GCC AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

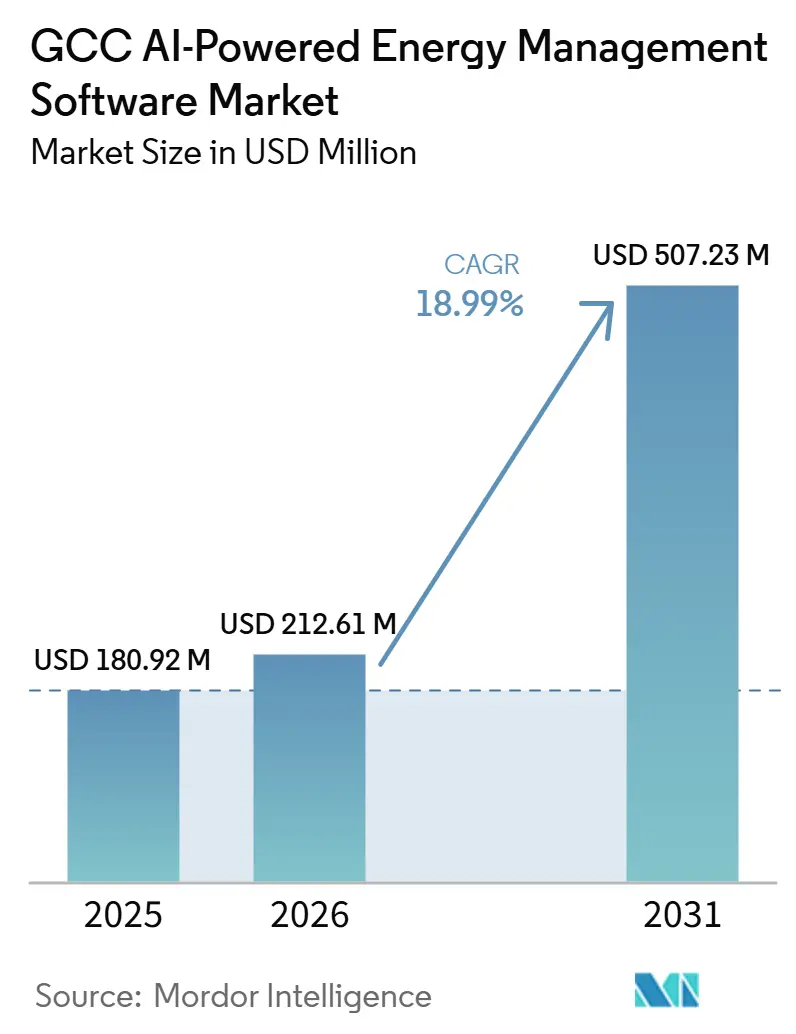

| Base Year Market Size (2025) | USD 180.92 Million |

| Market Size (2026) | USD 212.61 Million |

| Market Size (2031) | USD 507.23 Million |

| Growth Rate (2026 - 2031) | 18.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The GCC AI-powered Energy Management Software Market size is expected to increase from USD 180.92 million in 2025 to USD 212.61 million in 2026 and reach USD 507.23 million by 2031, growing at a CAGR of 18.99% over 2026-2031. The GCC AI-powered Energy Management Software Market is expanding as utilities, large property owners, and industrial operators move from basic monitoring to systems that can predict loads, optimize consumption, and enable faster operational decisions. Demand is also rising because renewable capacity additions across the Gulf are making solar forecasting, demand balancing, and battery coordination more important for daily grid operations. Compliance needs are widening the buyer base beyond utilities and premium buildings, as energy data now supports emissions reporting, internal efficiency targets, and operating transparency across more enterprise users. Vendor strategy in the GCC AI-powered Energy Management Software Market is centered on local hosting, stronger integration support, and deeper service delivery because many buyers need help connecting newer AI tools with older control environments. This leaves room for growth in cloud analytics, hybrid deployment models, and managed services, especially where operators want measurable savings without disrupting critical power or facility systems.

Key Report Takeaways

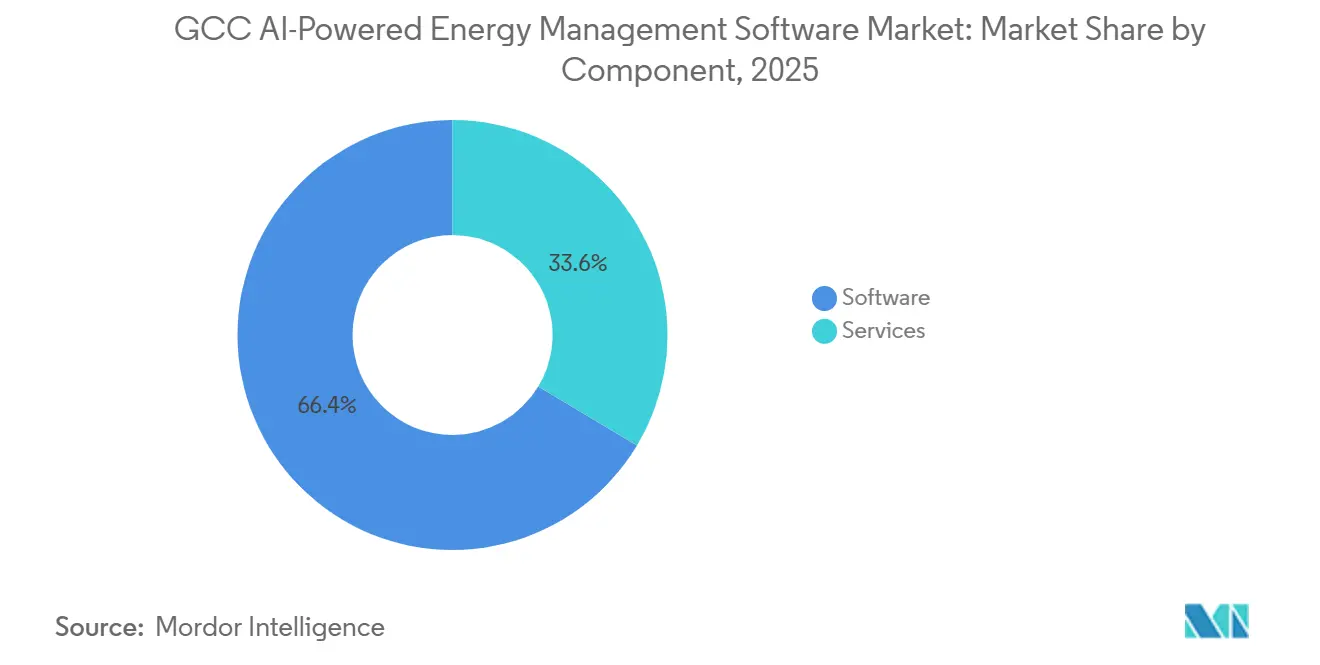

- By component, software held 66.41% of the GCC AI-powered Energy Management Software Market share in 2025, while services are projected to expand at a 22.04% CAGR through 2031.

- By deployment mode, cloud-based platforms accounted for 60.49% of the GCC Artificial Intelligence Powered Energy Management Software Market size in 2025, while hybrid deployments are expected to advance at a 21.78% CAGR through 2031.

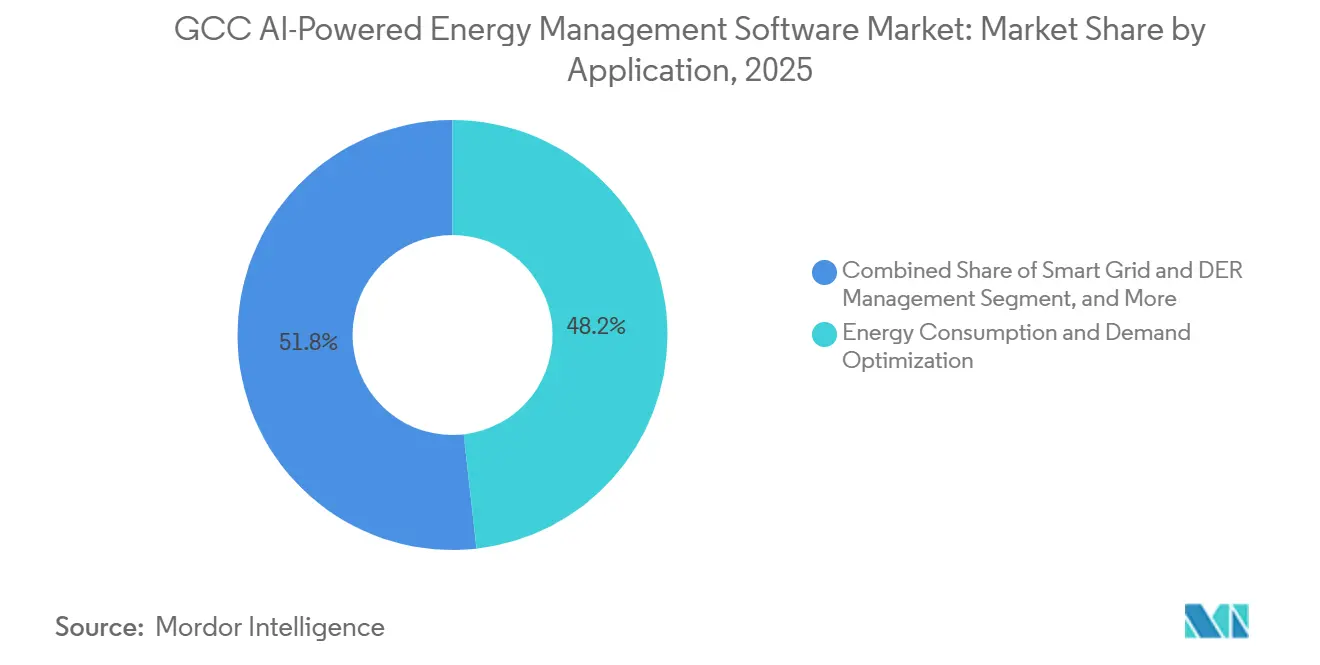

- By application, energy consumption and demand optimization captured 48.22% of the GCC Artificial Intelligence Powered Energy Management Software Market in 2025, while renewable energy forecasting and integration is projected to grow at a 20.89% CAGR to 2031.

- By end user, commercial buildings held a 58.91% share of the GCC AI-powered Energy Management Software Market in 2025, while utilities are expected to record the fastest CAGR of 21.32% through 2031.

- By geography, Saudi Arabia led the GCC AI-powered Energy Management Software Market with 37.24% in 2025, while the UAE is projected to expand at a 20.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising GCC Grid Digitization and Utility Analytics Adoption | +4.5% | Saudi Arabia, UAE, Kuwait, Oman | Short term (≤ 2 years) |

| Rapid Expansion of Smart Buildings and Connected Facility Operations | +3.8% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Renewable Integration Requiring Forecasting and Load Balancing | +3.2% | Saudi Arabia, UAE, Oman | Medium term (2-4 years) |

| Push for Carbon Reporting and Energy Efficiency Compliance | +2.5% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Cloud-First Enterprise IT Modernization in Energy-Intensive Sectors | +2.0% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Substation and Distributed Asset Optimization in Industrial Clusters | +1.5% | Saudi Arabia, Kuwait, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising GCC Grid Digitization and Utility Analytics Adoption

The GCC AI-powered Energy Management Software Market is benefiting from a utility base that already has a large installed layer of digital meters, automation assets, and network monitoring tools. The GCC Interconnection Authority stated that only 35% of GCC organizations were confident in their AI infrastructure readiness in April 2025, which shows that hardware rollout moved ahead of analytics maturity and left room for software adoption. The International Energy Agency reported that AI-based fault detection can cut outage durations by 30%-50% and unlock up to 175 GW of transmission capacity without building new lines, giving utilities a clear operating case for analytics investments.[1]International Energy Agency, “Executive Summary - Energy and AI,” International Energy Agency, iea.org This matters for the GCC AI-powered Energy Management Software Market because utilities in the region are moving beyond metering toward prediction, control support, and asset health management. The gap between installed digital infrastructure and day-to-day AI use is also widening the role of software vendors that can connect data streams, tune models, and prove savings across regulated grid environments. As more utilities move pilots into recurring operational use, procurement is likely to favor platforms that integrate with utility workflows rather than just deliver dashboards.

Rapid Expansion of Smart Buildings and Connected Facility Operations

The GCC AI-powered Energy Management Software Market is also gaining support from the region’s large stock of commercial buildings, where cooling remains a major energy cost for owners and operators. Johnson Controls launched Balanced Cooling in the UAE in April 2026 to address low Delta-T performance in buildings connected to centralized cooling systems, which shows that vendors are designing AI-led solutions for local operating conditions rather than selling generic building software. Johnson Controls also reported that Dubai Silicon Oasis achieved 30% annual energy savings through AI-powered solutions, providing building operators with a concrete local example of measurable operating value. In the GCC AI-powered Energy Management Software Market, this supports demand from hotels, mixed-use projects, office campuses, and district cooling-connected properties that face persistent pressure to reduce waste without affecting occupant comfort. Buyers in this segment are also placing greater weight on platforms that unify equipment visibility, automate cooling responses, and align with broader building modernization plans. That is why smart building demand is not limited to sustainability targets, because it is now tied directly to operating cost control, tenant service levels, and portfolio-level performance management.

Renewable Integration Requiring Forecasting and Load Balancing

Renewable expansion is creating a software requirement that conventional energy management systems are increasingly unable to handle. Columbia University’s Center on Global Energy Policy stated that GCC governments require USD 60 billion in renewable energy investment between 2025 and 2030 to add 102 GW of capacity, underscoring the need for better forecasting and coordination tools to link new generation buildout to these needs. A peer-reviewed study in Energy Strategy Reviews found that artificial intelligence and the digital economy had a statistically significant positive influence on energy transition outcomes across GCC countries, supporting the case for AI-led planning and operating systems as renewable energy shares rise. The GCC AI-powered Energy Management Software Market is therefore moving toward grid balancing, solar output prediction, and distributed energy coordination rather than remaining focused solely on efficiency dashboards. This shift is important because renewable additions increase variability while utilities are expected to maintain system reliability and power quality. As the renewable pipeline grows, buyers are likely to prioritize platforms that combine forecasting, asset visibility, and demand response logic within a single operating environment.

Push for Carbon Reporting and Energy Efficiency Compliance

The GCC AI-powered Energy Management Software Market is attracting more buyers as energy data becomes part of formal reporting and compliance processes. The UAE issued Federal Decree-Law No. 11 of 2024 to reduce the effects of climate change, establishing a national framework for emissions reduction and reporting obligations for relevant entities. This change matters because many organizations that once treated energy software as optional now need auditable consumption records, better data granularity, and traceable emissions inputs. The GCC AI-powered Energy Management Software Market is therefore widening beyond utilities and landmark real estate toward mid-sized enterprises with reporting and internal efficiency mandates. Once reporting workflows are linked to utility bills, building controls, and production systems, demand typically shifts from basic metering to platforms that automate analysis and alerting. That process also favors vendors that can package monitoring, analytics, and compliance-ready reporting into a single workflow, rather than requiring buyers to assemble separate tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy OT Integration Complexity Across Utility and Industrial Sites | -3.2% | Saudi Arabia, UAE, Kuwait | Long term (≥ 4 years) |

| Data Sovereignty and Critical Infrastructure Security Constraints | -2.5% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Limited Local AI Talent for Energy-Specific Model Tuning | -1.8% | GCC-wide | Medium term (2-4 years) |

| Interoperability Gaps Across Multi-Vendor Building and Grid Systems | -1.5% | UAE, Qatar, Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy OT Integration Complexity Across Utility and Industrial Sites

Legacy operational technology remains a major speed barrier for the GCC AI-powered Energy Management Software Market. The GCC Interconnection Authority said its Open Power AI Consortium was working with utilities and global members to develop and validate AI models for power system use, underscoring that the sector still needs dedicated effort to make AI work reliably in energy-sector operating environments. Many utilities and industrial operators still rely on proprietary control systems, older communications layers, and field equipment that was not designed for continuous analytics exchange. This slows implementation because software providers must spend more time on interfaces, testing, commissioning, and approval before models can be used in live operations. It also favors large incumbents with field-integration teams and local service depth, thereby raising the entry threshold for software-led challengers. Until integration becomes easier and more standardized, project timelines in the GCC AI-powered Energy Management Software Market are likely to remain longer than buyers initially expect.

Data Sovereignty and Critical Infrastructure Security Constraints

Security and data residency requirements are also shaping the development of the GCC AI-powered Energy Management Software Market. IBM and AWS expanded their collaboration in October 2025 to host IBM’s SaaS portfolio in local cloud regions in the UAE and Saudi Arabia, indicating that local hosting had become a practical condition for wider enterprise adoption. Even with that progress, buyers who manage grid, utility, and critical infrastructure data still require strict control over where information is stored and how it is accessed. This adds time to vendor qualification because software providers must prove local compliance, security processes, and operational reliability before contracts move forward. In the GCC AI-powered Energy Management Software Market, the result is a stronger position for suppliers that can combine cloud benefits with regional infrastructure and audit readiness. Smaller vendors can still enter, but they often need partnerships or hybrid deployment models to clear procurement hurdles in sensitive operating environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals a Shifting Value Chain

Software accounted for 66.41% of 2025 revenue in the GCC AI-powered Energy Management Software Market, which kept the installed base anchored in licensed platforms and SaaS subscriptions. That lead reflects the region’s existing use of monitoring, control, and analytics tools across utilities, large real estate portfolios, and critical infrastructure operators. The first buying decision still centers on platform capability, because operators need a usable system before they can pursue automation, optimization, or predictive workflows. Even so, the structure of the GCC AI-Powered Energy Management Software industry shows that software ownership alone does not guarantee performance gains or adoption depth. Buyers are increasingly selecting vendors that can support high-quality implementation, data integration, and ongoing model refinement, rather than just delivering a feature-rich application.

Services are projected to grow at a 22.04% CAGR between 2026 and 2031, making this the fastest-growing component of the GCC AI-powered Energy Management Software Market. The International Energy Agency noted that AI in energy can reduce outage durations by 30%-50% and unlock significant grid capacity, but those gains depend on proper deployment, configuration, and operating discipline rather than software licenses alone. This explains why buyers are spending more on integration, managed analytics, training, and model tuning after the initial sale. It also explains why services are becoming a larger value layer in a region where many organizations still have limited in-house AI operations capability. Over time, vendors that combine strong software with credible services are likely to hold the most durable customer relationships in the GCC AI-powered Energy Management Software Market.

By Deployment Mode: Hybrid Architectures Bridge Operational and Analytical Demands

Cloud-based deployments captured 60.49% of the GCC AI-powered Energy Management Software Market in 2025, indicating that scalable remote analytics has already become the preferred model for many users. This lead reflects the appeal of multi-site visibility, easier updates, and lower infrastructure burden for enterprises that manage distributed buildings or energy assets. It also reflects growing comfort with local cloud availability in the Gulf, which has removed part of the earlier hesitation around residency and latency. In practical terms, cloud deployments work best where buyers prioritize enterprise reporting, benchmarking, and centralized oversight over real-time control execution. That keeps cloud strong in commercial building portfolios, ESG-linked reporting, and broader enterprise energy analytics.

Hybrid deployments are projected to record the fastest 21.78% CAGR through 2031 in the GCC AI-powered Energy Management Software Market. IBM and AWS announced in October 2025 that IBM SaaS products would be hosted in AWS cloud regions in the UAE and Saudi Arabia, strengthening the local infrastructure base for mixed operating models. Hybrid demand is rising because many utility and industrial buyers want grid-control or plant-critical logic to remain on-premises while analytics, demand forecasting, and reporting move to cloud layers. This structure reduces operational risk without sacrificing the scale and flexibility that cloud analytics offers. The GCC AI-Powered Energy Management Software industry is therefore not shifting in a straight line toward full cloud, because critical operators still need architectures that respect control boundaries and security rules.

By Application: Demand Optimization Leads, Renewable Forecasting Accelerates

Energy consumption and demand optimization accounted for 48.22% of 2025 revenue, making it the largest application area in the GCC AI-powered Energy Management Software Market. That lead comes from the region’s heavy cooling loads, dense commercial property base, and strong incentive to smooth usage during high-demand periods. Johnson Controls reported that Dubai Silicon Oasis achieved 30% annual energy savings with AI-powered solutions, which supports the case for demand optimization as the most immediate and measurable use case for many building operators.[2]Johnson Controls, “Dubai Silicon Oasis Achieves 30% Annual Energy Savings with AI-Powered Solutions,” Johnson Controls, johnsoncontrols.com The size of this segment also reflects how buyers typically start with visible consumption control before moving to more advanced asset- and grid-based applications. As a result, vendors often use demand optimization as the entry point for wider software adoption across buildings and facilities.

Renewable energy forecasting and integration are expected to expand at a 20.89% CAGR through 2031 in the GCC AI-powered Energy Management Software Market. Columbia University’s Center on Global Energy Policy linked the GCC's renewable pipeline to 102 GW of added capacity between 2025 and 2030, underscoring the need for stronger solar forecasting and coordination tools. The DEWA and Siemens Energy Phase 2 agreement for the AI Plant Intelligent Controller followed Phase 1 results, which included a 2.2% efficiency improvement and a reduction of 35,000 tonnes of CO₂ per power block annually, demonstrating that AI-led operating intelligence is already delivering measurable energy outcomes in power assets. The market is therefore widening from cost control toward systems that can manage intermittency, improve dispatch quality, and support more complex generation mixes. This shift gives forecasting, balancing, and asset intelligence a much larger role in future buying decisions.

By End User: Commercial Buildings Lead, Utilities Build Momentum

Commercial buildings accounted for 58.91% of the GCC AI-powered Energy Management Software Market in 2025, making them the largest end-user group by a clear margin. This reflects the Gulf’s concentration of hotels, malls, mixed-use assets, offices, and large campuses where continuous cooling demand keeps energy software financially relevant. The business case for these properties is usually clear and immediate, as owners can track savings from reduced consumption, improved equipment performance, and better comfort control. Commercial demand also supports the recurring use of dashboards, alerts, automated building responses, and portfolio benchmarking. In the GCC AI-powered Energy Management Software Market, this broad base gives vendors a large, addressable market that is not dependent solely on utility-scale projects.

Utilities are projected to grow at a 21.32% CAGR through 2031, making them the fastest-growing end-user segment in the GCC AI-powered Energy Management Software Market. The International Energy Agency showed that AI can reduce outage durations and unlock transmission capacity, which is highly relevant for utilities that must manage reliability, asset health, and power quality at scale. Utility growth is accelerating because smart meter density, automation systems, and network visibility have reached a point where AI models can be used more systematically. That creates room for demand response, predictive maintenance, outage management, and grid balancing functions to move into regular operations. As utilities increase their software depth, the GCC Artificial Intelligence Powered Energy Management Software Market is likely to see larger contracts, longer implementation cycles, and stronger demand for hybrid and service-heavy delivery models.

Geography Analysis

Saudi Arabia held 37.24% of the GCC AI-powered Energy Management Software Market in 2025, maintaining its leading position. The country’s scale in utilities, refining, petrochemicals, desalination, and commercial development provides software vendors with a larger operating base than in any other GCC market. IBM and Aramco announced a strategic collaboration in May 2026 to advance AI, agentic AI, automation, and materials science capabilities across Saudi Arabia’s industrial sector, signaling strong top-level support for AI-led operating models in energy-intensive environments.[3]IBM Newsroom, “IBM and Aramco Explore Collaboration to Accelerate AI and Innovation Across Saudi Arabia,” IBM Newsroom, newsroom.ibm.com Saudi Arabia’s lead also reflects the depth of modernization activity across utility and industrial assets, where energy management software can be tied to efficiency, resilience, and broader digital transformation priorities. This gives the GCC Artificial Intelligence Powered Energy Management Software Market a strong anchor country with large deal sizes and a wide mix of utility, industrial, and property-related use cases.

The UAE is projected to grow at a 20.41% CAGR through 2031, which makes it the fastest-growing geography in the GCC AI-powered Energy Management Software Market. The Abu Dhabi Department of Energy partnered with Presight and AIQ in 2025 to develop AI and digital transformation solutions and to establish a global AI center of excellence for the energy sector, demonstrating active public-sector support for scaling energy AI capabilities. Masdar and Presight also signed an agreement to develop AI-powered asset management tools for renewable energy projects, which ties software demand directly to the UAE’s expanding clean energy portfolio. The UAE, therefore, stands out as both a deployment market and a test environment for new operating models across utilities, renewables, and advanced commercial infrastructure.

The rest of the GCC is building depth more gradually, but it still matters for the longer-term outlook of the GCC AI-powered Energy Management Software Market. Oman, Kuwait, Qatar, and Bahrain are expanding regional opportunities through metering rollouts, enterprise digitization, and tighter energy data requirements within utilities and large organizations. Their near-term demand may be smaller than Saudi Arabia's or the UAE's, but they add breadth to utility modernization and facility management use cases. As these markets strengthen their digital infrastructure and reporting needs, they should support the next layer of regional adoption beyond the current leaders.

Competitive Landscape

The GCC AI-powered Energy Management Software Market remains moderately consolidated, with Schneider Electric, Siemens, Honeywell, ABB, and IBM holding strong positions through installed system compatibility, deep field integration, and established access to utility and large-enterprise buyers. Their advantage comes less from broad software branding and more from the ability to connect with existing control systems, meet local hosting needs, and support long implementation cycles. This keeps competition high in large accounts, but it also makes market entry difficult for suppliers that lack regional delivery depth. IBM strengthened its position in 2025 by expanding local SaaS hosting with AWS in the UAE and Saudi Arabia, which improved compliance readiness for enterprise customers. Schneider Electric and Siemens continue to benefit from their long presence in power, automation, and building systems, which gives them a natural route into adjacent AI energy software demand.

Strategic moves in the GCC AI-powered Energy Management Software Market indicate that incumbents are seeking to deepen software capabilities rather than relying solely on hardware relationships. IBM’s May 2026 collaboration with Aramco aimed to advance AI, agentic AI, and automation across Saudi industrial operations, which strengthens its visibility in one of the region’s largest industrial environments. DEWA and Siemens Energy moved forward with Phase 2 of the AI Plant Intelligent Controller after Phase 1 delivered measurable efficiency gains, providing Siemens with a concrete performance reference for utility-scale energy assets.[4]Dubai Electricity and Water Authority, “DEWA and Siemens Energy Drive Global Innovation with Phase Two of Groundbreaking AI Plant Intelligent Controller,” Dubai Electricity and Water Authority, dewa.gov.ae Johnson Controls also introduced Balanced Cooling in the UAE in April 2026, which shows how building-focused players are tailoring AI-led offerings to Gulf cooling and campus conditions.

Specialists still have room in the GCC AI-powered Energy Management Software Market where buyers need deeper AI functionality, localized use cases, or renewable-focused tools. The Abu Dhabi Department of Energy, Presight, and AIQ partnership shows how regional specialists can closely align with local digital energy priorities and gain relevance alongside global incumbents. Masdar’s agreement with Presight also suggests that renewable asset intelligence can become a meaningful niche for focused software providers. The next phase of competition is likely to depend on which vendors can combine secure deployment, smoother integration, and measurable operating outcomes without making implementation too complex.

GCC AI-powered Energy Management Software Industry Leaders

Cisco Systems, Inc.

Schneider Electric SE

Siemens AG

Honeywell International Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IBM and Aramco announced a strategic collaboration to advance AI, agentic AI, automation, and material science capabilities across Saudi Arabia's industrial sector, building on an established relationship focused on operational excellence and large-scale innovation.

- April 2026: Johnson Controls launched Balanced Cooling in the UAE, a purpose-built AI-driven solution for buildings connected to centralized cooling systems, specifically addressing low Delta-T performance and improving energy efficiency across mission-critical commercial campuses.

- October 2025: DEWA and Siemens Energy signed a Phase 2 agreement for the AI Plant Intelligent Controller at the Jebel Ali Power and Desalination Complex, following Phase 1 results that included efficiency improvement and a 35,000-tonne annual CO₂ reduction per power block.

- October 2025: IBM and AWS expanded their collaboration to host IBM SaaS products on AWS cloud regions in the UAE and Saudi Arabia, enabling locally compliant AI and data analytics for energy and industrial clients across both markets.

GCC AI-powered Energy Management Software Market Report Scope

The GCC AI-powered Energy Management Software Market comprises AI-driven platforms at the forefront of optimizing energy use, boosting efficiency, and advancing decarbonization goals. These sophisticated solutions harness real-time analytics, automation, and predictive modeling to meet the energy consumption needs of the industrial, commercial, and utility sectors. National vision programs, ambitious smart city initiatives, and robust investments in both renewable energy and digital infrastructure underpin the market's growth. By enabling organizations to monitor performance and curtail energy waste, these platforms play a pivotal role in enhancing sustainability metrics. Bolstered by strong government backing and monumental energy projects, the GCC stands out as a premier regional hub for cutting-edge energy management technologies.

The GCC AI‑Powered Energy Management Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud‑Based, On‑Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the size of the GCC AI-powered Energy Management Software Market?

The GCC AI-powered Energy Management Software Market was valued at USD 180.92 million in 2025, stands at USD 212.61 million in 2026, and is forecast to reach USD 507.23 million by 2031 at an 18.99% CAGR.

Which application leads revenue generation across the Gulf?

Energy consumption and demand optimization led with 48.22% of 2025 revenue, supported by strong demand from commercial buildings and high cooling-related power use.

Which end-user group is growing the fastest?

Utilities are projected to expand at a 21.32% CAGR through 2031 as smart metering, grid automation, and reliability-focused analytics move deeper into operations.

Why are commercial buildings the largest user base?

Commercial buildings held 58.91% of 2025 end-user revenue because hotels, offices, malls, and mixed-use assets have constant pressure to cut cooling-related energy waste.

Which Gulf country offers the strongest near-term opportunity?

Saudi Arabia led with 37.24% of 2025 revenue, while the UAE is expected to grow fastest at a 20.41% CAGR, making both countries the main demand centers through the forecast period.

What is driving software buyers toward hybrid deployment models?

Hybrid deployments are projected to grow at a 21.78% CAGR because many operators want to keep control logic on-premises while moving analytics, forecasting, and reporting to secure cloud layers.

Page last updated on: