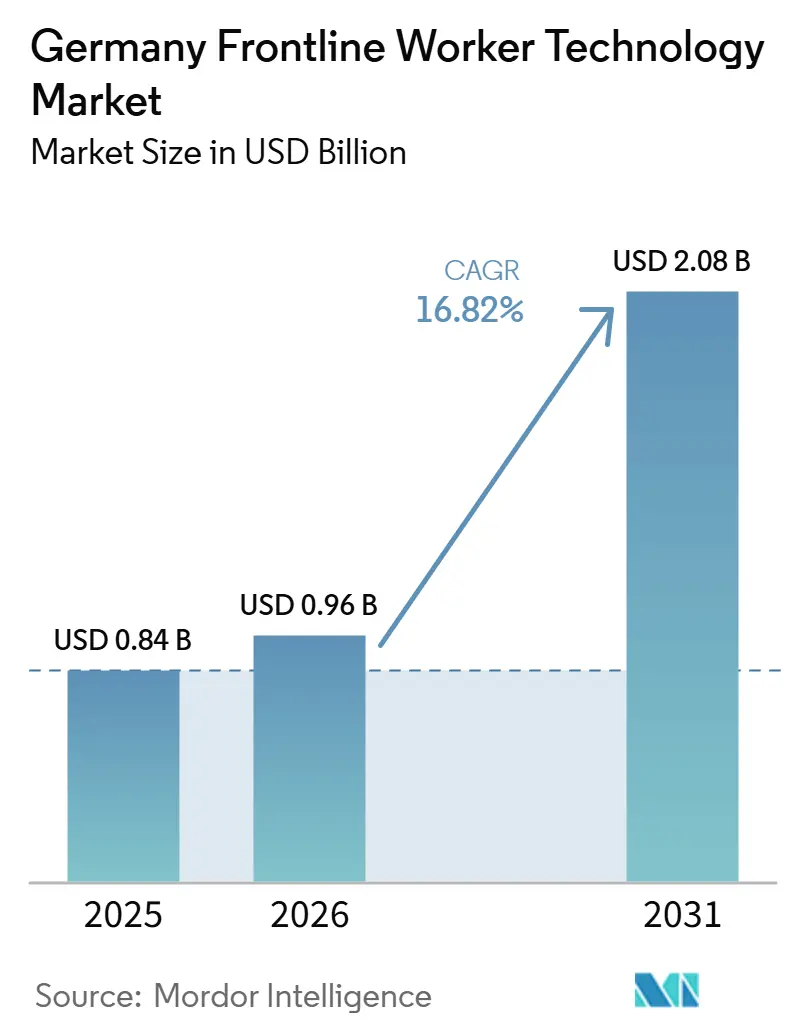

| Base Year Market Size (2025) | USD 0.84 Billion |

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 2.08 Billion |

| Growth Rate (2026 - 2031) | 16.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Frontline Worker Technology Market Analysis by Mordor Intelligence

The Germany frontline worker technology market size is projected to expand from USD 0.84 billion in 2025 to USD 0.96 billion in 2026, and reach USD 2.08 billion by 2031, growing at a CAGR of 16.82% from 2026 to 2031. The Germany frontline worker technology market is expanding because a very large share of the country’s workforce operates in deskless or field-based roles, while employer access to mobile and workflow tools still remains uneven across many frontline environments. Strong labor institutions, works councils, and sector-level agreements are also making digital workforce systems more necessary, especially for operators that manage many sites and cannot rely on manual shift administration. Competitive activity is increasingly centered on platform breadth, compliance readiness, and AI-enabled workflow automation, as vendors try to combine communication, scheduling, payroll, analytics, and identity functions in a single operating layer. The opportunity is also widening because employers are under pressure to improve output, retention, and staffing efficiency without depending on major headcount expansion. The main constraints still come from data governance, integration complexity, and employer caution around opaque workforce AI.

Key Report Takeaways

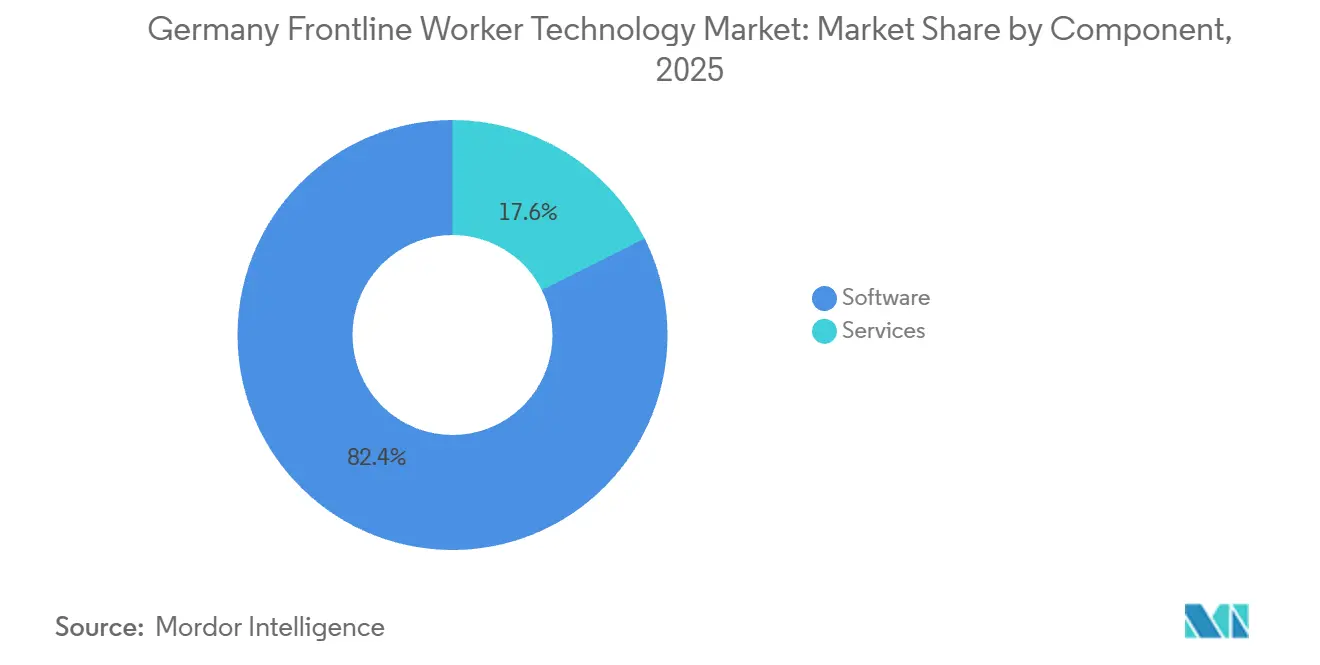

- By component, software led with 82.41% revenue share in 2025, while services are projected to expand at a 19.34% CAGR through 2031.

- By deployment, cloud-based deployment held 78.63% share in 2025 and is also projected to record the fastest growth at 17.42% CAGR through 2031.

- By organization size, large enterprises held 71.56% of the Germany frontline worker technology market share in 2025, while SMEs are projected to record the highest CAGR at 18.68% through 2031.

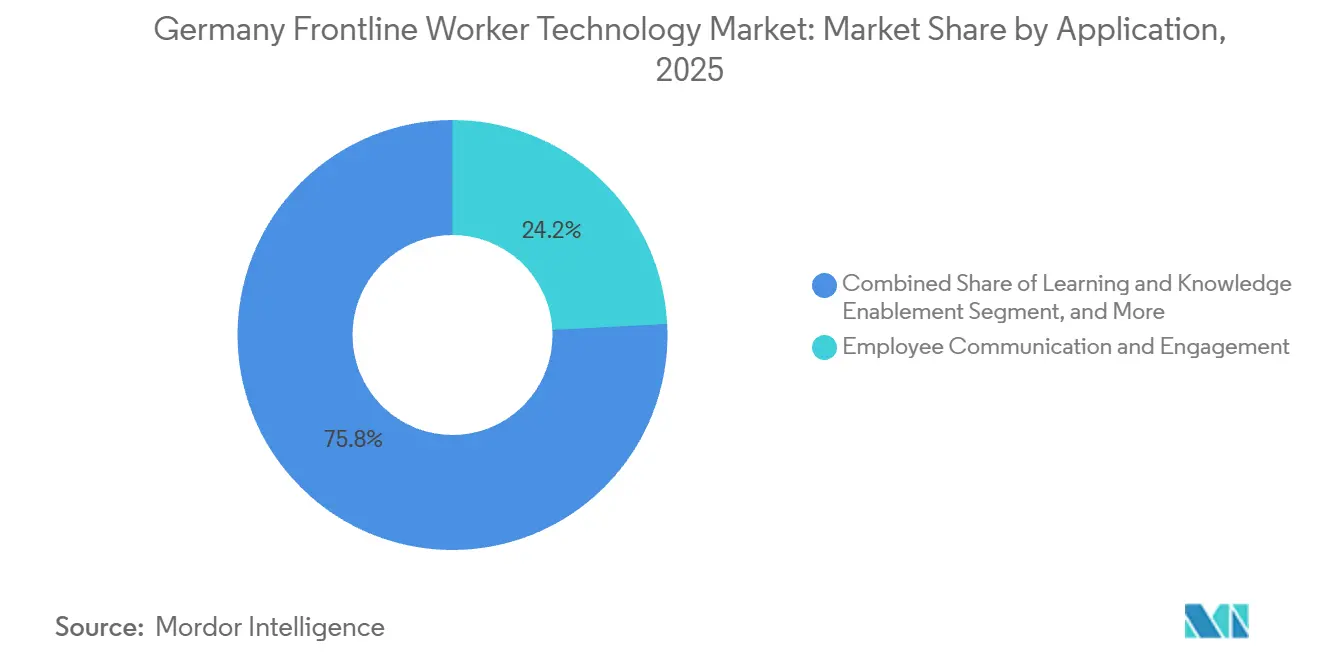

- By application, employee communication and engagement accounted for 24.18% of the Germany frontline worker technology market size in 2025, while workforce analytics and performance management is projected to expand at a 19.86% CAGR through 2031.

- By end-user industry, industrial manufacturing accounted for 32.36% share of the Germany frontline worker technology market in 2025, while transportation and logistics is projected to grow fastest at 19.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-First Digitization of Deskless Workflows | +4.2% | National, early penetration in Baden-Wurttemberg and Bavarian manufacturing corridors | Short term (≤ 2 years) |

| Labor-Rule Complexity Across Multi-Site Shift Operations | +3.5% | National, concentrated in NRW logistics hubs and multi-site retail chains | Short term (≤ 2 years) |

| AI-Led Labor Forecasting and Schedule Optimization | +3.0% | National, highest traction in retail, manufacturing, and last-mile logistics | Medium term (2-4 years) |

| Unified HR, Payroll, Scheduling, and Communication Stacks | +2.2% | National, strongest adoption momentum among German Mittelstand operators | Medium term (2-4 years) |

| Explainable AI and Audit-Ready Scheduling Demand | +1.5% | National, regulatory compliance hotspots in manufacturing and healthcare verticals | Medium term (2-4 years) |

| Worker Control Expectations Around Shifts, Pay, and Flexibility | +1.0% | National, generational shift most visible in hospitality and retail sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile-First Digitization of Deskless Workflows

A large part of the Germany frontline worker technology market still rests on a simple access gap, because many frontline workers lacked a company-provided mobile application in 2025. That gap matters because mobile-first platforms give workers access to schedules, tasks, learning content, and communication without requiring a PC, a shared terminal, or a company email address. This has made mobile access the practical first step for employers that want to improve coordination before they move into deeper workflow redesign. Flip’s growth from a German base into deployments that span more than 72 countries also showed that mobile-first frontline software can scale well beyond early communication use cases. Its customer examples, including Bosch, Rossmann, McDonald’s Germany, and Porsche, also showed that large enterprises were already using this model in demanding operating environments. Nagel-Group’s April 2025 pilot across 9 German sites and 600 employees showed that even established logistics operators were prioritizing this basic connectivity layer before broader process automation.[1]Nagel-Group, “Projektupdate Microsoft 365 Für ‘Frontline Worker’ - Nagel-Group Implementiert Pilotprojekt An Den Ersten Deutschen Standorten,” Nagel-Group, nagel-group.com

Labor-Rule Complexity Across Multi-Site Shift Operations

Germany’s labor framework creates a heavy administrative burden because federal working-time rules and site-level agreements both shape how frontline schedules must be built and recorded. This burden becomes much harder to manage when employers operate many sites and must reconcile tariff rules, rest periods, Sunday work rules, and public holiday premiums in real time. The coalition agreement and the expected Zeiterfassungsgesetz for 2026 are increasing the need for electronic time recording and compliant workforce tools across Germany. This regulatory pressure is one reason the Germany frontline worker technology market is moving from optional digitization toward more urgent operational adoption. For multi-site manufacturers, retailers, and logistics operators, the value of workforce platforms now lies as much in legal consistency as in labor efficiency. ATOSS’s FY2025 revenue of EUR 189.3 million (USD 204.8 million) reflected how compliance-driven demand continued to translate into enterprise renewal and expansion activity.

AI-Led Labor Forecasting and Schedule Optimization

The Germany frontline worker technology market is also being shaped by a shift from rules-based scheduling toward AI-led labor forecasting and schedule optimization. This shift matters because employers are no longer looking only for digital records; they are looking for better staffing decisions from the same workflow platform. Legion’s January 2026 release of more than 90 AI workforce management features showed how quickly forecasting, scheduling, and time-and-attendance decisions are being embedded into product design. Its platform analysis across more than 2 million employees linked full analytics use to a 33% average improvement in retention and an 11% improvement in employee NPS. As this capability matures, the Germany frontline worker technology market will increasingly reward vendors that can turn labor data into more reliable, explainable daily staffing decisions.

Unified HR, Payroll, Scheduling, and Communication Stacks

Platform consolidation is becoming more important because employers want fewer disconnected systems across payroll, communication, scheduling, task management, and HR administration. This matters in Germany because integration costs remain high when employers try to coordinate multiple point solutions across frontline and back-office processes. WorkJam’s January 2026 release introduced AI-native workflow capabilities and planned agent-to-agent orchestration, which showed how vendors were trying to work with existing enterprise systems rather than force full replacement. The need for unified stacks is also visible in German mid-market conditions, where AI usage is rising but often remains isolated instead of being connected through one operating layer. Ordio’s July 2025 funding round, which was tied directly to automated payroll for deskless sectors, showed that buyers were treating integrated payroll and scheduling workflows as a core requirement.[2]Ordio GmbH, “Ordio Sichert Sich €12M Series A Für Payroll AI,” Ordio, ordio.com This is helping the Germany frontline worker technology market move toward platforms that support compliance, pay, communication, and daily execution within one connected environment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Complexity Across HR, Payroll, POS, and EHR | -2.5% | National, most acute in German Mittelstand with heterogeneous ERP landscapes | Medium term (2-4 years) |

| Workforce Data Privacy and Mobile Cybersecurity Exposure | -1.8% | National, heightened sensitivity post-EuGH December 2024 and BAG May 2025 rulings | Short term (≤ 2 years) |

| Shared-Device Identity and Digital Access Gaps | -1.2% | National, concentrated in factory shopfloor and construction-site environments | Short term (≤ 2 years) |

| Manager and Worker Distrust of Opaque Scheduling AI | -0.8% | National, cross-sector, more pronounced in unionized manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Integration Complexity Across HR, Payroll, POS, and EHR

Legacy integration remains the most direct operating restraint on the Germany frontline worker technology market because frontline tools often need to connect with SAP, payroll systems, retail platforms, and sector-specific infrastructure. This issue is especially significant in Germany because many employers run mixed enterprise environments that were not designed for fast frontline application rollouts. As a result, pre-sales discovery, workflow mapping, and deployment planning can take much longer than the software evaluation itself. That slows deal velocity for vendors and also delays adoption among smaller employers that need clearer payback before they commit to implementation work. Vendors that can build around existing HR and workforce systems without forcing a full migration are therefore in a stronger position to win and retain enterprise accounts. Until interoperability becomes easier, this friction will continue to limit faster rollout across cost-sensitive parts of the Germany frontline worker technology market.

Workforce Data Privacy and Mobile Cybersecurity Exposure

Data privacy remains a major brake on adoption because German employers are highly sensitive to how employee information is collected, stored, and used. This issue becomes more difficult when frontline applications process location data, biometric time-clock records, or performance metrics on personal mobile devices. Shared-device environments in factories and logistics operations also make identity control and access governance more complex. That is why compliance design has become part of the product decision, rather than a legal review that happens after software selection. Platforms that embed DACH-specific compliance into the application layer can reduce risk for customers and shorten internal review cycles with works councils and legal teams. This makes data architecture, mobile security, and audit readiness central competitive factors in the Germany frontline worker technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates as Services Gain Strategic Depth

Software held 82.41% of Germany frontline worker technology market share in 2025, which kept it as the main revenue base because the earlier phase of adoption centered on core applications such as scheduling, communication, and learning. This position also reflected the strong role of SaaS delivery, which helped employers roll out standardized frontline tools across large employee groups with less infrastructure overhead. The software lead shows that most buyers still begin with application ownership before they widen spending into more complex operating support. At the same time, services are projected to expand at a 19.34% CAGR through 2031, which makes them the faster-growing side of the component mix in the Germany frontline worker technology market.

This stronger services growth reflects the greater need for implementation, customization, training, and managed support as employers adopt broader frontline platforms that touch payroll, HR, communication, and analytics. ATOSS’s consulting services revenue reached EUR 39.6 million (USD 42.8 million) in FY2025, which showed that service intensity was rising even inside a software-led supplier base. Flip’s June 2026 AI Flow Builder also pointed to a shift inside the services layer, because faster AI-assisted workflow creation can reduce routine configuration effort for standard use cases.[3]Flip GmbH, “Forward 2026: Four Product Launches for Better Frontline Work,” Flip GmbH, getflip.com That means the Germany frontline worker technology industry is likely to keep software dominant in absolute terms, while services move further toward compliance design, governance support, and AI training.

By Deployment: Cloud Adoption Shapes the Digital Access Model

Cloud-based deployment held 78.63% share in 2025 and is projected to expand at a 17.42% CAGR through 2031, which made it both the largest and the fastest-growing deployment model in the Germany frontline worker technology market. This dual position shows that the country is still moving through a broad cloud adoption cycle rather than nearing saturation. Cloud delivery has become the preferred model because it supports quicker deployment, easier updates, and better access for workers who do not operate from desks or fixed terminals. It also gives vendors a clearer route into mid-sized employers that do not want to maintain local infrastructure for every frontline application.

Hybrid deployment still remains relevant in regulated environments where employers want sensitive workforce information tied more closely to existing internal systems while using cloud orchestration for broader access and analytics. On-premises systems continue to matter for a narrower group of industrial operators with strict internal IT rules and large legacy investments, but their role is gradually receding in the Germany frontline worker technology market. Germany’s cloud transition has moved more carefully because works councils often require clarity on employee data location and access controls before approving migration. Flip’s Frontline Identity launch in June 2026 addressed one of the biggest access barriers by allowing authentication through QR code, passkey, or invite code without a company email, which directly supported broader cloud adoption.

By Organization Size: Enterprise Scale Leads as SMEs Accelerate

Large enterprises held 71.56% revenue share in 2025, which reflected the scale and complexity of managing large frontline workforces across many distributed sites in the Germany frontline worker technology market. This lead was structural because automotive groups, retailers, logistics operators, and manufacturers face much higher coordination costs when scheduling, and compliance still depends on fragmented local processes. For these buyers, the cost of manual administration becomes unsustainable earlier because even small process gaps multiply quickly across large teams and many locations. That has kept enterprise buyers at the center of vendor strategy, especially for deployments that connect workforce management with broader HR and payroll systems.

SMEs are projected to grow at an 18.68% CAGR through 2031, which places them above the overall market pace and points to a faster trickle-down adoption cycle. This acceleration suggests that lower deployment costs, cloud delivery, and simpler onboarding are making frontline technology more practical for smaller employers. Ordio’s July 2025 funding round, which was specifically aimed at automated payroll for Germany’s non-desk sectors, showed that suppliers already saw SME demand as a near-term growth path rather than a distant one. The expected electronic time-recording push in 2026 should reinforce this shift, because the compliance requirement is moving forward while affordable product access is improving in the Germany frontline worker technology market.

By Application: Communication Anchors Share as Analytics Drives Value

Employee communication and engagement accounted for 24.18% of the Germany frontline worker technology market size in 2025, which made it the largest application because employers usually begin with the most visible coordination problem first. Replacing whiteboards, paper notices, and fragmented messaging creates clear operating gains with less disruption than a full process redesign. This first layer also creates the access base on which scheduling, task coordination, learning, and compliance workflows can later be built. That sequence has helped the Germany frontline worker technology market expand in stages, with communication acting as the entry point for broader frontline digitization.

Workforce analytics and performance management are projected to expand at a 19.86% CAGR through 2031, which makes analytics the fastest-growing application group. That rise reflects a more mature buyer focus, because employers that already digitized communication are now looking for measurable labor, retention, and productivity gains. Legion’s platform results linked fuller analytics use to a 33% average improvement in retention and an 11% improvement in employee NPS, which strengthened the value case for this layer. Learning and enablement tools are also moving forward, as shown by Axonify’s May 2026 AI enhancements, which were designed to connect training activity more closely with operational execution.

By End-User Industry: Manufacturing Anchors Market as Logistics Accelerates

Industrial manufacturing accounted for 32.36% share of the Germany frontline worker technology market size in 2025, which made it the largest end-user base because Germany’s industrial system combines large frontline workforces with complex shift and compliance structures. This lead is reinforced by the high value of even small coordination gains in production continuity, labor utilization, and quality management. Bosch’s use of agentic AI in its Bamberg plant and its decision to offer the technology externally since late 2025 showed how frontline systems were starting to connect with broader operational automation. WorkJam’s Manufacturing Connect launch in December 2025 also showed direct vendor focus on automotive OEMs, suppliers, consumer packaged goods, pharmaceutical manufacturers, and warehouse and distribution operators inside the Germany frontline worker technology market.

Transportation and logistics are projected to grow at a 19.27% CAGR through 2031, which makes them the fastest-growing end-user category. That growth is tied to labor intensity, network complexity, and the need for better communication, documentation, and schedule discipline across distributed operations. Healthcare and life sciences are also becoming more relevant after the 2025 extension of Germany’s Telematics Infrastructure obligation into outpatient and inpatient care settings. Retail and e-commerce remain active through store-level productivity deployments, including DM’s October 2025 partnership with VusionGroup for the EdgeSense digital shelf platform, while construction and public administration still offer open space for further vendor focus.

Geography Analysis

The Germany frontline worker technology market is shaped by strong regional differences in industrial density, enterprise scale, and digital readiness, with Bavaria and Baden-Wurttemberg acting as the main adoption centers. Bavaria benefits from the presence of ATOSS in Munich and from the concentration of automotive and industrial employers that require structured workforce management across many facilities. Baden-Wurttemberg plays a similar role through Flip’s Stuttgart base and through the major manufacturing presence of Porsche, Robert Bosch, and Daimler Truck. This southern concentration gives the Germany frontline worker technology market a strong industrial anchor in mobile communication, scheduling, workforce control, and connected shopfloor execution.

North Rhine-Westphalia remains highly significant because its logistics scale and diverse industrial base create persistent demand for scheduling, compliance, and workforce coordination tools. Hamburg is also gaining importance because port logistics, retail operations, and distribution activities are creating more need for connected frontline systems. Berlin’s effect is more indirect, but its startup environment and pilot-friendly enterprise base help speed up vendor visibility and product testing. These western and northern centers widen the Germany frontline worker technology market beyond its southern manufacturing core. They also support a more varied demand base that includes logistics, retail, and mixed-service operating models alongside industrial users.

Germany’s eastern states, including Saxony and Thuringia, represent a meaningful mid-term opportunity because manufacturing presence is rising while digital adoption remains less mature. This creates room for vendors that can support organizations moving from limited digitization toward more connected frontline systems. The expected Zeiterfassungsgesetz should create a more uniform national trigger for adoption, even if implementation support remains concentrated in larger business centers. As a result, the Germany frontline worker technology market should continue to expand geographically, but adoption depth will still vary according to local enterprise concentration, operational complexity, and support capacity.

Competitive Landscape

The Germany frontline worker technology market remains moderately fragmented, with competition spread across German domestic specialists, pan-European workforce platforms, and global frontline operations providers. German vendors such as ATOSS, Flip, and Ordio retain clear relevance because local compliance depth, DACH labor familiarity, and existing enterprise relationships still matter in buying decisions. At the same time, pan-European and global suppliers continue to strengthen their position with broader product coverage across workforce management, engagement, learning, analytics, and connected execution. This keeps the Germany frontline worker technology market active on platform breadth, AI usefulness, and compliance readiness rather than on price alone.

The October 2024 acquisition of WorkForce Software by ADP strengthened the enterprise end of the market by adding specialized scheduling and deskless capabilities to a larger global HCM distribution network. The July 2025 merger of LumApps and Beekeeper created a larger combined platform for desk-based and frontline employees, which increased pressure on narrower specialists to differentiate more clearly.[4]LumApps, “LumApps And Beekeeper To Join Forces, Creating The Leading Employee Experience Platform For The Future Of Work,” LumApps, lumapps.com Flip responded by moving further beyond communication through its June 2026 launches, including Frontline Identity, Flip Fusion, an AI Agent Gateway, and an AI Flow Builder. ATOSS also reinforced its position by investing more than 15% of FY2025 revenue in research and development focused on AI-powered forecasting services, workforce intelligence, and AI agents.

Open space remains most visible in construction, SME hospitality, and public administration, where targeted frontline deployment models are still less developed than in manufacturing, retail, and logistics. That leaves room for emerging suppliers such as Ordio, which is targeting payroll automation for Germany’s deskless segments, and for other vendors that can bridge the gap between point tools and enterprise-grade workforce platforms. The Germany frontline worker technology industry is therefore consolidating around stronger platforms at the top, while still leaving space for specialized providers that solve local workflow and compliance issues well. This balance between selective consolidation and continued fragmentation is likely to remain a defining feature of the Germany frontline worker technology market through the forecast period.

Germany Frontline Worker Technology Industry Leaders

ATOSS Software SE

Axonify Inc.

LumApps

Connecteam Ltd.

Deputy Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Flip GmbH launched four AI-native products at its Forward 2026 conference in Frankfurt: Frontline Identity (secure personal digital credential for workers without company email), Flip Fusion (AI-native app builder with built-in DACH compliance framework), an AI Agent Gateway connecting frontline workflows to Workday, SAP, and Salesforce via Model Context Protocol, and an AI Flow Builder capable of generating complete operational workflows from plain-language instructions. The launches marked Flip's strategic positioning as a full frontline operating system rather than a communication point solution.

- May 2026: Axonify unveiled significant AI enhancements at the Association for Talent Development Annual Conference in Los Angeles, including the Rollout tool, an AI-powered capability replacing manual coordination with structured tracking across every location, and new AI coaching features. The platform additions are designed to close the gap between learning completion and measurable operational execution for frontline organizations.

- April 2026: WorkJam announced a partnership with Bensons for Beds to digitally connect more than 1,800 colleagues across 178 UK stores, manufacturing, and distribution, consolidating legacy communication, task, and learning systems into a single WorkJam platform. The deal reinforced WorkJam's European retail vertical strategy.

- January 2026: ATOSS Software SE reported FY2025 revenue of EUR 189.3 million (USD 204.8 million), a 20th consecutive record year, with cloud and subscription ARR growing 28% to EUR 101.3 million (USD 109.5 million). ATOSS guided FY2026 revenue to approximately EUR 215 million (USD 234.9 million).

Germany Frontline Worker Technology Market Report Scope

The Germany frontline worker technology market comprises software platforms, connected applications, and associated services designed to digitally enable deskless and field-based employees across industries such as retail, industrial manufacturing, healthcare, transportation and logistics, hospitality, construction, and the public sector. These solutions improve frontline productivity, communication, task execution, workforce coordination, learning, operational visibility, safety, and compliance by integrating mobile devices, wearable technologies, artificial intelligence (AI), Internet of Things (IoT) sensors, cloud platforms, and enterprise business systems. The market includes revenue from software subscriptions and licenses, as well as professional and managed services supporting deployment, integration, customization, training, and ongoing support.

The Germany Frontline Worker Technology Market Report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), and End-user Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the 2026 value of the Germany frontline worker technology sector?

It measures USD 0.96 billion in 2026 and is projected to reach USD 2.08 billion by 2031 at a 16.82% CAGR.

Which component leads revenue in Germany?

Software led with an 82.41% share in 2025, while services are forecast to grow faster at a 19.34% CAGR through 2031.

Why is cloud deployment leading adoption?

Cloud-based deployment held 78.63% share in 2025 and also has the fastest projected growth at 17.42% CAGR because it supports faster rollout and easier mobile access.

Which buyers are driving the next wave of adoption?

Large enterprises still lead revenue with 71.56% share, but SMEs are projected to grow faster at an 18.68% CAGR as lower-cost cloud tools become more practical.

Which application area is growing the fastest?

Workforce analytics and performance management is projected to expand at a 19.86% CAGR, even though employee communication and engagement held the largest share in 2025.

Which end-user group offers the strongest growth outlook?

Industrial manufacturing remains the largest end-user at 32.36% share, while transportation and logistics is projected to grow fastest at a 19.27% CAGR through 2031.

Page last updated on: