Genetic Analysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

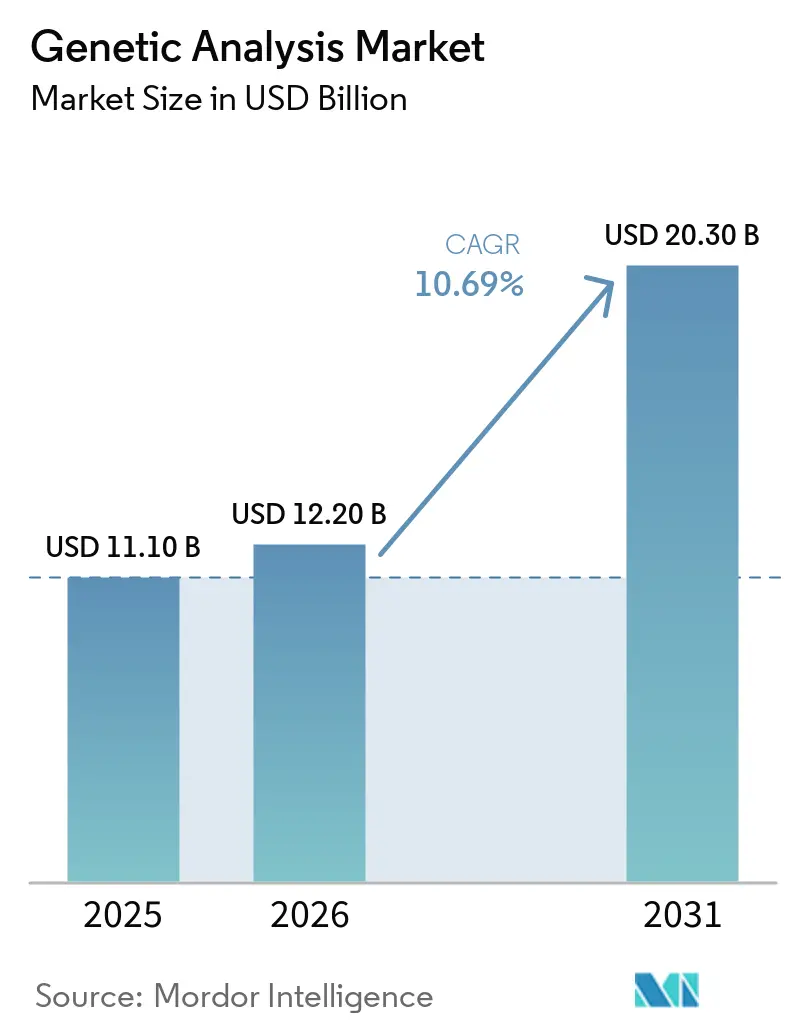

| Market Size (2026) | USD 12.20 Billion |

| Market Size (2031) | USD 20.30 Billion |

| Growth Rate (2026 - 2031) | 10.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Genetic Analysis Market Analysis by Mordor Intelligence

The Genetic Analysis Market size is expected to increase from USD 11.10 billion in 2025 to USD 12.20 billion in 2026 and reach USD 20.30 billion by 2031, growing at a CAGR of 10.69% over 2026-2031.

Reimbursement policies that now reward comprehensive genomic profiling rather than piecemeal testing, rapid compression of sequencing costs toward the USD 200-600 per-genome range, and large-scale governmental genomics programs are pulling genomic testing out of research silos and embedding it in routine care pathways. Vendors are realigning business models around software subscriptions and multiomics workflows because consumables, interpretation, and longitudinal data streams now generate higher lifetime value than the instruments alone. Hospitals are internalizing sequencing to capture margin, while platform companies are racing to add long-read capability and spatial or proteomic modules so customers are not tempted to switch suppliers. These intertwined shifts point to sustained expansion for the genetic analysis market through the end of the decade.

Key Report Takeaways

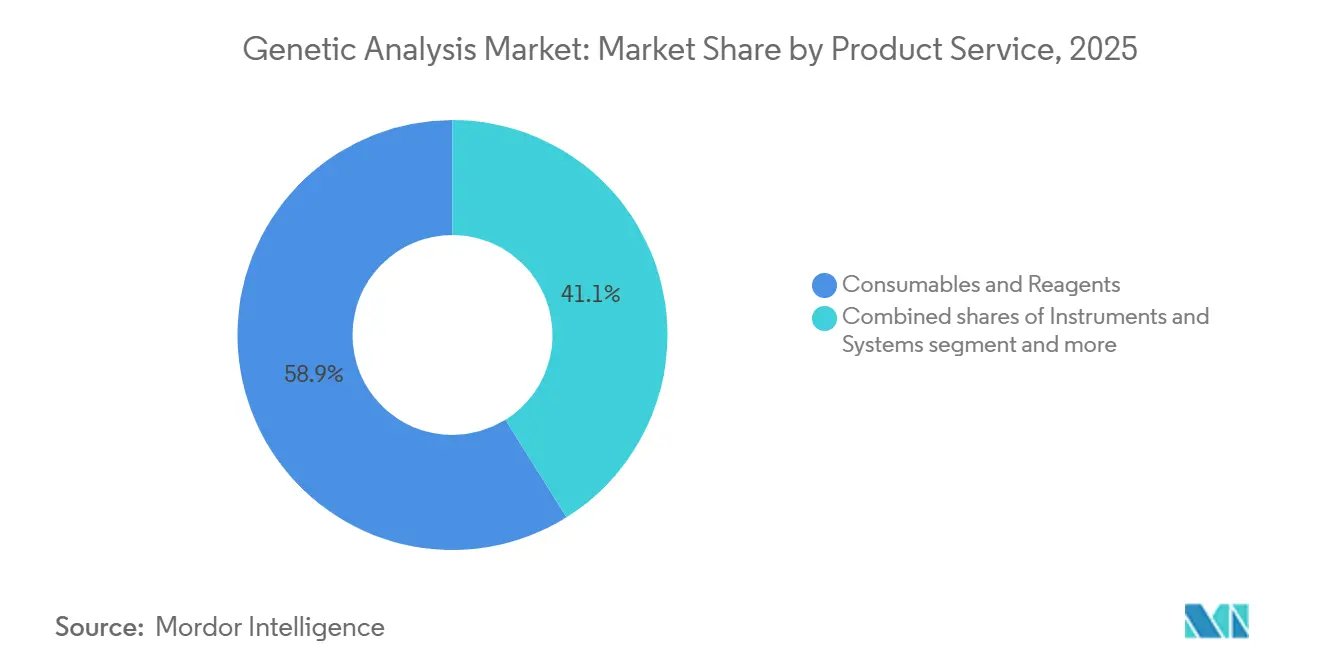

- By product and service, consumables & reagents captured 58.9% of the genetic analysis market share in 2025, yet Instruments & systems are forecast to post the fastest 12.4% CAGR to 2031.

- By technology, next-generation short-read sequencing led with 32.2% revenue share in 2025, while long-read sequencing is projected to expand at a 14.0% CAGR through 2031.

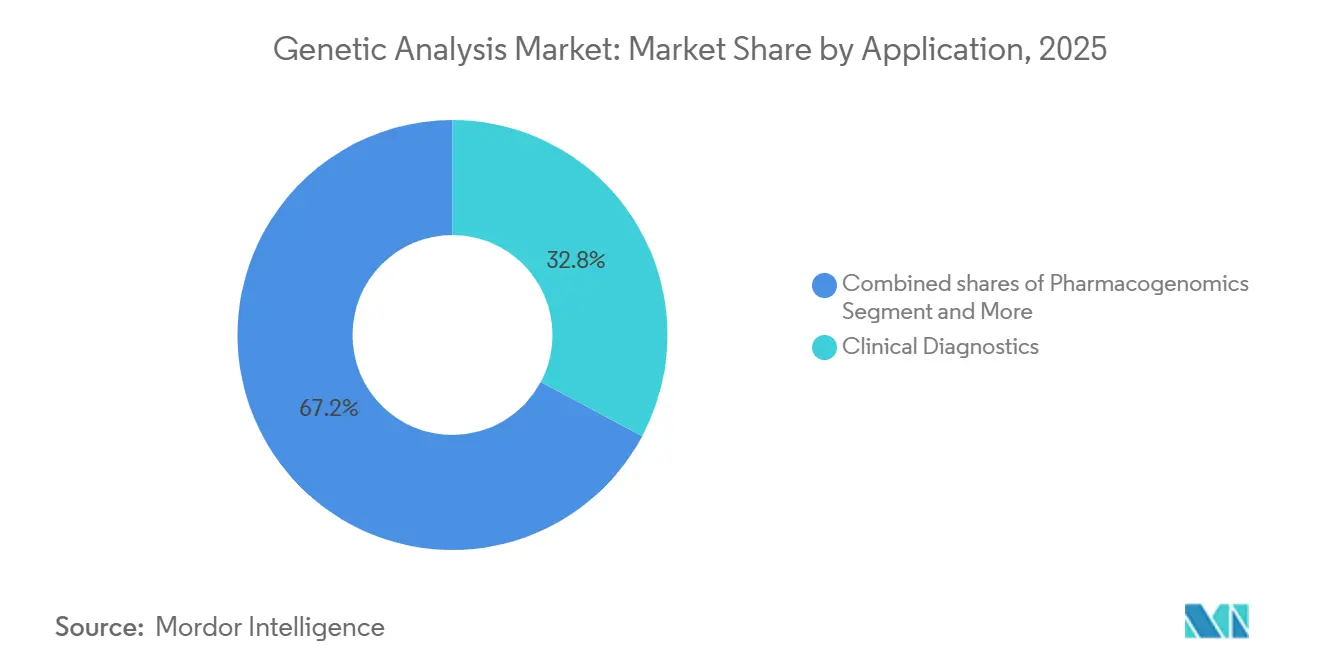

- By application, clinical diagnostics commanded 32.8% of the genetic analysis market size in 2025 and is advancing at a 12.6% CAGR toward 2031.

- By end user, hospitals & clinics are the fastest-growing cohort, set to climb at a 12.8% CAGR between 2026 and 2031, and reference laboratories reported with 35.0% share of 2025 revenue.

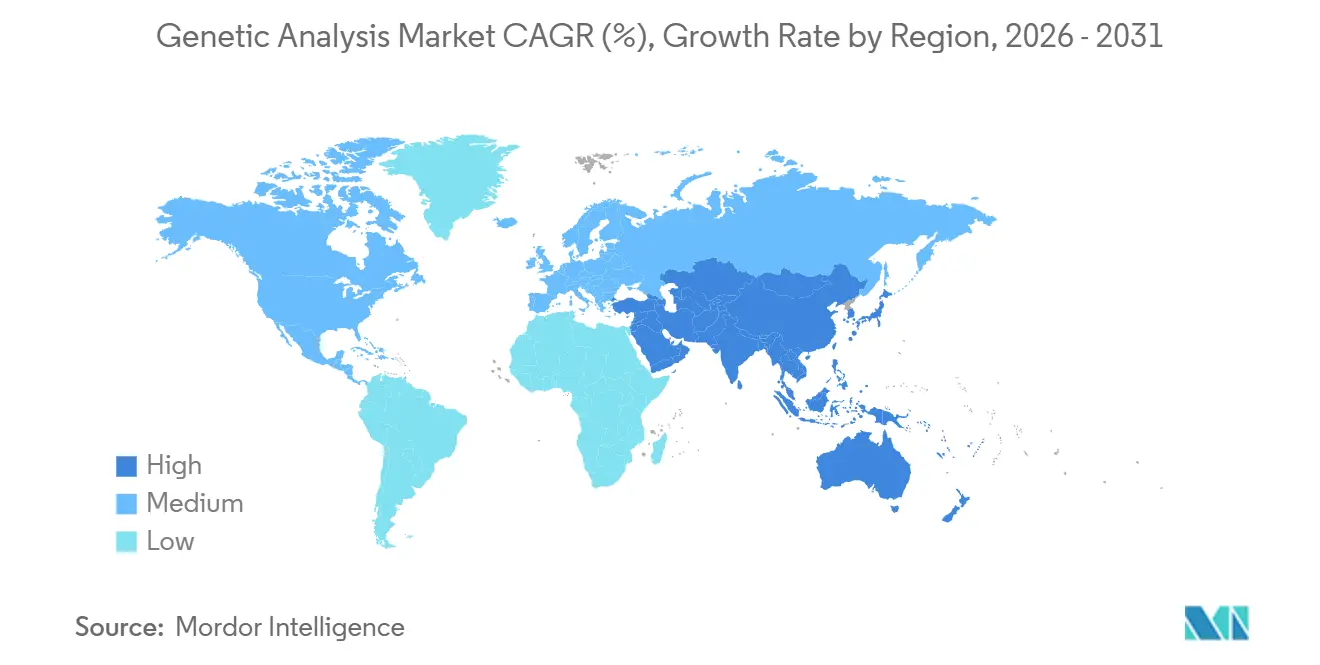

- By geography, North America led with 43.29% of the share in the genetic analysis market; however, Asia-Pacific is expected to record the highest 13.0% CAGR, eclipsing mature-market growth rates on the back of national sequencing initiatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Genetic Analysis Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining sequencing costs compress cost-per-genome | +2.1% | Global, strongest uptake in North America, Europe, China | Medium term (2-4 years) |

| Expanding clinical reimbursement and CDx approvals | +2.5% | North America, Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| National genomics programs embedding WGS in care | +1.8% | UK, US, China, Japan, India, spillover to Middle East, Latin America | Long term (≥ 4 years) |

| EU new genomic techniques accelerate agri-genomics | +0.9% | Europe, adoption spreading to North America, Brazil | Medium term (2-4 years) |

| AI-enabled variant interpretation speeds insights | +1.6% | Global, led by North America, Europe, rapid Asia-Pacific uptake | Short term (≤ 2 years) |

| Rising liquid biopsy adoption for MRD and early detection | +1.4% | North America, Europe, early use in Japan, South Korea, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Sequencing Costs Compress Cost-per-Genome

Whole-genome sequencing prices have dropped 96% since 2013, reaching USD 200-600 per sample in 2025, and Pacific Biosciences’ planned SPRQ-Nx platform aims to push costs below USD 300 in late 2026. As large newborn and adult studies in the United Kingdom, India, and China ramp up, vendors are pivoting from a hardware-sale mindset to recurring-reagent and software subscriptions, evidenced by Pacific Biosciences reporting 55% consumables growth in Q4 2025. Emerging-market projects such as GenomeIndia illustrate that lower per-genome costs open doors for population diversity studies. The result is a deeper installed base and recurring revenue streams that stabilize the genetic analysis market.

Expanding Clinical Reimbursement and CDx Approvals

CMS set a USD 2,989.55 payment for Illumina’s TruSight Oncology Comprehensive, effective January 2026, while Medicare also covered NeoGenomics’ 500-gene liquid biopsy in March 2026[1]Illumina Inc., “Press Release,” illumina.com. Private insurers such as UnitedHealthcare updated policies accordingly, catalyzing laboratory investment in higher-throughput sequencers. FDA approvals for Guardant 360 CDx and other large panels are teaching payers that broader tests reduce costly repeat biopsies. The trend escalates volumes flowing through the genetic analysis market and underpins demand for automated workflow solutions.

National Genomics Programs Integrating WGS into Care

The NHS Genomic Medicine Service performed more than 810,000 tests in 2024, and Genomics England is sequencing 100,000 newborns and 150,000 adults, embedding WGS into standard care. China’s National GeneBank has processed over 10 million genomes, while Japan’s Biobank Japan holds 300,000 samples. Government backing lowers perceived risk, spurs hospital adoption, and enlarges the genetic analysis market beyond early adopters.

AI-Enabled Variant Interpretation Accelerates Insights

QIAGEN’s Franklin platform has interpreted more than 750,000 clinical cases, demonstrating that AI can cut turnaround time and talent bottlenecks for small labs[2]BioPharma Boardroom, “QIAGEN Acquires Genoox for USD 70 Million,” biopharmaboardroom.com. Illumina’s April 2025 collaboration with Tempus AI aligns sequencer data with multimodal clinical records, improving algorithm accuracy. As reimbursement rises, software speed and accuracy become decisive differentiators, reshaping competitive dynamics throughout the genetic analysis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and GDPR-style rules | -1.2% | Europe and similar regimes | Long term (≥ 4 years) |

| China’s HGR rules on data transfer | -0.8% | China, global partners | Medium term (2-4 years) |

| Patchy reimbursement for CGP/WGS | -1.0% | Select U.S. regions, emerging markets | Short term (≤ 2 years) |

| Data-localization mandates | -0.7% | China, Russia, Middle East, parts of APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cross-Border Transfer Constraints

The European Health Data Space, operational through 2027, forces vendors to host data on EU-resident clouds and meet strict consent requirements, inflating compliance costs and favoring capital-rich players. Smaller labs may consolidate or exit, tempering pace but not direction of growth for the genetic analysis market.

High Capital Investment Requirements for Laboratory Infrastructure and Automation

Setting up an in-house genomics laboratory typically calls for USD 500,000 to USD 5 million in capital, covering sequencers, liquid-handling robots, bioinformatics servers, and a laboratory information management system. Premium long-read instruments such as Pacific Biosciences’ Revio, priced above USD 300,000, and Oxford Nanopore’s PromethION further require dedicated sample-prep automation and high-performance computing to deliver advertised throughput and turnaround times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Consumables Revenue Sustains Growth as Platforms Mature

Recurring reagent kits generated 58.9% of 2025 revenue, anchoring the genetic analysis market size at the laboratory bench. Instrument upgrades to long-read and spatial platforms support a 12.4% CAGR, and bundled software subscriptions are lifting average account value. Integrated ecosystems that lock in reagents, software, and service underpin vendor pricing power.

Instruments & systems are entering a replacement phase as labs shift to higher throughput and multiomics workflows. Revenue clustering around consumables allows vendors to weather capital-spending cycles, keeping the genetic analysis market on a steady growth track.

By Technology: Long-Read Sequencing Captures Structural-Variant Demand

Short-read NGS held 32.2% of the genetic analysis market share in 2025, but long-read sequencing is forecast to be the fastest segment with 14.0% CAGR through 2031. Clinical need for phasing and structural-variant clarity is bringing Pacific Biosciences and Oxford Nanopore into oncology and rare-disease labs. Meanwhile, digital PCR is expanding in gene-therapy QC. The technology mix is fragmenting, requiring informatics layers that can harmonize heterogeneous data streams and broaden the genetic analysis market footprint.

By Application: Clinical Diagnostics Outpaces Research as Reimbursement Widens

Clinical diagnostics generated 32.8% of total application revenue in 2025, and this slice is set to grow at a 12.6% CAGR through 2031 as payers broaden coverage for comprehensive genomic profiling and the FDA clears more companion diagnostics. A clear sign of this shift came when Guardant Health introduced Guardant360 Tissue in April 2025, a test that screens 742 DNA genes, 367 RNA genes, and tumor methylation markers while using 92% less tissue than standard assays, making profiling feasible for patients with limited biopsy material. Pharmacogenomics is also moving into everyday practice; the Clinical Pharmacogenetics Implementation Consortium has published updated guidelines that explain how NAT2, TPMT, NUDT15, and CYP2D6 variants should guide dosing for hydralazine, thiopurines, and beta-blockers.

Outside the clinic, agriculture and animal genomics are gaining momentum after the European Union’s 2025 rule exempted certain gene-edited crops and livestock from lengthy GMO procedures, speeding commercialization of CRISPR products.

By End User: Hospitals Accelerate In-House Testing to Capture Margin

Reference laboratories still led the end-user mix with 35.0% of 2025 revenue, but hospitals and clinics are projected to grow fastest, 12.8% a year to 2031, as administrators look to keep genomics revenue inside their own walls and shorten turnaround times. QIAGEN is easing that shift with new automation lines scheduled for 2026: QIAsymphony Connect for high-throughput liquid biopsy work, QIAsprint Connect for up to 192 samples per run, and the compact QIAmini for labs with space or budget limits, though entry packages still exceed USD 100,000 when training and first-year consumables are counted.

Academic and research institutes remain critical early adopters, snapping up long-read sequencers, spatial transcriptomics rigs, and single-cell systems for grant-funded projects. Drug makers are boosting in-house sequencing as well; Illumina’s Alliance for Genomic Discovery expansion in March 2026 brought Regeneron Genetics Center on board and added a 50,000-sample multiomic data set to help refine target discovery.

Geography Analysis

North America captured 43.29% of the genetic analysis market share in 2025. High reimbursement levels, dense hospital and laboratory networks, and early use of comprehensive genomic profiling sustain regional demand. The Centers for Medicare & Medicaid Services set a USD 2,989.55 payment for Illumina’s TruSight Oncology Comprehensive test effective January 2026, accelerating the adoption of broad multi-gene panels in oncology practices. Roche’s USD 50 billion commitment to new U.S. manufacturing and AI-driven R&D facilities through 2030 underscores confidence in the market’s long-term trajectory. While North America will remain the largest revenue contributor through 2031, growth is expected to moderate as oncology and rare-disease testing nears saturation, shifting vendor emphasis toward pharmacogenomics, prenatal screening, and population-health applications.

Asia-Pacific is projected to log the fastest 12.97% CAGR between 2026 and 2031, fueled by large-scale public genomics programs. China’s National GeneBank now houses data from more than 10 million genomes, supporting both research and clinical sequencing. India’s GenomeIndia initiative has completed 10,000 genomes and plans to broaden coverage of South Asian ancestry groups that are under-represented in global databases.

Europe benefits from coordinated country programs and the European Health Data Space, which standardizes cross-border genomic data sharing across member states. The NHS Genomic Medicine Service delivered more than 810,000 tests in 2024, while Genomics England is sequencing 100,000 newborns and 150,000 adults, weaving whole-genome testing into routine care. Beyond these regions, Gulf states, South Africa, and Brazil are scaling genomics centers, though reimbursement gaps in parts of Latin America and Eastern Europe still limit near-term uptake.

Competitive Landscape

The top three vendors control a significant global revenue, but aggressive vertical integration and multiomics acquisitions are redrawing lines of competition. Illumina’s USD 350 million SomaLogic purchase brings aptamer proteomics under its roof, while QIAGEN’s Genoox acquisition inserts AI interpretation directly into its digital suite[3]Illumina Inc., “Illumina to Acquire SomaLogic,” illumina.com. Roche’s sequencing-by-expansion program threatens to disrupt the duopoly in high-throughput instruments. These moves confirm that long-term success in the genetic analysis market depends less on chemistry alone and more on complete, data-rich ecosystems.

Genetic Analysis Industry Leaders

Illumina Inc

Thermo Fisher Scientific

Danaher Corporation

F. Hoffmann-La Roche

Agilent Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Illumina expanded the Alliance for Genomic Discovery, adding Regeneron Genetics Center and 50,000 proteomic-linked genomes.

- February 2026: Roche unveiled plans for a sequencing-by-expansion platform slated for 2027 release.

- January 2026: Illumina closed the USD 350 million SomaLogic deal, embedding proteomics into its workflow.

Global Genetic Analysis Market Report Scope

As per the scope of the report, genetic analysis is the process of studying DNA to understand how specific genes and variations influence traits, health, and heredity. It involves examining an organism's genetic material to identify mutations, sequence patterns, or chromosomal structures that differ from a standard reference. This can range from testing a single gene to scan for a specific hereditary condition to sequencing an entire genome to map out an individual's complete biological blueprint.

The genetic analysis market is segmented by product & service, technology, application, end users, and geography. Based on product & service, the market is segmented into instruments & systems, consumables & reagents, and software & bioinformatics services. Based on technology, the market is segmented into PCR/qPCR, Next-generation sequencing, long-read sequencing, Sanger sequencing, microarrays, cytogenetics, genotyping & gene expression. By application, the market is segmented into clinical diagnostics, pharmacogenomics, agriculture & animal genomics, forensics & human identification, consumer/ancestry & wellness, and research applications. By end users, the market is segmented into hospitals & clinics, diagnostic & reference laboratories, academic & research institutes, pharmaceutical & biotechnology companies, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Instruments & Systems |

| Consumables & Reagents |

| Software & Bioinformatics Services |

| PCR/qPCR |

| Next-Generation Sequencing (short-read) |

| Long-read Sequencing (SMRT, Nanopore) |

| Sanger Sequencing |

| Microarrays |

| Cytogenetics (Karyotyping, FISH) |

| Genotyping & Gene Expression (non-NGS) |

| Clinical Diagnostics |

| Pharmacogenomics |

| Agriculture & Animal Genomics |

| Forensics & Human Identification |

| Consumer/Ancestry & Wellness |

| Research Applications (functional, transcriptomics, single-cell) |

| Hospitals & Clinics |

| Diagnostic & Reference Laboratories |

| Academic & Research Institutes |

| Pharmaceutical & Biotechnology Companies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product & Service | Instruments & Systems | |

| Consumables & Reagents | ||

| Software & Bioinformatics Services | ||

| By Technology | PCR/qPCR | |

| Next-Generation Sequencing (short-read) | ||

| Long-read Sequencing (SMRT, Nanopore) | ||

| Sanger Sequencing | ||

| Microarrays | ||

| Cytogenetics (Karyotyping, FISH) | ||

| Genotyping & Gene Expression (non-NGS) | ||

| By Application | Clinical Diagnostics | |

| Pharmacogenomics | ||

| Agriculture & Animal Genomics | ||

| Forensics & Human Identification | ||

| Consumer/Ancestry & Wellness | ||

| Research Applications (functional, transcriptomics, single-cell) | ||

| By End User | Hospitals & Clinics | |

| Diagnostic & Reference Laboratories | ||

| Academic & Research Institutes | ||

| Pharmaceutical & Biotechnology Companies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the genetic analysis market be by 2031?

It is projected to reach USD 20.3 billion by 2031, expanding at a 10.7% CAGR from 2026 to 2031.

Which product segment drives most revenue today?

Consumables & reagents generate 58.9% of 2025 sales because every sequenced sample requires kits and flow cells

Why is long-read sequencing gaining momentum?

Clinical laboratories need phasing and structural-variant clarity that short-read chemistry cannot deliver, pushing long-read platforms toward a 14% CAGR by 2031.

What limits adoption in Europe?

GDPR and the European Health Data Space add data-residency and consent obligations that raise compliance costs for smaller labs.

Page last updated on: