GCC Gold Jewelry Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.81 Billion |

| Market Size (2026) | USD 17.23 Billion |

| Market Size (2031) | USD 20.55 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Gold Jewelry Market Analysis by Mordor Intelligence

The GCC gold jewelry market was valued at USD 16.81 billion in 2025 and is estimated at USD 17.23 billion in 2026, reaching USD 20.55 billion by 2031, growing at a CAGR of 3.59% during 2026–2031. The market is driven by the enduring cultural importance of gold jewelry in weddings, religious festivals, and gifting traditions, which ensures stable demand across the region. Growth is further supported by increasing preference for personalized and lightweight jewelry, expansion of luxury retail and tourism-driven purchases, and the rising adoption of omnichannel retail platforms offering digital customization and virtual shopping experiences. In addition, gold's dual role as both a fashion accessory and a long-term store of value continues to strengthen consumer demand, while ongoing investments in premium retail formats, responsible sourcing, and advanced jewelry manufacturing technologies are supporting sustained market expansion across the GCC.

Key Report Takeaways

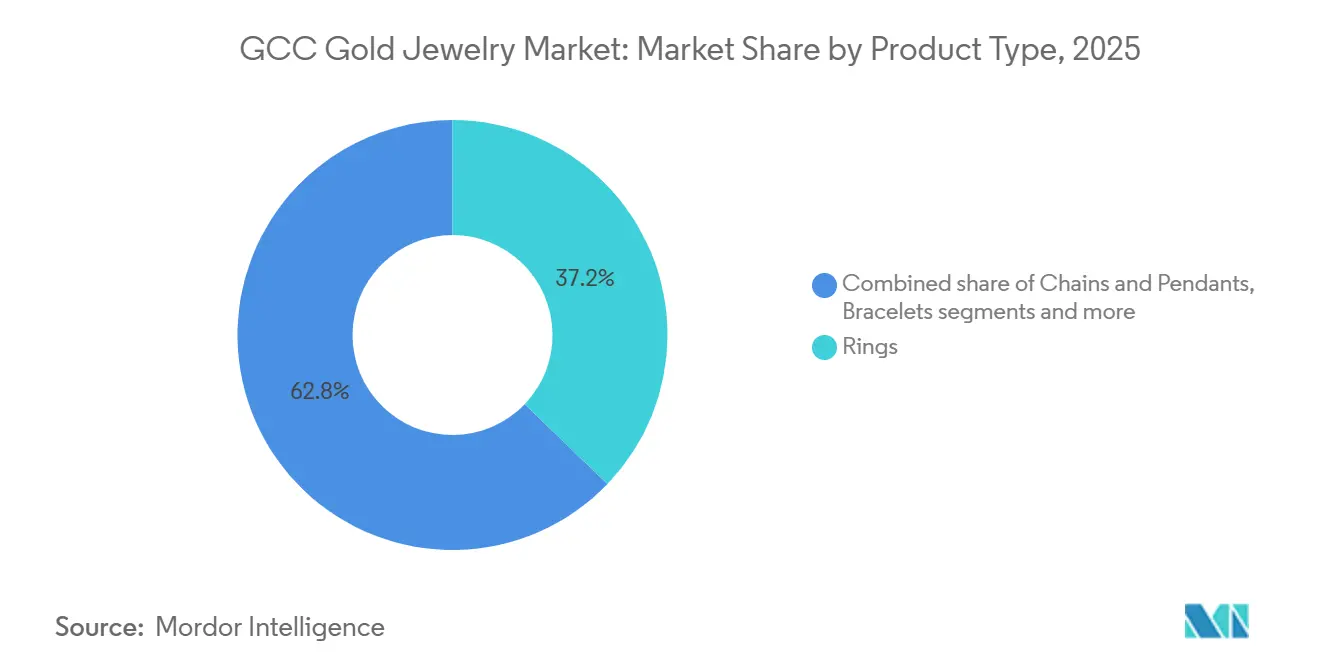

- By product type, rings led with 33.46% revenue share in 2025, while chains and pendants are forecast to expand at 4.81% CAGR through 2031.

- By karat or purity, 22 karat held 54.53% share in 2025, while 18 karat recorded the highest projected CAGR at 3.78% through 2031.

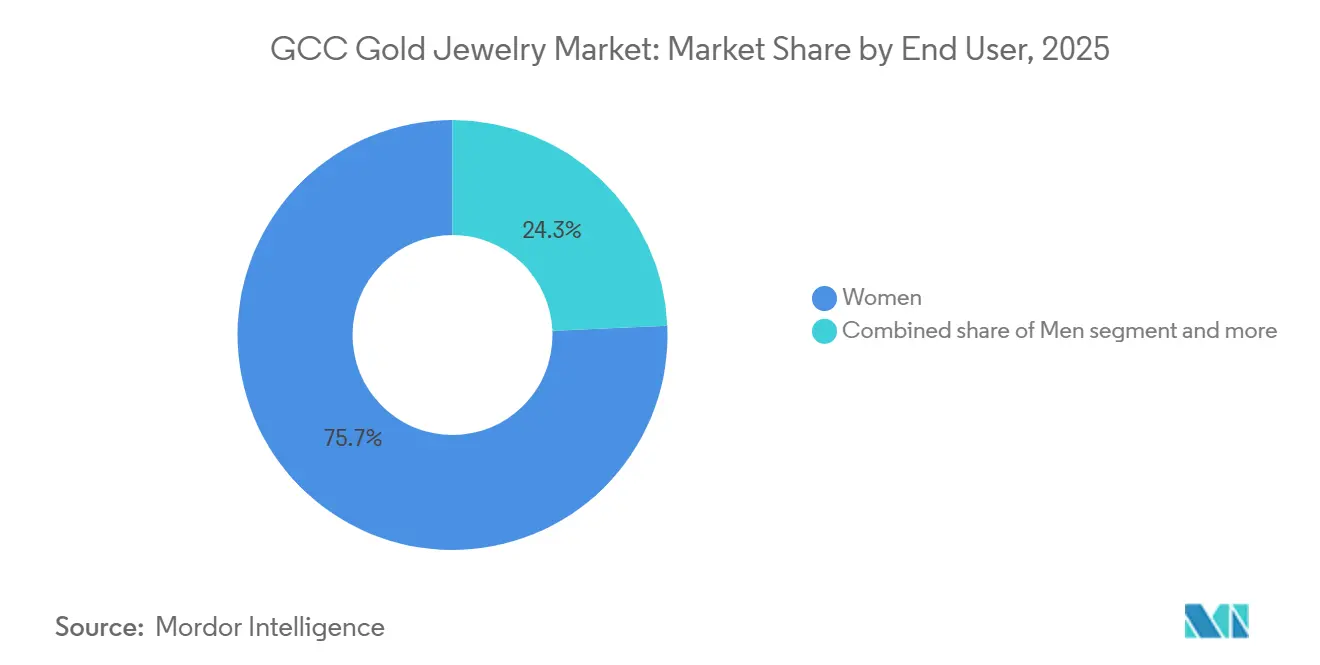

- By end user, women accounted for 75.69% share in 2025, while men are advancing at the fastest CAGR of 4.93% through 2031.

- By distribution channel, offline retail stores captured 84.55% share in 2025, while online retail stores are projected to grow at 5.45% CAGR through 2031.

- By geography, Saudi Arabia held 30.35% share of revenue in 2025, while the United Arab Emirates is expected to post the fastest CAGR at 5.09% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Gold Jewelry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural significance of gold jewelry in weddings and traditional celebrations | +0.8% | GCC-wide, concentrated in Saudi Arabia, Oman, and Kuwait | Long term (≥ 4 years) |

| Increasing adoption of personalized and customized gold jewelry | +0.5% | United Arab Emirates and Saudi Arabia as primary hubs | Medium term (2–4 years) |

| Gold jewelry's role as a dual-purpose asset | +0.7% | GCC-wide, with spill-over to expatriate communities | Long term (≥ 4 years) |

| Tourism-led luxury retail spend in Dubai and Saudi Arabia | +0.6% | United Arab Emirates and Saudi Arabia, with emerging gains in Qatar and Bahrain | Medium term (2–4 years) |

| Localized collections for Arab and expatriate taste profiles | +0.3% | United Arab Emirates, Saudi Arabia, Kuwait | Short term (≤ 2 years) |

| Popularity of ethically sourced and responsibly produced gold | +0.2% | United Arab Emirates and Saudi Arabia, with early gains in Qatar and Bahrain | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cultural significance of gold jewelry in weddings and traditional celebration

Gold jewelry remains deeply embedded in GCC wedding traditions and religious celebrations, creating a structural source of demand that is relatively resilient to gold price fluctuations. Unlike discretionary fashion purchases, bridal sets, engagement jewelry, and ceremonial gifts are considered essential components of weddings, Eid, Ramadan, and other family occasions, ensuring consistent purchasing activity throughout the year. Consumers often adjust jewelry weight or design preferences rather than postpone purchases, providing the market with a stable demand base. The significance of this cultural demand is reflected in the growing scale of industry events such as the Saudi Arabia Jewellery Exposition (SAJEX) 2025, held in September 2025, which brought together over 100 exhibitors across 200 booths and attracted more than 2,000 international trade buyers [1]Source: Saudi Arabia Jewelry Exposition (SAJEX), "The Ultimate B2B Jewellery Destination", gjepc.org/sajex. This highlights the region's strong bridal and traditional jewelry ecosystem while creating new opportunities for manufacturers and retailers to showcase culturally relevant collections.

Increasing adoption of personalized and customized gold jewelry

The growing adoption of personalized and customized gold jewelry is transforming the GCC market from a traditional commodity-based purchase into a design-led, value-added retail experience. Rather than competing solely on gold purity or weight, jewelry brands are increasingly differentiating themselves through bespoke craftsmanship, allowing consumers to create unique pieces that reflect individual identities, family heritage, and special occasions. Demand is rising for custom name necklaces, engraved pendants, initials, signet rings, zodiac motifs, and made-to-order bridal jewelry, particularly among younger consumers seeking exclusive designs. At the same time, retailers are integrating AI-powered jewelry design tools, 3D visualization, CAD/CAM technology, and digital customization platforms, enabling customers to preview, modify, and personalize jewelry before production.

Gold jewelry's role as a dual-purpose asset

Gold jewelry serves a dual role in the GCC market, functioning as both a fashion accessory and a store of value. This makes it a distinctive category within the luxury goods market. Consumers increasingly view gold purchases as assets that can be worn, gifted, exchanged, or resold while retaining intrinsic value, supporting demand across both ceremonial and everyday jewelry categories. This dual-purpose appeal has prompted retailers to integrate investment-oriented products with traditional jewelry offerings, creating a broader precious metals portfolio. For example, in December 2025, Joyalukkas partnered with Emirates Gold to introduce certified 24-karat gold bars across its retail network, enabling customers to purchase investment-grade gold from jewelry stores alongside conventional jewelry collections. This convergence of adornment and investment is encouraging retailers to redesign store formats, loyalty programs, and customer engagement strategies to address both motivations rather than treating them as separate purchasing segments.

Tourism-led luxury retail spend in dubai and saudi arabia

The expansion of tourism-driven luxury retail is strengthening demand for gold jewelry across the GCC, particularly in Dubai and Saudi Arabia, where international visitors contribute significantly to premium jewelry sales. Gold jewelry is frequently purchased by tourists as a luxury souvenir, an investment product, and a tax-efficient high-value purchase, encouraging retailers to expand flagship stores, multilingual sales services, and exclusive collections tailored to international buyers. Airports, luxury shopping malls, and established gold retail districts have become key sales channels, enabling brands to capture demand from both leisure and business travelers. According to the Dubai Department of Economy and Tourism, Dubai welcomed 2.00 million overnight visitors in January 2026, an increase of 3% compared with January 2025, reflecting sustained growth in international tourism that continues to support footfall across luxury retail destinations, including gold jewelry stores [2]Source: Dubai Department of Economy and Tourism, "Tourism Performance Report January 2026", dubaidet.gov.ae.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit risk and hallmarking compliance costs | −0.4% | GCC-wide; highest risk in e-commerce channels and informal souks | Short term (≤ 2 years) |

| Dependence on imported finished jewelry and inputs | −0.3% | United Arab Emirates (78% of import value), Kuwait, Qatar | Medium term (2–4 years) |

| Gold price volatility and inventory margin compression | −0.6% | GCC-wide | Short to medium term |

| Intense price transparency and low switching costs in mass gold | −0.3% | United Arab Emirates, Saudi Arabia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit risk and hallmarking compliance costs

The growing prevalence of counterfeit gold jewelry and rising hallmarking compliance costs present significant challenges for the GCC gold jewelry market, particularly for small and mid-sized retailers. Meeting stricter requirements for purity testing, hallmarking, traceability, and product certification demands continuous investment in quality assurance systems, certified sourcing, documentation, and regulatory audits, increasing operational costs across the value chain. While these measures strengthen consumer confidence, they also raise barriers for retailers with limited financial and technical resources. The persistence of counterfeit products further underscores the need for regulatory enforcement. For example, in August 2025, Saudi Arabia's Ministry of Commerce shut down a foreign e-commerce platform selling copper-coated counterfeit gold bullion at nearly half the prevailing market value, citing violations of the Kingdom's E-Commerce Law and its executive regulations [3]Source: The Ministry of Commerce, "Blocks a Non-Compliant Foreign E-Store for Selling Counterfeit Gold Bullion", mc.gov.sa.

Dependence on imported finished jewelry and inputs

The GCC gold jewelry market is highly dependent on imported finished jewelry, gemstones, specialized components, and manufacturing inputs, making the industry vulnerable to international supply chain disruptions and procurement delays. Many retailers rely on overseas suppliers for diamond-studded jewelry, luxury designer collections, precision findings, clasps, and colored gemstones that are not produced at sufficient scale within the region. This dependence can result in longer replenishment cycles, limited inventory availability, and delays in launching new collections when global logistics or sourcing conditions are disrupted. Additionally, fluctuations in shipping schedules, import procedures, and cross-border sourcing requirements increase operational complexity for jewelry manufacturers and retailers, limiting supply chain flexibility and slowing the introduction of new products into GCC markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rings Define Bridal Value, Chains Capture Gifting Growth

Rings accounted for 33.46% of the GCC gold jewelry market in 2025. The segment dominates because rings are purchased across multiple occasions rather than for a single purpose, creating consistently high replacement and repeat purchase cycles. Unlike necklaces or bracelets, consumers often own multiple rings for daily wear, formal events, religious occasions, engagements, and weddings, resulting in higher unit sales. The category also benefits from broad design flexibility, allowing manufacturers to offer products across different gold purities, weights, price points, and fashion preferences without significantly altering production processes. In addition, rings require comparatively lower gold content than larger jewelry pieces, enabling jewelers to introduce a wider variety of collections and refresh inventories more frequently.

Chains and pendants are the fastest-growing product type, projected to expand at a CAGR of 4.81% during 2026–2031. Growth is driven by their versatility and styling flexibility, as consumers increasingly prefer jewelry that can be worn individually or layered with other pieces for different occasions. The segment also benefits from frequent product innovation through interchangeable pendants, symbolic motifs, initials, religious charms, and gemstone additions, allowing consumers to personalize jewelry without replacing the entire chain. Furthermore, lightweight chain designs and detachable pendant collections enable brands to introduce new designs quickly while encouraging repeat purchases of complementary pieces.

By Karat/Purity: 22 Karat Commands Cultural Loyalty, 18 Karat Gains Urban Ground

The 22 karat purity segment held 54.53% of the GCC gold jewelry market in 2025. Its dominance is supported by its balance between high gold purity and structural strength, allowing manufacturers to produce both traditional handcrafted jewelry and contemporary designs without compromising durability. The segment serves as the industry benchmark for bridal sets, bangles, necklaces, rings, and ceremonial collections, resulting in extensive product availability across virtually every organized jewelry retailer in the GCC. Its standardized use throughout the regional jewelry ecosystem enables efficient sourcing, manufacturing, hallmarking, inventory management, and resale, further strengthening consumer preference. In addition, 22K gold offers a distinctive rich yellow appearance widely associated with premium quality and authenticity, making it the preferred purity for heritage-inspired collections and heirloom jewelry.

The 18 karat segment is projected to grow at a CAGR of 3.78% during 2026–2031. The segment is expanding as jewelry manufacturers increasingly prioritize design innovation over traditional purity preferences. Its higher alloy content provides greater hardness, enabling intricate settings, slimmer profiles, articulated links, and complex geometric designs that are difficult to achieve with 22K or 24K gold. This makes 18K the preferred choice for diamond jewelry, gemstone-studded collections, contemporary luxury pieces, and precision-crafted designer products. The segment also supports a wider range of finishes, including white gold, rose gold, and mixed-metal combinations, allowing brands to diversify collections and respond to evolving fashion trends. Furthermore, its durability makes it well suited for everyday wear, encouraging brands to expand premium lifestyle collections and increasing its adoption across modern retail formats, supporting its position as the fastest-growing purity segment.

By End User: Women Underpin Market Structure, Men Present Structural Upside

Women accounted for 75.69% of the GCC gold jewelry market in 2025. This dominance is driven by the breadth and frequency of jewelry ownership, as women typically purchase and receive multiple product categories throughout different stages of life. Unlike other end-user groups, women generate demand across both everyday and occasion-specific collections, creating continuous product replacement and wardrobe expansion. Jewelry brands therefore dedicate the majority of their product portfolios, seasonal launches, exclusive collections, and design innovations to women's preferences, resulting in greater product variety and faster collection refresh cycles. In addition, women's jewelry spans a wide spectrum of styles, ranging from traditional handcrafted sets to contemporary minimalist pieces and high-end designer collections, enabling retailers to address diverse fashion preferences within a single consumer segment.

Men are the fastest-growing end-user category, projected to expand at a CAGR of 4.93% during 2026–2031. This growth is being fueled by the rapid diversification of men's jewelry collections beyond conventional designs, with manufacturers introducing minimalist chains, signet rings, bracelets, pendants, and mixed-material products specifically tailored to male consumers. Unlike traditional collections, modern men's jewelry emphasizes versatility, allowing products to transition between casual, business, and formal wear. Luxury brands are also expanding dedicated men's product lines, collaborating with designers and celebrities to introduce contemporary collections that appeal to younger consumers seeking a distinctive personal style. Furthermore, innovations in lightweight construction, textured finishes, matte gold treatments, and combinations with leather, ceramic, and precious stones have broadened the appeal of men's gold jewelry.

By Distribution Channel: Offline Retail Anchors Trust, Online Rewrites Access

Offline retail stores accounted for 84.55% of the GCC gold jewelry market in 2025. This reflects established purchasing norms for high-value items, where physical verification of purity, craftsmanship, and hallmark certification is culturally embedded across all six GCC countries. The Dubai Central Laboratory (DCL)'s hallmarking enforcement, including the Bareeq Certification awarded to retailers meeting quality, pricing transparency, and ethical trading standards, has strengthened consumer confidence in licensed jewelry stores and reinforced preference for organized brick-and-mortar retail. Physical outlets also offer immediate product inspection, personalized consultations, customization, resizing, engraving, and after-sales services such as polishing, repairs, exchange, and buyback programs, which remain key differentiators for high-value jewelry purchases.

Online retail is projected to grow at a CAGR of 5.45% during 2026–2031, supported by the expansion of digital-first jewelry platforms offering 360-degree product visualization, virtual try-on technologies, AI-powered recommendations, and certified digital authentication. The channel allows consumers to browse a wider assortment of designs, compare purity levels and pricing across brands, and access exclusive online collections unavailable in physical stores. Jewelers are accelerating online adoption through omnichannel capabilities such as click-and-collect, virtual consultations, appointment booking, and home delivery of certified products. Improvements in secure digital payments, transparent return policies, and personalized online shopping experiences are expected to sustain the channel's above-average growth throughout the forecast period.

Geography Analysis

Saudi Arabia held the largest share of the GCC gold jewelry market at 30.35% in 2025, driven by its extensive organized jewelry retail network, strong domestic manufacturing base, and deep-rooted preference for gold jewelry across bridal, gifting, and ceremonial occasions. The country benefits from the presence of major regional jewelry retailers and manufacturers offering a broad portfolio of traditional and contemporary collections across multiple purity levels. Continuous expansion of premium shopping malls, luxury retail destinations, and branded jewelry boutiques has further improved product accessibility and strengthened consumer engagement. Increasing investments in modern jewelry design, digital retail integration, and localized collection development continue to reinforce Saudi Arabia's position as the largest market within the GCC.

The United Arab Emirates is projected to be the fastest-growing GCC gold jewelry market, expanding at a CAGR of 5.09% during 2026–2031, supported by its position as both a global gold trading hub and one of the world's prominent luxury jewelry retail destinations. The country's well-established refining, wholesale, and re-export ecosystem ensures a continuous supply of certified gold products and enables retailers to introduce new collections rapidly. The country also benefits from internationally recognized gold retail districts, duty-efficient trade infrastructure, and a strong tourism sector that generates substantial jewelry purchases from international visitors. Furthermore, gold reserves held by the Central Bank of the United Arab Emirates increased by 25.9% during the first five months of 2025, reflecting the country's continued strategic emphasis on gold within its financial and trade ecosystem, while strengthening confidence across the broader precious metals industry.

Kuwait, Qatar, Bahrain, and Oman collectively represent a smaller but structurally stable tier of the GCC gold jewelry market, with demand supported by mature retail ecosystems and strong consumer preference for high-purity gold jewelry. While each market differs in scale, all four countries benefit from well-established jewelry souqs, expanding branded retail outlets, and increasing availability of contemporary and customized collections. Retailers are strengthening market presence through omnichannel strategies, exclusive seasonal launches, and premium customer services such as customization, engraving, and jewelry maintenance. Growing adoption of certified gold products, alongside continuous product innovation and the gradual expansion of organized jewelry retail, is expected to sustain steady market development across these GCC countries over the forecast period.

Competitive Landscape

The GCC gold jewelry market is moderately fragmented, with competition shaped by a mix of regional jewelry groups, international luxury brands, and established family-owned retailers. Major participants, including Titan Company Limited, Malabar Gold & Diamonds, Joyalukkas Jewellery LLC, Mannai Corporation (Damas International), and L'azurde Company for Jewelry, compete through extensive showroom networks, diversified product portfolios, and regular collection launches spanning traditional bridal jewelry, contemporary fashion jewelry, and premium designer collections. Companies are increasingly differentiating themselves through exclusive in-house designs, customization services, omnichannel retail capabilities, and after-sales offerings such as exchange, buyback, and lifetime maintenance programs to strengthen customer retention.

Competition is increasingly shifting toward product innovation and premiumization, with manufacturers introducing lightweight collections, modular jewelry, personalized engravings, gemstone-studded designs, and limited-edition collections to address evolving consumer preferences. Brands are also expanding their 18K jewelry portfolios, ethically certified collections, and minimalist designs targeting younger consumers seeking jewelry for everyday wear rather than only ceremonial occasions. Investments in CAD/CAM design, 3D printing, precision manufacturing, and AI-enabled retail experiences are enabling companies to shorten product development cycles, improve design flexibility, and respond more rapidly to changing fashion trends.

Sustainability, transparency, and supply chain credibility are becoming important competitive differentiators across the GCC market. Companies that demonstrate LBMA-aligned responsible gold sourcing, transparent hallmarking practices, and traceable supply chains are strengthening consumer confidence and enhancing brand positioning in both domestic and international markets. Retailers are also expanding digital commerce through virtual consultations, 360-degree product visualization, online customization tools, and omnichannel fulfillment services, while investing in flagship stores across premium retail destinations to deliver integrated online and offline shopping experiences that support long-term market competitiveness.

GCC Gold Jewelry Industry Leaders

-

Malabar Gold and Diamonds

-

Titan Company Limited

-

Joyalukkas Jewellery LLC

-

Mannai Corporation (Damas International)

-

L'azurde Company for Jewelry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Titan Company completed its acquisition of a 67% stake in Damas Jewellery's GCC business through its wholly-owned subsidiary, Titan Holdings International, establishing Signature Jewellery Holding as the new holding entity at an enterprise value of AED 1,038 million.

- October 2025: Joyalukkas inaugurated a new showroom in Fujairah. To mark the occasion, Joyalukkas announced an inaugural offer: customers purchasing diamond, polki, precious, or pearl jewellery worth AED 3,500 and above will receive an AED 200 gift voucher, along with 0% deduction on old gold exchange.

- September 2025: Malabar Gold & Diamonds opened its 65th showroom in the United Arab Emirates at UW Mall, Dubai, located adjacent to BurJuman Mall. The outlet features a new concept design, a luxury customer lounge, and exclusive collections.

GCC Gold Jewelry Market Report Scope

Gold jewellery refers to personal ornaments such as rings, necklaces, earrings, and others, often serving as a symbol of wealth, prestige, and cultural heritage. The GCC gold jewelry market is segmented by product type, karat/purity, end user, distribution channel, and geography. Based on product type, the market is segmented into rings, necklaces, earrings, bracelets, chains and pendants, and other product types. Based on karat/purity, the market is segmented into 24 karat, 22 karat, 18 karat, and others. Based on end user, the market is segmented into men, women, and children. Based on distribution channel, the market is segmented into offline retail stores and online retail stores. Based on geography, the market is segmented into Saudi Arabia, United Arab Emirates, Kuwait, Qatar, Bahrain, and Oman. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Rings |

| Necklaces |

| Earrings |

| Bracelets |

| Chains and Pendants |

| Other Product Types |

| 24 Karat |

| 22 Karat |

| 18 Karat |

| Others |

| Men |

| Women |

| Children |

| Offline Retail Stores |

| Online Retail Stores |

| Saudi Arabia | United Arab Emirates |

| Kuwait | |

| Qatar | |

| Bahrain | |

| Oman |

| By Product Type | Rings | |

| Necklaces | ||

| Earrings | ||

| Bracelets | ||

| Chains and Pendants | ||

| Other Product Types | ||

| By Karat/Purity | 24 Karat | |

| 22 Karat | ||

| 18 Karat | ||

| Others | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | Saudi Arabia | United Arab Emirates |

| Kuwait | ||

| Qatar | ||

| Bahrain | ||

| Oman | ||

Key Questions Answered in the Report

What is the GCC gold jewelry market size in 2026 and where is it headed by 2031?

The GCC gold jewelry market stands at USD 17.23 billion in 2026 and is forecast to reach USD 20.55 billion by 2031 at a 3.59% CAGR.

Which country leads gold jewelry demand across the GCC?

Saudi Arabia led with 30.35% share in 2025, supported by strong domestic demand tied to weddings, gifting, and household gold ownership.

Which product category is growing fastest in the region?

Chains and pendants are the fastest-growing product type with a projected 4.81% CAGR through 2031 because they serve both adornment and value retention needs.

Why does offline retail still dominate purchases in the Gulf?

Offline stores held 84.55% share in 2025 because buyers still want in-person verification of purity, workmanship, and certification before making high-value purchases.

Page last updated on: