Geosynthetics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

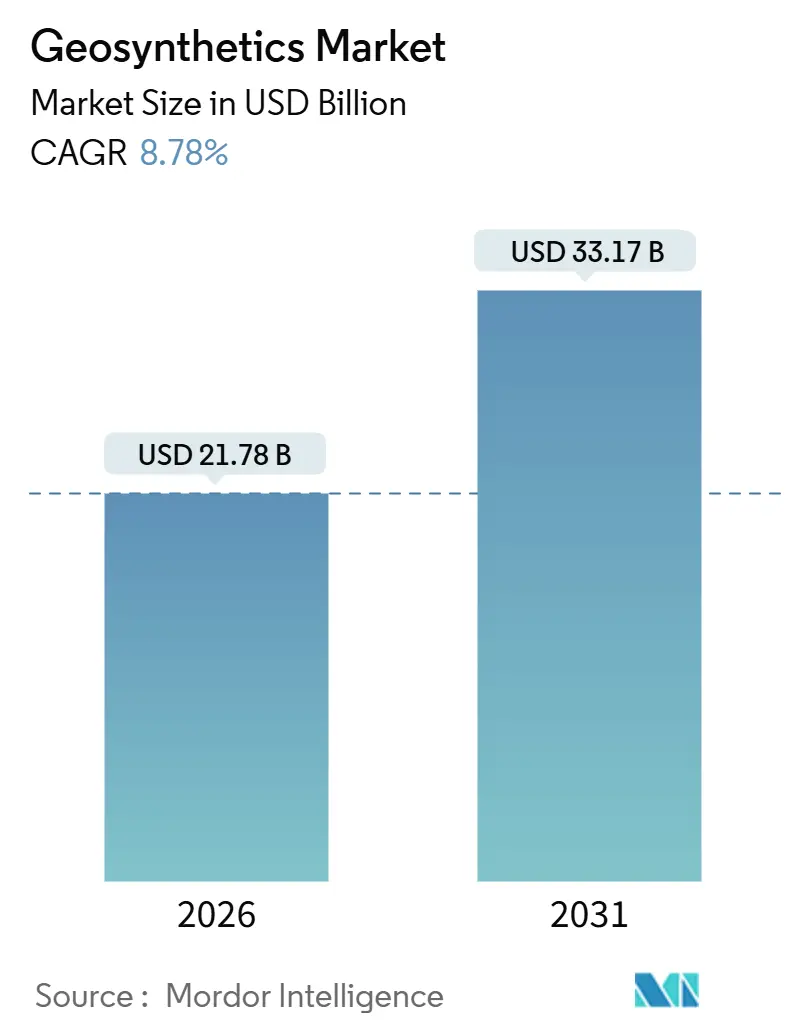

| Market Size (2026) | USD 21.78 Billion |

| Market Size (2031) | USD 33.17 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geosynthetics Market Analysis by Mordor Intelligence

The Geosynthetics Market size is estimated at USD 21.78 billion in 2026, and is expected to reach USD 33.17 billion by 2031, at a CAGR of 8.78% during the forecast period (2026-2031). Uptake is accelerating as public-works agencies in the Asia-Pacific region embed polymer-based soil-stabilization layers into expressway embankments, while landfill-liner mandates in North America and the European Union elevate geomembranes from optional upgrades to baseline compliance items. Geogrids and geotextiles lower earthwork volumes, shorten construction schedules, and reduce lifecycle greenhouse-gas footprints compared with aggregate-intensive designs, drawing the attention of contractors facing labor shortages and carbon-pricing pressures. Smart variants that incorporate fiber-optic strain sensors and RFID tags are also shifting procurement criteria from unit price to long-term monitoring value. Meanwhile, raw-material price volatility and divergent testing standards pose near-term hurdles but have not derailed the structural pivot toward polymer solutions, especially where sovereign infrastructure pipelines remain well funded.

Key Report Takeaways

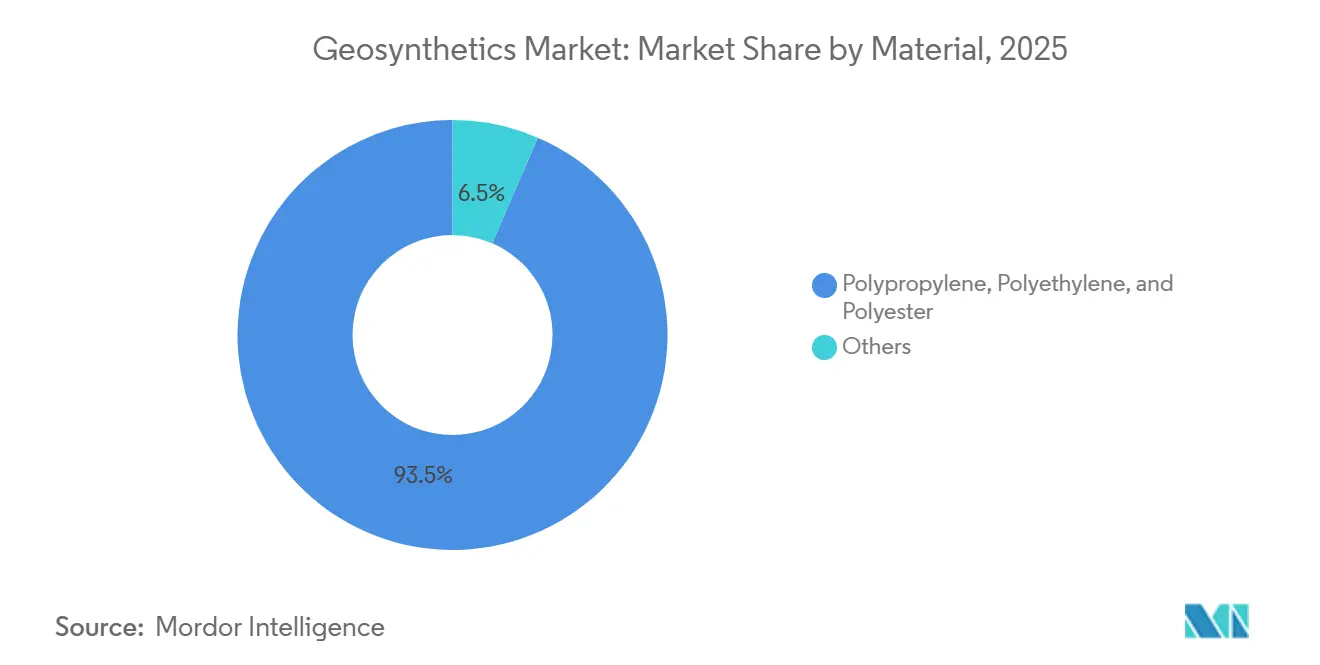

- By material, polypropylene, polyethylene, and polyester held 93.51% of the geosynthetics market share in 2025, and they are forecast to expand at an 8.80% CAGR through 2031.

- By type, geomembranes captured 34.68% of 2025 revenue and are advancing at a 10.15% CAGR, outpacing all other product categories.

- By function, reinforcement retained the largest 2025 share at 31.58%, while containment and barrier applications posted the fastest growth, accelerating at a 9.14% CAGR.

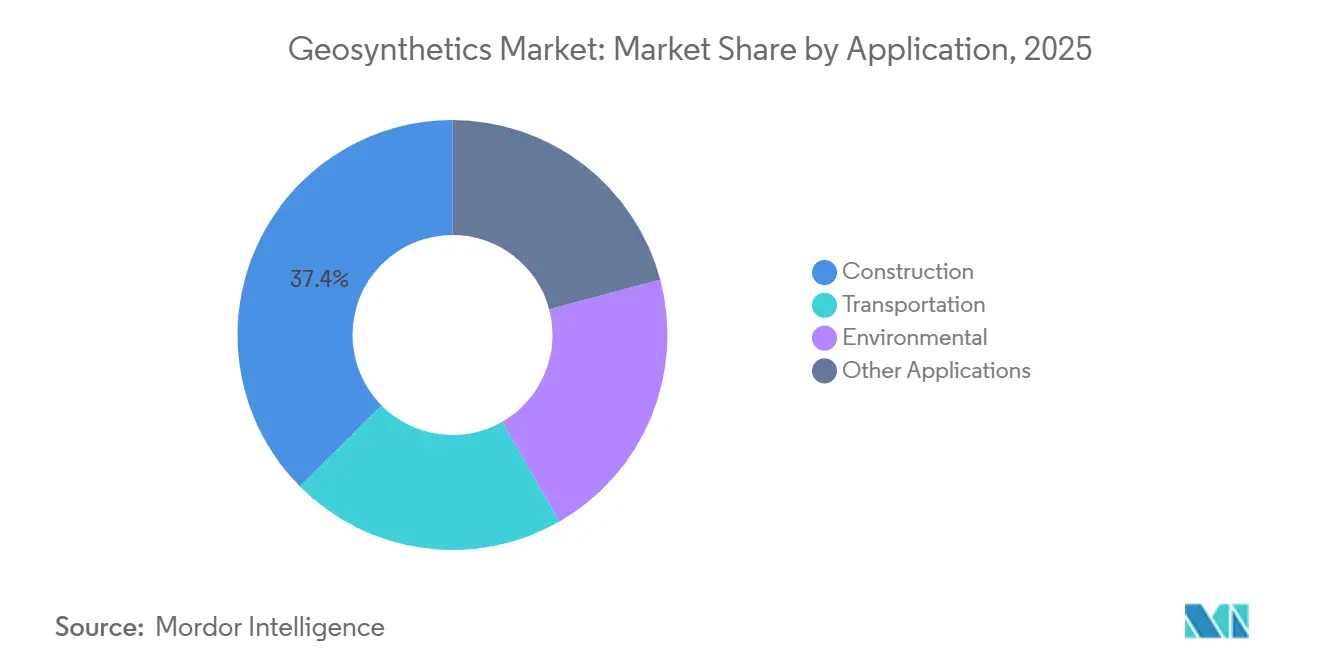

- By application, construction retained the largest 2025 share at 37.44%, and transportation is projected to grow at a 10.46% CAGR through 2031.

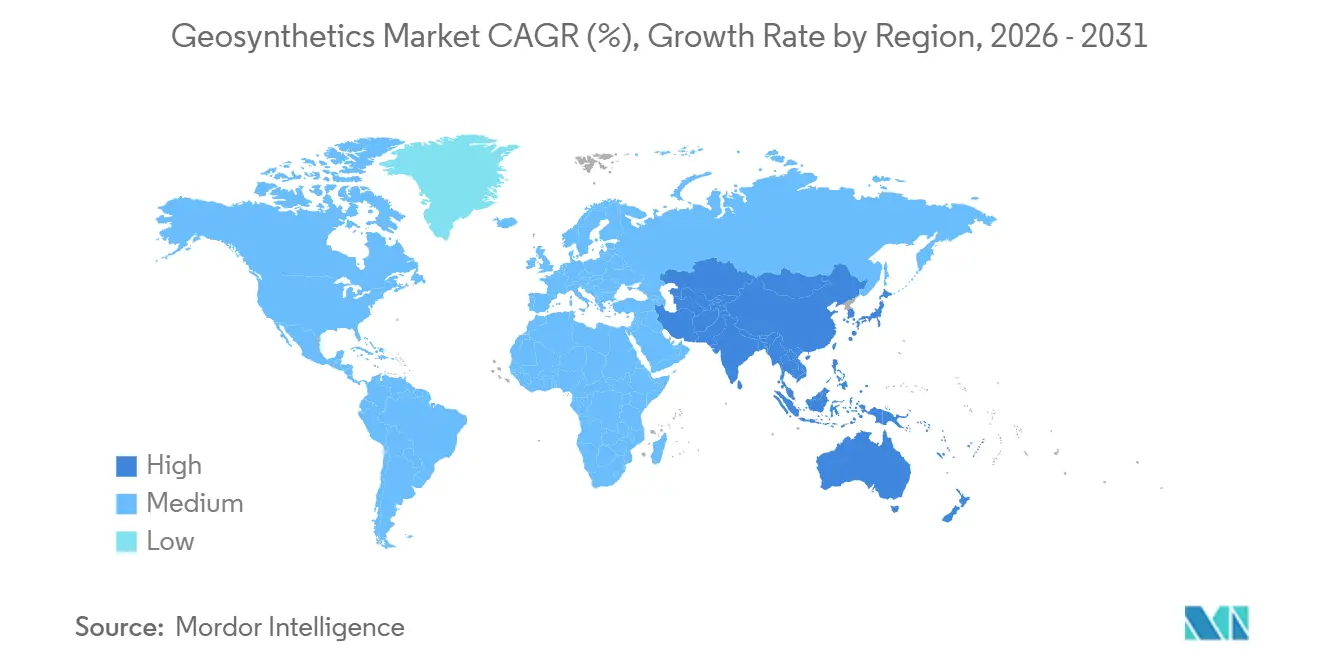

- By geography, Asia-Pacific accounted for 44.36% of 2025 revenue and is projected to maintain a 9.70% CAGR—the fastest regional trajectory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Geosynthetics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-led construction boom | +2.8% | APAC core, spill-over to the Middle East and Latin America | Medium term (2-4 years) |

| Mandatory landfill and wastewater containment | +2.1% | North America and EU, expanding to APAC urban centers | Long term (≥ 4 years) |

| Growth in tailings and heap-leach mining | +1.6% | South America (Chile, Peru, Brazil), Australia, parts of Africa | Medium term (2-4 years) |

| Cost-optimized durability versus traditional materials | +1.4% | Global, with early gains in cost-sensitive APAC and MEA markets | Short term (≤ 2 years) |

| Smart geosynthetics with embedded sensors | +0.9% | North America and EU pilot markets, APAC adoption by 2028 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Construction Boom

Across the Asia-Pacific, sustained public-works spending is increasingly integrating geogrids and geotextiles into highway embankments and rail beds. Under its 14th Five-Year Plan, China earmarked significant funding for transportation infrastructure. Provincial mandates now stipulate geogrid reinforcement for expressways to mitigate post-construction settlement. Meanwhile, India, under its National Infrastructure Pipeline, pledged substantial investments, standardizing geotextile separation layers in upgrades to rural roads. The Asian Development Bank, projecting regional infrastructure needs through 2030, bolsters the long-term outlook for geosynthetics suppliers. Contractors have noted reductions in earthwork volumes by adopting geogrid-reinforced designs, leading to swifter project completions and diminished carbon footprints. Such evident cost and scheduling advantages are propelling polymers into the forefront of civil engineering, expanding the geosynthetics market's scope beyond its traditional erosion-control niche.

Mandatory Landfill and Wastewater Containment

Regulatory tightening has elevated the status of geomembrane liners from optional upgrades to essential compliance mandates. The U.S. Environmental Protection Agency now requires all new municipal solid-waste landfills to implement double-liner systems equipped with leak-detection layers[1]“40 CFR Part 258,” U.S. Environmental Protection Agency, epa.gov. Echoing this move, the European Union's revision of its Landfill Directive has enforced stricter leachate-collection rules, leading to retrofits at older sites. In China, the newly introduced Technical Specification for Geomembrane Liners mandates certified polyethylene liners for both industrial wastewater lagoons and coal-ash impoundments. Given the risk of closure orders for non-compliance, operators' purchasing decisions remain shielded from economic fluctuations. This dynamic has solidified a robust demand for high-density polyethylene geomembranes within the geosynthetics market.

Growth in Tailings and Heap-Leach Mining

Mining regulators are mandating geosynthetic barriers to curb environmental liabilities. Chile’s updated DS 248 rules require geomembrane liners at all new copper tailings facilities. Peru now requires geocomposite drainage layers under heap-leach pads at precious-metal mines. Australia’s 2025 dam-design guidelines recommend geotextile filters in tailings-dam underdrains to reduce piping risk. These measures shift geosynthetics from value-engineering options to permitting prerequisites, expanding the geosynthetics market across South America and Oceania despite commodity-price swings.

Cost-Optimized Durability Versus Traditional Materials

Life-cycle analyses consistently favor polymers over traditional materials like concrete and steel. Geogrid-reinforced retaining walls can cut installed costs compared to cast-in-place concrete, especially for heights below 8 meters. Geotextile-wrapped columns in soft soils offer significant savings in foundation costs. Polyethylene geomembranes, used in landfill applications, not only boast long service lives but also come at a lower installed cost than compacted-clay liners. Such economic benefits are particularly appealing in cost-sensitive emerging markets, ensuring continued adoption even amidst tightening capital budgets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polypropylene and resin pricing | -1.2% | Global, with acute impact on import-dependent markets | Short term (≤ 2 years) |

| Global product-standard disparities | -0.7% | Cross-border procurement in APAC, MEA, and Latin America | Medium term (2-4 years) |

| Microplastic compliance risk | -0.6% | EU and North America, expanding to APAC coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Polypropylene and Resin Pricing

Feedstock fluctuations are squeezing margins and complicating bidding strategies. Polypropylene prices surged significantly by mid-2025. Following suit, polyethylene prices climbed before stabilizing in late 2025. Resin inflation impacted engineered-materials margins in 2025, leading to selective price increases. Meanwhile, smaller fabricators, without hedging strategies, are now incorporating escalation clauses linked to polymer indices. This move shifts price risk back to owners and heightens volatility in the short-term outlook for the geosynthetics market.

Global Product-Standard Disparities

Fragmented supply chains and heightened compliance costs stem from divergent testing protocols. ASTM D4595 calls for a 100-millimeter-wide specimen for tensile testing, while ISO 10319 opts for 200 millimeters, necessitating dual certifications[2]ASTM International, “ASTM D4595,” astm.org. China's GB/T 17643 requires ultrasonic thickness tests for geomembranes, contrasting with Europe's EN 13249, which depends on mechanical calipers. India, in its IS 15351:2024, introduced distinct puncture-resistance thresholds, mandating separate tests for domestic projects. Standard harmonization remains a priority over tariff reduction, highlighting the operational challenges faced by multinational suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polymer Dominance Continues

Polypropylene, polyethylene, and polyester delivered 93.51% of 2025 volume and are forecast to expand at an 8.80% CAGR to 2031, reinforcing their grip on the geosynthetics market. Polypropylene remains the workhorse for geotextiles and geogrids, offering high tensile strength, chemical resistance, and process flexibility that fabricators rely on to meet rigorous transportation-infrastructure specifications. In parallel, high-density polyethylene (HDPE) governs geomembrane production because its low permeability and reliable welding performance satisfy landfill and mining regulators worldwide. Polyester is carving out a share in reinforcement niches requiring low creep and high modulus, illustrated by a capacity boost in Germany in 2025.

Bio-based pathways are gaining experimental traction. Natural fibers such as jute and coir provide biodegradable erosion-control blankets in coastal projects. Sugarcane-based polyethylene offers fossil-free carbon credentials but carries a cost premium and therefore targets projects seeking sustainability certifications. While these niches are too small to dent the dominant polymer share, they illustrate the diversification trend and open an upgrade path as economies put a price on carbon.

By Type: Geomembranes Lead the Growth Curve

Geomembranes accounted for 34.68% of 2025 revenue and continue to outpace other products at a 10.15% CAGR, reflecting escalating liner mandates in waste-management and mining applications. Municipal-solid-waste cells now standardize on HDPE sheets with thicknesses ranging from 1.0 to 2.5 millimeters. In contrast, tailings dams often require sheets up to 3 millimeters thick, with textured surfaces to boost slope friction. The industry's optimistic demand outlook is highlighted by Solmax's ambitious expansion in Quebec, set for 2025.

In highway construction, geotextiles lead in volume, playing crucial roles in separation, filtration, and drainage. Nonwoven needle-punched geotextiles are preferred for their puncture resistance and ability to handle high flow rates. Geocomposites, like Huesker's Fortrac, merge a geogrid with a nonwoven filter. This innovation streamlines the process, allowing for reinforcement and drainage in a single roll, and boasts a faster placement rate on European highways. Specialty products, such as TriAx geogrids with their unique triangular apertures, secured a notable share of North America's mechanically stabilized earth segment in 2025, thanks to their enhanced multi-directional load distribution capabilities.

By Function: Containment Barriers Accelerate

Reinforcement retained the largest 2025 slice at 31.58% as transportation agencies embed geogrids to extend pavement life and minimize settlement in embankments. Yet containment and barrier functions are the fastest climbers, advancing at 9.14% annually because landfill operators and mining firms face strict impermeability thresholds enforced by the U.S. EPA and China’s Ministry of Ecology and Environment. As a result, the geosynthetics market size for containment applications is projected to widen its contribution to overall growth through 2031.

Separation geotextiles prevent intermixing of subgrade and base layers, saving aggregate in weak-soil regions and mitigating scarcity of high-quality rock. Drainage functions benefit from geocomposite cores that offer a higher flow rate of gravel drains in half the depth, an attractive attribute for land-constrained sites. Filtration requirements, codified under ISO 10318, ensure geotextile pore sizes align with soil gradation to avoid clogging. Moisture-barrier roles, though smaller, remain vital in methane-control caps and concrete-slab underlays where vapor migration can undermine structural integrity.

By Application: Transportation Takes the Fast Lane

Construction activities held 37.44% of 2025 revenue as builders used geotextiles to reinforce foundations and slope walls. However, transportation is sprinting ahead at a 10.46% CAGR to 2031, buoyed by sovereign programs that prioritize road, rail, and airport links. By 2027, India will complete geogrid reinforcement on rural roads. In 2025, China introduced geosynthetics in new high-speed rail corridors to address soft-soil settlement issues.

As waste and wastewater standards tighten, lining systems have become essential design components. Europe's 2024 directive mandates retrofits for existing landfills. Niche sectors like agriculture, aquaculture, and coastal defense present growth opportunities. In water-scarce areas, geomembrane canal liners cut irrigation seepage. Meanwhile, geotextile sand tubes offer quick shoreline stabilization, costing significantly less than traditional rock-revetments.

Geography Analysis

Asia-Pacific delivered 44.36% of 2025 revenue and is forecast to post the fastest 9.70% CAGR. This growth is buoyed by China's Belt and Road corridors and India's ambitious pipeline. In Japan, seismic-retrofit guidelines now endorse geosynthetic-reinforced soil structures for their adaptability during ground motion. Meanwhile, South Korea's Green New Deal is financing geomembrane-lined stormwater basins across cities. Smaller economies in ASEAN are ramping up their adoption, backed by financing from the Asian Development Bank. This surge in adoption is broadening the addressable demand, solidifying Asia-Pacific's position as the dominant growth engine in the geosynthetics market.

North America accounted for a significant portion of revenue. This was largely driven by the Infrastructure Investment and Jobs Act, which allocated a substantial budget for road and bridge projects, alongside the EPA's regulations on landfill liners. In Canada, tightening effluent criteria necessitate upgrades to wastewater systems, specifically requiring geomembrane lagoons. Meanwhile, Mexico's infrastructure initiatives are forging connections between industrial corridors and Pacific ports, thereby extending the regional supply chain for essential materials like polypropylene and polyethylene resins.

Europe contributed significantly to the sales figures. Amendments to Germany's Federal Water Act are mandating the use of geomembrane liners in new industrial wastewater lagoons, subsequently boosting demand in Central Europe. While circular-economy directives are promoting the use of recycled-polymer geotextiles, there's ongoing scrutiny regarding the consistency of their mechanical properties. In contrast, South America and the combined regions of the Middle East and Africa represent a modest share of the revenue. Projects like Chile's copper tailings and Brazil's expansive highway concessions underscore the volatility tied to commodities. Yet, they also spotlight opportunities, especially when policies harmonize with environmental protections. In Saudi Arabia, both the ambitious NEOM project and the Riyadh Metro are turning to swift-install geosynthetic solutions to adhere to the stringent timelines set by Vision 2030. Simultaneously, South Africa has mandated geomembrane liners for upgrades in municipal wastewater systems, aiming to rectify water quality issues.

Competitive Landscape

The geosynthetics market is moderately fragmented. White-space innovation centers on smart and sustainable variants. Naue and Solmax have commercialized sensor-embedded products that support condition-based maintenance, offering price premiums over conventional materials and shifting sales dialogs toward data services. Recycled-polyethylene geomembranes are gaining traction in Europe due to carbon-reduction incentives, though long-term durability testing remains a gating factor. Regional specialists such as KayTech in South Africa and Taian Modern Plastic in China win niche projects by providing rapid customization and local technical service, particularly where import logistics and currency swings challenge multinationals. ISO 10318 and ASTM D-series certifications remain the passport for global projects, preserving barriers to entry and stabilizing pricing power among established brands.

Geosynthetics Industry Leaders

Solmax

Tensar, A Division of CMC

Huesker International

Naue GmbH & Co. KG

Agru America Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: HUESKER has acquired Sineco International, expanding its product portfolio with high-quality drainage and dewatering solutions. This move strengthens HUESKER's position in the geosynthetics market.

- January 2025: Officine Maccaferri S.p.A. acquired Synteen Technical Fabrics Inc., strengthening its North American footprint in high-performance geosynthetics.

- December 2024: Solmax revealed plans to centralize its nonwoven geotextile production at a single, advanced facility in the EMEA region, aiming to enhance efficiency and innovation.

- May 2024: Solmax Americas has completed a capacity upgrade at its Houston facility, introducing new extrusion capabilities to boost geomembrane production. This enhancement supports increased output and product performance.

Global Geosynthetics Market Report Scope

Geosynthetics are man-made polymeric materials used in civil engineering and construction to improve the performance and durability of soil structures.

The geosynthetics market is segmented by material, type, function, application, and geography. By Material, the market is segmented into polypropylene, polyethylene, polyester, and others. By Type, the market is segmented into geotextile, geomembrane, geocomposite, and geosynthetic liner, and others. By Function, the market is segmented into separation, drainage, reinforcement, filtration, and moisture barrier. By Application, the market is segmented into construction, transportation, environmental, and other applications. The report also covers the market size and forecasts for the geosynthetics market in 15 countries across the major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Polypropylene, Polyethylene, and Polyester |

| Others |

| Geotextile |

| Geomembrane |

| Geocomposite |

| Geosynthetic Liner and Others |

| Separation |

| Drainage |

| Reinforcement |

| Filtration |

| Moisture Barrier |

| Construction |

| Transportation |

| Environmental |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Polypropylene, Polyethylene, and Polyester | |

| Others | ||

| By Type | Geotextile | |

| Geomembrane | ||

| Geocomposite | ||

| Geosynthetic Liner and Others | ||

| By Function | Separation | |

| Drainage | ||

| Reinforcement | ||

| Filtration | ||

| Moisture Barrier | ||

| By Application | Construction | |

| Transportation | ||

| Environmental | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the geosynthetics market in 2026?

The global geosynthetics market stands at USD 21.78 billion in 2026 and is forecast to reach USD 33.17 billion by 2031, reflecting a 8.78% CAGR over 2026-2031.

Which product type is expected to expand the fastest through 2031?

Geomembranes hold the largest 34.68% share in 2025 and are projected to grow at the highest 10.15% CAGR through 2031, driven by stringent environmental containment rules.

How will transportation projects influence demand through 2031?

Transportation applications are set for a 10.46% CAGR, outpacing all other segments as governments adopt geosynthetic reinforcement to cut roadbed costs and carbon footprints.

Why is Asia Pacific the dominant regional market in 2025, and what is its outlook to 2031?

Asia Pacific commands 44.36% of 2025 revenue and should post a 9.70% CAGR between 2026 and 2031 thanks to China’s Belt and Road investments and India’s Smart Cities Mission, both of which specify geosynthetics in large-scale infrastructure.

Which sustainability trends will reshape competitive positioning?

Biodegradable polymers, sensor-enabled membranes, and recycled-content geogrids are emerging as procurement criteria as regulators target a 30% microplastic-leakage cut by 2030 in the European Union.

Page last updated on: