Generative AI In Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

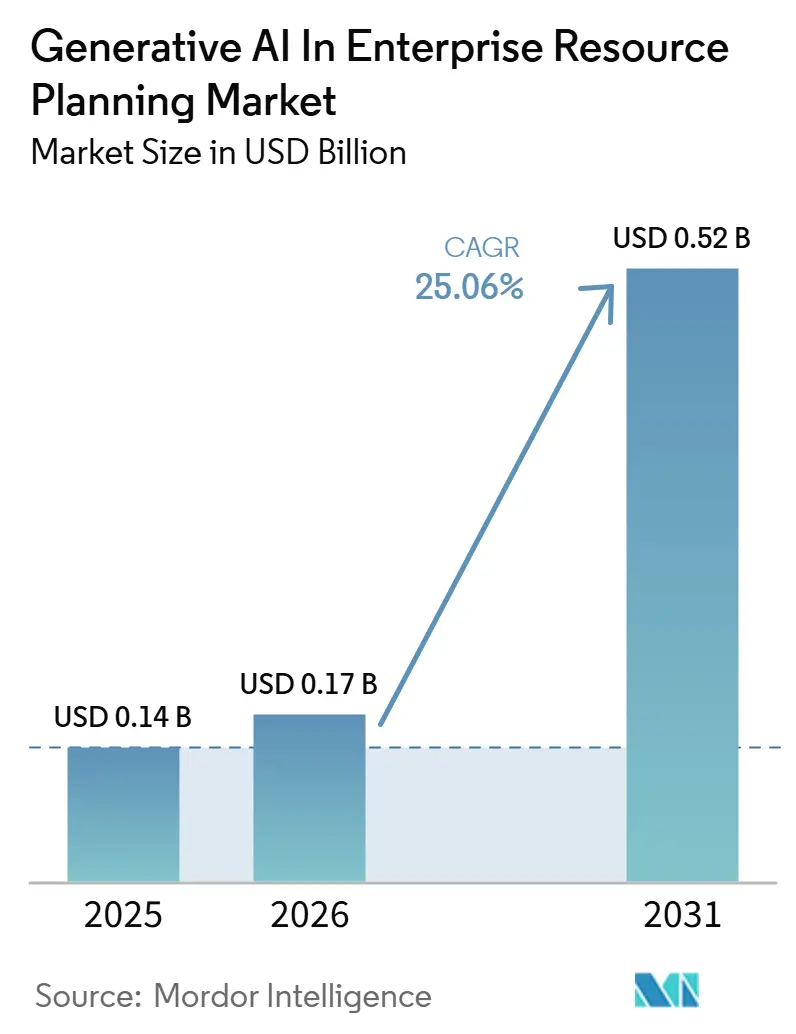

| Market Size (2026) | USD 0.17 Billion |

| Market Size (2031) | USD 0.52 Billion |

| Growth Rate (2026 - 2031) | 25.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Generative AI In Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Generative AI in Enterprise Resource Planning market size is expected to increase from USD 0.14 billion in 2025 to USD 0.17 billion in 2026 and reach USD 0.52 billion by 2031, growing at a CAGR of 25.06% over 2026-2031. Intensifying competitive pressure to compress operating costs, rapid model-as-a-service rollouts by the incumbent vendors, and hyperscale cloud access to AI accelerators collectively shift transaction systems from rule-based automation to context-aware workflows. Expanding vertical-specific foundation models raises inference accuracy, while conversational interfaces broaden the user base beyond trained super-users. Falling inference costs move generative features from executive dashboards into routine tasks such as invoice matching. Nevertheless, regulatory scrutiny of algorithmic reliability and data sovereignty continues to make adoption uneven across regions and industries.

Key Report Takeaways

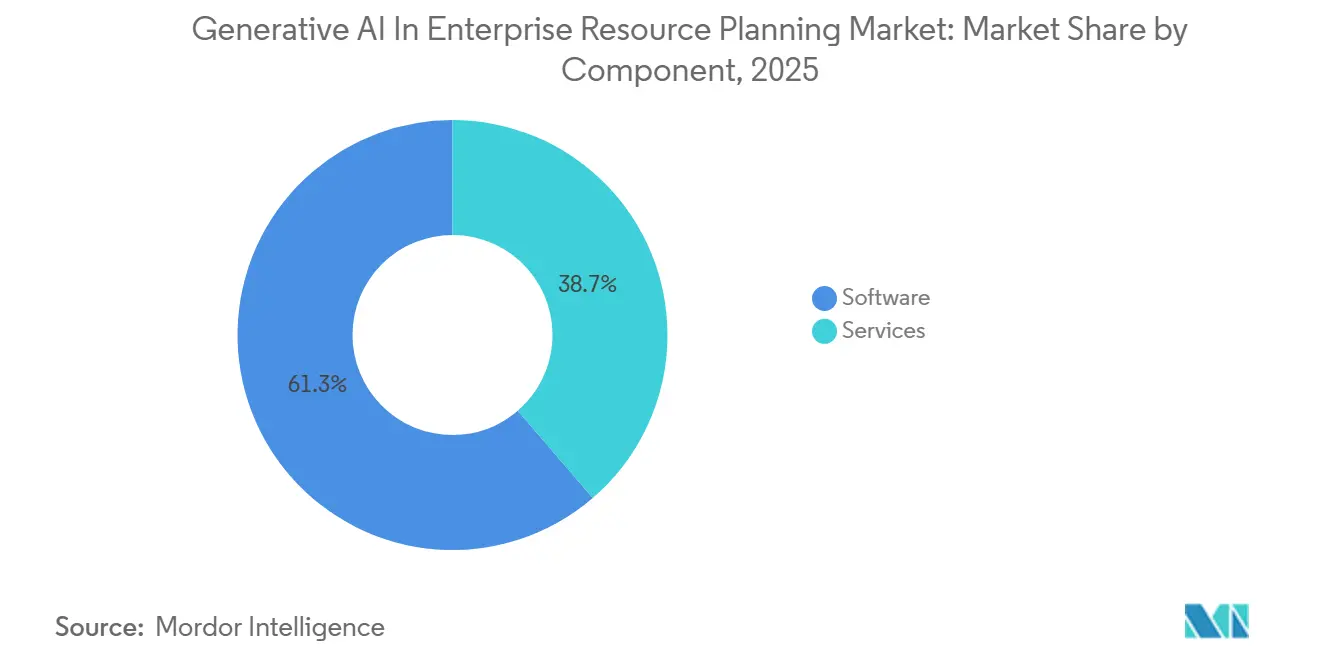

- By component, software led with 61.31% revenue share in 2025, whereas services are advancing at a 25.46% CAGR through 2031.

- By deployment model, cloud captured 72.41% of 2025 spending, yet hybrid configurations are growing at a 25.66% CAGR to 2031.

- By enterprise size, large enterprises held 64.59% of the 2025 value, while small and medium enterprises are expanding at a 26.26% CAGR through 2031.

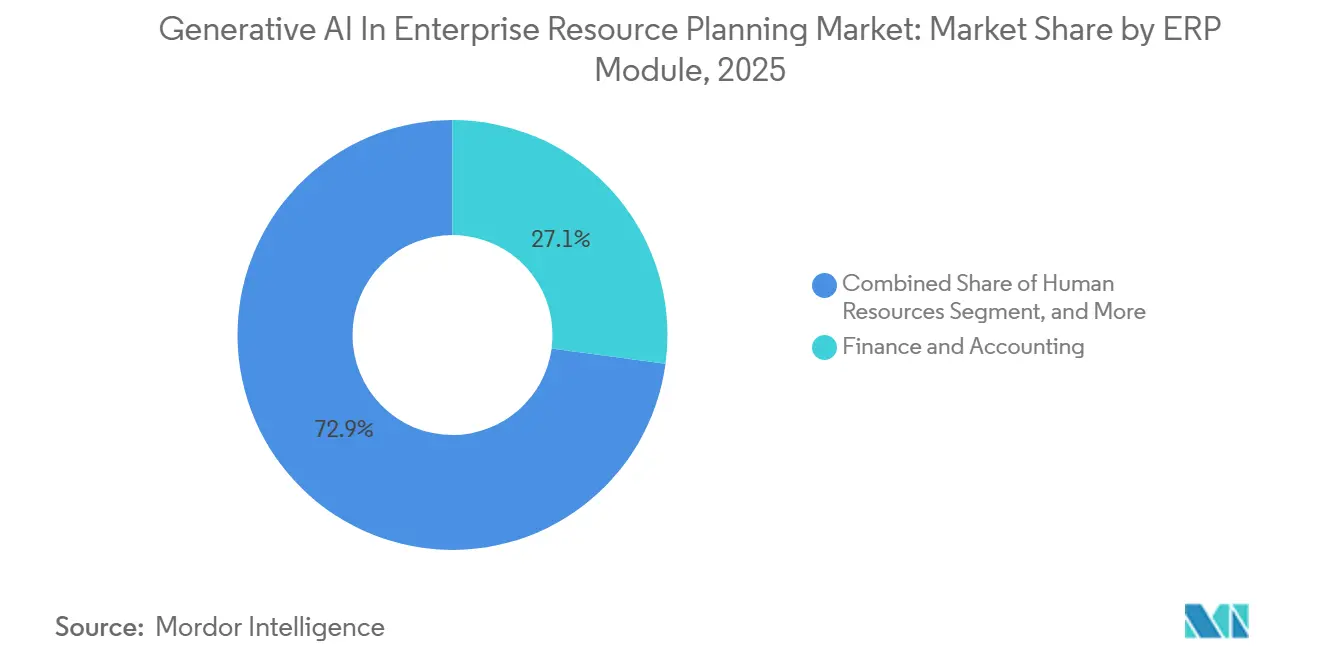

- By ERP module, finance and accounting accounted for 27.14% of revenue in 2025; sales and CRM modules are forecast to post a 25.61% CAGR through 2031.

- By industry vertical, manufacturing accounted for 29.84% of 2025 revenue, and healthcare and life sciences are projected to rise at a 26.06% CAGR to 2031.

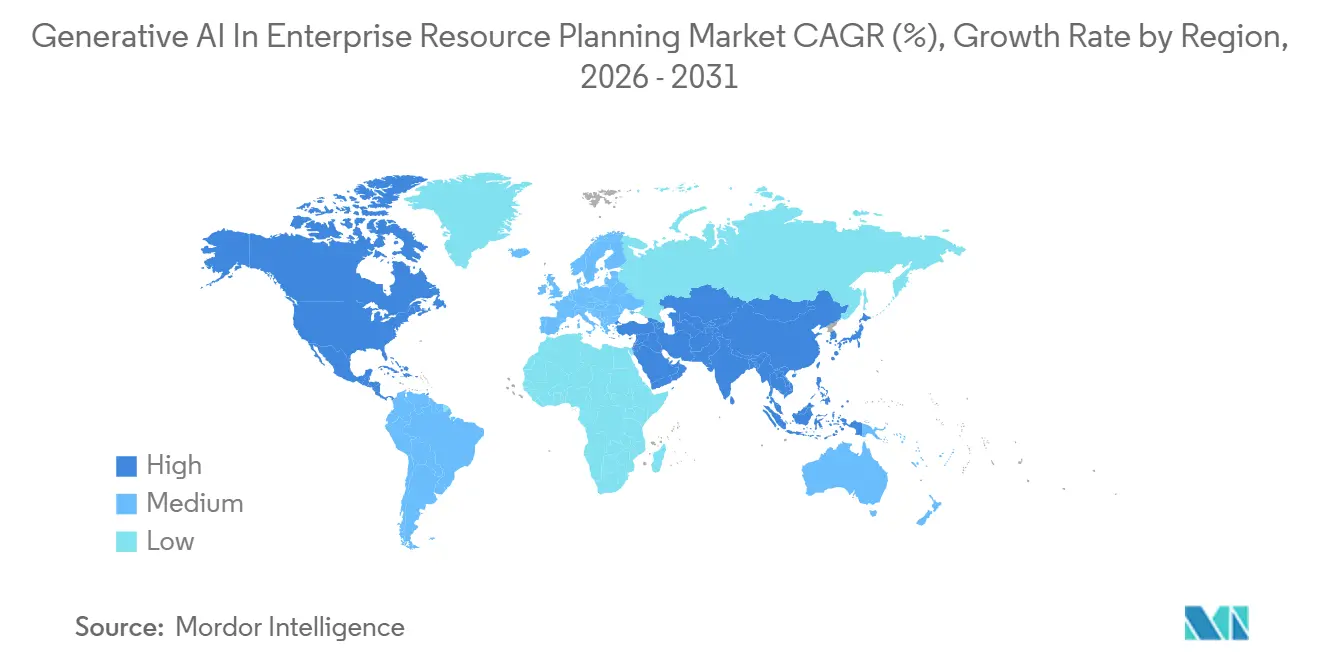

- North America led with 41.29% of 2025 spend, whereas Asia-Pacific is positioned for a 26.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Generative AI In Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative AI-driven code generation cuts ERP customization costs | +5.2% | Global, with early gains in North America and Western Europe | Medium term (2-4 years) |

| Transformer-based natural-language interfaces expand end-user adoption | +4.8% | Global, particularly in Asia-Pacific markets with multilingual requirements | Short term (≤ 2 years) |

| Rapid expansion of industry-specific foundation models for ERP workflows | +4.3% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Falling inference costs thanks to ASIC-based AI accelerators | +3.9% | Global, with infrastructure concentration in North America and Asia-Pacific | Long term (≥ 4 years) |

| Cloud-native ERP roadmaps embedding generative copilots by default | +3.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Vendor ecosystem race to build proprietary domain data lakes | +3.1% | Global, with competitive intensity highest in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generative AI-Driven Code Generation Cuts ERP Customization Costs

Historically, enterprises allocated between 40% and 60% of their total ERP budgets to custom coding efforts to adapt systems to legacy processes and unique business requirements. However, advancements in generative code-completion technology now enable the creation of ABAP, PL SQL, and C# extensions directly from plain-language prompts. This innovation significantly reduces delivery timelines, cutting them by up to half.[1]SAP SE, “SAP Business AI for ABAP Code Generation,” sap.com For instance, Microsoft GitHub Copilot Enterprise demonstrated that complex revenue-recognition logic, which previously required weeks of manual effort, can now be generated, unit-tested, and deployed within just a few hours. This transformation is reshaping the ERP landscape by compressing systems integrators' profit margins and shifting the consulting value proposition toward expertise in prompt engineering rather than traditional manual coding practices.

Transformer-Based Natural-Language Interfaces Expand End-User Adoption

Complex menu structures, which previously discouraged casual users due to their intricate navigation, are now being simplified with the integration of transformer-powered assistants. These advanced assistants can execute multistep processes, such as approvals or variance analyses, through intuitive conversational commands. For instance, Oracle Fusion Cloud ERP agents can interpret complex queries such as 'why did gross margin dip last quarter,' seamlessly integrate data from sources such as the ledger, pricing, and inventory, and provide actionable insights that previously required specialized SQL expertise. Similarly, SAP Joule, which supports 44 languages, has demonstrated its effectiveness by reducing help-desk tickets by 35% during pilot implementations, thereby expanding the range of potential licensees who can benefit from its capabilities.

Rapid Expansion of Industry-Specific Foundation Models for ERP Workflows

Generic public web-trained models often struggle to accurately classify procurement codes or interpret clinical terminology, leading to frequent errors. In contrast, vendors who fine-tune their models using proprietary transactional data have achieved over 90% precision in spend classification, significantly outperforming the 60-70% accuracy typically seen with generic models. This improvement highlights the value of specialized training. Additionally, Infor’s strategic partnership with AWS, set for 2025, focuses on training manufacturing and hospitality-specific AI agents using data from 60,000 customers. This collaboration aims to create robust, industry-specific solutions that effectively establish strong competitive barriers for their products.

Falling Inference Costs Thanks to ASIC-Based AI Accelerators

Inference, which previously made generative ERP unsuitable for transactional workloads due to high costs, has advanced significantly. Trillium TPUs now deliver 3.4 times the throughput of earlier systems, while AWS Trainium2 reduces per-query costs by half. These improvements have enabled seamless integration of real-time suggestions into every module.[2]Amazon Web Services, “Trainium2 Delivers 4× Performance,” aws.amazon.com As a result, vendors can deploy copilots for high-frequency tasks, such as invoice matching, without increasing the total cost of ownership, making these solutions more accessible and efficient for businesses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithmic hallucination risk in mission-critical transactions | -2.8% | Global, with heightened sensitivity in regulated industries across North America and Europe | Short term (≤ 2 years) |

| Copyright and training-data IP exposure in regulated industries | -2.3% | North America and Europe, with emerging litigation in Asia-Pacific | Medium term (2-4 years) |

| Talent shortage for ERP-focused prompt engineering | -1.9% | Global, most acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Escalating sovereign-cloud compliance requirements | -1.7% | Europe, China, India, with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Algorithmic Hallucination Risk in Mission-Critical Transactions

Probabilistic errors, or hallucinations, pose a significant threat to Sarbanes-Oxley compliance because even a single false journal entry can cascade through consolidation hierarchies, leading to widespread inaccuracies in financial reporting. To mitigate these risks, enterprises implement layered rule checks and human approval processes, which, while necessary, partially offset the productivity gains achieved through automation. Additionally, the EU AI Act categorizes AI applications used for financial records as high-risk systems, mandating strict incident-reporting requirements and introducing additional regulatory hurdles that slow adoption.

Copyright and Training-Data IP Exposure in Regulated Industries

Foundation models rely on web-scraped content, which frequently infringes on copyright laws. The ongoing New York Times lawsuit accuses these models of willful copyright infringement, creating uncertainty and hindering rollouts in scenarios where liability remains undefined. Organizations in heavily regulated industries, such as healthcare and banking, are hesitant to adopt these models on a large scale. They are waiting for the introduction of indemnification clauses or the establishment of safe harbor provisions to mitigate potential legal risks before proceeding with broader deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component – Services Momentum Reflects Sustained Implementation Complexity

Services accounted for 38.69% of 2025 revenue and are forecast to grow faster than software with a CAGR of 25.46% over the forecast period, as organizations increasingly recognize the importance of prompt libraries, retrieval pipelines, and user change management in ensuring project success. The demand for consulting hours is rising as teams focus on curating knowledge graphs to ground model outputs effectively. This trend is driving the Generative AI in Enterprise Resource Planning market size closer to achieving parity between product and services revenue streams.[3]Accenture plc, “Consulting Hours Rise for Generative ERP Implementations,” accenture.com

Vendors are now unbundling platform licenses from application add-ons, allowing for greater flexibility in service offerings. Additionally, managed services are taking on the operation of inference clusters while ensuring guaranteed latency, which is critical for seamless operations. SAP’s AI Business Services unit expanded its workforce by 40% in 2026 to address the growing demand for retraining services. This development highlights why advisory and managed service offerings are expected to continue gaining a larger share in the Generative AI in Enterprise Resource Planning market.

By Deployment Model – Hybrid Architectures Balance Sovereignty and Scale

Cloud configurations, which are projected to account for 72.41% of spending by 2025, however, the hybrid deployment model is expected to register a CAGR of 25.66% over the forecast period. The traction as data-localization laws become increasingly stringent. Multinational corporations are adopting a dual approach by maintaining sensitive ledgers on-premise while leveraging cloud GPUs for functions such as sales or HR copilots. This strategy allows them to balance regulatory compliance with enhanced performance. For instance, Microsoft Dynamics 365 hybrid enables customers to synchronize model weights while ensuring inference processes remain close to the data, a feature that aligns with residency mandates in countries such as India and China.

Additionally, edge-optimized distilled models are being deployed to deliver low-latency experiences directly on factory floors, while centralized cloud systems handle monthly updates to model weights. This flexible approach is driving the growth trajectory of Generative AI in the Enterprise Resource Planning market, particularly for hybrid setups. At the same time, it limits the expansion of pure on-premises solutions to specific sectors, such as defense or critical infrastructure, where stringent security requirements prevail.

By Enterprise Size – Low-Code Platforms Democratize SME Adoption

Large organizations accounted for 64.59% of 2025 spending, while small and medium-sized enterprises (SMEs) posted the fastest growth rate, with a CAGR of 26.26%. This trend highlights the increasing adoption of generative AI solutions by SMEs, driven by their need to remain competitive in a rapidly evolving market. Solutions like Zoho Zia and Odoo Copilot offer pretrained models that are seamlessly integrated into ready-to-use workflows, effectively eliminating the necessity for in-house data science expertise. These tools enable SMEs to leverage advanced AI capabilities without requiring significant technical resources, making them more accessible to smaller businesses. Additionally, pay-as-you-go pricing models further reduce financial risk, allowing SMEs to experiment with these technologies without committing to large upfront investments. This flexibility has been a key factor in driving adoption among smaller enterprises.

At the same time, enterprise contracts remain significantly larger in absolute value due to global organizations investing heavily in multilingual fine-tuning, compliance audits, and other advanced customizations. These investments are necessary to meet the complex operational and regulatory requirements of large-scale businesses. For instance, Microsoft revealed that Dynamics 365 contracts with companies employing over 10,000 individuals averaged eight times the value of mid-market contracts. This disparity underscores the differing needs and capabilities of large enterprises compared to SMEs. While SMEs focus on cost-effective and ready-to-deploy solutions, large enterprises prioritize tailored implementations that align with their extensive operational frameworks. This trend is expected to persist in the Generative AI for Enterprise Resource Planning industry, reflecting the distinct approaches and priorities of these two market segments.

By ERP Module – Sales and CRM Lead Future Upside

Finance and accounting provide the foundation for the market, with a 27.14% share in 2025, yet sales and CRM modules are expected to experience the fastest growth, with a CAGR of 25.61%, driven by advancements in quote-generation and contract-negotiation copilots. For example, Dynamics 365 Sales Copilot has demonstrated its ability to reduce deal cycles by up to 30% for pilot customers, showcasing its potential to enhance sales efficiency and streamline sales processes. This highlights the increasing reliance on AI-driven tools to optimize sales operations. As a result, sales modules are anticipated to capture an increasingly significant share of the Generative AI in the Enterprise Resource Planning market by the end of the decade, reflecting their growing importance in driving business outcomes and improving overall productivity.

Human resources and supply chain modules are also gaining traction, incorporating advanced features such as generative policy creation and exception handling to streamline and optimize operational processes. These modules are becoming essential for organizations aiming to enhance workforce management and supply chain efficiency. Furthermore, manufacturing modules are integrating predictive maintenance capabilities, which are increasingly being adopted to address the rising demand for diversified and efficient solutions in the Generative AI in Enterprise Resource Planning market. This integration not only helps in reducing downtime but also ensures better resource utilization, making it a critical component of modern ERP systems.

By Industry Vertical – Healthcare Accelerates Under Clearer Liability Rules

Manufacturing remains the largest sector in the Generative AI for Enterprise Resource Planning market, with a 29.84% share, driven by extensive adoption of predictive maintenance capabilities and process optimization tools. However, the healthcare sector is experiencing the fastest compound annual growth rate (CAGR) with 26.06%, fueled by the FDA's draft guidance that legitimizes AI-augmented clinical documentation.[4]U.S. Food and Drug Administration, “Draft Guidance on AI Clinical Documentation,” fda.gov This regulatory support has encouraged healthcare providers to adopt AI-driven solutions to streamline administrative processes and improve operational efficiency. For instance, Philips and Oracle have partnered to co-develop prior-authorization agents that reduce administrative workloads by 30%, showcasing the potential of AI in transforming healthcare operations.

In the retail sector, companies are leveraging generative AI to enhance demand forecasting and optimize markdown strategies, enabling better inventory management and improved profitability. Meanwhile, the banking, financial services, and insurance (BFSI) sector is cautiously piloting AI-driven solutions for disclosure-grade narrative generation, ensuring compliance with stringent regulatory requirements. Additionally, energy utilities are embedding AI copilots into asset management filings, enabling more efficient resource allocation and operational planning. Collectively, these developments highlight the expanding vertical footprint of Generative AI in the Enterprise Resource Planning market, as industries increasingly recognize its value in addressing sector-specific challenges and driving growth.

Geography Analysis

North America accounted for 41.29% of 2025 expenditure, leveraging its robust cloud infrastructure and a significant pool of prompt engineering talent. U.S. enterprises have been quick to integrate generative features into procurement and supply chain operations to mitigate the impact of rising wage inflation. Meanwhile, Canadian natural resources firms are prioritizing cross-border logistics optimization to enhance operational efficiency. In Mexico, maquiladoras are adopting generative ERP solutions to ensure compliance with USMCA sourcing regulations, further driving the region's adoption of advanced ERP technologies.

Asia-Pacific is anticipated to experience the fastest growth, with a projected CAGR of 26.06%. In China, the government’s directive for state enterprises to adopt local foundation models is driving the growth of domestic ERP suppliers. India’s outsourcing industry is transforming, with shared-service centers being retooled using AI-augmented workflows to boost export competitiveness. Japan is addressing its labor shortages by implementing conversational shop-floor scheduling solutions, while South Korean conglomerates are capitalizing on government AI subsidies to optimize semiconductor and consumer electronics supply chains, further strengthening their global competitiveness.

Europe is expected to grow steadily, albeit under stricter regulatory oversight. The EU AI Act is increasing compliance-related investments, giving larger incumbents with substantial financial resources an advantage. German automakers are deploying generative ERP solutions to mitigate the impact of semiconductor supply chain volatility. In the United Kingdom, companies are utilizing AI copilots to streamline post-Brexit customs paperwork, achieving a 25% reduction in documentation errors. France is channeling its sovereign-cloud policies to drive demand for hybrid ERP solutions, while Italy and Spain are lagging due to the prevalence of smaller-sized firms that face challenges in adopting such technologies. The Middle East and Africa region presents emerging growth potential, driven by Gulf countries’ investments in AI infrastructure programs and South African banks’ focus on managing regulatory workloads effectively.

Competitive Landscape

The Generative AI in Enterprise Resource Planning market remains moderately concentrated. SAP, Oracle, and Microsoft embed copilots across their portfolios, leveraging their extensive installed bases to secure renewals and maintain customer loyalty. The competition among these vendors has shifted towards ensuring model reliability, which provides an advantage to those controlling vast amounts of proprietary transaction data. Strategic cloud alliances further enhance the capabilities of ERP suites by granting early access to next-generation ASICs and foundational models. For instance, Microsoft’s multi-year Azure OpenAI extension for Dynamics 365 exemplifies how such partnerships enable the integration of advanced AI technologies into ERP systems.

Opportunities for growth exist in niche verticals where generic copilots struggle to meet specific requirements. Startups are focusing on areas such as aerospace, serialized inventory management, or pharmaceutical trial accounting by developing bespoke AI agents tailored to these industries. However, the high complexity of integration poses significant challenges to scaling these solutions. Patent activity in this space is concentrated around retrieval-augmented generation, a technology that grounds AI model responses in structured ERP tables. This approach helps mitigate issues like hallucinations while strengthening the competitive advantage of established players in the market.

Innovations in pricing models are also emerging, with vendors introducing consumption-based inference fees that increase with usage intensity. This pricing strategy aligns vendor incentives with customer productivity, encouraging greater adoption of AI-driven ERP solutions. However, it also introduces a risk of customer churn if the systems fail to implement effective guardrails against hallucinations. Overall, established vendors are solidifying their market position by leveraging their dataset gravity, forming strategic cloud partnerships, and navigating regulatory requirements effectively.

Generative AI In Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor, Inc.

Workday, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SAP released SAP-RPT-1, a domain model that automates journal entries with 94% accuracy across pilot S/4HANA Cloud sites.

- February 2026: Oracle launched OCI AI Agent Platform, offering custom agents for payables, supplier talks, and demand forecasting at USD 0.02 per inference.

- January 2026: Microsoft debuted Agent 365, enabling autonomous purchase order creation and invoice matching, cutting accounts payable cycle time by 40%.

- December 2026: Workday partnered with Anthropic to embed Claude in Financial Management and HCM, with general availability slated for Q2 2026.

Global Generative AI In Enterprise Resource Planning Market Report Scope

The Generative AI in Enterprise Resource Planning (ERP) market refers to the global ecosystem of software solutions and related services that integrate generative AI into ERP systems to enhance, automate, and optimize core business processes. This market encompasses AI-powered capabilities such as automated content generation, intelligent data analysis, predictive insights, conversational interfaces, and workflow automation embedded within ERP modules.

The Generative AI in Enterprise Resource Planning Market Report is Segmented by Component (Software, and Services), Deployment Model (On-Premise, Hybrid, and Cloud), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), ERP Module (Finance and Accounting, Human Resources, Supply Chain and Logistics, Manufacturing and Production, Sales and Customer Relationship, and Other ERP Modules), Industry Vertical (Manufacturing, Retail and E-commerce, Healthcare and Life Sciences, BFSI, Energy and Utilities, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-Premise |

| Hybrid |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Finance and Accounting |

| Human Resources |

| Supply Chain and Logistics |

| Manufacturing and Production |

| Sales and Customer Rlationship |

| Other ERP Modules |

| Manufacturing |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| BFSI |

| Energy and Utilities |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| Saudi Arabia | ||

| Rest of Middle East | ||

| South Africa | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Model | On-Premise | ||

| Hybrid | |||

| Cloud | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By ERP Module | Finance and Accounting | ||

| Human Resources | |||

| Supply Chain and Logistics | |||

| Manufacturing and Production | |||

| Sales and Customer Rlationship | |||

| Other ERP Modules | |||

| By Industry Vertical | Manufacturing | ||

| Retail and E-commerce | |||

| Healthcare and Life Sciences | |||

| BFSI | |||

| Energy and Utilities | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| Saudi Arabia | |||

| Rest of Middle East | |||

| South Africa | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Generative AI in Enterprise Resource Planning market by 2031?

The market is forecast to reach USD 0.52 billion by 2031, expanding at a 25.06% CAGR from 2026-2031.

Which deployment model is growing fastest?

Hybrid architectures show the highest growth, expanding at a 25.66% CAGR as firms balance data sovereignty with cloud scalability.

Why are services outpacing software growth?

Prompt engineering, retrieval pipeline design, and change management make implementation complex, so consulting and managed services revenue rises faster than license sales.

Which ERP module will lead future revenue growth?

Sales and CRM modules are expected to post the strongest CAGR as generative copilots automate quoting, negotiation, and customer responses.

How does regulation affect adoption in Europe?

The EU AI Act designates financial record-keeping AI as high risk, adding conformity assessments and slowing rollouts, particularly among smaller vendors.

What are key risks enterprises must mitigate?

Algorithmic hallucination that can trigger financial misstatements and unresolved copyright liability from training data remain primary adoption constraints.

Page last updated on: