GDDR7 For AI Inference GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 5.03 Billion |

| Growth Rate (2026 - 2031) | 41.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GDDR7 For AI Inference GPU Market Analysis by Mordor Intelligence

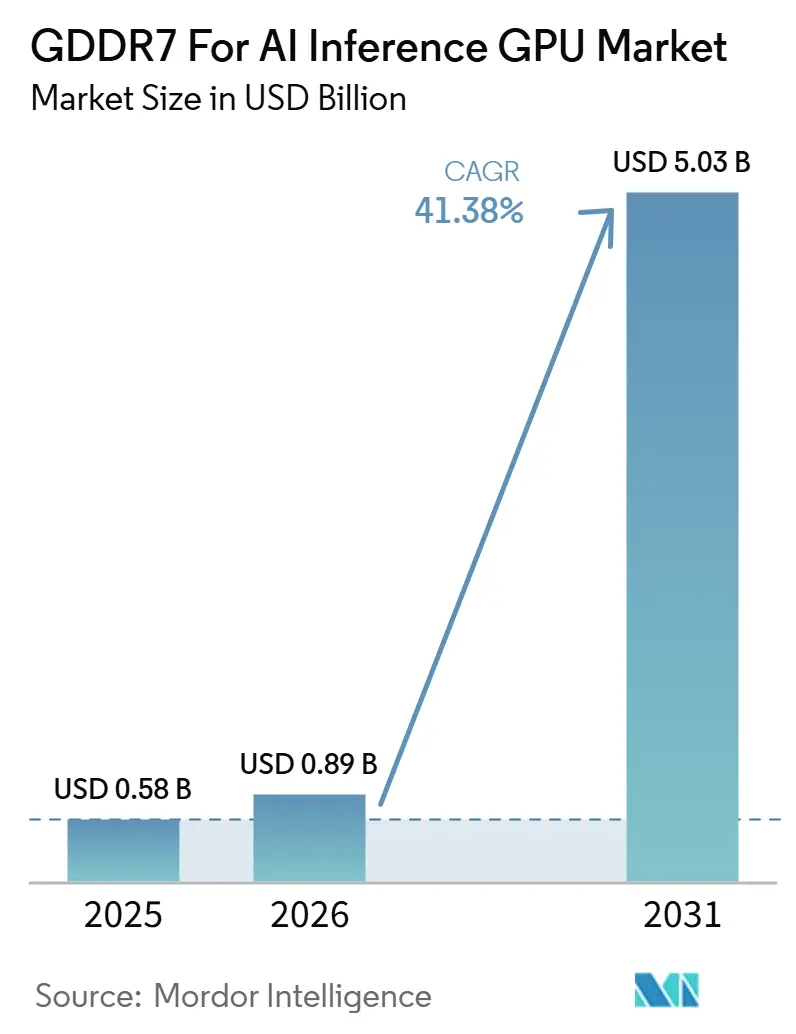

The GDDR7 for AI inference GPU market size is expected to increase from USD 0.58 billion in 2025 to USD 0.89 billion in 2026 and reach USD 5.03 billion by 2031, growing at a CAGR of 41.4% over 2026-2031. The GDDR7 for AI inference GPU market is expanding as AI deployment shifts from centralized model training to distributed inference systems that require high bandwidth, low latency, and tighter cost control. The GDDR7 for AI inference GPU market is also benefiting from the early standardization of the memory interface, faster supplier readiness across Samsung, SK hynix, and Micron, and broader confidence in a multi-vendor supply chain. Demand is widening as enterprises, cloud operators, and defense-oriented edge platforms adopt inference hardware that is easier to integrate than high-bandwidth memory-based alternatives. Export control changes are also reshaping accelerator design choices, which is opening more room for GDDR7-based products in cost-sensitive deployments across Asia. Competitive positioning now depends on production scale, qualification depth, and the ability to support higher-density and higher-speed configurations without sharply increasing total system cost.

Key Report Takeaways

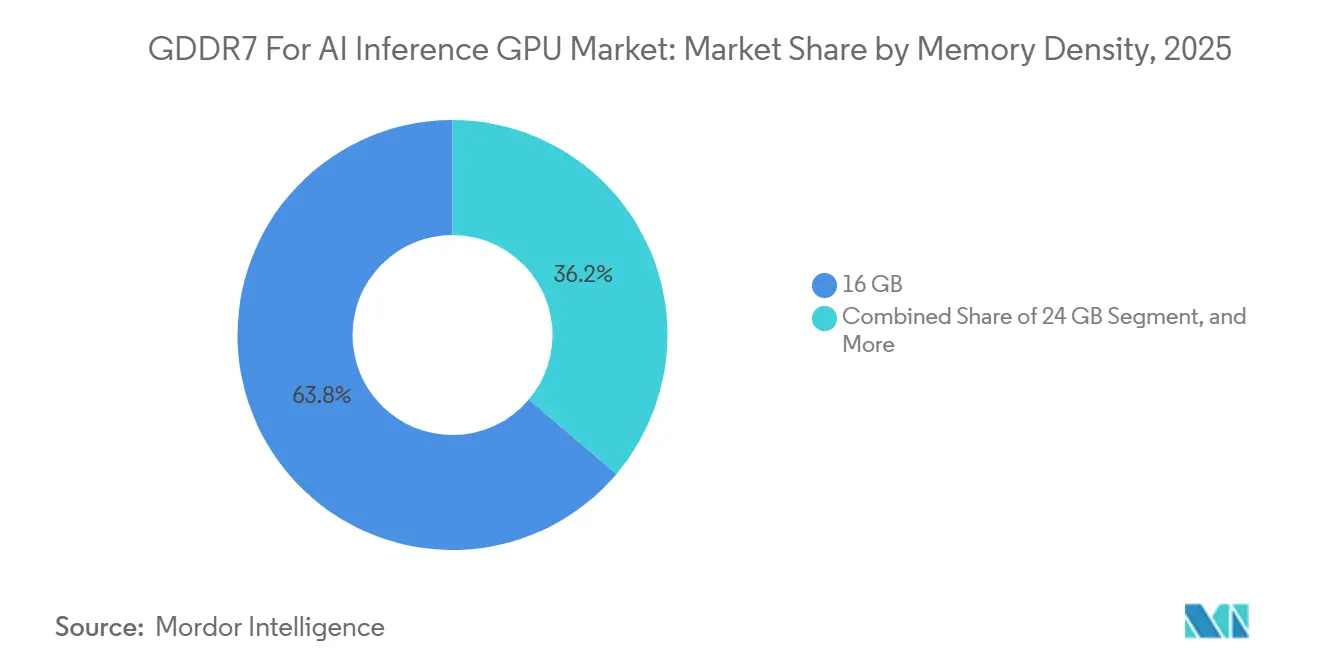

- By memory density, 16 GB led with 63.8% share of the GDDR7 for AI inference GPU market in 2025, while 32 GB and Above is projected to grow at 44.6% CAGR through 2031.

- By memory data rate, up to 32 Gbps held 81.1% share of the GDDR7 for AI inference GPU market in 2025, while above 32 Gbps is forecast to expand at 43.9% CAGR through 2031.

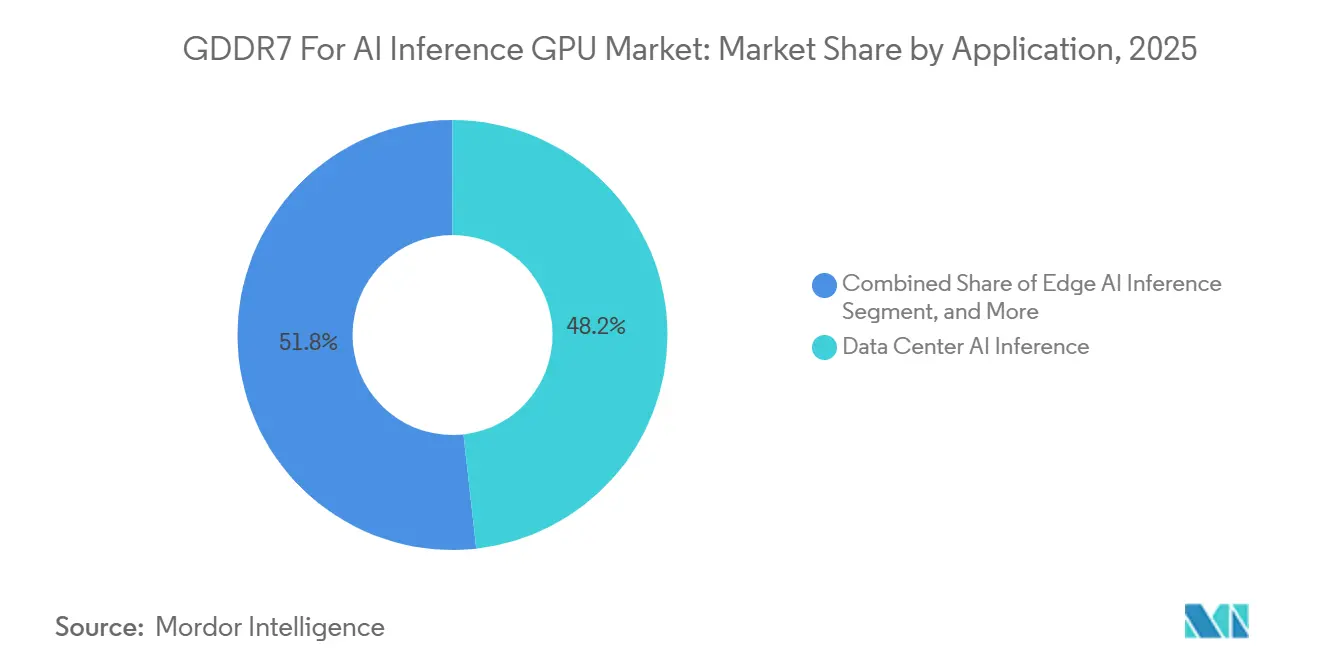

- By application, data center AI inference accounted for 48.2% of the market in 2025, while edge AI inference is advancing at a 43.8% CAGR through 2031.

- By end-user industry, cloud and hyperscale data centers captured 57.6% share of the GDDR7 for AI inference GPU market in 2025, while enterprise IT is projected to grow at 43.4% CAGR through 2031.

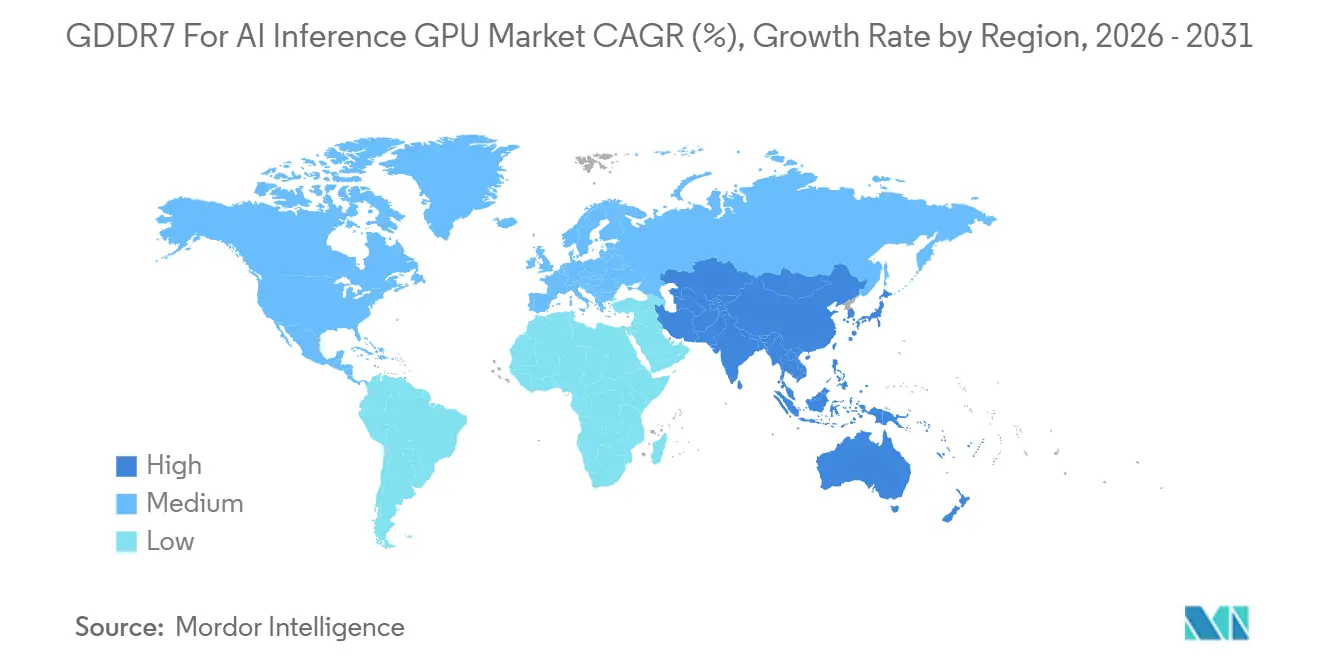

- By geography, North America held 45.9% share in 2025, while Asia-Pacific is forecast to expand at 43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GDDR7 For AI Inference GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Inference Throughput Gains on GDDR7 Platforms | +14.5% | Global | Short term (≤ 2 years) |

| Power-Efficient Bandwidth Scaling With PAM3 Signaling | +8.2% | Global, with early gains in North America and East Asia | Medium term (2-4 years) |

| Rapid Adoption in AI Workstations and Enterprise Appliances | +6.4% | North America and Europe | Short term (≤ 2 years) |

| GDDR7 Design Wins in Premium AI GPU Segments | +5.8% | Global, North America and Asia-Pacific core | Medium term (2-4 years) |

| Supplier Qualification Progress for Major GPU Ecosystems | +3.9% | Asia-Pacific, South Korea and the United States, with spillover to Europe | Short term (≤ 2 years) |

| Localized Inference Demand From Edge and On-Device Deployments | +3.2% | Global, with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Inference Throughput Gains on GDDR7 Platforms

The GDDR7 for AI inference GPU market is moving higher because memory bandwidth has become a direct limiter for token generation and response speed in production inference. The JEDEC GDDR7 standard sets initial data rates up to 32 Gbps and defines a roadmap to 48 Gbps, which materially increases data throughput compared to the prior generation.[1]JEDEC Solid State Technology Association, “JESD239 Graphics Double Data Rate GDDR7 SGRAM Standard,” JEDEC Solid State Technology Association, jedec.org Rambus also noted that GDDR7 can deliver up to 192 GB/s per device, compared with 96 GB/s for GDDR6, which improves throughput without forcing a full shift to more expensive memory architectures.[2]Rambus Inc., “All You Need to Know About GDDR7,” Rambus, rambus.com This matters in inference servers because higher bandwidth can reduce the number of memory devices needed to achieve a target performance level, helping lower board complexity and improve cost discipline. The same advantage matters in workstation and appliance formats, where power, thermal limits, and board space are tighter than in large training clusters. As more inference tasks move into commercial systems rather than research environments, the GDDR7 for AI inference GPU market is gaining from this practical balance between speed, cost, and system simplicity.

Power-Efficient Bandwidth Scaling With PAM3 Signaling

The GDDR7 for AI inference GPU market is also being supported by better energy efficiency, which matters as power density limits tighten across data centers and edge systems. Rambus explained that PAM3 signaling carries 50% more data per clock cycle than prior signaling methods, thereby raising effective data rates without an equal increase in clock frequency. Samsung stated that its 24 GB GDDR7 used clock control management and a dual-VDD structure, cutting power draw by more than 30% compared to its predecessor.[3]Samsung Electronics, “Samsung Develops Industry's First 24Gb GDDR7 DRAM for Next-Generation AI Computing,” Samsung Global Newsroom, news.samsung.com Micron has also positioned GDDR7 as a platform for lower-latency and more power-efficient AI workflows across hybrid CPU, GPU, and NPU systems.[4]Micron Technology, “The New Performance Bottleneck, How More GPU Memory Unlocks Next-Gen Gaming and AI PCs,” Micron Technology, micron.com This efficiency profile helps the GDDR7 for AI inference GPU market extend beyond mainstream cloud hardware into industrial appliances, telecom edge systems, and on-device AI platforms. It also gives suppliers a stronger case when buyers compare inference economics rather than peak training performance alone.

Rapid Adoption in AI Workstations and Enterprise Appliances

The GDDR7 for AI inference GPU market is seeing faster adoption in workstation and appliance formats, as enterprises seek local inference capacity for privacy, lower latency, and greater control. AWS launched EC2 G7e instances in January 2026 using NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs, bringing up to 768 GB of GDDR7 GPU memory per instance into the cloud, accessible to enterprise users.[5]Amazon Web Services, “Announcing Amazon EC2 G7e Instances Accelerated by NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs,” Amazon Web Services Japan, aws.amazon.com Dell introduced the Pro Precision 7 R1 in 2026 as a dense rack workstation built around NVIDIA RTX PRO Blackwell GPUs, showing that compact enterprise deployment is now a real product category rather than a concept. AMD widened platform choice in July 2025 with the Radeon AI PRO R9700 and ROCm 6.4.1 support for inference, fine-tuning, and custom model workflows. These launches show that the GDDR7 for the AI inference GPU market is no longer tied only to large cloud buyers. It is now reaching enterprise IT teams that want a practical path to private inference infrastructure without the cost and integration burden of full server-class training systems.

GDDR7 Design Wins in Premium AI GPU Segments

The GDDR7 for AI inference GPU market is also getting support from premium accelerator designs that use GDDR7 as a deliberate architectural choice rather than a temporary compromise. Reuters reported in May 2025 that NVIDIA planned a lower-cost Blackwell AI chip for China that would use GDDR7 instead of HBM, in response to U.S. export restrictions. That decision matters because it shows GDDR7 can meet the needs of mid-range to high-range inference hardware when bandwidth needs are lower than in frontier model training. It also broadens the addressable demand base for the GDDR7 for the AI inference GPU market by linking product design to policy constraints, pricing targets, and regional hardware access. The effect is strongest in Asia, where compliance-driven product redesign is creating new space for accelerators built around GDDR7 rather than HBM-heavy configurations. Once these platforms are qualified and shipped at scale, the design win can influence procurement patterns for several product cycles rather than a single launch window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HBM Preference in Large-Scale AI Training | -4.8% | North America and Asia-Pacific | Medium term (2-4 years) |

| Limited Leading-Edge DRAM Capacity Amid HBM Competition | -3.2% | Asia-Pacific, especially South Korea and Taiwan | Short term (≤ 2 years) |

| Thermal and Board-Level Integration Complexity | -2.1% | Global | Medium term (2-4 years) |

| Qualification Friction Across Diverse GPU Ecosystems | -1.5% | Global, especially North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HBM Preference in Large-Scale AI Training

The largest restraint on the GDDR7 for the AI inference GPU market is the continued preference for HBM in large-scale AI training systems. Training clusters still prioritize the highest possible bandwidth per accelerator, and that makes HBM3e and HBM4 more attractive for the most expensive compute budgets. This limits how far the GDDR7 for AI inference GPU market can penetrate the top tier of hyperscale spending, even when it is well-suited for inference. Buyer familiarity adds another barrier, because procurement teams often apply training-era benchmarks and qualification expectations to inference hardware. That slows adoption in accounts that already standardized around HBM-equipped platforms and vendor stacks. The result is not a collapse in demand, but a ceiling on participation in the most premium training-led portions of the AI hardware cycle.

Limited Leading-Edge DRAM Capacity Amid HBM Competition

The GDDR7 for AI inference GPU market also faces capacity risk because advanced DRAM manufacturing is concentrated in only a few suppliers. Samsung, SK hynix, and Micron dominate GDDR7 supply, and each supplier must balance GDDR7 output against more lucrative HBM ramps. When allocation shifts toward HBM, GDDR7 availability can tighten quickly, especially for new density points and faster speed bins. Supply tightness then moves into GPU bill-of-materials costs, which pressure workstation vendors, board partners, and system integrators that sell into competitive price bands. This matters most in Asia-Pacific because much of the production base sits there, but the effect spreads globally through GPU launch schedules and component pricing. Until more capacity is qualified and supply planning becomes more stable, the GDDR7 for AI inference GPU market will remain exposed to periodic shortages in key configurations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Density: 16 Gb Leads While Higher Capacities Expand Real Workloads

The 16 GB segment held 63.8% of the GDDR7 for AI inference GPU market size in 2025, which reflected the first wave of Blackwell-based deployments and the wide availability of 16 GB parts across early product launches. This installed base gives 16 GB a durable role because enterprise and cloud refresh cycles do not turn over in a single year. Many buyers are still choosing this tier because it offers a practical balance between throughput, cost, and availability in current platforms. The 32 GB and Above segment is projected to grow at a 44.6% CAGR through 2031, making it the fastest-expanding density band in the GDDR7 for AI inference GPU market. That growth reflects rising demand for larger VRAM pools as inference jobs handle longer context windows, multimodal inputs, and more local model hosting.

The 24 GB segment sits in the middle and plays an important role, raising capacity per channel without requiring a full redesign of the memory subsystem. Samsung said in 2024 that its 24 Gb GDDR7 was built for next-generation AI computing and delivered both higher density and improved power efficiency. That makes 24 GB useful for vendors that need more memory headroom than 16 GB can offer but want a more measured cost step than very high-density configurations. Over time, the GDDR7 for AI inference GPU market is likely to see 16 Gb remain important for volume shipments while 24 Gb and 32 Gb and Above increasingly define the ceiling for premium inference hardware. In practical terms, density is becoming less about specification positioning and more about whether a model can stay resident in local VRAM without pushing data into slower system memory.

By Memory Data Rate: Volume Stays Below 32 Gbps While Faster Tiers Gain Relevance

The Up to 32 Gbps segment captured 81.1% of the GDDR7 for AI inference GPU market in 2025, showing that the early market favored mature, more readily available speed bins. This tier benefits from broader supplier readiness and a better fit with current board designs, which lowers qualification friction for GPU makers. It also supports mainstream inference use cases that need strong throughput but do not require the most aggressive performance profile. The Above 32 Gbps segment is forecast to expand at a 43.9% CAGR through 2031, reflecting rising demand for larger context handling, real-time multimodal processing, and more demanding visual AI workloads. As system designers push for more performance per board, speed is becoming a stronger point of differentiation inside the GDDR7 for the AI inference GPU market.

The shift to faster tiers is not only a matter of memory silicon, because board materials, routing precision, and thermal design also become more demanding as speeds rise. JEDEC finalized the interoperability framework for GDDR7 in March 2024, which helps vendors scale across speed grades within a common standards structure. That standardization reduces single-supplier dependence and supports a clearer roadmap for future products. Even so, the GDDR7 for AI inference GPU industry will likely keep most near-term shipment volume in the Up to 32 Gbps band while faster bins remain concentrated in premium appliances and high-end accelerator designs. The result is a split structure where mature speed grades support volume growth and higher speed grades shape future performance leadership.

By Application: Data Centers Hold the Base While Edge Systems Grow Faster

Data center AI inference accounted for 48.2% of the GDDR7 for AI inference GPU market share in 2025, making it the largest application segment by current revenue. This position reflects the role of hyperscale and cloud operators in making GDDR7-based inference a standard service layer beneath high-cost training clusters. AWS reinforced that pattern in January 2026 by launching EC2 G7e instances with NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs and up to 768 GB of GDDR7 memory per instance. That kind of cloud deployment matters because it makes large memory pools available to enterprise users without requiring them to own the full infrastructure stack. It also supports a two-tier compute model in which GDDR7 handles inference-heavy workloads, while HBM remains concentrated in training systems.

Edge AI inference is the fastest-growing application segment, with a 43.8% CAGR through 2031, pointing to a wider spread of inference beyond centralized facilities. Kontron launched the VX33211 in July 2026, a rugged 3U VPX board with 8 GB GDDR7 and 384 GB/s bandwidth for defense and aerospace AI inference. This kind of product shows why the GDDR7 for AI inference GPU market is gaining traction in compact and mission-specific platforms where packaging and board simplicity matter. Workstation AI and consumer AI acceleration remain part of the mix, but edge growth is stronger because it connects directly to industrial sites, defense systems, and enterprise appliances that need local decision speed. The application structure, therefore, combines a large cloud-led base with a faster edge-led expansion path.

By End-User Industry: Hyperscalers Lead Spending While Enterprise IT Moves Quickly

Cloud and hyperscale data centers held 57.6% share in 2025, giving them the largest purchasing role in the GDDR7 for AI inference GPU market. Their lead comes from direct procurement of accelerator hardware, the ability to deploy inference at scale, and the need to balance training and inference economics inside the same AI estate. This segment is likely to stay dominant in absolute spending even if its share eases as other buyer groups scale. The strongest near-term challenge to hyperscaler concentration comes from enterprise IT, which is projected to grow at 43.4% CAGR through 2031. That pace reflects private inference deployments for proprietary models, local fine-tuning, and workloads that must stay inside controlled environments.

Enterprise adoption is becoming more credible as vendors build denser, more manageable systems for local deployment. Dell said its Pro Precision 7 R1 was designed to bring high GPU density into a compact rack workstation format, which fits engineering and distributed AI environments. AMD also broadened the choice set for this buyer group with the Radeon AI PRO R9700 and ROCm 6.4.1 support for inference and custom model workflows. Government, defense, OEM workstation, automotive, telecom, and industrial buyers add further depth, but they tend to move through longer qualification cycles. That means the GDDR7 for AI inference GPU market is still anchored by hyperscalers today, while enterprise IT is becoming the most important source of incremental diversification.

Geography Analysis

North America accounted for 45.9% of the GDDR7 market share for the AI inference GPU market in 2025, making it the largest regional contributor. The region benefits from the concentration of hyperscale cloud operators, AI chip designers, and enterprise hardware buyers in the United States. It also has strong pull-through from platform operators that can quickly commercialize new inference infrastructure. AWS showed that in January 2026, with its EC2 G7e launch, which brought GDDR7-based inference capacity into a broad enterprise cloud offering. North America also shapes the product roadmap because many system-level decisions by GPU architects, cloud companies, and enterprise software stacks begin there.

Europe represents a smaller but stable part of the GDDR7 for AI inference GPU market, supported by enterprise AI adoption, industrial automation, and public sector interest in more controlled compute environments. The region is well-suited to workstation and appliance deployments where privacy, data handling, and local control matter. Defense demand is also becoming more visible, especially in ruggedized and embedded compute formats. Kontron’s July 2026 launch of the VX33211 for defense and aerospace AI inference reflects that shift toward mission-ready edge platforms. These factors give Europe a measured growth path rather than a sudden volume surge.

Asia-Pacific is the fastest-growing region, with a 43% CAGR through 2031, and it stands out because it combines production leadership with rising end-user demand. Samsung and SK hynix give the region major supply-side weight, while China, Japan, South Korea, and Taiwan add important demand and integration roles. Reuters reported that NVIDIA’s China-focused Blackwell product would use GDDR7 instead of HBM, which shows how policy and regional access conditions are reshaping hardware design in Asia. Micron also positioned GDDR7 for AI PC and hybrid compute workflows in Japan, which points to widening enterprise demand beyond cloud infrastructure alone. Rest of the World remains smaller today, but sovereign AI investment and expanding cloud infrastructure could lift its role later in the forecast period.

Competitive Landscape

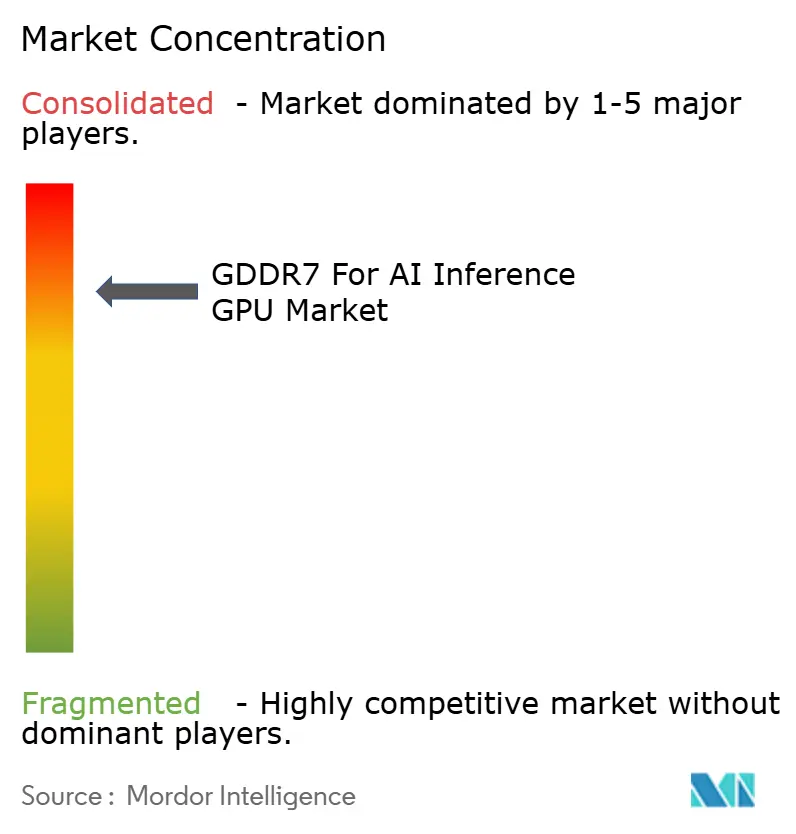

The GDDR7 for AI inference GPU market is moderately concentrated at the memory chip supply layer and more fragmented at the system integration layer. Samsung, SK hynix, and Micron control GDDR7 chip supply, giving the memory side of the value chain a narrow competitive landscape. At the same time, system-level competition is broader because cloud operators, workstation vendors, board makers, and appliance integrators all shape product positioning. This two-level structure means pricing power, qualification leverage, and capacity planning are concentrated at the component level, while configuration and deployment strategies are more diverse downstream. The GDDR7 for AI inference GPU market, therefore, shows high dependence on a few memory suppliers, even though end-user solutions reach the market through many different channels.

Several strategic moves underline how suppliers and platform vendors are trying to strengthen their positions. Samsung announced the industry’s first 24 Gb GDDR7 DRAM for next-generation AI computing and emphasized both higher density and lower power draw, which helps it compete on scale and efficiency at the same time. AMD expanded the professional GPU field in July 2025 with the Radeon AI PRO R9700, giving enterprise users a second major platform path for inference and model workflow tasks. AWS then extended the reach of GDDR7 by packaging it into EC2 G7e cloud instances, which turns a component choice into a scalable service offering. Dell added another angle with the Pro Precision 7 R1, which shows that dense local deployment is becoming a meaningful competitive lane.

Technology support and standards are also shaping rivalry in the GDDR7 for AI inference GPU market. JEDEC’s JESD239 standard gives the market a shared interoperability base, which lowers the risk of a closed ecosystem. Rambus has built a strong position around controller IP and has framed GDDR7 as a long-range option for AI-focused graphics memory scaling. Reuters also showed how export rules can affect product architecture, which means regulation now has a direct influence on competitive outcomes in accelerator design. Over the next few years, winners in the GDDR7 for AI inference GPU market are likely to be the companies that can secure supply, qualify multiple densities and speed tiers, and package those choices into cloud, workstation, and edge systems with clear cost advantages.

GDDR7 For AI Inference GPU Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Kontron launched the VX33211, a 3U VPX GPU board powered by the NVIDIA RTX PRO 2000 Blackwell GPU, integrating 8 GB GDDR7 with 384 GB/s bandwidth for defense and aerospace AI inference including EO/IR sensor processing and real-time intelligence analytics. Designed to SOSA-aligned OpenVPX rugged standards, the launch marked GDDR7's meaningful entry into military-grade inference hardware, a segment previously inaccessible due to GDDR6's lower density and bandwidth.

- April 2026: Micron officially added 24 Gb GDDR7 to its publicly available product catalog, completing the three-vendor qualified supply ecosystem for 3 GB-per-chip GDDR7 alongside Samsung and SK hynix. This supply diversification materially reduces single-source risk for GPU system integrators building next-generation AI inference platforms.

- January 2026: Amazon Web Services launched EC2 G7e instances powered by NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs, delivering up to 768 GB of GDDR7 GPU memory per instance with 1.85x the GPU memory bandwidth of prior-generation G-series instances, making GDDR7-based AI inference accessible to enterprise cloud users at the terabyte scale.

- September 2025: NVIDIA requested Samsung to double its GDDR7 production volume to support the Blackwell B40 AI GPU for the Chinese market. Samsung completed facility expansion within weeks, with mass production imminent as B40 annual demand was estimated at 1 million units, generating USD 384 million in GDDR7 revenue for Samsung based on Morgan Stanley projections.

Global GDDR7 For AI Inference GPU Market Report Scope

The GDDR7 for AI Inference GPU Market Report is Segmented by Memory Density (16 Gb, 24 Gb, and 32 Gb and Above), Memory Data Rate (Up to 32 Gbps, and Above 32 Gbps), Application (Data Center AI Inference, Edge AI Inference, Workstation AI, and More), End-User Industry (Cloud and Hyperscale Data Centers, Enterprise IT, OEM Workstations, Government and Defense, and More), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| 16 Gb |

| 24 Gb |

| 32 Gb and Above |

| Up To 32 Gbps |

| Above 32 Gbps |

| Data Center AI Inference |

| Edge AI Inference |

| Workstation AI |

| Consumer AI Acceleration |

| Cloud and Hyperscale Data Centers |

| Enterprise IT |

| OEM Workstations |

| Government and Defense |

| Other End-user Industries |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Memory Density | 16 Gb | |

| 24 Gb | ||

| 32 Gb and Above | ||

| By Memory Data Rate | Up To 32 Gbps | |

| Above 32 Gbps | ||

| By Application | Data Center AI Inference | |

| Edge AI Inference | ||

| Workstation AI | ||

| Consumer AI Acceleration | ||

| By End-User Industry | Cloud and Hyperscale Data Centers | |

| Enterprise IT | ||

| OEM Workstations | ||

| Government and Defense | ||

| Other End-user Industries | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large is the GDDR7 for AI inference GPU space by 2031?

The GDDR7 for AI inference GPU market size is forecast to reach USD 5.03 billion by 2031, rising from USD 0.89 billion in 2026 at a 41.4% CAGR.

What is driving growth in GDDR7 for AI inference GPU adoption?

Growth is being driven by the move from centralized AI training toward distributed inference, along with the need for higher bandwidth, lower latency, and better system cost control.

Which application area currently leads demand for GDDR7-based AI inference GPUs?

Data center AI inference led with 48.2% share in 2025, supported by cloud and hyperscale deployment of inference-focused GPU capacity.

Which application area is growing the fastest?

Edge AI inference is the fastest-growing application, with a projected 43.8% CAGR through 2031 as deployment spreads into industrial, defense, and enterprise endpoints.

Which end-user group is spending the most on these GPUs?

Cloud and hyperscale data centers held the largest share at 57.6% in 2025, reflecting their role as the main institutional buyers of inference hardware.

Which region is expected to grow the fastest?

Asia-Pacific is projected to expand at 43% CAGR through 2031 because it combines GDDR7 production leadership with strong regional demand for inference hardware.

Page last updated on: