Germany Cutting Machine and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

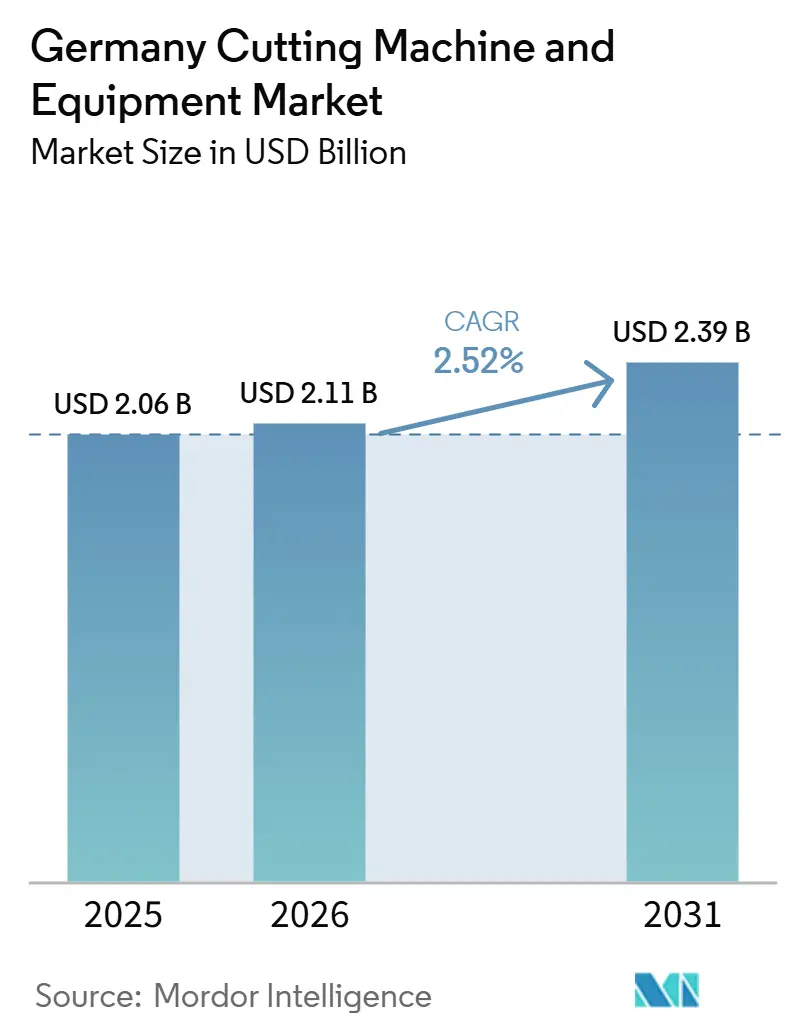

| Base Year Market Size (2025) | USD 2.06 Billion |

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 2.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Cutting Machine and Equipment Market Analysis by Mordor Intelligence

The Germany Cutting Machine and Equipment Market size is projected to be USD 2.06 billion in 2025, USD 2.11 billion in 2026, and reach USD 2.39 billion by 2031, growing at a CAGR of 2.52% from 2026 to 2031.

The Germany cutting machine and equipment market is entering a replacement cycle in which buyers are favoring automation-ready, digitally connected systems over older, standalone units, even when the initial cost is higher. This shift is supported by Germany’s broad manufacturing base, which spans automotive structures, aerospace parts, electrical enclosures, and heavy plate fabrication. It gives the Germany cutting machine and equipment market a more balanced demand profile than many neighboring industrial markets. Public spending on defense, infrastructure, climate measures, and digitalization is also beginning to redirect procurement toward precision-fabrication systems, especially for applications tied to armored structures, aerospace components, and public investment programs. At the same time, weaker industrial production and delayed investment plans among automotive suppliers are limiting short-term purchasing momentum, keeping the Germany cutting machine and equipment market on a moderate growth trajectory. Vendors are responding by placing greater emphasis on software, energy efficiency, and service contracts, gradually shifting competition in the Germany cutting machine and equipment market away from price alone.

Key Report Takeaways

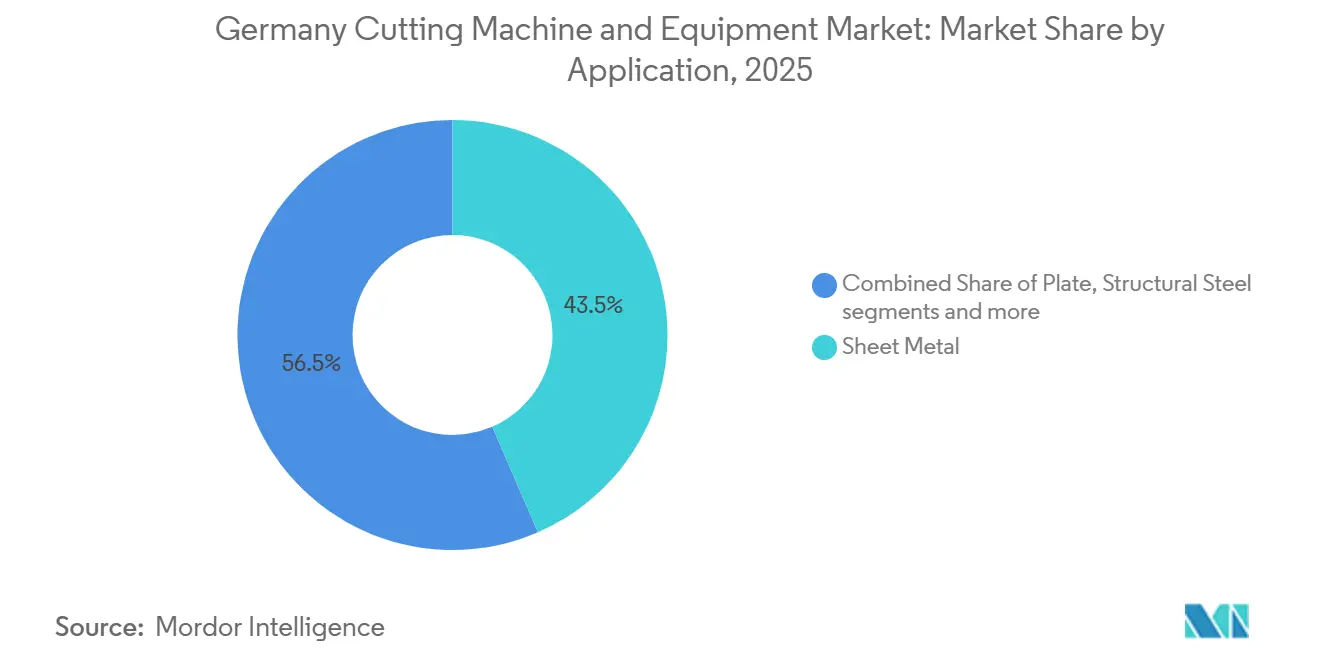

- By application, sheet metal held 43.5% share in 2025, while tube and pipe is projected to grow at a 3.1% CAGR during 2026-2031.

- By technology, laser accounted for 50.2% of the Germany cutting machine and equipment market share in 2025 and is also set to record the fastest growth at a 3.7% CAGR during 2026-2031.

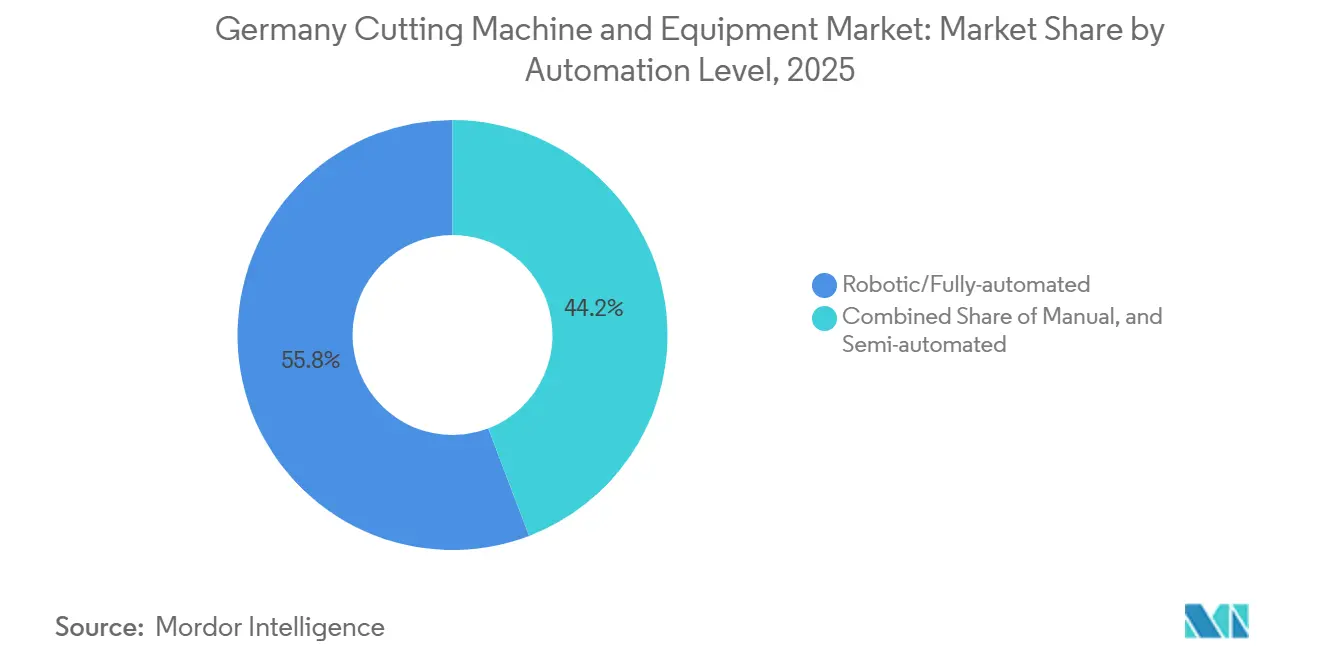

- By automation level, the robotic/fully automated segment captured 55.8% share of the Germany cutting machine and equipment market size in 2025 and is projected to expand at a 3.8% CAGR during 2026-2031.

- By end-user industry, automotive led with a 28.6% share in 2025, while aerospace and defense are forecast to advance at a 3.6% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Cutting Machine and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Industry 4.0 and Factory Automation | +0.7% | National, with a concentration in Baden-Württemberg and Bavaria | Medium term (2-4 years) |

| Rising Demand for High-Precision Laser Cutting Systems | +0.6% | National, strongest in automotive and electronics clusters | Short term (≤ 2 years) |

| Strong Automotive and Industrial Machinery Manufacturing Base | +0.5% | National, with early gains in Stuttgart, Munich, and Wolfsburg corridors | Medium term (2-4 years) |

| Expansion of Aerospace, Defense, and Engineering Applications | +0.4% | National, with concentrations in Munich, Hamburg, and Bremen | Long term (≥ 4 years) |

| Increasing Investment in Advanced Metal Processing Technologies | +0.3% | National, with spill-over to Central and Eastern Germany | Medium term (2-4 years) |

| Focus on Energy-Efficient and Sustainable Manufacturing | +0.2% | National, with early compliance gains in energy-intensive Länder | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Industry 4.0 and Factory Automation

The Germany cutting machine and equipment market is benefiting from a clear shift from pilot-stage digitalization to plant-level automation in production environments. A German Machinery and Plant Manufacturers Association survey in 2026 showed that more than 80% of German mechanical engineering companies viewed AI as increasingly important, and close to one-third had already begun using AI in live production, supporting demand for cutting systems with adaptive controls and connected monitoring. The same body of research also pointed to a significant retraining push across the engineering workforce, which improves factories' practical readiness to adopt more advanced cutting platforms. In the Germany cutting machine and equipment market, this matters because connected cutting cells shorten the economic case for replacing legacy systems when utilization is high. Buyers are also under greater pressure to install equipment that aligns with automated line layouts, remote monitoring protocols, and modern safety configurations. That combination is making automation a purchasing requirement in many projects rather than an optional upgrade.

Rising Demand for High-Precision Laser Cutting Systems

Stricter quality requirements in metalworking and fabrication are also driving the Germany cutting machine and equipment market. Research reported in 2025 found that laser-based manufacturing can increase production throughput by up to 30% compared with conventional methods in demanding aerospace and automotive applications, supporting the broader use of precision cutting systems. Premium suppliers have continued investing heavily in research and development, indicating they still see strong product development value in higher-efficiency fiber laser systems and automated nozzle management. A 2025 approval for laser cutting of armor-grade ballistic steel at a German facility also showed that laser processing is moving into more tightly certified defense applications. In the Germany cutting machine and equipment market, this raises the commercial value of higher precision, process stability, and traceable cutting quality. It also speeds up the replacement of lower-tolerance plasma and flame systems in customer groups where edge quality and repeatability now matter more than simple cutting speed.

Strong Automotive and Industrial Machinery Manufacturing Base

The Germany cutting machine and equipment market still rests on the depth of the country’s automotive and machinery manufacturing base. Industry reports stated that in 2025, Germany remained the world’s second-largest electric vehicle production location after China, and German OEMs registered more than 1.5 million electric cars in the EU, as per Germany Trade & Invest (GTAI). Industry sources also reported major commitments to research and development and plant conversion during 2026-2030, which supports ongoing demand for modern fabrication systems. In the Germany cutting machine and equipment market, the shift to electric vehicle platforms increases the need for tighter cutting quality for thin aluminum, boron steel, and battery enclosure components. Official production data also showed a month-on-month rise in machinery and equipment manufacturing output in March 2025, indicating that industrial demand was not moving down evenly across all manufacturing categories. These conditions continue to give advanced cutting vendors a large installed base to target when investment programs reopen.

Expansion of Aerospace, Defense, and Engineering Applications

The Germany cutting machine and equipment market is seeing a meaningful shift in demand from the aerospace, defense, and engineering sectors. Germany’s 2026 defense appropriation was significantly higher than the prior year's level. That level of spending is broadening procurement for armor plate, structural aerospace panels, and other fabricated parts that require precise metal cutting. The Germany cutting machine and equipment market is therefore supported by demand that is less tied to near-term commercial returns and more tied to national capability and program execution. Small and medium enterprises that previously supplied automotive and general engineering work are also starting to reposition toward defense-linked projects. This expands the potential buyer base for equipment capable of processing ballistic steel, titanium, and other harder materials under tighter qualification rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Labor and Manufacturing Operating Costs | -0.8% | National, with a more severe impact in Western Germany | Short term (≤ 2 years) |

| Elevated Cost of Advanced Cutting Equipment | -0.6% | National, with a stronger impact on SME-dominated regions | Medium term (2-4 years) |

| Shortage of Skilled Technical Workforce | -0.5% | National, critical in machinery and automotive hubs | Long term (≥ 4 years) |

| Economic Slowdown Affecting Industrial Investments | -0.4% | National, with cross-sector spill-over effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Labor and Manufacturing Operating Costs

The Germany cutting machine and equipment market faces direct pressure from high labor costs, social charges, and general operating expenses. VDMA data referenced in 2025 showed that employment in Germany’s machinery and equipment sector fell by 2.4% to nearly 1 million workers by September 2025, reflecting a structural cost problem rather than only a short-term demand decline. VDA also reported in 2026 that 64% of automotive suppliers reduced German headcount during 2025, and 87% cited weak location competitiveness as a major or very major cause. In the Germany cutting machine and equipment market, this reduces the capital budget available for replacement projects and extends approval timelines. Companies that still need new equipment are placing greater weight on systems that reduce labor hours, scrap, and energy intensity over the full operating life. This is why even modest purchasing activity is shifting toward higher-productivity platforms rather than simple low-cost substitutions.

Elevated Cost of Advanced Cutting Equipment

The high upfront cost of advanced fiber laser and robotic cutting systems also constrains the Germany cutting machine and equipment market. The financial burden of high capital expenditure is strongest among small and medium-sized fabrication companies that need long utilization runs and stable order visibility before they can finance a new machine purchase. In practice, this is creating a split market in which larger OEM-linked manufacturers continue to adopt next-generation equipment, while a broad mid-tier delays purchases and keeps older plasma or lower-power laser units in service for longer. New environmental management expectations tied to the implementation of the revised Industrial Emissions Directive in Germany from 2026 add further indirect compliance costs for operators already facing high procurement costs. In the Germany cutting machine and equipment market, this means technology adoption is continuing, but unevenly across customer groups. The result is slower market expansion, even when the technical case for newer equipment is clear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Sheet Metal Anchors Demand While Tube and Pipe Expand Faster

Sheet metal accounted for 43.5% of the market in 2025, making it the largest application segment in the Germany cutting machine and equipment market. Its leading position reflects steady demand from automotive body structures, electrical enclosures, HVAC parts, and general fabricated metal products. This segment benefits from a wide installed base of flat sheet cutting systems across Germany’s major manufacturing regions. It also remains the most established use case for high-throughput laser cutting lines in industrial production. The scale of replacement demand keeps sheet metal at the center of equipment spending even when new capacity additions remain selective.

Tube and pipe is the fastest-growing application segment and is projected to expand at a 3.1% CAGR during 2026-2031. Growth is supported by rising demand for fabrication in renewable energy systems, defense hardware, and industrial heat exchanger production. Compared with sheet metal, this segment is starting from a smaller base, but its use cases are broadening across profile-intensive manufacturing. The shift toward structural tube assemblies and hollow-section components is also improving demand for higher-precision cutting systems. As a result, the Germany cutting machine and equipment market is expected to retain sheet metal as the volume anchor, while tube and pipe delivers stronger growth momentum through the forecast period.

By Technology: Laser Leads While Other Processes Hold Specialized Roles

Laser technology held 50.2% share in 2025, making it the largest technology segment in the Germany cutting machine and equipment market. This leadership is reflected in its wide use across sheet metal, tube, plate, and precision component applications. Laser systems are preferred because they offer high cutting speed, high edge quality, consistent processing, and better compatibility with automated production setups. The segment has also benefited from continued supplier investment in fiber laser efficiency, software integration, and smarter process control. These factors have helped lasers maintain a clear lead over plasma, waterjet, flame, and other specialized technologies.

Laser is also the fastest-growing technology segment, projected to expand at a 3.7% CAGR during 2026-2031. Its growth is supported by replacing older systems with higher-efficiency, digitally integrated platforms. The technology is gaining further ground in applications where tighter tolerances, lower scrap, and energy performance matter more in procurement decisions. While plasma and waterjet remain relevant in thicker materials and temperature-sensitive applications, their expansion is expected to remain more limited. This keeps the laser at the center of both the current Germany cutting machine and equipment market share and future growth.

By Automation Level: Robotic Systems Deliver the Fastest Growth

Robotic/fully automated systems accounted for a 55.8% share in 2025, giving them the largest share by automation level in the Germany cutting machine and equipment market. This high share shows that German manufacturers already rely heavily on automated cutting setups in production environments that require repeatability, throughput, and tighter labor control. These systems are especially important in larger plants and advanced fabrication lines where uptime and quality consistency are critical. Their adoption has also been supported by rising labor costs and the need to reduce operator dependence in repetitive production tasks. This gives robotic and fully automated systems a structural advantage over manual and semi-automated alternatives.

Robotic/fully automated systems are also the fastest-growing automation category, with a projected CAGR of 3.8% during 2026-2031. Demand is expected to remain strong as manufacturers continue to raise automation intensity to protect output and improve process stability. Semi-automated systems still serve medium-volume users, but the gap between semi-automated and fully automated solutions is narrowing. Manual systems will remain relevant in maintenance and low-volume custom work, yet their role in mainstream production is likely to decline further. This means the Germany cutting machine and equipment market will continue to move toward more integrated, software-led cutting cells during the forecast period.

By End-User Industry: Automotive Leads While Aerospace and Defense Accelerate

Automotive held 28.6% share in 2025, making it the largest end-user segment in the Germany cutting machine and equipment market. The sector’s leadership reflects its broad use of cutting equipment in body-in-white structures, battery trays, reinforcement parts, chassis components, and safety-critical fabricated assemblies. Automotive also has one of the country’s deepest supplier networks, which supports a large installed base of cutting systems across OEMs and component manufacturers. Even amid mixed investment conditions, the sector remains the single largest source of demand for replacement and process-upgrade spending. This ensures that automotive will continue to shape equipment requirements across a wide range of materials and production standards.

Aerospace and defense is the fastest-growing end-user segment and is projected to expand at a 3.6% CAGR during 2026-2031. This segment is benefiting from stronger demand for precision processing of armor-grade steel, aerospace structures, titanium parts, and other specialized components. Its growth profile is also more durable because procurement is increasingly supported by defense and national capability programs rather than only by short-cycle commercial spending. As the aerospace and defense industry expands, it will add an important second layer of demand alongside automotive in the Germany cutting machine and equipment market. The result is a more balanced end-user mix, with automotive providing scale and aerospace and defense contributing faster growth.

Geography Analysis

Baden-Württemberg, Bavaria, and North Rhine-Westphalia are the main demand centers in the Germany cutting machine and equipment market because they account for a large share of the country’s precision manufacturing base. Baden-Württemberg stands out because it combines TRUMPF’s headquarters with a dense network of automotive and precision-engineering suppliers, which supports higher-intensity demand for fiber lasers and robotic systems. Bavaria adds a different layer of demand in aerospace, semiconductor equipment, and industrial machinery, broadening the regional technology mix across laser, plasma, and ultrasonic processes. Destatis reported that fabricated metal product manufacturing output rose by 3.2% month on month in December 2025, showing that metal processing activity held up better than several other industrial categories.

North Rhine-Westphalia and Lower Saxony form a heavy-industrial corridor within the Germany cutting machine and equipment market, with stronger demand for thick-plate plasma and oxy-fuel systems tied to shipbuilding, structural steel, and energy infrastructure. These regions are likely to benefit from capital flows linked to defense, mobility, climate, and public infrastructure programs, as large industrial projects here tend to quickly translate into fabrication demand. The Germany cutting machine and equipment market also remains closely tied to export-oriented manufacturing, so global trade conditions can influence domestic machine purchases even when local production activity is stable. That dynamic is especially important in Western industrial regions, where fabricated parts are often produced for foreign end markets. As a result, regional demand is shaped by both domestic policy support and the visibility of export orders for export-facing manufacturers.

Thuringia and Saxony are becoming more visible in the Germany cutting machine and equipment market because research institutions and photonics activity are deepening the local precision manufacturing base. Fraunhofer-linked work in Dresden is helping bring newer laser and ultrasonic processing concepts closer to commercial use, which supports future demand for more specialized cutting platforms. Jenoptik’s investment of EUR 100 million (USD 117.6 million) in a new photonics factory in Dresden underscores eastern Germany's growing importance as a high-precision production location. Beyond traditional industrial regions, Germany cutting machine and equipment market demonstrates a geographically diverse industrial base rather than being concentrated solely around automotive clusters. Defense work, energy equipment, and deep-tech manufacturing are driving new replacement and upgrade demand beyond traditional southern strongholds.

Competitive Landscape

The Germany cutting machine and equipment market is moderately concentrated in the premium technology tier, where TRUMPF Group, Bystronic Deutschland, Jenoptik, and DMG MORI hold durable positions through product depth, engineering capability, and installed service presence. Outside that tier, the market is more fragmented, especially across plasma, waterjet, entry-level laser, and specialized application equipment. Suppliers such as Messer Cutting Systems, Kjellberg Finsterwalde, MicroStep Europa, and other European and Asian vendors compete more directly in those categories. In the Germany cutting machine and equipment market, this means pricing pressure is stronger in conventional systems, while premium suppliers defend margins through performance, integration, and lifecycle support.

TRUMPF remains the clearest technology reference point in the Germany cutting machine and equipment market because its FY2024/25 revenue reached EUR 4.3 billion (USD 5.1 billion), and its machine tools division generated EUR 2.4 billion (USD 2.8 billion). In contrast, research and development spending remained at EUR 519 million (USD 610.5 million).[1]TRUMPF Group, “TRUMPF Laser Technology Reduces Manufacturing Costs in Hot Forming,” TRUMPF Newsroom, trumpf.com DMG MORI is strengthening its position through capacity expansion and hybrid process development, including expanding the Stipshausen site and launching the LASERTEC 65 DED hybrid 2nd Generation in 2026.[2]DMG MORI AG, “DMG MORI Celebrates Expansion of Stipshausen Facility – ULTRASONIC Technology Days,” DMG MORI, dmgmori.com Kjellberg is reinforcing its role in digitally enabled plasma cutting through the 2025 iQ-series launch, which added automated torch-head change and digital consumable tracking.[3]Kjellberg Finsterwalde, “Trade Fair Schweißen & Schneiden 2025 – iQ-Series Plasma Cutting Systems,” Kjellberg, kjellberg.de Jenoptik’s Dresden investment and 2026 growth strategy are enhancing its photonics capabilities, particularly in advanced optics and laser technologies that improve the performance and precision of industrial laser cutting systems. These moves show that competition in the Germany cutting machine and equipment market is centered on product development, manufacturing capability, and differentiated applications rather than simple unit expansion.

Strategy in the Germany cutting machine and equipment market is increasingly shaped by three priorities: software-linked service revenue, modular automation, and entry into defense-qualified fabrication work. TRUMPF has also signaled interest in defense-related industrial applications, suggesting that commercial laser expertise is being positioned for dual-use demand. The compliance burden around laser safety and machinery standards gives established domestic vendors an advantage because they already have local certification, service, and installation experience. New entrants can still win business in the Germany cutting machine and equipment market, but they need a stronger local support model than price-led exporters usually provide. An emerging opportunity persists in certified robotic cells for ballistic steel, titanium, and other defense-grade materials, where demand is rising but production-ready offerings remain limited.

Germany Cutting Machine and Equipment Industry Leaders

TRUMPF Group

Messer Cutting Systems GmbH

Kjellberg Finsterwalde Plasma und Maschinen GmbH

DMG MORI AG

Bystronic Deutschland GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: DMG MORI AG expanded its Stipshausen facility by 1,400 square meters to advance research and development capabilities in ULTRASONIC and LASERTEC technologies, and it premiered the ULTRASONIC 80 Precision as a world-first machine at the inaugural ULTRASONIC Technology Days. The expansion reinforces DMG MORI's positioning in multi-process cutting and machining integration for aerospace and hard-material applications.

- January 2026: DMG MORI unveiled the LASERTEC 65 DED hybrid 2nd Generation, a hybrid manufacturing system that combines laser deposition welding with 5-axis simultaneous milling, enabling the production, repair, and surface enhancement of complex components.

Germany Cutting Machine and Equipment Market Report Scope

The Germany Cutting Machine and Equipment Market Report is Segmented by Application (Sheet Metal, Plate, Tube & Pipe, Structural Steel, and Others), by Technology (Laser, Plasma, Waterjet, and More), by Automation Level (Manual, Semi-Automated, and Robotic/Fully-automated), and by End-User Industry (Automotive, Aerospace & Defense, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Sheet Metal |

| Plate |

| Tube & Pipe |

| Structural Steel |

| Others |

| Laser | Fiber |

| CO2 | |

| Others | |

| Plasma | High-definition |

| Conventional | |

| Waterjet | Abrasive |

| Pure | |

| Flame / Oxy-fuel | |

| Ultrasonic & Emerging |

| Manual |

| Semi-automated |

| Robotic / Fully-automated |

| Automotive |

| Aerospace & Defense |

| Electrical & Electronics |

| Construction & Infrastructure |

| Metal-Fabrication Job Shops |

| Shipbuilding |

| Energy & Power |

| Others (Medical Devices, etc.) |

| By Application | Sheet Metal | |

| Plate | ||

| Tube & Pipe | ||

| Structural Steel | ||

| Others | ||

| By Technology | Laser | Fiber |

| CO2 | ||

| Others | ||

| Plasma | High-definition | |

| Conventional | ||

| Waterjet | Abrasive | |

| Pure | ||

| Flame / Oxy-fuel | ||

| Ultrasonic & Emerging | ||

| By Automation Level | Manual | |

| Semi-automated | ||

| Robotic / Fully-automated | ||

| By End-User Industry | Automotive | |

| Aerospace & Defense | ||

| Electrical & Electronics | ||

| Construction & Infrastructure | ||

| Metal-Fabrication Job Shops | ||

| Shipbuilding | ||

| Energy & Power | ||

| Others (Medical Devices, etc.) | ||

Key Questions Answered in the Report

What is the 2031 outlook for cutting machine and equipment demand in Germany?

The Germany cutting machine and equipment market is projected to reach USD 2.39 billion by 2031, up from USD 2.06 billion in 2026, with a 2.5% CAGR over 2026-2031.

Which technology currently leads equipment demand in Germany?

Laser led the market, accounting for 50.2% of the market value in 2025, supported by its higher efficiency, broader application range, and stronger supplier investment.

Which application is growing the fastest?

Tube and pipe are the fastest-growing applications, with a projected 3.1% CAGR through 2031, supported by demand for renewable energy, defense, and heat exchanger fabrication.

Why does automotive still matter so much for suppliers?

Automotive held 28.6% of end-user demand in 2025 because it uses cutting equipment across body structures, battery trays, chassis parts, and safety components.

What is driving faster growth in aerospace and defense?

Higher defense spending in 2026 and longer program timelines support demand for equipment used in armor, aerospace panels, and other certified precision metal applications.

Are German buyers moving toward more automation?

Yes. Robotic/fully automated systems are projected to grow at a 3.8% CAGR through 2031 as manufacturers try to offset labor costs, raise output, and improve consistency.

Page last updated on: