Functional Native Starch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

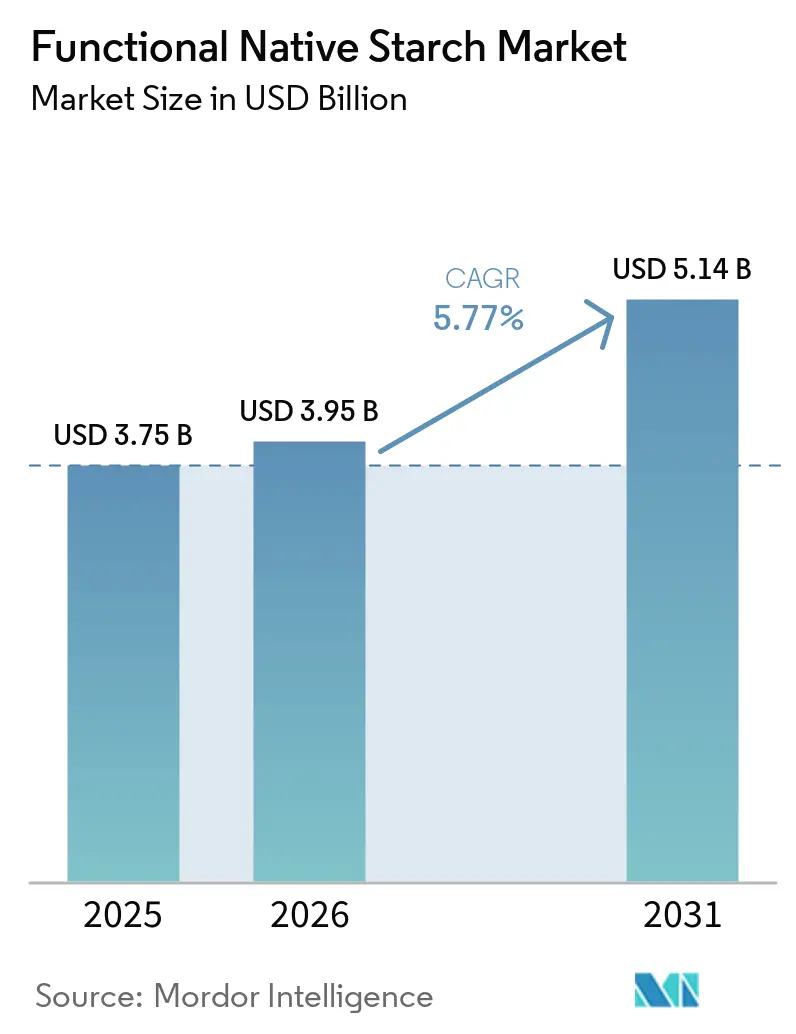

| Market Size (2026) | USD 3.95 Billion |

| Market Size (2031) | USD 5.14 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

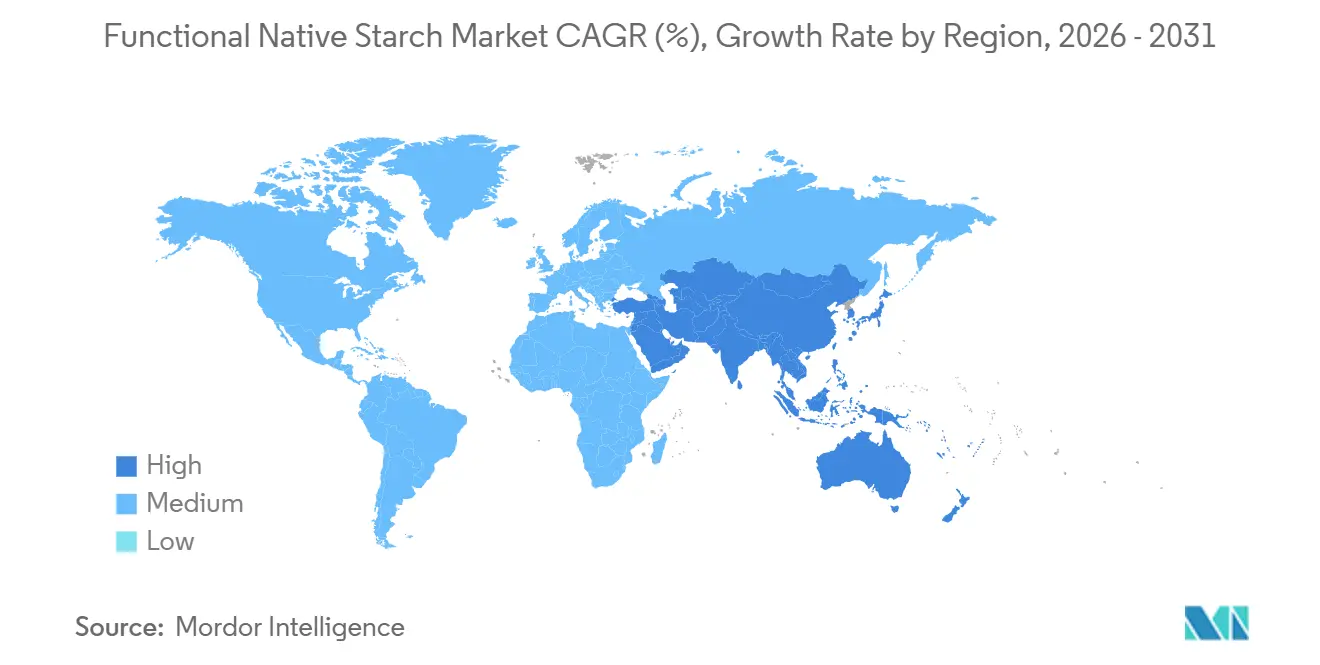

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Functional Native Starch Market Analysis by Mordor Intelligence

The Functional native starch market size is expected to increase from USD 3.8 billion in 2025 to USD 4.0 billion in 2026 and reach USD 5.1 billion by 2031, growing at a CAGR of 5.8% over 2026-2031. Driven by regulatory pressures and shifting consumer preferences, the Functional Native Starch market is witnessing significant growth. Buyers across food, pharmaceutical, and industrial sectors are increasingly opting for native starches over their chemically modified counterparts and synthetic texturants, drawn by the appeal of simpler label declarations. This trend is further bolstered by tightening regulations, especially in major consuming regions, that emphasize organic compliance, ingredient traceability, and stringent packaging rules [1]Source: United States Department of Agriculture, "Organic Regulations", ams.usda.gov. Native starches are carving out a niche in applications that demand cost-effective functionality and satisfactory process performance, all without resorting to chemically modified ingredients. Moreover, the market is benefiting from the heightened demand for paper and board coatings, especially as European packaging regulations underscore the importance of PFAS-free material choices [2]Source: European Commission, "Packaging Waste Regulation", environment.ec.europa.eu. However, challenges loom large: raw material volatility, constraints in non-GMO sourcing, and humidity-related handling issues are influencing supplier strategies, product positioning, and investment decisions in the Functional Native Starch market.

Key Report Takeaways

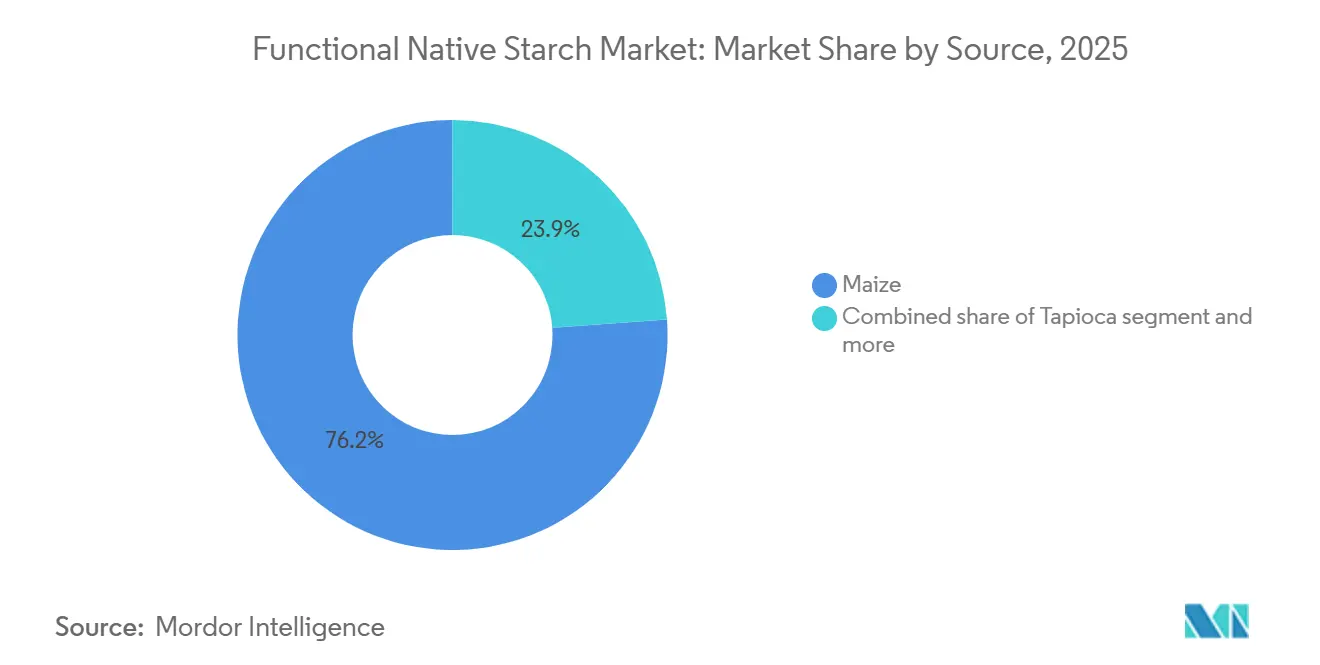

- By source, corn accounted for the largest share of the functional native starch market, at 76.2% in 2025, while tapioca is projected to grow at the fastest CAGR of 5.5% during 2026-2031.

- By form, powder led the functional starch market with a 74.2% share in 2025, while liquid is anticipated to register the fastest CAGR of 5.1% during 2026-2031.

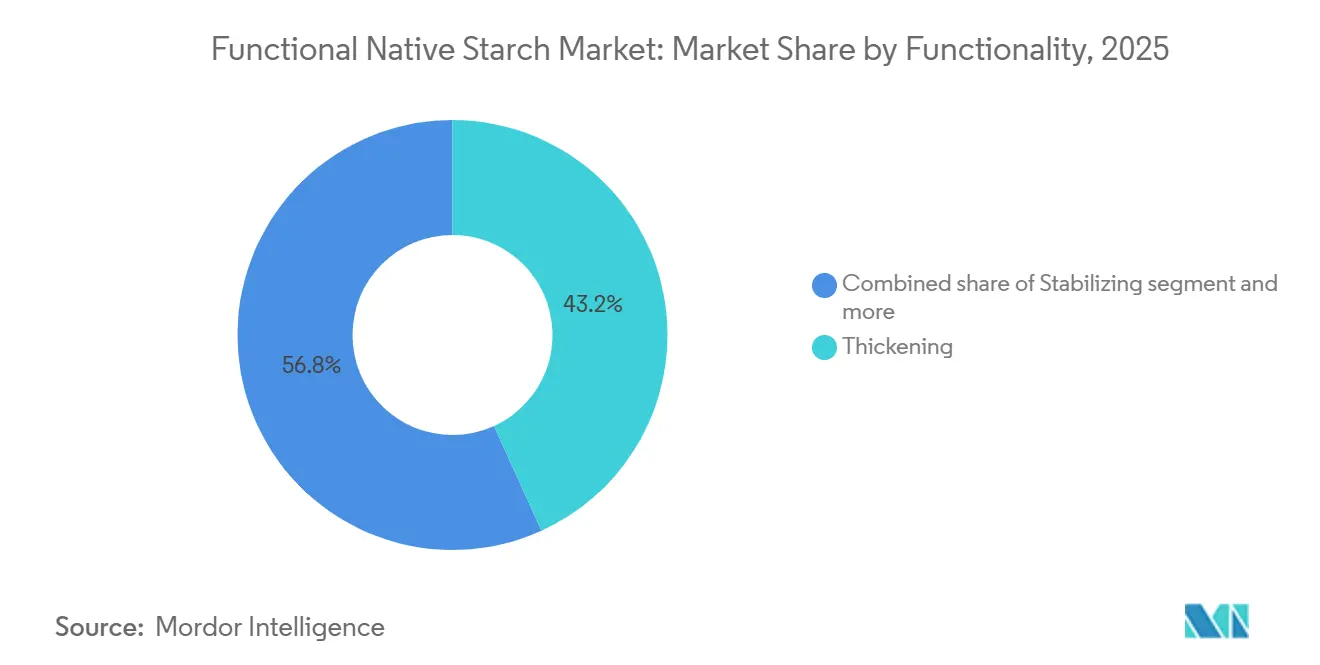

- By functionality, thickening led the functional starch market with a 43.2% share in 2025, while stabilizing is anticipated to register the fastest CAGR of 5.1% during 2026-2031.

- By application, food and beverages led the functional starch market with a 57.2% share in 2025, while stabilizing is anticipated to register the fastest CAGR of 57.2% during 2026-2031.

- By geography, Asia-Pacific led with 34.9% of 2025 sales, whereas the Middle East and Africa are projected to register the fastest growth, at a 6.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Functional Native Starch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label reformulation and ingredient transparency | +1.5% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Functional native starch as a cost-competitive alternative to hydrocolloids | +1.2% | Global, with strongest pull in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion in plant-based dairy and meat formulations | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising demand for non-gmo and organic food inputs | +0.7% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Growth in natural excipients for oral solid dosage pharmaceuticals | +0.6% | Asia-Pacific, Middle East and Africa, South America | Medium term (2-4 years) |

| Industrialization of native starch in paper, packaging, and bio-based materials | +0.5% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clean-Label Reformulation and Ingredient Transparency

As the market for functional native starches evolves, there's a noticeable trend: a push towards simpler ingredient statements and a growing aversion to additives that sound overly chemical. Native starches, whether labeled as corn, tapioca, or potato starch, offer a solution, allowing for familiar terminology rather than more technical descriptions. This is particularly significant in packaged foods, where reformulation choices are increasingly weighing label clarity against cost and processing efficiency. Furthermore, organic compliance regulations in the U.S. and Europe are bolstering this trend. These regulations tighten the scope for ingredient substitutions and emphasize the importance of traceable sourcing and approved input lists. Consequently, in the functional native starch market, demand remains anchored to long-term product reformulation initiatives, rather than being swayed by fleeting seasonal trends.

Functional Native Starch as a Cost-Competitive Alternative to Hydrocolloids

Buyer interest in functional native starches is on the rise, driven by a desire for ingredients that provide effective thickening and texture without the premium costs of hydrocolloids. This trend of substitution is most pronounced in formulations with milder process conditions, where native starch can achieve desired texture targets without the need for chemical modifications. However, this shift isn't consistent across all applications; for instance, systems that are acidic, frozen, or subjected to very high shear still highlight the limitations of native starch performance. Nevertheless, the market for functional native starches is buoyed as suppliers enhance process tolerance using physical treatment methods, all while maintaining the essence of native positioning. Consequently, the ability to develop products emerges as a crucial competitive edge, rivaling even access to raw materials.

Rising Demand for Non-GMO and Organic Food Inputs

Stronger demand for non-GMO and organic grades is evident in the Functional native starch market, yet scaling supply to meet this demand proves challenging. As of July 2024, the USDA's 2025 technical review noted that only 123 operations in the U.S. were certified as organic cornstarch handlers, with most being distributors rather than primary producers. In Europe, tighter regulatory rules apply, as cornstarch isn't recognized as a permitted non-organic ingredient in organic processed products under EC Regulation 2021/1165[3]Source: European Commission, "Organic production and products", agriculture.ec.europa.eu. Such regulations favor producers with identity-preserved supply chains, whether corn, potato, or tapioca, while sidelining those reliant on commodity procurement. Consequently, the Functional native starch market features a distinct premium tier, where the ability to certify and trace products carries equal weight with production volume.

Growth in Natural Excipients for Oral Solid Dosage Pharmaceuticals

Pharmaceuticals are increasingly turning to functional native starch, using it as a binder, disintegrant, and diluent in the production of oral solid dosage forms. A 2025 study published in the Indian Journal of Natural Products and Resources highlighted the physicochemical properties and formulation significance of native starches derived from various botanical sources for pharmaceutical applications. Another 2025 study on ScienceDirect revealed that rice starch-based co-processed excipients enhance direct compression and colon-targeted delivery. These findings elevate the perception of native starch in the functional native starch market, moving it beyond its traditional role as a low-value commodity excipient. The demand for native starch is surging, particularly in regions witnessing a boom in generic drug manufacturing. Here, buyers are keen on sourcing natural-origin materials that meet established quality standards, such as Codex CXS 77-1981.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material volatility in maize, potato, tapioca, and wheat supply | -0.9% | Global, most acute in North America, Europe, and Southeast Asia | Short term (≤ 2 years) |

| Moisture and shelf-life sensitivity in high-humidity distribution environments | -0.5% | Asia-Pacific core, with spillover to Middle East and Africa | Medium term (2-4 years) |

| Functionality gap versus modified starches in high-stress processing | -0.7% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Certification bottlenecks for organic, non-GMO, and identity-preserved grades | -0.4% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Volatility in Maize, Potato, Tapioca, and Wheat Supply

Raw material volatility continues to challenge the functional native starch market. Starch prices are heavily influenced by agricultural conditions, trade dynamics, and certification requirements. Insights from user-supplied content highlight a tight supply of tapioca and organic potato starch. Even with increased planted areas, premium-grade availability remains a challenge. Factors such as processor certification, identity preservation, and weather-related impacts can restrict usable supply, despite an overall boost in crop output. Consequently, the market grapples with margin pressures. While conventional supplies may seem sufficient, constraints on certified or application-specific grades become evident. As a result, procurement strategies, contract structures, and source diversification take precedence in supplier decision-making.

Moisture and Shelf-Life Sensitivity in High-Humidity Distribution Environments

In humid regions, handling challenges plague the functional native starch market. During shipping and storage, powdered starch is prone to moisture absorption. Once moisture seeps in, the starch can clump, lose viscosity, or become more susceptible to microbial degradation, all before it reaches the processor. This concern is particularly pronounced in Southeast Asia, West Africa, and other tropical areas, where humidity control is often inconsistent. As a result, companies in the functional native starch market are leaning towards local supplies, investing in moisture-barrier packaging, or exploring alternative delivery methods. These adjustments are made with an eye on fast-growing, yet climate-sensitive, markets. Furthermore, while companies strive to meet food safety compliance standards, the added documentation and packaging costs don't entirely mitigate the associated physical risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Corn Dominates, Tapioca Gains Through Clean-Label Functionality

In 2025, corn (maize) dominated the Functional native starch market, capturing a substantial 76.2% share. This dominance is largely attributed to North America and China's extensive wet-milling infrastructure and the cost advantages corn offers to both food and industrial sectors. However, there's a caveat: the USDA highlighted that in 2024, a staggering 94% of U.S. corn was genetically engineered. This prevalence complicates identity-preserved procurement, especially for organic and non-GMO initiatives. Such complexities are significant; buyers in the premium food and pharmaceutical sectors prioritize consistent traceability over mere crop abundance. While corn firmly anchors mainstream demand in the Functional native starch market, its rigidity becomes evident under stringent certification rules.

Tapioca is set to outpace its competitors, projected to grow at a robust 5.5% CAGR from 2026 to 2031, marking it as the fastest-growing source in the Functional native starch arena. Its rising popularity can be attributed to its neutral flavor, clarity in pastes, and a cleaner non-GMO stance, making it a perfect fit for premium sauces, plant-based foods, and other label-sensitive items. Thailand's cassava production surged to 24.98 million tons in the 2024/2025 season, up from 21.82 million tons in the 2023/2024 season. This increase provides the region with ample raw material to expand tapioca starch capacities and boost export supplies. Moreover, tapioca sidesteps the challenges of procuring genetically engineered crops that corn faces, streamlining certification for numerous buyers. As a result, while tapioca's current market presence is dwarfed by corn, it boasts a strategically advantageous position in non-GMO and clean-label initiatives.

By Form: Powder Entrenched, Liquid Format Accelerates in Industrial Channels

In 2025, powder accounted for 74.2% of the Functional Native Starch market. Its supremacy stems from advantages such as a longer shelf life, ease of transport, and compatibility with dry-blending systems prevalent in the food and pharmaceutical sectors. Production lines often favor free-flowing powder inputs, making transitions to liquid forms challenging and costly unless clear benefits are evident. Furthermore, powder's practicality shines in broad distribution, catering to numerous small and mid-scale clients with standard handling systems. Thus, in the Functional Native Starch arena, powder stands as a structural leader, not merely a default choice.

Liquid, on the other hand, is set to grow at a 5.1% CAGR from 2026 to 2031, emerging as the fastest-growing variant in the Functional Native Starch market. Its growth is particularly pronounced in paper, board, and coating sectors, where continuous dispensing aligns seamlessly with industrial production lines, outpacing dry input systems. Europe's ongoing packaging transition is pivotal, as starch-based barrier systems are gaining traction, especially with the shift away from PFAS-based coatings under Regulation (EU) 2025/40. In these contexts, liquid dispersions seamlessly integrate into coating processes, enhancing throughput. This landscape reveals a divergence in the Functional Native Starch market: while powder maintains its broad leadership, liquid is reaping significant rewards, especially in industrial packaging applications.

By Functionality: Thickening Remains the Anchor, Stabilizing Scales Fast

In 2025, thickening claimed a dominant 43.2% share of the Functional native starch market, underscoring its status as the leading functionality segment. This prominence is rooted in the traditional application of native starch in a variety of products, including soups, gravies, sauces, dairy items, and processed meats, where achieving the right viscosity is paramount. Native starch has cemented its position in these applications due to its ability to meet texture goals cost-effectively and with familiar labeling. Furthermore, the thickening segment enjoys widespread patronage, with both major processors and smaller regional manufacturers relying on its functionality in their daily operations. Thus, in the Functional native starch market, thickening serves as the foundational application, enabling many suppliers to scale and optimize their plant usage.

Stabilizing is poised to achieve a 5.1% CAGR from 2026 to 2031, emerging as the fastest-growing functionality segment in the Functional native starch market. This growth trajectory is bolstered by a shift towards cleaner-label formulations and advancements in physically treated starches, which exhibit enhanced structural integrity during processing and storage. Insights from industry players highlight a surge in product innovations focused on enhancing granular stability and viscosity retention sans chemical modifications, indicating a clear direction for technical investments. A testament to this trend is Ulrick & Short’s 2025 Synergie A range, designed specifically to bolster native starch stability in cooking-intensive applications. Consequently, the Functional native starch market is evolving, transitioning from its foundational thickening role to embracing more sophisticated stability functions that were previously challenging for native products to achieve.

By Application: Food and Beverages Lead, Pharmaceuticals Accelerate

In 2025, food and beverages commanded a dominant 57.2% share of the Functional native starch market. This sector's prominence stems from its extensive application in bakery, dairy, sauces, confectionery, and plant-based foods, where starch plays a pivotal role in enhancing texture, binding water, and ensuring consistent processing. Given the vastness of this application base, it's poised to remain a focal point, even as emerging uses accelerate. Additionally, ongoing reformulation activities underscore a steady demand, as food manufacturers seek ingredients that balance label simplicity, cost-effectiveness, and dependable plant performance. Thus, in the realm of Functional native starch, food and beverages stand out as the primary demand hub, thanks to their combination of volume, consistent consumption, and extensive product range.

Pharmaceuticals are set to grow at a robust 5.7% CAGR from 2026 to 2031, emerging as the fastest-growing segment in the Functional native starch market. This surge is attributed to the burgeoning production of generic oral solid dosage forms in nations such as India, Indonesia, Egypt, and Saudi Arabia, where tablet manufacturing is scaling up. Native starch seamlessly integrates into these processes as a binder, diluent, and disintegrant. Moreover, its profile, derived from natural sources, aligns with regulatory standards, particularly under Codex quality benchmarks. A 2025 study published in the Research Journal of Pharmacy and Technology highlighted that potato starch not only met but exceeded hardness and disintegration metrics for direct-compression tablet formulations. This positions the Functional native starch market as not just reliant on food but also bolstered by a rapidly expanding pharmaceutical sector.

Geography Analysis

In 2025, the Asia-Pacific region dominated the Functional native starch market, accounting for 34.9% of the market share. The region's strength lies in its rich raw material resources and a diverse food processing industry, notably in cassava cultivation and tapioca processing in Thailand, Vietnam, and Indonesia. For the 2024/2025 period, Thailand produced 24.98 million tons of cassava, bolstering both its local starch production and the broader regional supply. China's expanding premium food processing sector further cements the region's dominance, as it increasingly seeks localized formulation support. Highlighting this trend, Roquette inaugurated its Starch & Polyol Pilot Center in Lianyungang in March 2026, underscoring major suppliers' commitment to developing regional applications near demand hubs.

Between 2026 and 2031, the Middle East and Africa are set to lead the pack with a projected 6.2% CAGR in the Functional native starch market. This growth is fueled by surging processed food consumption, urbanization, and an expanding halal-compliant food sector in countries such as Egypt, Saudi Arabia, and Nigeria. Furthermore, the region's significance is underscored by its burgeoning pharmaceutical demand, with tablet production and generic medicine supply chains on the rise. However, challenges such as moisture control, reliance on imported supplies, and stringent traceability requirements pose hurdles to deeper market penetration.

While North America and Europe are established players in the Functional native starch market, their roles are strategically pivotal. In North America, the emphasis on non-GMO and organic sourcing underscores the importance of traceability in premium product development. Meanwhile, Europe is driving fresh industrial demand, particularly with PFAS-free paper and board coatings, in line with Regulation (EU) 2025/40. South America, though less detailed in user-supplied content compared to Asia-Pacific or Europe, remains significant as a cassava-centric supply hub and a regional food processing center. Collectively, the landscape of the Functional native starch market reveals a distinct geographic divide: Asia-Pacific leads in scale, the Middle East outpaceca outpaces in growth, and North America and Europe set the benchmarks for standards, certifications, and industrial applications.

Competitive Landscape

The Functional native starch market is led by a small group of global agribusiness and specialty ingredient companies, but it still leaves room for regional suppliers with strong local sourcing or application focus. Cargill, Archer Daniels Midland, Ingredion, Roquette, AGRANA, Emsland Group, Avebe, Thai Wah, and Sanstar operate across different source bases, end uses, and regional strengths. The industry's giants leverage their scale in wet milling and global customer relationships, serving food, pharmaceutical, and industrial clients through a unified supply network. Meanwhile, regional specialists carve out their niche by providing local feedstock access, swift commercial responses, and focused portfolios in areas such as potato, tapioca, non-GMO corn, or pharmaceutical grades. This dynamic keeps the functional native starch market competitive, even as leading multinationals steer the broader investment and product development trajectory.

In a significant strategic move, Ingredion announced its all-cash acquisition of Tate & Lyle in June 2026, valued at USD 5.0 billion. Upon completion, this deal promises to amalgamate capabilities in starch, texturants, sugar reduction, mouthfeel enhancement, and fortification, thereby amplifying Ingredion’s reach in specialty ingredients. Roquette, not to be outdone, inaugurated its Starch & Polyol Pilot Center in Lianyungang in March 2026, underscoring its commitment to localized development and pilot-scale support for regional clientele. Such maneuvers highlight that the functional native starch market's competition transcends mere commodity volume, delving into formulation prowess, application agility, and premium technical services.

The mid-tier dynamics play a pivotal role in the functional native starch market. Suppliers like AGRANA, Emsland, Avebe, Thai Wah, and Sanstar carve out unique competitive paths. European entities gravitate towards physically treated starches and offer robust technical support. In contrast, Asian suppliers capitalize on their proximity to cassava or corn sources, ensuring reliable delivery economics. Roquette's launches of AMYSTA L 123 in October 2025 and ST 305 in April 2025, both targeting the cosmetics market, further illustrate the industry's shift. Producers are not just confining native starch to traditional realms but are expanding its footprint into label-friendly food systems and diverse non-food applications. Consequently, market leadership hinges on a blend of raw-material mastery, depth of certification, process expertise, and the knack for tailoring native starches to specific applications.

Functional Native Starch Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Ingredion Incorporated

-

Tate and Lyle PLC

-

Roquette Frères

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Ingredion Incorporated announced a recommended all-cash acquisition of Tate & Lyle PLC for approximately USD 3.6 billion in cash, implying a total enterprise value of approximately USD 5.0 billion.

- March 2026: Roquette inaugurated its new Starch & Polyol Pilot Center at the Lianyungang, China facility, spanning more than 1,000 square meters. The investment, initiated in late 2024, integrates physicochemical analysis, lab-scale research, and pilot-scale industrial transformation into a unified platform for the starch and polyol sector, designed to accelerate development cycles and improve responsiveness to Chinese and regional customer formulation needs.

- October 2025: Roquette launched AMYSTA L 123, the first product in its AMYSTA label-friendly starch range, developed via a patented process using no enzymes or chemicals. The thermally soluble pea starch is suitable for dry mixes, ready-to-mix beverages, and condiment systems, expanding clean-label starch options for food manufacturers targeting plant-based and simplicity-positioned categories. The product was announced in October 2025.

- April 2025: Roquette Beauté launched ST 305 (INCI Amylopectin) at In-Cosmetics Global 2025 in Amsterdam (April 8-10, 2025). The amylopectin-based powder ingredient offers an alternative to mineral and synthetic powders for makeup, skin care, and hair care applications, and was shortlisted for the In-Cosmetics Global 2025 Innovation Zone Best Ingredient Award in the Functional Category.

Global Functional Native Starch Market Report Scope

| Corn |

| Wheat |

| Potato |

| Tapioca |

| Others |

| Powder |

| Liquid |

| Thickening |

| Stabilizing |

| Gelling |

| Emulsifying |

| Others(If Any) |

| Food and Beverages |

| Pharmaceutical |

| Personal Care and Cosmetics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Morocco | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Source | Corn | |

| Wheat | ||

| Potato | ||

| Tapioca | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Functionality | Thickening | |

| Stabilizing | ||

| Gelling | ||

| Emulsifying | ||

| Others(If Any) | ||

| By Application | Food and Beverages | |

| Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Morocco | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for functional native starch demand?

The Functional native starch market is forecast to reach USD 5.1 billion by 2031 from USD 4.0 billion in 2026, expanding at a 5.8% CAGR over 2026-2031.

Which source type leads current revenue generation?

Corn or maize led with 76.2% share in 2025, supported by large wet-milling infrastructure and broad use across food and industrial applications.

Which application is growing the fastest through 2031?

Pharmaceuticals is the fastest-growing application, with a projected 5.7% CAGR during 2026-2031, driven by oral solid dosage production in emerging markets.

Why is Asia-Pacific the leading regional cluster?

Asia-Pacific held 34.9% share in 2025 because it combines cassava supply depth, tapioca processing strength, and a large food manufacturing base.

Page last updated on: