Germany Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

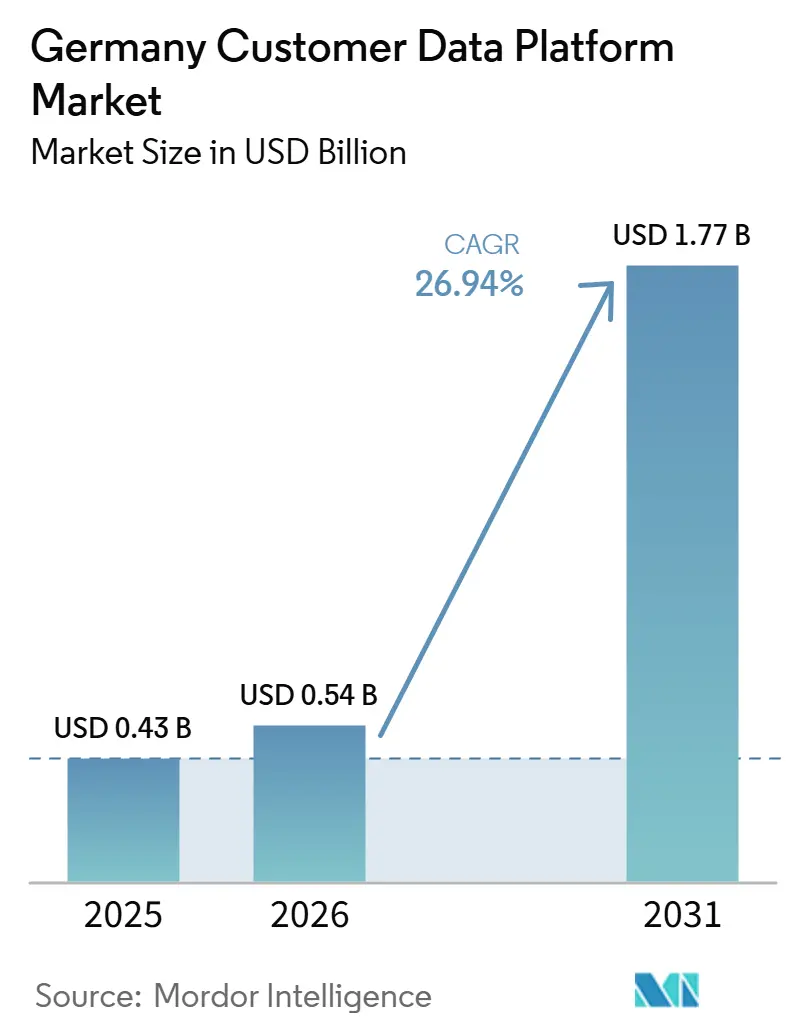

| Base Year Market Size (2025) | USD 0.43 Billion |

| Market Size (2026) | USD 0.54 Billion |

| Market Size (2031) | USD 1.77 Billion |

| Growth Rate (2026 - 2031) | 26.94% CAGR |

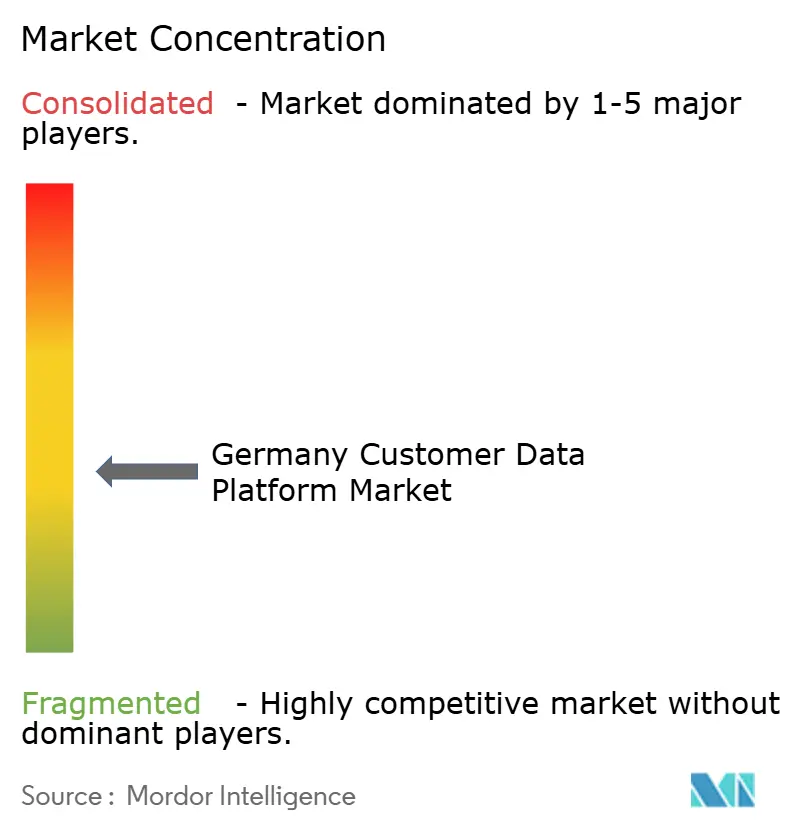

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Customer Data Platform Market Analysis by Mordor Intelligence

The Germany customer data platform market size is projected to expand from USD 0.43 billion in 2025 and USD 0.54 billion in 2026 to USD 1.77 billion by 2031, registering a CAGR of 26.94% between 2026 to 2031. Growth reflects a clear shift from campaign-led data tools toward real-time customer data infrastructure that can support AI use cases while fitting Germany’s strict consent and data governance environment. The market is also being shaped by the need to treat consent handling, data minimization, and auditability as core product requirements instead of add-on compliance features. Demand is further supported by Germany’s industrial and business-to-business base, where enterprises increasingly want to connect machine data, service records, distributor activity, and direct customer interactions in one usable profile. Hybrid deployment momentum and the rapid rise of analytics-led applications show that buyers are not only trying to centralize data, they are also trying to keep sensitive assets under tighter control while improving decision quality. Competition in the Germany customer data platform market, therefore, centers on global software suites, EU-native platforms, and delivery partners, while data residency concerns, legacy integration complexity, and implementation effort continue to influence vendor selection.

Key Report Takeaways

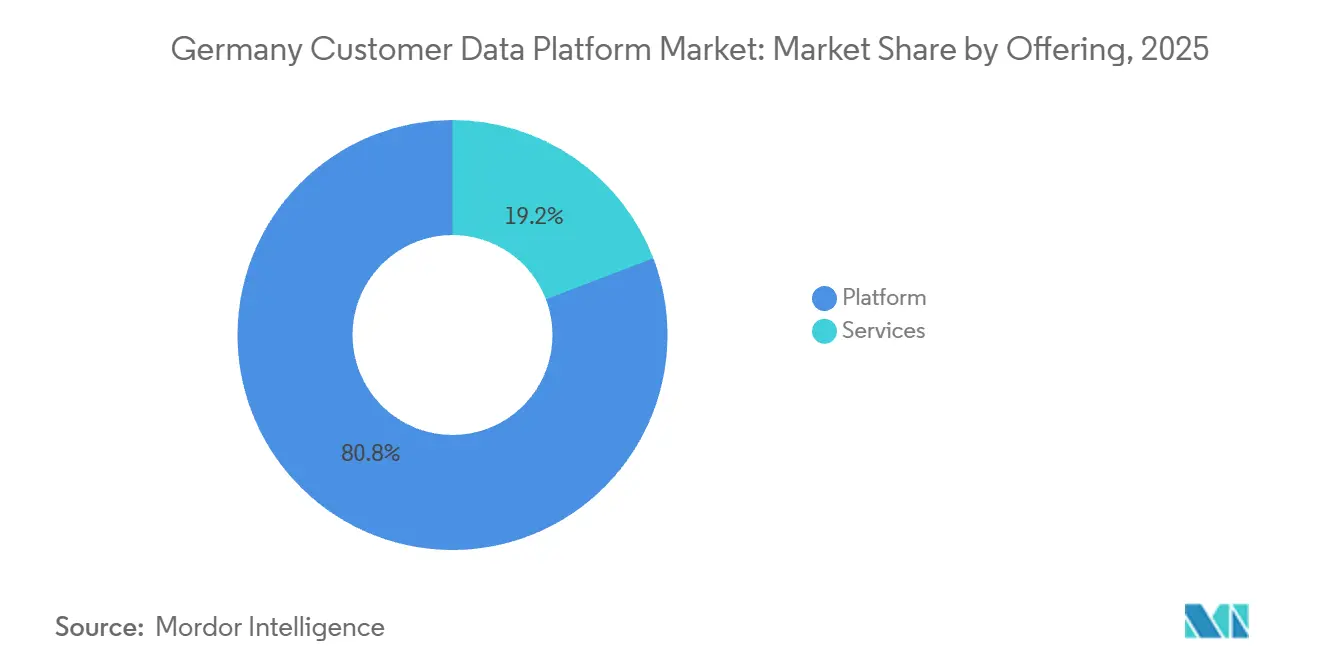

- By offering, Platform led with 80.81% share in 2025, while Services is projected to expand at a 30.58% CAGR through 2031.

- By deployment mode, Cloud accounted for 63.56% of the Germany customer data platform market size in 2025, while Hybrid is projected to record the highest CAGR at 31.76% through 2031.

- By organization size, Large Enterprises held 72.45% of the Germany customer data platform market share in 2025, while SMEs are projected to advance at a 29.84% CAGR through 2031.

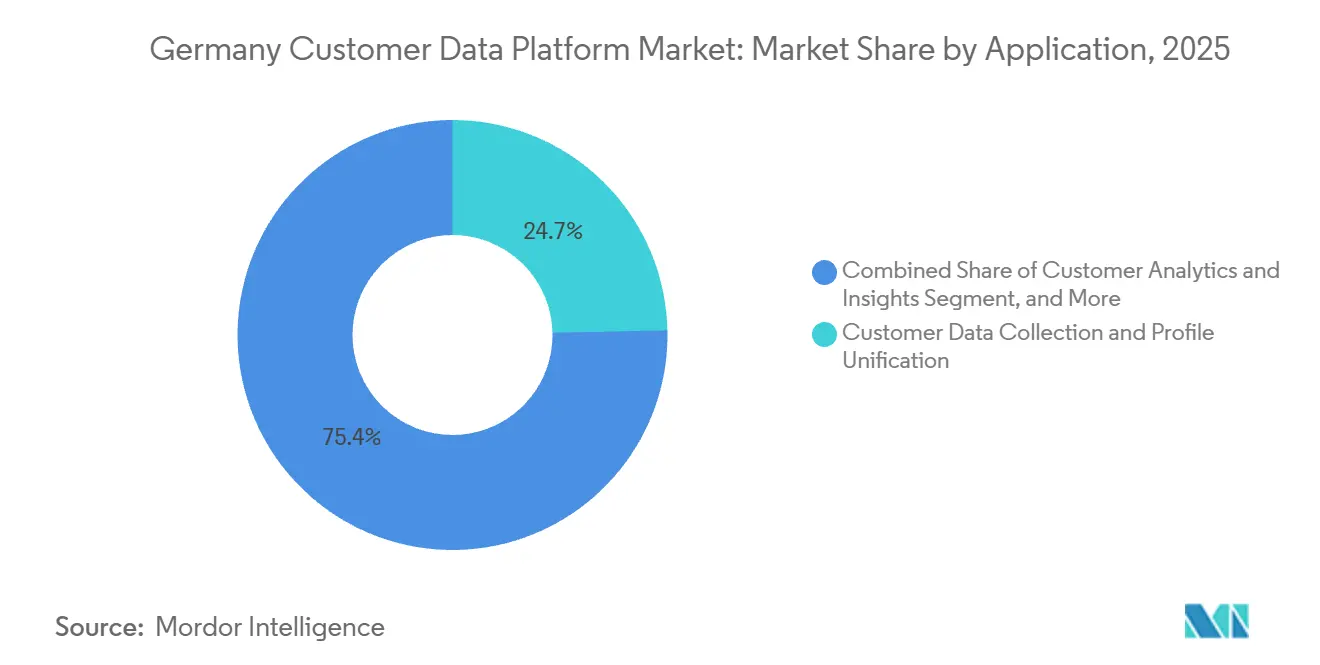

- By application, Customer Data Collection and Profile Unification accounted for 24.65% of the Germany customer data platform market size in 2025, while Customer Analytics and Insights is projected to grow at a 32.25% CAGR through 2031.

- By end-user industry, Industrial Manufacturing led with a 21.25% share in 2025, while Healthcare and Life Sciences is projected to expand at a 33.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Unified First-Party Customer Profiles | +6.4% | Germany, DACH region, Global | Short term (≤ 2 years) |

| AI-Enabled Identity Resolution and Next-Best-Action Orchestration | +5.7% | Global, particularly Germany and DACH | Medium term (2-4 years) |

| Real-Time Personalization Across Regulated Channels | +4.8% | Germany, EU-wide | Short term (≤ 2 years) |

| Consent-Centric Measurement and Server-Side Tracking Migration | +3.4% | Germany, EU | Short term (≤ 2 years) |

| Retail Media and Omnichannel Activation Expansion | +3.0% | Germany, Western Europe | Medium term (2-4 years) |

| Data Warehouse Native CDP Adoption in Mid-Market Germany | +2.9% | Germany-specific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Need for Unified First-Party Customer Profiles

The move away from third-party tracking has made first-party profile building a central investment theme in the Germany customer data platform market. German enterprises are using CDPs to combine web, mobile, store, CRM, and service identifiers into a single customer record that can be activated with better control over consent and purpose limits. This matters because fragmented customer files create weak audience logic, duplicate outreach, and poor measurement across channels. Deloitte’s work for REWE showed that a production CDP can process large data volumes in real time and support AI-driven personalization across customer segments across multiple countries from one platform. The same need is visible beyond retail, where German companies want a cleaner way to connect transactional, behavioral, and service data before they add more advanced activation layers. As a result, unified profiles have become the base requirement for new programs in the Germany customer data platform market rather than a later-stage enhancement.

AI-Enabled Identity Resolution and Next-Best-Action Orchestration

AI-enabled identity work is changing how buyers define value in the Germany customer data platform market. The discussion is moving from passive storage toward systems that can connect profiles, score behavior, and support immediate action in a governed way. Salesforce and Google Cloud expanded their integration in April 2026 so AI agents can execute workflows across Salesforce Data Cloud and Google Cloud with zero-copy data access, which shows how unified data and AI execution are being tied more closely together.[1]Salesforce, “Salesforce and Google Cloud Launch New Integrations,” Salesforce, salesforce.com Adobe also repositioned its customer experience stack in April 2026 around Engagement Intelligence, expanded Real-Time CDP collaboration, and agentic workflows, which reflects the same move toward action on top of unified profiles. In Germany, this shift is especially important because buyers need identity logic that works under tighter consent controls and stronger expectations around data governance. That is why AI-led orchestration is supporting expansion in the Germany customer data platform market, but only when it is built on profiles that are already trusted and usable.

Real-Time Personalization Across Regulated Channels

Real-time personalization has become a practical growth driver in the Germany customer data platform market because enterprises want event-based customer engagement instead of scheduled batch campaigns. In Germany, this only works well when consent state and behavioral data are handled together at the moment of activation. IBM iX’s work for METRO used Adobe CDP and Journey Optimizer to support precise real-time campaign personalization across multiple countries from one central platform, while still adapting execution to each market’s consent state. That example shows why legacy personalization stacks are losing ground when they cannot process customer context and permissions in the same operational flow. Adobe’s broader CX Enterprise launch in 2026 also reinforced how the Germany customer data platform market is moving toward decisioning, collaboration, and orchestrated customer journeys rather than simple audience storage. Vendors that treat consent as a native profile attribute are therefore better placed to win new mandates in the Germany customer data platform market.

Consent-Centric Measurement and Server-Side Tracking Migration

Measurement architecture is also being rebuilt in the Germany customer data platform market as enterprises respond to tighter privacy expectations and weaker browser-side signal quality. The practical answer has been a stronger move toward first-party collection paths, governed data routing, and server-side event handling. Tealium’s 2026 product releases, including AI at the Edge, AI Decisioning, and a Snowflake Native App for governance inside customer-controlled environments, illustrate how vendors are bringing control, decisioning, and activation closer to the enterprise data layer. This shift matters because better-controlled event collection can improve data quality while reducing dependence on less reliable client-side mechanisms. It also supports the broader preference in the Germany customer data platform market for architectures that help brands make more of the consented audience they already have. Over time, that makes consent-centric measurement a structural support for platform demand rather than a narrow compliance project.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR, TTDSG, and Consent Management Complexity | -4.1% | Germany (most stringent enforcement in EU), EU-wide | Long term (≥ 4 years) |

| Legacy CRM, ERP, and Marketing Stack Integration Friction | -3.4% | Germany, particularly the Mittelstand | Medium term (2-4 years) |

| High Switching Costs and Implementation Resource Burden | -2.7% | Global | Medium term (2-4 years) |

| Data Residency and Cross-Border Transfer Constraints | -2.0% | Germany, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR, TTDSG, And Consent Management Complexity

Regulatory complexity remains one of the strongest limiting factors for the Germany customer data platform market. Germany applies strict consent expectations, and enterprises must make sure data use rules stay consistent from collection through activation. This creates more engineering work because customer profiles, audience logic, and downstream journeys all need to respect purpose limits and permission status. IBM iX’s METRO deployment highlights this operational reality because personalization was adapted to each market’s consent state rather than treated as a single universal rule set.[2]IBM iX, “Transformation Der Globalen CX, METRO,” IBM iX, ibmix.de The issue is not that German enterprises lack awareness of compliance; the issue is that maintaining consent-aware pipelines across many systems takes time, budget, and specialist support. That burden slows some projects in the Germany customer data platform market, even when the long-term business case remains strong.

Legacy CRM, ERP, And Marketing Stack Integration Friction

Legacy system density is another material restraint on the Germany customer data platform market. Many German enterprises run long-established ERP, CRM, and marketing environments that cannot be replaced quickly, so CDP projects need to fit around them instead of starting from a clean slate. This is especially important in companies with deep SAP estates, where customer data, order data, service records, and workflow logic are spread across multiple enterprise systems. SAP and Google Cloud’s expanded partnership around multi-agent AI in SAP Engagement Cloud shows how vendors are trying to reduce that friction by working within existing enterprise application landscapes instead of forcing parallel environments. For the Germany customer data platform market, integration difficulty does not remove demand, but it does stretch sales cycles, implementation periods, and total ownership costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Dominance Holds While Services Scale with Complexity

Platform held 80.81% of the Germany customer data platform market share in 2025, which shows that software-led data unification remains the main spending center. Buyers still place the highest value on the packaged layer that brings together identity resolution, profile management, segmentation, and activation. That pattern is consistent with the way large German enterprises procure customer data capabilities, because they want a central system of record before they expand into more specialized workflows. Platform demand in the Germany customer data platform market is also reinforced by the need to connect enterprise applications, customer service systems, and digital interaction channels through one operating layer. In practice, this keeps software licenses at the core of total spending even as use cases become more advanced.

Services is projected to grow at a 30.58% CAGR from 2026 to 2031, which makes it the fastest-growing offering in the Germany customer data platform market. That pace reflects the reality that German deployments often need systems integration, governance design, managed operations, and ongoing optimization after the initial installation. Adobe expanded its partner ecosystem in April 2026 with Accenture, Capgemini, Deloitte Digital, EY, IBM, and PwC to co-develop CX Enterprise solutions, which aligns closely with this services-led buying pattern. As a result, competition in the Germany customer data platform market is no longer centered only on software features, because delivery capability and implementation depth now influence vendor selection more directly. The services layer should therefore keep gaining weight as buyers move from installation toward governance, AI activation, and ongoing operating support.

By Deployment Mode: Cloud Leadership Continues as Hybrid Accelerates

Cloud accounted for 63.56% of the Germany customer data platform market size in 2025, which confirms that scalable software-as-a-service deployment remains the preferred starting point for many buyers. The appeal is straightforward because cloud models offer faster setup, simpler upgrades, and easier access to new decisioning and AI features. This is particularly relevant in the Germany customer data platform market, where vendors need to keep adding controls, governance functions, and orchestration tools without forcing long upgrade cycles. At the same time, on-premises deployments still matter in highly regulated environments where buyers want the strictest possible control over sensitive data. That mixed demand structure explains why cloud remains the largest mode even though it is no longer the only architecture buyers consider.

Hybrid is projected to expand at a 31.76% CAGR through 2031, which makes it the fastest-growing deployment model in the Germany customer data platform market. Buyers increasingly want to keep sensitive data assets inside their own environments while still using cloud-based activation, decisioning, and AI services. Tealium’s May 2026 Snowflake Native App, which allows audience building and governance inside a customer-controlled Snowflake environment, reflects the kind of deployment logic now gaining traction in the Germany customer data platform market. Hybrid growth therefore comes from a practical balance between sovereignty and agility, not from a rejection of cloud itself. This keeps the Germany customer data platform market on a path where architecture choice is increasingly tied to governance needs and existing data estate design.

By Organization Size: Large Enterprises Lead While SMEs Catch Up

Large Enterprises held 72.45% of the Germany customer data platform market share in 2025, which shows how strongly spending is concentrated in companies with bigger budgets, larger data volumes, and more mature technology teams. These buyers usually have enough internal capacity to connect a CDP to multiple transactional, service, and engagement systems. They also tend to have existing relationships with broad enterprise software vendors, which lowers adoption friction in the Germany customer data platform market. This gives SAP, Salesforce, and Adobe a strong position in large-account sales where CDP adoption can be bundled into wider platform expansion. As long as complex integration and governance requirements remain high, large enterprises should stay the biggest revenue pool in the Germany customer data platform market.

SMEs are projected to grow at a 29.84% CAGR through 2031, which marks them as the next major expansion pocket in the Germany customer data platform market. Growth in this group is being supported by simpler onboarding, more flexible consumption models, and rising digital activity among mid-sized businesses. The opportunity is real, but SME demand in the Germany customer data platform market requires different execution, including easier connectors, German-language support, and more direct compliance templates. Vendors that only shrink an enterprise product without changing implementation effort are likely to struggle in this part of the market. The Germany customer data platform industry therefore faces a clear product design split between large-enterprise depth and mid-market usability.

By Application: Unification Leads Today While Analytics Gains Speed

Customer Data Collection and Profile Unification accounted for 24.65% of the Germany customer data platform market size in 2025, which confirms that many enterprises are still in the foundational stage of adoption. The first task for many buyers is to consolidate fragmented customer records across marketing, commerce, service, and offline systems. This workload remains central because other use cases in the Germany customer data platform market depend on having a clean, persistent profile that can be trusted across teams. Audience segmentation, personalization, and campaign orchestration build on that base, which is why they remain important second-layer applications. Consent and preference management has also become a more visible workload in Germany because buyers want permission logic to sit directly inside profile and activation design.

Customer Analytics and Insights is forecast to grow at a 32.25% CAGR through 2031, which makes it the fastest-rising application in the Germany customer data platform market. Buyers increasingly want predictive scoring, next-best-action logic, churn modeling, and lifetime value analysis on top of the same unified profiles used for activation. Tealium’s June 2026 Context API, which connects historical warehouse data with real-time customer context for AI agents and applications, directly reflects this shift toward more analytical and AI-led use cases. That progression means the Germany customer data platform market is moving from data collection into decision support without abandoning its original unification role. The Germany customer data platform industry is therefore becoming more intelligence-led, even while profile building remains the core operational base.

By End-User Industry: Manufacturing Leads While Healthcare Expands Fastest

Industrial Manufacturing held a 21.25% share in 2025, making it the largest end-user segment in the Germany customer data platform market. This pattern stands out because many customer data platform markets are led by retail or digital-first service sectors, while Germany’s structure reflects its industrial economy. Manufacturers are using CDPs to connect distributor activity, direct customer interactions, service records, and equipment-related information into more usable commercial profiles. That gives the Germany customer data platform market a stronger business-to-business flavor than in many peer markets. Retail and e-commerce, along with BFSI, remain important demand centers, but manufacturing still anchors overall spending because of its scale and data complexity.

Healthcare and Life Sciences is projected to grow at a 33.18% CAGR through 2031, which makes it the fastest-growing vertical in the Germany customer data platform market. Growth in this segment reflects rising interest in more connected patient, provider, and engagement data environments that can support better journey management and communication. Germany’s Manufacturing-X initiative also matters here because it shows broader federal support for interoperable and sovereign data ecosystems across complex industries.[3]German Federal Ministry for Economic Affairs, “Manufacturing-X, Wie Das Datenökosystem Für Eine Intelligent Vernetzte Industrie Zur Digitalen Souveränität Beiträgt,” Bundesministerium für Wirtschaft und Energie, bundeswirtschaftsministerium.de While Manufacturing-X is centered on industrial supply chains, it reinforces the wider direction of the Germany customer data platform market toward orchestrated first-party data use within trusted operating frameworks. That keeps healthcare growth aligned with the same governance and interoperability priorities that are shaping the rest of the market.

Geography Analysis

Germany represented the full revenue base of the Germany customer data platform market in 2025, and its domestic demand reflects the country’s position as the largest economy in the European Union. The market’s geographic importance is not only a function of scale, because Germany also sets a demanding standard for privacy, consent, and enterprise integration. This makes the Germany customer data platform market a reference point for wider DACH deployments, where buyers often look for models that can be adapted across neighboring markets. In effect, vendors that can satisfy German requirements improve their credibility across other regulated European environments as well.

A key geographic advantage for the Germany customer data platform market is the country’s dense enterprise and cloud infrastructure base. Germany combines large industrial users, major retail and service groups, and deep software ecosystems, which creates a broad customer pool for CDP vendors. The country also benefits from the presence of SAP, whose enterprise footprint gives the Germany customer data platform market a strong domestic platform anchor. SAP and Google Cloud’s April 2026 partnership around multi-agent AI within SAP Engagement Cloud shows how local enterprise relationships can be extended into newer customer data and orchestration layers. [4]SAP, “SAP and Google Cloud Partnership to Deploy Multi-Agent AI,” SAP News Center, news.sap.com This matters geographically because buyers in Germany often prefer solutions that can fit established enterprise landscapes instead of requiring a full rebuild.

The sovereignty discussion remains especially important in the Germany customer data platform market. Buyers continue to favor architectures that let them keep tighter control over sensitive customer data while still accessing modern activation and AI capabilities. That is one reason hybrid and warehouse-centered designs are gaining ground in the Germany customer data platform market, especially where regulated data and cross-functional usage have to coexist. Tealium’s Snowflake Native App and Context API releases both point to this design preference by keeping governance and context closer to the customer-controlled data environment. Over the forecast period, Germany should remain one of the clearest examples of how privacy expectations, enterprise depth, and deployment architecture combine to shape CDP demand in Europe.

Competitive Landscape

The Germany customer data platform market is moderately fragmented at the vendor level, but major enterprise contract value is concentrated among a relatively small group of platform providers. Salesforce, Adobe, SAP, and Oracle remain central to large-account competition because they can connect CDP capabilities with broader application suites and enterprise data estates. This gives incumbents an advantage when buyers want customer data functions to fit into existing CRM, commerce, service, and ERP environments. At the same time, the Germany customer data platform market still leaves room for EU-native vendors and composable providers that position themselves around privacy, flexibility, or warehouse-centered design. The result is a market where concentration is visible in top-tier accounts, but specialization remains important across mid-sized and use-case-driven deals.

Strategic moves in 2026 show how quickly competition in the Germany customer data platform market is shifting from basic unification toward AI-led orchestration. Adobe’s CX Enterprise relaunch added expanded Real-Time CDP collaboration, an Engagement Intelligence engine, and agentic workflow support, which broadened its positioning from data management into customer lifecycle orchestration. SAP’s expanded partnership with Google Cloud pushed in the same direction by linking multi-agent AI with SAP Engagement Cloud and the wider SAP CX environment Salesforce also deepened its integration with Google Cloud in April 2026 so AI agents can execute workflows across Salesforce Data Cloud and Google Cloud without heavy data movement, which strengthens its enterprise relevance in the Germany customer data platform market.

Composable and warehouse-native models are the main structural challenge to incumbent suites in the Germany customer data platform market. Tealium’s May and June 2026 launches, including AI Decisioning, a Snowflake Native App, and Context API, show how vendors are competing by keeping more control in customer-managed data environments while still enabling real-time activation and AI use cases. Bloomreach’s June 2026 role as a launch partner for Databricks CustomerLake also points in the same direction, because it links Loomi AI to unified profiles in a warehouse-native setting that suits sovereignty-conscious buyers.[5]Bloomreach, “Bloomreach Deepens Partnership With Databricks,” Bloomreach, bloomreach.com Competition in the Germany customer data platform market is therefore broadening from platform breadth alone toward a more complex mix of ecosystem fit, governance design, AI execution, and deployment control.

Germany Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Bloomreach announced its role as a launch partner for Databricks CustomerLake, a new agentic CDP built on the Databricks platform. The integration connects Bloomreach's Loomi AI marketing agent directly to unified customer profiles in Databricks, enabling scaled 1:1 personalization across email, web, and messaging without data movement outside the warehouse. This partnership positions Bloomreach for warehouse-native enterprise customers in Germany's data-sovereignty-conscious market.

- June 2026: Tealium launched Context API, extending its Moments API to add a governed context layer that bridges historical warehouse data with real-time customer context for AI agents, applications, and experiences. The launch broadens Tealium's addressable use case from event streaming to enterprise AI orchestration, directly competing with composable CDP frameworks.

- April 2026: Adobe unveiled CX Enterprise at Adobe Summit, rebranding Adobe Experience Cloud with a new agentic AI layer built on open standards, Model Context Protocol, and Agent2Agent. The launch included expanded Real-Time CDP collaboration capabilities, a new Engagement Intelligence decisioning engine, and partnerships with Accenture, Capgemini, Deloitte Digital, EY, IBM, and PwC for co-developed enterprise delivery.

- April 2026: Salesforce and Google Cloud announced expanded integrations enabling AI agents to execute end-to-end workflows across Salesforce Data Cloud and Google Cloud via Agentforce and Gemini Enterprise, including zero-copy data access with Google Lakehouse and IDMC BigQuery connectors available in April 2026.

Germany Customer Data Platform Market Report Scope

The Germany Customer Data Platform (CDP) market comprises software platforms and associated services that collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent, unified customer profiles. These platforms enable organizations to deliver personalized, privacy-compliant, and omnichannel customer experiences through capabilities such as identity resolution, audience segmentation, real-time data activation, customer journey orchestration, analytics, and consent management.

The Germany Customer Data Platform Market Report is Segmented by Offering (Platform, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Platform |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Platform |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for the Germany customer data platform space?

The Germany customer data platform market was valued at USD 0.43 billion in 2025 and is forecast to reach USD 1.77 billion by 2031 at a CAGR of 26.94% during 2026-2031.

Which offering leads spending in Germany customer data platforms?

Platform remained the largest offering with an 80.81% share in 2025, showing that core software for unification, identity, and activation still drives most spending.

Which deployment model is growing fastest in Germany?

Hybrid is the fastest-growing deployment mode with a 31.76% CAGR through 2031, as buyers balance sovereignty needs with cloud-based activation and AI tools.

Which customer data platform application is growing fastest in Germany?

Customer Analytics and Insights is projected to grow at a 32.25% CAGR through 2031, reflecting stronger demand for predictive scoring and AI-based decision support.

Which end-user segment leads demand in Germany?

Industrial Manufacturing led with a 21.25% share in 2025, which reflects Germany’s industrial economy and the value of linking commercial, service, and operational data.

Why are services growing quickly in Germany customer data platforms?

Services is projected to expand at a 30.58% CAGR through 2031 because German deployments often require ongoing integration, governance setup, optimization, and partner support.

Page last updated on: