Germany Enterprise Content Management (ECM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

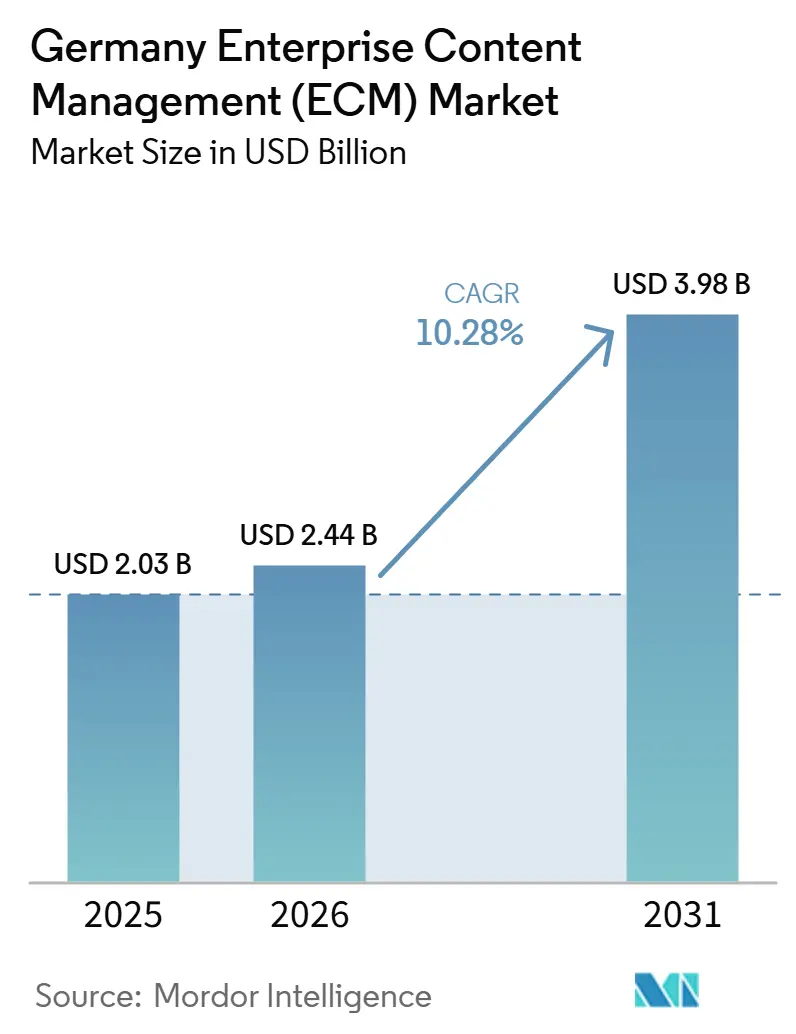

| Base Year Market Size (2025) | USD 2.03 Billion |

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.98 Billion |

| Growth Rate (2026 - 2031) | 10.28% CAGR |

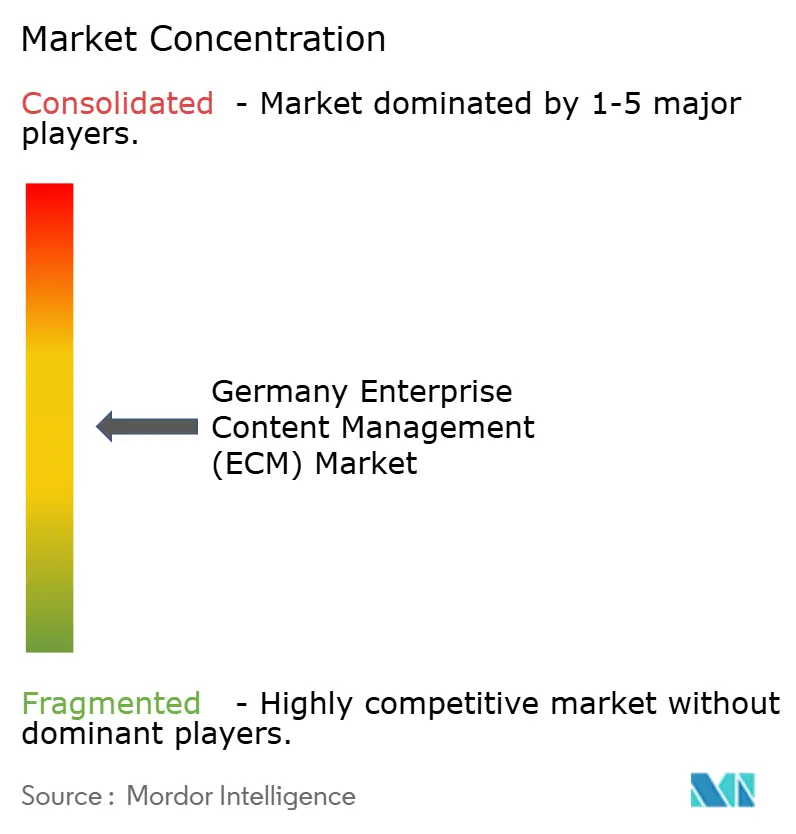

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Enterprise Content Management (ECM) Market Analysis by Mordor Intelligence

The Germany enterprise content management (ECM) market size was valued at USD 2.03 billion in 2025, USD 2.44 billion in 2026 and is projected to reach USD 3.98 billion by 2031, at a CAGR of 10.28% from 2026 to 2031. Demand is closely tied to compliance needs because tax record retention, data protection, and structured invoicing rules have made document control an operating requirement. SAP modernization is also shaping buying decisions, as enterprises seek content platforms that integrate cleanly into S/4HANA environments and support workflows outside the ERP core. AI is raising expectations beyond storage, and buyers now look for faster classification, search, and task routing across large volumes of unstructured files. Cloud adoption remains strong because subscription delivery and prebuilt workflow services lower entry barriers, yet sovereignty concerns still keep hybrid models relevant in regulated settings. Competition remains balanced between global software groups and German specialists, leaving room for vendors that combine compliance depth, local delivery, and certified integration.

Key Report Takeaways

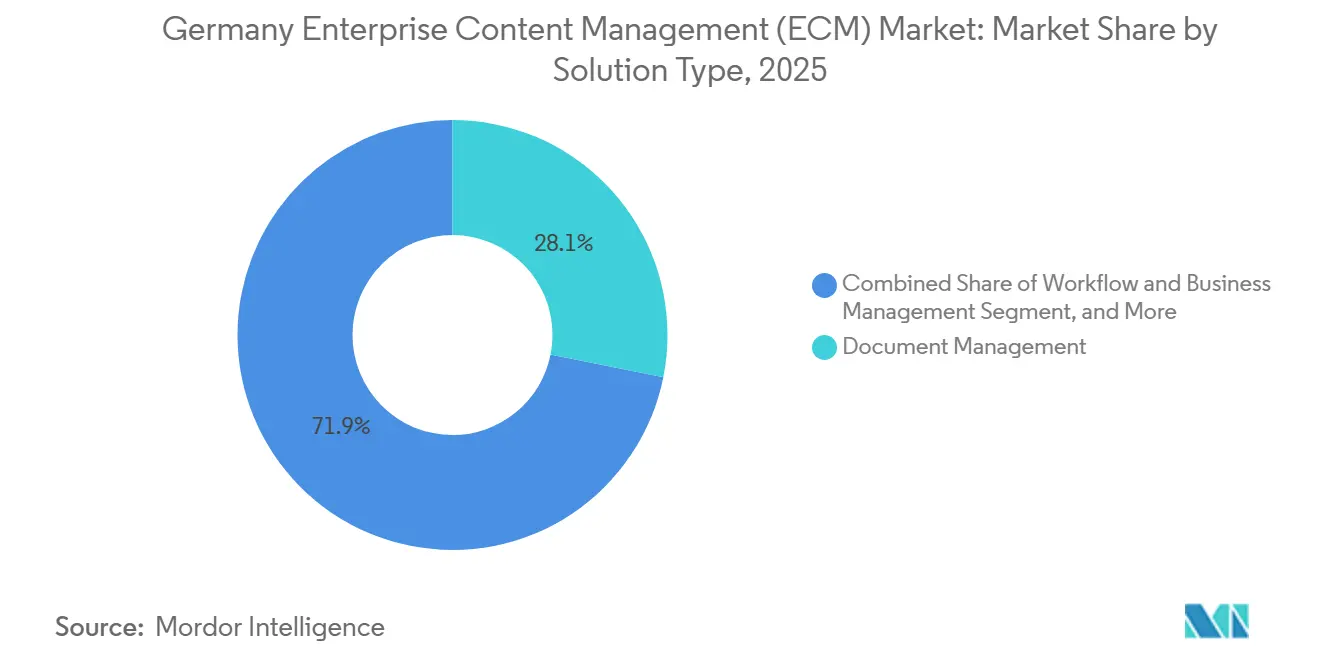

- By solution type, document management held 28.14% share in Germany enterprise content management (ECM) market in 2025, while workflow and business process management are projected to expand at a 12.82% CAGR through 2031.

- By deployment mode, cloud held 73.41% share of the Germany enterprise content management (ECM) market in 2025 and is projected to record the highest growth at a 13.24% CAGR through 2031.

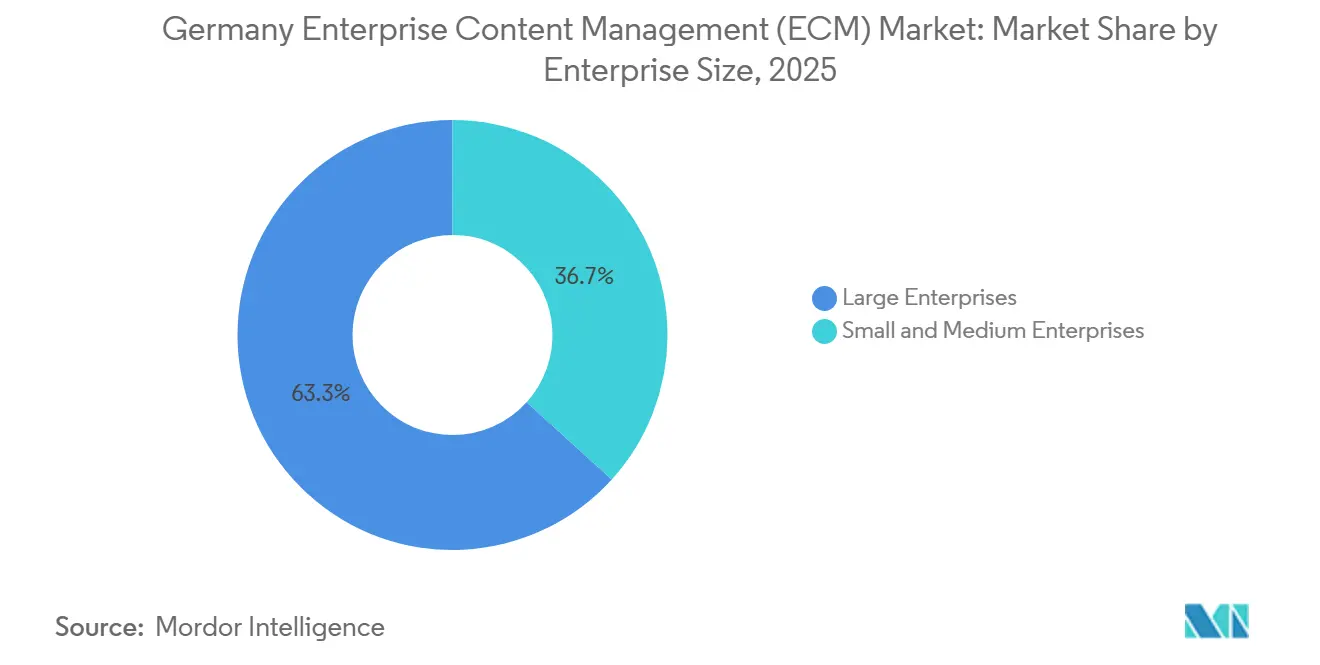

- By enterprise size, large enterprises accounted for 63.28% of revenue in 2025, while SMEs are projected to grow at a 12.49% CAGR through 2031.

- By end-user industry, BFSI held 24.53% share in 2025, while healthcare is projected to advance at a 12.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Enterprise Content Management (ECM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Compliance and Audit Readiness Across German Enterprises | +2.8% | National, concentrated in Frankfurt, Munich, and Hamburg | Short term (≤ 2 years) |

| AI-Enabled Classification and Search for Unstructured Content | +2.2% | National, with early intensity in BFSI and manufacturing hubs | Medium term (2-4 years) |

| Accelerated Cloud Migration From Legacy On-Premises Repositories | +1.8% | National, with higher traction in NRW and Bayern SME clusters | Medium term (2-4 years) |

| SAP-Centric Content Integration Demand in Industrial Enterprises | +1.5% | National, concentrated in Bayern, Baden-Württemberg, and NRW | Medium term (2-4 years) |

| Hybrid Workforces Increasing Need for Secure Content Collaboration | +1.0% | National, led by IT and professional services clusters | Short term (≤ 2 years) |

| Public Sector eFile and eAkte Modernization Programs | +0.8% | National, concentrated in Berlin, Hamburg, and Munich | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance And Audit Readiness Across German Enterprises

Germany’s compliance structure gives the Germany enterprise content management (ECM) market a firm demand base. The Wachstumschancengesetz required all VAT-registered enterprises to receive invoices in structured digital formats from Jan 1, 2025.[1]Federal Ministry of Finance, “Wachstumschancengesetz,” Bundesministerium der Finanzen, bundesfinanzministerium.de The rollout also extends to invoice issuance from 2027 for enterprises with annual turnover above EUR 800,000 (USD 866,000), and from 2028 for the remaining businesses. These rules matter because document storage now has to support traceability, retention, and reliable retrieval during audits. That change is bringing smaller firms into formal document management for the first time. As those firms move beyond invoice archiving, the Germany enterprise content management (ECM) market gains follow-on demand for workflow, records control, and search tools.

AI-Enabled Classification and Search for Unstructured Content

AI adoption is pushing the Germany enterprise content management (ECM) market toward more active use of content rather than passive storage. The DSAG Investment Report 2026 showed that 43% of surveyed DACH companies had already implemented AI use cases, and 77% of those production deployments relied on non-SAP AI solutions.[2]German-Speaking SAP User Group, “DSAG Investment Report 2026: AI Establishes Itself,” DSAG, impulsant.dsag.de That pattern favors ECM vendors that can connect to multiple AI stacks, rather than locking customers into a single route. ELO strengthened its position in this direction with ELO ECM Suite 25, which added an AI assistant and broader low-code support in 2025. Buyers are now expecting better classification, faster retrieval, and less manual handling in document-heavy processes. As these functions improve, the Germany enterprise content management (ECM) market is likely to see more spending on process acceleration and search quality.[3]ELO Digital Office GmbH, “ELO ECM Suite 25: Consistent Focus on Low-Code and AI,” ELO Digital Office, elo.com

Accelerated Cloud Migration from Legacy On-Premises Repositories

Cloud migration continues to support the Germany enterprise content management (ECM) market, but the shift is moving in stages rather than in a straight line. The DSAG Investment Report 2026 showed that on-premises S/4HANA use reached 56% across DACH enterprises, indicating that many ECM environments still sit alongside locally managed ERP estates. At the same time, the DIHK Digitalization Survey 2026 showed that German businesses see themselves as strongly or fully dependent on non-EU providers for cloud infrastructure and AI platforms. That tension supports hybrid transition models, where firms add cloud services without removing regulated repositories too quickly. Sovereignty programs such as Gaia-X also keep architecture choices under close review during enterprise and public-sector buying cycles. Vendors that combine cloud delivery with migration support and residency controls are therefore in a stronger position.

SAP-Centric Content Integration Demand in Industrial Enterprises

SAP integration remains one of the clearest purchasing filters in the Germany enterprise content management (ECM) market. The DSAG Investment Report 2026 showed that 45% of respondents assigned a high or medium investment priority to SAP Business Technology Platform integration, which links ECM demand to SAP modernization budgets. OpenText strengthened its standing in Nov 2025 when it became the first SAP Solution Extensions document management platform certified for SAP S/4HANA Cloud Public Edition under GROW with SAP.[4]OpenText Corporation, “OpenText Expands Collaboration with SAP to Deliver AI-Ready Cloud Content Management at Scale,” OpenText, opentext.com This matters in Germany because large industrial firms often treat SAP as the center of process control, records flow, and master data management. Vendors without certified interfaces face longer sales cycles and higher technical scrutiny. SAP also widened the ecosystem signal in Sep 2025 through its sovereign OpenAI for Germany partnership, indicating that content-heavy public sector workflows are moving closer to SAP-led environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Migration Complexity From Legacy ECM Estates | -1.5% | National, most acute in manufacturing and public sector with 15+ year legacy deployments | Long term (≥ 4 years) |

| Data Sovereignty Concerns Slowing Cloud Adoption | -1.2% | National, concentrated in BFSI, healthcare, and public sector | Medium term (2-4 years) |

| Integration Friction With ERP, CRM, and Sector-Specific Applications | -0.8% | National, strongest in manufacturing and healthcare | Medium term (2-4 years) |

| Premium Implementation and Governance Costs for Mid-Market Buyers | -0.5% | National, concentrated in SMEs below EUR 100 million (USD 108 million) annual revenue | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Migration Complexity from Legacy ECM Estates

Legacy repositories continue to slow the Germany enterprise content management (ECM) market where old systems remain deeply tied to operating processes. Many large organizations still manage years of archived documents, custom metadata structures, and sector-specific retention rules inside systems that cannot be moved quickly. The problem is even larger when ECM environments are linked to customized SAP ECC workflows that now need redesign to achieve cleaner S/4HANA integration paths. The DSAG evidence continues on-premises S/4HANA use supports the view that many enterprises are still carrying long transition cycles across core systems. Migration programs, therefore, often become multi-year efforts before users see clear functional gains. This slows replacement activity even when enterprises accept the long-term need to modernize.

Data Sovereignty Concerns Slowing Cloud Adoption

Data sovereignty remains a meaningful restraint on the Germany enterprise content management (ECM) market, especially in regulated sectors. The DIHK Digitalization Survey 2026 showed that German companies are highly dependent on non-EU providers for cloud infrastructure and AI platforms. That concern raises scrutiny over data residency, operational control, and vendor access conditions during procurement. OpenText responded to this pressure in Apr 2026 by expanding sovereign cloud options through its S3NS partnership and its European cloud positioning. Public sector, healthcare, and BFSI buyers are therefore moving more cautiously when evaluating multi-tenant content platforms. The result is a slower cloud decision cycle, even when the long-term economic case remains favorable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Process Automation Expands Beyond Core Document Control

Document management held 28.14% of Germany enterprise content management (ECM) market share in 2025, while workflow and business process management is projected to expand at a 12.82% CAGR through 2031. This split shows that storage and control still anchor revenue, but new spending is moving toward process execution. German enterprises increasingly want content systems to trigger approvals, validate records, and support exception handling across regulated workflows. SAP’s clean-core direction raises the value of ECM platforms that can handle workflow outside the ERP core while remaining tightly connected to enterprise data. The Germany enterprise content management (ECM) market is therefore shifting from repository-led buying toward process-led buying without reducing the need for compliant archiving.

ELO ECM Suite 25 strengthened this direction in 2025 through broader low-code workflow tools and AI-assisted task handling. Document management continues to lead because compliance starts with capture, retention, and retrieval. The structured e-invoicing requirement widened the need for reliable archiving across firms of different sizes, especially among organizations that had not formalized document controls before 2025. Records management and case management are also benefiting as organizations tighten audit trails across finance, public administration, and regulated services. Web content management and digital asset management remain smaller parts of the Germany enterprise content management (ECM) market, but they are gaining attention where multi-channel publishing and content consistency matter.

By Deployment Mode: Cloud Leads In Both Scale And Forward Momentum

Cloud held a 73.41% share of the Germany enterprise content management (ECM) market in 2025 and is projected to grow at a 13.24% CAGR through 2031. This makes cloud both the largest and the fastest-moving deployment path in the Germany enterprise content management (ECM) market. The result suggests that a large part of new demand is entering through subscription delivery, prebuilt services, and easier rollout models. It also shows that buyers want content platforms that can support e-invoicing, search, and workflow without long local infrastructure projects. For many mid-sized firms, cloud delivery reduces the up-front burden of deployment and ongoing maintenance.

On-premises deployment still retains a meaningful base because many German enterprises continue to run core ERP environments locally. The DSAG Investment Report 2026 showed on-premises S/4HANA use at 56% across DACH, which supports continued demand for locally aligned archiving and controlled repository models. Hybrid architecture remains important because it lets firms keep sensitive records in tightly governed environments while using cloud layers for workflow and collaboration. Gaia-X has also added weight to sovereignty-led cloud design choices, especially when public-sector and regulated procurement standards are involved. That balance means the Germany enterprise content management (ECM) market is likely to stay mixed in architecture even as cloud keeps extending its lead.

By Enterprise Size: SME Adoption Broadens While Large Enterprises Anchor Revenue

Large enterprises held 63.28% of Germany enterprise content management (ECM) market share in 2025, while SMEs are projected to expand at a 12.49% CAGR through 2031. Large organizations still dominate spending because they manage complex content estates across multiple functions, legal entities, and regulated workflows. Their deployments are usually tied to ERP, CRM, and sector-specific systems, which makes replacement slow and vendor relationships sticky. The Germany enterprise content management (ECM) market continues to draw steady large-enterprise demand from manufacturers, financial institutions, and national service organizations that cannot tolerate process gaps in archiving or records access. These buyers also place more weight on certified integration, governance controls, and long-term product support.

SMEs are growing faster because the structured invoicing mandate pushed many smaller firms to move beyond informal file storage and manual archiving. For this group, the first purchase often starts with document capture and invoice handling, then expands into workflow, approvals, and records control. Cloud delivery is especially important here because it lowers infrastructure needs and speeds implementation. The DSAG finding that SAP integration sits at the top of investment priorities also matters for larger SMEs that already operate around SAP environments and now want cleaner content connectivity. As a result, the Germany enterprise content management (ECM) market is adding new buyer groups at the same time that its biggest accounts continue to deepen platform use.

By End-User Industry: BFSI Holds The Lead While Healthcare Expands The Fastest

BFSI accounted for 24.53% share of the Germany enterprise content management (ECM) market in 2025, while healthcare is projected to grow at a 12.91% CAGR through 2031. BFSI remains the largest user group because banks, insurers, and investment firms operate under dense documentation and audit requirements. They need controlled content environments for customer files, advisory records, underwriting material, and compliance reviews. Frankfurt gives this segment extra weight because the region is home to financial institutions, supervisory oversight, and data governance requirements. The Germany enterprise content management (ECM) market therefore keeps a strong BFSI spending base even as other verticals accelerate.

Healthcare is expanding faster because digital health policy is now creating direct content infrastructure demand across providers. Germany launched the electronic patient record on Jan 15, 2025, under an opt-out model, which highlighted the need for structured content handling across practices, hospitals, and pharmacies. The Federal Ministry of Health’s 2026 strategy also set the goal of transmitting 100% of medical reports electronically between providers by the end of 2027. The draft GeDIG law adds further support by expanding the role of interoperable digital health data in system access and exchange. This leaves healthcare as one of the clearest forward growth paths in the Germany enterprise content management (ECM) market.

Geography Analysis

The Germany enterprise content management (ECM) market does not revolve around one internal geography, and demand follows the country’s main economic clusters instead. Bayern remains one of the strongest spending regions because Munich supports large automotive, aerospace, and advanced technology operations with heavy document and workflow requirements. Baden-Württemberg also contributes strong demand through precision machinery and industrial manufacturing, where content control supports engineering records, supplier files, and quality documentation. North Rhine-Westphalia adds another large demand pool through its mix of retail, logistics, energy, and professional services buyers. The continued presence of on-premises S/4HANA across DACH supports the view that manufacturing-heavy regions still need hybrid or locally aligned ECM architectures.

Hessen, led by Frankfurt, is the most regulation-driven sub-market inside the Germany enterprise content management (ECM) market. Financial institutions there face strong demand for records management, case handling, and auditable archiving due to high compliance exposure and recurring renewal cycles. Data residency and operational control carry extra weight in this region because buyers are more sensitive to provider location and cloud governance. The DIHK survey result on dependence on non-EU cloud and AI providers helps explain why sovereignty remains central in Frankfurt-led procurement. OpenText’s sovereign cloud, which is set to move in 2026, directly addresses this need by offering cloud options better aligned with EU data control expectations.

Berlin serves as the primary hub for public-sector ECM modernization because federal ministry programs, eAkte work, and digital administration projects are concentrated there. SAP’s Sep 2025 sovereign OpenAI for Germany announcement reinforced Berlin’s relevance for future public sector records and workflow programs. Hamburg continues to matter through trade and logistics activity, where contract handling and the exchange of supply chain documents support steady demand. Public sector procurement standards became more formal with the OZSV regulation, which took effect on Oct 1, 2025, and this provides a clearer compliance floor for document and records platforms across federal, state, and municipal bodies.

Competitive Landscape

he Germany enterprise content management (ECM) market shows moderate concentration at the upper end, with global enterprise software groups competing alongside established German specialists. OpenText, Microsoft, IBM, SAP, and Oracle remain important in large accounts because they bring scale, enterprise relationships, and broad integration capability. ELO Digital Office, DocuWare, and Doxis continue to hold strong relevance in the mid-market through their local implementation depth and familiarity with German compliance requirements. SAP ecosystem positioning remains one of the main competitive filters because many industrial buyers want content tools that fit cleanly into broader ERP modernization programs. OpenText strengthened its competitive standing in Nov 2025 when it became the first SAP Solution Extensions document management platform certified for SAP S/4HANA Cloud Public Edition.

Sovereign cloud capability is becoming another clear differentiator in the Germany enterprise content management (ECM) market. OpenText’s Apr 2026 partnership with S3NS showed that vendors are investing directly in European cloud control models rather than relying only on general cloud positioning. ELO also advanced its product position in 2025 by adding AI assistance and stronger workflow tooling to ELO ECM Suite 25. SAP widened the competitive context in Sep 2025 with its sovereign OpenAI for Germany initiative, which more closely linked public-sector workflow modernization to its ecosystem. These moves show that product depth alone is no longer enough, and vendors now need a stronger position in compliance, architecture, and ecosystem access.

White space remains visible in the Mittelstand, where many firms still need practical workflow automation built on compliant document control. Public sector and healthcare also remain open areas because buyers there require both data sovereignty and operational simplicity. The lower tier of the Germany enterprise content management (ECM) market stays actively contested because buyers can still choose among several local and global options. No single vendor appears to dominate the field, which keeps competitive pressure balanced across price, functionality, and implementation trust.

Germany Enterprise Content Management (ECM) Industry Leaders

OpenText Corporation

Hyland Software, Inc.

SERgroup Holding International GmbH

Microsoft Corporation

M-Files Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: OpenText announced a strategic partnership with S3NS, a Thales and Google Cloud alliance, to deliver European sovereign cloud content management. The offering includes OpenText Content Management and Documentum on a dedicated private cloud, and OpenText Core Archive for SAP Solutions as a sovereign SaaS with EU data residency, supporting GDPR and SecNumCloud 3.2 compliance.

- November 2025: OpenText received certification for its Core Content Management for SAP solutions as an SAP Solution Extensions partner for SAP S/4HANA Cloud Public Edition, qualifying it as the first document management platform for the GROW with SAP program, a certification with direct commercial relevance to Germany’s large SAP-dependent enterprise base.

- September 2025: SAP SE and OpenAI jointly announced "OpenAI for Germany," a sovereign AI partnership targeting German public sector records management and administrative workflow automation, planned for 2026 launch via SAP’s Delos Cloud on Microsoft Azure. SAP concurrently announced plans to expand Delos Cloud infrastructure to 4,000 GPUs and a commitment of over EUR 20 billion (USD 21.6 billion) to strengthen Europe’s digital sovereignty.

- August 2025: ELO Digital Office released ELO ECM Suite 25, introducing an AI-powered ELO Assistant supporting user-deployed LLMs and integrated AI providers, alongside a low-code workflow engine with expanded SAP, Microsoft 365, and Salesforce integration. The release marked ELO’s broadest AI feature expansion to date, developed from its AI hub in Saarbrücken, Germany, and available across cloud, hybrid, and on-premises environments.

Germany Enterprise Content Management (ECM) Market Report Scope

The Germany Enterprise Content Management (ECM) Market Report is Segmented by Solution Type (Document Management, Records Management, Workflow and Business Process Management, Case Management, Digital Asset Management, Web Content Management, and Other Solutions), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), and End-User Industry (BFSI, Government and Public Sector, Healthcare, IT and Telecommunications, Manufacturing, Retail, Media and Entertainment, Education, Energy and Utilities, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

The Germany enterprise content management (ECM) market refers to the ecosystem of software solutions and services designed to systematically capture, manage, store, preserve, and deliver an organization's unstructured and structured content and documents within the country. This includes technologies such as document management, records management, workflow, business process management, case management, digital asset management, and web content management. Deployed on-premises, in the cloud, or in hybrid models, these solutions cater to organizations of all sizes across diverse industries in Germany, including BFSI, government, healthcare, IT, and manufacturing. Driven by the country's advanced Industry 4.0 initiatives, a strong focus on operational efficiency, and the critical need to comply with stringent European data protection and privacy regulations (such as the GDPR), ECM solutions enable German businesses to streamline complex administrative workflows, enhance cross-departmental collaboration, ensure strict information governance, and transition from legacy paper-based systems to secure, digitized operations.

| Document Management |

| Records Management |

| Workflow and Business Process Management |

| Case Management |

| Digital Asset Management |

| Web Content Management |

| Other Solutions |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Government and Public Sector |

| Healthcare |

| IT and Telecommunications |

| Manufacturing |

| Retail |

| Media and Entertainment |

| Education |

| Energy and Utilities |

| Other End-User Industries |

| By Solution Type | Document Management |

| Records Management | |

| Workflow and Business Process Management | |

| Case Management | |

| Digital Asset Management | |

| Web Content Management | |

| Other Solutions | |

| By Deployment Mode | On-Premises |

| Cloud | |

| Hybrid | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-User Industry | BFSI |

| Government and Public Sector | |

| Healthcare | |

| IT and Telecommunications | |

| Manufacturing | |

| Retail | |

| Media and Entertainment | |

| Education | |

| Energy and Utilities | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Germany enterprise content management (ECM) space?

It was valued at USD 2.03 billion in 2025 and is projected to reach USD 3.98 billion by 2031 at a 10.28% CAGR from 2026 to 2031.

Which deployment model leads adoption in Germany?

Cloud leads adoption with a 73.41% share in 2025 and is also projected to post the fastest growth at a 13.24% CAGR through 2031.

Why are German companies investing more in content management platforms?

Compliance requirements, structured e-invoicing, SAP modernization, AI-enabled automation, and data governance needs are the main forces behind spending.

Which business segment grows the fastest by enterprise size?

SMEs are projected to grow the fastest at a 12.49% CAGR because the e-invoicing mandate is pushing smaller firms toward formal document and workflow systems.

Which end-user group is the largest and which one is growing the fastest?

BFSI held the largest share at 24.53% in 2025, while healthcare is projected to grow the fastest at a 12.91% CAGR through 2031.

What is shaping vendor competition in Germany the most?

Certified SAP integration, sovereign cloud readiness, local compliance depth, and practical workflow automation are shaping competition more than basic document storage alone.

Page last updated on: