Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.06 Billion |

| Market Size (2026) | USD 19.39 Billion |

| Market Size (2031) | USD 27.45 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Air Freight Transport Market Analysis by Mordor Intelligence

The GCC air freight transport market size is expected to increase from USD 18.06 billion in 2025 to USD 19.39 billion in 2026 and reach USD 27.45 billion by 2031, growing at a 7.2% CAGR over 2026-2031.

The region is shifting from a pure trans-shipment corridor into a value-added logistics hub where forwarders orchestrate multi-modal flows between Asian manufacturers, European consumers, and emerging African demand centers. Open-skies agreements with key Asian partners added 18% new belly capacity on passenger routes during 2025, letting forwarders consolidate smaller loads without relying on freighter charters. Nearshoring has attracted component producers to GCC free zones, creating two-way flows that favor forwarders with bonded warehouses and customs depth. Rapid growth in cross-border e-commerce is generating high-margin reverse logistics volumes, prompting Kuehne+Nagel to break ground on a 23,000-square-meter fulfillment center beside Al Maktoum International Airport in February 2025. AI-driven capacity platforms are compressing spot-rate discovery time, pushing incumbents to invest in proprietary digital tools while maintaining physical assets that protect margins on complex shipments.

Key Report Takeaways

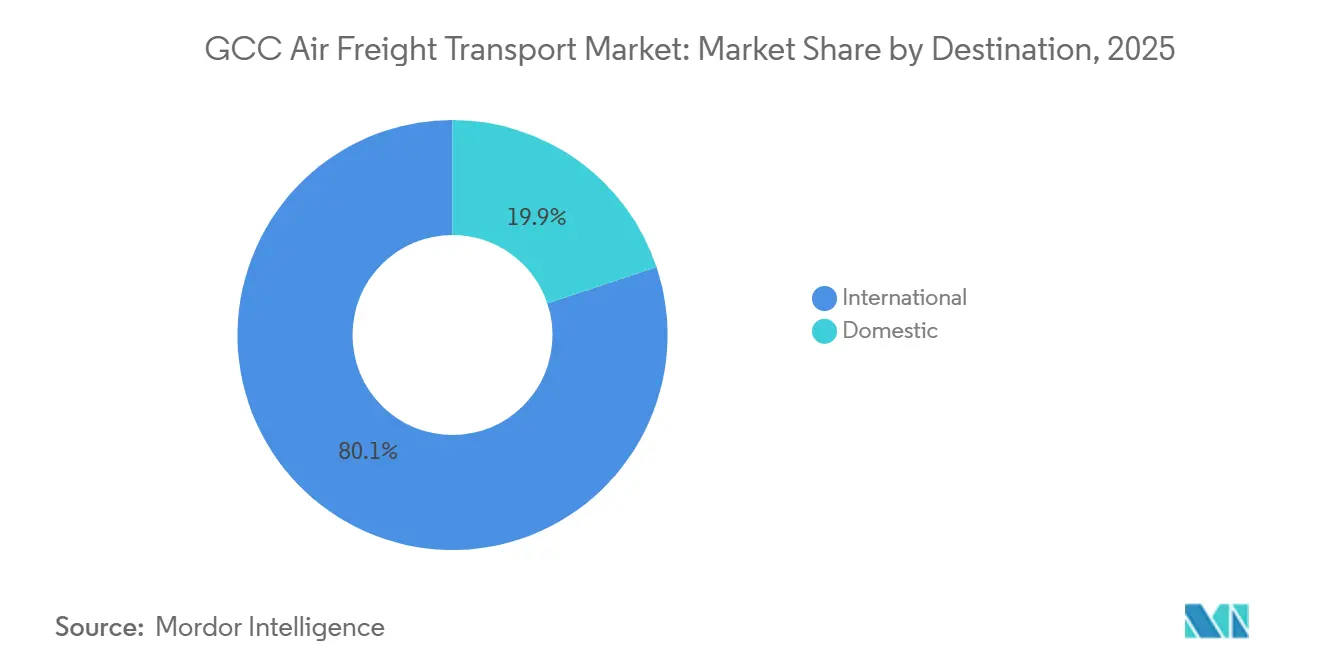

- By destination, international shipments led with 80.12% of the GCC air freight transport market share in 2025; domestic forwarding is advancing at an 8.57% CAGR through 2031.

- By carrier type, belly cargo arrangements captured 66.30% market share of forwarded values in 2025, while freighter solutions are forecast to post a 7.90% CAGR to 2031.

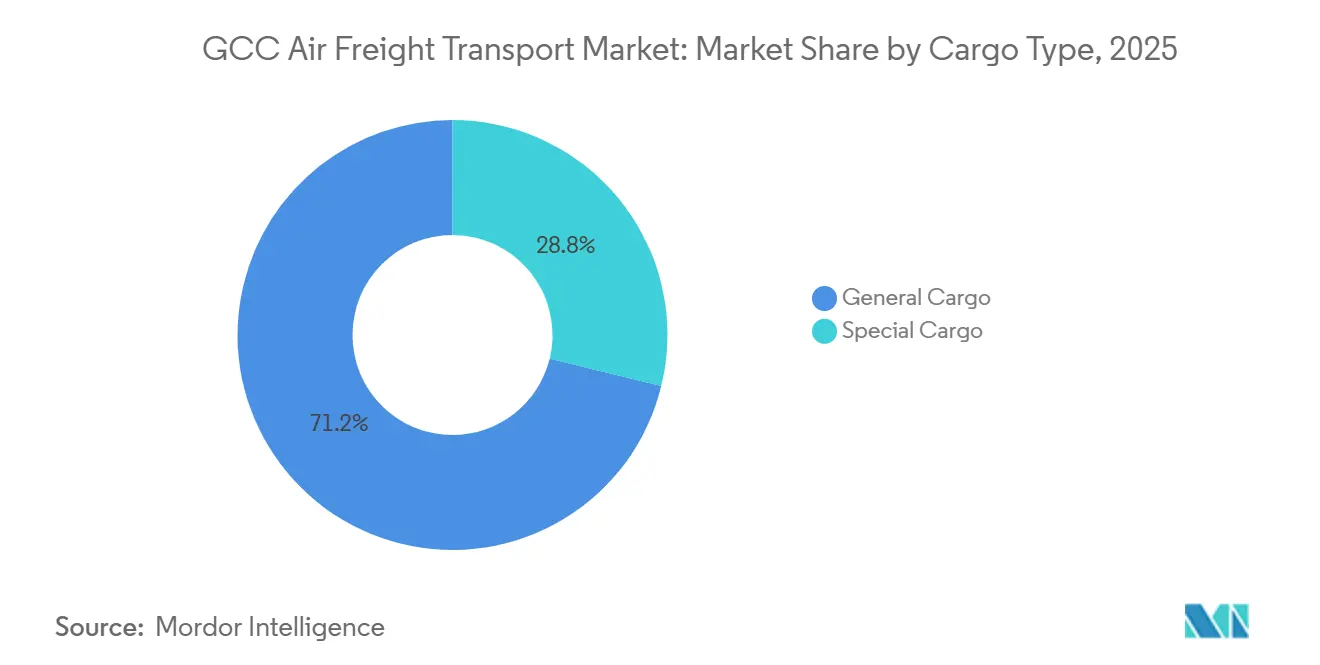

- By cargo type, general cargo accounted for 71.18% of the GCC air freight transport market size in 2025, whereas special cargo segments are projected to expand at an 8.26% CAGR over 2026-2031.

- By end-user industry, manufacturing and automotive held 26.21% market share of demand in 2025, while e-commerce and retail are set to grow fastest at 9.35% CAGR to 2031.

- By country, Saudi Arabia dominated with 36.11% market share in 2025; the UAE is the quickest riser at an 8.09% CAGR on the back of Dubai’s digital freight marketplace growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Air Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-shoring led component inflows to GCC free zones | +1.6% | Saudi Arabia and UAE free zones, spillover to Qatar | Medium term (2-4 years) |

| Reverse-logistics of e-commerce returns by air | +1.3% | GCC-wide, concentrated in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Open-skies pacts unlocking additional belly capacity | +1.1% | Regional bilateral agreements, Asia-GCC routes | Medium term (2-4 years) |

| AI-driven dynamic capacity marketplaces | +0.9% | Digital platforms operating across GCC | Short term (≤ 2 years) |

| Hydrogen-electric UAV feeder networks pilot projects | +0.4% | UAE and Saudi Arabia pilot zones | Long term (≥ 4 years) |

| Precision-therapy cold-chain corridors (cell and gene) | +0.8% | GCC medical tourism hubs, UAE and Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-Shoring Led Component Inflows to GCC Free Zones

Light manufacturers moving into tax-free industrial zones are generating two-way air freight flows. Dubai South’s Logistics District offers full foreign ownership and duty deferment, prompting forwarders to open bonded facilities that allow staged clearance. Saudi Arabia is investing USD 266 billion to build 59 specialized logistics centers, each designed with direct apron access so parts can move from aircraft to assembly lines in under four hours posted 22% tenant growth during 2024, with electronics and automotive sub-assemblies leading inflows. The bidirectional model increases forwarder revenue touchpoints by adding kitting, labeling, and quality checks to traditional uplift. Customs brokers holding warehouse licenses capture more value than pure capacity brokers because they can defer duties until goods reach their final GCC market[1]“KIZAD Industrial Zone Growth Report,” Invest in Abu Dhabi, investinabudhabi.gov.ae.

Reverse Logistics of E-Commerce Returns by Air

GCC online retail is set to hit USD 49.78 billion in 2027 with return rates of 15-20% for fashion and electronics. Kuehne+Nagel’s new Dubai site, operational since Q2 2025, integrates return processing so rejected items ride the same flight as outbound orders, lowering per-unit transport costs by 30%. Returns need re-import documentation, inspection, and refurbishment, services that airlines have little incentive to provide. Emirates Delivers launched in Saudi Arabia during 2024 to serve direct-to-consumer flows, yet still outsources last-mile and returns to forwarders. Fragmented regulations across GCC states heighten compliance complexity, tilting competitive advantage toward multi-country customs specialists[2]“New Training Provisions for Dangerous Goods,” ICAO, icao.int.

Open-Skies Pacts Unlocking Extra Belly Capacity

New bilateral pacts signed during 2024-2025 added 18% belly capacity by allowing foreign carriers more frequencies and gauge flexibility. Saudi Arabia’s May 2025 liberalization opened domestic charters to foreign operators, letting forwarders source lift on empty repositioning legs. Qatar’s regulator forecasts 5.1% annual fleet growth through 2030; every new wide-body adds 15-20 tons of belly space. While capacity abundance pressures yields, forwarders capable of value-added services still maintain premium pricing on specialized moves. Tighter IATA dangerous goods rules effective June 2024 increase training costs and offset some of the rate advantage.

AI-Driven Dynamic Capacity Marketplaces

Digital platforms now match shipper demand with real-time carrier space, reducing booking friction but eroding margins on commoditized general cargo. Qatar Airways Cargo integrated CargoFlash in August 2024 to allow instant booking and track-and-trace without forwarder intermediation for routine loads. Forwarders are responding by spending 8-12% of revenue on proprietary AI tools that predict demand spikes and lock in capacity before spot rates rise. The winners will blend digital engines with bonded warehouses, giving shippers online speed plus physical control points inside free zones.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CORSIA and EU ETS carbon-cost pass-through | -1.0% | GCC-Europe routes primarily, global spillover | Medium term (2-4 years) |

| Freighter oversupply from P2F wave | -0.7% | Regional capacity markets, charter rate pressure | Short term (≤ 2 years) |

| Mega-event apron congestion risk | -0.4% | Saudi Arabia and UAE event host cities | Short term (≤ 2 years) |

| Cyber vulnerabilities in cargo community systems | -0.3% | Digital infrastructure across GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CORSIA and EU ETS Carbon-Cost Pass-Through

EU ETS charges of EUR 80-100 per tonne CO₂ now apply to non-EU airlines, adding roughly USD 15-20 per tonne of cargo on Europe-bound flights. Emirates has earmarked USD 200 million for sustainability projects, yet sustainable aviation fuel costs remain two to four times higher than Jet A-1. Cost escalation encourages shippers of non-urgent goods to switch to ocean freight, shrinking the accessible pool for forwarders. Fragmented carbon disclosure regimes across the GCC add further administrative overhead[3]“Capacity Constraints at Kuwait International Airport,” Gulf News, gulfnews.com.

Freighter Oversupply from P2F Wave

Conversions of retired passenger wide-bodies topped 150 orders in 2024, implying a 15-20% jump in global freighter capacity between 2025-2027. Emirates SkyCargo ordered five Boeing 777Fs in July 2024 with deliveries during 2025-2026, while Gulf Air’s July 2025 order added 12 Boeing 787s featuring cargo-optimized holds. If passenger belly capacity rises simultaneously, charter yields fall, forcing forwarders locked into long-term block-space agreements to renegotiate or accept losses. Specialized temperature-controlled lanes suffer less because few P2F aircraft are fitted for deep-frozen moves[4]“Middle East Fleet Growth Outlook,” CAA Qatar, caa.gov.qa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Destination: International Dominance with Rising Domestic Potential

International services captured 80.12% market share of traffic in 2025, reflecting the GCC air freight transport market’s traditional bridge role between Asia, Europe, and Africa. Domestic uplift is forecast to post an 8.57% CAGR as Saudi Arabia’s industrial clusters in Riyadh, Jeddah, and Dammam require same-day component deliveries that bypass port congestion. The GCC air freight transport market size for domestic corridors is projected to double by 2031, supported by Riyadh’s move to allow foreign charter operators on intra-Kingdom runs.

Forwarders continue to dominate cross-border flows because every shipment still needs dual customs clearances and multi-currency documentation. Digital booking tools win small parcels, but larger component movements depend on bonded facilities that stage parts for assembly plants. Saudia Cargo’s “Landing in China in 24” service validates growing eastbound export appetite for Saudi electronics and auto parts.

By Carrier Type: Belly Capacity Leads but Main-Deck Specialty Grows

Belly holds supplied 66.30% market size of lift in 2025 because passenger flights offer dense frequency and competitive tariffs. The GCC air freight transport market share for freighter solutions will rise as oversized project cargo and -80°C pharma lanes outgrow dimensional and temperature limits of passenger aircraft.

Freighter tonnage is projected to record a 7.90% CAGR through 2031, yet charter yields may soften if P2F conversions overshoot demand. Forwarders arbitrage between lower belly spot rates in slack months and main-deck charters in peak seasons, protecting margin with dynamic procurement systems backed by AI. Emirates SkyCargo’s extra B777Fs expand the GCC air freight transport market size for main-deck moves that cannot fit through lower-deck doors.

By Cargo Type: Special Cargo Offers Margin Shelter

General cargo still held 71.18% market share of shipments in 2025, but special cargo is projected to grow at 8.26% CAGR as pharma, perishables, and high-tech goods demand specialized handling. The GCC air freight transport market size for ultra-cold logistics will expand rapidly after multiple GCC hospitals began cell-and-gene therapy programs requiring -80°C door-to-door compliance.

Carriers have invested in CEIV certifications, yet forwarders remain essential for lane validation, dry-ice replenishment, and escorts. Live animal volumes also rise due to elevated demand for racehorses and breeding stock in Gulf states. Commoditized general cargo faces the heaviest price pressure from digital spot marketplaces.

By End-User Industry: E-Commerce and Retail Sets the Growth Pace

Manufacturing and automotive generated 26.21% of the market size in 2025, sustained by near-shored component inflows. The GCC air freight transport market is witnessing the sharpest expansion in e-commerce and retail, which is poised to advance at 9.35% CAGR due to surging cross-border shopping and associated returns. Forwarders have responded by adding fulfillment centers inside airport free zones that integrate inventory, packaging, and same-day re-export.

Pharmaceutical demand stays resilient because medical tourism draws patients to Emirati and Saudi clinics that need time-critical biologics. Renewable energy components under “Others” create episodic peaks aligned with solar park construction milestones.

Geography Analysis

Saudi Arabia held 36.11% of the GCC air freight transport market share in 2025 on the back of Vision 2030 logistical investments worth USD 266 billion, including 59 airport-linked logistics parks. The UAE is forecast to outpace peers at an 8.09% CAGR through 2031, fueled by Dubai’s positioning as a digital freight exchange where global forwarders pilot AI engines and blockchain documentation stacks. Qatar benefits from Hamad International Airport’s new concourses, raising passenger capacity above 65 million and delivering extra belly space that forwarders can tap at competitive rates.

Bahrain targets pharma and high-tech niches through the expansion of DHL’s regional hub and an integrated air-sea cargo village that links Bahrain International Airport with Khalifa bin Salman Port. Kuwait faces infrastructure bottlenecks, illustrated by 14 airlines withdrawing services in 2025, which tightens capacity and permits forwarders to charge scarcity premiums.

Oman Air Cargo’s Amsterdam entry expands European reach, but limited belly lift caps growth potential. Sharjah International Airport’s 38.6% cargo surge in 2024 shows how secondary hubs absorb overflow from Dubai and Abu Dhabi, giving forwarders alternative staging points at lower handling fees.

Competitive Landscape

The players Etihad Cargo, Emirates SkyCargo, Qatar Airways Cargo, and Saudia Cargo control about 48% of regional throughput, leaving space for regional specialists and tech-enabled entrants. Kuehne+Nagel’s Dubai e-commerce hub exemplifies the trend of forwarders embedding fulfillment assets within airport perimeters to secure sticky reverse-logistics revenue.

Saudia Cargo formed Saudia Cargo Global with TAM Group in June 2025, aiming to capture forwarding margins beyond airline uplift alone. Etihad and SF Airlines inked a joint cargo pact to widen Asia-Gulf network density, underscoring carrier-forwarder collaboration for smoother line-haul visibility.

Investment in AI and blockchain averages 10% of revenue among leading players compared with 4% for mid-tier firms, creating a widening tech gap. Upcoming hydrogen-electric UAV feeder pilots in the UAE and Saudi Arabia could give early adopters same-day delivery capability to remote industrial sites. Cybersecurity is emerging as a differentiator; forwarders offering ISO 27001-certified cargo community systems report higher win rates on contracts involving high-value electronics.

GCC Air Freight Transport Industry Leaders

Emirates SkyCargo

Qatar Airways Cargo

Saudia Cargo

Etihad Cargo

Jazeera Airways Cargo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Emirates launched Emirates Courier Express, an end-to-end delivery solution designed to address express delivery challenges. The service, piloted with global customers, delivered thousands of packages in under 48 hours from multiple countries.

- November 2025: Emirates SkyCargo and LODD Autonomous signed a Memorandum of Understanding (MoU) at the 2025 Dubai Airshow to explore air cargo solutions. They collaborated to evaluate VTOL (Vertical Take Off and Landing) aircraft through feasibility studies, regulatory engagement, and live demonstrations.

- June 2025: Etihad Airways and SF Airlines signed a joint cargo deal to deepen Asia-Middle East Lane cooperation.

- May 2025: Turkish Cargo and Hong Kong Air Cargo agreed to enhance operational collaboration and network sharing.

GCC Air Freight Transport Market Report Scope

By Destination

| Domestic |

| International |

By Carrier Type

| Belly Cargo |

| Freighter |

By Cargo Type

| General Cargo |

| Special Cargo |

By End-User Industry

| E-commerce and Retail |

| Manufacturing and Automotive |

| Healthcare and Pharmaceuticals |

| Perishables and Fresh Produce |

| High-Tech and Electronics |

| Others |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| By Destination | Domestic |

| International | |

| By Carrier Type | Belly Cargo |

| Freighter | |

| By Cargo Type | General Cargo |

| Special Cargo | |

| By End-User Industry | E-commerce and Retail |

| Manufacturing and Automotive | |

| Healthcare and Pharmaceuticals | |

| Perishables and Fresh Produce | |

| High-Tech and Electronics | |

| Others | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman |

Key Questions Answered in the Report

How fast is air freight value growing across Gulf states?

The GCC air freight transport market is set to climb from USD 19.39 billion in 2026 to USD 27.45 billion by 2031, translating to a 7.2% CAGR.

Which shipment type commands the most volume today?

General cargo still leads with 71.18% of 2025 volume, though special cargo segments such as pharma are expanding faster at 8.26% CAGR.

Why are forwarders investing in fulfillment centers near Dubai’s airports?

Growing cross-border e-commerce and the need to process high return rates make integrated inventory and returns hubs near flight gates more cost-effective.

What carbon pricing rules affect Gulf-Europe air lanes?

EU ETS now levies carbon allowances that add about USD 15-20 per ton of cargo, costs that forwarders must either absorb or pass on.

How will passenger-to-freighter conversions influence rates?

More converted freighters entering service between 2025-2027 could oversupply capacity and push charter yields down, especially on general cargo lanes.

Which Gulf country shows the quickest growth momentum?

The UAE leads on growth with an 8.09% CAGR to 2031, driven by Dubai’s emergence as a regional digital freight marketplace.

Page last updated on: