Gel Permeation Chromatography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

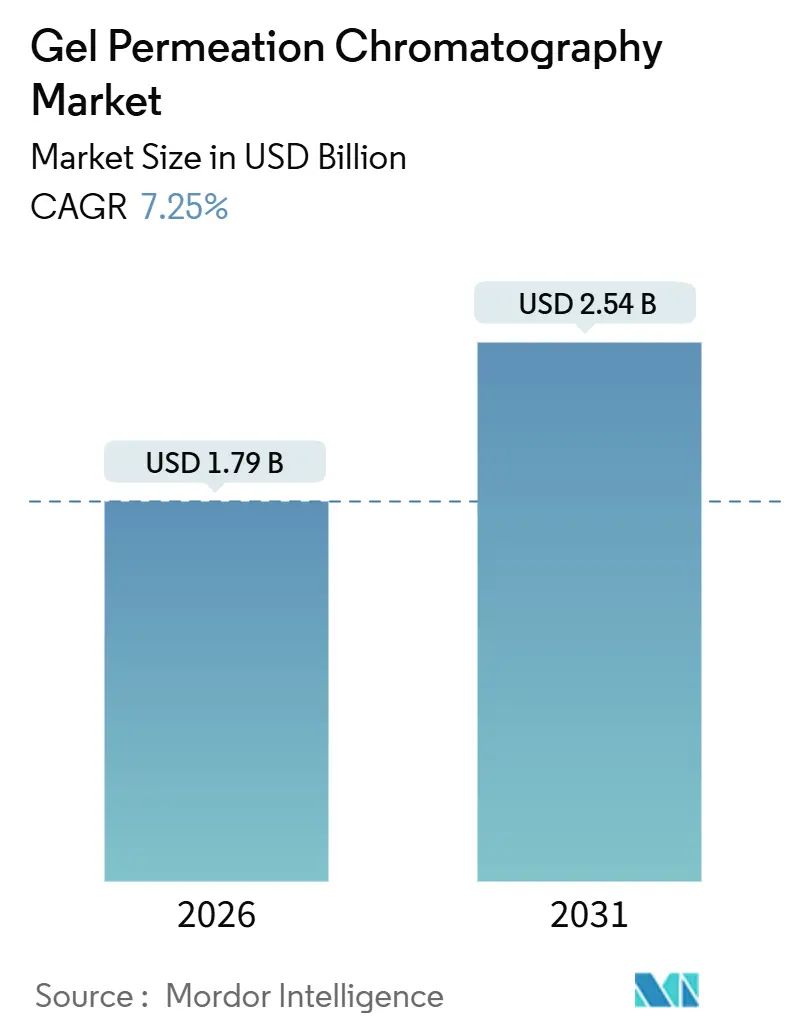

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

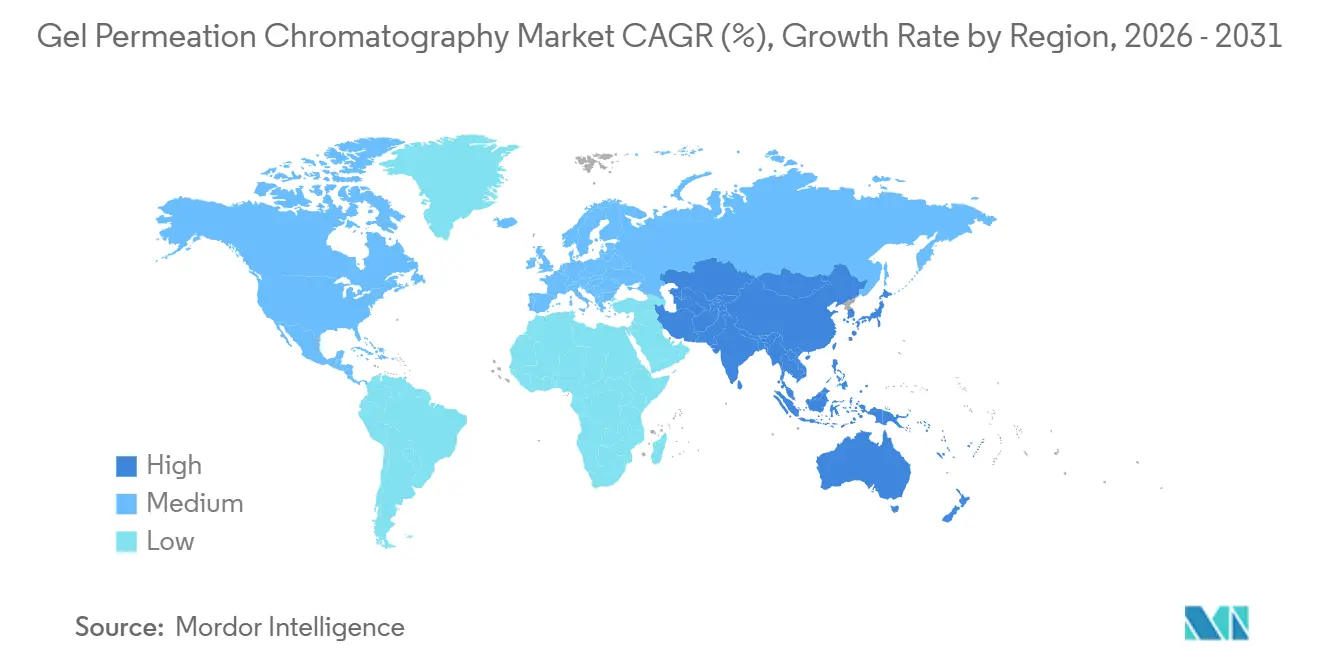

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gel Permeation Chromatography Market Analysis by Mordor Intelligence

The Gel Permeation Chromatography Market size is estimated at USD 1.79 billion in 2026, and is expected to reach USD 2.54 billion by 2031, at a CAGR of 7.25% during the forecast period (2026-2031).

Accelerating biologics pipelines, circular-economy mandates for polymers, and the rapid scale-up of contract research organizations are converging to keep capital equipment utilization high and to pull through columns, standards, and data-analysis software. Pharmaceutical quality-control laboratories are standardizing size-exclusion methods to comply with ICH Q2(R2) revisions, while polymer manufacturers seeking recycled-content certifications require precise molecular-weight profiles to validate batch consistency. CROs, whose revenues are tied to analytical throughput rather than instrumentation ownership, are acquiring multi-detector platforms and automation modules to compress turn-around times for biosimilars and gene-therapy vectors. Vendors are responding with shorter-run-time columns, AI-driven method-development software, and high-temperature systems that extend GPC into polyolefin recycling analytics. Price sensitivity in academic and emerging-market laboratories, however, is lengthening replacement cycles for pumps and detectors in favor of consumables and service contracts.

Key Report Takeaways

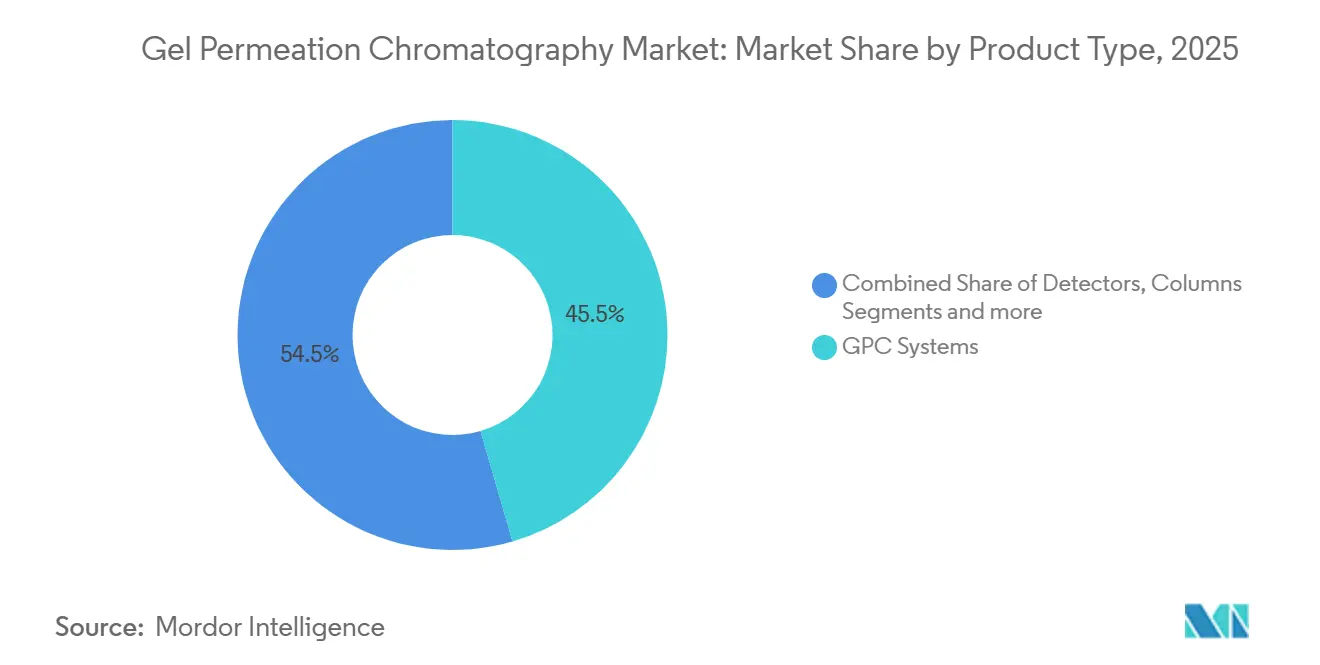

- By product type, GPC systems led with 45.55% of Gel Permeation Chromatography market share in 2025, while columns are advancing at an 8.25% CAGR through 2031.

- By technology, ambient-temperature platforms accounted for 56.53% of the Gel Permeation Chromatography market size in 2025, whereas automated and clean-up systems are expanding at a 9.05% CAGR.

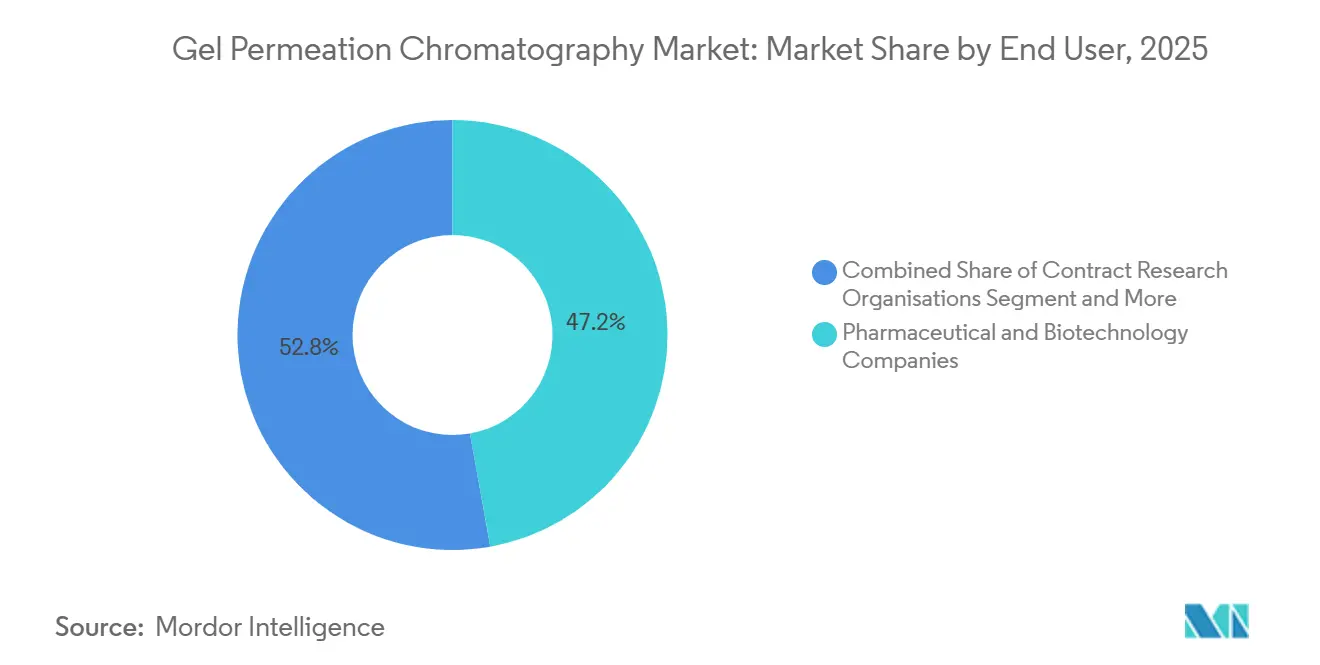

- By end user, pharmaceutical and biotechnology companies held 47.23% of Gel Permeation Chromatography market share in 2025; CROs record the fastest growth at 9.15% CAGR to 2031.

- By application, polymer characterisation accounted for 40.25% of the market size in 2025, and biopharmaceutical analysis is advancing at a 10.21% CAGR.

- By geography, North America retained 38.15% revenue share in 2025, yet Asia-Pacific is projected to post the highest regional CAGR at 8.51% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gel Permeation Chromatography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising biopharma & polymer R&D spend | +1.8% | Global, with concentration in North America, Europe, and Asia-Pacific (China, India, South Korea) | Medium term (2-4 years) |

| Stringent global QC / regulatory compliance | +1.5% | Global, particularly North America (FDA) and Europe (EMA); emerging in Asia-Pacific as regulatory harmonization advances | Short term (≤ 2 years) |

| Technological advances in multi-detector & HT-GPC systems | +1.2% | North America & Europe for multi-detector; Asia-Pacific (China, Japan) for HT-GPC in polyolefin industries | Medium term (2-4 years) |

| Expansion of SEC use in micro-plastics & recycling analytics | +0.9% | Europe (circular economy mandates), North America (environmental monitoring), emerging in Asia-Pacific | Long term (≥ 4 years) |

| AI-driven automation improving throughput & data quality | +1.0% | Global, with early adoption in North America and Europe pharmaceutical QC labs; spreading to Asia-Pacific CROs | Short term (≤ 2 years) |

| Sustainable-materials push requiring precise MW characterisation | +0.8% | Europe (regulatory-driven), North America (corporate sustainability commitments), Asia-Pacific (export compliance) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Biopharma & Polymer R&D Spend

Global R&D outlays for monoclonal antibodies, antibody-drug conjugates, and gene-therapy vectors exceed USD 310 billion in 2026, and each program requires molecular-weight distribution data for release testing, stability, and comparability exercises. India’s pharmaceutical exports alone are slated to climb to USD 60–65 billion by 2030, increasing the installed base of GPC units in both captive and contract development facilities. Polyolefin producers are simultaneously investing to tailor chain-length distributions so that recycled grades match virgin material performance targets. South Korean CDMOs that specialize in antibody-drug conjugates procure multi-detector platforms to verify conjugation homogeneity, and Japanese precision-medicine centers integrate sub-2 µm columns to shorten run times for clinical-trial batch release. Together these capital and consumable flows add roughly 1.8 percentage points to the forecast CAGR.

Stringent Global QC / Regulatory Compliance

The FDA, EMA, and PMDA have harmonized analytical procedure validation under ICH Q2(R2), making system suitability, robustness, and intermediate precision mandatory for biologic and small-molecule assays[1]European Medicines Agency, “ICH Q2(R2) Guideline on Validation of Analytical Procedures,” ema.europa.eu. As a result, pharmaceutical quality-control departments are updating legacy ambient systems with autosamplers that can execute replicate injections overnight and with audit-tractable software that stores raw chromatograms for at least 15 years. Polymer producers selling into food-contact and medical markets reference ISO 16014 for SEC protocols, pushing demand for traceable reference standards. Emerging regulators in China and Brazil increasingly require full method-validation dossiers, accelerating installations of compliant data-systems and validated column chemistries. The immediate compliance burden elevates instrument utilization rates and sustains spare-parts and service-contract revenues.

Technological Advances in Multi-Detector & HT-GPC Systems

Multi-angle light scattering, viscometry, and differential refractive-index modules configured in sequence now deliver absolute molecular-weight determination without external calibration, reducing reportable variance for branched polymers by up to 30%. In high-temperature GPC, column ovens capable of 220 °C and solvent-delivery systems rated for chlorinated aromatics allow petrochemical labs to profile recycled polyethylene and polypropylene. Polymer Char’s GPC-IR portfolio couples infrared detection with HT-GPC to quantify short-chain branching in minutes, an analysis previously relegated to offline spectroscopy. Incremental detector attachments for installed HPLC chassis lower adoption hurdles and shift purchasing toward consumables that can tolerate elevated pressures and aggressive eluents.

AI-Driven Automation Improving Throughput & Data Quality

Genedata’s Chromatics platform applies machine-learning algorithms to baseline correction and peak assignment, cutting data-review time by up to 70% in Phase III biologics programs. Shimadzu’s Methodintelligence suite suggests column particle size, pore diameter, and mobile-phase composition based on analyte descriptors, allowing CROs to develop validated methods in under one week. Pharmaceutical QC laboratories pair robotic liquid handlers with column-switching valves to process 400 samples per analyst shift, thus redeploying staff to deviation investigations. Automated workflows lift analytical throughput without immediate capital purchase of new pumps or ovens, but they increase demand for columns, seals, and high-purity solvents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex & consumable costs | -0.6% | Global, with acute pressure in Asia-Pacific and South America where budget constraints limit adoption | Short term (≤ 2 years) |

| Competition from alternative separation techniques (FFF, LC-MS) | -0.5% | North America & Europe where technique diversity is highest; emerging in Asia-Pacific research institutions | Medium term (2-4 years) |

| Skilled-labour shortage & steep learning curve | -0.4% | Global, particularly acute in Asia-Pacific and South America where trained chromatography specialists are scarce | Long term (≥ 4 years) |

| Supply-chain volatility for ultrapure solvents & columns | -0.3% | Global, with episodic disruptions in Asia-Pacific and Europe due to raw-material availability and logistics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex & Consumable Costs

A full multi-detector GPC configuration with high-temperature capability surpasses USD 150,000, and laboratories running 50 samples per day spend USD 30,000 annually on columns and solvents[2]Agilent Technologies, “Form 10-K 2024,” agilent.com. Budget-constrained academics in Thailand and public health labs in Colombia therefore postpone upgrades, opting instead for certified pre-owned units and extended-warranty packages. Consumables, unlike instruments, are non-deferrable; silica-based columns lose efficiency after 1,500 injections with proteinaceous feeds, and tetrahydrofuran must be HPLC-grade to avoid baseline drift. The capital hurdle contracts the addressable market in lower-income regions and subtracts roughly 0.6 percentage points from long-term growth.

Competition from Alternative Separation Techniques

Asymmetric-flow field-flow fractionation (AF4) eliminates stationary-phase shearing of ultra-high-molecular-weight polymers, appealing to research programs developing branched polyethylene and nanocomposite resins. LC-MS workflows targeting oligomers under 2 kDa provide exact-mass data that refractive-index detection cannot achieve. Early adopters in Boston and Munich now allocate budget to AF4 and LC-MS modules, reducing incremental spending on GPC detectors. Nevertheless, GPC retains entrenched positions in regulated QC laboratories, where validated methods and existing reference-standard libraries would be costly to replace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Sustain Momentum as Instrument Cycles Stretch

Columns, standards, and detector membranes are outpacing pumps and autosamplers, reflecting a structural pivot toward recurring revenue. Columns using sub-2 µm particles reduce run times from 30 minutes to 3 minutes when paired with 600 bar pumps, enabling laboratories to process 8-fold more samples without additional hardware. The Gel Permeation Chromatography market size for columns is projected to expand at 8.25% CAGR, compared with 5.1% for systems. Laboratories manage capital budgets by retrofitting multi-detector arrays onto legacy pump stacks, deferring full replacement until a next-generation chromatographic chassis justifies the expense. Service-contract attach rates now exceed 60% on new installations, providing vendors a hedge against cyclical instrument demand.

The Gel Permeation Chromatography market share for systems will continue to erode as consumables capture incremental spend, yet installed-base lock-in still underpins revenue visibility for leading suppliers. Agilent’s CrossLab services group reported 5% growth in 2024, despite an 8% decline in instrument sales, illustrating how maintenance and compliance validation offset hardware softness. Delivered-software modules that flag pressure deviations and predict seal failure further entrench OEM-branded consumables, as third-party columns may not feed diagnostic data to vendor dashboards.

By Technology: Automation and HT-GPC Unlock Adjacent Workflows

Ambient-temperature setups remain workhorses, particularly for aqueous SEC of therapeutic proteins. Yet automated and clean-up systems are projected to grow 9.05% annually, propelled by ICH Q2(R2) requirements that call for documented intermediate precision across multiple analysts and days. Automation packages include carousel autosamplers, column-switching manifolds, and AI-assisted data-systems that register sample metadata via barcode readers. Regulatory inspectors now request electronic raw-data archives and method-parameter traceability, features embedded in next-generation chromatography-data systems.

High-temperature GPC occupies a specialized but influential niche. Polyolefin circular-economy policies in Europe and Canada compel resin suppliers to verify that post-consumer recycled content does not suffer chain scission during reprocessing. HT-GPC provides quantitative evidence by revealing reductions in weight-average molecular weight and shifts in polydispersity index. Vendors differentiate through solvent-containment engineering and integrated infrared detectors that simultaneously profile branching. Consequently, HT-GPC columns rated to 220 °C command premium pricing and deliver margins exceeding 60%, underpinning R&D pipelines for vendors such as Polymer Char and Malvern Panalytical.

By End User: CRO Demand Accelerates

Pharmaceutical and biotechnology companies remain the primary buyers of qualification and validation services, but CROs are projected to post 9.15% CAGR as they absorb analytical tasks once handled internally. Larger firms contract out stability protocols for biosimilar candidates to avoid building redundant capacity in multiple regulatory jurisdictions. The Gel Permeation Chromatography market size attached to CRO workflows reached USD 410 million in 2026 and is on pace to double by 2031.

Academic institutes and government research labs, while smaller in spending, play disproportionate roles in method innovation. Collaborations between universities and instrument manufacturers often seed prototypes of multi-detector arrays that later migrate to commercial QC settings. Petrochemical companies remain committed to HT-GPC for process control, but price sensitivity in commodity resins keeps system upgrades on a five-to-seven-year cadence, slower than the three-to-five-year cadence in biologics QC.

By Application: Biopharma Surges Ahead of Polymer Characterization

Polymer characterization represented 40.25% of 2025 revenue, but its mid-single-digit growth is eclipsed by biopharmaceutical analysis, which is advancing at 10.21% CAGR. Aggregation testing for monoclonal antibodies, antibody-drug conjugates, and gene-therapy vectors is mandatory under ICH guidance, positioning GPC as an integral release assay. The Gel Permeation Chromatography market size allocated to biopharma exceeded USD 720 million in 2026 and could surpass polymer characterization by 2028 if current acceleration persists.

Gene-therapy developers require chromatographic verification that capsid aggregates remain below 5% to avoid immunogenicity. Lipid-nanoparticle platforms for mRNA vaccines similarly need molecular-weight distribution data to ensure batch consistency. Environmental testing stays niche but strategic; ISO-adapting protocols for microplastic identification rely on SEC coupled with light scattering to profile particle-size distributions.

Geography Analysis

North America anchors the market with 38.15% revenue share, supported by the United States’ dominance in biologics approvals and petrochemical polymers. FDA guidance referencing size-exclusion chromatography in method-validation filings under 21 CFR Part 211 secures recurring demand for compliant columns and reference standards. Canada’s CDMO corridor in Quebec increases purchases of multi-detector packages optimized for glycoprotein therapeutics, while Mexican automotive polymer suppliers use HT-GPC to monitor recycled polypropylene blends.

Europe follows closely, driven by Germany, France, and the United Kingdom. EMA harmonization with ICH Q2(R2) in 2024 triggered a wave of laboratory upgrades, especially among biosimilar manufacturers in Germany. Simultaneously, the European Green Deal imposes recycled-content thresholds on packaging, spurring resin makers to verify molecular-weight retention via HT-GPC. Scandinavian environmental agencies fund labs that apply SEC to monitor microplastics in coastal waters, widening the installed detector base.

Asia-Pacific is the fastest-growing territory, forecast at 8.51% CAGR through 2031 on the back of Indian CDMO expansion and Chinese polymer research. The Gel Permeation Chromatography market share is expected to rebalance as regional suppliers localize column manufacturing, reducing import duties and lead times. Japan’s precision-medicine initiatives incentivize high-throughput SEC for companion-diagnostic biologics, whereas South Korea’s antibody-drug-conjugate clusters acquire multi-detector rigs to perform DAR (drug-to-antibody ratio) profiling.

Latin America and the Middle East remain comparatively small but strategically important. Brazil’s petrochemical complex in Rio de Janeiro runs HT-GPC for ethylene-cracking optimization, and Saudi Arabia’s Vision 2030 chemicals strategy includes pilot plants for recyclable polyolefins that will need molecular-weight verification. Currency volatility and limited skilled-labor pools constrain immediate uptake, but growing environmental regulations could catalyze incremental demand.

Competitive Landscape

Five suppliers—Agilent Technologies, Waters Corporation, Shimadzu Corporation, Thermo Fisher Scientific, and Tosoh Corporation—collectively account for a majority of revenue, keeping market concentration moderate. System commoditization forces vendors to differentiate via detector innovation, AI-embedded software, and lifecycle services. Agilent’s 2024 acquisition of Resolution Biosciences’ digital-PCR assets enhances its upstream sample-prep footprint, enabling cross-sale of GPC consumables into nucleic-acid analytics. Waters leverages its MaxPeak surface-passivation chemistry to bundle columns and vials that reduce metal-ion leaching, tying users to proprietary consumables ecosystems.

Thermo Fisher’s February 2025 agreement to buy Solventum’s filtration business strengthens bundled offerings that link sample preparation directly to chromatography workflows[3]Thermo Fisher Scientific, “2024 Annual Report,” thermofisher.com . Shimadzu’s purchase of Zef Scientific extends multi-vendor service coverage, positioning the firm as a neutral maintenance provider capable of servicing heterogeneous laboratory fleets. Polymer Char and Malvern Panalytical withstand competitive pressure by specializing in HT-GPC and light-scattering detectors, respectively, selling expertise where scale alone is insufficient.

Alternative techniques, notably AF4, add a layer of competition. Wyatt Technology’s Eclipse platform captures polymer scientists seeking to avoid stationary-phase interactions, compelling GPC incumbents to co-market FFF modules as orthogonal companions rather than outright substitutes. Software partnerships are proliferating; Genedata licenses its Chromatics analytics to OEMs, embedding AI functionality within instrument control packages and elevating switching costs for end users.

Gel Permeation Chromatography Industry Leaders

Agilent Technologies Inc.

Waters Corporation

Shimadzu Corporation

Thermo Fisher Scientific Inc.

Tosoh Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Phenomenex introduced Biozen dSEC-1 columns, extending its protein-SEC line with sub-2 µm particles optimized for rapid aggregate profiling.

- July 2025: TESTA Analytical released an OEM-grade viscometer module, enabling chromatography manufacturers to integrate intrinsic-viscosity detection into advanced GPC/SEC stacks.

Global Gel Permeation Chromatography Market Report Scope

As per the scope of the report, gel permeation chromatography (GPC), also known as size exclusion chromatography (SEC), is a chromatographic technique used to separate and analyze molecules based on their size and molecular weight.

The segmentation for the gel permeation chromatography market is categorized by product types, including GPC systems, detectors, columns, pumps, and software & services; by technologies, such as ambient-temperature GPC, high-temperature GPC, and automated/clean-up GPC; by end-users, comprising pharmaceutical & biotechnology companies, academic & research institutes, chemical & biochemical companies, contract research organizations, and other end users; by applications, including polymer characterization, biopharmaceutical analysis, environmental testing, and other applications; and by geographies, covering North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| GPC Systems |

| Detectors |

| Columns |

| Pumps |

| Software & Services |

| Ambient-Temperature GPC |

| High-Temperature GPC |

| Automated / Clean-up GPC |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Chemical & Biochemical Companies |

| Contract Research Organisations |

| Other End Users |

| Polymer Characterisation |

| Biopharmaceutical Analysis |

| Environmental Testing |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | GPC Systems | |

| Detectors | ||

| Columns | ||

| Pumps | ||

| Software & Services | ||

| By Technology | Ambient-Temperature GPC | |

| High-Temperature GPC | ||

| Automated / Clean-up GPC | ||

| By End-User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Chemical & Biochemical Companies | ||

| Contract Research Organisations | ||

| Other End Users | ||

| By Application | Polymer Characterisation | |

| Biopharmaceutical Analysis | ||

| Environmental Testing | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Gel Permeation Chromatography market?

The market is valued at USD 1.79 billion in 2026.

How fast is Gel Permeation Chromatography demand growing in Asia-Pacific?

Asia-Pacific revenue is projected to rise at an 8.51% CAGR to 2031.

Which segment is expanding quickest within Gel Permeation Chromatography?

Columns are growing the fastest, posting an 8.25% CAGR through 2031.

Why are CROs investing heavily in new GPC systems?

Outsourcing of biologics analytical testing is driving CROs to scale throughput and meet ICH Q2(R2) validation needs.

What restraint most affects Gel Permeation Chromatography adoption?

High upfront instrument costs and recurring consumable expenses temper uptake, especially in cost-sensitive regions.

Which technology is emerging for recycled-polyolefin analysis?

High-temperature GPC equipped with infrared detection is gaining traction for verifying molecular-weight retention in recycled polyethylene and polypropylene.

Page last updated on: