GCC AI Copilot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

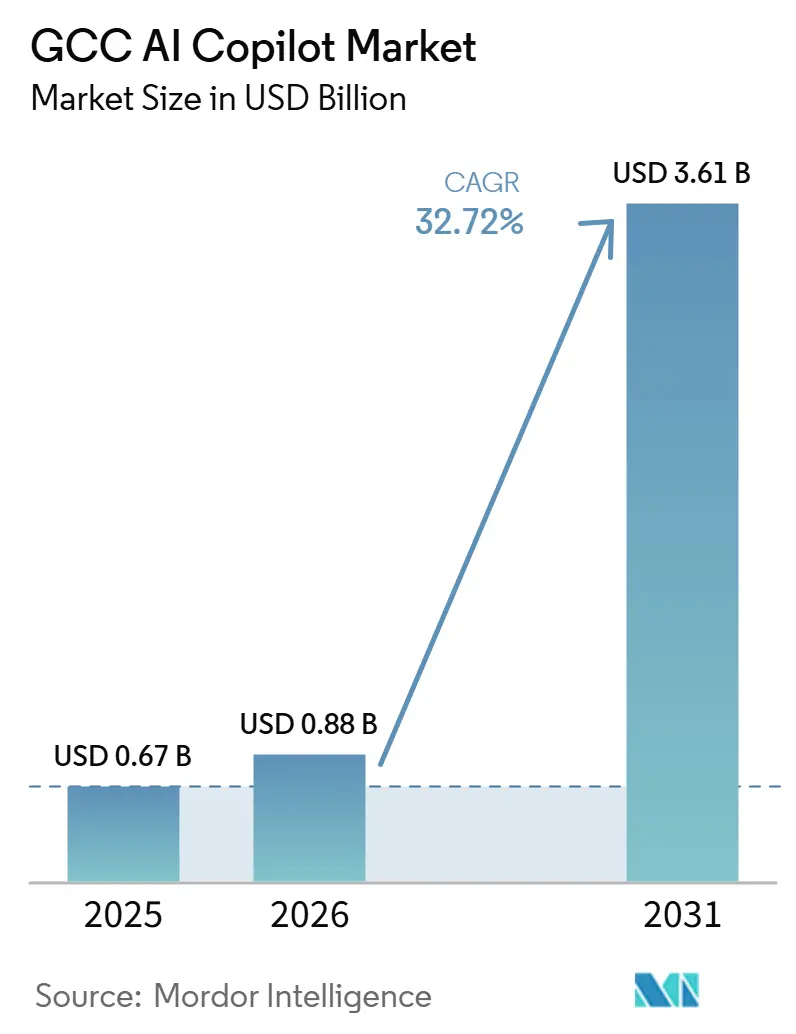

| Base Year Market Size (2025) | USD 0.67 Billion |

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 3.61 Billion |

| Growth Rate (2026 - 2031) | 32.72% CAGR |

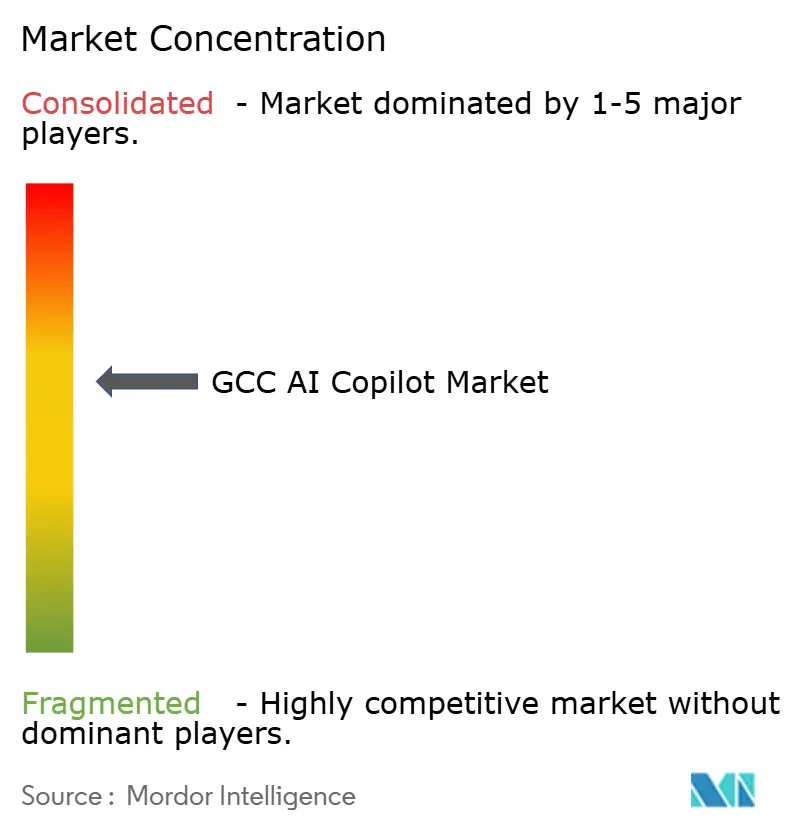

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC AI Copilot Market Analysis by Mordor Intelligence

The GCC AI copilot market size was valued at USD 0.67 billion in 2025 and is estimated to grow from USD 0.88 billion in 2026 to reach USD 3.61 billion by 2031, at a CAGR of 32.72% during the forecast period 2026-2031. The GCC AI copilot market is moving forward as enterprises no longer treat copilots as side tools but instead embed them into daily workflows, document tasks, service operations, and internal decision support. The region is also benefiting from steady sovereign infrastructure buildout, which is making it easier to support cloud access, local processing, and regulated deployment models at scale. Improving Arabic language skills is expanding the practical use of copilots across public services, banking, telecom, and large-employer environments, where English-only systems limit adoption. The GCC AI copilot market is also benefiting from the fact that leading software vendors are attaching AI capabilities to existing productivity, cloud, and enterprise application contracts, which lowers friction for first-time deployments. At the same time, compliance, data residency, and enterprise change management remain central buying filters, so commercial success in the GCC AI copilot market depends as much on trust and deployment design as on model capability.

Key Report Takeaways

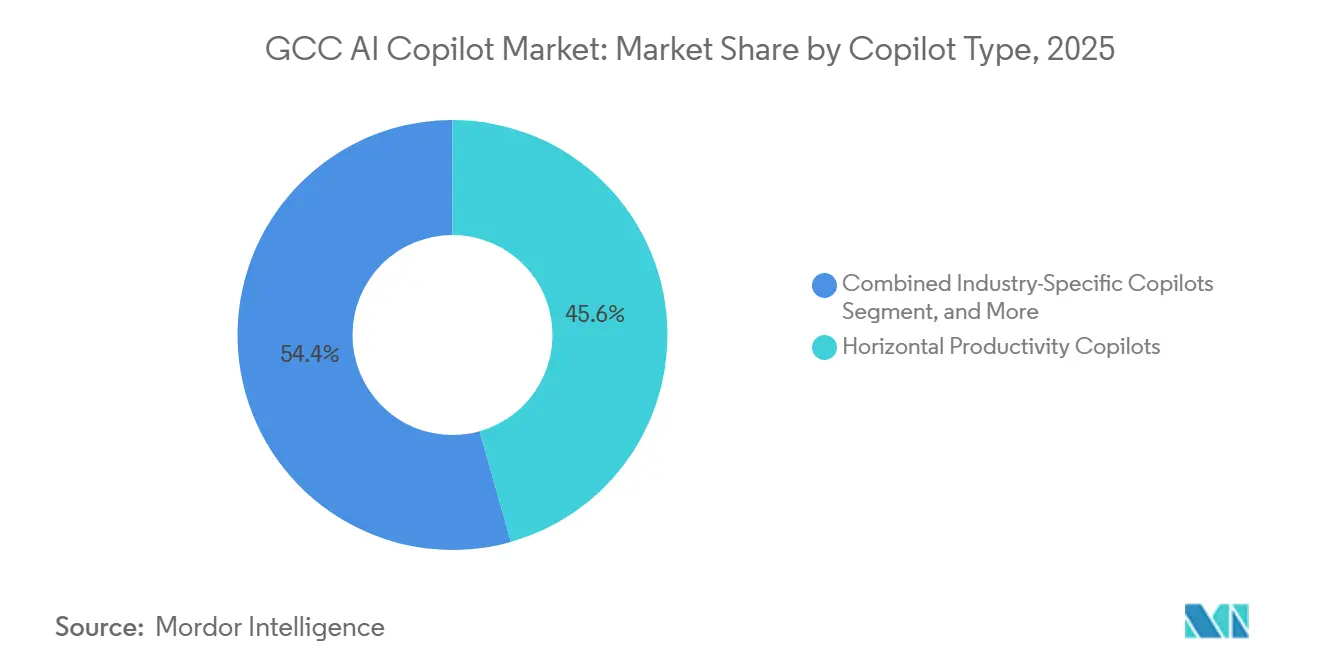

- By copilot type, horizontal productivity copilots held 45.62% of the GCC AI copilot market share in 2025, while industry-specific copilots are projected to expand at 35.14% CAGR through 2031.

- By deployment, cloud-based delivery accounted for 77.28% of revenue in 2025, while hybrid deployment is expected to grow at 34.82% CAGR through 2031.

- By organization size, large enterprises held 71.43% share in 2025, while SMEs are projected to expand at 35.36% CAGR through 2031.

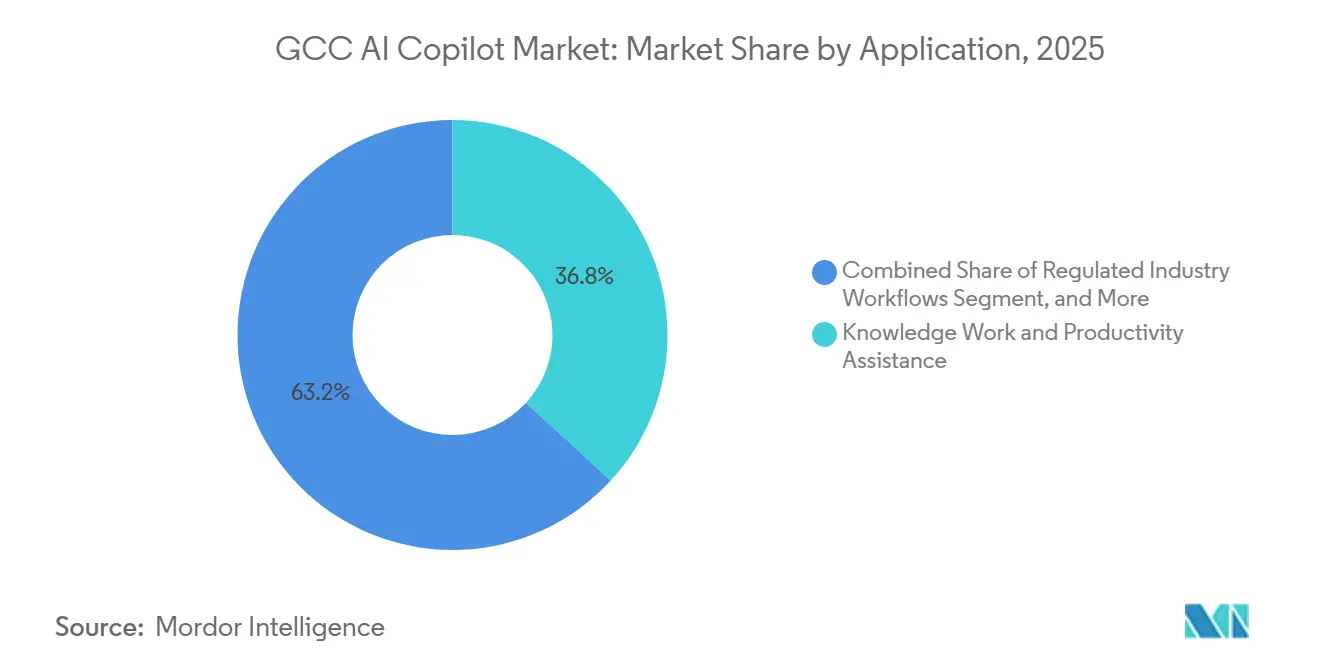

- By application, knowledge work and productivity assistance accounted for 36.84% share in 2025, while regulated industry workflows are projected to grow at 34.93% CAGR through 2031.

- By end-user industry, BFSI held 25.16% share in 2025, while government and administration are projected to expand at 36.21% CAGR through 2031.

- By geography, Saudi Arabia held 26.86% share in 2025, while Qatar is projected to record the fastest growth at 34.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC AI Copilot Market Trends and Insights

Drivers Impact Analysis*

| river | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Enterprise Copilot Adoption Across Knowledge Workflows | +7.5% | UAE and Saudi Arabia core, pan-GCC spillover | Short term (≤ 2 years) |

| Government-Led Digital Transformation and AI National Strategies | +6.8% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Arabic Language Support and Localization Improvements | +5.2% | Pan-GCC, led by Saudi Arabia and UAE | Medium term (2-4 years) |

| Integration With Microsoft 365, Google Workspace, and Salesforce Ecosystems | +4.6% | Pan-GCC | Short term (≤ 2 years) |

| Demand for Secure, Compliant AI in Regulated Industries | +4.1% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Growing Use of Domain-Specific Copilots in Customer Support and Internal Operations | +3.5% | Pan-GCC, with early gains in Kuwait and Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Copilot Adoption Across Knowledge Workflows

The GCC AI copilot market is advancing as enterprises move from limited testing to wider use in writing, summarization, internal search, workflow guidance, and employee support. SAP’s July 2025 Joule rollout at Red Sea Global covered human capital workflows for 10,500 employees, demonstrating that copilots can move from concept to large-scale operating environments in the region without remaining confined to innovation teams.[1]SAP Staff, “SAP’s AI-Powered Copilot, Joule, Deployed at Red Sea Global,” SAP MENA Press Room, news.sap.com Microsoft also announced in-country processing for Microsoft 365 Copilot in the UAE, removing one of the main barriers to broader enterprise adoption in regulated and government-linked settings. OpenAI’s July 2026 decision to make GPT-5.6 the preferred model in Microsoft 365 Copilot raised the capabilities available to organizations already in the Microsoft productivity stack, without forcing them to restart vendor selection or application redesign. The same pattern supports the GCC AI copilot market because buyers can activate AI within software that employees already use every day, reducing training friction and improving early adoption depth. As usage expands, prompt histories, workflow templates, and enterprise-specific data connections also make follow-on purchases easier, which supports a wider second wave of adoption across departments.

Government-Led Digital Transformation and AI National Strategies

The GCC AI copilot market is also being supported by state-backed digital agendas that favor local infrastructure, enterprise readiness, and regulated AI deployment. Qatar Investment Authority announced in December 2025 that Brookfield and Qai formed a USD 20 billion strategic investment partnership for AI infrastructure, signaling that sovereign capital in the region is backing the compute and platform layers that copilots need to scale.[2]Qatar Investment Authority Staff, “Brookfield and Qai Form $20 Billion Strategic Investment Partnership for AI Infrastructure,” Qatar Investment Authority, qia.qa Microsoft’s UAE copilot processing launch was built with local compliance alignment and showed that hyperscalers now treat sovereign deployment standards as a core commercial requirement rather than an optional regional add-on. Oracle reinforced this direction when it launched the first OCI Supercluster deployment in the UAE, giving enterprises access to sovereign AI compute relevant for large internal copilots and controlled inference workloads. These moves matter because public institutions and large regulated employers often become reference buyers for the rest of the economy, and their procurement standards shape the design choices of suppliers across the GCC AI copilot market. As more sovereign and semi-sovereign entities set local processing, auditability, and enterprise integration as minimum conditions, vendor roadmaps in the GCC AI copilot market are likely to stay closely tied to national digital priorities.

Arabic Language Support and Localization Improvements

Arabic support has become a practical requirement for the GCC AI copilot market, as many high-volume workflows involve citizen communication, internal policy materials, customer support, and regulated documentation that cannot rely on weak language coverage. The Jais 2 family was released in 8B and 70B variants and was pre-trained on 624 billion Arabic tokens, which showed that large-scale Arabic model development is no longer a theoretical regional ambition.[3]Jais Research Team, “Jais 2: A Family of Arabic-Centric Open Large Language Models,” Jais, jais.pages.dev Cohere’s Command R7B Arabic work also showed strong benchmark performance across instruction following, cultural knowledge, retrieval-augmented generation, and contextual faithfulness, which matters for enterprise applications that depend on consistency rather than novelty. This progress improves the quality ceiling for sector tuning and makes it easier for vendors to build tools that can handle Arabic prompts, Arabic documents, and mixed Arabic-English working environments. It also raises buyer expectations, because once strong Arabic performance becomes available, organizations are less willing to accept generic copilots that work well in English but fail in service, compliance, or policy tasks. In the GCC AI copilot market, better Arabic support not only widens adoption but also changes competitive positioning, as localization quality begins to influence contract wins, renewal strength, and long-term seat expansion.

Integration With Microsoft 365, Google Workspace, and Salesforce Ecosystems

The GCC AI copilot market benefits from the fact that AI functions are increasingly being embedded inside platforms that enterprises already license and operate. Microsoft’s in-country Microsoft 365 Copilot processing in the UAE gave existing Microsoft customers a path to adoption that aligned with both workflow familiarity and local compliance expectations. OpenAI’s model update in Microsoft 365 Copilot then improved the capabilities of that installed base, reinforcing the appeal of staying within established productivity environments rather than sourcing entirely separate AI systems. Salesforce supported the same pattern in Saudi Arabia through its USD 500 million investment, regional headquarters expansion in Riyadh, Arabic Agentforce commitments, and local skills development plans. SAP added another enterprise route via Joule, giving large ERP and human capital users a direct path to AI augmentation within systems they already trust for core operations. Because of this, the GCC AI copilot market is being shaped less by one-time experimental buying and more by the steady conversion of installed software estates into AI-enabled operating environments.[4]Salesforce Staff, “Salesforce Invests $500M in Saudi Arabia,” Salesforce News, salesforce.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Sovereignty And Cross-Border Data Transfer Constraints | -3.4% | Saudi Arabia, UAE, Qatar, Oman | Medium term (2-4 years) |

| High Cost Of Enterprise Deployment, Integration, And Change Management | -2.8% | Pan-GCC, highest impact in SME segment | Short term (≤ 2 years) |

| Limited High-Quality Arabic Enterprise Training Data | -2.1% | Pan-GCC | Long term (≥ 4 years) |

| AI Output Trust, Hallucination Risk, And Governance Gaps | -1.7% | Pan-GCC, concentrated in regulated sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Sovereignty And Cross-Border Data Transfer Constraints

Data residency remains one of the clearest limits on how quickly the GCC AI copilot market can scale across regulated environments. Microsoft’s UAE launch for in-country processing was important precisely because it addressed buyer concern over where data is processed and how enterprise content moves across borders. Oracle’s sovereign AI compute launch in Abu Dhabi highlighted the same issue: large buyers want infrastructure choices that let them pair advanced models with local control over sensitive workloads. This means the GCC AI copilot market does not reward model quality alone, since vendors also need to demonstrate where inference runs, how logs are stored, and whether enterprise data can remain within approved jurisdictions. The result is a market where globally known products may still face slower procurement if they cannot meet local hosting or compliance architecture requirements. That pressure is strongest in banking, government, utilities, and critical infrastructure, where trust, auditability, and processing location influence purchase timing as much as productivity gains.

High Cost of Enterprise Deployment, Integration, and Change Management

The GCC AI copilot market also faces friction from the real cost of implementation, especially when organizations want deeper deployment than simple seat activation. SAP’s Red Sea Global rollout showed that meaningful adoption often involves large workforce environments, workflow alignment, and operational system integration rather than a narrow software switch-on exercise. Salesforce’s Saudi buildout also reflected that enterprise expansion needs local partnerships, training capacity, and customer support ecosystems, which add cost and time before benefits become visible at scale. For many buyers, especially smaller firms, the challenge is not only license cost but also process redesign, security review, role mapping, usage governance, and employee adoption management. That is why the GCC AI copilot market often moves first in large organizations with stronger budgets and dedicated transformation teams. Over time, template-based deployments and packaged integrations should reduce this barrier, but in the near term, the cost of doing deployment properly still slows broad-based expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Copilot Type: Horizontal Productivity Leads, Vertical Models Accelerate

Horizontal productivity copilots accounted for 45.62% of revenue in 2025, placing them at the center of the GCC AI copilot market during the early phase of broad commercial adoption. Their lead came from a simple buying pattern: many organizations already ran Microsoft 365, SAP, or Salesforce, and could add AI support to the software employees used every day. This helped shorten approval cycles and made initial business cases easier to justify in writing, communication, summarization, and internal coordination tasks. Microsoft’s in-country processing launch in the UAE further strengthened this segment by removing a major compliance concern for customers who wanted productivity AI without shifting their core software stack. OpenAI’s preferred model upgrade in Microsoft 365 Copilot also increased the practical value of existing deployments and enabled greater usage within current customer accounts.

Industry-specific copilots are projected to grow at a 35.14% CAGR through 2031, making them the strongest long-term growth engine in the GCC AI copilot market. This shift reflects the needs of banks, government bodies, healthcare operators, and service-intensive employers that want copilots trained for narrower vocabulary, stronger controls, and more reliable task outcomes. The availability of Jais 2 and high-performing Arabic enterprise model research improves that transition because sector-specific tuning becomes more realistic when the language foundation is stronger. Functional workflow copilots and technical copilots should also grow as enterprises look beyond generic writing help and move into finance, HR, engineering, service, and policy workflows. In that sense, the GCC AI copilot industry is likely to keep horizontal tools as the first deployment layer while vertical tools capture the next wave of budget growth and differentiation.

By Deployment: Cloud Infrastructure Leads, Hybrid Gains Compliance Traction

Cloud-based deployment accounted for 77.28% of revenue in 2025, making it the dominant operating model in the GCC AI copilot market share in the base year. Cloud held this position because it offers faster activation, lower upfront infrastructure burden, and easier access to model upgrades, connector libraries, and productivity suite integration. For many enterprises, cloud remains the fastest way to move from evaluation to active usage, especially when copilots are tied to email, documents, meetings, knowledge bases, and workflow records. Microsoft’s UAE rollout of in-country Microsoft 365 Copilot processing showed that cloud adoption in the region is increasingly aligned with sovereign requirements rather than standing in opposition to them. That matters because it lets buyers retain the convenience of managed services while reducing concern around cross-border data movement and infrastructure control.

Hybrid deployment is projected to grow at a 34.82% CAGR through 2031, making it the fastest-rising delivery model as procurement matures. This growth reflects a middle path where organizations want the scale and update speed of cloud tools but still need local handling for more sensitive content, regulated records, or internal inference steps. Oracle’s sovereign AI compute expansion in Abu Dhabi supports that direction by giving enterprises more options to place high-value workloads inside regional infrastructure while continuing to use broader cloud ecosystems. On-premises models should remain relevant in defense, security, and certain critical infrastructure settings, although their volume base is likely to remain smaller than in cloud and hybrid environments. In practical terms, the GCC AI copilot market is moving toward a layered infrastructure model where deployment choice becomes part of the product decision rather than an afterthought. That shift also raises the importance of vendors that can support policy controls, local hosting options, and system integration without forcing customers into fully isolated environments. The GCC AI copilot industry, therefore, favors suppliers that can combine flexibility with governance rather than relying on a single deployment posture for every buyer.

By Organization Size: Large Enterprises Command Volume, SMEs Accelerate Fastest

Large enterprises accounted for 71.43% of the GCC AI copilot market in 2025, indicating that revenue was highly concentrated among larger employers during the early adoption stage. These organizations had the budget, governance structures, and application complexity to justify large deployments across multiple departments rather than single-team trials. They also tended to have long-standing software relationships with Microsoft, SAP, Salesforce, Oracle, and other major vendors, which made Copilot adoption easier to package into existing digital transformation programs. SAP’s Joule rollout at Red Sea Global, across 10,500 employees, offered a clear example of how enterprise-scale adoption can drive substantial contract value and serve as a visible reference case for the wider GCC AI copilot market. Large enterprises are therefore likely to remain the main revenue pool, even as adoption spreads further.

SMEs are projected to expand at a 35.36% CAGR through 2031, indicating strong momentum as cost, language, and deployment barriers continue to ease. Smaller firms usually need faster setup, clearer pricing, and immediate workflow value, which makes embedded productivity tools and packaged service copilots especially important for this segment. As Arabic model quality improves and enterprise platforms simplify configuration, more SMEs should find that copilots can support sales communication, customer support, document drafting, and daily administrative tasks without major custom build work. Microsoft, Salesforce, and other platform vendors are also expanding their regional partner and training ecosystems, which should gradually reduce onboarding friction for smaller users. The gap between large enterprises and SMEs is therefore more about current implementation depth than lack of long-term relevance. As copilots become more standardized, SMEs should contribute a larger share of net new user additions within the GCC AI copilot market.

By Application: Knowledge Work Anchors Revenue, Regulated Workflows Surge

Knowledge work and productivity assistance accounted for 36.84% of application revenue in 2025 and represented the largest share of the GCC AI copilot market size across use-case categories. The lead reflects the simple fact that writing, summarization, meeting support, search, drafting, and internal communication touch a very large share of office-based employees. These tasks also fit well with mainstream productivity suites, which lets enterprises introduce copilots without redesigning every business process on day 1. Microsoft 365 Copilot, SAP Joule, and related tools fit this pattern because they sit inside software environments that already handle documents, communication, records, and operational workflows. As a result, knowledge work should remain the primary revenue source even as other applications grow faster.

Regulated industry workflows are projected to grow at a 34.93% CAGR through 2031, making them the most dynamic application area in the GCC AI copilot market. This segment is rising because organizations in banking, government, utilities, and similar fields need controlled automation that can work within approval steps, documented processes, and local data rules. Oracle’s sovereign compute push and Microsoft’s local processing move both support that direction by making it easier to pair AI assistance with stronger control over sensitive records and inference paths. Customer and employee service operations, software engineering support, and business process assistance should also see healthy uptake, but regulated workflows can command higher strategic value once governance and audit needs are built into the product. This means growth in the GCC AI copilot market is not only coming from broader usage, but it is also driven by deeper workflow integration in environments where compliance design matters. Over time, success in these applications should strengthen vendor retention because switching costs rise when copilots become part of formal operational processes.

By End-User Industry: BFSI Leads, Government And Administration Accelerates Fastest

BFSI accounted for 25.16% of end-user revenue in 2025, making it the largest vertical in the GCC AI copilot market. Financial institutions have large knowledge workforces, high document intensity, and constant demand for internal productivity, service quality, workflow control, and risk-aware automation. They are also more likely than many sectors to invest in systems that improve accuracy, employee efficiency, and controlled response times across customer and internal operations. The rise of sovereign infrastructure offerings from Microsoft and Oracle is especially relevant here because banking-related workloads often require stronger location and oversight controls than general office usage. BFSI, therefore, combines readiness, budget, and regulatory pressure to support steady commercial demand across the GCC AI copilot market.

Government and administration is projected to expand at a 36.21% CAGR through 2031, making it the fastest-growing end-user category. Public-sector organizations often manage large volumes of forms, policies, correspondence, records, and service interactions, so they can benefit quickly when copilots are designed for structured workflow support. The GCC AI copilot market is well-positioned here because sovereign infrastructure investment and progress in Arabic model improve the fit for citizen-facing and policy-intensive tasks. IT and telecommunications, healthcare and life sciences, retail and e-commerce, industrial manufacturing, education and research institutions, and energy and utilities should also remain active demand pools as more organizations seek workflow-specific AI assistance. In the broader GCC AI copilot industry, this vertical mix matters because it prevents growth from relying on a single sector. It also means that vendors that can adapt a single core platform to multiple compliance settings may have stronger expansion paths than those tied to a single use case.

Geography Analysis

Saudi Arabia accounted for 26.86% of revenue in 2025, making it the largest national contributor to the GCC AI copilot market. Its position reflects strong enterprise digital demand, rising interest in Arabic-capable tools, and the need for local processing options across large employers and regulated institutions. Salesforce reinforced Saudi Arabia’s importance through its USD 500 million investment, the buildout of its Riyadh regional headquarters, its Arabic Agentforce commitment, and its local skills agenda. SAP also provided a practical adoption marker in the Kingdom through the Red Sea Global Joule deployment, which showed that enterprise copilots can move into large workforce environments with direct operational relevance. As local infrastructure and buyer readiness continue to improve, Saudi Arabia should remain a major anchor for the GCC AI copilot market.

The UAE remained the most operationally mature environment within the GCC AI copilot market because it combined enterprise demand with early sovereign-ready infrastructure options. Microsoft’s in-country Microsoft 365 Copilot processing in the UAE created an important commercial advantage for buyers who wanted productivity AI without sending sensitive content outside the country. Oracle strengthened the same ecosystem in Abu Dhabi through its OCI Supercluster deployment, which expanded sovereign AI compute capacity for enterprises seeking controlled, high-performance infrastructure. The UAE, therefore, serves as a proving ground where commercial rollout models, compliance patterns, and platform partnerships often take shape before spreading to the rest of the GCC AI copilot market.

Qatar is projected to grow at a 34.72% CAGR through 2031, making it the fastest-growing geography in the GCC AI copilot market. The December 2025 USD 20 billion Brookfield-Qai partnership sent a significant sovereign infrastructure signal to the country and positioned it to build stronger local AI capacity over the forecast period. Kuwait, Oman, and Bahrain should continue to add demand at a steadier pace, supported by regional vendor expansion and growing enterprise familiarity with copilots. Across these smaller markets, adoption is likely to follow practical templates proven first in Saudi Arabia and the UAE, which should help the GCC AI copilot market spread without requiring every country to build a full local ecosystem at the same speed.

Competitive Landscape

The GCC AI copilot market is moderately concentrated at the enterprise platform layer, where a small set of global technology vendors controls much of the installed base of productivity, cloud, and applications. Microsoft holds a strong structural position because it combines workplace software, cloud infrastructure, and local processing capabilities in a form that meets the needs of enterprises and public sectors in the region. OpenAI’s preferred model role in Microsoft 365 Copilot further strengthens that position by upgrading capabilities within an already-deployed enterprise environment rather than asking customers to adopt a separate AI estate. SAP and Salesforce also occupy important competitive ground because both can bring copilots into enterprise systems that already manage operations, workforce records, customer engagement, and sector-specific processes. The result is a market where competition is shaped less by stand-alone chatbot visibility and more by which vendors can attach AI value to software environments that customers already trust.

Strategic moves in 2025 and 2026 have made that pattern clearer. Microsoft’s launch of in-country Microsoft 365 Copilot processing in the UAE turned compliance readiness into a commercial differentiator rather than a technical detail. Salesforce’s USD 500 million commitment in Saudi Arabia signaled that language support, regional headquarters presence, and ecosystem building can all matter in winning future workloads. SAP’s Joule deployment at Red Sea Global demonstrated that copilots can be directly tied to enterprise operations at scale, helping vendors move the conversation from experimentation to measurable business use. Oracle’s sovereign AI compute investment added another layer of competition by strengthening the infrastructure side of enterprise AI delivery in the region.

The GCC AI copilot market still leaves room for specialized challengers even with these larger platforms in place. Glean reported more than USD 250 million in ARR and more than 150% year-over-year growth in 2025, which shows that platform-agnostic work AI can still carve out strong demand when it solves search, knowledge access, and multi-system productivity problems. Arabic-native model development also gives regionally aligned providers a path to differentiate when they can combine local language strength with enterprise deployment discipline. In practical terms, the most durable competitive advantages in the GCC AI copilot market are likely to come from compliance fit, Arabic quality, deep workflow integration, and strong delivery partnerships. Vendors that meet all 4 conditions should be better positioned than those competing solely on general model access.

GCC AI Copilot Industry Leaders

Microsoft Corporation

Alphabet Inc

OpenAI, L.L.C

Salesforce, Inc

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: OpenAI designated GPT-5.6 as the preferred model within Microsoft 365 Copilot, raising the capability ceiling for GCC enterprises using the Microsoft productivity stack and broadening Copilot's competitive positioning against standalone generative AI platforms in regulated enterprise environments.

- June 2026: SAP unveiled its Autonomous Enterprise strategy at SAP Sapphire 2026, launching the unified SAP Business AI Platform and Joule Studio, an agentic AI workflow builder, alongside platform partnerships with Anthropic, Google Cloud, Microsoft, Cohere, and Mistral AI. The strategy directly targets GCC enterprises running SAP ERP across BFSI, manufacturing, and government verticals.

- December 2025: Brookfield and Qai, Qatar's AI company and a subsidiary of the Qatar Investment Authority, formed a USD 20 billion joint venture to invest in AI infrastructure in Qatar and select international markets, establishing the sovereign capital base for Qatar's enterprise AI and copilot adoption expansion.

- October 2025: Microsoft announced in-country data processing for Microsoft 365 Copilot in the UAE, hosted in Dubai and Abu Dhabi datacenters and fully compliant with the UAE Cybersecurity Council's AI Policy. The capability, made available in early 2026, was developed in collaboration with the Cybersecurity Council and Dubai Electronic Security Center to remove the data sovereignty barrier from public-sector copilot adoption.

GCC AI Copilot Market Report Scope

The GCC AI copilot market refers to the ecosystem of artificial intelligence-driven intelligent assistants integrated into enterprise and consumer software applications to enhance human capabilities and automate complex tasks across the Gulf Cooperation Council (GCC) countries. These copilots leverage advanced foundation models, including large language models (LLMs) and generative AI, to provide real-time contextual suggestions, generate content, analyze data, and execute workflows seamlessly within existing digital tools. The market encompasses various copilot types ranging from general horizontal productivity tools to specialized functional, technical, and industry-specific solutions. Deployed across cloud-based, hybrid, and on-premises environments, these AI systems cater to organizations of all sizes across the GCC region. They are used across diverse applications, including knowledge work assistance, software development, customer service, and sales enablement, in industries such as IT, BFSI, healthcare, and government. Driven by aggressive national vision programs (such as Saudi Vision 2030 and the UAE Centennial 2071), rapid smart city developments, and a strong strategic push to diversify economies away from oil dependency, AI copilots help GCC organizations drive operational efficiency, foster innovation, and accelerate their transition into highly digitized, knowledge-based economies.

The GCC AI Copilot Market Report is Segmented by Copilot Type (Horizontal Productivity Copilots, Functional Workflow Copilots, Technical and Engineering Copilots, and Industry-Specific Copilots), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Knowledge Work and Productivity Assistance, Software Engineering and Technical Operations, Customer and Employee Service Operations, Sales, Marketing and Revenue Enablement, Business Process and Enterprise Operations, and Regulated Industry Workflows), End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Industrial Manufacturing, Education and Research Institutions, Media and Entertainment, Government and Administration, Energy and Utilities, and Other End-User Industries), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Productivity Copilots |

| Functional Workflow Copilots |

| Technical and Engineering Copilots |

| Industry-Specific Copilots |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations |

| Customer and Employee Service Operations |

| Sales, Marketing and Revenue Enablement |

| Business Process and Enterprise Operations |

| Regulated Industry Workflows |

| IT and Telecommunication |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Education and Research Institutions |

| Media and Entertainment |

| Government and administration |

| Energy and Utilities |

| Other End-User Industries |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Copilot Type | Horizontal Productivity Copilots |

| Functional Workflow Copilots | |

| Technical and Engineering Copilots | |

| Industry-Specific Copilots | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations | |

| Customer and Employee Service Operations | |

| Sales, Marketing and Revenue Enablement | |

| Business Process and Enterprise Operations | |

| Regulated Industry Workflows | |

| By End-User Industry | IT and Telecommunication |

| BFSI | |

| Healthcare and Life Sciences | |

| Retail and E-Commerce | |

| Industrial Manufacturing | |

| Education and Research Institutions | |

| Media and Entertainment | |

| Government and administration | |

| Energy and Utilities | |

| Other End-User Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the current and forecast value of the GCC AI copilot space?

The GCC AI copilot market size stood at USD 0.67 billion in 2025, is estimated at USD 0.88 billion in 2026, and is forecast to reach USD 3.61 billion by 2031 at a 32.72% CAGR.

Which copilot type leads revenue across the GCC?

Horizontal productivity copilots led with 45.62% revenue share in 2025 because enterprises first deployed AI inside familiar productivity and enterprise software environments.

Which deployment model is expanding fastest in the GCC region?

Hybrid deployment is projected to grow at 34.82% CAGR through 2031 as enterprises seek a balance between cloud scale and local control over sensitive workloads.

Why is BFSI the leading end-user category for these tools?

BFSI led with 25.16% share in 2025 because financial institutions need productivity gains, workflow control, and stronger support for regulated records and customer operations.

Which country is growing fastest for AI copilots in the GCC?

Qatar is projected to expand at 34.72% CAGR through 2031, supported by major sovereign AI infrastructure investment through the Brookfield and Qai partnership.

What are the biggest barriers to wider enterprise adoption?

Data sovereignty, cross-border transfer limits, integration cost, and change management remain the main barriers, especially for regulated buyers and smaller organizations.

Page last updated on: