Freemium OTT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

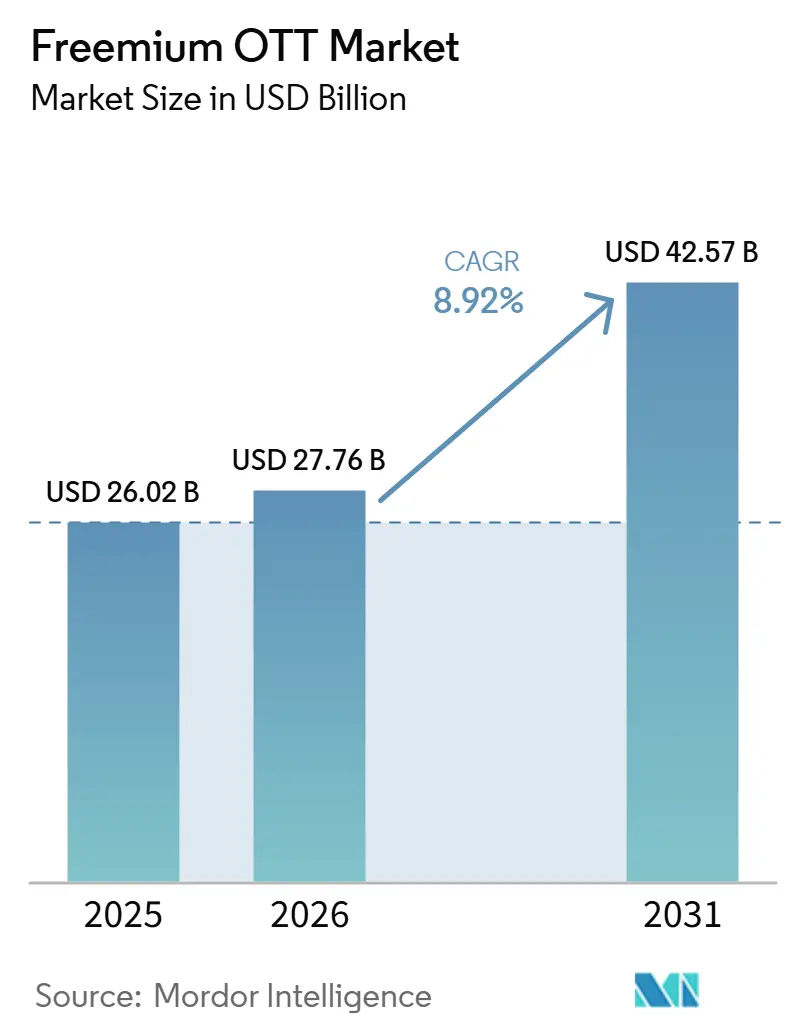

| Market Size (2026) | USD 27.76 Billion |

| Market Size (2031) | USD 42.57 Billion |

| Growth Rate (2026 - 2031) | 8.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Freemium OTT Market Analysis by Mordor Intelligence

The freemium OTT market size is expected to increase from USD 26.02 billion in 2025 to USD 27.76 billion in 2026 and reach USD 42.57 billion by 2031, growing at a CAGR of 8.92% over 2026-2031. The freemium OTT market is expanding because platforms are no longer treating free access as a side offering; they are using it as a core route to build audience scale and support later premium upgrades. Advertisers are also shifting more budget toward connected TV inventory, which gives ad-supported streaming stronger pricing support than it had when mobile video carried more of the demand. Telecom bundles and device partnerships are lowering customer acquisition costs and making it easier for users to sample several services without taking multiple direct subscriptions at full price. Regional platforms are using local-language programming, live events, and mobile-first distribution to defend their share against larger global brands, keeping competition active across mature and emerging markets. At the same time, higher content costs, tighter privacy rules, and softer premium conversion rates are pushing the freemium OTT market toward a more consolidated structure where scale matters more than it did a few years ago.

Key Report Takeaways

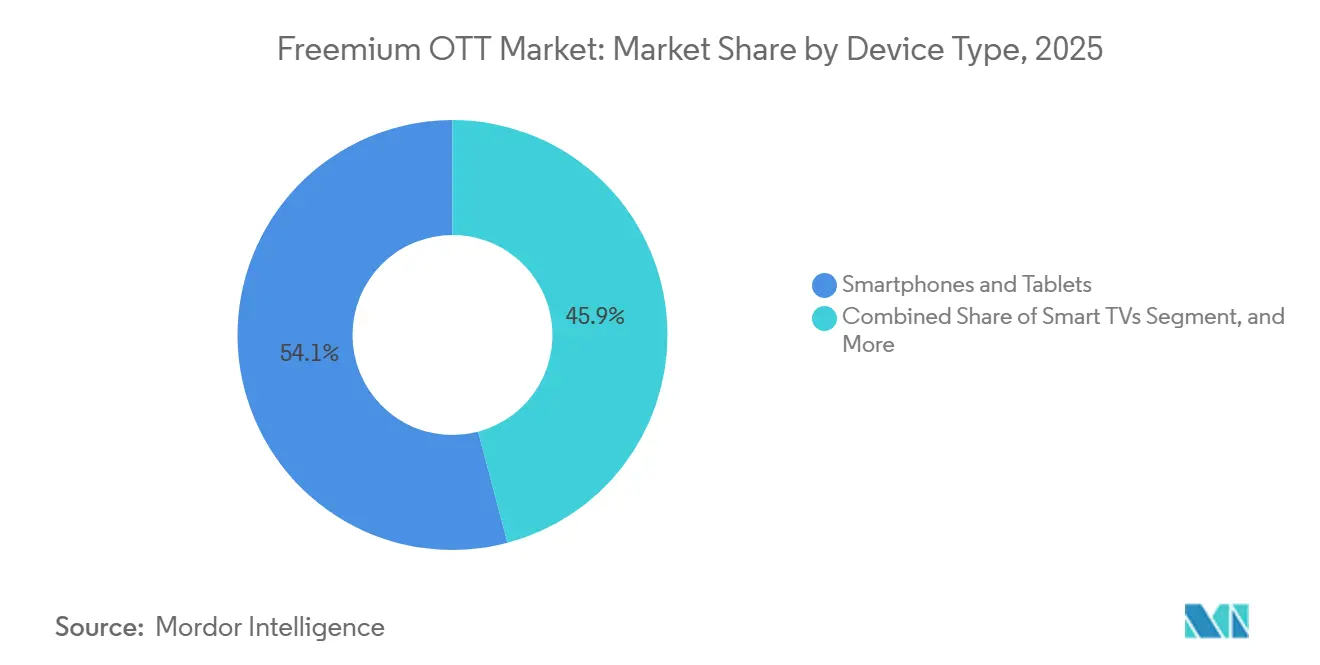

- By device type, smartphones and tablets accounted for 54.12% of the freemium OTT market share in 2025, while smart TVs are projected to expand at a 9.48% CAGR through 2031.

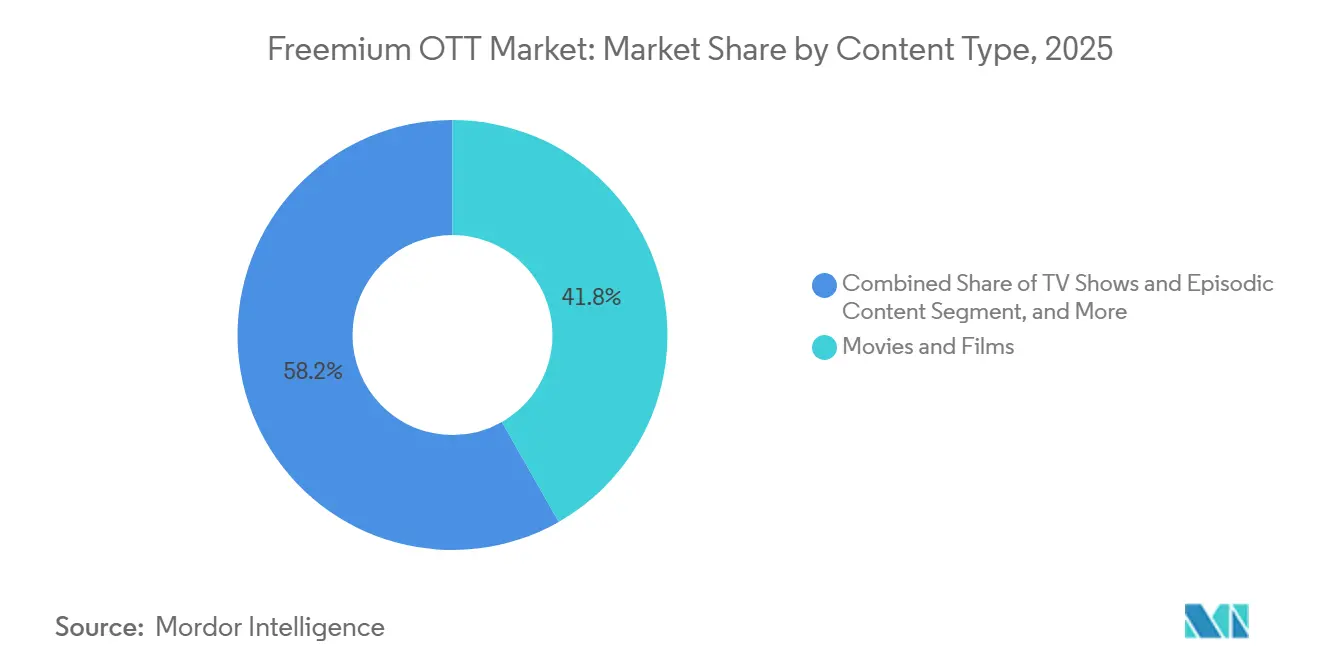

- By content type, movies and films accounted for 41.77% of the market in 2025, while TV shows and episodic content are projected to expand at a 10.21% CAGR through 2031.

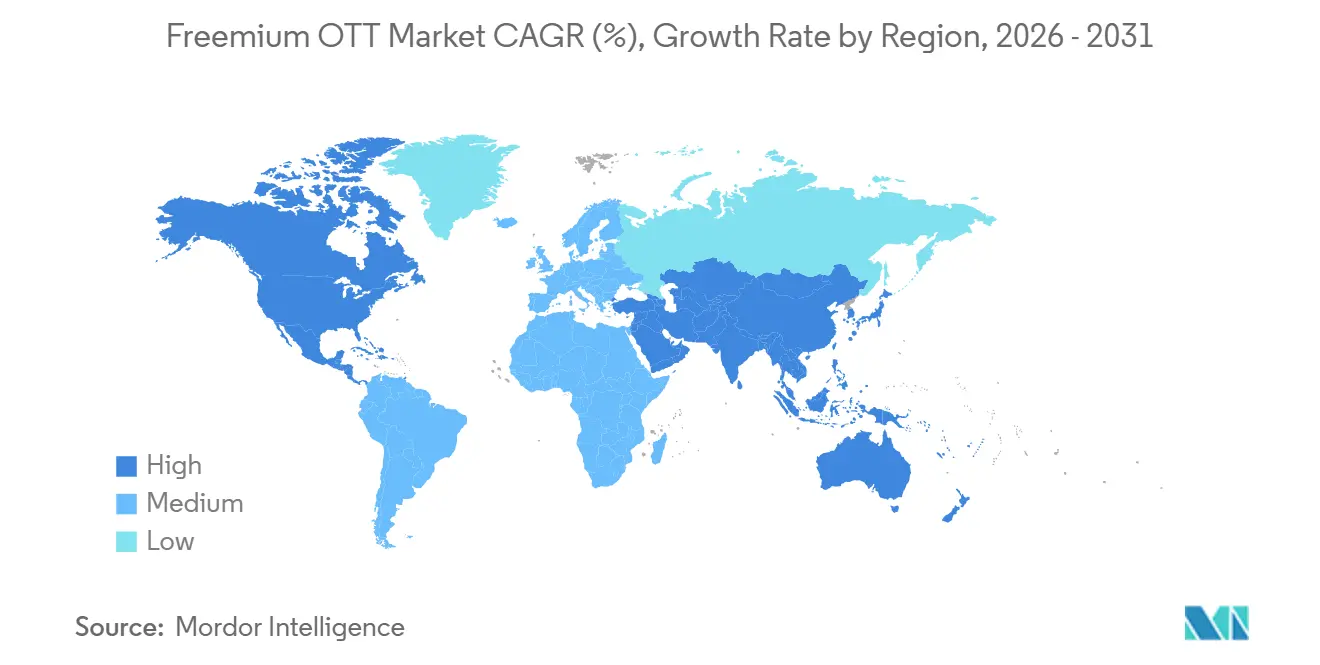

- By geography, North America held 38.38% share of the freemium over-the-top (OTT) market in 2025, while Asia-Pacific recorded the highest projected CAGR at 10.64% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Freemium OTT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Acceptance of Ad-Supported Viewing for Free Access | +2.5% | Global | Short term (≤ 2 years) |

| Faster Ad-Tier Conversion Through Low-Friction Upgrade Paths | +2.0% | North America and Europe | Medium term (2-4 years) |

| Connected-TV Inventory Expansion Improves Monetization Depth | +1.8% | North America, Europe, and Asia-Pacific core | Medium term (2-4 years) |

| Telco and Device Bundles Lower Customer Acquisition Cost | +1.5% | Asia-Pacific core, South America, and Middle East and Africa | Medium term (2-4 years) |

| Mobile-First Broadband Expansion Broadens Free-Tier Reach | +1.2% | Asia-Pacific core, with spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Niche Content and Creator Libraries Monetize Long-Tail Demand | +0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Acceptance of Ad-Supported Viewing for Free Access

Ad-supported viewing has become a normal part of streaming behavior, and that shift is giving the freemium OTT market a broader, more stable user base than pure subscription models can achieve on their own. When viewers accept advertising in return for free access, platforms can scale reach faster, keep re-engaging churned users, and create more inventory without asking households to take another paid commitment. The effect is stronger in content categories such as news and sports, where viewers are more tolerant of denser ad loads and are less likely to exit a session due to interruption frequency. That allows services to more closely match ad pressure to content type, helping protect viewing time while still increasing monetization depth across the freemium OTT market. Amagi reported a 55% year-over-year rise in FAST viewing hours in Q2 2026, which showed that free streaming had already become a routine viewing behavior rather than a niche fallback option.[1]Amagi, “Amagi Releases June 2026 AIRTIME Report: FAST Viewing Hours Grow 55% YoY as Metadata Friction Escalates,” Amagi Newsroom, www.amagi.com

Faster Ad-Tier Conversion Through Low-Friction Upgrade Paths

Low-friction upgrade paths are improving the economics of the freemium OTT market because platforms no longer need to win every user through a direct full-price subscription pitch at the first touchpoint. Free tiers let services observe what people watch, how often they return, when they abandon sessions, and which titles create the strongest intent to continue. That data supports better timing for premium prompts, especially around season breaks, access locks, or live events that create a sharper reason to pay. Paramount Skydance reported that its mid-2026 technology convergence between Pluto TV and Paramount+ would support cross-service recommendations, demonstrating how platform design is being used to turn free discovery into paid conversion. The freemium over-the-top (OTT) market benefits whenever this funnel improves, because each free user can support current ad revenue and future upgrade potential without requiring the same level of new customer-acquisition spending.

Connected-TV Inventory Expansion Improves Monetization Depth

Connected TV is deepening monetization in the freemium OTT market because large-screen viewing typically delivers stronger ad value than smaller-screen viewing and often attracts brand budgets that prefer television-like environments. Device makers are also opening new ad surfaces before any app session begins, meaning monetization now starts at the operating system level rather than only within a content library. LG and Teads expanded their exclusive smart TV home-screen partnership across more than two dozen countries in April 2026, underscoring how device-level placements are becoming a central part of ad-supported streaming strategy. Premion reported that 50% of CTV and OTT advertising was expected to be bought programmatically in 2026, which improves liquidity for both large platforms and smaller operators with specialized inventory. As more inventory becomes tradable, measurable, and easier to buy, the freemium OTT market can lift yield even when premium subscription growth is less predictable.

Telco and Device Bundles Lower Customer Acquisition Cost

Telco and device bundles are widening access to the freemium OTT market by reducing the number of separate purchase decisions a user or household needs to make. Reliance Jio launched an INR 200 (USD 2.08) OTT Pass in May 2026 that bundled 15 OTT platforms, 30 GB of data, and unlimited 5G for 28 days, making multi-platform access much easier for price-sensitive users in India. Telefónica's O2 brand introduced four household plans in Spain in July 2026 that bundled fiber broadband, mobile data, Movistar Plus+, Netflix, and Disney+ from EUR 45 (USD 51.80) per month. These structures lower acquisition costs for streaming services, reduce billing friction for consumers, and raise the effort required to cancel a single service inside a larger package. In the freemium OTT market, bundles matter because they make free tiers easier to sample, keep audience relationships active for longer, and increase the likelihood that a premium upgrade stays within the same billing environment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subscription Fatigue Limits Premium Conversion | -0.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Escalating Licensing and Original Content Costs Compress Margins | -0.6% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| CTV Measurement Fragmentation Weakens Advertiser Confidence | -0.4% | North America and Europe | Medium term (2-4 years) |

| Privacy Rules and Ad-Load Limits Constrain Targeting Yield | -0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subscription Fatigue Limits Premium Conversion

Subscription fatigue is limiting how many free users in the freemium OTT market can be converted into stable paid subscribers over time. The average US household subscribed to 4.2 streaming services in 2026, and premium SVOD subscriber growth in the United States slowed to 7% in 2025, suggesting a more selective paid-demand base than platforms enjoyed during the earlier expansion period.[2]Antenna, “Q1 2026 State of Subscriptions Report,” The State of Streaming, thestateofstreaming.com When viewers rotate in and out for a single title, a single sports event, or a short seasonal window, platforms can keep some of them on the free tier but lose some of the revenue depth that a longer paid relationship would have delivered. This leaves the freemium OTT market more dependent on ad yield per user, especially when the same viewers are unwilling to maintain multiple paid subscriptions simultaneously. The result is not weaker audience reach, but a harder path to premium monetization at scale and a tighter margin for operators that depend on paid upgrades to balance content spending.

Escalating Licensing and Original Content Costs Compress Margins

Rising licensing and original production costs are tightening margins across the freemium OTT market and are increasing the advantage held by platforms with greater scale or broader library control. Amazon's video and music content spending reached USD 22.4 billion in 2025, up 10% year over year, which showed how expensive premium content supply had become across streaming. Free tiers are more exposed to this pressure because advertising revenue per viewer hour is usually lower than subscription revenue per viewer hour, so the same rise in content cost has a heavier effect on economics. Large platforms with strong brands, extensive libraries, or user-generated ecosystems can spread that burden more effectively than mid-sized services that depend on outside licensing for audience retention. In the freemium OTT market, this cost gap favors scale players, encourages partnerships, and puts pressure on smaller operators to narrow their focus to sports, local-language programming, or other more defensible niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Mobile Screens Lead While Smart TVs Gain Ground

Smartphones and tablets accounted for 54.12% of the freemium OTT market share in 2025, keeping mobile screens as the main access point across much of global demand. That position reflects markets where streaming reached consumers first through mobile data rather than fixed broadband, and where price-sensitive users still prefer portable access over household screen setups. Mobile viewing also fits short sessions, commute-based use, and second-screen behavior at home, which gives free tiers a steady flow of daily engagement even when viewing time per session is not as long as television viewing. Laptops and desktops still support long-form consumption, and some student and professional use, but their relative role is diminishing as smart TV access becomes simpler and more widespread in the home. Other device types, including streaming sticks and gaming consoles, remain relevant where legacy pay TV hardware coexists with newer app-based viewing habits and where households continue to experiment with several forms of connected entertainment.

Smart TVs are projected to expand at a 9.48% CAGR through 2031, and this part of the freemium OTT market is growing as television screens support stronger ad monetization and easier FAST discovery within device operating systems. LG and Teads widened the reach of smart TV home-screen advertising in April 2026, reinforcing the value of pre-app inventory for services that depend on ad-funded viewing. iQIYI also used its 2026 World Conference to highlight AI-based recommendation and creation tools, demonstrating how the freemium OTT industry is tailoring content delivery and ad placement based on device context. Fox Corporation reported that it would keep Tubi and The Roku Channel as separate services after the Roku deal, which suggested that device-specific user behavior still matters enough to shape product design across the freemium OTT market.

By Content Type: Film Libraries Support Scale While Episodic Titles Lift Engagement

Movies and films accounted for 41.77% of the freemium OTT market in 2025, keeping film libraries at the center of free-tier scale-building. Licensed film catalogs are often less costly to stock at volume than large original episodic slates, so they remain a practical base for FAST channels and AVOD services that need breadth before they can justify deeper investment. This helps explain why several major services first built audience reach through catalog depth and only later expanded more selectively into originals, specials, and other higher-cost formats. TV shows and episodic content are projected to grow at a 10.21% CAGR through 2031 because recurring story arcs create more frequent return visits, steadier session habits, and more opportunities to surface ads or upgrade prompts. Documentaries remain smaller in volume but attract focused audiences, support a more controlled viewing environment, and align well with advertisers who prefer clearer brand environments.

The other content types category includes live sports, news, user-generated content, and short-form micro-dramas, and each of these formats serves a different role in retention or monetization inside the freemium over-the-top (OTT) market. Paramount Skydance reported that its Pluto TV and Paramount+ convergence would support cross-service recommendations, giving episodic and documentary titles a clearer role in the free-to-paid movement. iQIYI reported in 2026 that it planned to launch more than 100 short-form dramas internationally, underscoring how the freemium OTT industry treats micro-format programming as a scalable content lever in mobile-first markets. Live sports remain expensive to secure, but they remain one of the strongest tools for repeat viewing, higher ad impression density, and upgrade pressure when rights are available.

Geography Analysis

North America held 38.38% of the freemium OTT market share in 2025, making it the largest revenue contributor. The United States remains central because connected TV use is mature, ad-supported streaming is deeply established, and advertisers pay stronger rates for streaming inventory there than in most other markets. Fox announced a USD 22 billion acquisition of Roku in June 2026, and the combined business is projected to control more than 50% of US FAST inventory, potentially reshaping media buying power, platform leverage, and distribution economics in the region. Canada and Mexico are smaller, but both benefit from the same bundle logic and connected TV adoption patterns that support ad-funded viewing and make free tiers easier to scale. South America is becoming a stronger corridor for the freemium OTT market as mobile broadband use and multi-service billing models make access easier for mass audiences that remain sensitive to direct subscription spending.

Asia-Pacific is projected to post the fastest regional growth in the freemium OTT market at a 10.64% CAGR through 2031. India stands out because JioStar had 500 million monthly active users in 2026, and Reliance Jio added a low-cost pass that bundled 15 OTT services into one plan, strengthening both reach and affordability within a very large mobile-first base. In Southeast Asia, CelcomDigi launched bundles from MYR 19.90 (USD 4.50) per month in June 2026, demonstrating how regional operators are compressing OTT access costs through a single billing relationship. China also remains important because domestic platforms operate freemium models within local licensing and content compliance rules that shape what can be distributed at scale and how international competition enters the market. Across the Asia-Pacific region, the freemium OTT market is benefiting from the combination of mobile reach, price-sensitive demand, large local language audiences, and platform-telco cooperation.

Europe combines strong local broadcaster platforms with rising pressure from global services investing more in local-language originals for the freemium OTT market. GDPR limits the precision of behavioral advertising in Europe and the United Kingdom, reducing targeting flexibility and increasing compliance requirements for operators without a stronger data infrastructure. In the Middle East, Shahid gives MBC Group a meaningful ad-supported presence across Arabic-speaking audiences, while Africa is earlier in adoption but remains important for future mobile-first expansion. GSMA reported in 2026 that Africa's mobile network coverage gap had narrowed to 9%, which supports the longer-term reach outlook for the freemium over-the-top (OTT) market even though affordability and usage gaps still limit full monetization today.[3]GSMA, “The Mobile Economy 2026,” GSMA, gsma.com

Competitive Landscape

The freemium OTT market has a split competitive structure, with a moderately concentrated top tier of global platforms and a wider regional layer of broadcasters, telco-backed services, and niche operators. Scale matters because the largest companies can spread content spending, ad sales infrastructure, product development, measurement tools, and distribution partnerships across a much broader audience base. Fox's Roku deal was the clearest 2026 example, because it brought together Tubi, The Roku Channel, and Roku's operating system into a single structure that more tightly linked inventory, distribution, and data.[4]Fox Corporation, “Fox Corporation to Acquire Roku, Inc.,” Fox Corporation, www.foxcorporation.com That kind of vertical alignment is difficult for smaller services to match, even when they hold strong local content positions or established brand recognition in one country. At the same time, the freemium OTT market is not fully closed, as regional players still compete for attention with language depth, broadcaster familiarity, local sports rights, and more tailored audience relationships.

Cross-platform partnerships are also changing the competition in the freemium OTT market, especially when no single service can meet every audience's needs on its own. Viu and iQIYI International announced a bundle for Indonesia, Thailand, the Philippines, and Malaysia in June 2026, which combined Southeast Asian local content with Chinese drama depth in one offer. JioStar also introduced JAMS in 2026, an AI-native production pipeline meant to support premium content creation across Indian languages at greater speed and scale. These moves show that the freemium OTT market is competing on content operations, localization, and workflow efficiency, not only on headline catalog size. The same pattern appears when services use telecom relationships and hardware partnerships to build reach more efficiently than direct digital marketing can deliver on its own.

Measurement and data quality are becoming harder lines of separation inside the freemium OTT market. Rakuten TV joined the BARB panel in the United Kingdom in 2026, and its early weekly reach of 2 million viewers showed why third-party measurement remains important for winning premium ad budgets in regulated markets. Amagi reported in its June 2026 AIRTIME Report that metadata quality was a leading factor in revenue performance across 6,500 FAST channel deliveries, indicating that operational discipline now shapes monetization as much as content acquisition does. This leaves the freemium over-the-top (OTT) market open to companies that can combine good local programming with reliable measurement, cleaner metadata, and steadier advertiser confidence.

Freemium OTT Industry Leaders

Netflix, Inc.

Google LLC

Amazon.com, Inc.

The Walt Disney Company

Comcast Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Telefónica's O2 brand in Spain introduced four new household plans bundling fiber broadband, mobile data, Movistar Plus+, Netflix, and Disney+, starting at EUR 45 (USD 51.80) per month. The launch marked O2's most comprehensive integration of streaming bundles to date and is expected to reduce per-platform customer acquisition costs for Disney+ and Netflix in the Spanish market while raising Telefónica's household connectivity average revenue per user.

- July 2026: iQIYI International reported that its global trending content for H1 2026 generated a 130% year-over-year surge in total viewership across its international platform, driven by Chinese dramas and micro-dramas delivered in 13 languages through dedicated dubbing and the iQIYI Starship Project fan engagement initiative. Seven Chinese dramas with Thai-language dubbing entered Thailand's local top 10, reflecting the platform's success in converting cultural affinity for Chinese IP into addressable AVOD audiences across Southeast Asia.

- July 2026: ZEE5 crossed 200 million registered users and secured ICC tournament and IPL cricket rights as part of an aggressive sports-led pivot, with ZEE Entertainment Enterprises reporting that ZEE5 revenue for the first nine months of FY2026 rose 45% year over year. The cricket rights acquisition positioned ZEE5 to recapture audience share lost to JioHotstar, using live sports events as the highest-frequency content type for driving both ad impressions and premium tier upgrades.

- June 2026: Fox Corporation announced a USD 22 billion cash-and-stock acquisition of Roku, combining Tubi, its profitable AVOD platform, with The Roku Channel and Roku's connected TV operating system. CEO Lachlan Murdoch confirmed that the 2 platforms would be maintained as separate services due to their 1/3 audience overlap, which effectively triples the combined reach, and that the acquisition positions Fox-Roku to control over 50% of US free ad-supported streaming TV inventory.

Global Freemium OTT Market Report Scope

The Freemium OTT market comprises over-the-top (OTT) video streaming services that offer users free access to a library of digital video content, with premium subscription tiers or paid features that unlock additional content, enhanced viewing experiences, or ad-free access. These platforms deliver content over the internet across multiple connected devices, enabling users to stream movies, television series, documentaries, and other video programming without relying on traditional broadcast, cable, or satellite television services.

The Freemium OTT Market Report is Segmented by Device Type (Smartphones and Tablets, Smart TVs, Laptops and Desktops, and Other Device Types), Content Type (Movies and Films, TV Shows and Episodic Content, Documentaries, and Other Content Types), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Types |

| Movies and Films |

| TV Shows and Episodic Content |

| Documentaries |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Types | ||

| By Content Type | Movies and Films | |

| TV Shows and Episodic Content | ||

| Documentaries | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the freemium OTT market size through 2031?

The freemium OTT market size was USD 26.02 billion in 2025, is estimated at USD 27.76 billion in 2026, and is forecast to reach USD 42.57 billion by 2031 at an 8.92% CAGR.

Which device category leads revenue generation in freemium OTT?

Smartphones and tablets led with 54.12% share in 2025, reflecting the strength of mobile-first viewing and the role of portable access in daily streaming behavior.

Which content format is growing fastest in ad-supported streaming platforms?

TV shows and episodic content are projected to grow at a 10.21% CAGR through 2031 because serialized viewing creates stronger repeat traffic and more frequent ad exposure.

Which region is leading, and which one is expanding fastest?

North America held the largest share at 38.38% in 2025, while Asia-Pacific is projected to grow the fastest at a 10.64% CAGR through 2031.

Why are telecom bundles important for streaming competition?

Bundles reduce acquisition costs, simplify billing, and keep users inside a larger service package, which helps both free-tier sampling and premium retention.

What is shaping competition among major platform operators in 2026?

Vertical integration, regional bundles, AI-led content workflows, and stronger audience measurement are shaping competitive positions, with Fox-Roku, Viu-iQIYI, JioStar, Rakuten TV, and Amagi standing out in the current cycle.

Page last updated on: