GCC Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

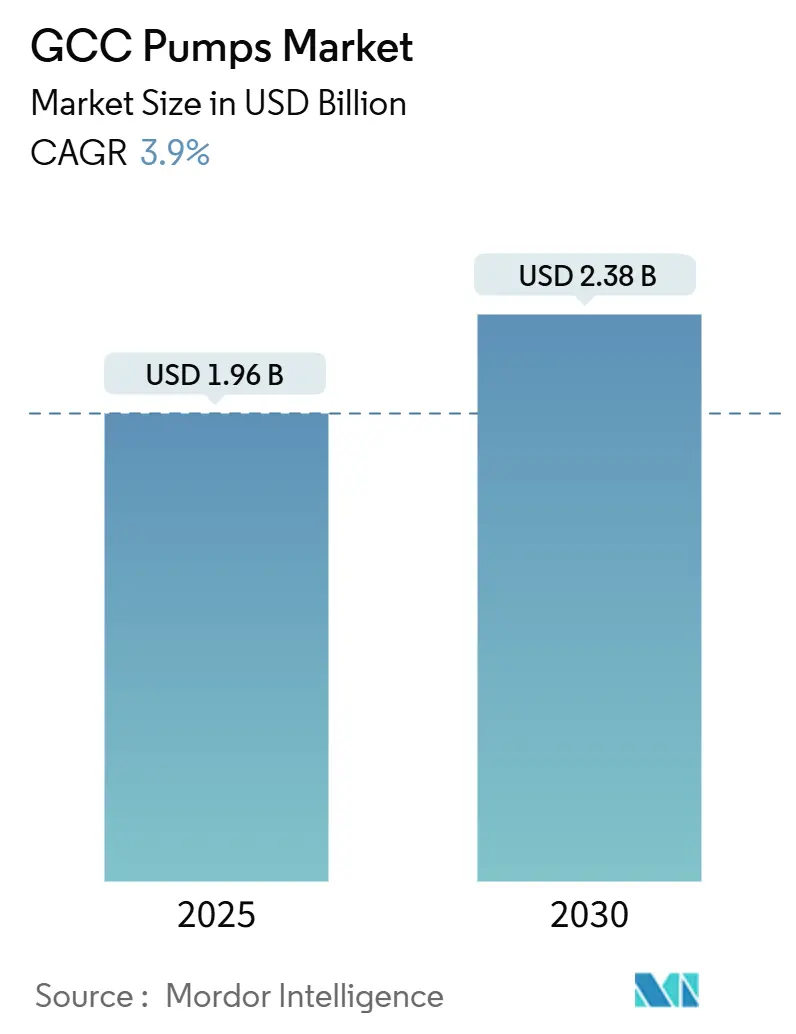

| Market Size (2025) | USD 1.96 Billion |

| Market Size (2030) | USD 2.38 Billion |

| Growth Rate (2025 - 2030) | 3.90% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Pumps Market Analysis by Mordor Intelligence

The GCC Pumps Market size is estimated at USD 1.96 billion in 2025, and is expected to reach USD 2.38 billion by 2030, at a CAGR of 3.9% during the forecast period (2025-2030).

This trajectory mirrors the region’s gradual pivot away from hydrocarbon dependency toward industrial diversification, water-security programs, and low-carbon energy infrastructure. Growing municipal investment in desalination, rising hydrogen and carbon-capture pipelines, and the tightening of energy-efficiency mandates are guiding procurement decisions toward higher-specification equipment. Competitive intensity is shaped by global OEMs offering digital-twin platforms, oilfield-service majors bundling pumps with integrated well packages, and growing regional assemblers exploiting in-country-value rules. Against this backdrop, project developers increasingly evaluate whole-life cost, cybersecurity compliance, and local-content credentials alongside headline purchase price, altering traditional tender dynamics across the GCC pumps market.

Key Report Takeaways

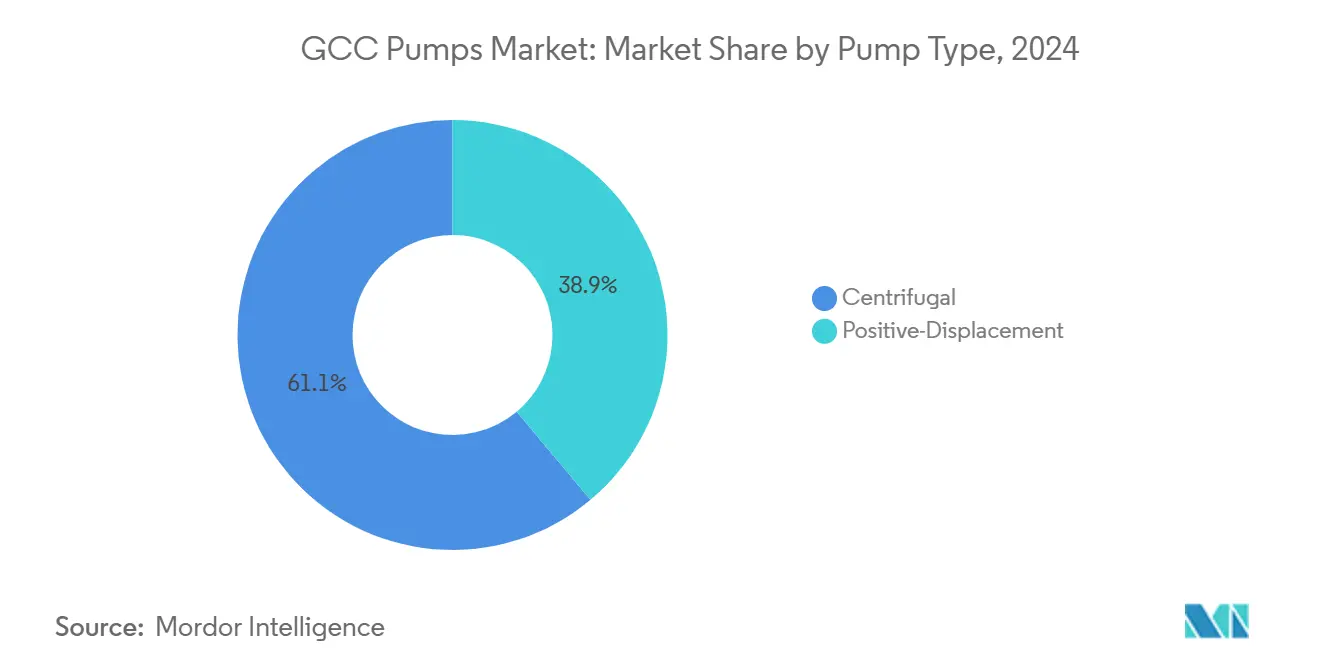

- By pump type, centrifugal units held 61.1% of the GCC pumps market in 2024 and are advancing at a 4.7% CAGR to 2030.

- By drive technology, electric-motor systems accounted for 68.5% of the GCC pumps market size in 2024, whereas solar-powered variants constitute the highest 10.1% CAGR growth path.

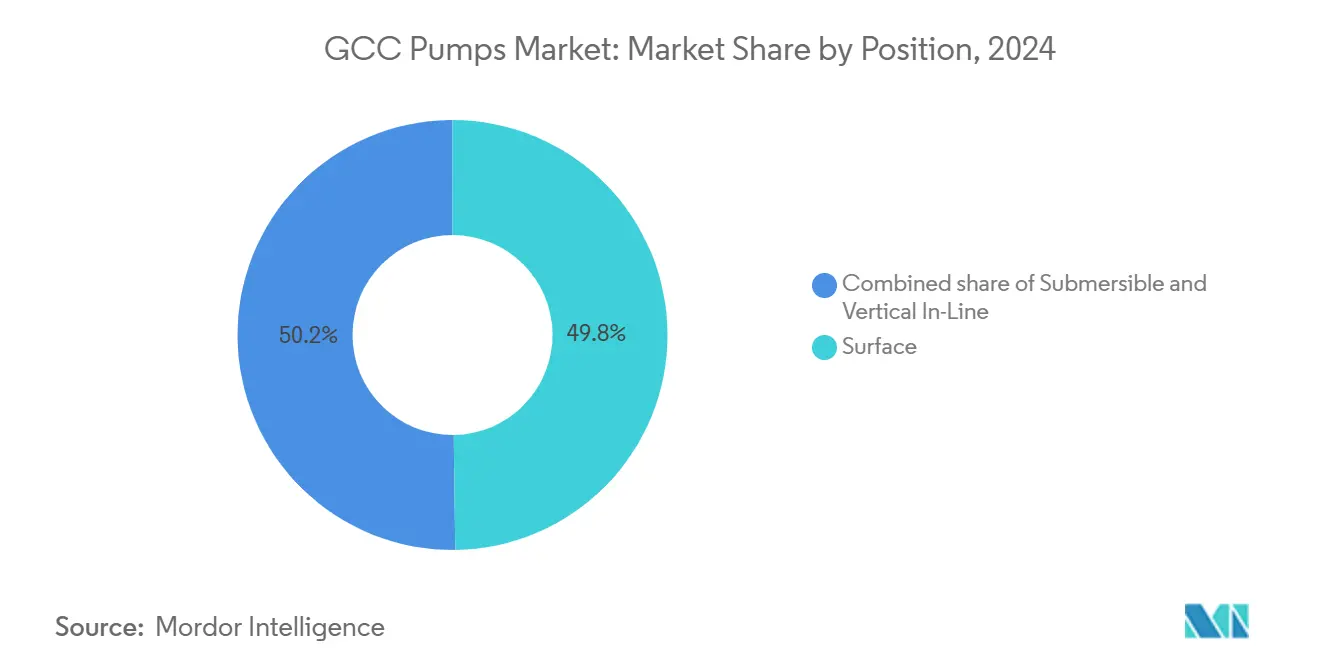

- By position, surface installations captured 49.8% of the GCC pumps market in 2024, yet submersible solutions are expanding at a 6.3% CAGR to 2030.

- By application, water and wastewater represented 33.4% of the GCC pumps market size in 2024 and continue to expand at a 4.5% CAGR throughout the period.

- By geography, the United Arab Emirates led with 63.4% of GCC pumps market share in 2024, while Oman is forecast to post the region’s fastest 5.9% CAGR through 2030.

GCC Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrialisation and large infrastructure pipelines | +1.2% | Saudi Arabia, UAE (core); Qatar, Oman (secondary) | Medium term (2-4 years) |

| Expanding upstream and midstream oil-and-gas projects | +0.9% | Saudi Arabia, UAE, Kuwait, Qatar | Short term (≤ 2 years) |

| Intensifying desalination and wastewater reuse investments | +1.4% | GCC-wide, with concentration in Saudi Arabia, UAE | Long term (≥ 4 years) |

| Mandates for smart and energy-efficient pumping systems | +0.7% | Saudi Arabia, UAE (regulatory leadership); spill-over to Kuwait, Bahrain | Medium term (2-4 years) |

| In-country-value programmes boosting local pump assemblies | +0.5% | Saudi Arabia (IKTVA), UAE (ICV); limited adoption in Qatar, Oman | Short term (≤ 2 years) |

| Hydrogen and CCUS pilot pipelines needing specialist pumps | +0.6% | Saudi Arabia (NEOM, Jubail); UAE (al-Reyadah); Oman (green hydrogen projects) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Industrialisation and Large Infrastructure Pipelines

Multi-billion-dollar mega-projects such as NEOM, Qiddiya, the Red Sea Project, and the Dubai 2040 Urban Master Plan demand extensive pumping systems spanning district cooling loops, potable-water grids, and wastewater networks. Compressed construction schedules favor suppliers with in-region assembly and pre-qualified product catalogs that meet Gulf technical standards. Growing use of design-build-operate contracts pushes lifecycle risk onto EPC consortia, stimulating preference for premium-efficiency motors and predictive-maintenance sensors that lower the total cost of ownership. Scorching summer temperatures above 45 °C in Gulf cities reinforce the need for reliable HVAC circulation pumps, while sprawling metro extensions install variable-speed drives to satisfy green-building codes. As procurement teams weigh energy-performance savings against budget limits, manufacturers that bundle finance and long-term service agreements win share in the GCC pumps market.

Expanding Upstream and Midstream Oil-and-Gas Projects

ADNOC’s USD 25 billion gas-processing build-out, Saudi Aramco’s Jafurah unconventional gas development, and Qatar’s North Field LNG expansion depend on multistage centrifugal pumps and cryogenic units engineered for sour-service conditions. Pipeline extensions such as the UAE’s Habshan–Fujairah crude link deploy mainline pumps with real-time vibration monitoring to avert unplanned shutdowns that can halt refinery feedstock. Digital-twin models simulate hydraulic transients, optimizing staging and trimming energy use by up to 15% relative to fixed-speed layouts. Kuwait’s enhanced oil-recovery programs inject high-salinity seawater, creating demand for super-duplex materials that withstand chloride stress-corrosion. As national oil companies prioritize single-provider accountability, oilfield-service conglomerates bundle downhole pumps with drilling and completion services, gaining cross-segment momentum inside the GCC pumps market.[1]Staff Report, “Digital Twins Cut Energy by 15%,” Bloomberg, bloomberg.com

Intensifying Desalination and Wastewater Reuse Investments

Owning roughly 60% of global desalination capacity, the region continues to commission high-pressure reverse-osmosis plants that run feed pumps at 70 bar. Abu Dhabi’s Saadiyat Island facility integrates energy-recovery devices to slash specific energy consumption below 3 kWh per cubic meter. Saudi Arabia’s regulation calling for 70% effluent reuse by 2030 accelerates retrofits of municipal plants with non-clog submersible pumps and cloud-linked diagnostics. Brine streams laden with abrasive solids stimulate demand for duplex-steel and ceramic-coated pump casings. As groundwater depletion intensifies, regulators fast-track wastewater-to-irrigation projects, keeping this end-use the fastest-growing slice of the GCC pumps market.[2]Staff Report, “Desalination Capacity Expansion in GCC,” Financial Times, ft.com

Mandates for Smart and Energy-Efficient Pumping Systems

Regional standards bodies now require IE3 or IE4 motors, pushing OEMs to incorporate permanent-magnet designs and advanced variable-frequency drives. Smart pumps embedded with IoT sensors stream flow, temperature, and vibration data into analytics platforms that cut unplanned downtime by up to 30%. Utilities link pump efficiency scores to tariff incentives, rewarding operators that flatten peak-demand curves. Artificial-intelligence algorithms detect cavitation, seal wear, and bearing fatigue weeks ahead, lowering spare-parts inventory and extending overhaul intervals. These connectivity gains, however, enlarge cyber-attack surfaces, prompting contractual insistence on IEC 62443 compliance across the GCC pumps market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and opex for advanced pump systems | -0.8% | GCC-wide, with acute sensitivity in Bahrain, Oman | Short term (≤ 2 years) |

| Raw-material price volatility (stainless, super-duplex) | -0.6% | Global supply-chain impact; procurement delays in Saudi Arabia, UAE | Medium term (2-4 years) |

| Cyber-security risks to connected pump networks | -0.3% | Saudi Arabia, UAE (high digitalization); emerging concern in Kuwait, Qatar | Medium term (2-4 years) |

| Surge in pump-rental and service outsourcing dampening new sales | -0.5% | UAE, Saudi Arabia (construction-heavy markets); limited in oil-and-gas capex | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex and Opex for Advanced Pump Systems

Premium-efficiency pumps add 40% – 60% to upfront cost, creating hurdles for fiscally constrained utilities despite three- to five-year paybacks from lower energy draw. Smart-pump maintenance demands technicians skilled in PLC programming and Ethernet protocols, raising service budgets. Bahrain and Oman, under tighter fiscal envelopes, often default to minimum-spec equipment, prolonging legacy inefficiencies. Energy-performance contracting offers off-balance-sheet financing but remains underutilized due to complexity and awareness gaps. This spending hesitation trims immediate addressable volumes in the GCC pumps market.

Raw-Material Price Volatility (Stainless, Super-Duplex)

Nickel and molybdenum price spikes exceeding 20% during 2024 compressed OEM margins on corrosion-resistant pump models critical for desalination and petrochemical service. Fixed-price contracts forced suppliers to absorb cost inflation, while pass-through clauses triggered customer deferrals. Lead times on super-duplex castings stretched to 12 months, jeopardizing project schedules. Exploratory work on composites and ceramic coatings continues, yet code-compliance hurdles delay commercial substitution. Currency mismatches between dollar-denominated Gulf contracts and euro- or yuan-based alloy invoices add hedging costs, tempering momentum in the GCC pumps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Units Sustain Lead Through Operational Simplicity

Centrifugal designs captured 61.1% of the GCC pumps market share in 2024 and are projected to grow at a 4.7% CAGR to 2030. Their suitability for high-volume, moderate-head duties in water transfer, HVAC circulation, and crude-oil boosting underpins this lead. Rapid impeller replacement during scheduled turnarounds curbs downtime in continuous process plants. Multistage centrifugal variants power reverse-osmosis trains, and magnetic-drive designs gain traction in zero-leakage pharmaceutical settings. In contrast, positive-displacement pumps satisfy niche demands such as chemical dosing in enhanced oil recovery, where constant-flow accuracy is paramount. Elevated maintenance intensity and abrasion sensitivity restrict their wider uptake, keeping centrifugal solutions the backbone of the GCC pumps market.

Centrifugal’s broad installed base spurs aftermarket revenue for seals, bearings, and efficiency upgrades, creating recurring cash flows for OEMs and distributors. Drop-in retrofit kits with variable-speed drives raise hydraulic efficiency by 15% without footprint changes, appealing to upgrade projects inside desalination and district-cooling plants. Meanwhile, progressive-cavity pumps remain vital for viscous-fluid handling in petrochemical complexes, yet their share is capped by stator replacement costs. Composite impeller developments aim to prolong life in sand-laden water wells, but qualification cycles slow mass rollout. Overall, centrifugal technology’s balance of reliability, cost, and adaptability secures its primary role in the GCC pumps market.

By Drive Technology: Solar Surge Outpaces Electric Dominance

Electric-motor systems commanded 73.1% of installations in 2024, anchoring their primacy in the GCC pumps market size. Grid reliability and historically subsidized tariffs encourage electricity-driven equipment, while variable-frequency drives improve energy efficiency by 20% – 40%. Diesel and gas engines persist in remote oilfields, yet growing carbon-pricing rules and fuel-cost exposure temper new orders. Solar-powered pumps are expanding at 10.1% annually, leveraging dropping photovoltaic module prices and national clean-energy targets. Saudi Arabia’s plan for 50% renewables in its power mix by 2030 incentivizes utilities to deploy off-grid solar pumping stations in desert communities.

Hybrid arrays combining solar photovoltaics with battery storage drive adoption in irrigation and remote pipeline leakage-management schemes. Magnetically coupled drive systems eliminate seals and fugitive emissions, winning share in chemicals and pharmaceuticals; however, torque limitations restrict unit power to about 150 kW. Permanent-magnet synchronous motors achieve IE5 efficiencies, yet their higher rare-earth content exposes cost to dysprosium price swings. As carbon accounting gains regulatory bite, drive-type selection increasingly weighs life-cycle emissions, favoring renewable hybrids that promise lower total cost of ownership inside the GCC pumps market.

By Position: Submersibles Gain on Offshore and Agricultural Expansion

Surface pumps retained a 49.8% share in 2024 for ease of in-situ maintenance at pipeline boosters and cooling towers. Submersible demand is climbing 6.3% annually, a response to 500 m-plus aquifer drawdowns in Saudi farms and offshore injection wells in ADNOC fields. Their retrieval costs are high, yet cavitation-free deep-set operation justifies total-cost math for operators.

Vertical in-line units continue as retrofit darlings, shaving 50% floor area in space-constrained mechanical rooms, but shaft-alignment vigilance is mandatory to avoid vibration-induced failures.

By Application: Water Infrastructure Leads, Diverse End-Uses Sustain Breadth

Water and wastewater installations accounted for 33.4% of 2024 demand and are forecast to expand at a 4.5% CAGR, the swiftest among end uses. Reverse-osmosis plants use high-pressure centrifugal feed pumps, and sewage treatment upgrades deploy clog-resistant submersibles coupled with cloud-linked diagnostics. Desalination brine-energy-recovery systems channel captured pressure into booster pumps, trimming power bills appreciably. Oil and gas remain a stable buyer group, needing API 610-compliant units in crude pipelines, amine circulation, and refinery hydrotreaters, reinforced by Saudi Aramco’s carbon-capture plans.

Chemical and petrochemical complexes favor super-duplex or fluoropolymer-lined pumps that shrug off acids and solvents. HVAC and building-services pumps serve district-cooling networks across Gulf megacities, and their vertical in-line orientation preserves valuable real estate in service basements. Power-generation projects, especially concentrated solar power plants, adopt molten-salt transfer pumps capable of 550 °C duty, carving a specialized yet visible niche. Mining, food-processing, and pharmaceuticals form smaller segments but demand sanitary or abrasion-resistant pumps, diversifying the customer base of the GCC pumps market.

Geography Analysis

The GCC pumps market finds its epicenter in the United Arab Emirates, capturing 63.4% of 2024 demand. ADNOC’s USD 25 billion gas-expansion ties, Saadiyat Island’s reverse-osmosis plant, and sprawling district-cooling grids across Dubai’s business districts ensure a deep order pipeline. Local-content rules prompted Flowserve, Xylem, and Sulzer to inaugurate assembly cells in Dubai Industrial City, cutting lead times on API-610 frames to six weeks.[3]Staff Report, “Dubai Industrial City Hosts New Pump Hubs,” Bloomberg, bloomberg.com

Saudi Arabia ranks second, motivated by NEOM’s hydrogen hub, Jubail’s CCUS complex, and the National Water Company’s USD 3.2 billion network overhaul. IKTVA’s 70% domestic-value rule shifted Grundfos and KSB to a joint venture with Alkhorayef Petroleum near Dammam, underlining how localization is now a prerequisite for major tenders.[4]Staff Report, “IKTVA Drives Localization Partnerships,” Gulf News, gulfnews.com

Oman is the forecast growth champion, clocking a 5.9% CAGR to 2030. Eight Hydrom-aligned hydrogen projects, Duqm port expansion, and LNG nameplate lift to 15.2 million tpa demand electrolysis feed pumps, cryogenic compression skids, and cooling-water pumps rated for high salinity. Qatar’s North Field LNG debottlenecking and Bahrain’s desalination doubling complete the regional mosaic, with each niche contributing incremental tonnage to the GCC pumps market.

Competitive Landscape

Global OEMs, Grundfos, Flowserve, Sulzer, Xylem, and KSB, anchor the upper tier of the GCC pumps market, leveraging broad catalogs certified to API, ISO, and energy-efficiency standards. Digital-twin platforms bundled with IoT sensors yield predictive-maintenance insights that tie customers into multi-year service contracts. Oilfield-service giants Baker Hughes, Schlumberger, and Halliburton package electric submersible pumps within integrated well-completion offerings, capturing high-margin aftermarket sales and deepening relationships with national oil companies.

Regional assemblers such as Alkhorayef Petroleum and Emirates Industrial Pumps ride in-country-value mandates to gain share, assembling imported wet-end skids locally and offering rapid turnaround on spare parts. White-space opportunities cluster around hydrogen and carbon-capture pipelines, where high-pressure, low-molecular-weight fluid handling remains nascent. Niche firms like Klaus Union and Hermetic-Pumpen exploit zero-leakage magnetically driven products to serve chemical micro-markets seeking strict environmental compliance, unsettling incumbents through focused innovation.

Technology convergence is redrawing competitive maps. Suppliers embedding robust cybersecurity, IEC 62443-certified controllers, and AI diagnostic suites meet rising contractual thresholds from water utilities and oil majors. The shift toward pump-rental and performance-based service contracts compresses up-front sales but stabilizes revenue streams over asset lifecycles, rewarding vendors with fleet-management expertise. M&A remains tactical, aimed at filling service-network gaps or acquiring niche material science capabilities rather than restructuring the broader GCC pumps market.

GCC Pumps Industry Leaders

Grundfos

Flowserve

Sulzer

Xylem

KSB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Wilo SE completed the doubling of its Dubai manufacturing facility capacity, positioning the company to serve growing regional demand while establishing an export hub for Middle East and Africa markets.

- December 2024: ACWA Power secured a USD 693 million contract for the Hamriyah Independent Water Project in Sharjah, featuring 410,000 m³ per day desalination capacity that will require hundreds of specialized pumps.

- September 2024: Alkhorayef Water and Power Technologies won a USD 59 million contract for Dammam sewage treatment plant expansion, raising capacity to 125,000 m³ per day and necessitating comprehensive pump system upgrades.

- September 2024: Taqa Water Solutions allocated USD 2.7 billion for 80 water infrastructure projects across Abu Dhabi, driving future pump demand.

GCC Pumps Market Report Scope

Pumps, mechanical devices, convert energy to elevate, transport, or compress fluids, be it liquids or gases. By transforming mechanical energy into hydraulic or pneumatic energy, pumps generate a pressure difference, propelling fluids from lower to higher pressure zones.

The GCC pumps market is segmented by pump type, drive technology, position, application, and geography. By pump type, the market is segmented into centrifugal and positive-displacement. By drive technology, the market is segmented into electric motor, diesel/gas engine, solar/renewable, and magnetically-driven/sealless. By position, the market is segmented into surface, submersible, and vertical in-line. By application, the market is segmented into water and wastewater, chemical and petrochemical, HVAC and building services, oil and gas, food and beverage, mining and metals, power generation, pharmaceuticals and biotech, and others. The report also covers the market sizes and forecasts for the GCC pumps market across major countries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Centrifugal |

| Positive-Displacement |

| Electric Motor |

| Diesel/Gas Engine |

| Solar/Renewable |

| Magnetically-Driven/Sealless |

| Surface |

| Submersible |

| Vertical In-Line |

| Water and Wastewater |

| Chemical and Petrochemical |

| HVAC and Building Services |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Food and Beverage |

| Mining and Metals |

| Power Generation (Thermal, Nuclear, Renewables) |

| Pharmaceuticals and Biotech |

| Others |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| By Pump Type | Centrifugal |

| Positive-Displacement | |

| By Drive Technology | Electric Motor |

| Diesel/Gas Engine | |

| Solar/Renewable | |

| Magnetically-Driven/Sealless | |

| By Position | Surface |

| Submersible | |

| Vertical In-Line | |

| By Application | Water and Wastewater |

| Chemical and Petrochemical | |

| HVAC and Building Services | |

| Oil and Gas (Upstream, Midstream, Downstream) | |

| Food and Beverage | |

| Mining and Metals | |

| Power Generation (Thermal, Nuclear, Renewables) | |

| Pharmaceuticals and Biotech | |

| Others | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman |

Key Questions Answered in the Report

What CAGR is forecast for the GCC pumps market between 2024 and 2030?

The market is set to grow at 3.9% CAGR, adding USD 520 million in incremental revenue.

Which country currently leads spending?

The United Arab Emirates held 63.4% of 2024 demand owing to large ADNOC gas and district-cooling projects.

Why are solar-powered pumps expanding so quickly?

Falling PV prices and clean-energy mandates give solar-driven sets a forecast 10.1% CAGR, the fastest among drive types.

Which pump type remains dominant?

Centrifugal models retain a 61.1% share because they suit high-flow applications and offer easier maintenance.

How do local-content rules affect suppliers?

IKTVA and ICV schemes force OEMs to assemble and source within the region, helping regional firms secure contract preference.

What is the main restraint on adopting smart pumps?

Premium-efficiency models cost 40% – 60% more up front and demand specialized maintenance skills, stretching budgets for smaller utilities.

Page last updated on: