Frontline Worker Technology In Healthcare and Life Sciences Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 6.32 Billion |

| Growth Rate (2026 - 2031) | 22.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frontline Worker Technology In Healthcare and Life Sciences Market Analysis by Mordor Intelligence

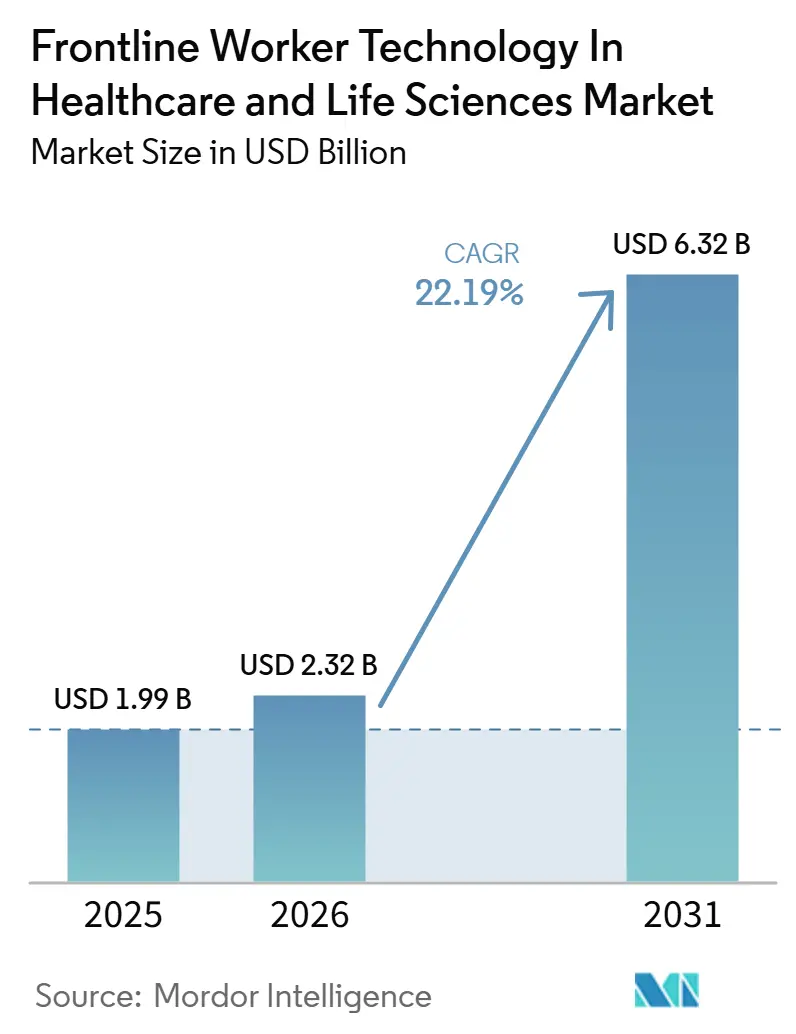

The frontline worker technology in healthcare and life sciences market size is expected to increase from USD 1.99 billion in 2025 to USD 2.32 billion in 2026 and reach USD 6.32 billion by 2031, growing at a CAGR of 22.19% over 2026-2031. The pace of expansion reflects a deeper change in how healthcare providers and life sciences organizations support nurses, care teams, and field staff who work closest to patients and at the point of service. Demand is rising because documentation pressure, staffing shortages, and coordination gaps continue to weigh on care quality, workforce stability, and operating costs across the frontline worker technology in healthcare and life sciences market. The market is also moving beyond basic digitization, as organizations now expect these tools to connect with existing clinical workflows, reduce repetitive tasks, and produce cleaner operational data for staffing and performance decisions. Competitive activity centers on software-led platforms, workflow integration, and clinical usability, while adoption opportunities are expanding across home-based care, smaller provider settings, and digital field operations. Even with regulatory, cybersecurity, and training hurdles, the long-term direction of the frontline worker technology in healthcare and life sciences market remains favorable because workforce pressure is structural rather than cyclical.

Key Report Takeaways

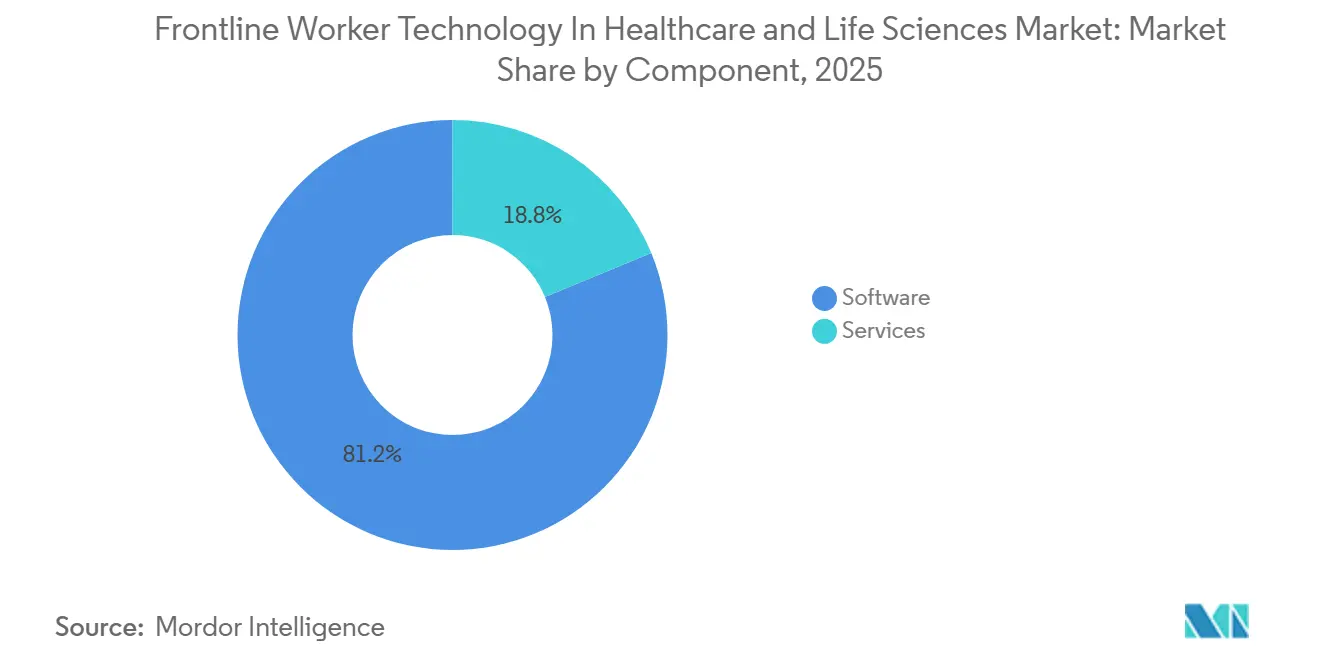

- By component, software held 81.22% share in 2025, while services are projected to expand at a 23.14% CAGR through 2031.

- By deployment, cloud-based deployment captured 78.61% share in 2025, while the same segment is expected to record the fastest growth at a 24.39% CAGR through 2031.

- By organization size, large enterprises accounted for 71.11% of the market share in 2025, while SMEs are projected to grow at a 25.66% CAGR through 2031.

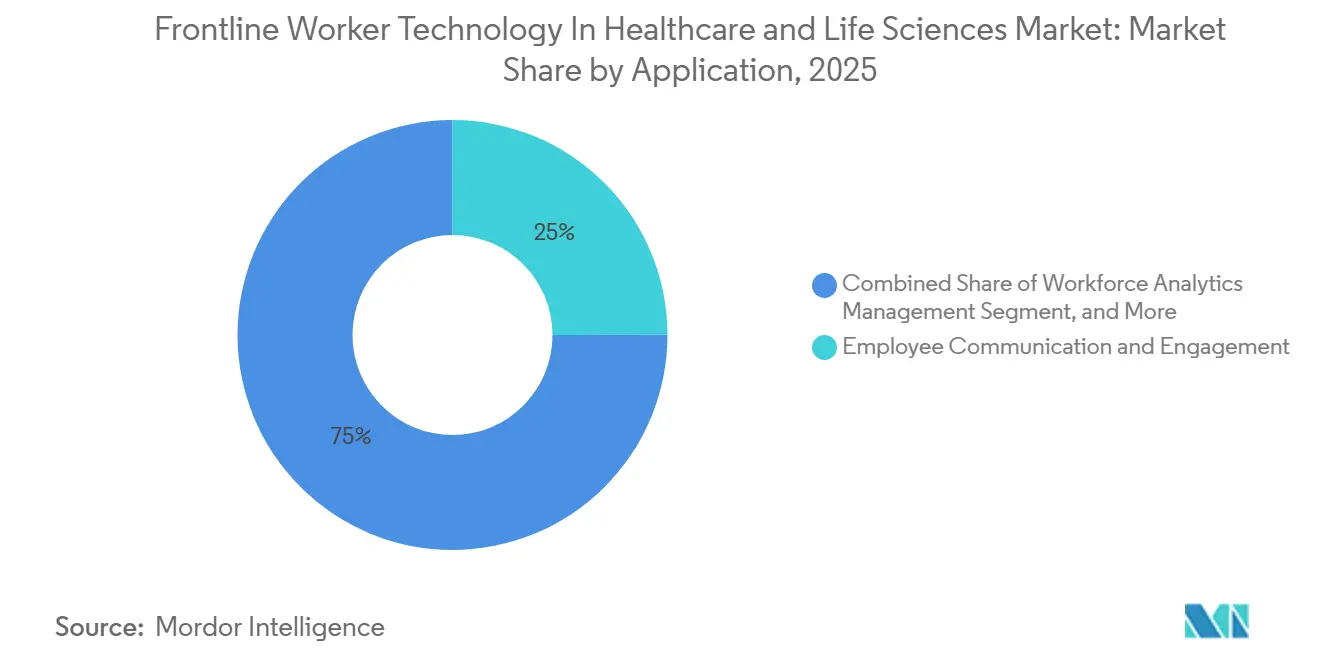

- By application, employee communication and engagement led with 24.99% share in 2025, while workforce analytics and performance management are projected to grow at a 26.81% CAGR through 2031.

- By end-user industry, hospitals and health systems held 33.24% share in 2025, while home healthcare agencies are expected to expand at a 23.12% CAGR through 2031.

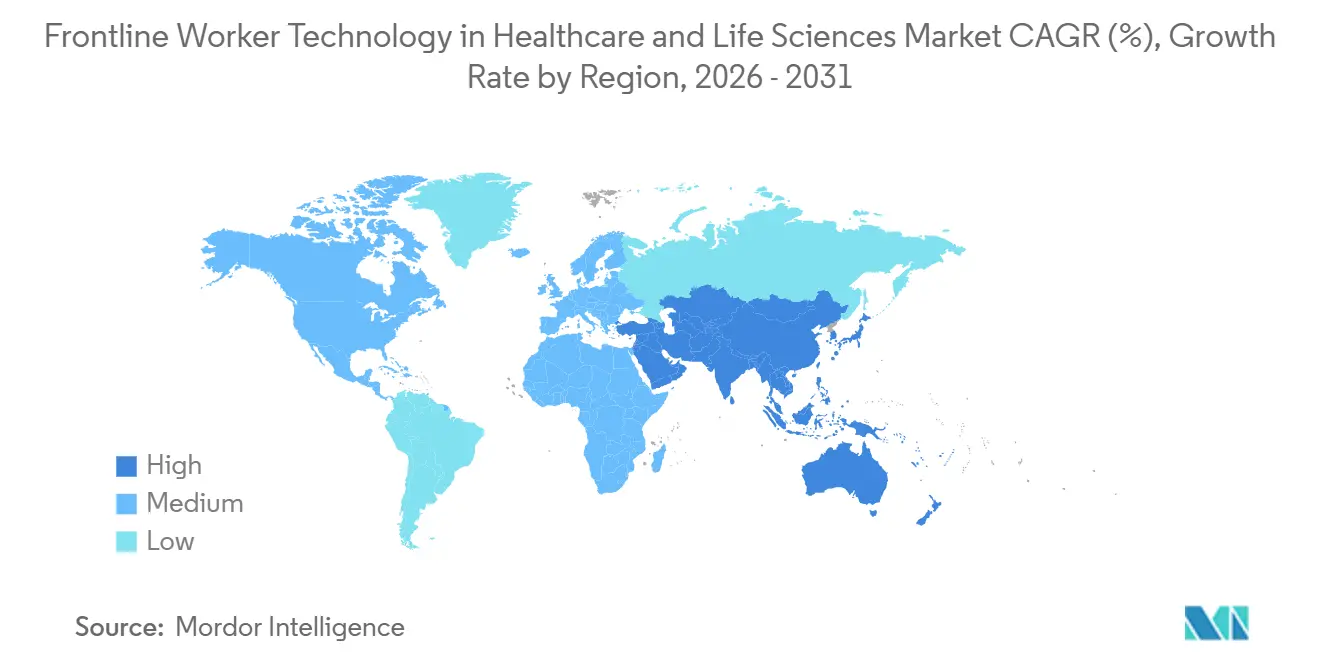

- By geography, North America held 41.11% of the frontline worker technology in healthcare and life sciences market in 2025, while Asia Pacific is projected to record the highest CAGR at 27.99% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Frontline Worker Technology In Healthcare and Life Sciences Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Hands-Free Clinical Workflow Tools | +5.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Staffing Pressure and Burnout Reduction Imperative | +5.2% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Interoperability with EHR, RTLS, and Medication Safety Systems | +4.1% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Voice, Vision, and Sensor Fusion for Bedside Productivity | +3.6% | North America, APAC core, emerging in Middle East and Africa | Medium term (2-4 years) |

| Infection Control and Device Sanitization Requirements | +2.4% | Global, concentrated in acute care environments | Short term (≤ 2 years) |

| Expansion of Decentralized Trials and Life Sciences Field Operations | +1.8% | North America, EU, spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Hands-Free Clinical Workflow Tools

Hands-free workflow support is moving into the practical core of the frontline worker technology in healthcare and life sciences market because nurses and care teams need faster ways to capture information without stepping away from patient-facing tasks. A 2026 study in JMIR Nursing showed that a voice-based nursing documentation system built on speech recognition and large language models achieved an F1-score of 0.82 for structured record generation and reduced perceived documentation burden during routine care.[1]Voice-Based Structured Nursing Documentation Using Automatic Speech Recognition and Large Language Models: Development and Evaluation Study, JMIR Nursing, nursing.jmir.org That result matters because documentation quality and speed influence shift handoffs, chart completeness, and care coordination, making bedside usability more important than broad feature count in the frontline worker technology market for healthcare and life sciences. Deutsche Telekom presented an AI-supported nursing documentation solution in 2025 that enabled bedside voice dictation and structured report generation within German data centers, demonstrating that hands-free documentation is being adapted to strict healthcare data-handling requirements rather than treated as a consumer-style add-on. Mayo Clinic moved in a similar direction in 2025 by deploying a nurse virtual assistant embedded within its EHR, underscoring that clinical teams want tools that fit the record system already used in daily care rather than separate, standalone applications. As a result, the frontline worker technology in healthcare and life sciences market is leaning toward solutions that reduce manual input while preserving workflow continuity and clinical control.[2]Mit KI: Telekom Erleichtert Pflegekräften Die Arbeit, Deutsche Telekom, telekom.com

Staffing Pressure and Burnout Reduction Imperative

Workforce strain remains one of the clearest growth drivers for the frontline worker technology in healthcare and life sciences market because providers are trying to stabilize care delivery with lean staffing and high documentation demand. In 2025, Incredible Health reported, based on data from more than 1 million nursing professionals in the United States, that 71% of nurses said understaffing was harming care quality.[3]Workforce Pressures Mount for Nurses and Technicians as AI and Politics Enter the Workplace: New Report, Incredible Health, incrediblehealth.com That pressure changes how digital spending is evaluated, since workflow tools are now judged not only by efficiency gains but also by their ability to improve retention, reduce avoidable workload, and support safer staffing choices. In the frontline worker technology in healthcare and life sciences market, this has raised interest in scheduling tools, workflow coordination, mobile documentation, and analytics that help managers spot stress points before they become absenteeism or turnover problems. The same dynamic is evident across hospitals, clinics, and home-based care operations, as each setting relies on workers who must handle more tasks in less time while still meeting quality and compliance standards. This keeps demand broad-based across the frontline worker technology in healthcare and life sciences market even when provider budgets are selective.

Interoperability With EHR, RTLS, and Medication Safety Systems

Interoperability is becoming a practical requirement in the frontline worker technology in healthcare and life sciences market because frontline applications have limited value when staff must still reenter data across separate systems. Evangelisches Krankenhaus Wesel in Germany launched closed-loop digital medication management in 2025, with documentation integration built for frontline clinical use, demonstrating that medication safety workflows depend on connected systems rather than isolated tools.[4]Closed-Loop-Medikationsmanagement Im EVK Wesel Gestartet, Gesundheitscampus Wesel, gesundheitscampuswesel.de Mayo Clinic’s nurse virtual assistant was also embedded within the EHR in 2025, reinforcing that adoption improves when documentation and information retrieval stay within the system already trusted by nursing teams. In practical terms, providers want communication, task execution, medication, and staffing tools that can work with patient records, clinical protocols, and operational systems without adding more manual reconciliation. That expectation raises the barrier to entry in the frontline worker technology in healthcare and life sciences market because vendors now need workflow fit, data structure discipline, and implementation depth in addition to product features. It also favors platforms that can support both care delivery and operational visibility from the same connected environment.

Voice, Vision, and Sensor Fusion for Bedside Productivity

The frontline worker technology in healthcare and life sciences market is also being shaped by a shift toward multimodal worker assistance, where voice capture, structured documentation, and contextual support are brought closer to the bedside. The 2026 JMIR Nursing study showed that voice-based documentation can produce structured nursing records with high accuracy, supporting the case for low-touch clinical input in fast-paced care settings. Deutsche Telekom’s 2025 nursing documentation solution further demonstrated that speech-enabled reporting can be adapted to provider-grade environments with controlled data processing, which is important for broader adoption in hospitals handling sensitive patient information. In the frontline worker technology in healthcare and life sciences market, the value of these tools comes from reducing device switching, shortening note capture time, and allowing staff to stay focused on the patient while still producing usable digital records. Over time, this architecture can extend beyond voice into a broader support layer that more tightly links bedside actions, workflow prompts, and clinical context than older mobile point solutions. That direction supports deeper adoption across the frontline worker technology in healthcare and life sciences market because it aligns with the day-to-day realities of high-motion clinical work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Validation Burden in Clinical and Regulated Environments | -3.8% | Global, most restrictive in North America and EU | Long term (≥ 4 years) |

| Cybersecurity, Privacy, and Identity Governance Complexity | -3.2% | Global, concentrated in North America | Medium term (2-4 years) |

| Workflow Disruption During Change Management and Training | -2.1% | Global, most acute in large enterprise deployments | Short term (≤ 2 years) |

| Battery Life, Device Durability, and Sanitization Trade-Offs | -1.4% | Global, particularly in acute care environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Validation Burden in Clinical and Regulated Environments

Validation remains a meaningful restraint for the frontline worker technology in healthcare and life sciences market because healthcare tools are used in settings where documentation quality, reliability, and device behavior can affect care decisions. Coverage of the FDA Quality Management System Regulation in 2026 noted that the rule incorporates ISO 13485:2016 and clarifies the inclusion of cybersecurity validation within the medical device quality framework, raising the compliance standard for connected clinical software and wearables. This matters because even products with strong workflow value may face longer deployment cycles when hospitals require evidence of design controls, testing discipline, and risk management before procurement. In the frontline worker technology in healthcare and life sciences market, that burden tends to favor vendors with established quality systems, stronger regulatory documentation, and implementation teams that understand inpatient validation requirements. Smaller vendors can still compete, but they often face slower entry into highly regulated provider environments and may gain traction first in lower-complexity settings. As a result, compliance readiness affects not only time-to-revenue but also which use cases and customer groups can be reached first.

Cybersecurity, Privacy, and Identity Governance Complexity

Cybersecurity and identity governance are slowing parts of the frontline worker technology in healthcare and life sciences market because more frontline tools now capture or transmit sensitive patient and operational data at the edge. Discussion of the 2026 FDA cybersecurity expectations highlighted the need for standardized software bill of materials practices for connected devices, which adds documentation and lifecycle monitoring requirements for vendors serving clinical environments. The practical issue is that hospitals are not only buying features but also security posture, patching discipline, user access controls, and auditability across mobile and wearable endpoints. In the frontline worker technology in healthcare and life sciences market, this can delay procurement when IT and clinical teams must evaluate whether a tool fits existing privacy, access, and device management policies. It also increases implementation costs because security reviews, device provisioning, and role-based control design must be completed before frontline scale-up can occur. These demands do not reduce long-term need, but they do make sales cycles and deployment decisions more complex.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads While Services Deepen Adoption

Software accounted for 81.22% of the market in 2025, which made it the core commercial layer across the frontline worker technology in healthcare and life sciences market. That lead reflects how workflow applications, communication platforms, analytics dashboards, and documentation tools can be rolled out on existing devices without waiting for a large hardware refresh cycle. Software also remains the first purchase in many provider settings because hospitals and care networks typically want visible workflow gains before committing to broader device or infrastructure changes. In the frontline worker technology in healthcare and life sciences market, this gives software vendors an early position in customer accounts and a wider opening for module expansion over time. It also explains why the market continues to show strong software concentration even as other parts of the offering become more important.

Services are projected to grow at a 23.14% CAGR through 2031, making them the fastest-growing segment of this market. That pace suggests providers increasingly understand that adoption problems are often rooted in workflow design, training, integration, and change management rather than missing product features alone. A 2026 systematic review in BMC Health Services Research found that technostress, workflow impact, and task dynamism were central to successful EHR adaptation, which supports the need for deeper implementation support in clinical settings. In the frontline worker technology in healthcare and life sciences industry, services help turn software into daily practice by aligning tools with staffing models, clinical roles, and local operating routines. Over time, service intensity is likely to remain a competitive differentiator because providers want measurable workflow improvement, not just access to a platform.

By Deployment: Cloud-Based Architecture Becomes The Default

Cloud-based deployment held 78.61% share in 2025, which placed it well ahead of hybrid and on-premises models across the frontline worker technology in healthcare and life sciences market. This dominance reflects a practical need for real-time coordination, as dispersed teams require current schedules, tasks, alerts, and access to documentation across shifts and care locations. Cloud-based deployment also aligns better with budgetary patterns in many healthcare settings because it reduces capital requirements and allows organizations to add functionality without a major infrastructure overhaul. In the frontline worker technology in healthcare and life sciences market, that flexibility is especially useful where providers are supporting both facility-based and field-based teams from a shared operating model. The result is that cloud architecture is no longer viewed as a niche option; it is increasingly the normal starting point for new deployments.

The same segment is projected to grow at a 24.39% CAGR through 2031, making it the leader in both scale and momentum. That combination shows that new buyers and existing customers are still moving in the same direction rather than shifting back to legacy hosting models. Providers want faster implementation, easier updates, and broader mobile access, and those needs closely align with cloud-led platform design in the frontline worker technology market for healthcare and life sciences. Hybrid deployments still retain a role where data residency, legacy systems, or internal governance require a slower transition path. Even so, the broader trajectory points toward cloud-native operating models as the preferred foundation for communication, analytics, scheduling, and frontline execution tools.

By Organization Size: Large Enterprises Still Dominate, SMEs Are Catching Up

Large enterprises accounted for 71.11% of the market in 2025, reflecting their stronger IT budgets, larger workforces, and greater ability to validate and govern multi-site deployments. Large health systems and enterprise life sciences organizations can spread implementation costs across broader operations, making it easier to justify investment in workflow and workforce technology. They also tend to have more mature digital governance, which helps with vendor assessment, integration planning, and compliance review inside the frontline worker technology in healthcare and life sciences market. That position keeps them at the center of demand, especially for platforms that combine communication, documentation, task management, and analytics across large clinical networks. It also means enterprise buyers continue to shape product expectations for usability, security, and interoperability.

SMEs are projected to expand at a 25.66% CAGR through 2031, making them the fastest-growing segment by organization size. This growth shows that smaller hospitals, specialty clinics, and focused care providers are no longer waiting for large-scale enterprise models to trickle down before adopting digital frontline tools. Usage-based software pricing, modular deployment, and more targeted workflow templates are helping SMEs enter the frontline worker technology in healthcare and life sciences market with less capital strain and less operational disruption. In the frontline worker technology in healthcare and life sciences industry, that shift broadens the customer base and reduces dependence on a few very large buyers. It also points to stronger growth in vendor offerings that are easier to deploy, train, and manage without a large internal IT team.

By Application: Communication Holds The Base, Analytics Drives The Next Wave

Employee communication and engagement accounted for a 24.99% share of the frontline worker technology in healthcare and life sciences market size in 2025. This segment leads because communication is often the first friction point organizations try to address when they digitize frontline operations. Staff need faster updates, clearer task visibility, easier escalation, and more reliable team coordination before more advanced workflow tools can deliver full value. In the frontline worker technology in healthcare and life sciences market, communication platforms often serve as the first operational layer that later supports scheduling, analytics, and execution modules. That foundation keeps the segment large even as the market matures into more specialized use cases.

Workforce analytics and performance management is projected to expand at a 26.81% CAGR through 2031, making it the fastest-growing application in this segment. A 2026 study in Scientific Reports showed that an AI-driven hospital workforce management system improved task completion and nurse job satisfaction when compared with static rule-based scheduling methods. That evidence supports the growing view that providers want tools that not only connect workers but also help leaders understand deployment quality, workload intensity, and performance patterns. In the frontline worker technology in healthcare and life sciences market, analytics is gaining importance because it gives finance, nursing, and operations leaders clearer evidence on staffing effectiveness and workflow bottlenecks. This is why communication remains the largest use case today, while analytics is shaping the next stage of value capture.

By End-User Industry: Hospitals Lead Revenue, Home Healthcare Drives Expansion

Hospitals and health systems held 33.24% share in 2025 and retained the broadest installed base in the frontline worker technology in healthcare and life sciences market. Their lead reflects workforce density, higher care volumes, stronger digital infrastructure, and the operational costs of poor coordination in complex clinical environments. Hospitals also face constant documentation, medication, staffing, and handoff demands, which create multiple entry points for frontline technology within the same account. In the frontline worker technology in healthcare and life sciences market, this produces deeper platform penetration because one provider organization may adopt communication tools, documentation support, analytics, and safety workflows together. That account depth helps explain why hospitals remain the anchor of revenue for many vendors.

Home healthcare agencies are projected to grow at a 23.12% CAGR through 2031, which makes them the fastest-expanding end-user segment. Growth is being supported by the broader movement of chronic, post-acute, and some acute care activities into home settings, where coordination and field-worker support are essential. As care shifts outward, the frontline worker technology in healthcare and life sciences market is extending beyond fixed-site staffing problems into route-based scheduling, remote documentation, and field-level task execution. This creates demand for tools that help dispersed workers stay aligned with care plans, documentation expectations, and service timing without constant direct supervision. The long-term implication is that home-focused deployment models will become a more visible source of growth, even though hospitals remain the largest current demand center.

Geography Analysis

North America held 41.11% of the market in 2025 and represented the largest regional base within the frontline worker technology in healthcare and life sciences market. The region benefits from stronger hospital technology spending, wider use of digital records, and acute workforce pressure that makes frontline productivity a strategic issue rather than a narrow IT concern. It also has a large installed base of enterprise healthcare systems that can support broader rollout of workflow, documentation, and staffing applications once early use cases show operational value. In the frontline worker technology in healthcare and life sciences market, that mix supports both repeat deployment within large systems and ongoing demand for more specialized applications. Even with tighter security and compliance review, North America remains the clearest near-term revenue center.

Europe remains an important but mixed opportunity because provider funding models, data rules, and implementation pace differ across countries. Germany has made visible progress in hospital digitalization, and Evangelisches Krankenhaus Wesel’s closed-loop medication management rollout in 2025 demonstrated how frontline documentation and medication processes are being more closely connected within care settings. Deutsche Telekom’s 2025 AI-assisted nursing documentation solution also showed that European providers are pursuing bedside productivity tools that align with domestic data processing expectations. This means the frontline worker technology in healthcare and life sciences market in Europe is advancing with strong interest, but with greater emphasis on localized deployment models and governance fit.

Asia Pacific is projected to advance at a 27.99% CAGR through 2031 and is the fastest-growing regional segment in the frontline worker technology in healthcare and life sciences market. China’s National Health Commission and other ministries issued implementation guidelines for AI plus healthcare in late 2025, which placed AI-assisted diagnostic and workflow coverage on a much firmer policy footing for the years ahead. China also saw scaled hospital deployment in 2026, including an AI-powered patient navigation agent system at Xiangya Jiangxi Hospital, demonstrating that frontline AI is moving further into operational use. India and Southeast Asia add to the regional outlook because smartphone-led workflows and telemedicine infrastructure create practical entry points for communication, scheduling, and field-worker coordination. Middle East and Africa remain smaller in revenue terms, yet organized digital investment in Gulf healthcare systems gives the frontline worker technology in healthcare and life sciences market a meaningful long-term runway there as well.

Competitive Landscape

The frontline worker technology in healthcare and life sciences market remains moderately fragmented, with diversified technology companies, clinical software specialists, workflow vendors, and provider-built solutions all competing for adoption. This structure reflects the fact that frontline needs do not center on a single product class, since providers may buy communication tools, documentation support, staffing analytics, safety systems, or task execution platforms from different vendors. Large firms usually compete on integration depth, security posture, and deployment scale, while smaller firms often compete on workflow fit, nursing usability, and configuration speed. In the frontline worker technology in healthcare and life sciences market, that creates room for both broad platforms and narrower specialists to win business. Competition, therefore, depends as much on clinical fit and implementation quality as it does on product breadth.

Several strategic moves show how vendors and provider organizations are positioning themselves. Deutsche Telekom introduced an AI-based nursing documentation solution at DMEA 2025, featuring structured bedside voice dictation processed within German data centers, signaling a clear push toward clinically relevant workflow tools built around local trust and data requirements. Provation launched Provation Mira Documentation Assist in March 2026 within its cloud-based GI procedure platform, reflecting a strategy of embedding voice-driven documentation directly into an established specialty workflow rather than offering it as a detached productivity tool. Mayo Clinic’s 2025 deployment of its internally developed Nurse Virtual Assistant showed another route to competition, where leading providers build and refine tools tailored to their own nursing workflows and EHR environments before broader scaling or replication. These examples show that the frontline worker technology in healthcare and life sciences market rewards operational relevance and trusted workflow placement more than generic digital feature expansion.

The competitive landscape also suggests that connected documentation, staffing intelligence, and point-of-care workflow support are converging. Vendors that can link frontline actions with structured operational data are better placed to expand from a single use case into broader workforce management or clinical coordination layers. At the same time, provider buyers are becoming more selective, so product claims alone are less persuasive than real evidence of usability and workflow compatibility in live care settings. In the frontline worker technology in healthcare and life sciences market, this favors companies that can show clinical validation, secure deployment design, and a credible path from pilot use to enterprise routine. The result is a market where breadth helps, but trust, implementation discipline, and everyday clinical usefulness remain the stronger long-term differentiators.

Frontline Worker Technology In Healthcare and Life Sciences Industry Leaders

Zebra Technologies Corporation

Securitas Healthcare LLC

CenTrak, Inc.

Sonitor Technologies AS

TeleTracking Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Zebra Technologies Corporation and Aiva Health announced a partnership to deploy Aiva's AI-powered nurse assistant on Zebra's HC20/HC50 healthcare-grade mobile computers and the new WS101-H wearable badge. The integration enables fully hands-free nurse workflows, including voice-activated clinical documentation and service requests, without device touch even while wearing gloves.

- March 2025: Provation launched Provation Mira Documentation Assist, a voice-driven documentation capability within its cloud-based GI procedure platform, enabling clinicians to document in real time by speaking during procedures and eliminating post-procedure recall burden through structured AI-generated clinical records.

- March 2026: Speech Processing Solutions launched Philips SpeechLive Health AI Assistant, an AI-powered clinical documentation platform designed for healthcare professionals across multiple care settings. It was paired with the Philips SpeechMike Ambient Wearable AI Assistant, a multi-microphone array wearable device with AI-based voice filtering for busy clinical environments, marking the expansion of professional dictation technology into hands-free clinical documentation.

- February 2026: The FDA's Quality Management System Regulation took full effect on February 2, 2026, incorporating ISO 13485:2016 into the regulatory framework for medical devices, including connected clinical software and wearables. The regulation embedded cybersecurity validation requirements and mandatory Software Bill of Materials submissions into standard premarket pathways, materially raising the compliance bar for connected frontline clinical devices.

Global Frontline Worker Technology In Healthcare and Life Sciences Market Report Scope

The frontline worker technology in healthcare and life sciences market refers to the ecosystem of software and services designed to empower non-desk healthcare professionals, including nurses, clinicians, technicians, and support staff, who operate in dynamic clinical and care environments. This includes tools tailored to facilitate secure communication, task execution, shift scheduling, knowledge sharing, and stringent safety and compliance management. The market encompasses cloud-based, on-premises, and hybrid solutions deployed by healthcare organizations of varying sizes, ranging from large hospital systems to small clinics and home healthcare agencies. These technologies aim to bridge the communication gap between administrative management and on-the-ground medical personnel, ultimately reducing administrative burdens, improving care coordination, ensuring regulatory compliance, and enhancing overall patient outcomes.

The Frontline Worker Technology In Healthcare And Life Sciences Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-user Industry (Hospitals and Health Systems, Clinics and Ambulatory Care Centers, Long-Term Care and Skilled Nursing Facilities, Home Healthcare Agencies, and Senior Living and Assisted Living Facilities), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Hospitals and Health Systems |

| Clinics and Ambulatory Care Centers |

| Long-Term Care and Skilled Nursing Facilities |

| Home Healthcare Agencies |

| Senior Living and Assisted Living Facilities |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment | Cloud-Based | ||

| Hybrid | |||

| On-Premises | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Application | Employee Communication and Engagement | ||

| Workforce Execution and Task Management | |||

| Workforce Scheduling and Coordination | |||

| Learning and Knowledge Enablement | |||

| Workforce Analytics and Performance Management | |||

| Safety and Compliance Management | |||

| Other Applications | |||

| By End-user Industry | Hospitals and Health Systems | ||

| Clinics and Ambulatory Care Centers | |||

| Long-Term Care and Skilled Nursing Facilities | |||

| Home Healthcare Agencies | |||

| Senior Living and Assisted Living Facilities | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast size of the frontline worker technology in healthcare and life sciences space?

The frontline worker technology in healthcare and life sciences market was valued at USD 1.99 billion in 2025, is estimated at USD 2.32 billion in 2026, and is projected to reach USD 6.32 billion by 2031 at a 22.19% CAGR.

What is driving adoption of frontline technology across healthcare and life sciences operations?

The main demand drivers are staffing shortages, burnout reduction needs, faster documentation, and the need to coordinate frontline work more effectively across hospitals, clinics, and home-based care settings.

Which component category leads demand today?

Software led the market in 2025 with an 81.22% share because organizations usually begin with workflow applications, communication tools, documentation support, and analytics before expanding service intensity.

Which application area is growing the fastest through 2031?

Workforce analytics and performance management is projected to grow at a 26.81% CAGR through 2031 as providers seek better visibility into staffing deployment, workload, and operational performance.

Why are hospitals still the largest end-user group?

Hospitals and health systems held 33.24% share in 2025 because they manage dense workforces, complex care coordination, and high documentation pressure, which creates multiple use cases for frontline tools.

Which region offers the strongest growth outlook?

Asia Pacific is expected to post the highest CAGR at 27.99% through 2031, supported by hospital digitization, aging demographics, and broader use of AI-enabled frontline care workflows.

Page last updated on: