Germany CRM Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

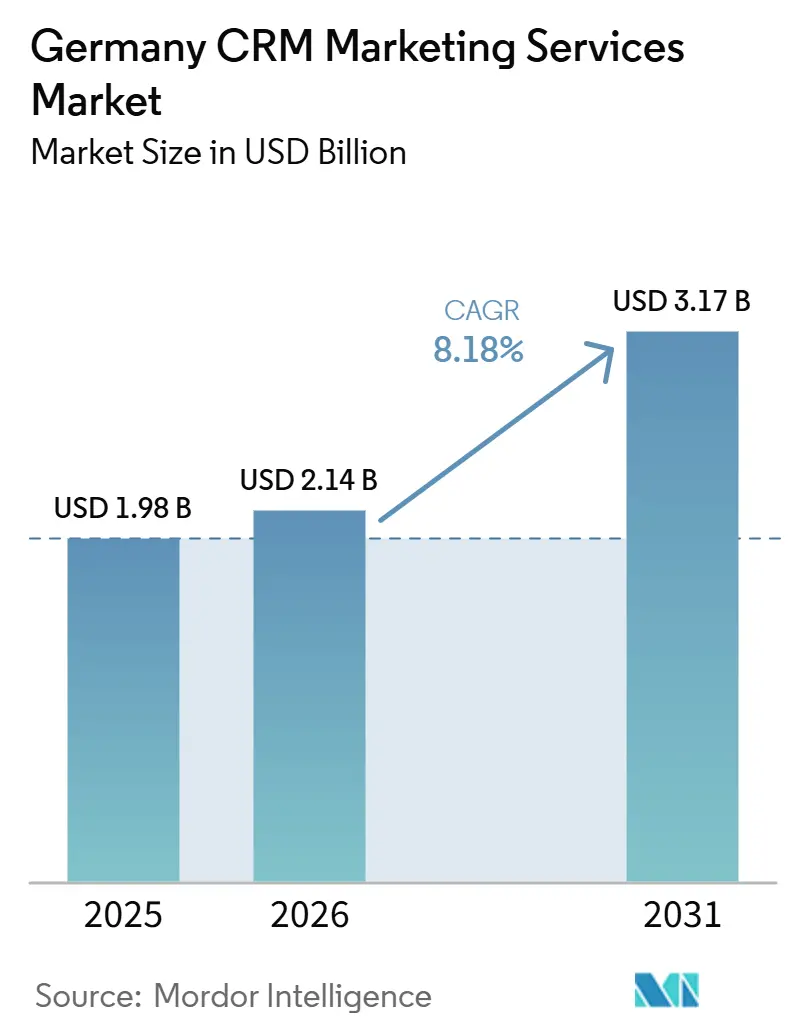

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

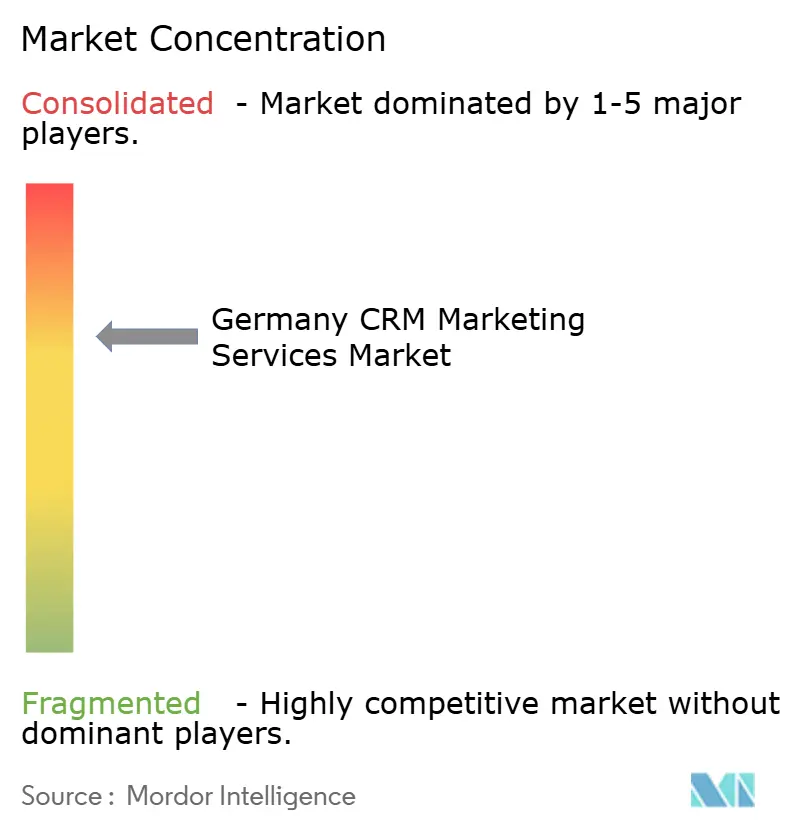

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany CRM Marketing Services Market Analysis by Mordor Intelligence

The Germany CRM marketing services market size is expected to increase from USD 1.98 billion in 2025 to USD 2.14 billion in 2026 and reach USD 3.17 billion by 2031, growing at a CAGR of 8.18% over 2026-2031. The Germany CRM marketing services market is being supported by broad CRM adoption across German companies, even though many users still do not extract full operating value from their existing systems. Demand is also being sustained by Germany's strict privacy and data handling framework, which keeps compliance work tied to CRM programs instead of treating it as a one-time project. The shift of SAP and other cloud CRM environments into a more Mittelstand-accessible model is widening the client base for implementation, migration, and managed support services. Leadership transition across family-owned firms is also pushing customer management from relationship-led practices toward more formal, measurable CRM processes. At the same time, e-invoicing changes, AI governance requirements, and multi-platform integration needs are extending engagement scope and supporting recurring service demand in the Germany CRM marketing services market.

Key Report Takeaways

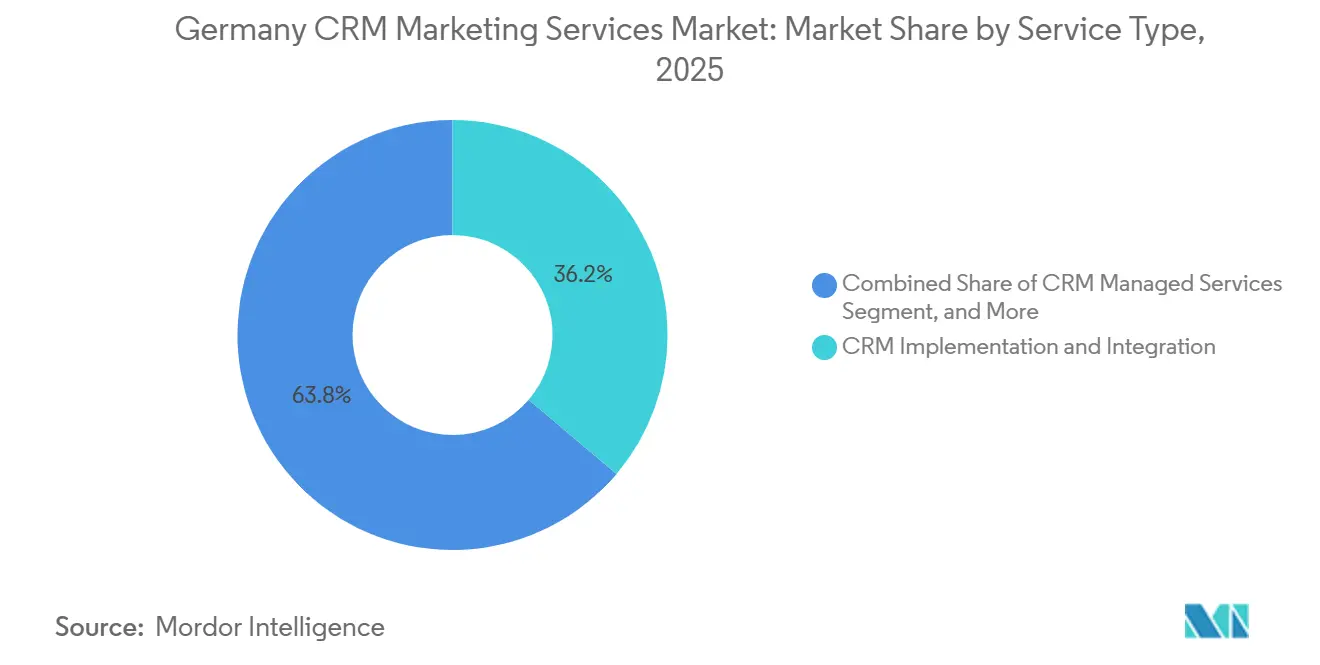

- By service type, CRM implementation and integration led with 36.19% revenue share in 2025, while CRM managed services are projected to expand at an 11.93% CAGR through 2031.

- By enterprise size, large enterprises held 68.49% of the Germany CRM marketing services market share in 2025, while small and medium enterprises are projected to grow at an 11.86% CAGR through 2031.

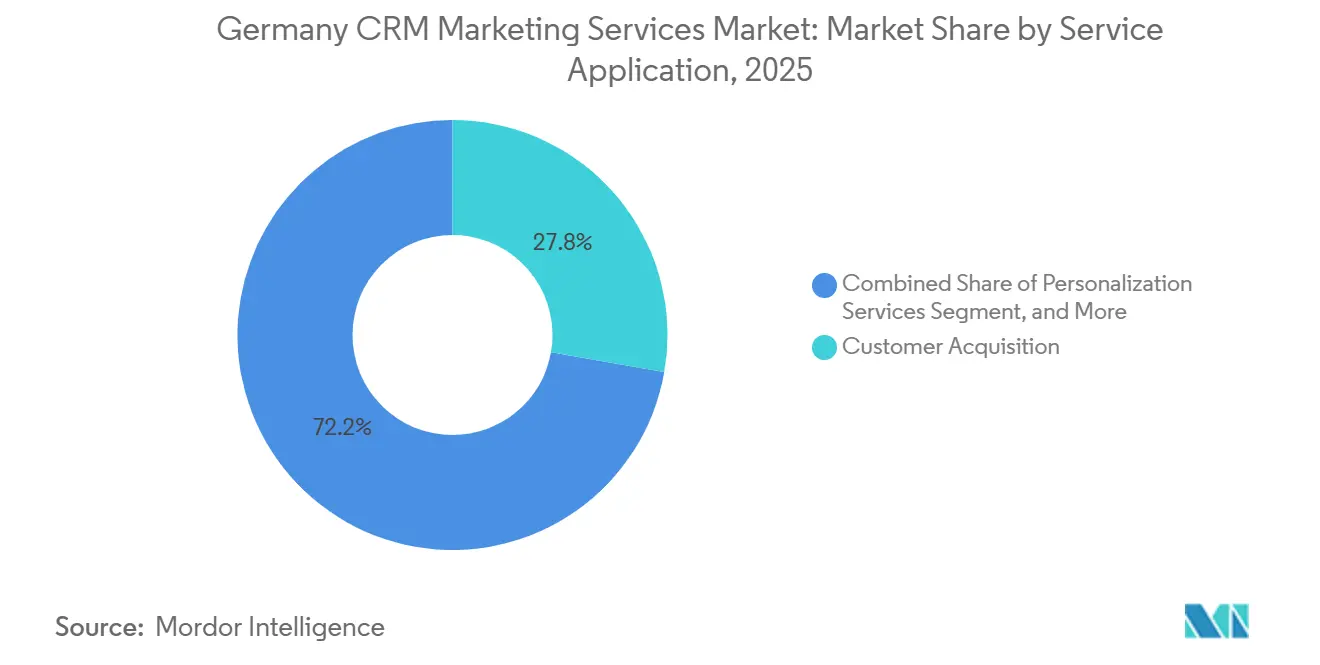

- By service application, customer acquisition accounted for 27.76% share of the Germany CRM marketing services market size in 2025, while customer analytics and insights are projected to expand at a 13.83% CAGR through 2031.

- By end-user industry, BFSI held 22.67% revenue share in 2025, while retail and e-commerce are projected to grow at a 13.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany CRM Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Under-Monetized Mid-Market CRM Modernization Demand | +1.9% | National, with highest density in Baden-Württemberg, Bavaria, and NRW Mittelstand corridors | Long term (≥ 4 years) |

| Rising Demand for Data-Driven Personalization | +1.8% | National, most acute in retail, e-commerce, and BFSI verticals across major German states | Short term (≤ 2 years) |

| Stronger Focus on CRM-to-Marketing Stack Integration | +1.3% | National, led by DAX 40 corporations and large family-owned groups, with spillover to upper Mittelstand | Medium term (2-4 years) |

| Compliance-Led Shift Toward First-Party Data Activation | +1.2% | National, most acute in states with active data protection authorities such as Hamburg, Bavaria, and Berlin | Short term (≤ 2 years) |

| Faster Adoption of AI-Assisted Campaign Orchestration | +0.9% | National, with earlier uptake in technology, financial services, and retail | Medium term (2-4 years) |

| Growth of Cloud-Native Marketing Service Delivery Models | +0.6% | National, with stronger uptake in digital-native SMEs and startups | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Under-Monetized Mid-Market CRM Modernization Demand in Mittelstand Firms

The unmet demand in the Germany CRM marketing services market is deepest in Mittelstand firms, where CRM use is already widespread but full value capture remains limited. Bitkom's 2026 survey said 72% of German companies use CRM marketing tools, but only 8% fully use their CRM system's capabilities, which leaves a large service gap after initial deployment.[1]Bitkom, “Marketing Im Digitalen Wandel 2026,” Absatzwirtschaft, absatzwirtschaft.de That gap keeps advisory, implementation, and managed services commercially relevant even after a company has installed a platform. Leadership transition inside family-owned firms is also moving customer management away from founder-led relationships and toward formal CRM processes. SAP's May 2026 move to extend SAP Commerce Cloud to Mittelstand and growing companies lowers the adoption threshold and widens the serviceable client pool.

Rising Demand for Data-Driven Personalization Across Customer Journeys

The Germany CRM marketing services market is also being supported by rising demand for more consistent personalization across acquisition, service, and loyalty programs. SAP Emarsys reported that true customer loyalty declined by 5 percentage points, while nearly 1 in 3 German customers is lost because of inconsistent customer experiences.[2]SAP SE, “Innovationen Im Bereich SAP Customer Experience Fördern Profitables Wachstum,” SAP News, news.sap.com Salesforce reported that 84% of German marketers still ran generic campaigns even though 75% had adopted AI, which points to configuration and data integration gaps rather than missing software. Bitkom also found that 76% of German enterprises expect marketing automation to become more important by 2027, while 35% cited the lack of an AI strategy as the main internal barrier. These conditions favor providers that can connect customer data, prove campaign attribution, and turn platform features into repeatable operating processes.

Stronger Enterprise Focus on CRM-To-Marketing Stack Integration

Enterprise demand in the Germany CRM marketing services market is rising because CRM platforms need tighter links with ERP, commerce, analytics, and campaign systems. CRM Implementation and Integration accounted for 36.19% of revenue in 2025, which reflects the constant work needed to align customer workflows with complex enterprise stacks. SAP's Q1 2026 customer experience release added AI-assisted segmentation, natural language analytics for SMS campaigns, and deep research tools, which increased the amount of configuration and training work tied to SAP environments. The general availability of SAP Engagement Cloud in Q1 2026 created a new wave of reconfiguration work for German enterprises that already run SAP-centered processes. In Germany, that work usually extends beyond technical deployment because works council consultation can slow projects that introduce AI-enabled CRM functions.

Compliance-Led Shift Toward First-Party Data Activation

Compliance requirements continue to shape the Germany CRM marketing services market because first-party data activation now sits at the center of campaign execution. Germany combines GDPR obligations with the BDSG, works council consultation for AI-related deployments, and e-invoicing-related workflow changes that affect CRM-linked billing and record keeping. The European Data Protection Board said cumulative GDPR penalties had surpassed EUR 5 billion (USD 5.70 billion) in 2025, and its 2026 enforcement focus centered on transparency and information obligations under Articles 12 to 14. That enforcement climate makes consent management, data lineage documentation, and processing record updates part of ongoing CRM service scopes rather than optional add-ons. As third-party tracking becomes less dependable, German enterprises have stronger reasons to rebuild engagement programs around governed first-party CRM data.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Integration Complexity With Legacy ERP and CRM Environments | -1.8% | National, most severe in Baden-Württemberg and NRW where legacy SAP installations are concentrated | Medium term (2-4 years) |

| Persistent Privacy and Consent Management Overhead | -1.2% | National, most acute in Hamburg, Munich, and Berlin where data protection authorities maintain active enforcement | Short term (≤ 2 years) |

| Shortage of Specialized CRM Marketing Talent and Implementation Capacity | -0.9% | National, most acute in Baden-Württemberg, Bavaria, and NRW where demand concentration exceeds local talent supply | Long term (≥ 4 years) |

| Budget Scrutiny on Discretionary Marketing Transformation Spend | -0.7% | National, most pronounced among mid-market Mittelstand firms sensitive to economic conditions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity With Legacy ERP and CRM Environments

Legacy ERP and CRM environments remain a major brake on the Germany CRM marketing services market because many large German firms still run heavily customized systems built over long periods. Integrating CRM marketing workflows with SAP S/4HANA, DATEV connections, and local invoicing rules expands data mapping and middleware work in almost every large deployment. The same complexity increases the risk that implementation goals slip when data models, governance rules, and process ownership are not aligned early. In practice, providers often need longer diagnostic and migration phases before they can move into campaign execution or analytics optimization. When AI features are added, works council consultation can lengthen already complex projects and pressure delivery margins further.

Persistent Privacy and Consent Management Overhead

Privacy and consent management overhead also slows the Germany CRM marketing services market because compliance work must be maintained across every active customer touchpoint. The 2026 EDPB enforcement focus on transparency obligations creates immediate work in consent capture, privacy notice updates, and processing record maintenance across CRM programs. This increases recurring service demand but also adds approval steps, documentation tasks, and testing cycles that slow rollout speed. German buyers are therefore more selective about platform design, data residency, and vendor documentation than many peers in other markets. Providers that cannot show disciplined compliance practices face longer sales cycles and a higher risk of procurement rejection, especially in regulated sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Implementation Scale Anchors Revenue as Managed Services Accelerate

CRM implementation and integration held 36.19% of the Germany CRM marketing services market share in 2025, which made it the revenue anchor for service providers operating in SAP-heavy client environments. That position reflects the recurring need to connect CRM workflows with ERP, commerce, analytics, tax, and invoicing systems before campaigns can scale. SAP's shift toward SAP Engagement Cloud and its Q1 2026 feature releases kept implementation work active because clients needed partner support to reconfigure customer data, orchestration rules, and reporting structures. In the Germany CRM marketing services industry, implementation work still carries strategic weight because it often determines whether later analytics and managed services can perform as promised.

CRM managed services are projected to expand at 11.93% CAGR through 2031, making it the fastest-growing service type in the Germany CRM marketing services market. Mittelstand firms increasingly prefer ongoing support because many lack dedicated CRM operations teams and want predictable delivery after go-live. Training and support remain relevant where providers embed German-language enablement into long-term contracts, which helps improve user adoption and reduces service friction. Basic implementation is becoming more standardized in the SME tier, while differentiation is shifting toward analytics, compliance support, and continuous optimization.[3]HubSpot GmbH, “HubSpot Für Geschäftsführer, CRM Für Den Deutschen Mittelstand,” HubSpot, hubspot.de

By Enterprise Size: Enterprise Accounts Lead While SME Adoption Accelerates

Large enterprises accounted for 68.49% of the Germany CRM marketing services market share in 2025, reflecting the weight of DAX 40 groups, large industrial companies, and major financial institutions. These clients usually run multi-platform environments across marketing, sales, service, and commerce, so service providers capture larger contract values and longer engagement timelines. Enterprise accounts also demand deeper specialization in SAP, Salesforce, governance, and sector-specific compliance, which favors providers with broad delivery benches. In the Germany CRM marketing services industry, large accounts remain the base load for revenue because their harmonization and modernization needs do not end after one deployment cycle.

Small and medium enterprises are projected to grow at 11.86% CAGR from 2026 to 2031, which makes them the fastest-expanding client tier in the Germany CRM marketing services market. Cloud-native platforms, shorter implementation cycles, and standardized service packages have made CRM adoption easier at Mittelstand price points. HubSpot's German-language support model and Frankfurt data residency proposition show why SME demand is moving toward faster deployments with ongoing managed support rather than large custom builds. This shift creates room for regional specialists that can deliver fixed-fee, compliant, and easy-to-manage service models for clients that are too large for self-service and too small for major consultancies.

By Service Application: Acquisition Leads Share While Analytics Delivers the Fastest Growth

Customer acquisition accounted for 27.76% share of the Germany CRM marketing services market size in 2025, which kept it at the center of commercial spending across BFSI, retail, and manufacturing accounts. Many German clients still judge CRM programs by measurable lead generation, pipeline contribution, and new customer conversion rather than by softer brand metrics. SAP Emarsys reported that nearly 1 in 3 German customers is lost because of inconsistent customer experiences, which keeps acquisition spending active as companies replace churned demand with a new pipeline. Providers that can tie acquisition work to clear attribution and channel discipline are better placed to defend premium fees in the Germany CRM marketing services market.

Customer analytics and insights is projected to expand at 13.83% CAGR through 2031, which makes it the fastest-growing application area. SAP's Q1 2026 release added plain-language analytics and AI-assisted segmentation, which increased demand for services that govern data models, configure logic, and translate output into campaign actions. Salesforce reported that only 58% of marketers had access to cross-functional service data in 2025, which shows why analytics work often starts with data readiness before it reaches advanced personalization. As a result, retention, automation, campaign management, omnichannel engagement, and personalization are increasingly sold as connected service layers instead of separate projects.

By End-User Industry: BFSI Anchors Demand While Retail and E-Commerce Expands Faster

BFSI accounted for 22.67% share of the Germany CRM marketing services market size in 2025, which made it the largest end-user segment. German banks, insurers, and asset managers rely on CRM data for compliant personalization, multi-product cross-sell, and retention programs that must work within strict data rules. This keeps demand high for implementation, integration, consent management, and analytics services that can support complex customer journeys without weakening control standards. The segment also gives providers stable account economics because BFSI clients usually retain vendors across strategy, deployment, optimization, and managed support cycles.

Retail and e-commerce is projected to grow at 13.54% CAGR through 2031, which makes it the fastest-expanding vertical in the Germany CRM marketing services market. Large digital merchants and omnichannel retailers need deeper personalization, quicker segmentation, and stronger campaign orchestration as they compete with digital-native peers. Healthcare and Life Sciences, Information Technology and Telecom, Industrial Manufacturing, and Government and Public Administration also add meaningful demand, each with different compliance and workflow needs. Industrial manufacturing is especially important because many German suppliers are moving from dealer or distributor tools toward broader engagement platforms that connect with existing SAP-centered operations.

Geography Analysis

Southern Germany, especially Bavaria and Baden-Württemberg, generates the highest CRM marketing services density in Germany in 2026, which gives this area an outsized role in the Germany CRM marketing services market. The region benefits from the concentration of SAP-linked implementation activity, automotive suppliers, precision manufacturers, and large insurance groups. SAP's headquarters in Walldorf supports a dense ecosystem of certified partners that compete for S/4HANA migration and SAP Engagement Cloud work. Munich adds large BFSI demand because major insurers and financial institutions continue to invest in personalization, loyalty, and cross-sell programs. The same regional mix also helps managed service providers because manufacturing and financial accounts tend to require continuous support after deployment.

North Rhine-Westphalia and the adjacent Hessen corridor generate the largest absolute revenue pool by state scale and client diversity in the Germany CRM marketing services market. Düsseldorf acts as a major delivery base for global agency networks and consulting firms serving retail, consumer goods, and fashion accounts. Frankfurt adds a strong BFSI bias because national banks, international financial institutions, and related data infrastructure are concentrated there. The area's relevance is strengthened by enterprise demand for compliant hosting and integration support, especially where CRM environments must align with strict localization expectations. Bonn and Cologne widen the addressable client base through telecom, retail, and media organizations that need implementation and managed services across multiple customer channels.

Berlin is the fastest-growing geography within the Germany CRM marketing services market because digital-native companies there scale customer data operations faster than the national average. Large e-commerce and platform businesses headquartered in Berlin create strong demand for analytics, personalization, and retainer-based optimization work. Hamburg adds another mature demand pocket through major retail and consumer businesses, while eastern states such as Saxony, Thuringia, and Brandenburg are becoming more relevant as SME digitalization programs advance. Public sector digitalization also supports demand across all German states because citizen engagement and service delivery projects increasingly require sovereign CRM environments and long-term support.

Competitive Landscape

The Germany CRM marketing services market remains moderately concentrated at the top tier, but it is not closed because local compliance credibility and German-language delivery still shape buying decisions as much as scale. SAP-centered implementation capability is the clearest gatekeeper in large enterprise and upper Mittelstand accounts because so many customer workflows remain tied to SAP environments. SAP strengthened that position when SAP Engagement Cloud reached general availability in February 2026 and when it expanded its Google Cloud partnership in June 2026 to push autonomous CX capabilities. Global consultancies and agency groups compete for these accounts, but they still need platform depth, governance fluency, and local delivery capacity to win durable contracts. This keeps the Germany CRM marketing services market competitive among large providers, while still leaving room for specialists that can operate closer to client workflows.

A second layer of competition comes from German IT service firms such as adesso SE, msg systems, Arvato Systems, and T-Systems International, which are better aligned with Mittelstand procurement expectations. These firms benefit when buyers value sovereign delivery models, German documentation, and closer operating support over international brand reach. The white space is strongest in mid-sized accounts that need more than software onboarding but cannot justify the cost structure of a large global consultancy. This is also why product-only CRM vendors sit outside the core competitive set, while implementation-led firms with managed service capability are more relevant comparators in the Germany CRM marketing services market.

Strategic moves in 2026 show that competition is shifting toward AI-enabled execution and first-party data capabilities. Salesforce's agreement to acquire Fin in June 2026 broadened the service scope around autonomous customer agents for partners serving German clients. Publicis moved in May 2026 to acquire LiveRamp, and WPP had already acquired InfoSum in April 2025, both moves aimed at strengthening privacy-safe data collaboration and activation capabilities. Adobe also announced new agentic AI partnerships in June 2026 with Accenture Song, Omnicom, WPP, and Stagwell, which shows how platform vendors are using partner ecosystems to scale campaign orchestration services.[4]Adobe, “Adobe Accelerates Agentic AI Adoption Through New Agency And Technology Partnerships,” Adobe News, news.adobe.com

Germany CRM Marketing Services Industry Leaders

Salesforce, Inc.

SAP SE

Adobe Inc.

HubSpot, Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SAP SE announced an expanded partnership with Google Cloud to elevate SAP Customer Experience with AI-powered autonomous CX capabilities, integrating real-time customer profiles, transaction data, and consented engagement data from SAP CX with Google Cloud's AI agent infrastructure. The partnership positions SAP CX as an agentic CRM platform for German enterprises and creates new implementation and integration services demand for SAP and Google Cloud-certified implementation partners.

- June 2026: Salesforce signed a definitive agreement to acquire Fin, the AI customer agent platform formerly known as Intercom, for USD 3.6 billion, adding packaged autonomous CRM agent capabilities to its Agentforce platform. For Germany, where Salesforce ranked #1 in the WirtschaftsWoche Beste Mittelstandsdienstleister 2026 with 74.6 points, this acquisition directly expands the professional services scope for Salesforce-aligned CRM implementation partners serving the Mittelstand.

- June 2026: Adobe announced new agentic AI adoption partnerships at Cannes Lions with Accenture Song, Omnicom, WPP, and Stagwell, creating implementation architectures for AI-powered campaign orchestration and CRM-integrated customer experience workflows. These agency partnerships accelerate the availability of certified agentic CRM marketing services capabilities in Germany through the major agency networks operating in Düsseldorf, Hamburg, and Munich.

- May 2026: Publicis Groupe announced a definitive agreement to acquire LiveRamp, a global data collaboration platform, for USD 2.2 billion. The acquisition strengthens Publicis's first-party data activation capabilities for its German DAX 40 and consumer goods clients, directly enhancing the CRM marketing services value it can deliver in Germany's first-party data-constrained post-cookie environment.

Germany CRM Marketing Services Market Report Scope

Germany CRM marketing services market refers to the platforms and services that enable businesses in Germany to manage customer relationships and improve marketing operations. The market includes customer data management, campaign automation, analytics, personalization, and omnichannel engagement solutions designed to support Germany’s business environment and comply with strict regulatory frameworks, such as the EU GDPR and the German Federal Data Protection Act (BDSG). Germany’s strong industrial base, advanced digital adoption, and focus on secure, compliant, and AI-powered customer engagement strategies drive the market.

Germany CRM Marketing Services Market Report is Segmented by Service Type (CRM Strategy and Consulting, CRM Implementation and Integration, CRM Migration and Modernization, CRM Managed Services, and CRM Training and Support), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Service Application (Customer Acquisition, Customer Retention and Loyalty, Campaign Management Services, Marketing Automation Services, Customer Analytics and Insights, Omnichannel Customer Engagement, and Personalization Services), and End-user Industry (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Administration, and Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| CRM Strategy and Consulting |

| CRM Implementation and Integration |

| CRM Migration and Modernization |

| CRM Managed Services |

| CRM Training and Support |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Acquisition |

| Customer Retention and Loyalty |

| Campaign Management Services |

| Marketing Automation Services |

| Customer Analytics and Insights |

| Omnichannel Customer Engagement |

| Personalization Services |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-user Industries |

| By Service Type | CRM Strategy and Consulting |

| CRM Implementation and Integration | |

| CRM Migration and Modernization | |

| CRM Managed Services | |

| CRM Training and Support | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Service Application | Customer Acquisition |

| Customer Retention and Loyalty | |

| Campaign Management Services | |

| Marketing Automation Services | |

| Customer Analytics and Insights | |

| Omnichannel Customer Engagement | |

| Personalization Services | |

| By End-user Industry | Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current and future size of the Germany CRM marketing services market?

The Germany CRM marketing services market was valued at USD 1.98 billion in 2025, stands at USD 2.14 billion in 2026, and is forecast to reach USD 3.17 billion by 2031 at an 8.18% CAGR.

Which service type leads revenue and which one is growing fastest in Germany?

CRM Implementation and Integration led with 36.19% share in 2025, while CRM Managed Services is projected to grow fastest at an 11.93% CAGR through 2031.

Why are SMEs becoming more important for service providers in Germany?

SMEs are projected to grow at 11.86% CAGR because cloud-native CRM platforms, shorter deployments, and standardized managed service packages are making adoption easier for Mittelstand firms.

Why does BFSI lead demand while retail and e-commerce grows faster?

BFSI led with 22.67% share in 2025 because of compliance-heavy personalization and cross-sell needs, while retail and e-commerce is growing faster at 13.54% CAGR due to rising demand for analytics and tailored customer engagement.

Which service application is becoming the biggest growth area?

Customer Analytics and Insights is the fastest-growing application at a 13.83% CAGR, showing that clients increasingly want CRM systems to support decision-making, segmentation, and measurable campaign improvement.

Which parts of Germany matter most for providers of CRM marketing services?

Southern Germany has the highest service density because of SAP and manufacturing concentration, NRW and Hessen offer the largest absolute revenue pool, and Berlin is the fastest-growing geography due to digital-native demand.

Page last updated on: